Embed Size (px)

Citation preview

Production and Costs

In this chapter, In this chapter,

look for the answers to these questions:look for the answers to these questions:

• What is a production function? What is marginal product? How are they related?

• What are the various costs, and how are they related to each other and to output?

• How are costs different in the short run vs. the long run?

• What are “economies of scale”?

2

The Production Function

• Production function– Relationship between

• Quantity of inputs used to make a good• And the quantity of output of that good

– Gets flatter as production rises

• It can be represented by a table, equation, or graph.

• Input sometimes called factors of production to produce output.

THE COSTS OF PRODUCTION

4

0

500

1,000

1,500

2,000

2,500

3,000

0 1 2 3 4 5

No. of workers

Qu

anti

ty o

f ou

tpu

t

Example 1: Farmer Jack’s Production Function

30005

28004

24003

18002

10001

00

Q (bushels of wheat)

L(no. of

workers)

Marginal Product

• The marginal product of any input is the increase in output arising from an additional unit of that input, holding all other inputs constant.

• Notation: ∆ (delta) = “change in…”

Examples: ∆Q = change in output, ∆L = change in labor

• Marginal product of labor (MPL) = ∆Q∆L

THE COSTS OF PRODUCTION

6

30005

28004

24003

18002

10001

00

Q (bushels

of wheat)

L(no. of

workers)

EXAMPLE 1: Total & Marginal Product

200

400

600

800

1000

MPL

∆Q = 1000∆L = 1

∆Q = 800∆L = 1

∆Q = 600∆L = 1

∆Q = 400∆L = 1

∆Q = 200∆L = 1

THE COSTS OF PRODUCTION

7

MPL equals the slope of the production function.

Notice that MPL diminishes as L increases.

This explains why the production function gets flatter as L increases.

0

500

1,000

1,500

2,000

2,500

3,000

0 1 2 3 4 5

No. of workers

Qu

anti

ty o

f ou

tpu

t

EXAMPLE 1: MPL = Slope of Prod Function

30005200

28004400

24003600

18002800

100011000

00

MPLQ

(bushels of wheat)

L(no. of

workers)

Production and Costs

• Diminishing marginal product– Marginal product of an input declines as the

quantity of the input increases

• Total-cost curve– Relationship between quantity produced and total

costs

– Gets steeper as the amount produced rises

Total Revenue, Total Cost, Profit

• We assume that the firm’s goal is to maximize profit.

• Profit = Total revenue – Total cost

the amount a firm receives from the sale of its output

the market value of the inputs a firm uses in production

Costs: Explicit vs. Implicit

• Costs as opportunity costs– The cost of something is what you give up to get it

• Firm’s cost of production– Include all the opportunity costs of making its

output of goods and services

– Explicit costs

– Implicit costs

Costs: Explicit vs. Implicit

• Explicit costs– Input costs that require an outlay of money by the

firm

• Implicit costs– Input costs that do not require an outlay of money

by the firm– Ignored by accountants

• Total costs– Explicit costs + Implicit costs

THE COSTS OF PRODUCTION

12

Explicit vs. Implicit Costs: An ExampleYou need $100,000 to start your business.

The interest rate is 5%. • Case 1: borrow $100,000

– explicit cost = $5000 interest on loan

• Case 2: use $40,000 of your savings, borrow the other $60,000– explicit cost = $3000 (5%) interest on the loan– implicit cost = $2000 (5%) foregone interest you

could have earned on your $40,000.

In both cases, total (exp + imp) costs are $5000.

Economic Profit vs. Accounting Profit

Accounting profit = total revenue minus total explicit costs

Economic profit= total revenue minus total costs (including

explicit and implicit costs)

Accounting profit ignores implicit costs, so it’s higher than economic profit.

14

Economists include all opportunity costs when analyzing a firm, whereas accountants measure only explicit costs. Therefore, economic profit is smaller than accounting profit.

THE COSTS OF PRODUCTION

15

EXAMPLE 1: Farmer Jack’s Costs

$11,000

$9,000

$7,000

$5,000

$3,000

$1,000

Total Cost

30005

28004

24003

18002

10001

$10,000

$8,000

$6,000

$4,000

$2,000

$0

$1,000

$1,000

$1,000

$1,000

$1,000

$1,00000

Cost of labor

Cost of land

Q(bushels of wheat)

L(no. of

workers)

THE COSTS OF PRODUCTION

16

EXAMPLE 1: Farmer Jack’s Total Cost Curve

Q (bushels of wheat)

Total Cost

0 $1,000

1000 $3,000

1800 $5,000

2400 $7,000

2800 $9,000

3000 $11,000

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

0 1000 2000 3000

Quantity of wheat

To

tal c

ost

Various Measures of Cost

• Fixed costs– Costs that do not vary with the quantity of output

produced

• Variable costs– Costs that vary with the quantity of output

produced

• Total cost– Fixed cost + Variable cost

Costs in Short and Long Run

• Many decisions– Fixed in the short run

– Short run: Some inputs are fixed (e.g., factories, land). The costs of these inputs are FC.

– Variable in the long run

– All inputs are variable (e.g., firms can build more factories, or sell existing ones).

THE COSTS OF PRODUCTION

19

EXAMPLE 2: Costs

7

6

5

4

3

2

1

620

480

380

310

260

220

170

$100

520

380

280

210

160

120

70

$0

100

100

100

100

100

100

100

$1000

TCVCFCQ

$0

$100

$200

$300

$400

$500

$600

$700

$800

0 1 2 3 4 5 6 7

Q

Cos

ts

FC

VC

TC

Marginal cost

• Marginal cost The change in a firm’s total cost from producing one more unit of a good or service.

• MC= ∆TC/ ∆Q

• Rising marginal cost curve– Because of diminishing marginal product

THE COSTS OF PRODUCTION

21

Recall, Marginal Cost (MC) is the change in total cost from producing one more unit:

Usually, MC rises as Q rises, due to diminishing marginal product.

Sometimes (as here), MC falls before rising.

(In other examples, MC may be constant.)

EXAMPLE 2: Marginal Cost

6207

4806

3805

3104

2603

2202

1701

$1000

MCTCQ

140

100

70

50

40

50

$70

∆TC∆Q

MC =

$0

$25

$50

$75

$100

$125

$150

$175

$200

0 1 2 3 4 5 6 7

Q

Co

sts

THE COSTS OF PRODUCTION

22

Why Marginal Cost is U-shaped• When the marginal product of labor is raising the

marginal cost of output is falling.

• When the marginal product of labor is falling the marginal cost of production is raising.

Labour Quantity Marginal Product of Labour (MPL)

Total Cost Marginal Cost (MC) $

0 0 - 800 -

1 200 200 1450 3.25

2 450 250 2100 2.60

3 550 100 2750 6.50

4 600 50 3400 13.00

Various Measures of Cost

• Average total cost (ATC) equals total cost divided by the quantity of output:

• ATC = TC/Q– Cost of a typical unit of output

• ATC = AFC + AVC• Average fixed cost (AFC), Fixed cost divided by

the quantity of output produced= FC/Q• Average variable cost (AVC), Variable cost

divided by the quantity of output produced=VC/Q

Various Measures of Cost

• U-shaped average total cost curveATC = AVC + AFC

– AFC – always declines as output rises

– AVC – typically rises as output increases • Because of diminishing marginal product

– The bottom of the U-shape• At quantity that minimizes average total cost

25© 2012 Cengage Learning. All Rights

Reserved.

Cost Curves for a Typical Firm

Costs

1.00

0.50

2.00

1.50

2.50

$3.00Many firms experience increasing marginal product before diminishing marginal product. As a result, they have cost curves shaped like those in this figure. Notice that marginal cost and average variable cost fall for a while before starting to rise.

Quantity of Output0 2 4 6 8 10 12 14

MC

ATC

AVC

AFC

Various Measures of Cost

• Efficient scale– Quantity of output that minimizes ATC

• Relationship between MC and ATC – When MC < ATC: average total cost is falling

– When MC > ATC: average total cost is rising

– The marginal-cost curve crosses the average-total-cost curve at its minimum

THE COSTS OF PRODUCTION

27

EXAMPLE 2: ATC and MC

ATCMC

$0

$25

$50

$75

$100

$125

$150

$175

$200

0 1 2 3 4 5 6 7

Q

Cos

ts

When MC < ATC,

ATC is falling.

When MC > ATC,

ATC is rising.

The MC curve crosses the ATC curve at the ATC curve’s minimum.

Costs in Long Run

• Long-run average cost curve A curve showing the lowest cost at which a firm is able to produce a given quantity of output in the long run, when no inputs are fixed.

• In the long run, ATC at any Q is cost per unit using the most efficient mix of inputs for that Q (e.g., the factory size with the lowest ATC).

© 2012 Cengage Learning. All Rights Reserved.

Average Total Cost in the Short and Long RunsAverage

TotalCost

Because fixed costs are variable in the long run, the average-total-cost curve in the short run differs from the average-total-cost curve in the long run.

Quantity of Cars per Day0

ATC in short run with small factory

ATC in short runwith medium factory ATC in short run

with large factory

ATC in long run

10,000

$12,000

1,000 1,200

Economiesof scale

Diseconomiesof scale

Constant returns to scale

THE COSTS OF PRODUCTION

30

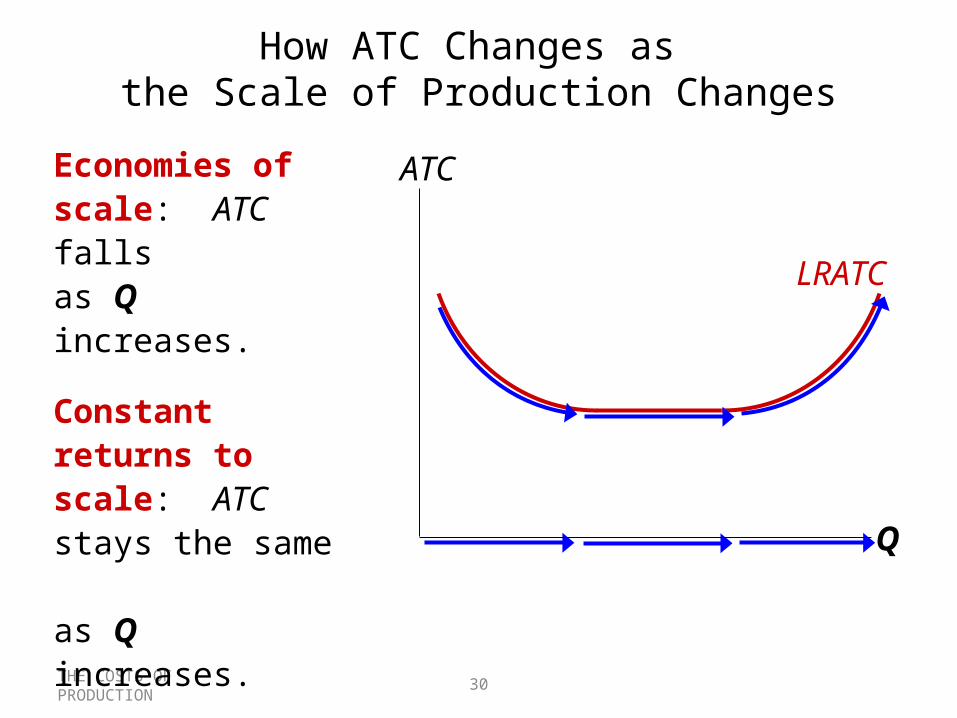

How ATC Changes as the Scale of Production Changes

Economies of scale: ATC falls as Q increases.

Constant returns to scale: ATC stays the same as Q increases.

Diseconomies of scale: ATC rises as Q increases.

LRATC

Q

ATC

Costs in Long Run• Economies of scale The situation when a firm’s

long-run average total costs fall as it increases output– Increasing specialization among workers .

• Constant returns to scale– Long-run average total cost stays the same as the

quantity of output changes

Diseconomies of scale

– The situation when a firm’s long-run average costs rise as the firm increases output.

– Increasing coordination problems

TERM DEFINITIONSYMBOLS AND EQUATIONS

Total cost The cost of all the inputs used by a firm, or fixed cost plus variable cost

TC

Fixed costs Costs that remain constant when a firm’s level of output changes

FC

Variable costs Costs that change when the firm’s level of output changes

VC

Marginal cost Increase in total cost resulting from producing another unit of output

Average total cost Total cost divided by the quantity of output produced

Average fixed cost Fixed cost divided by the quantity of output produced

Average variable cost Variable cost divided by the quantity of output produced

Implicit cost A nonmonetary opportunity cost ―

Explicit cost A cost that involves spending money ―

Q

TCATC

Q

FCAFC

Q

VCAVC

Q

TCMC

Table 10-4A Summary of Definitions of Cost

Conclusion

EXERCISE• Table 13-1• Listed in the table are the long-run total costs for three

different firms.

• Refer to Table 13-1. Firm A is experiencing economies of scale.• ANS: T/F

•

Quantity 1 2 3 4 5

Firm A 100 100 100 100 100

Firm B 100 200 300 400 500

Firm C 100 300 600 1,000 1,500