Embed Size (px)

Citation preview

Presented by Ed Slott, CPA and Jeffrey Levine, CPA

Ed Slott and Company, LLC

The Only Thing Constant is Change

• Each year the rules and/or the interpretation of the rules

for retirement accounts change dramatically.

• There are always new

• Laws

• Revenue rulings

• Private letter rulings

• Tax Court cases

• IRS notices

• IRS announcements and other guidance

2016 Contribution and Income Limits

• Maximum IRA contribution - $5,500

• IRA catch-up contribution $1,000

• Elective deferral limit for 401(k), 403(b), Thrift

Savings Plan and most 457 plans - $18,000

• Catch-up contribution for 401(k), 403(b), Thrift

Savings Plan and most 457 plans - $6,000

All unchanged from 2015

3

2016 Contribution and Income Limits

• What did change?

• Roth IRA contribution income limits rose to: • $184,000 - $194,000 married-joint

• $117,000 - $132,000 single

• Traditional IRA contribution deduction phase-out

(spouse of IRA owner an active participant) • $184,000 - $194,000

• Saver’s Credit thresholds have also increased

4

The “New” Once-Per-Year Rollover Rule Transition Relief Expired

• Only one 60-day IRA-to-IRA or Roth IRA-to-Roth IRA

each year (365 days)

• Bobrow decision changes rule from per-account-rule to

an aggregate rule

• Trustee-to-trustee transfers do not count

• The following rollovers also do not count:

• Plan-to-IRA rollovers

• IRA-to-plan rollovers

• Roth IRA conversions

The “New” Once-Per-Year Rollover Rule Transition Relief Expired

• New interpretation of the once-per-year

rollover rule was effective January 1, 2015,

BUT...

• Clients had a (somewhat) fresh start in 2015 • 2014 60-day rollovers were disregarded for NEW interpretation

• That transition relief will have fully expired by

January 1, 2016

Qualified Charitable Distributions

• NOT CURRENTLY IN EFFECT

FOR 2015 OR BEYOND!!!

• Each time the provision has expired in the past, it’s been reinstated

retroactively.

• No guarantees that will happen this time though!

Qualified Charitable Distributions

• QCD vs. “regular” charitable contribution

• QCD

• No deduction

• Not added to income

• “Regular” charitable contribution

• IRA distribution added to income

• Itemized deduction • Charitable deductions may be limited

• Clients may not itemize

• Does not prevent reduction of tax benefits tied to AGI/MAGI

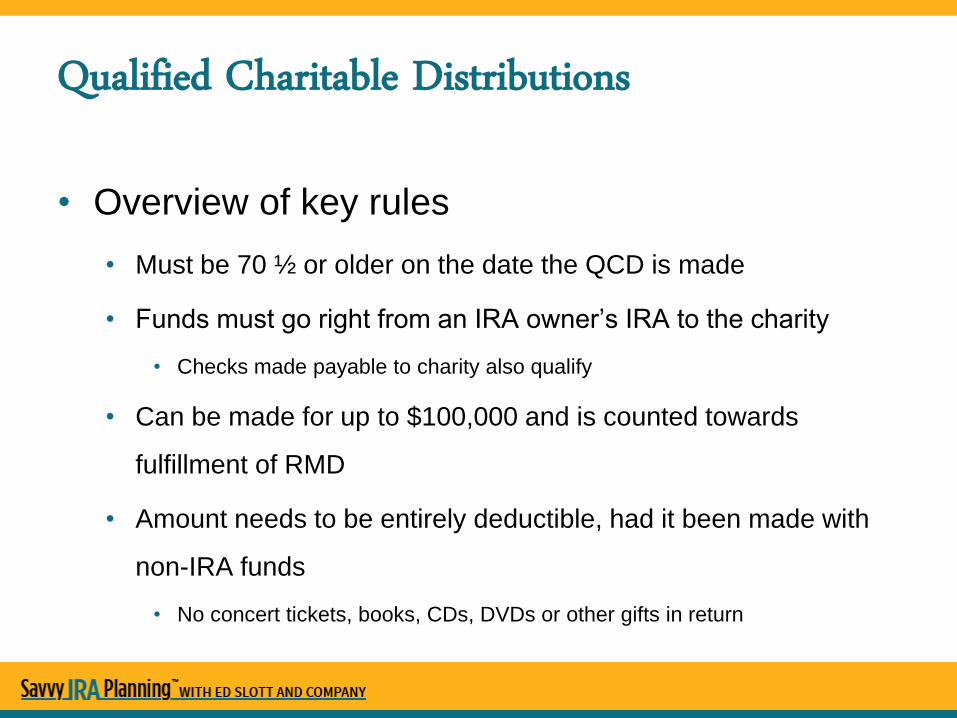

Qualified Charitable Distributions

• Overview of key rules

• Must be 70 ½ or older on the date the QCD is made

• Funds must go right from an IRA owner’s IRA to the charity

• Checks made payable to charity also qualify

• Can be made for up to $100,000 and is counted towards

fulfillment of RMD

• Amount needs to be entirely deductible, had it been made with

non-IRA funds

• No concert tickets, books, CDs, DVDs or other gifts in return

Qualified Charitable Distributions

• Two QCD Strategies

• Wait-and-see

• Act-like-it’s-already-there

“New” 10% Penalty Exception

• Trade Priorities and Accountability Act of 2015

• Signed into Law on June 29, 2015

• Includes provision changing the “Age 50

Exception”

Current “Age 50 Exception” Rules

• Applicable to state and local public safety workers

• Firefighters

• Police

• EMS

• Client must separate from service in the year they

turn 50 or later

• Applicable only to defined benefit plans

The “New” Age 50 Exception

• Expands availability to additional professions

• Federal law enforcement

• Federal Firefighters

• Border Patrol

• Customs

• Air Traffic Controllers

The “New” Age 50 Exception

• Will apply to both defined benefit and defined

contribution plans

• Can be used in conjunction with 72(t)

distributions!

• THE CHANGES DO NOT TAKE EFFECT UNTIL

JANUARY 1, 2016

Review Retirement Income Plans to Account for Budget Act’s Changes

• Bipartisan Budget Act of 2015

• Eliminates file-and-suspend strategy • Effective 180 days after signing of the law

• After grace period expires: • Clients still allowed to suspend benefit at FRA or

later, BUT

• If benefits are suspended, all other benefits

received based on individuals earnings history are

also suspended

Review Retirement Income Plans to Account for Budget Act’s Changes

• Bipartisan Budget Act of 2015

• Eliminates restricted application strategy • Effective for individuals turning reaching age 62 on

or after January 2, 2016

• After grace period expires: • Regardless of client’s age, they will not be able to

restrict their application to just their spousal benefit

• No more “free” spousal benefits

Review Retirement Income Plans to Account for Budget Act’s Changes

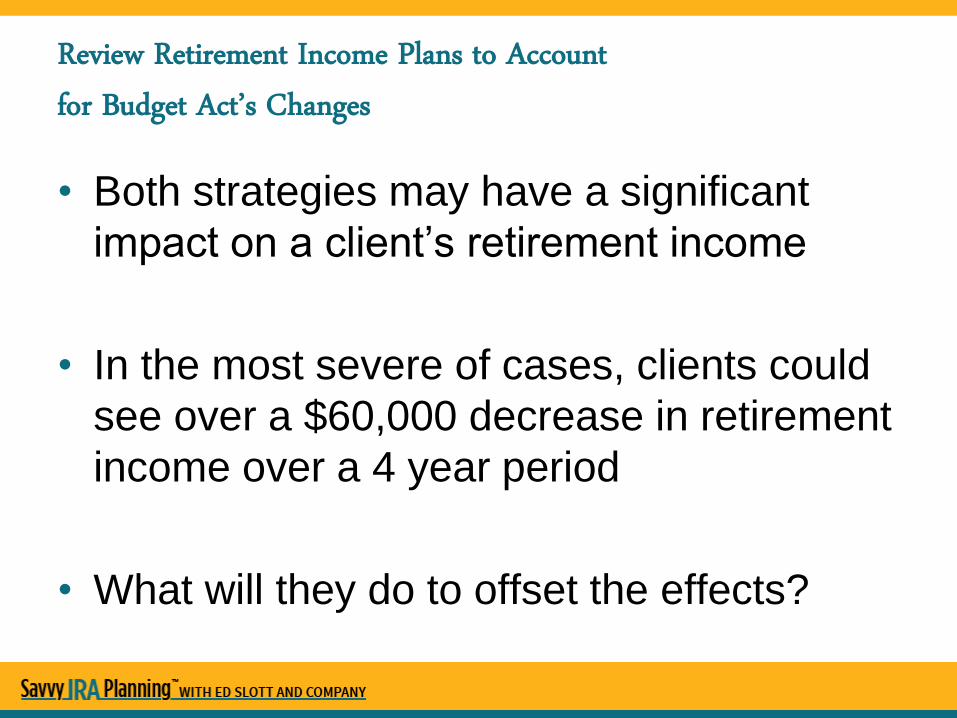

• Both strategies may have a significant

impact on a client’s retirement income

• In the most severe of cases, clients could

see over a $60,000 decrease in retirement

income over a 4 year period

• What will they do to offset the effects?

Review Retirement Income Plans to Account for Budget Act’s Changes

• Will clients still delay Social Security benefits

• Will they have to withdraw more from their IRA in the

interim years?

• How will this impact them?

• Will clients claim Social Security benefits

sooner?

• Will they have to withdraw larger than previously

anticipated amounts from their IRA to account for

smaller Social Security benefits?

• How will this impact them?

New Reporting Requirements for Hard-to-Value Assets

• New reporting for IRS forms

• 5498, IRA Contribution Information

• 1099-R, Distributions From Pensions, Annuities,

Retirement or Profit Sharing Plans, IRAs, Insurance

Contracts, etc.

• Was optional for 2014

• Mandatory for 2015 an beyond

• 2015 1099-Rs and 5498s received in 2016

• First time many clients/CPAs will see the changes

More Options for QLACs

• Qualifying longevity annuity contracts (QLACs)

• Established July 2014

• Initially only a few carriers had QLAC-qualifying

products available

• More carriers have begun to offer these

products and additional options are expected to

continue to come on line

20

More Options for QLACs

• Key QLAC rules

• Value of contract excluded for RMD purposes

• Distributions must begin no later than first day

of month following client’s 85th birthday

• Premium limited to lesser of 25% of client’s

retirement funds or $125,000

• Limited death benefit options

• Fixed contracts only

• No cash surrender value or similar benefit

21

5 Critical IRA Items to Check Before Year-End

1) Have clients maxed-out on retirement

contributions?

2) Have beneficiary forms been reviewed?

3) Should you initiate a Roth IRA conversion?

4) Are clients behind on their estimated tax

payments?

5) Have all RMDs been taken?

Maxed-Out Retirement Accounts?

• 2015 IRA contributions can generally be made up

to April 15, 2016

• Salary deferrals to employer-sponsored retirement

plans for 2015 must generally be made in 2015

• Many companies pay their bonuses around year-

end. Encourage clients to use some of these new-

found funds to save for their retirement.

Have Beneficiary Forms Been Reviewed?

• Have there been any

• Births

• Deaths

• Marriages

• Divorces

• Beneficiaries who have reached the age of

majority

• Changes that would suggest the use of a trust as

an IRA beneficiary (or suggest eliminating a trust as

an IRA beneficiary)

Roth IRA Conversion Before Year-End?

• Can always be recharacterized up to October 15,

2016

• As long as the funds leave a client’s traditional

account by December 31, 2015, it will be considered

a 2015 Roth IRA conversion... Even if the funds

don’t get into the Roth IRA until 2016

• May effectively turn the 5-year rule into a 4-year rule

Short on Estimated Tax Payments? Use This Trick! • Take a distribution from the client’s IRA for an amount equal to the

estimated tax shortfall.

• Withhold 100% of the distribution

• Eliminates estimated tax penalty

• Withholdings are treated as paid in ratably throughout the year

• Take other, non-IRA money and, within 60-days, rollover an amount

equal to the distribution.

• Restores client’s IRA and eliminates the tax on the distribution.

***Be careful of the once-per-year rollover rule***

Have All RMDs Been Taken?

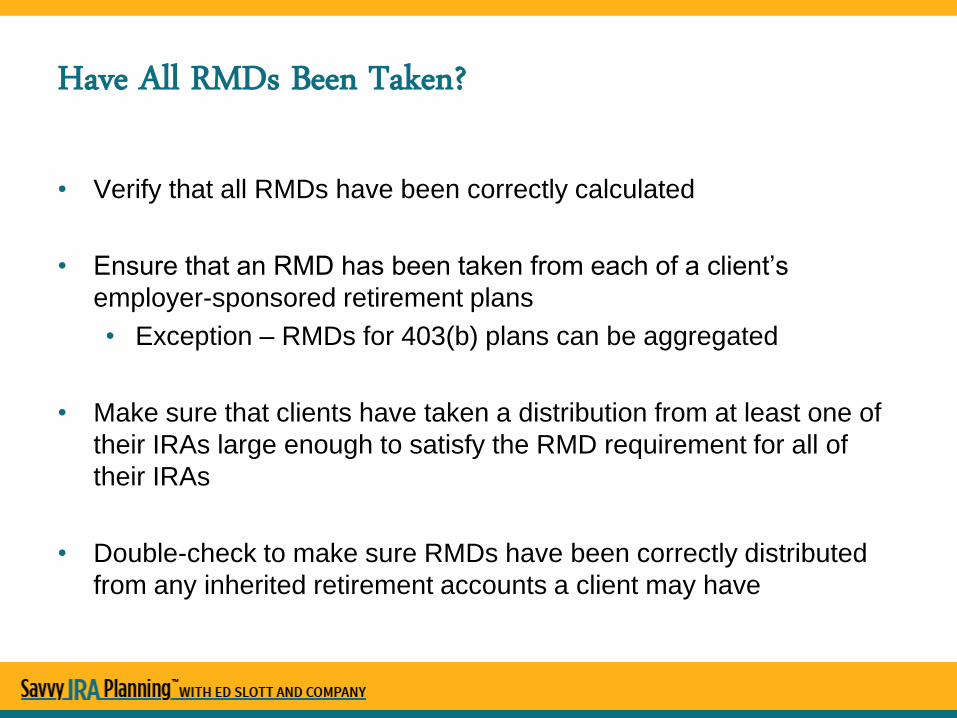

• Verify that all RMDs have been correctly calculated

• Ensure that an RMD has been taken from each of a client’s

employer-sponsored retirement plans

• Exception – RMDs for 403(b) plans can be aggregated

• Make sure that clients have taken a distribution from at least one of

their IRAs large enough to satisfy the RMD requirement for all of

their IRAs

• Double-check to make sure RMDs have been correctly distributed

from any inherited retirement accounts a client may have

Introducing Savvy IRA Planning With Ed Slott and Company

A comprehensive new resource to help you

attract more clients, including: • 4-part IRA webinar training series delivered by the Ed Slott and Company

team (CE credit)

• Seminar presentations to deliver to clients and prospects (FINRA -reviewed)

• 2 IRA study guides to support your learning and expertise

• Live webinars with Ed Slott and Company experts answering select

subscriber questions

• Marketing toolkit to promote the seminar presentations

• IRA article reprints and IRA Boomer guides to hand out

• Plus, lots more.

28

Join now and save! •Questions: [email protected] | More Info: www.horsesmouth.com/ira