Embed Size (px)

Citation preview

Prof. Bernd Fitzenberger, Ph.D. April 2012

Quantile Regression

Universitat Linz

Abstract: Quantile regression is increasingly used in applied economet-

ric research. The method allows to estimate the differential effects of

covariates along the conditional distribution of the response variable.

Linear quantile regression can now be estimated with most econometric

software packages. This course provides an up–to–date introduction

into linear quantile regression. The course involves computer exercises

illustrating the use of basic linear quantile regression and some ad-

vanced quantile regression techniques as well as the interpretation of

results using the software package STATA.

Outline

1. Introduction to linear quantile regression: Distance function, Asymp-

totic distribution, Properties of the estimator, Interpretation as

Method-of-Moments Estimator

Application: Mincer Earnings Equation

2. Minimum-Distance estimation of quantile regression

Application: Earnings Regression based on cell data

3. Censored Quantile Regression

4. Decomposition Analysis with Quantile Regression and Uncondi-

tional Quantile Regression

Application: Gender Wage Gap

5. Quantile Regression for Duration Analysis

Application: Duration of Unemployment

6. Quantile Regression for Panel Data

References:

Abrevaya, J. and C.M. Dahl (2008), ”The effects of birth inputs on

birthweight: evidence from quantile estimation on panel data.”

Journal of Business and Economic Statistics, 26(4):379-397.

Antonczyk, D., B. Fitzenberger, and K. Sommerfeld (2010) “Rising

Wage Inequality, the Decline of Collective Bargaining, and the

Gender Wage Gap”, Labour Economics, 17 (5), 835-847.

Angrist, J. V. Chernozhukov, and I. Fernandez (2006) “Quantile Re-

gression under Misspecification, with an Application to the U.S.

Wage Structure”, Econometrica, 74(2), 539-564.

Chamberlain, G. (1994) Quantile Regression, Censoring, and the

Structure of Wages. In: Sims, C., (ed.), Advances in Econo-

metrics: Sixth World Congress. Econometric Society Monograph,

Volume 1.

Chernozhukov, V., I. Fernandez-Val and B. Melly (2008). “Inference

on counterfactual distributions.” MIT Working Paper, 08-16.

Firpo, S., Fortin, N.M., and T. Lemieux (2009). “Unconditional

Quantile Regressions” Econometrica, vol. 77(3), 953-973.

Firpo, S., Fortin, N.M., and T. Lemieux (2011). “Occupational Tasks

and Changes in the Wage Structure”, IZA Discussion Paper 5542.

Fitzenberger, B. (1997). A Guide to Censored Quantile Regres-

sions. In: Handbook of Statistics, Volume 15: Robust Inference

(Eds. G.S. Maddala & C.R. Rao), 405-437. Amsterdam: North–

Holland.

Fitzenberger, B., Koenker, R. and J.F.Machado (2001) Economic

Applications of Quantile Regression, Special Issue of Empirical

Economics, Springer, Heidelberg.

2

Fitzenberger, B. and A. Kunze (2005) “Vocational Training and Gen-

der: Wages and Occupational Mobility among young Workers”,

Oxford Review of Economic Policy, 2005, Vol. 21(3), pp. 392-

415.

Fitzenberger, B. and Wilke, R.A. (2006) “Using Quantile Regression

for Duration Analysis”. Allgemeines Statistisches Archiv, 90(1),

105-120.

Fortin, N.M., Lemieux, T. and S. Firpo (2011). ”Decomposition

Methods”, (with T. Lemieux and S. Firpo), in O. Ashenfelter

and D. Card (eds.) Handbook of Labor Economics, Vol. 4A,

Amsterdam: North-Holland, 1-102.

Koenker, R. (2005) Quantile Regression. Econometric Society Mono-

graph, Cambridge University Press, Cambridge.

Koenker, R. and Bassett, G. (1978). Regression Quantiles. Econo-

metrica, 46, 33–50.

Koenker, R. and K.F. Hallock (2001). “Quantile Regression”, Journal

of Economic Perspectives, vol. 15(4), 143-156.

Lamarche, C. (2010). Robust penalized quantile regression estimation

for panel data, Journal of Econometrics, 157, 396-408.

Machado, J. and Mata, J. (2005). Counterfactual Decomposition of

Changes in Wage Distributions using Quantile Regression. Jour-

nal of Applied Econometrics, 20(4), 445–465.

Melly, B. (2005) “Decomposition of differences in distribution using

quantile regression”. Labour Economics 12 (4), 577-590.

Melly, B. (2006) “Public and private sector wage distributions control-

ling for endogenous sector choice”, Discussion Paper, University

of St. Gallen.

3

1. Introduction to linear quantile regression

Definition: The θ–quantile of a random variable X with cumulative

distribution function (CDF) F (x) = P (X ≤ x) is the minimum

(≡infimum) value qθ such that

qθ = F−1(θ) = infx : F (x) ≥ θ.

Example: θ = 0.5 describes the median (the 50%–value).

The θ–quantile of the sample X1, . . . , XN can be computed by the

following minimization problem:

qθ = argminz

N∑i=1

ρθ(Xi − z)

=N∑i=1

[θ · I(Xi > z) + (1− θ) · I(Xi < z)] · |Xi − z|

The so–called ”check function” ρθ is based on the absolute deviation

of residual |Xi − z| which is weighted by θ if positive and by (1− θ)

if negative.

Asymmetric loss

-

6

HHHHHHHHHHHH

ρθ(u)

θu

−(1− θ)u

u0

4

Example: For θ = 0.5 (median) positive and negative residuals are

weighted equally, i.e. the sum of absolute deviations is minimized

(Least Absolute Deviation: LAD).

Show qθ = argminN∑i=1

[θI(xi > z) + (1− θ)I(xi < z)] · (xi − z)︸ ︷︷ ︸≡ D

Order x1, ..., xN such that x1 < x2 < ... < xN (ignore equality for

simplicity)

-

x1 x2 x3 ... xk xk+1 ... xN

?

z

︸ ︷︷ ︸Ik

z ϵ (xk, xk+1) = Ik

∂D

∂z≡ Dk = (1− θ)

k∑i=1

1 + θN∑

i=k+1(−1)

= (1− θ)k − (N − k)θ

= k − θN

= constant in Ik3 cases:

i) Dk = 0 ⇔ k = θN

→ all values in Ik minimize D and represent q − quantile

→ qθ not unique (qθ ∈ Ik), e.g. qθ =xk+xk+1

2

5

ii) ∂D∂z > 0 then z is to be reduced until Dk−1 = (k − 1)− θN < 0

→ minimum at xk

-

6

@@

@@@@

@@@@

@@

D

zxk

It follows k−1N < θ < k

N , i.e. F (z) jumps above θ at z = xkTherefore qθ = xk

iii) Dk = k − θN < 0, i.e. increase z until Dk+1 > 0

→ qθ = xk+1 becausekN < θ < k+1

N

6

Semiparametric linear quantile regression

Motivation: A linear quantile regression specifies the conditional θ–

quantile qθ(Yi|X2i, . . . , Xki) of Yi as a linear function of regressors

X2i, . . . , Xki .

Model: For sample i = 1, ..., N

Yi = βθ,1 + βθ,2X2i + . . . + βθ,kXki + εθi = x′iβθ + εθi

where Xji observation i for regressor j = 2, . . . , k

qθ(εθi |xi) = 0 and εθi = Yi − x′iβθ continuously i.i.d. random

variable (conditional on xi).

Estimator for βθ = (βθ,1, . . . , βθ,k)′:

βθ = argminβ1,...,βk

N∑i=1

ρθ(Yi − x′iβθ)

=N∑i=1

[θ · I(Yi > x′iβθ)︸ ︷︷ ︸positive

residual

+(1− θ) · I(Yi < x′iβθ)︸ ︷︷ ︸negative

residual

] · |Yi − x′iβθ|

with xi = (X2i, . . . , Xki)′ .

Asymptotic distribution of βθ (i.i.d. error terms):√N(βθ − βθ) ∼ N

[0, λ ·

(N−1 ·X ′X

)−1]

with λ = θ(1−θ)fθ(0)

2 and fθ(0) the density of εθi (and Yi) at 0

(and qθ(Yi|xi), resp.) conditional on xi.

Asymptotic covariance of βθ1 and βθ2 for θ1 = θ2

Cov(βθ1, βθ2) =min(θ1, θ2)− θ1 · θ2

fθ1(0) · fθ2(0)·X ′X−1

7

Properties of quantile regression line:

i) Interpolation property: For design matrix X having full rank

(rank(X) = k), there are k linearly independent data points

with zero residual

Yi(j) = x′i(j)β with j = 1, ..., k .

The fitted line interpolates at least k data points (assuming full

rank of the regressor matrix and a unique solution of the min-

imization problem), i.e. the estimated residuals are exactly zero

for these data points. This is the case because minimization in-

volves a linear programming problem. fθ(0) can be estimated

based on the fitted residuals. However, those residuals which are

exactly zero due to the minimization process can not be used to

estimate this density.

ii) At most a share θ of observations have a negative residual and at

most a share (1 − θ) of observations have a positive residual (if

Xi contains an intercept).

M =N∑i=1

I(ui < 0) negative

Z =N∑i=1

I(ui = 0) zero

P =N∑i=1

I(ui > 0) positive

residuals

MN ≤ θ ≤ M+Z

N and PN ≤ 1− θ ≤ P+Z

N

8

Figure1:ExampleforQuantileRegressionq (YijX i)=;1+ ;2X i

Y

X

X 1X 2X 3

=0:75 =0:5 =0:25

0;75;2> 0;5;2>0;25;2

Dispersionofthe onditionalDis-

tributionofY iin reaseswithX

9

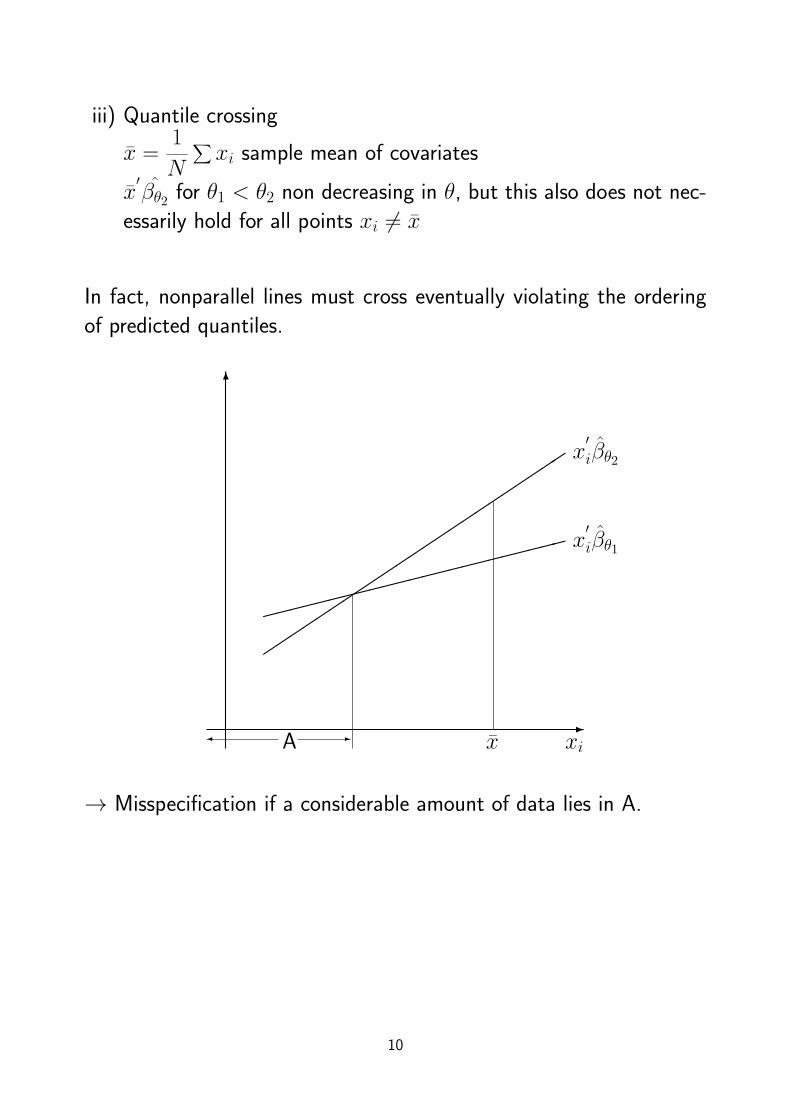

iii) Quantile crossing

x =1

N

∑xi sample mean of covariates

x′βθ2 for θ1 < θ2 non decreasing in θ, but this also does not nec-

essarily hold for all points xi = x

In fact, nonparallel lines must cross eventually violating the ordering

of predicted quantiles.

-

6

A x xi -

x′iβθ1

x′iβθ2

→ Misspecification if a considerable amount of data lies in A.

10

Asymptotic distribution of βθ for heteroscedastic, independent er-

ror terms:√N(βθ − βθ) ∼ N

[0, L−1

θ,NJθ,NL−1θ,N

]

where the k × k matrices are

Lθ,N = E1

N

∑ifθ,i(0)xi x

′i and

Jθ,N =θ(1− θ)

N·X ′X =

θ(1− θ)

N· ∑

ixi x

′i .

Asymptotic covariance:

Cov(βθ1, βθ2) = L−1θ1,N

· (min(θ1, θ2)− θ1 · θ2)N 2

X ′X · L−1θ2,N

In the case of heteroskedastic error terms, it is difficult to estimate con-

sistently the expression Lθ,N due to the observation specific densities

fθ,i(0) ≡ fθ(εθi = 0|xi) ≡ fθ(Yi = qθ(Yi|xi)|xi).

Alternatively, one can use the Design–Matrix (or pairwise, xy) Boot-

strap by resampling the entire observation vector (Yi, X2i, . . . , Xki).

The bootstrap yields automatically an estimate for the joint distribu-

tion βθ1 and βθ2 for θ1 = θ2. This way it is possible to perform tests

across the distribution.

Using estimates of the asymptotic covariance across quantiles allows

to performing tests involving estimates at different quantiles θ1, θ2.

Equality of slope coefficients implies that the difference in the condi-

tional quantiles of Yi does not vary with the respective covariate.

11

Asymptotic distribution with heteroscedastic observations and mis-

specification of linear quantile regression (Angrist, Chernozhukov, Fer-

nandez-Ival, 2006)

The linear quantile regression estimates consistently the coefficient βθwhich solves the population minimization problem (’best linear quantile

predictor’)

βθ := argminβ

E[ρθ(Y −X ′β)]

but qθ(Yi|xi) does not necessarily coincide with x′iβθ

Asymptotic distribution:√N(βθ − βθ) ∼ N

[0, L−1

θ,NJθ,NL−1θ,N

]

where Lθ,N is as above and only Jθ,N changes to

Jθ,N =1

N· ∑

i(θ − I(Yi < x′iβθ))

2xi x′i .

Note: In my previous work, I define the θ–weighted sign function

sgnθ(u) =

θ if u > 0

0 if u = 0

θ − 1 if u < 0

and sgnθ(Yi − x′iβθ) = θ − I(Yi < x′iβθ) except for zero residuals.

12

Interpret linear quantile regression as a method of moment estimator

which solves the approximate moment condition

1

N· ∑

ixi(θ − I(Yi < x′iβθ)) ≈ 0

which is asymptotically equivalent to

1

N· ∑

ixisgnθ(Yi − x′iβθ) ≈ 0

Therefore:

Jθ,N =1

N· V ar(

∑ixi(θ − I(Yi < x′iβθ)))

=1

N· V ar(

∑ixisgnθ(Yi − x′iβθ))

and for the covariance across quantiles

Jθ1,θ2,N =1

N· ∑

iCov(xi(θ1 − I(Yi < x′iβθ1)), xi(θ2 − I(Yi < x′iβθ2)))

= ...

Asymptotic distribution with heteroscedastic and dependent observa-

tions

Then,

Jθ,N =1

N· V ar(

∑ixi(θ − I(Yi < x′iβθ)

with Lθ,N unchanged. Thus, autocorrelation robust estimate has to

take account of covariance in xi(θ− I(Yi < x′iβθ) across observations

i, analogous to Newey–West or clustered standard errors.

13

Heuristic derivation of QR as Method of Moment Estimator

minN∑i=1

[θI(Yi − x′iβ > 0)− (1− θ)I(Yi − x

′iβ < 0)](Yi − x

′iβ)

=N∑i=1

[θ − I(Yi − x′iβ < 0)](Yi − x

′iβ)

Approximate FOC:

1

N

N∑i=1

[θ − I(Yi − x′iβ < 0)](−xi) = op(N

−12) ≈ 0

because data points with Yi = x′iβ are negligible asymptotically com-

pared to N.

Precisely:

1

N

N∑i=1

[θ − I(Yi − x′iβ < 0)]xi = op(N

−12)

Note: θ − I(Yi − x′iβ) = sgnθ(Yi − x

′iβ)

14

Heuristic derivation of asymptotic distribution

Yi − x′iβ = x

′iβ + ui − x

′iβ

= ui − x′i(β − β)

Assume: plimβ = β has been shown

S =1√N

∑xi[θ − I(ui − x

′i(β − β) < 0)] ≈ 0

B =1√N

∑Exi[θ − I(ui − x

′i(β − β) < 0)]

=1√N

∑E(xi)E[θ − I(ui < x

′i(β − β))|xi]︸ ︷︷ ︸

A

A = θ − Fui(x′i(β − β))

= θ − Fui(0)− fui(0)x′i(β − β)

= −fui(0)x′i(β − β)

⇒ B = − 1√N

∑Efui(0)xix

′i(β − β)

= −(1

N

∑Efui(0)xix

′i)√N(β − β)

= −Lθ,N

√N(β − β)

15

One can show:

0 ≈ 1√N

∑xi[θ − I(ui < −x′i(β − β))] = S

a

≈ 1√N

∑xi[θ − I(ui < 0)] + B

It follows

√N(β − β) ≈ ((Lθ,N)

−1 1√N

∑xi(θ − I(ui < 0))

Jθ,N = V ar

1√N

∑xi(θ − I(ui < 0))

Independence: Jθ,N =1

N

∑V ar[xi(θ − I(ui < 0))]

V ar(xi(θ − I(ui < 0))|xi) = xix′iθ(1− θ)

= V ar(I(ui < 0)|Xi)

= P (ui < 0|xi)(1− P (ui < 0|xi))= θ(1− θ)

Asymptotic distribution:

√N(β − β) ∼ N(0, L−1

θ,NJθ,NL−1θ,N)

Lθ,N =1

N

∑fui(0|xi)xix

′i

Jθ,N =θ(1− θ))

N

∑xix

′i

16

Estimation of asymptotic standard errors

i) (IID) Sparsity estimator: For iid setting require estimate of sparsity

sθ =1

fθ(0)where fθ(0) is density of Yi at qθ(Yi|xi).

sN(θ) =F−1N (θ + hN)− F−1

N (θ − hN)

2hN

where F is the distribution function of the residual (Yi − qθ(Yi|xi))

Choice of bandwidth hN

1. Bofinger (1975) based on standard density estimation asymptotics

and assuming a Gaussian distribution

hN = N−1/5

4.5ϕ4(Φ−1(θ))

(2Φ−1(θ)2 + 1)2

1/5

2. Hall and Sheather (1988) explicitly addressing confidence interval

estimation and assuming a Gaussian distribution (Koenker, 2005,

p. 140)

hN = N−1/3z2/3α

1.5ϕ2(Φ−1(θ))

2Φ−1(θ)2 + 1

1/3

where zα satisfies Φ(zα) = 1− α/2 and α is the error probability

(size) for the test.

Computation of F−1N (.)

1. Based on empirical distribution of residuals, excluding zeroes

2. Use fitted quantiles directly F−1N (θ) = x′βθ where x = 1/N

∑i xi

(difference x′(βθ+hN − βθ−hN ) is necessarily nonnegative)

17

ii) Heteroscedasticity, independence case: Need observation specific

estimate of density fθ,i(0) in matrix Lθ,N

1. Hendricks-Koenker (1991) estimate

fθ,i(0) =2hN

x′i(βθ+hN − βθ−hN )

Crossing problem: difference in denominator can be negative –

rarely happens unless model is strongly misspecified!

2. Powell (1991) estimate

Lθ,N =1

NcN

N∑i=1

K(ui(θ)/cN)xix′i

where cN is a bandwidth parameter analogous to density estima-

tion with cN → 0 and√NcN → ∞.

Specific suggestion

Lθ,N =1

NcN

N∑i=1

(I(|ui(θ)| < cN)xix′i

and cN = κ · (Φ−1(θ + hN) − Φ−1(θ − hN)) and κ is a robust

estimate of scale, e.g. κ = IQR/1.34 and IQR is interquartile

range of residuals

18

2. Minimum-Distance estimation of quantile regression

Linear Quantile Regression for Grouped Data (Chamberlain, 1994)

When the regressors can be grouped in discrete cells and the number of

observations per cell is not too small (typically it should be larger than

30), then a simple two–stage minimum–distance approach is possible

which can be easily extended to account for censoring.

1. Compute the empirical θ–quantile in each cell j defined by the set

of regressors taking the value xj.

2. Estimate the coefficients of the linear quantile regression by com-

puting a weighted least squares regression of the empirical θ–

quantiles on the cell characteristics xj.

When applying this two–stage approach to censored data, just use

those cells in the second stage for which the empirical θ–quantile is

not censored.

19

Formal Description of Chamberlain’s (1994) Minimum-DistanceEstimator

Observations (xi, yi) sample i = 1, ..., N

Grouped by values of x: J cells x = xj with j = 1, ..., J

P (x = xj) = αj

Cell size: Nj =∑Ni=1 I(xi = xj) and

Nj

N→ αj

First Stage: πj = qθ(Yi|xj) empirical θ- quantile of Yi in jthcell

π′0 = (π1, ..., πJ) ; π

′ = (π1, ..., πJ)

√N(π − π0) → N(0,Ω)

V ar(πj)a=

θ(1− θ)

Njf (π0j)2=

1

NΩjj =

1

N

σ2j

αj

Ωij = 0 for i = j whereσ2j

Nj= Asymptotic variance of sample quantile

Second Stage: Run Minimum Distance (GLS estimator) based on cell

data for linear relationship

π0j = qθ(Yi|xj) = xj′β0

by minβ

(π −Gβ)′Ψ(π −Gβ) where G =

x1...

xJ

and Ψ → Ψ

20

Weighted Least Squares ( Ψ diagonal matrix)

i) weights are cell sizes

Ψ = diag(N1, ..., NJ)

ii) Optimal weights asymptotically Ψ = Ω−1 inverse of estimated

variances of cell quantiles on diagonal

Asymptotic distribution (analogous to GMM):

√N(β − β) ∼ N(0,Λ)

with Λ = (G′ΨG)−1G′ΨΩΨG(G′ΨG)−1

with optimal choice Ψ = Ω−1 ⇒ Λ = (G′ΨG)−1

Assumes correct specification of qθ(Yi|x) = x′β

Estimation of Ω−1 = (diag(σ21

α1, ...,

σ2J

αJ))−1

αj =Nj

Nand σ2

j =θ(1− θ)

fj

2

with fj(πj) density estimate in cell j at θ-quantile πj

21

Misspecification:

δ = (δ1, ..., δy)′ = π0 −Gβ ⇒ specification error

√N(β − β) ∼ N(0,Λ1 + Λ2)

Λ1 is Λ from above, Ψ = diagN1N , ..., NJ

N

Λ2 = (G′ΨG)−1)G′ΨM ΨG(G′ΨG)−1

M = diag

δ21α1

, ...,δ2JαJ

δj = πj − x′jβ

Chamberlain recommends not to attempt to estimate and use an op-

timal choice of Ψ when model is misspecified.

Asymptotic Minimum - Distance - Test statistic

N(π −Gβ)′Ω−1(π −Gβ)a∼χ2J−K

for β using the optimal choice of Ψ = Ω−1 (analogous to Sargan GMM

test)

⇒ Goodness-of-Fit test

22

3. Censored Quantile Regression

Censored regression model

Yi = min(x′iβ + εi, Yi)

with observation specific censoring from above at Yi .

Censored quantile regression (Powell, 1984, 1986):

βθ = argminβ

N∑i=1

ρθ(Yi −min(x′iβ, Yi))

Motivation for estimator: When the empirical θ–quantile in a uni-

variate sample Y1, . . . , YN lies below the censoring point Yi, then

censoring has no impact on the estimation of this quantile and con-

sistent estimation is possible. This idea is extended to the regression

context and yields an estimator which is very attractive theoretically.

This estimator is consistent under much more general assumptions

compared to the standard Maximum–Likelihood Tobit–estimator.

Asymptotic distribution of βθ (i.i.d. error terms):

√N(βθ − βθ) ∼ N

0, λ ·N−1 ∑

iI(x′iβθ < Yi)xi x

′i

−1

where λ = θ(1−θ)fθ(0)

2 and fθ(0) the density of εθi at point 0. The asymp-

totic distribution depends only upon the non censored data points

(I(x′iβθ < Yi)). These points must allow for a unique identification

of the estimate.

The actual computation of the estimator is a big problem!

23

Computation unfortunately complicated

i) Easy case: For grouped data use only cells for which cell quantile

is not censored → Chamberlain (1994)

ii) Iterative Linear programming algorithm (Buchinsky, 1994)

Idea: iterate and base quantile regression only on observations where

fitted values are not censored.

1) Start with some estimate β0 and j = 0

2) Compute x′iβj and use observations i : x′iβj < Y i to form sub-

sample Sj

3) Based on Sj calculate standard linear quantile regression coef-

ficients βj+1 and change sample to Sj+1 the set of observation

i : x′iβj+1 < Y i

4) If Sj = Sj+1 or j + 1 = maxiteration then stop.

5) Set j = j + 1 and go to 3)

Problems:

a) ILPA not guaranteed to converge

b) Upon convergence, ILPA is not guaranteed to obtain a local min-

imum of non-convex distance function

24

c) True CQR may interpolate censored points

-

6

Yi

xi

Yi

ILPA can be modified to keep observations x′iβj ≤ Yi, i.e. allow cen-

sored points to be interpolated

→ Problems a) and b) still remain

25

BRCENS: Linear programming algorithm with takes account of kinks

at zero residuals and at points interpolating censoring points

- BRCENS developed by myself, see Fitzenberger (1997)

- BRCENS guarantees local minimum of nonconvex distance func-

tion

- BRCENS performs better than ILPA but also has major problems

when there is a lot of censoring

- ILPA implemented as command CLAD in STATA

- BRCENS implemented as command LAD (censor...) in TSP and

also in R

→ Recently alternative algorithms and modifications of estimation

problem

26

Bootstrapping method of Bilias et al. (2000)

Note that asymptotic variance depends only on observations i for which

x′iβ < Y i

are uncensored.

Idea of Bilias et al. method:

i) Resample only for subset of observations i : x′iβθ < Y i with

size N a resample of size N (pairwise bootstrap)

ii) Calculate standard linear quantile regression for this resample ig-

noring censoring

iii) Use empirical distribution across resamples as estimate of variance-

covariance-matrix

27

4. Decomposition Analysis with Quantile Regression

References: Machado/Mata (2005), Melly (2006),

Fortin/Firpo/Lemieux (2011)

Problem: Differences in wage distributions between Males and Females

can be attributed to different characteristics or different coefficients

Want to compare qθ(Yi|female) and qθ(Yi|male) based on quantile

regression estimates

qθ(Yi|female, xi) = x′iβ

femaleθ

qθ(Yi|male, xi) = x′iβ

maleθ

Problem: Conditional quantiles and unconditional quantiles can not

be linked directly !

e.g. qθ(Yi|female) = x′femaleβ

femaleθ

in contrast to means where Yfemale

= xfemale′βfemalemean

28

Machado/Mata suggest to simulate the unconditional distribution based

on quantile regression fits.

1. Generate a random sample of size m from Uniform (0,1)

θ1, ..., θm

2. Estimate m different quantile regression coefficients:

βθj , j = 1, ...,m

3. Generate a random sample of sizem with replacement from xifemaledenoted by xjmj=1

4. Yj = x′jβθjmj=1 is a random sample from the unconditional dis-

tribution. Determine possibly counterfactual quantiles from this

sample.

– Procedure builds on probability integral transformation from ele-

mentary statistics: If continuous random variable Y has distribution

function F (y) and U is uniformly distributed on the interval [0, 1],

then random variable Y = F−1(U) is distributed following the dis-

tribution function F (y). This is because P (Y < y = F−1(u)) =

P (U < F (y) = u) = F (y).

– Procedure addresses problem of quantile crossings in an elegant way.

– For computational ease: 1. can be replaced by

1.’ Draw θj from uniform discrete distribution of equispaced per-

centiles i.e. 0.01, 0.02, ..., 0.99 with probability 1/99 each.

approximating the continuous distribution of Yi given xj.

29

Use this simulation method to undertake decompositions of the fol-

lowing type:

qθ(Yi|female)− qθ(Yi|male)

= qθ(Yi|female)− qθ(Yi|female characteristics, male coefficients)︸ ︷︷ ︸coefficient effect

+ qθ(Yi|female characteristics, male coefficient) − qθ(Yi|male)︸ ︷︷ ︸characteristics effect

- The second/third term is counterfactual and has to be simulated.

- The first and the last term can be taken from the observed sam-

ples or they can be simulated as well

→ Check for misspecification of qθ

- The decomposition can be performed in reverse order, i.e. it is

not unique.

→ analogous to Blinder/Oaxaca

30

The Machado/Mata estimator’s efficiency increases with the number

of random draws m. Melly (2006) suggests an analytical estimator

which avoids the computational burden of simulation and which is

equivalent to MM for m → ∞.

Melly uses the fact that the distribution function is vertically additive,

i.e.

F (y) = Prob(Y ≤ y) = 1N

∑Prob(Yi ≤ y|xi) = 1

N

∑F (y|xi)

Note that F (y|xi) =1∫0I(x′iβ ≤ y)dθ

=J∑

j=1(θj − θj−1)I(x

′iβθj ≤ y)

because βθ changes only at a finite number of percentiles θ1, ..., θj i.e. βθ =

constant for θ ∈ (θj−1, θj)

(θ0 = 0, θJ = 1)

→ have to calculate the entire quantile regression process across θ

31

Computational simplification:

Calculate βθ at equispaced discrete percentiles, i.e. 0.01, 0.02, ...

0.99, and pretend that x′iβθ can take one of the corresponding 99 fit-

ted values with equal probability.

To obtain the unconditional quantiles the distribution function F(y)

calculated by Melly’s method has to be inverted:

qθ(Yi) = infy : 1N

∑F (y|xi) ≥ θ

Melly develops also an asymptotic distribution theory for his estimator.

→ Application also for estimation of quantile treatment effects (QTE).

32

Unconditional Quantile Regression andDecomposition Analysis

References:

Firpo, S., Fortin, N.M., and T. Lemieux (2009) [henceforth FFL09],

Firpo, S., Fortin, N.M., and T. Lemieux (2011)

Fortin, N.M., Lemieux, T. and S. Firpo (2010). Decomposition Meth-

ods in Economics. NBER Working Paper 16045, Chapter prepared for

the Handbook of Labor Economics, Volume 4. [henceforth FLF10]

Idea: Unconditional Quantile Regression (UQR) focus on the impact of

the distribution of covariates on the unconditional (marginal) distribu-

tion of the outcome variable, e.g. on the unconditional quantile qθ(Y ).

The most basic UQR estimates the impact of a uniform rightward shift

of the distribution of one covariate holding all other covariates con-

stant, i.e. of X → X + t.

Problem: The impact of a covariate on the conditional distribution of

the outcome variable – as estimated by a conditional quantile regress-

sion qθ(Y |X) – does not necessarily translate into the impact on the

unconditional distribution of Y – i.e. on qθ(Y ).

33

Partial Effects (FFL09), univariate X :

Unconditional Quantile Partial Effect (UQPE):

α(θ) = limt↓0

qθ(Y (X + t))− qθ(Y (X))

t

Conditional Quantile Partial Effect (CQPE):

CQPR(θ, x) = limt↓0

qθ(Y |X = x + t)− qθ(Y |X = x)

t

=∂qθ(Y |X = x)

∂x

FFL09 develop UQR based on the statistical concept of the influence

function.

Definition: The influence function of a quantile is defined as

IF (y, qθ) = limt↓0

qθ((1− t)F + t∆y)− qθ(F )

t

where F represents the sample probability distribution of the data

and ∆y is the distribution for a point mass at the value y. Thus,

(1 − t)F + t∆y is a mixture distribution with weight (1 − t) for the

actual distribution F and weight t for the value y. The influence

function measures the marginal influence of an observation at value y

on the sample quantile.

For instance, this is important to study the influence of outliers. It

turns out that the influence only depends on whether y lies below or

above qθ(Y ) but not the actual value of y, i.e. quantiles are not outlier

sensitive.

34

What is the influence function?

First, determine quantile of mixture distribution qθ((1− t)F + t∆y) as

a function of qθ(F ), t, and y for t small and F continuous distribution:

qθ((1− t)F + t∆y) = q′θ

We have

(1− t)F (q′θ) + t∆y(q′θ) = θ

where ∆y(q′θ) = I(y ≤ q′θ) (contribution to probability of Y ≤ q′θ).

By the implicit function theorem

∂q′θ∂t

= −−F (q′θ) + I(y ≤ q′θ)

(1− t)fY (q′θ)

For t ↓ 0, one obtains

IF (y, qθ) =θ − I(y ≤ qθ)

fY (qθ)

because q′θ → qθ and F (q′θ) → θ.

Note

E[IF (Y, qθ)] =∫IF (y, qθ) · fY (y)dy

=∫ θ − I(y ≤ qθ)

fY (qθ)· fY (y)dy

= (1/fY (qθ))∫(θ − I(y ≤ qθ)) · fY (y)dy = 0

because by definition of the θ-quantile E[I(y ≤ qθ)] = θ.

Now, define the recentered influence function (RIF):

RIF (y, qθ) = qθ + IF (y, qθ)

We have E[RIF (Y, qθ)] = qθ.

Note the change between y (value of outcome variable) and Y (ran-

dom variable).

35

Rewrite

RIF (y, qθ) = qθ +θ − I(y ≤ qθ)

fY (qθ)

=I(y > qθ)

fY (qθ)+ qθ −

1− θ

fY (qθ)= c1,θI(y > qθ) + c2,θ

where c1,θ = 1/fY (qθ) and c2,θ = qθ − c1,θ(1− θ).

We have E[RIF (Y, qθ)] = c1,θP (Y > qθ) + c2,θ = qθbecause E[I(Y > qθ)] = P (Y > qθ) = 1− θ.

By the Law of Iterated Expectations (LIE), i.e. because

E[RIF (Y, qθ)] = EXE[RIF (Y, qθ)|X ] ,one can specify the RIF-regression by conditioning on the covariates

(X = x):

E[RIF (Y, qθ)|X = x] = mθ(x) = c1,θP (Y > qθ|X = x) + c2,θ

Since only P (Y > qθ|X = x) depends upon X = x, a RIF-regression

amounts to regressing the binary outcome (dummy) variable I(y >

qθ) on X . Marginal effects for P (Y > qθ|X = x) translate into

marginal effects for qθ (inverse function) through the division by the

unconditional density fY (qθ).

UQPE (Average Marginal Effect): Continuous regressor

UQPE(θ) = α(θ) =∫ dE[RIF (Y, qθ)|X = x]

dx· dFX(x)

= c1,θ∫ dP (Y > qθ|X = x)

dx· dFX(x)

UQPE (Average Marginal Effect): Dummy regressor

UQPE(θ) = αD(θ) = c1,θ[P (Y > qθ|X = 1)− P (Y > qθ|X = 0)]

36

Specification and Estimation of RIF-regression

1. Need to estimate the unconditional density function of Y at em-

pirical θ-quantile qθ. Kernel density estimator:

fY (qθ) =1

N · byN∑i=1

KY

Yi − qθby

KY (.) is a kernel function and bY bandwidth.

2. RIF-OLS Regression

mθ,RIF−OLS(x) = x′γ

Corresponds to a renormalized linear probability model (LPM) re-

gressing

RIF (Yi, qθ) = I(Yi > qθ)/fY (qθ) + c2,θ

on x. The coefficient estimates γθ (except for the constant) are

equal to the coefficients in a LPM divided by the rescaling factor

fY (qθ).

UQPERIF−OLS(θ) = γ

Unconditonal quantile regression estimates typically report this

estimated UQPE.

37

3. RIF-Logit Regression

Specify P (Y > qθ|X = x) as a logit regression

mθ,RIF−Logit(x) = c1,θΛ(x′γ) + c2,θ

where P (Y > qθ|X = x) = Λ(x′γ) = exp(x′γ)/(1 + exp(x′γ)).

Run Logit regression of I(Yi > qθ) on X to obtain γ.

We have

dmθ,RIF−logit(x)

dx= c1,θ · γ · Λ(x′γ) · (1− Λ(x′γ))

Then,

UQPERIF−Logit(θ) = c1,θ · γ · 1

N

N∑i=1

Λ(x′iγ) · (1− Λ(x′iγ))

Analogous as the estimation of average marginal effects for logit

(average probability derivatives).

4. Nonparametric-RIF Regression (RIF-NP)

Specify P (Y > qθ|X = x) nonparametrically, e.g. by a polyno-

mial approximation as argument of the logit function. Then, x′γ

involves a flexible polynomial specification of the regressors. The

calculation of the marginal effects (UQPE) proceeds as above ac-

counting for the fact that a regressor variable appears more than

once in the polynomial approximation.

38

5. Quantile Regression for Duration Analysis

References:

Koenker (2005, Chapter 8.1), Fitzenberger and Wilke (2006)

Quantile Regression and Proportional Hazard Rate Model

Our focus is on linear quantile regression for duration data involving the

estimation of the following accelerated failure time model at different

quantiles θ ∈ (0, 1) for the completed duration Ti of spell i

h(Ti) = x′iβθ + ϵθi (1)

where the θ-quantile of ϵθi conditional on xi, qθ(ϵθi |xi), is zero and

h(.) is a strictly monotone transformation preserving the ordering of

the quantiles. The most popular choice is the log–transformation

h(.) = log(.) (a simple, more flexible alternative involves a Box–Cox–

transformation).

In fact, quantile regression model the conditional quantile of the re-

sponse variable

qθ(h(Ti)|xi) = x′iβθ

or, alternatively, due to the equivariance property of quantiles

qθ(Ti|xi) = h−1(x′iβθ) .

The linear specification of the quantiles allows for differences in the im-

pact of covariates xi across the conditional distribution of the response

variable. However, the coefficient is the same for a given quantile θ

irrespective of the actual value of qθ(h(Ti)|xi).

A possible problem of quantile regression is the possibility that the

coefficient estimates can be quite noisy (even more so for censored

quantile regression) and often non-monotonic across quantiles. To

39

mitigate this problem, it is possible to obtain smoothed estimates

through a minimum–distance approach. Minimize

(β − f [δ])′Ψ−1(β − f [δ]) (2)

with respect to δ, the coefficients of a smooth parametric specification

of the coefficients as a funtion of θ. β is the stacked vector of quantile

regression coefficient estimates βθ at different quantiles and Ψ is the

estimated covariance matrix of β.

The most popular parametric Cox proportional hazard model (PHM),

Kiefer (1988), is based on the concept of the hazard rate conditional

upon the covariate vector xi given by

λi(t) =fi(t)

P (Ti ≥ t)= exp(x′iβ)λ0(t) , (3)

where fi(t) is the density of Ti at duration t and λ(t) is the so called

baseline hazard rate. The hazard rate is the continuous time version

of an instantaneous transition rate, i.e. it represents approximately the

conditional probability that the spell i ends during the next period of

time after t conditional upon survival up to period t.

There is a one–to–one correspondence between the hazard rate and the

survival function, Si(t) = P (Ti ≥ t), of the duration random variable,

Si(t) = exp (− ∫ t0 λi(s)ds). A prominent example of the parametric

proportional hazard model is the Weibull model where λ0(t) = ptp−1

with a shape parameter p > 0 and the normalizing constant is included

in β. The case p = 1 is the special case of an exponential model with

a constant hazard rate differentiating the increasing (p > 1) and the

decreasing (0 < p < 1) case.

40

Within the Weibull family, the proportional hazard specification can

be reformulated as the accelerated failure time model

log(Ti) = x′iβ + ϵi (4)

where β = −p−1β and the error term ϵi follows an extreme value

distribution, Kiefer (1988, sections IV and V).

The main thrust of the above result generalizes to any PHM (3).

Define the integrated baseline hazard Λ0(t) =∫ t0 λ0(t)dt, then the fol-

lowing well known generalization of the accelerated failure time model

holds

log(Λ0(Ti)) = x′iβ + ϵi (5)

with ϵi again following an extreme value distribution and β = −β, see

Koenker and Bilias (2001) for a discussion contrasting this result to

quantile regression. Thus, the proportional hazard rate model (3) im-

plies a linear regression model for the a priori unknown transformation

h(Ti) = log(Λ0(Ti)). This regression model involves an error term

with an a priori known distribution of the error term and a constant

coefficient vector across quantiles.

From a quantile regression perspective, it is clear that these properties

of the PHM are quite restrictive. It is possible to investigate whether

these restrictions hold by testing for the constancy of the estimated

coefficients across quantiles. However, if a researcher does not apply

the correct transformation in (5), e.g. the log transformation in (4) is

used though the baseline hazard is not Weibull, then the implications

are weaker. Koenker and Geling (2001, p. 462) show that the quan-

tile regression coefficients must have the same sign if the the data is

generated by a PHM.

A strong, and quite apparent violation of the proportional hazard

assumption occurs, if for two different covariate vectors xi and xj,

41

the survival functions Si(t) and Sj(t), or equivalently the predicted

conditional quantiles, do cross. Crossing occurs, if for two quantiles

θ1 < θ2 and two values of the covariate vector xi and xj, the ranking

of the conditional quantiles changes, e.g. if qθ1(Ti|xi) < qθ1(Tj|xj)and qθ2(Ti|xi) > qθ2(Tj|xj). Our empirical application below involves

cases with such a finding. This is a valid rejection of the PHM, pro-

vided our estimated quantile regression provides a sufficient goodness–

of–fit for the conditional quantiles.

Summing up the comparison so far, while there are some problems

when using the PHM with both unobserved heterogeneity and time–

varying covariates, the PHM can take account of these issues in a

somewhat better way than quantile regression. Presently, there is also

a clear advantage of the PHM regarding the estimation of compet-

ing risk models. However, the estimation of a PHM comes at the

cost of the proportional hazard assumption which itself might not be

justifiable in the context of the application of interest. Furthermore,

quantile regression can account of right censoring by estimating cen-

sored quantile regression.

42

Estimating the Hazard Rate based on Quantile Regression

Applications of duration analysis often focus on the impact of covari-

ates on the hazard rate. Quantile regression estimate the conditional

distribution of Ti conditional on covariates and it is possible to infer

the estimated conditional hazard rates from the quantile regression

estimates.

A direct approach is to construct a density estimate from the fitted

conditional quantiles qθ(Ti|xi) = h−1(x′iβθ). A simple estimate for

the hazard rate as a linear approximation of the hazard rates between

the different θ–quantiles would be

λi(t) =(θ2 − θ1)(

h−1(x′iβθ2)− h−1(x′iβθ1))(1− 0.5(θ1 + θ2))

, (6)

where λi(t) approximates the hazard rates between the estimated θ1–

quantile and θ2–quantile.

1. The estimated conditional quantiles are piecewise constant due to

the linear programming nature of quantile regression.

2. It is not guaranteed that the estimated conditional quantiles are

ordered correctly, i.e. it can occur that qθ1(Ti|xi) > qθ2(Ti|xi)even though θ1 < θ2.

In order to avoid these problems, Machado and Portugal (2002) and

Guimaraes et al. (2004) suggest a resampling procedure (henceforth

denoted as GMP) to obtain the hazard rates implied by the esti-

mated quantile regression. Based on the same motivation as the

Machado/Mata (2005) approach introduced for decomposition analy-

sis, the main idea of the GMP is to simulate data based on the esti-

mated quantile regressions for the conditional distribution of Ti given

the covariate and to obtain estimate the density and the distribution

function directly from the simulated data.

43

GMP works as follows (possibly only simulating non–extreme quan-

tiles):

1. Generate M independent random draws θm,m = 1, ...,M from a

uniform distribution on (θl, θu), i.e. extreme quantiles with θ < θlor θ > θu are not considered here. θl and θu are chosen in light

of the type and the degree of censoring in the data. Additional

concerns relate to the fact that quantile regression estimates at

extreme quantiles are typically statistically less reliable, and that

duration data might exhibit a mass point at zero or other extreme

values. The benchmark case with the entire distribution is given

by θl = 0 and θu = 1.

2. For each θm, estimate the quantile regression model obtaining M

vectors βθm (and the transformation h(.) if part of the estimation

approach).

3. For a given value of the covariates x0, the sample of size M with

the simulated durations is obtained as,

T ∗m ≡ qθm(Ti|x0) = h−1(x′0β

θm) with m = 1, ...,M .

4. Based on the sample T ∗m,m = 1, ...,M, estimate the condi-

tional density f ∗(t|x0) and the conditional distribution function

F ∗(t|x0).

5. We suggest to estimate the hazard rate conditional on x0 in the

interval (θl, θu) by1

λ0(t) =(θu − θl)f

∗(t|x0)1− θl − (θu − θl)F ∗(t|x0)

.

Simulating the full distribution (θl = 0 and θu = 1), one obtains

the usual expression: λ0(t) = f ∗(t|x0)/[1− F ∗(t|x0)].1Our estimate differs from the version suggested in Guimaraes et al. (2004). f∗(t|x0) estimates the conditional

density in the quantile range (θl, θu), i.e. f (T = t|qθl(T |x0) < T < qθu(T |x0), x0), and the probability of theconditioning event is θu− θl = P (qθl(T |x0) < T < qθu(T |x0)|x0). By analogous reasoning, the expression in thedenominator corresponds to the unconditional survival function, see Zhang (2004) for further details.

44

This procedure (step 3) is based on the probability integral transfor-

mation theorem from elementary statistics implying T ∗m = F−1(θm)

is distributed according to the conditional distribution of Ti given x0if F (.) is the conditional distribution function and θm is uniformly

distributed on (0, 1).

The GMP procedure uses a kernel estimator for the conditional density

f ∗(t|x0) =1

M h

M∑m=1

K

t− T ∗i

h

where h is the bandwidth and K(.) the kernel function. Based on this

density estimate, the distribution function estimator is

F ∗(t|x0) =1

M

M∑m=1

Kt− T ∗

i

h

with K(u) =∫ t

aK(v) dv .

Machado and Portugal (2002) and Guimaraes, J., Machado, J.A.F.,

and Portugal, P. (2004) suggest to start the integration at zero (a =

0), probably because durations are strictly positive. However, the

kernel density estimator also puts probability mass into the region of

negative durations, which can be sizeable with a large bandwidth. Us-

ing the above procedure directly, it seems more advisable to integrate

starting from minus infinity a = −∞.

A better and simple alternative would be to use a kernel density estima-

tor based on log durations. This is possible when observed durations

are always positive, i.e. there is no mass point at zero. Then, the

estimates for density and distribution function for the duration itself

can easily be derived from the density estimates for log duration by

applying an appropriate transformation.

45

Unemployment Duration Among German Youth

Reference: Fitzenberger and Wilke (2006, long version)

The purpose is to apply censored quantile regression (CQR) to un-

employment duration among German Youth in order to illustrate the

applicability of the method. Youth unemployment is a critical issue

in the literature. The CQR results suggest that a simple proportional

hazard rate model with time–invariant covariates is not justified for

the data.

Set of covariates used for estimation based on large micro data from

IAB for German young workers:

• gender of the unemployed.

• marital status of the unemployed.

• married females. This variable absorbs possible effects of out of

the labor force periods or parental leave periods of females. A child

indicator is not used because information about the presence of

children is not available for all years.

• married females in the 1990s. This variable accounts for a possible

change in the labor force participation rate of the females in the

1990s.

• we use 5 business sector categories: agriculture, trade/services/traffic,

construction, public sector, others (mainly production). The vari-

ables are grouped according to the similarity of the results in pre-

liminary estimations.

• wage quintile 4,5. This variables indicates whether the unem-

ployed had pre–unemployment earnings in the highest 40% of the

population earnings distribution.

46

• quarterly GDP growth rate. This variable is the quarterly change

in gross GDP measured in prices of 1995. It is affected by seasonal

variation and by the business cycle in general.

• recall dummy indicating a recall to the former employer at the end

of the previous unemployment period.

• four categories for regional information: Rhineland-Palatinate/Hesse,

Baden-Wuerttemberg, Bavaria and nothern states/Saarland (ref-

erence group). These categories are also constructed according to

similarity in preliminary estimation results.

• monthly unemployment rate at the state level unemployment of-

fice districts which mainly overlap with the areas of the federal

states.

• length of tenure before unemployment: less than one year, 1-3

years (reference category), more than 3 years.

• three calender year indicators: 1981 (reference year), 1985, 1990,

1995.

• indicator for no completed apprenticeship in 1995.

• winter time indicator, which is one if the unemployment spell starts

between October and March.

Only about 8% of the unemployment spells are right censored, which

is quite a moderate degree of censoring in the context of duration

analysis.

47

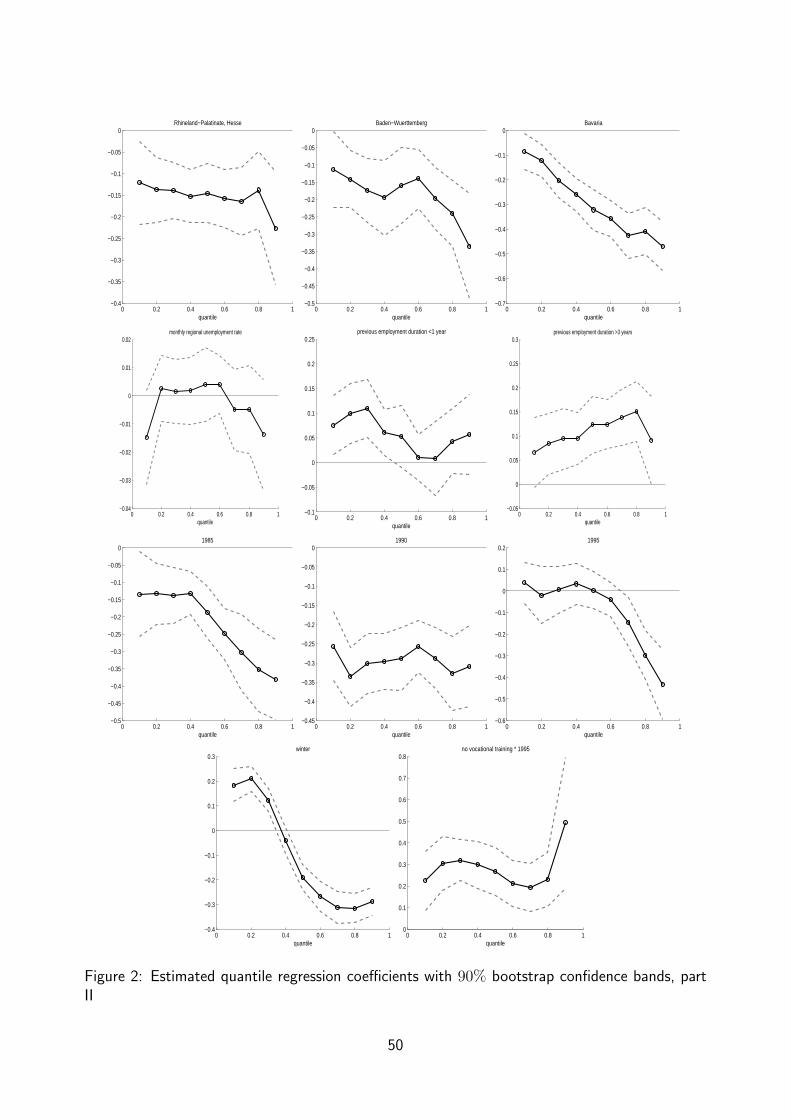

Estimation Results

We estimate a log-linear version of model (1), i.e.

log(Ti) = x′iβθ + ϵθi ,

at each decile, θ = 0.1, 0.2, . . . , 0.9. The CQR model is estimated

using the BRCENS algorithm implemented in TSP. Inference on the

CQR coefficients is based on a standard bootstrap using 50 resam-

ples. The estimated coefficients are reported in figures 1 and 2. It is

evident that many of them vary significantly over the quantiles. The

magnitude or even the sign of the effect of a covariate then differs be-

tween short-term (lower quantiles) and long-term unemployed (upper

quantiles) indicating the need for a flexible estimation method. For

example, the coefficient for the covariate ”married” is not significant

for short unemployment duration but its magnitude increases continu-

ously and it is highly negative at the upper quantiles. The winter time

variable elongates short duration and shortens long duration. However,

the calender time effect has to be considered jointly with the quarterly

GDP growth rate, the calender year dummies, and the monthly unem-

ployment rate. For this reason, it is hard to interpret this result. As

outlined in the previous section, the Cox-proportional hazard model

does not allow for a change of sign of the partial derivative of the con-

ditional quantile function, as observed very clearly for the coefficient

of the winter dummy.

48

0 0.2 0.4 0.6 0.8 10

1

2

3

4

5

6

7

8

9intercept

quantile0 0.2 0.4 0.6 0.8 1

−0.7

−0.6

−0.5

−0.4

−0.3

−0.2

−0.1

0female

quantile0 0.2 0.4 0.6 0.8 1

−0.5

−0.4

−0.3

−0.2

−0.1

0

0.1

0.2married

quantile

0 0.2 0.4 0.6 0.8 10

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

2female*married

quantile0 0.2 0.4 0.6 0.8 1

−1

−0.8

−0.6

−0.4

−0.2

0

0.2

0.4female*married (1990,1995)

quantile0 0.2 0.4 0.6 0.8 1

−0.5

−0.4

−0.3

−0.2

−0.1

0

0.1

0.2agriculture

quantile

0 0.2 0.4 0.6 0.8 1−0.3

−0.25

−0.2

−0.15

−0.1

−0.05

0

0.05trade, services, traffic

quantile0 0.2 0.4 0.6 0.8 1

−0.7

−0.6

−0.5

−0.4

−0.3

−0.2

−0.1

0construction

quantile0 0.2 0.4 0.6 0.8 1

−0.5

−0.4

−0.3

−0.2

−0.1

0

0.1

0.2

0.3

0.4public sector

quantile

0 0.2 0.4 0.6 0.8 1−0.4

−0.35

−0.3

−0.25

−0.2

−0.15

−0.1

−0.05

0

0.05wage quintile 4,5

quantile0 0.2 0.4 0.6 0.8 1

−1

0

1

2

3

4

5

6GDP growth

quantile0 0.2 0.4 0.6 0.8 1

−0.9

−0.8

−0.7

−0.6

−0.5

−0.4

−0.3

−0.2

−0.1

0recall

quantile

Figure 1: Estimated quantile regression coefficients with 90% bootstrap confidence bands, part I

49

0 0.2 0.4 0.6 0.8 1−0.4

−0.35

−0.3

−0.25

−0.2

−0.15

−0.1

−0.05

0Rhineland−Palatinate, Hesse

quantile0 0.2 0.4 0.6 0.8 1

−0.5

−0.45

−0.4

−0.35

−0.3

−0.25

−0.2

−0.15

−0.1

−0.05

0Baden−Wuerttemberg

quantile0 0.2 0.4 0.6 0.8 1

−0.7

−0.6

−0.5

−0.4

−0.3

−0.2

−0.1

0Bavaria

quantile

0 0.2 0.4 0.6 0.8 1−0.04

−0.03

−0.02

−0.01

0

0.01

0.02monthly regional unemployment rate

quantile0 0.2 0.4 0.6 0.8 1

−0.1

−0.05

0

0.05

0.1

0.15

0.2

0.25previous employment duration <1 year

quantile

0 0.2 0.4 0.6 0.8 1−0.05

0

0.05

0.1

0.15

0.2

0.25

0.3previous employment duration >3 years

quantile

0 0.2 0.4 0.6 0.8 1−0.5

−0.45

−0.4

−0.35

−0.3

−0.25

−0.2

−0.15

−0.1

−0.05

01985

quantile0 0.2 0.4 0.6 0.8 1

−0.45

−0.4

−0.35

−0.3

−0.25

−0.2

−0.15

−0.1

−0.05

01990

quantile0 0.2 0.4 0.6 0.8 1

−0.6

−0.5

−0.4

−0.3

−0.2

−0.1

0

0.1

0.21995

quantile

0 0.2 0.4 0.6 0.8 1−0.4

−0.3

−0.2

−0.1

0

0.1

0.2

0.3winter

quantile0 0.2 0.4 0.6 0.8 1

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8no vocational training * 1995

quantile

Figure 2: Estimated quantile regression coefficients with 90% bootstrap confidence bands, partII

50

0 100 200 300 400 500 600 700 8001

1.5

2

2.5

3

3.5

4

4.5

5

5.5x 10

−3

days unemployed

unmarriedmarried

0 100 200 300 400 500 600 700 8001

1.5

2

2.5

3

3.5

4

4.5

5

5.5x 10

−3

days unemployed

summerwinter

Figure 3: Estimated conditional hazard rates evaluated at sample means of the other regressors.

We also estimate hazard functions using the GMP resampling proce-

dure. Figure 3 presents different hazard rate estimates based on this

methodology. For the reasons discussed above, we base our hazard

rate estimations on nonparametric density estimates for the log du-

ration. The number of resamples is 500. Since almost 10% of our

observations are right censored, we draw θm from the uniform distri-

bution on (θl, θu) = (0, 0.9). Both plots in figure 3 show that the

estimated hazard rates are non–proportional over the duration time.

The proportional hazard assumption is apparently violated in this ap-

plication.

51

6. Quantile Regression for Panel Data

References:

Koenker (2005, Chapter 8.7), Abrevaya/Dahl (2008)

Panel data (i=1,...,N; t=1,...,T)

yit = x′itβ + αi + uit

where αi individual specific effect.

Random Effects estimation (GLS):

βGLS = (X ′Ω−1X)−1X ′Ω−1Y

where T ×T -matrix, Ω = diag(Ω1,Ω2, ...,ΩN), Ωi = σ2αιT ι

′T +σ2

uIT ,

IT is T × T identity matrix, and ιT = (1, ..., 1)′.

βGLS solves

min(α,β)∑i,t(1/σ2

u)(yit − xitβ − αi)2 + (1/σ2

α)∑iα2i

where α = (α1, ..., αN).

Fixed Effects estimation (FE): Within Regression

yit − yi = (xit − xi)′βFE + uit − ui

where yi, xi, and ui individual specific means.

52

Quantile Regression with Penalized Fixed Effects

(α(θ), β(θ)) = argminα,β∑i,tρθ(yit − x′itβ − αi) + λ

∑i|αi|

where αi(θ) is an individual-specific shifter of the conditional θ-quantile

of yit given xit and αi.

l1- penalty: λ∑i |αi| implies shrinkage towards zero, linear program-

ming techniques can be applied

Uniform shifter αi across k quantiles (θ1, ..., θk) (location-shift fixed

effects):

(α, β(θ)) = argminα,β

q∑k=1

∑i,tρθk(yit − x′itβ(θk)− αi) + λ

∑i|αi|

Choice of λ for median regression: If σu and σα were known, λ could

be chosen as σu/σα in analogy to random effects GLS estimation.

Estimator does not overcome the incidental parameter problem!

Alternatives:

i) Two-step estimator using OLS FE-estimates of αi:

1. Estimate FE-OLS estimator βFE and calculate estimated individ-

ual specific effect αi = yi − x′iβFE.

2. Run pooled quantile regression of yit−αi on xit to obtain quantile

regression estimate for βθ

ii) Chamberlain-Mundlak type quantile regression estimator (Abre-

vaya/Dahl 2008):

yit = x′itβ(θ) + x′iγ + uit

where x′iγ is control function for individual specific effect. This esti-

mator could be combined with penalized fixed effects estimator.

53