Embed Size (px)

Citation preview

Malaysia

Property Market Index

Q3 2021

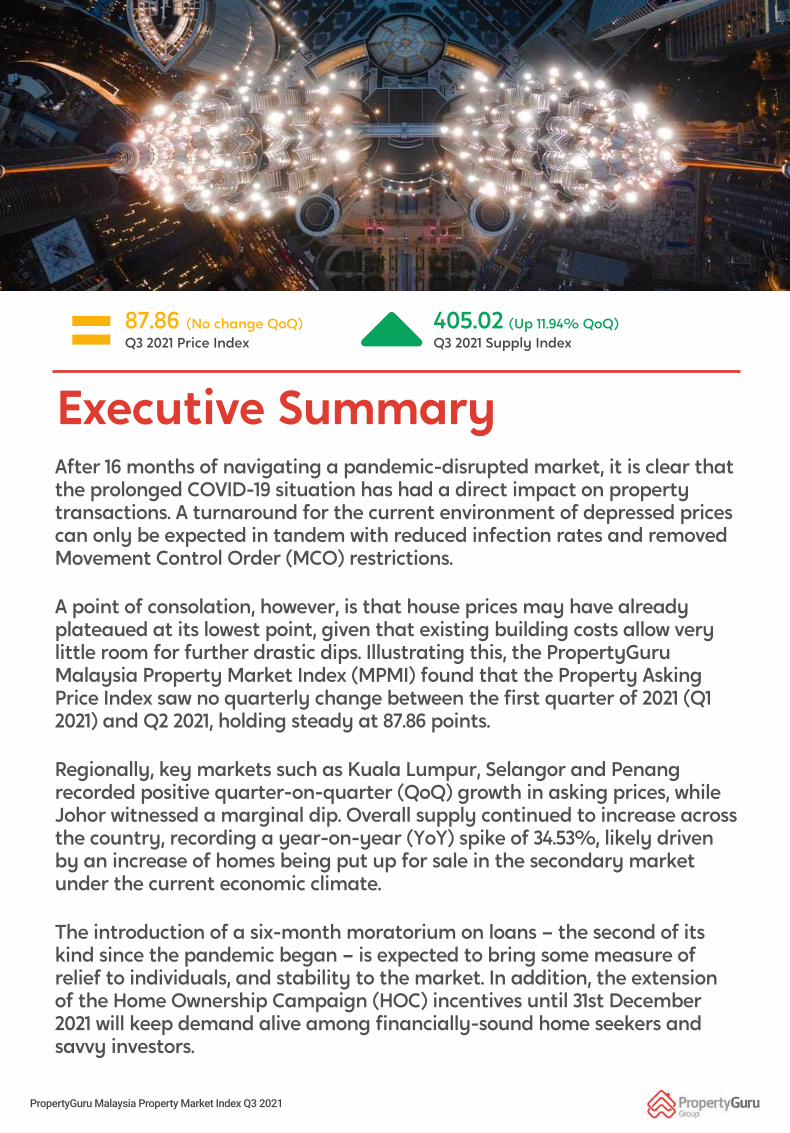

After 16 months of navigating a pandemic-disrupted market, it is clear that

the prolonged COVID-19 situation has had a direct impact on property

transactions. A turnaround for the current environment of depressed prices

can only be expected in tandem with reduced infection rates and removed

Movement Control Order (MCO) restrictions.

A point of consolation, however, is that house prices may have already

plateaued at its lowest point, given that existing building costs allow very

little room for further drastic dips. Illustrating this, the PropertyGuru

Malaysia Property Market Index (MPMI) found that the Property Asking

Price Index saw no quarterly change between the first quarter of 2021 (Q1

2021) and Q2 2021, holding steady at 87.86 points.

Regionally, key markets such as Kuala Lumpur, Selangor and Penang

recorded positive quarter-on-quarter (QoQ) growth in asking prices, while

Johor witnessed a marginal dip. Overall supply continued to increase across

the country, recording a year-on-year (YoY) spike of 34.53%, likely driven

by an increase of homes being put up for sale in the secondary market

under the current economic climate.

The introduction of a six-month moratorium on loans – the second of its

kind since the pandemic began – is expected to bring some measure of

relief to individuals, and stability to the market. In addition, the extension

of the Home Ownership Campaign (HOC) incentives until 31st December

2021 will keep demand alive among financially-sound home seekers and

savvy investors.

Executive Summary

87.86 (No change QoQ)

Q3 2021 Price Index

405.02 (Up 11.94% QoQ)

Q3 2021 Supply Index=

PropertyGuru Malaysia Property Market Index Q3 2021

Content

1 Get The Guru View

2 Price Index Overview

3 Supply Index Overview

4 Region Analysis

5

6

What does this mean

for buyers?

7

What to look out for in

the quarter?

About This Report &

Methodology

PropertyGuru Malaysia Property Market Index Q3 2021

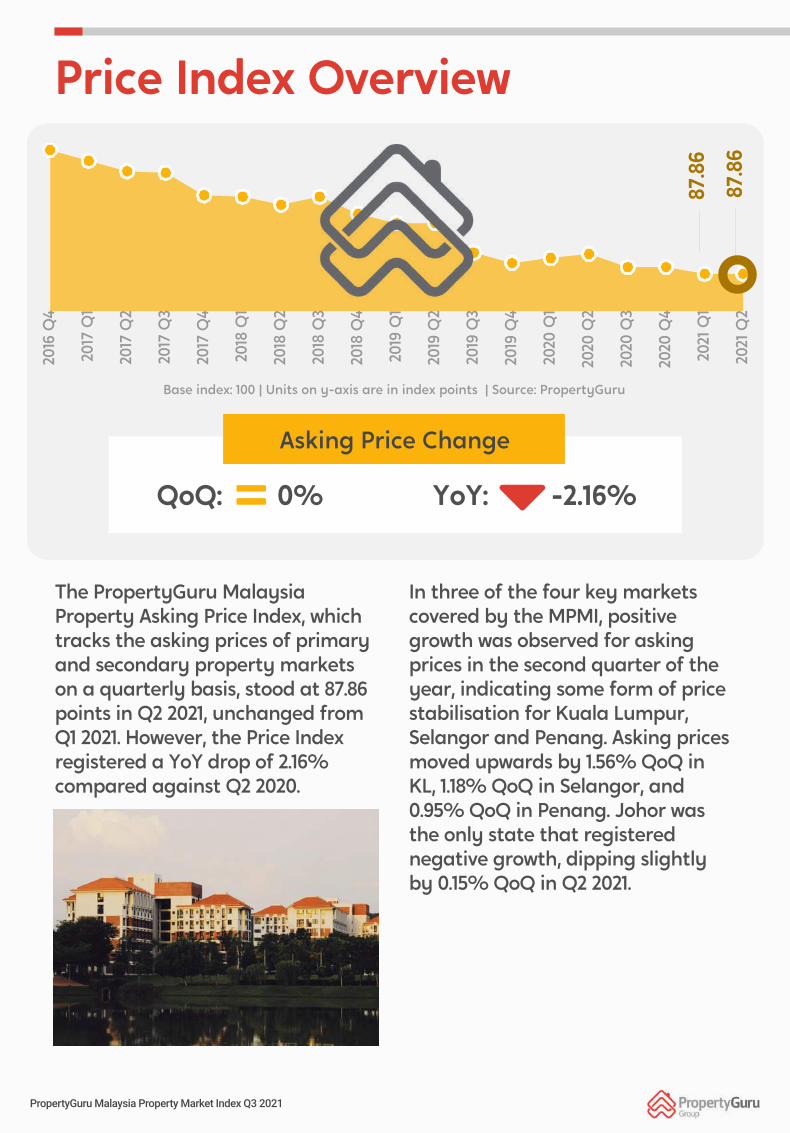

Prices stabilising at current level

The PropertyGuru Malaysia Property Asking Price

Index saw no quarterly change between Q1 2021

and Q2 2021, holding at 87.86 points, indicating

that prices are stabilising at the current low.

Most markets recorded price growth

Key markets such as Kuala Lumpur, Selangor,

and Penang recorded positive QoQ growth of

between 0.95% to 1.56% in asking prices, while

Johor witnessed a marginal dip of 0.15%.

Supply still on the rise

The PropertyGuru Malaysia Property Supply

Index continued to grow strongly with a YoY

spike of 34.53%, which is likely to be driven

by an increase of homes being put up for

sale in the secondary market.

Delayed recovery expected

In light of the new wave of COVID-19 infections

and the reinstatement of strict movement

restrictions, market recovery is likely to be

pushed forward to next year when

improvements are expected on both the COVID-

19 and economic front.

Plenty of buying opportunities

Cash-rich buyers and savvy investors will be

keen to capitalise on the current climate of

low prices and low interest rates to swoop in

on prime property opportunities.

20

16 Q

4

20

17 Q

1

20

17 Q

2

20

17 Q

3

20

17 Q

4

20

18 Q

1

20

18 Q

2

20

18 Q

3

20

18 Q

4

20

19 Q

1

20

19 Q

2

20

19 Q

3

20

19 Q

4

2020

Q1

2020

Q2

2020

Q3

2020

Q4

2021

Q1

2021

Q2

Price Index Overview

87.8

6

87.8

6

Base index: 100 | Units on y-axis are in index points | Source: PropertyGuru

In three of the four key markets

covered by the MPMI, positive

growth was observed for asking

prices in the second quarter of the

year, indicating some form of price

stabilisation for Kuala Lumpur,

Selangor and Penang. Asking prices

moved upwards by 1.56% QoQ in

KL, 1.18% QoQ in Selangor, and

0.95% QoQ in Penang. Johor was

the only state that registered

negative growth, dipping slightly

by 0.15% QoQ in Q2 2021.

The PropertyGuru Malaysia

Property Asking Price Index, which

tracks the asking prices of primary

and secondary property markets

on a quarterly basis, stood at 87.86

points in Q2 2021, unchanged from

Q1 2021. However, the Price Index

registered a YoY drop of 2.16%

compared against Q2 2020.

YoY: -2.16%QoQ: 0%

Asking Price Change

=

PropertyGuru Malaysia Property Market Index Q3 2021

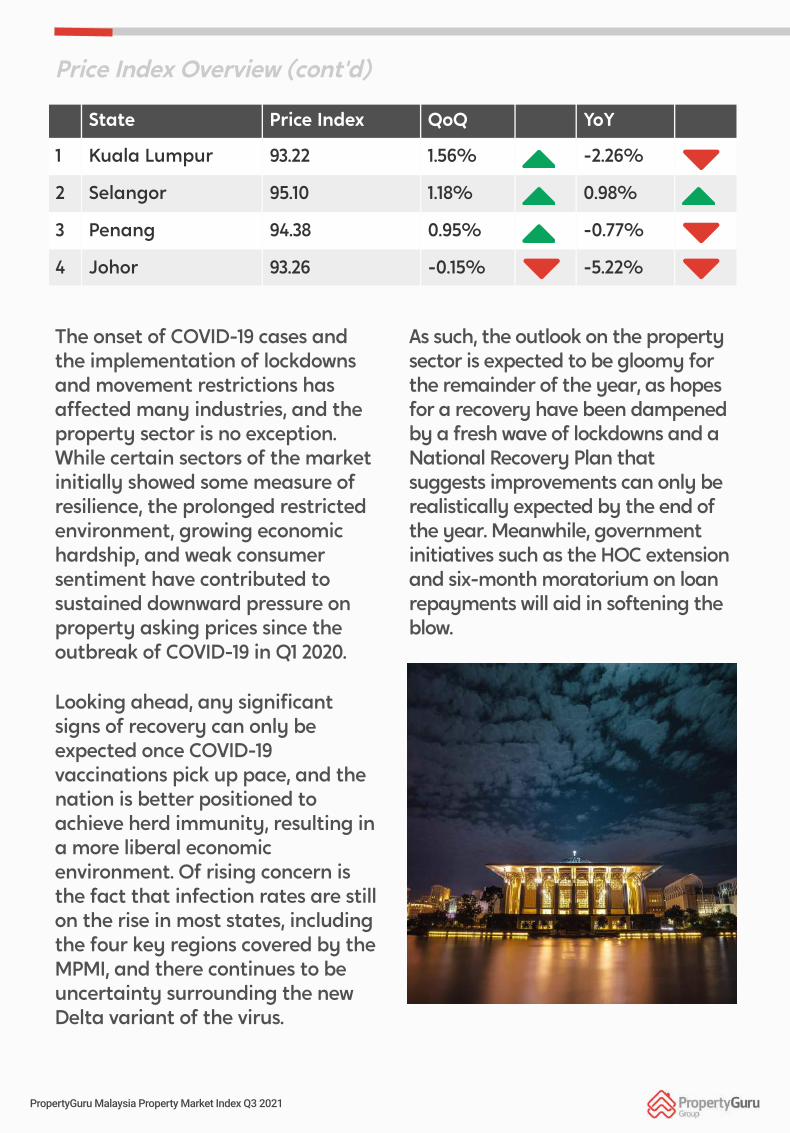

The onset of COVID-19 cases and

the implementation of lockdowns

and movement restrictions has

affected many industries, and the

property sector is no exception.

While certain sectors of the market

initially showed some measure of

resilience, the prolonged restricted

environment, growing economic

hardship, and weak consumer

sentiment have contributed to

sustained downward pressure on

property asking prices since the

outbreak of COVID-19 in Q1 2020.

Looking ahead, any significant

signs of recovery can only be

expected once COVID-19

vaccinations pick up pace, and the

nation is better positioned to

achieve herd immunity, resulting in

a more liberal economic

environment. Of rising concern is

the fact that infection rates are still

on the rise in most states, including

the four key regions covered by the

MPMI, and there continues to be

uncertainty surrounding the new

Delta variant of the virus.

As such, the outlook on the property

sector is expected to be gloomy for

the remainder of the year, as hopes

for a recovery have been dampened

by a fresh wave of lockdowns and a

National Recovery Plan that

suggests improvements can only be

realistically expected by the end of

the year. Meanwhile, government

initiatives such as the HOC extension

and six-month moratorium on loan

repayments will aid in softening the

blow.

Price Index Overview (cont'd)

1 Kuala Lumpur 93.22 1.56% -2.26%

2 Selangor 95.10 1.18% 0.98%

3 Penang 94.38 0.95% -0.77%

4 Johor 93.26 -0.15% -5.22%

State Price Index QoQ YoY

PropertyGuru Malaysia Property Market Index Q3 2021

20

16 Q

4

20

17 Q

1

20

17 Q

2

20

17 Q

3

20

17 Q

4

20

18 Q

1

20

18 Q

2

20

18 Q

3

20

18 Q

4

20

19 Q

1

20

19 Q

2

20

19 Q

3

20

19 Q

4

2020

Q1

2020

Q2

2020

Q3

2020

Q4

2021

Q1

2021

Q2

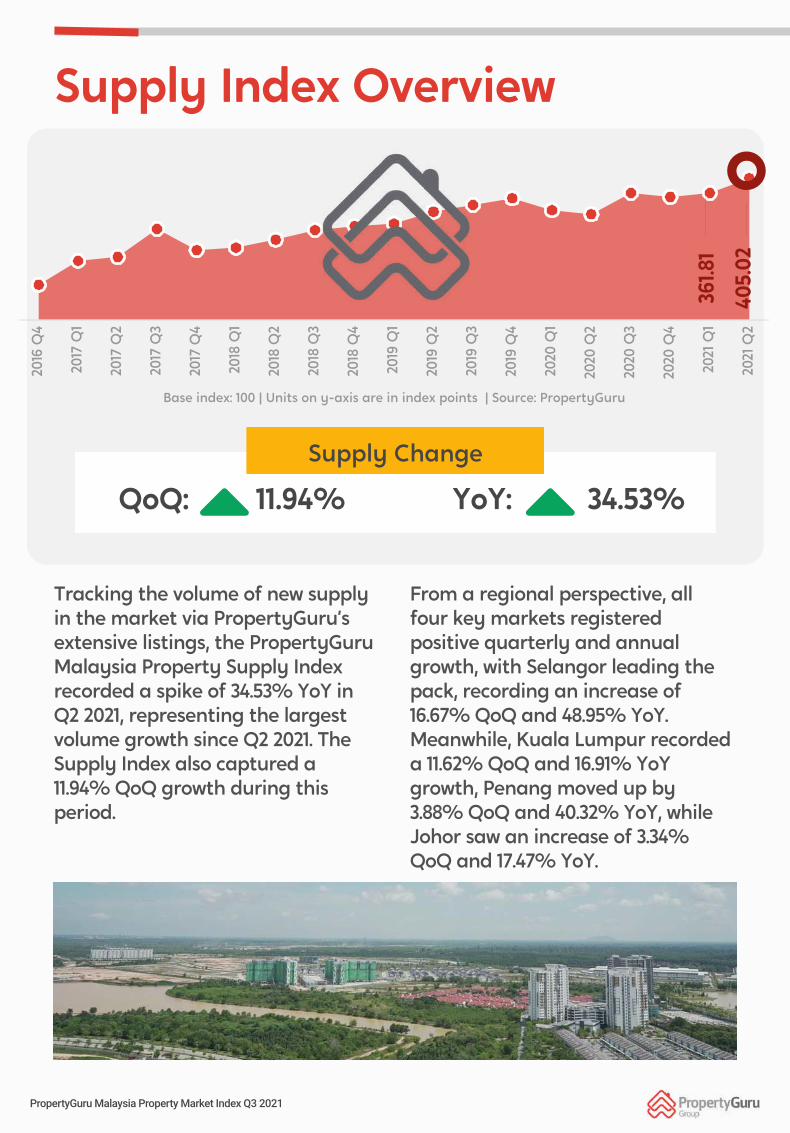

Supply Index Overview

361.81

Base index: 100 | Units on y-axis are in index points | Source: PropertyGuru

40

5.0

2

Tracking the volume of new supply

in the market via PropertyGuru’s

extensive listings, the PropertyGuru

Malaysia Property Supply Index

recorded a spike of 34.53% YoY in

Q2 2021, representing the largest

volume growth since Q2 2021. The

Supply Index also captured a

11.94% QoQ growth during this

period.

YoY: 34.53%QoQ: 11.94%

Supply Change

From a regional perspective, all

four key markets registered

positive quarterly and annual

growth, with Selangor leading the

pack, recording an increase of

16.67% QoQ and 48.95% YoY.

Meanwhile, Kuala Lumpur recorded

a 11.62% QoQ and 16.91% YoY

growth, Penang moved up by

3.88% QoQ and 40.32% YoY, while

Johor saw an increase of 3.34%

QoQ and 17.47% YoY.

PropertyGuru Malaysia Property Market Index Q3 2021

While the numbers suggest a robust supply growth, it is also

important to note that much of the incoming supply is also due to

more homeowners putting their properties on the market to

generate better cashflow in this harsh economic climate. In this

scenario, an influx of properties for sale could further adversely

impact asking prices in the secondary market, going forward.

The recent implementation of a total lockdown in June 2021 under

the Full Movement Control Order (FMCO), and the potential of

extended restrictions, will likely affect the overall supply in the

coming quarter. At the start of the year, the number of newly

launched residential units had already dropped significantly from

14,865 units in Q4 2020 to 5,919 units in Q1 2021, according to the

National Property Information Centre (NAPIC).

Despite this, the country is still coping with a significant overhang of

unsold, completed property units in the market, which is a situation

that is not expected to be resolved any time in the near future. The

latest data from NAPIC indicates that there are currently 27,468

units of residential overhang in Q1 2021, not including SoHos and

serviced apartments that fall under the commercial classification.

Coupled with the 25,439 overhang units of SoHos and serviced

apartments, the overhang totaled at 52,907 units as at Q1 2021, one

of the highest levels since 2016.

Supply Index Overview (cont'd)

PropertyGuru Malaysia Property Market Index Q3 2021

According to Bank Negara Malaysia, the six-month

moratorium period is applicable to all individuals,

micro-enterprises and small-and-medium

enterprises (SMEs) from 7th July this year, under

the National People’s Well-Being and Economic

Recovery Package (PEMULIH). During this period,

bank customers do not need to make instalment

payments for loans, and there will be no

compounded interest and penalty charges during

this time. Borrowers will need to contact their

respective banks to opt-in for this plan, however,

they will not be required to provide supporting

documentation.

Six-Month Moratorium

Explained

PropertyGuru Malaysia Property Market Index Q3 2021

Regional Analysis

Kuala Lumpur: Back in positive territory

QoQ: 1.56% YoY: -2.26%

20

16 Q

4

20

17 Q

1

20

17 Q

2

20

17 Q

3

20

17 Q

4

20

18 Q

1

20

18 Q

2

20

18 Q

3

20

18 Q

4

20

19 Q

1

20

19 Q

2

20

19 Q

3

20

19 Q

4

2020

Q1

2020

Q2

2020

Q3

2020

Q4

2021

Q1

2021

Q2

PRICE INDEX Base index: 100 | Units on y-axis are in index points | Source: PropertyGuru

After witnessing price contractions in

the last four consecutive quarters, the

median asking price in Kuala Lumpur

rebounded with a 1.56% QoQ gain in

Q2 2021. This would indicate that

asking prices in the capital district

could stabilise at this current point,

before moving in tandem with the

situation over the next few months.

Overall, however, asking prices are

down by 2.26% YoY, continuing a

downtrend which began in Q4 2017,

following an overheated market

period.

There were also gains on the supply

front, which grew by 11.62% QoQ and

16.91% YoY in Q2 2021. This is

significantly higher than the 0.52%

QoQ and 2.03% YoY growth captured

in the previous quarter.

Areas within the KL district that are

currently witnessing increased

popularity and rising median asking

prices on a QoQ-basis include Jalan

Ampang in KL City (+9.55%), Kenny

Hills in Bukit Tunku (+6.60%) and

Happy Garden in Kuchai Lama

(+5.50%).

1Jalan Ampang (KL

City)9.55%

2Kenny Hills (Bukit

Tunku)6.60%

3Happy Garden

(Kuchai Lama)5.50%

NoKuala Lumpur

Area

QoQ

Change

PropertyGuru Malaysia Property Market Index Q3 2021

Region Analysis (cont'd)

PropertyGuru Malaysia Property Market Index Q3 2021

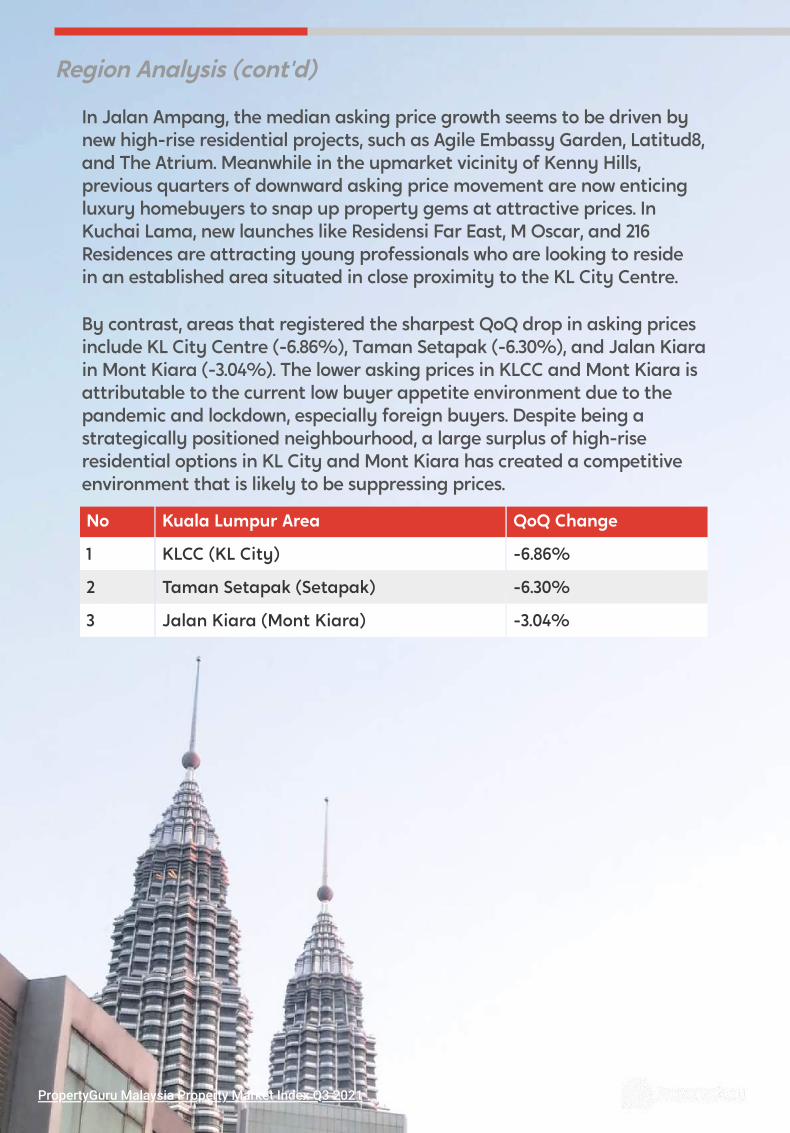

In Jalan Ampang, the median asking price growth seems to be driven by

new high-rise residential projects, such as Agile Embassy Garden, Latitud8,

and The Atrium. Meanwhile in the upmarket vicinity of Kenny Hills,

previous quarters of downward asking price movement are now enticing

luxury homebuyers to snap up property gems at attractive prices. In

Kuchai Lama, new launches like Residensi Far East, M Oscar, and 216

Residences are attracting young professionals who are looking to reside

in an established area situated in close proximity to the KL City Centre.

By contrast, areas that registered the sharpest QoQ drop in asking prices

include KL City Centre (-6.86%), Taman Setapak (-6.30%), and Jalan Kiara

in Mont Kiara (-3.04%). The lower asking prices in KLCC and Mont Kiara is

attributable to the current low buyer appetite environment due to the

pandemic and lockdown, especially foreign buyers. Despite being a

strategically positioned neighbourhood, a large surplus of high-rise

residential options in KL City and Mont Kiara has created a competitive

environment that is likely to be suppressing prices.

1 KLCC (KL City) -6.86%

2 Taman Setapak (Setapak) -6.30%

3 Jalan Kiara (Mont Kiara) -3.04%

No Kuala Lumpur Area QoQ Change

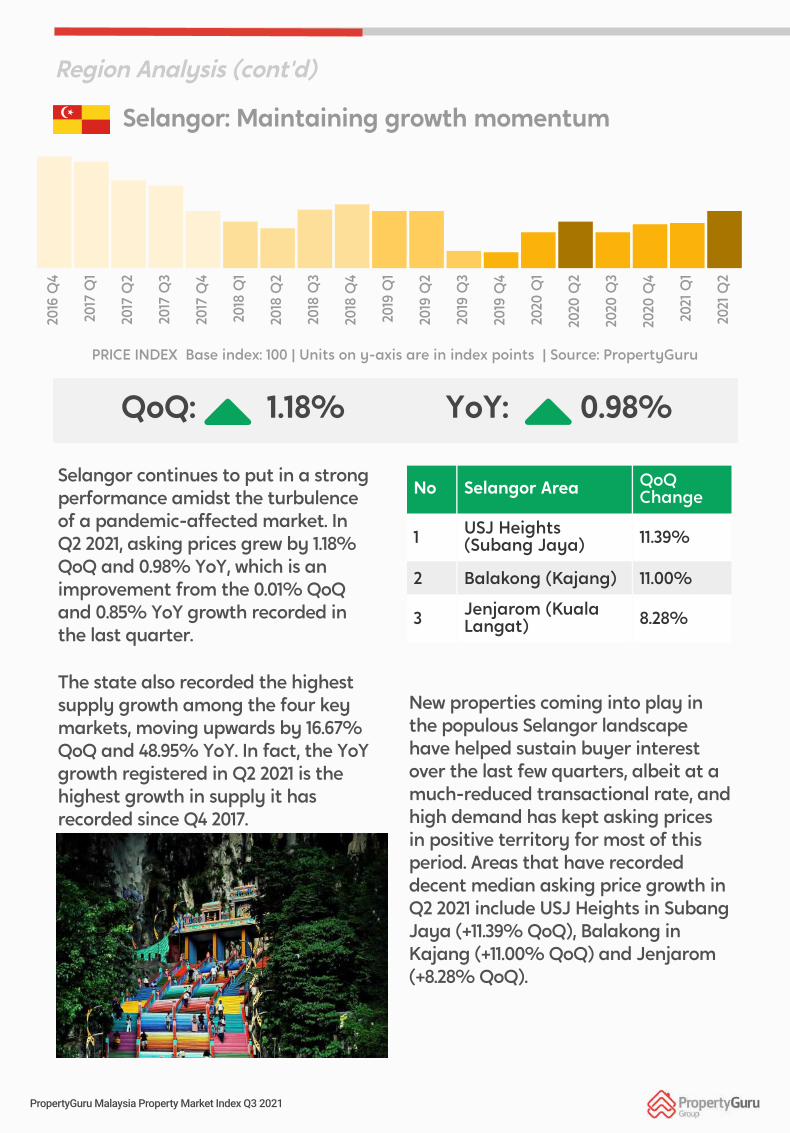

Selangor: Maintaining growth momentum

20

16 Q

4

20

17 Q

1

20

17 Q

2

20

17 Q

3

20

17 Q

4

20

18 Q

1

20

18 Q

2

20

18 Q

3

20

18 Q

4

20

19 Q

1

20

19 Q

2

20

19 Q

3

20

19 Q

4

2020

Q1

2020

Q2

2020

Q3

2020

Q4

2021

Q1

2021

Q2

QoQ: 1.18% YoY: 0.98%

Region Analysis (cont'd)

PRICE INDEX Base index: 100 | Units on y-axis are in index points | Source: PropertyGuru

Selangor continues to put in a strong

performance amidst the turbulence

of a pandemic-affected market. In

Q2 2021, asking prices grew by 1.18%

QoQ and 0.98% YoY, which is an

improvement from the 0.01% QoQ

and 0.85% YoY growth recorded in

the last quarter.

The state also recorded the highest

supply growth among the four key

markets, moving upwards by 16.67%

QoQ and 48.95% YoY. In fact, the YoY

growth registered in Q2 2021 is the

highest growth in supply it has

recorded since Q4 2017.

New properties coming into play in

the populous Selangor landscape

have helped sustain buyer interest

over the last few quarters, albeit at a

much-reduced transactional rate, and

high demand has kept asking prices

in positive territory for most of this

period. Areas that have recorded

decent median asking price growth in

Q2 2021 include USJ Heights in Subang

Jaya (+11.39% QoQ), Balakong in

Kajang (+11.00% QoQ) and Jenjarom

(+8.28% QoQ).

1USJ Heights

(Subang Jaya)11.39%

2 Balakong (Kajang) 11.00%

3Jenjarom (Kuala

Langat)8.28%

No Selangor AreaQoQ

Change

PropertyGuru Malaysia Property Market Index Q3 2021

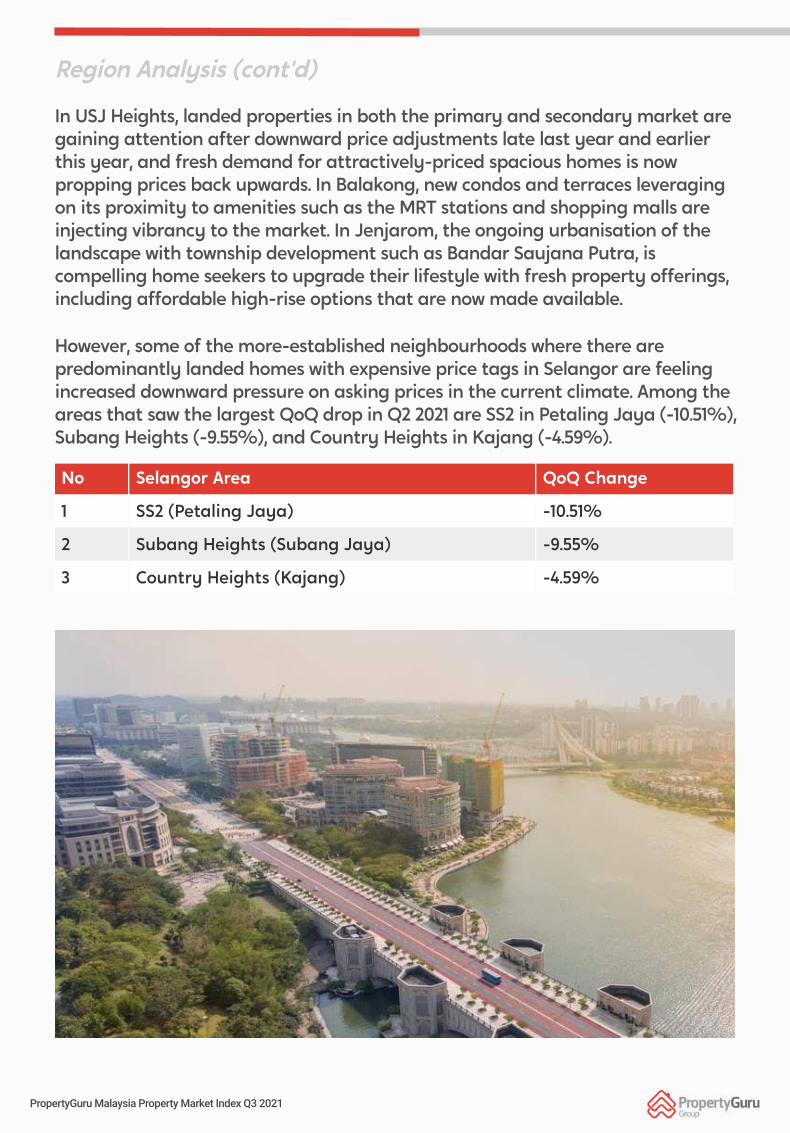

In USJ Heights, landed properties in both the primary and secondary market are

gaining attention after downward price adjustments late last year and earlier

this year, and fresh demand for attractively-priced spacious homes is now

propping prices back upwards. In Balakong, new condos and terraces leveraging

on its proximity to amenities such as the MRT stations and shopping malls are

injecting vibrancy to the market. In Jenjarom, the ongoing urbanisation of the

landscape with township development such as Bandar Saujana Putra, is

compelling home seekers to upgrade their lifestyle with fresh property offerings,

including affordable high-rise options that are now made available.

However, some of the more-established neighbourhoods where there are

predominantly landed homes with expensive price tags in Selangor are feeling

increased downward pressure on asking prices in the current climate. Among the

areas that saw the largest QoQ drop in Q2 2021 are SS2 in Petaling Jaya (-10.51%),

Subang Heights (-9.55%), and Country Heights in Kajang (-4.59%).

Region Analysis (cont'd)

1 SS2 (Petaling Jaya) -10.51%

2 Subang Heights (Subang Jaya) -9.55%

3 Country Heights (Kajang) -4.59%

No Selangor Area QoQ Change

PropertyGuru Malaysia Property Market Index Q3 2021

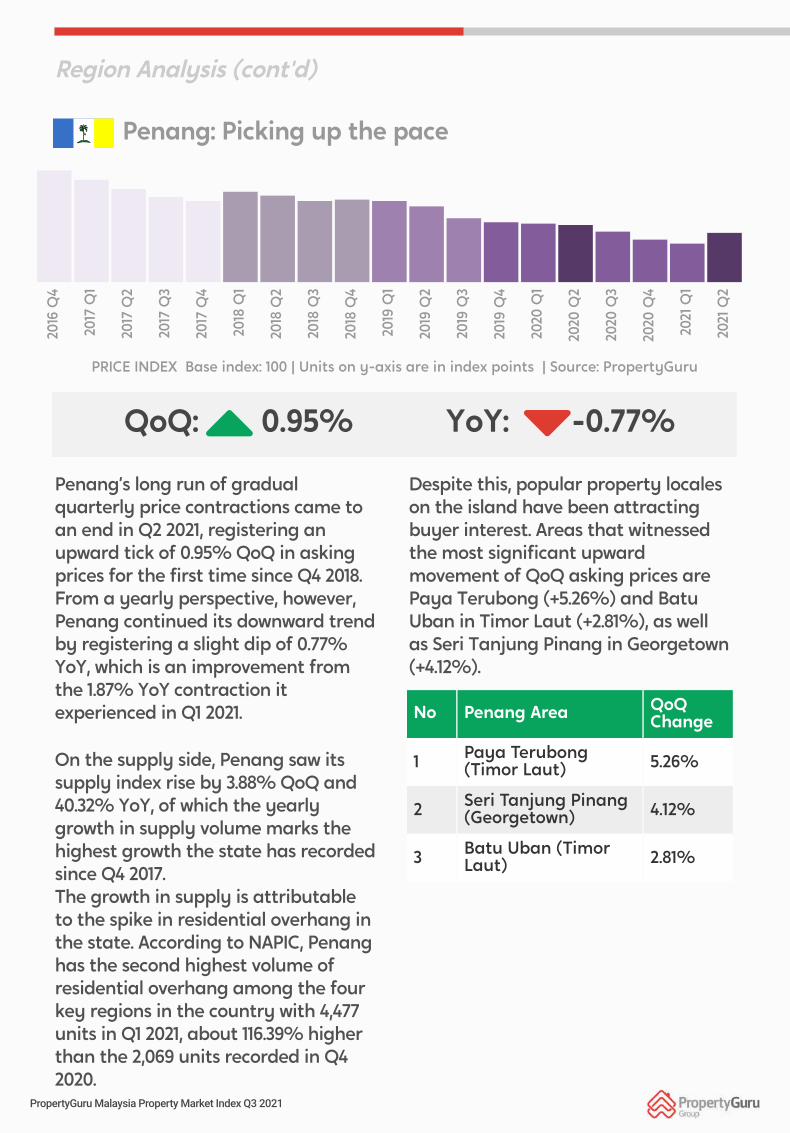

Penang: Picking up the pace

QoQ: 0.95% YoY: -0.77%

20

16 Q

4

20

17 Q

1

20

17 Q

2

20

17 Q

3

20

17 Q

4

20

18 Q

1

20

18 Q

2

20

18 Q

3

20

18 Q

4

20

19 Q

1

20

19 Q

2

20

19 Q

3

20

19 Q

4

2020

Q1

2020

Q2

2020

Q3

2020

Q4

2021

Q1

2021

Q2

Penang’s long run of gradual

quarterly price contractions came to

an end in Q2 2021, registering an

upward tick of 0.95% QoQ in asking

prices for the first time since Q4 2018.

From a yearly perspective, however,

Penang continued its downward trend

by registering a slight dip of 0.77%

YoY, which is an improvement from

the 1.87% YoY contraction it

experienced in Q1 2021.

On the supply side, Penang saw its

supply index rise by 3.88% QoQ and

40.32% YoY, of which the yearly

growth in supply volume marks the

highest growth the state has recorded

since Q4 2017.

The growth in supply is attributable

to the spike in residential overhang in

the state. According to NAPIC, Penang

has the second highest volume of

residential overhang among the four

key regions in the country with 4,477

units in Q1 2021, about 116.39% higher

than the 2,069 units recorded in Q4

2020.

Despite this, popular property locales

on the island have been attracting

buyer interest. Areas that witnessed

the most significant upward

movement of QoQ asking prices are

Paya Terubong (+5.26%) and Batu

Uban in Timor Laut (+2.81%), as well

as Seri Tanjung Pinang in Georgetown

(+4.12%).

PRICE INDEX Base index: 100 | Units on y-axis are in index points | Source: PropertyGuru

Region Analysis (cont'd)

1Paya Terubong

(Timor Laut)5.26%

2Seri Tanjung Pinang

(Georgetown)4.12%

3Batu Uban (Timor

Laut)2.81%

No Penang AreaQoQ

Change

PropertyGuru Malaysia Property Market Index Q3 2021

Prominent new developments such as Eco Terraces and

Penang World City are bringing a new vibrancy to the

Timor Laut district, luring buyers to areas close to the

Penang Bridge such as Batu Uban, and green vicinities

such as Paya Terubong close to the island’s hilly

centre. Meanwhile, large scale seafront developments

close to the main city centre of Georgetown have

always enjoyed attention, and in this low-price, low-

interest rate climate, buyers could be moving in to

snap up prime property in the vicinity.

Areas that saw the sharpest QoQ price drops in

Penang include Gelugor (-3.25%) and Bukit Dumbar

(-2.46%) on the island, as well as Nibong Tebal (-1.40%)

on the mainland.

Region Analysis (cont'd)

PropertyGuru Malaysia Property Market Index Q3 2021

1 Gelugor (Timor Laut) -3.25%

2 Bukit Dumbar (Timor Laut) -2.46%

3Nibong Tebal (Seberang Perai

Selatan)-1.40%

No Penang AreaQoQ

Change

Johor: Downward trend is easing off

QoQ: -0.15% YoY: -5.22%

20

16 Q

4

20

17 Q

1

20

17 Q

2

20

17 Q

3

20

17 Q

4

20

18 Q

1

20

18 Q

2

20

18 Q

3

20

18 Q

4

20

19 Q

1

20

19 Q

2

20

19 Q

3

20

19 Q

4

2020

Q1

2020

Q2

2020

Q3

2020

Q4

2021

Q1

2021

Q2

Johor experienced another quarter of

shrinking asking prices in Q2 2021,

registering a dip of 0.15% QoQ and

5.22% YoY. However, this is a much

lower rate of decline than the one

captured in Q1 2021, suggesting the

trend of price drops could be

gradually reducing pace.

Supply volume continued its upward

trajectory from the previous quarter,

this time up by 3.34% QoQ and 17.47%

YoY, which is the highest yearly

growth registered since Q2 2020. Still

plagued with the highest overhang

figures of 6,001 units in Q1 2021 in the

country, the southern state will have

to move forward with well-planned

caution in order to manage its

sizeable unsold property stock.

Relying heavily on cross-border

interest from neighbouring Singapore

for most of its upmarket properties,

Johor will be looking forward to the

removal of travel restrictions and the

reopening of borders to improve

future prospects.

PRICE INDEX Base index: 100 | Units on y-axis are in % | Source: PropertyGuru

Region Analysis (cont'd)

PropertyGuru Malaysia Property Market Index Q3 2021

Region Analysis (cont'd)

Landed homes seem to be the main

focus of buyers in Taman Pelangi,

which is a prime area that is close to

the Malaysia-Singapore border,

making it a good investment target

with future potential for value

appreciation. Taman Nusa Bestari is

also an emerging prime locale that

benefits from proximity to the Second

Link Expressway as well as established

amenities such as schools, shopping

malls and eateries. Meanwhile, Taman

Universiti is enjoying an enhancement

in its appeal as a property investment

destination due to its close proximity

to the Universiti Teknologi Malaysia,

where there is a steady housing

demand from a vibrant population of

students and academicians.

Experiencing the highest QoQ price

drops in Johor are areas such as

Taman Daya (-4.47%), Kempas

(-4.02%), and Johor Jaya (-3.81%), all

located in JB city. Interest may be

waning for centrally-located

properties within the city in JB,

especially when there is a surplus of

emerging alternatives in new areas

offering fresh lifestyle and

commercial opportunities.

Areas that have been performing

better than most in terms of QoQ

asking price movement include

Taman Pelangi in Johor Bahru

(+4.39%), Taman Nusa Bestari in

Iskandar Puteri (+3.52%), and Taman

Universiti in JB (+3.14%).

1Taman Daya

(Johor Bahru)-4.47%

2Kempas (Johor

Bahru)-4.02%

3Johor Jaya (Johor

Bahru)-3.81%

No Johor AreaQoQ

Change

1Taman Pelangi

(Johor Bahru)4.39%

2Taman Nusa Bestari

(Iskandar Puteri)3.52%

3Taman Universiti

(Johor Bahru)3.14%

No Johor AreaQoQ

Change

PropertyGuru Malaysia Property Market Index Q3 2021

While most individuals will opt to prioritise job

and financial security in the current climate,

savvy investors and financially secure home

seekers will see this as an opportune moment to

snap up prime property at below ordinary

market value to maximise gains in the future.

What it means for those

hoping to buy/sell in the

current market?

Country Manager

PropertyGuru Malaysia

Sheldon Fernandez

PropertyGuru Malaysia Property Market Index Q3 2021

What does

this mean

for buyers?

Macro-economic factors continue to

shape prospects for the Malaysian

property market and its potential

recovery, as typically, an upswing in

property activity usually follows on

the heels of an improved economic

outlook, as well as stronger consumer

confidence.

At the Monetary Policy Committee

meeting in July, Bank Negara

Malaysia has projected the headline

inflation to be averaged closer to the

lower bound, of a range between 2.5%

and 4.0% for the entirety of 2021,

citing the uncertainty over the path

of the pandemic as well as potential

risks of heightened financial market

volatility. Finance Minister Tengku

Datuk Seri Zafrul Tengku Abdul Aziz

has said in a media interview that the

government is in the midst of revising

its current GDP growth projection of

6% to 7.5%. Meanwhile, the World

Bank has lowered its GDP growth

projection for Malaysia from 6.0% to

4.5% this year in the wake of the new

wave of COVID-19 infections and the

reinstatement of strict movement

restrictions.

Despite a slow start, the national

vaccination programme is now

picking up pace, and consumer

sentiment will no doubt improve as we

move closer to achieving our herd

immunity target of 80% by late 2021.

Until then, however, the outlook for

the property market will be one of

lingering uncertainty and limited

visibility.

In this environment, the government’s

decision to implement a six-month

moratorium on bank loan

repayments will offer some relief to

consumers, while the extension of the

HOC and incentives offered under it

will keep property interest afloat for a

select few who still enjoy sound

financial footing. Cash-rich buyers

and savvy investors will be keen to

capitalise on the current climate of

low prices and low interest rates to

swoop in on prime property

opportunities.

PropertyGuru Malaysia Property Market Index Q3 2021

Expect asking prices to stabilise at the current low, before

gradually moving upwards again in tandem with the progress of

the national vaccination programme, as well as when lower new

infection rates are recorded.

A more competitive environment among developers who will be

vying for buyer’s attention with innovative packages and heavily

incentivised deals, in addition to those offered under HOC.

More residential supply could be making its way into the

secondary market, resulting from those who wish to cash out on

their property investments to alleviate current financial burdens.

Savvy investors and home seekers will see the current

environment as an opportune moment to snap up prime

property at attractive prices, while taking advantage of low

interest rates and financial incentives.

PropertyGuru Malaysia Property Market Index Q3 2021

What to look out for

in the quarter?

Buying a property is one of the most challenging decisions of our lives. It is also

likely to be the most expensive one. When committing to a home purchase, it is

important to make an informed choice, so that decisions can be made

confidently.

At PropertyGuru, we are passionate about helping homebuyers find and secure

the home they have always wanted. We created this report to help regular

Malaysians understand the movement of the property market better, so that

buyers can offer reasonable prices in line with market sentiments or try to time

their purchases better.

We look at the property market across Malaysia, in different locations, and

across different property types, to provide a comprehensive, insightful overview

of home pricing across the country.

As the largest property site in Malaysia, PropertyGuru processes a vast amount

of real estate data daily. As such, we are uniquely positioned to bring solid

insights about the market. We certainly hope these insights help Malaysians

make more confident property decisions.

Using a range of statistical techniques, the data from over 500,000 home choices

and over 12 million monthly visits on PropertyGuru.com.my are aggregated and

indexed, demonstrating the movement of supply side pricing.

The Malaysia Property Market Index (MPMI) shows seller sentiment and

indicates the price level that real estate developers and home owners feel that

they can fetch for their respective properties.

Short term increases in the Index demonstrate buoyancy of sentiment while in

the long term, the Index indicates which part of the property cycle the market is

currently going through.

The Index reflects the most recent (Q2 2021) price trend, relative to a reference

period of Q4 2016. This means that aggregated price levels are denominated as

100 at Q4 2016, and all subsequent quarters’ pricing are relative to that.

We complement the price with a view on supply volumes in the market through

the number of property listings on PropertyGuru.com.my. Our supply volumes

not only take into account residential resale supply, but also new launch supply

in the Malaysian property market.

Methodology

About this report

PropertyGuru Malaysia Property Market Index Q3 2021

The company is part of PropertyGuru Group,

Southeast Asia’s leading property

technology company.

For more information, please visit

www.PropertyGuru.com.my

www.linkedin.com/company/PropertyGuru-

Malaysia

About PropertyGuru

PropertyGuru is the leading property

website in Malaysia, with over 500,000 home

choices and over 12 million monthly visits.

Recognised by the Malaysia Book of Records

as the ‘Largest Property Website’ and voted

‘Top Brand in Online Property Search’ by

home seekers, PropertyGuru is the most

preferred destination for Malaysians to find

and own their dream home.

Contact

For media or press inquiries, or to understand more about the Malaysia

Property Market Index, contact [email protected]

Financial Disclaimer

This publication has been prepared for general guidance on matters of

interest only, and does not constitute professional advice. You should not act

upon the information contained in this publication without obtaining specific

professional advice. No representation or warranty (express or implied) is

given as to the accuracy or completeness of the information contained in this

publication, and, to the extent permitted by law, PropertyGuru Group does

not accept or assume any liability, responsibility or duty of care for any

consequences of you or anyone else acting, or refraining to act, in reliance on

the information contained in this publication or for any decision based on it.

PropertyGuru Group

REG PropertyGuruGroup.com | AsiaPropertyAwards.com

AsiaRealEstateSummit.com

MY PropertyGuru.com.my

SG PropertyGuru.com.sg | CommercialGuru.com.sg

ID Rumah.com | RumahDijual.com

TH DDproperty.com

VN Batdongsan.com.vn