Embed Size (px)

Citation preview

1 Property Market Report—March 2012

March quarter 2012

Property Market Report

Queensland

About This Report

PRP Valuers and Consultants prepare standard research reports covering the

main markets within which we operate in each of our capital cities and major

regional locations.

The markets covered in this research report include the commercial office

market, industrial market, retail market, hotel and leisure market and residential

market.

We regularly undertake valuations of residential property for mortgage

purposes, as well as for development funding purposes. We also undertake

valuations of commercial, retail, industrial, hotel and leisure and special purpose

properties for many varied reasons, as set out later herein.

Please contact a Director of our relevant office for any valuation or consulting

quotations and advice.

Economic Fundamentals 2

Brisbane CBD Office Market 3

Gold Coast Office Market 5

Retail Market 6

Industrial Market 7

Residential Market 9

Hotel and Leisure Market 12

About Preston Rowe Paterson 16

INSIDE THIS ISSUE:

2 Property Market Report—March 2012

The Australian economy continues to

record moderate growth, despite the

global outlook remaining cloudy.

Slightly below trend, GDP increased

by 2.3 percent over 2011, with the

December quarter recording a 0.4

percent increase. Lower than

expected GDP growth is a partial

reflection of the extreme weather

conditions experienced earlier in the

year.

Another disappointing month for retail

spending in February 2012, as total

retail sales rose by a mere 0.2

percent. Welcomed rises were seen in

Food Retailing, Department Stores

and Other Retailing, whilst falls were

recorded in Cafes & Restaurants,

Clothing Retailers and Household

Goods Retailing.

The unemployment rate rose to 5.2

percent in February. Job figures fell by

15,400, underpinned by falls in part

time employment, as fulltime jobs

remained flat. The participation rate

fell from 65.3 percent to 65.2 percent,

with the decline concentrated in

Males, whilst total hours worked rose

by 1.4 percent.

The RBA held the official cash rate

unchanged at 4.25 percent, and

explained that despite easing interest

rates by 50 basis points in late 2011,

the current pace of output growth is

somewhat lower than earl ier

anticipated. The RBA stated that it

would wait for Q1 CPI data before

considering a further step in easing

monetary policy.

Consumer sentiment tumbled in

March, with the Westpac-Melbourne

Institute index recording a 5 percent

decline over the month. The index fell

from 101.10 in February 2012 to 96.1 in

March 2012. Domestic economic

conditions and employment listed as

Survey respondents main concerns.

The Consumer Price Index (CPI)

remained unchanged in the

December 2011 quarter, compared

to a 0.6 percent rise experienced in

the September quarter. A significant

rise was recorded in domestic holiday

travel and accommodation with a 7.3

percent increase. Not surprisingly falls

were observed in fruit and vegetables

with falls of 13.4 percent and 5.0

percent respectively.

Economic Fundamentals

-3

-2

-1

0

1

2

3

4

5

0.0

50,000.0

100,000.0

150,000.0

200,000.0

250,000.0

300,000.0

350,000.0

400,000.0

Se

p-0

6

De

c-0

6

Ma

r-0

7

Ju

n-0

7

Se

p-0

7

De

c-0

7

Ma

r-0

8

Ju

n-0

8

Se

p-0

8

De

c-0

8

Ma

r-0

9

Ju

n-0

9

Se

p-0

9

De

c-0

9

Ma

r-1

0

Ju

n-1

0

Se

p-1

0

De

c-1

0

Ma

r-1

1

Ju

n-1

1

Se

p-1

1

De

c-1

1

% C

ha

ng

e

GD

P M

illio

ns

Gross Domestic Product

Gross Domestic Product Seasonally Adjusted % Change Seasonally Adjusted

Source: ABS/PRP Research

3,000

3,200

3,400

3,600

3,800

4,000

4,200

4,400

4,600

4,800

5,000

75.0

80.0

85.0

90.0

95.0

100.0

105.0

110.0

115.0

120.0

125.0

130.0

De

c-0

6

Ma

r-0

7

Ju

n-0

7

Se

p-0

7

De

c-0

7

Ma

r-0

8

Ju

n-0

8

Se

p-0

8

De

c-0

8

Ma

r-0

9

Ju

n-0

9

Se

p-0

9

De

c-0

9

Ma

r-1

0

Ju

n-1

0

Se

p-1

0

De

c-1

0

Ma

r-1

1

Ju

n-1

1

Se

p-1

1

De

c-1

1

QLD

Tu

rno

ve

r ($

millio

n)

We

stp

ac

-Me

lb In

stit

ute

Co

nsu

me

r Se

nti

me

nt

Ind

ex

QLD Turnover and Consumer Sentiment

Consumer Sentiment Index QLD TurnoverSource: ABS/PRP Research

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

3,000,000

3,500,000

4,000,000

4,500,000

5,000,000

5,500,000

Ma

r-0

7

Ju

n-0

7

Se

p-0

7

De

c-0

7

Ma

r-0

8

Ju

n-0

8

Se

p-0

8

De

c-0

8

Ma

r-0

9

Ju

n-0

9

Se

p-0

9

De

c-0

9

Ma

r-1

0

Ju

n-1

0

Se

p-1

0

De

c-1

0

Ma

r-1

1

Ju

n-1

1

Se

p-1

1

De

c-1

1

Ma

r-1

2

Un

em

plo

yme

nt

Rat

e %

Un

em

plo

yed

pe

rso

ns

Unemployment (Rate and Persons)

Unemployed Persons Unemployment RateSource: ABS/PRP Research

3 Property Market Report—March 2012

total space in the Brisbane CBD office

market has risen by 1.4 percent, rising

from 2.04 million sqm in the six months

to January 2011 to 2.07 million sqm in

the six months to January 2012. A

Grade stock saw the sharpest in-

crease in occupancy levels over the

year, rising by 4.9 percent. B Grade

still dominates the market with 40.4

percent of share; however A grade

space has been in demand in the six

month to January 2012, rising to 39.2

percent of market share. C Grade

space saw a marginal decline in oc-

cupancy rates, falling from 220,646

sqm to 220,220 sqm in the six months

to January 2012.

Commercial Office Market

Stock (m2) Vacancy % Stock (m2) Vacancy %

Total (All Grades) 2,071,240 6.16% 1,136,347 7.63%

Premium 140,015 2.65%

A Grade 812,629 4.05% 526,795 3.09%

B Grade 837,034 7.49% 411,912 13.36%

C Grade 220,220 8.36% 175,622 8.79%

D Grade 61,342 16.09% 22,018 0.00%

Brisbane Commercial - Stock & Vacancy

Precinct/GradeBrisbane CBD Brisbane Fringe

-30,000

-10,000

10,000

30,000

50,000

70,000

90,000

Jan-06 Jul-06 Jan-07 Jul-07 Jan-08 Jul-08 Jan-09 Jul-09 Jan-10 Jul-10 Jan-11 Jul-11 Jan-12

Au

dit

ed

Ne

t A

bso

rpti

on

12

mo

nth

s to

...(

sqm

)

Brisbane CBD Office Market

Net Absorption

Source: PCA/PRP Research

6.8%

39.2%

40.4%

10.6%3.0%

Brisbane CBD Office Market

Premium A-Grade B-Grade C-Grade D-Grade

Source: PCA/PRP Research

BRISBANE CBD OFFICE

MARKET

Supply In the six months to January 2012,

39,400 sqm of office space entered

the Brisbane CBD office market follow-

ing the completion of 123 Albert

Street. When construction reached

completion in early 2012, The Dexus

owned 26 level building, added

38,500 sqm of Premium office space

to the Brisbane CBD office market. Rio

Tinto committed to 25,000 sqm of

space in 2008, whilst recent agree-

ments were reached with QTC and

Urbis to secure 4,000 and 1,500 sqm

respectively.

The Brisbane CBD supply pipeline

looks set to return to more positive

territory in the coming years with

111,000 sqm of additional space ex-

pected to reach completion over

2012. 64,000 sqm is forecast to come

on line with the completion of the GPT

Wholesale Office Fund/Abu Dhabi

Investment Authority joint venture at

111 Eagle Street, with a further 28,200

sqm after the completion of 145 Ann

Street. An additional 18,800 sqm of

refurbished office space will further

bolster current CBD office market

levels. Looking further into the supply

pipeline, 2013 completion levels sof-

ten to sub 20,000 sqm, before return-

ing to more buoyant levels in 2014.

Net Absorption/Vacancy Lev-

els Brisbane CBD vacancy levels firmed

1.2 percentage points in the six

months to January 2012, falling from

7.4 percent recorded in the six months

to July, to 6.2 percent in the six months

to January 2012. Lower grade stock (c

& d) in Brisbane CBD office market

experienced a softening in vacancy

rates over this period, with D grade

recording the most marked increase

in vacancy rates, lifting from 10.5 per-

cent in the six months to July to 16.1

percent in the six month to January

2012. On a more positive note B

grade vacancy rates tightened from

10.9 percent recorded in the six

months to July 2011 to 7.5 percent in

the six months to January 2012.

Occupancy levels In the 12 months to January 2012,

4 Property Market Report—March 2012

Demand/Leasing Activity With record levels of expansion by the

resources sector and a renew confi-

dence is other sectors, net absorption

was well above historical long term

averages. Just over 54,000 sqm of

space was absorbed in CBD office

market over the six months to January

2012, taking the 12 months total ab-

sorption rate to over 92,000 sqm. Since

January 2010, approximately 187,000

sqm of space has been absorbed in

the Brisbane CBD office market. As

supply levels increased by only

118,000 sqm over this period, declin-

ing vacancy rates resulted. Looking

into further detail, 37,000 sqm of A

grade space was absorbed in the six

months to January 2012, with B grade

space seeing robust demand with

over 21,000 sqm of take-up.

Reinforcing confidence in the market,

demand levels remained buoyant in

the first quarter of 2012, with several

large leasing deals transacted over

the three months to March. Dominate

players in the market include the pro-

fessional services and the enormous

presence felt by the resource sectors.

Xstrata secured just under 2,500 sqm

of premium space from GPT Group at

111 Eagle Street, whilst late March

saw Arrow Energy leasing 14,800 sqm

at the same address, on an eight year

lease for an undisclosed rent.

Not forgetting the professional ser-

vices sector, Queensland Treasury

Corporation leased just over 3,800

sqm of space from Dexus Property

Group at 123 Albert Street, for re-

ported par $725 sqm pa for a period

of seven years and after 20 years at

300 Queens street, BDO has commit-

ted to 6,000 sqm of refurbished space

at 12 Creek street for a period of 12

years.

Following trend of decentralisation

activity by core service providers and

public sector industries, a number of

tenants are moving outside the CBD

and relocating to the suburbs &

Fringe. The bank of Queensland has

pre-committed to leasing 12,500 sqm

of space at the new “Gasworks” de-

velopment at Newstead Riverpark in

the Brisbane Fringe. The development

is expected to begin construction in

2013 and scheduled for completion in

February 2014, with rents believed to

be in the low $500 per sqm bracket.

The Macquarie Group has leased

3,200 sqm of space at 825 Ann Street,

Fortitude Valley from Laing O’Rourke

for undisclosed terms. The Building is

now 100 percent precommitted and

is expected to reach completion in

mid 2012.

Rents A robust leasing environment and

tightening vacancy rates in the Bris-

bane CBD have underpinned rental

growth in both premium and A grade

space. Premium grade rents have

increased by over 2 percent in the last

twelve months to sit between $700 -

$825 sqm pa. A Grade office space in

the Brisbane CBD attracts rental rates

of between $625 - $725 sqm. In the six

months to March 2012, Lower grade

office space (b) has transacted rang-

ing between $500 -$625 sqm.

Investment Activity Strengthening tenant demand com-

bined with a robust economic growth

outlook over the medium term, has

caught the attention of both the do-

mestic and the offshore investor alike.

Five major transactions were re-

corded by PRP Research in the Bris-

bane Office Market, during the first

quarter of 2012, with a total transac-

tion value of $291 million. The most

notable transaction to occur during

this period was the purchase of 215

Adelaide Street, Brisbane by US based

Preamerica Real Estate Investors for

$134.5 million. The 30,000 sqm office

tower was purchased from GIC on an

approximate passing yield 8.5 per-

cent. A further notable transaction to

occur during the first quarter of 2012

was The Hines Global REIT purchase of

144 Montague Street in South Brisbane

for a reported $88 million. The 15,000

sqm building was purchased from

Empricia Management Trust on an

initial yield of 8.5 percent.

379 Queen Street sold in March 2012,

for a reported $21 million to

Kingsmede Pty Ltd. The 15 level, 5500

sqm commercial tower is fully leased

with a net income of approx $2.4 mil-

lion per year, representing an initial

passing yield of around 11.5 percent.

An undisclosed private investor pur-

chased 20 Wharf Street for approxi-

mately $11.3 million in January this

year. Chesterton International bro-

kered the deal for vendor, NEXTDC on

an initial passing yield of 8.3 percent.

The final transaction to have occurred

in the first quarter of 2012 was sale of

the Becton office Fund’s 369 Ann

Street for approximately $36.25 million.

An undisclosed private investor pur-

chased the 6,700 sqm office block on

an initial passing yield of 10.04 per-

cent. With long term growth drivers in

place for the Queensland economy

and demand set to remain strong,

good quality assets are expected to

continue to attract attention from

investors.

215 Adelaide Street, Brisbane was purchased

by Preamerica Real Estate, for $134.5 Million.

5 Property Market Report—March 2012

GOLD COAST OFFICE

MARKET

Supply An additional 931 sqm was added to

the Gold Coast Office Market in the

six months to January 2012 with the

completion of a two storey office

complex at Via Roma Isle of Capri.

The Gold Coast office Market now

consists of 473,700 sqm of space, of

which 21.8 percent is vacant. The

2012 supply pipeline remains positive

with an anticipated 3,192 sqm of ad-

ditional space due to complete over

the year. Just under 2,000 sqm of

office space will be added to the

market with the completion of 237

Scottsdale Drive Robina, which is ex-

pected in the first half of this year. A

Further 1,200 sqm of space will come

on line when 82 Marine Parade South-

port completes during the June quar-

ter.

Demand/Vacancy Levels In the six months to January 2011 just

over 3,200 sqm of space was ab-

sorbed in the Gold Coast Office Mar-

ket, taking the 12 month total to 9,888

sqm. Positive net absorption and

scarce new supply has led to a 0.6

percent tightening in the Gold Coast

Office Market vacancy. Vacancy in

this market fell from 22.4 percent re-

corded in the six months to July 2011

to currently sit at 21.8 percent. B

Grade vacancy saw the most marked

improvement, tightening by 1.9 per-

cent points over the six month period.

However in stark contrast D Grade

office vacancy weakened by 9.8

percent over the six months to Janu-

ary 2012. Vacancy rates in the Gold

Coast D Grade Office Market rose

from 12.6 percent in the six months to

July 2011 to 22.4 percent over the six

months to January 2012.

Occupancy B Grade space dominates occu-

pancy levels in the Gold Coast Office

Market, with 39.6 percent of total sup-

ply. A and C Grade space equate for

28.8 and 28.0 percent of the market

respectively. Little change has been

seen in total occupancy levels over

the last 12 months. A mere 2.7 per-

cent increase was seen in occupancy

levels over the 12 months to January

2012, however looking closer at a sub-

market level, A Grade stock posted a

13.9 percent increase in occupied

stock over the period whilst D Grade

saw its third decline recording nega-

tive growth of 11.1 percent over the

period.

Investment Activity PRP Research did not record any sales

or lease transactions over 2,500 sqm or

par $5 million that occurred during the

three months to March 2012.

-20,000

-10,000

0

10,000

20,000

30,000

40,000

50,000

Jan-06 Jul-06 Jan-07 Jul-07 Jan-08 Jul-08 Jan-09 Jul-09 Jan-10 Jul-10 Jan-11 Jul-11 Jan-12

Au

dit

ed

Ne

t A

bso

rpti

on

12

mo

nth

s to

...(

sqm

)

Gold Coast Office Market

Net Absorption

Source: PCA/PRP Research

0.0%

28.0%

39.6%

28.8%

3.7%

Gold Coast Office Market

Premium A-Grade B-Grade C-Grade D-Grade

Source: PCA/PRP Research

6 Property Market Report—March 2012

Demand Total Retail turnover in the state of

Queensland saw a 2.1 percent in-

crease over a 12 month period to

February 2012, with robust growth

seen in ‘Other Retailing’ categories

and Food Retailing alike. “Other retail-

ing” underpinned by buoyant in-

creases in both Pharmaceutical, Cos-

metics etc and Newspaper, Book

Retailing, saw a 6.9 percent increase

over the 12 months to February 2012.

Food Retailing grew by 5.2 percent

over the 12 month period, to its high-

est level ever recorded. A growth

spike was also seen in Cafe and Res-

taurant Retailing, however falls were

recorded in Household Good, Depart-

ment Stores, and Clothing and Foot-

wear Retailing. Clothing and Foot-

wear recorded the largest decline

over the 12 months to February 2012,

falling by 5.7 percent, whilst Depart-

ment Store and Household Good

Retailing fell by 5.4 percent and 3.3

percent respectively.

Investment During the three months to March

2012, PRP Research recorded four

major retail transactions within the

Queensland Retail Sector, with a total

market value of $452.2 million. Most

Notably, Late March saw CFS Retail

Property Trust announce the sale of a

50% share of the Myer Centre in Bris-

bane, to Unlisted Property Trust, ISPT

for $366 million, representing an initial

yield of 6.5 percent. The six level CBD

Regional Shopping Centres provides

63,700 sqm of retail space, and

houses Myer, Target, Coles, and 180

additional speciality retail stores. Prior

to this sale, LaSalle Australia Core Plus

Fund purchased Nerang Mall Shop-

ping centre in February 2012 for a

reported $23.4 million. The 8,700 sqm

neighbourhood shopping centre has

been purchased from Mr Henry Yuen

on a yield in excess of 10 percent.

Mid March, saw Stockland’s purchase

Centro Townsville at Aitkenvale in

North Queensland for approximately

$36.5 million. The 13,650 sqm Subre-

gional shopping centre was pur-

chased from the Centro owned MCS

17 Syndicate on an initial yield of 8.3

percent. The centre is anchored by

Kmart and Coles and contains a fur-

ther 25 specialty shops. Increased

investment activity exhibits a renewed

confidence in the retail property sec-

tor despite weakened consumer

spending and increased online retail-

ing. Particular interest has been

placed on Queensland and the re-

source states for investment opportu-

nity, as stronger economic growth is

forecast.

Retail Market

-3.0

-2.5

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

3500.0

3750.0

4000.0

4250.0

4500.0

Fe

b-1

1

Ma

r-1

1

Ap

r-1

1

Ma

y-1

1

Ju

n-1

1

Ju

l-1

1

Au

g-1

1

Se

p-1

1

Oc

t-1

1

No

v-1

1

De

c-1

1

Ja

n-1

2

Fe

b-1

2

Mo

nth

ly P

erc

en

tag

e C

ha

ng

e (

%)

Re

tail T

urn

ov

er $

millio

n

Queensland Retail Turnover

Retail Turnover % Change

Source: ABS/PRP Research

-0.08

-0.06

-0.04

-0.02

0

0.02

0.04

0.06

0.08

0.1

0.12

Nov-2011 Dec-2011 Jan-2012 Feb-2012Mon

thly

% C

hang

e

Food Retailing Household goods Clothing, Footwear Department Stores Other Retailing Cafe, Restaurants

Queensland

Turnover

% Monthly Change

Source: ABS/PRP Research

50% share of Myer Centre in Brisbane was

purchased by ISPT for $366 million, on a yield

of 6.5 percent

7 Property Market Report—March 2012

Leasing Activity: Brisbane A renewed confidence in the Queen-

sland industrial property market, on

the back of increased investment in

the resources sector and positive eco-

nomic growth saw leasing activity

trend upwards in the three months to

March 2012. PRP Research recorded

a number of major transactions that

occurred over this period. The Austra-

lian Mud company, a subsidiary of the

Imdex Group has leased just under

3,000 sqm of space at 67 Wolston

Road in Sumner Park. The industrial

facility was leased for a five year term,

with a five year option, for a net rent

of approx $95 per sqm pa. The AMC

will relocate to its new premises at

Wolston Road after outgrowing its

current premises at Neon Street.

DHL Express has pre-committed to

4,300 sqm of space in Brisbane’s Air-

port Precinct. Construction of the $15

million project will commence in May

this year and is located at the corner

of Lomandra Drive and Boronia Road.

Engineering and construction giant

Clough will lease a 46.9 hectares site

at 70 Darlington Drive, Yatala on a five

year term, reportably worth $1.8 million

plus per year . The facility comprises of

9,500 sqm of factory, and 1,800 sqm of

office space.

Supply The South East Queensland Industrial

land Monitoring Program identified as

at December 2010, 8,852 hectares of

industrial land that currently exists in

the South East Queensland industrial

land area, with a further 5,594 hec-

tare of potential industrial land supply

available within in the region. It is esti-

mated that industrial land consump-

tion in the four years to December

2010, was 120 hectares per annum,

However estimated annual consump-

tion of industrial land in South East

Queensland for the six months to De-

cember 2010 has declined to 41 hec-

tares (or approx 82 hectares per an-

num). It is predicted that for a 5 to 15

year time frame, 3,940 hectares of

land will be required to meet esti-

mated average consumption.

Tenant Demand

Fluctuations in demand for logistics

and warehouse space can partly be

explained by ebbs and flow in port

activity. Brisbane Port activity contin-

ues to see growth in full import and

export TEU’s. Since the 2007-2008 Fi-

nancial year, TEU activity has grown

by 10.7 percent in the Port of Bris-

bane. Last year, TEU’s activity saw

exceptional growth with an 8.5 per-

cent increase. The number of TEU’s in

the Port of Brisbane has grown from

639,800 in the 2009-2010 Financial

year to 694,000 in the 2010-2011 finan-

cial year.

As a percentage of Queensland’s

gross state product, income derived

from the manufacturing sector de-

clined by 0.4 percentage points in the

12 months to June 2011. June 2008

saw the trough of total factor income

from manufacturing as a percent of

gross state product, falling to 11.5

percent. Although total factor income

from manufacturing rose to its highest

level recorded, Queensland Gross

State product also saw robust growth

over the year, resulting in a decline in

percentage total. A fall in manufac-

turing income is consistent with the

declines seen in average consump-

tion levels for industrial land over the

six months to December 2010.

Industrial

0

5000

10000

15000

20000

25000

0

50000

100000

150000

200000

250000

300000

Jan

-19

91

Jan

-19

92

Jan

-19

93

Jan

-19

94

Jan

-19

95

Jan

-19

96

Jan

-19

97

Jan

-19

98

Jan

-19

99

Jan

-20

00

Jan

-20

01

Jan

-20

02

Jan

-20

03

Jan

-20

04

Jan

-20

05

Jan

-20

06

Jan

-20

07

Jan

-20

08

Jan

-20

09

Jan

-20

10

Jan

-20

11

Ma

nu

fac

turi

ng

Inc

om

e $

mill

ion

Sta

te P

rod

uc

t $m

illio

n

Queensland Manufacturing Income

V's Gross State Product

Queensland Gross State Product Manufacturing Total Factor IncomeSource:ABS/PRP Research

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

Jan

-04

Jan

-05

Jan

-06

Jan

-07

Jan

-08

Jan

-09

Jan

-10

Jan

-11

Nu

mb

er

of

TEU

's

Port of Brisbane -

Container Trade - TEU's

Import ExportSource: Port of Brisbane /PRP Research

8 Property Market Report—March 2012

Leasing Activity: Gold Coast An undisclosed construction com-

pany, linked to Queensland’s boom-

ing resources sector has leased 5,500

sqm of industrial space plus 660 sqm

of office space at 32 Demand Ave-

nue in Arundel on the Gold Coast. The

property is expected to fetch net

$450,000 per year in rental income for

the owner, equating to $82 plus per

sqm pa .

Investment Activity Undoubtedly one of the largest trans-

action in Queensland industrial his-

tory , Springfield Land Corporation has

purchased half of the high-tech Po-

laris Data Centre in Greater Springfield

for a reported $110.5 million. The pur-

chase give Springfield Land Corpora-

tion 100 percent ownership of the

14,000 sqm building. Tenants include

British Gas, AAPT and Suncorp, who

will retain one third of the floor space.

Sydney based Fund manager Heath-

ley, purchased a nine hectare indus-

trial property at Richlands, from Trinity

Group for $24.5 million. The property

contains a 13,000 sqm building cur-

rently leased to John Holland (a sub-

sidiary of Leighton Holdings).

In February 2012, Dexus Wholesale

property fund purchased a 12,483

sqm industrial facility in Morningside

for a reported $19.7 million, reflecting

a yield of 8.25 percent. And Finally,

Mainfreight has purchased a 5.4 hec-

tare site at 20 Distribution Street, Lara-

pinta for a reported $15.8 Million.

Mainfreight secured the land adja-

cent to Woolworths distribution centre

from Australand, who purchased the

property in November 2010 for $12.25

Million.

The Polaris Data Centre in Greater Spring-

field sold for a reported $110.5 million to

The Springfield Land Corporation.

An undisclosed construction company

will lease 5,000 sqm of industrial space at

32 Demand Avenue, Arundel

9 Property Market Report—March 2012

Demand Population growth is a factor used in

establishing the demand for future

housing. The starting point in deter-

mining population growth is the popu-

lation statistics taken in the Australian

Bureau of Statistics 2006 Census. The

current population at 2006 was esti-

mated at 1.8 million persons in the

Brisbane Region. By the start of 2017

the population of Brisbane is forecast

to increase to 2.24 million, equating to

an additional 420,000 persons over a

ten year period, or an average of

42,000 additional persons per annum.

Changing demographics and house-

hold characteristics have an impact

of demand for housing within Austra-

lia. The A starting point for additional

households is the Census undertaken

in 2006 by the ABS. The Australian Bu-

reau of statistics indicated as at June

2006 there were approximately

671,600 households in the Brisbane

Region. In 2017 the ABS predicts an

additional 195,200 households will be

required to meet demand. This

equates to an average of 17,700

homes per annum. The ABS forecasts

that by 2017 the total number of

households in Brisbane Region will

reach 866,800 households.

Supply Land supply in the South East Queen-

sland Regional plan is currently limited

by new stock coming through. This

stock is often dominated by large lots

and premium product that meets only

the requirements for up-graders. In

2009 stronger demand was evident

for smaller lots in response to the first

home buyer grant; this supply how-

ever, was quickly taken up. Housing

supply in Brisbane is based on the

boundaries of the South-East Queen-

sland Regional Plan 2009-2031 (SEQ).

The SEQ Regional Plan is forecast to

accommodate growth to 2031. These

boundaries are assessed every five

years and extensions are based on

demand and sustainability.

As at June 2009, SEQ had 10,700 hec-

tares of land identified for future ur-

ban use in the supply pipeline with an

estimated dwelling yield of 122,000

lots. Potential land further down the

supply pipeline contains an additional

142,000 dwellings, with 35,500

Greenfield lots identified at the devel-

opment and subdivisional approval

stage.

In comparison to 12 months prior, the

total number of dwelling approvals in

the Brisbane Statistical Division de-

clined by 16 percent over the year to

December 2011. There were a total of

13,480 dwelling approvals in the 2011

calendar year, compared to 16,050

dwelling approvals one year prior. The

decline in total dwelling approvals

was underpinned by a 25 percent

decline in the number of ‘house’

dwellings. The number of non house

dwelling approvals fared better sliding

only five percent over the 12 month

period.

Construction activity in the Sunshine

state continues to decline, with a

further 17 percent fall in the number

of dwelling commencement occur-

ring in the nine months to September

2011 in comparison to the same nine

months, the year prior. The total num-

ber of dwellings that commenced

during the nine months to September

2010 reached 15,600 dwellings; how-

ever the nine months to September

2011 saw total dwelling commence-

ments decline by 3,660 dwellings, to

just under 12,000 dwellings. The num-

ber of new ‘house’ dwelling com-

mencements in the nine months to

September 2011 saw the largest year

on year decline falling 23 percent.

Residential

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

2,000,000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Pro

jec

ted

No

.of h

ou

seh

old

s

Projected No. household - Brisbane SD

Family households Group households Lone person householdsSource: ABS / PRP Research

0

5,000

10,000

15,000

20,000

25,000

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

An

nu

al A

pp

rov

als

Brisbane SD Dwelling Approvals

Houses Other

Source: ABS / PRP Research

10 Property Market Report—March 2012

Market Affordability According to the HIA/Commonwealth

Bank Housing Affordability Index, The

December 2011 quarter, saw housing

affordability in Brisbane improved by

7.9 percent, well above the national

trend of a 2.2 percent increase. Bris-

bane recorded the strongest national

result ahead of Canberra at 6.1 per-

cent and the 4.6 percent improve-

ment seen in Melbourne housing af-

fordability, and now makes Brisbane

more affordable than Adelaide. Un-

derpinning the result was a fall in aver-

age required loan repayments. Re-

cent interest rate cuts by the RBA

along with lower house prices have

resulted in significant improvements in

housing affordability in Brisbane, as

the average requirement loan repay-

ment has fallen in Brisbane to $3078

per month, a drop of 7 percent since

last quarter. The ANZ Australian hous-

ing snapshot released in April 2012,

suggests that the outlook for Queen-

sland remains positive, with increased

investment in major projects resulting

in an upswing in economic conditions.

A tightening of fundamental and im-

proved affordability should result in

the Queensland housing market stabi-

lising over the next six months before

trending upwards.

Over the December 2011quarter, The

Brisbane median house price de-

clined by 0.6 percent, falling from

$427,500 in September to currently sit

at $425,000. The Real Estate institute of

Australia also recorded a year on year

decline of 5.6 percent for Brisbane

median house prices. Median ‘Other

Dwelling’ prices in Brisbane saw posi-

tive results over the quarter, rising by

1.9 percent, however experienced

slight falls year on year, declining 1.1

percent to sit at $376,000.

Over the quarter, falls were recorded

in all zones of Queensland excluding

Inner Brisbane and Townville, where

median house prices rose by 6.3 per-

cent and 0.6 percent respectively.

The most prominent fall in median

house price over the December quar-

ter was recorded in Cairns, where

median house prices fell by 4.4 per-

cent. In comparison to 12 months

prior, all zones in Queensland experi-

enced falls year on year, with the

largest decline evident in the Gold

Coast market, falling by 8.0 percent.

Year on year results for median ‘Other

Dwelling’ prices were mixed. Falls

were recorded in all Queensland

zones excluding the Brisbane Outer

and Middle zones where increases of

5.6 percent and 0.8 percent were

seen respectively. All zones in Queen-

sland experienced increases over the

December 2011 quarter excluding

Sunshine Coast, Townsville and Cairns.

The largest increase over the quarter

was recorded in the Outer Brisbane

market, which rose by 8.3 percent to

sit at $325,000.

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

$0

$45,000

$90,000

$135,000

$180,000

$225,000

$270,000

$315,000

$360,000

$405,000

$450,000

$495,000

$540,000

$585,000

$630,000

$675,000

$720,000

$765,000

Brisbane Inner Brisbane Middle Brisbane Outer Gold Coast Sunshine Coast Townsville Cairns

Qu

art

erl

y P

erc

en

tag

e C

ha

ng

e (

%)

Me

dia

n H

ou

se P

ric

e

Median House Price by Zone

Median House Price Quarterly % ChangeSource: REIA/PRP Research

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

$150,000

$175,000

$200,000

$225,000

$250,000

$275,000

$300,000

$325,000

$350,000

$375,000

$400,000

$425,000

$450,000

Brisbane Inner Brisbane Middle Brisbane Outer Gold Coast Sunshine Coast Townsville CairnsQ

ua

rte

rly

Pe

rce

nta

ge

Ch

an

ge

(%

)

Oth

er d

we

llin

gs

me

dia

n p

ric

e

Median Price for Other Dwellings by Zone

Other Dwelling Quarterly % ChangeSource: REIA/PRP Research

11 Property Market Report—March 2012

Rental Market Positive results were seen in the

Queensland rental market over the

December 2011 quarter. The only

declines recorded over this period

were seen in two bedroom houses in

both the Outer Brisbane and Gold

Coast zones. Median rental rates for a

two bedroom house in Outer Brisbane

fell by 1.9 percent to $260 per week,

whilst Gold Coast two bedroom

homes declined by 7.2 percent to

$320 per week. With the exception of

two bedroom houses in the Gold

Coast, there were no declines in me-

dian house rents over the 12 month

months to December 2011. The most

significant year on year rise in median

house rents was recorded by four

bedroom houses in the Inner Brisbane

Zone. Inner Brisbane Four Bedroom

house median rent rose by 11.3 per-

cent year on year to sit at $690 per

week.

Rental rates for ‘other dwellings’ in

Queensland also remained positive

over the December quarter. Brisbane

Outer Zone, Other dwelling one bed-

room rental rates recorded the only

decline over the quarter, falling 4.8

percent to $200 per week. Most zones

remained unchanged over the pe-

riod; however a substantial increase

was recorded in one bedroom ‘other

dwelling’ rental rates in Townsville.

Townsville one bedroom other dwell-

ing median rental rates, increased by

8.7 percent over the quarter, to $250

per week. Year on year results also

proved positive for median rental

rates in the sunshine state. The most

momentous increase over the 12

month period was recorded for

Townsville one bedroom ‘other dwell-

ing’ median rental rates, rising by 25

percent to $250 per week.

$0

$100

$200

$300

$400

$500

$600

$700

$800

Brisbane Inner Brisbane Middle Brisbane Outer Gold Coast Townsville Cairns

Me

dia

n W

ee

kly

Re

nt

($)

Median Weekly Rents for Houses by Zone

2 Bed House 3 Bed House 4 Bed House

Source: REIA/PRP Research

$50

$100

$150

$200

$250

$300

$350

$400

$450

$500

$550

Brisbane Inner Brisbane Middle Brisbane Outer Gold Coast Townsville Cairns

Me

dia

n W

ee

kly

Re

nt

($)

Median Weekly Rents for Other Dwellings by Zone

1 Bed unit 2 Bed unit 3 Bed unit

Source: REIA/PRP Research

12 Property Market Report—March 2012

QUEENSLAND/BRISBANE

Supply Supply levels in the Queensland Hotel

Motel and Service Apartment market

have remained relatively flat since the

March 2009 quarter, when over the

three years prior 4900 new rooms

flooded the market. The 12 months to

December 2011, saw a decline in the

total number of rooms available, fal-

ling by 1.3 percent. There are cur-

rently just over 61,000 rooms available

per night in the Queensland Hotel

Motel and Serviced Apartment mar-

ket. Deloittes Access Economics states

that Brisbane Hotel Motel and Ser-

viced Apartment market “outlook is

characterised by a relatively high

volume of new hotel projects that are

due for completion over the next two

to four years” Increased supply is ex-

pected to negatively impact occu-

pancy rates.

It is reported that with North Queen-

sland resources boom driving de-

mand for local accommodation in

Townsville and the area’s surrounding

mining towns, two new properties in

Townsville will open during May. The

Country Comfort City Oasis and

Chifley Plaza Townsville will offer 4 &

4½ star accommodation, as well as

function and conference facilities.

Demand Occupancy rates in the Queensland

Hotel Motel and Serviced Apartment

Total Stargraded market grew by 2.1

percentage points in the 12 months to

December 2011 to 66.9 percent. Oc-

cupancy rates peaked in the Decem-

ber 2006 quarter at 69.3 percent.

Looking further into Stargraded detail:

Occupancy rates over all stargrad-

ing’s in the Queensland Hotel Motel

and Serviced Apartment market grew

excluding 5 Stargraded, which de-

clined slightly by 0.1 percentage

points. Surprising results were seen in

1&2 Star combined occupancy rates

over the December quarter, rising 7.1

percent in comparison to 12 months

prior, to 57.2 percent occupancy.

Occupancy rates in the Brisbane Tour-

ism Region Total Stargraded Hotel,

Motel and Serviced apartment mar-

ket continued on an upward trajec-

tory rising a further 1.8 percentage

points in the 12 months to December

2011, to currently sit at 77.2 percent.

Hotel and Leisure

35%

40%

45%

50%

55%

60%

65%

70%

75%

80%

85%

De

c-0

6

Ma

r-07

Jun

-07

Se

p-0

7

De

c-0

7

Ma

r-08

Jun

-08

Se

p-0

8

De

c-0

8

Ma

r-09

Jun

-09

Se

p-0

9

De

c-0

9

Ma

r-10

Jun

-10

Se

p-1

0

De

c-1

0

Ma

r-11

Jun

-11

Se

p-1

1

De

c-1

1

Oc

cu

pa

nc

y R

ate

Queensland HMSA

Graded Occupancy

1 & 2 Star 3 Star 4 Star 5 StarSource: ABS/PRP Research

50%

55%

60%

65%

70%

75%

80%

85%

90%

9500

10000

10500

11000

11500

12000

12500

13000

13500

De

c-0

6

Ma

r-0

7

Ju

n-0

7

Se

p-0

7

De

c-0

7

Ma

r-0

8

Ju

n-0

8

Se

p-0

8

De

c-0

8

Ma

r-0

9

Ju

n-0

9

Se

p-0

9

De

c-0

9

Ma

r-1

0

Ju

n-1

0

Se

p-1

0

De

c-1

0

Ma

r-1

1

Ju

n-1

1

Se

p-1

1

De

c-1

1

Oc

cu

pa

nc

y

No

. of

Ro

om

s

Brisbane Tourism Region HMSA

Rooms and Occupancy - Total Stargraded

No Rooms Occupancy (%)

Source: ABS/PRP Research

$80

$100

$120

$140

$160

$180

$200

De

c-0

6

Ma

r-0

7

Ju

n-0

7

Se

p-0

7

De

c-0

7

Ma

r-0

8

Ju

n-0

8

Se

p-0

8

De

c-0

8

Ma

r-0

9

Ju

n-0

9

Se

p-0

9

De

c-0

9

Ma

r-1

0

Ju

n-1

0

Se

p-1

0

De

c-1

0

Ma

r-1

1

Ju

n-1

1

Se

p-1

1

De

c-1

1

Av

era

ge

Ro

om

Ra

te

Brisbane Tourism Region HMSA

Average Room Rate - Total Stargraded

Source: ABS/PRP Research

13 Property Market Report—March 2012

Deloittes Access forecasts occupancy

rates in the Brisbane hotel motel and

serviced apartment market will be

weighed down by increased supply,

and are expected to ease by 1 per-

centage point over 2012.

After falling 1.3 percent over the 12

months to December 2010, Queen-

sland Hotel Motel and Serviced Apart-

ment market total stargraded aver-

age room rate rose by 2.3 percent in

the 12 months to December 2011 to sit

at $156.22. This is the highest level

seen over the December quarter, with

average room rates rising in all star-

graded room. Average room rates

increased by 17.5 percent in the 1

stargraded Hotel Motel and Serviced

Apartment market to reach $122.39.

The 1&2 Stargraded average room

rates also saw significant rises over the

12 months to December 2011, in-

creasing from $84.39 in December

2010 to $97.47 12 months later.

After seeing a fall in average room

rates in the Brisbane Tourism market

over the 12 months to December

2009, average room rates have in-

creased for the second consecutive

year, rising by 3.6 percent over the

last 12 month period, a top of a 10.2

percent increase over the 12 months

to December 2010. Average room

rates in the Brisbane Tourism Region

total stargraded Hotel Motel and Ser-

viced Apartment market, reached

$178.34 in the December 2011 quar-

ter.

Investment Despite the positive outlook in hotel

accommodation created by the re-

sources sector, limited Transactions

activity has occurred in the 3 months

to March 2012. West Australian Hotel-

ier Peter Prendiville has purchased the

Grand Mercure Apartment complex

on Palmer Street in Townsville for ap-

proximately $20 million. With 106 dual

rooms, the 4 & ½ Star complex was in

the hands of Owenlaw mortgage

Investments. After the takeover the

Grand Mercure has been officially

rebranded to the Grand Hotel, Towns-

ville. The property was formally man-

aged by Accor Asia Pacific. It has also

been reported that The Metro Prop-

erty Group is negotiating to purchase

the Couran Cove Resort on Strad-

Broke Island for nearly $20 million.

Couran Cove closed after being

placed into voluntary liquidation. The

resort offers 158 water front units, con-

ference facilities and function rooms.

The Prendiville Group purchased the

Grand Mercure apartment complex on

Palmer Street in Townsville for approxi-

mately $20 Million.

14 Property Market Report—March 2012

GOLD COAST

Supply Supply levels in the Gold Coast hotel

motel and serviced apartment market

have remained stagnant over the last

10 years rising by a mere 3.6 percent

since 2002. Over the 12 months to

December 2008 the number of rooms

in the Gold Coast Tourism Region

grew by approximately 400 rooms,

resulting in declining occupancy rates

over this period. The number of rooms

currently available in the Gold Coast

hotel motel and serviced apartment

market is approximately around

13,300 rooms, down by 2.3 percent

since the peak in 2008.

Demand The Gold Coast hotel motel and ser-

viced apartment market has histori-

cally seen occupancy rates sit above

70 percent, however, due to in-

creased supply levels ,saw occu-

pancy dip to 68.9 percent in the De-

cember quarter 2008. The December

2011 quarter saw occupancy rates in

the Gold Coast hotel motel and ser-

viced apartment market sit at 70.9

percent. Occupancy rates in this mar-

ket fell by 1.2 percentage points over

the last 12 months and by 3.8 percent-

age points since the peak of the mar-

ket in December 2007.

After two years of declining average

room rates between December 2009

and December 2010, average room

rates moved to positive territory in the

12 months to December 2011 rising by

2.0 percent. Average room rates in

the Gold Coast Hotel motel and ser-

viced apartment market reached

$155.04 in December 2011. Average

room rates have declined by 2.8 per-

cent over the December quarter

since peaking at$159.52 in December

2008.

50%

55%

60%

65%

70%

75%

80%

12500

12700

12900

13100

13300

13500

13700

13900

De

c-0

6

Ma

r-0

7

Ju

n-0

7

Se

p-0

7

De

c-0

7

Ma

r-0

8

Ju

n-0

8

Se

p-0

8

De

c-0

8

Ma

r-0

9

Ju

n-0

9

Se

p-0

9

De

c-0

9

Ma

r-1

0

Ju

n-1

0

Se

p-1

0

De

c-1

0

Ma

r-1

1

Ju

n-1

1

Se

p-1

1

De

c-1

1

Oc

cu

pa

nc

y

No

. of

Ro

om

s

Gold Coast Tourism Region HMSA

Rooms and Occupancy

No Rooms Occupancy (%)Source: ABS/PRP Research

$80

$90

$100

$110

$120

$130

$140

$150

$160

$170

De

c-0

6

Ma

r-0

7

Ju

n-0

7

Se

p-0

7

De

c-0

7

Ma

r-0

8

Ju

n-0

8

Se

p-0

8

De

c-0

8

Ma

r-0

9

Ju

n-0

9

Se

p-0

9

De

c-0

9

Ma

r-1

0

Ju

n-1

0

Se

p-1

0

De

c-1

0

Ma

r-1

1

Ju

n-1

1

Se

p-1

1

De

c-1

1

Av

era

ge

Ro

om

Ra

te

Gold Coast HMSA

Average Room Rate - Total Stargraded

Source: ABS/PRP Research

15 Property Market Report—March 2012

TROPICAL FAR NORTH

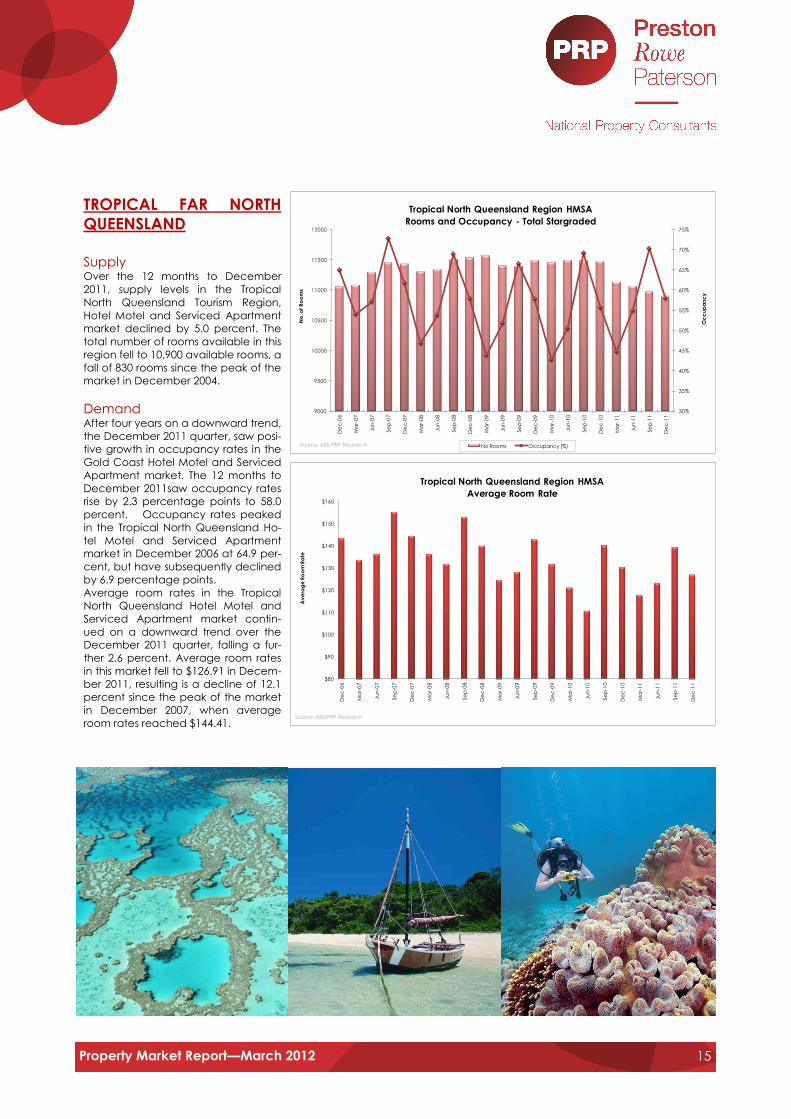

QUEENSLAND

Supply Over the 12 months to December

2011, supply levels in the Tropical

North Queensland Tourism Region,

Hotel Motel and Serviced Apartment

market declined by 5.0 percent. The

total number of rooms available in this

region fell to 10,900 available rooms, a

fall of 830 rooms since the peak of the

market in December 2004.

Demand

After four years on a downward trend,

the December 2011 quarter, saw posi-

tive growth in occupancy rates in the

Gold Coast Hotel Motel and Serviced

Apartment market. The 12 months to

December 2011saw occupancy rates

rise by 2.3 percentage points to 58.0

percent. Occupancy rates peaked

in the Tropical North Queensland Ho-

tel Motel and Serviced Apartment

market in December 2006 at 64.9 per-

cent, but have subsequently declined

by 6.9 percentage points.

Average room rates in the Tropical

North Queensland Hotel Motel and

Serviced Apartment market contin-

ued on a downward trend over the

December 2011 quarter, falling a fur-

ther 2.6 percent. Average room rates

in this market fell to $126.91 in Decem-

ber 2011, resulting is a decline of 12.1

percent since the peak of the market

in December 2007, when average

room rates reached $144.41.

$80

$90

$100

$110

$120

$130

$140

$150

$160

De

c-0

6

Ma

r-0

7

Ju

n-0

7

Se

p-0

7

De

c-0

7

Ma

r-0

8

Ju

n-0

8

Se

p-0

8

De

c-0

8

Ma

r-0

9

Ju

n-0

9

Se

p-0

9

De

c-0

9

Ma

r-1

0

Ju

n-1

0

Se

p-1

0

De

c-1

0

Ma

r-1

1

Ju

n-1

1

Se

p-1

1

De

c-1

1

Av

era

ge

Ro

om

Ra

te

Tropical North Queensland Region HMSA

Average Room Rate

Source: ABS/PRP Research

30%

35%

40%

45%

50%

55%

60%

65%

70%

75%

9000

9500

10000

10500

11000

11500

12000

De

c-0

6

Ma

r-0

7

Ju

n-0

7

Se

p-0

7

De

c-0

7

Ma

r-0

8

Ju

n-0

8

Se

p-0

8

De

c-0

8

Ma

r-0

9

Ju

n-0

9

Se

p-0

9

De

c-0

9

Ma

r-1

0

Ju

n-1

0

Se

p-1

0

De

c-1

0

Ma

r-1

1

Ju

n-1

1

Se

p-1

1

De

c-1

1

Oc

cu

pa

nc

y

No

. of

Ro

om

s

Tropical North Queensland Region HMSA

Rooms and Occupancy - Total Stargraded

No Rooms Occupancy (%)Source: ABS/PRP Research

16 Property Market Report—March 2012

Our Clients Preston Rowe Paterson acts for an array of clients with all types

of real estate, plant, machinery and equipment interests such

as:

Accountants

Banks, finance companies and lending

institutions

Commercial and Residential non bank lenders

Co-operatives

Developers

Finance and mortgage brokers

Hotel owners and operators

Institutional investors

Insurance brokers and companies

Investment advisors

Lessors and lessees

Listed and private companies corporations

Listed Property Trusts

Local, State and Federal Government Departments

and Agencies

Mining companies

Mortgage trusts

Overseas clients

Private investors

Property Syndication Managers

Rural landholders

Solicitors and barristers

Stock brokers

Trustee and Custodial companies

For more information, please visit our website

www.prpaustralia.com.au

Our Research At Preston Rowe Paterson, we pride ourselves on the research

which we prepare in the market sectors within which we operate.

These include Commercial, Retail, Industrial, Hotel & Leisure and

Residential.

Our Corporate Property Services

Real Estate Investment Valuation

Real Estate Development Valuation

Property Consultancy and Advisory

Transaction Advisory

Property and Asset Management

Listed Fund, Property Trust, Super Fund

and Syndicate Advisors

Plant & Machinery Valuation

General and Insurance Valuation

Economic and Property Market Research

Types of Real Property We regularly provide valuation, property and asset management,

consultancy and leasing services for all types of Real Estate

including:

CBD and Metropolitan commercial office buildings

Retail shopping centres and shops

Industrial, office/warehouses and factories

Business parks

Hotels (accommodation) and resorts

Hotels (pubs), motels and caravan parks

Residential development projects

Residential dwellings (individual houses and apartments/units)

Rural properties

Special purpose properties such as: nursing homes; private hospitals, service stations, oil terminals and refineries, theatre complexes; etc.

Extractive industries, land fills and resource based enterprises

Types of Plant & Machinery We regularly undertake valuations of all forms of plant, machinery,

furniture, fittings and equipment including:

Mining & earth moving equipment/road plant

Office fit outs, equipment & furniture

Agricultural machinery & equipment

Heavy, light commercial & passenger vehicles

Industrial manufacturing equipment

Wineries and processing plants

Special purpose plant, machinery & equipment

Hotel furniture, fittings & equipment

Preston Rowe Paterson Australasia Pty Ltd ACN: 060 005 807

The information provided within this research report should be regarded solely as a general guide. We believe that the information herein

is accurate however no warranty of accuracy or reliability is given in relation to any advice or information contained in this publication

and nor any responsibility for any loss or damage whatsoever arising in any way for any representation, act or omission, whether expressed

or implied (including responsibility to any person or entity by reason of negligence) is accepted by Preston Rowe Paterson Australasia Pty

Ltd or any of its associated offices or any officer, agent or employee of Preston Rowe Paterson Australasia Pty Ltd.

17 Property Market Report—March 2012

Capital City Offices

Sydney (Head Office) Level 11, 80 Clarence Street

Sydney NSW 2000

PO BOX 4120, Sydney NSW 2001

P: 02 9292 7400

F: 02 9292 7403

Directors

Greg Preston

M: 0408 622 400

Greg Rowe

M: 0411 191 179

Associate Directors

Asset Management

Ben Greenwood

M: 0448 656 103

Commercial Valuation/Advisory

Neal Smith

M: 0448 656 647

Rachel Cooper

M: 0448 757 134

Residential Valuation

Ben Toole

M: 0448 886 335

Asset, Plant & Machinery Valuation

Greg Mason

M: 0448 757 046

Manager - Research & Marketing

Tammy Smith

M: 0416 004 964

Affiliate offices in Canberra, Perth,

Hobart, Darwin and other regional

areas.

Locally owned, Globally associated

Capital City Offices

Melbourne Suite 6.02, 488 Bourke Street

Melbourne VIC 3000

P: 03 9602 0517

F: 03 9602 1337

Directors

Neal Ellis

M: 0417 053 116

Damian Kininmonth

M: 0417 059 836

Adelaide Suite 4, 2A Daws Road

Adelaide SA 5043

P: 08 8277 0500

F: 08 8277 0533

Director

Rob Simmons

M: 0418 857 555

Brisbane Suite 16, 105 Vulture Street

West End QLD 4101

GPO BOX 1234, Brisbane QLD 4001

P: 07 3846 2822

F: 07 3846 2833

Director

Troy Chaplin

M: 0419 029 045

Regional Offices

Albury Wodonga

Daniel Hogg

M: 0408 585 119

Ballarat

Darren Evans

M: 0417 380 324

Cairns

Robert Cowell

M: 0410 693 799

E: [email protected] Richard Cowell

M: 0408 987 554

Central Coast/Gosford

Robert Dupont

M: 0418 681 874

E: [email protected] David Rich

M: 0413 052 166

E: [email protected] Joshua Smith

M: 0412 099 908

Geelong

Gareth Kent

M: 0413 407 820

E: [email protected] Stuart Mcdonald

M: 0405 266 783

Gold Coast

Troy Chaplin

M: 0419 029 045

Gippsland

Tim Barlow

M: 0400 724 444

E: [email protected] Alexandra Ellis

M: 0407 724 444

Mornington

Neal Ellis

M: 0417 053 116

E: [email protected] Damian Kininmonth

M: 0417 059 836

Newcastle

Robert Dupont

M: 0418 681 874

E: [email protected] David Rich

M: 0413 052 166

E: [email protected] Joshua Smith

M: 0412 099 908

Wagga Wagga

Michael Redfern

M: 0428 235 588