Embed Size (px)

Citation preview

2017 11 17

··· Boards and institutional

investors

A RELATIONSHIP TO REINFORCE

La Sapienza

Facoltà di Economia e Commercio

Fiduciary’s Duty | 24.02.2017

2

INDEX

1.0 — Fiduciary’s duty

2.0 — Italian AGMs: the context

3 .0 — The players of the market

4.0 — Regulatory context

5.0 — Board diversities

6.0 — Renewal of the Board

7.0 — Board evaluation

8.0 — Succession Plans

9.0 — Board Induction

10.0 — Remuneration Policy

11.0 — AGM preparation: why?

12.0 — The engagement with Institutional Investors

13.0 — Case studies

1.0

···

Fiduciary’s Duty

Fiduciary’s Duty | 24.02.2017

Capital Structure

Risk Management

Executive

Remuneration

4 1 .0 F IDUC IAR Y ’ S DUTY

THE MEDIATION PARADIGM: A CLOSER LOOK

The Board is responsible for “aligning interests” by balancing the conflicting but equally valid perspectives of

management and shareholders on issues as:

Shareholders are part of the

stakeholder community to

which Boards should deal with:

DIRECTORS

MANAGEMENT SHAREHOLDERS Disclosure/Dividends&Growth

Investments

Investor Relations

MEDIATION

&

“ALIGNING

INTERESTS”

Transparency

ESG &

Sustainability

Long-term

approach

Integrated

thinking

Director

Nomination

Shareholder Rights

Control

Fiduciary’s Duty | 24.02.2017

5 1 .0 F IDUC IAR Y ’ S DUTY

A NEW APPROACH TO BOARD

HARDWARE

• The Board infrastructure.

• It defines governance policies and best practices.

• Principle-based approach.

• No transparency on decision making process inside

the Boardroom.

• Not enough to satisfy investors’ growing demands.

SOFTWARE

• The Board functioning.

• It defines how Board sets priorities, mediates

conflict and links its policies to business strategy

and performance.

• Clear Board’s role, responsibilities and behaviors.

• Board full awareness on processes connected to

the new approach.

• Board transparency.

• Stakeholder governance.

Roger Ferguson, CEO TIAA-CREF: “Corporate Governance “hardware” is in place, but CG

“software” is not.

The driver of cultural change inside the Boardroom Board should be a self-governing oversight body composed of highly competent, independent-minded, conflict-free

individuals with diverse characteristics and backgrounds who are well-informed, diligent, knowledgeable about the

Company’s business, focused on long-term performance, committed to serve the interests of the Company’s owners

and stakeholders and willing to take a high public profile in fulfilling their responsibilities.

Fiduciary’s Duty | 24.02.2017

6 1 .0 F IDUC IAR Y ’ S DUTY

THE ITALIAN GOVERNANCE ENVIRONMENT

HARDWARE

• The Governance infrastructure is clearly a

benchmark within EU countries and worldwide.

• Italian CG Code strongly promotes long-term value

creation for Shareholders.

• The Bank of Italy goes further promoting long-term

value creation for all stakeholders.

• Related party transaction regulation and slate

system for Board nomination is widely considered

as a benchmark.

• Voting obstacles have been eliminated (RD).

SOFTWARE

• Transparency on Board functioning is generally

not exhaustive.

• Board diversities still linked to old-style drivers.

• Board evaluation generally performed without an

external facilitator.

• Sustainable thinking or integrated reporting are

generally at a an early stage or “parallel” to the

strategy and not integrated.

• Long-term drivers on compensation as vesting

period are generally not sufficiently aligned with

long-term performance.

• Engagement with Shareholders is often reactive.

The driver of cultural change inside the Boardroom • CG Codes and norms are in place but business model and connected Boards, Directors and Companies are not

predominantly focused on operating for long-term value creation.

• Governance needs to update itself and this should start from the main actors: Board’s directors, which through

their Fiduciary’s duty should bring into the Boardroom a new model of sustainable business integrated with ESG

factors and ask for a cultural change at both Board and Company level.

Fiduciary’s Duty | 24.02.2017

7 1 .0 F IDUC IAR Y ’ S DUTY

FIDUCIARY DUTY

TWO MAIN DUTIES

Loyalty: placing the company’s interests ahead of

individual own interest.

Prudence: applying proper care, skill, and diligence

to business decisions.

• • • Main principle guiding Board responsibility is

mediating between the “legitimate but often

conflicting interests of Management and

Shareholders”.

• • •

• • •

Board members' time commitment might increase in 2016

and Director’s responsibilities become more complex.

• • •

BOARD RESPONSIB IL IT IES

Companies should carefully compile and disclose its

own list of Board responsibilities that reflects its

individual characteristics, circumstances and goals on

the basis of:

• Strong leadership skills and self-evaluations -

important to be effective.

• Effective strategy and risk oversight - for better

Board-Management information flow.

• Board addressing the corporate culture change.

• Effectively manage reputational risk on a global

scale.

• Improve dialogue with stakeholders, the quality of

disclosures around how boards are carrying out

their oversight responsibilities.

Fiduciary’s Duty | 24.02.2017

8 1 .0 F IDUC IAR Y ’ S DUTY

KEY GOVERNANCE – BOARD OVERSIGHT

TRENDS Leon Panetta: “Can we end the long

tradition of the Boardroom as a sealed

chamber …? Can we move toward

more transparency about boardroom

process …?”

More important trends will impact Board oversight across

jurisdictions in 2017:

Board composition: independence and diversity as

measures of effectiveness.

Board structure and processes: majority voting, annual

elections, CEO/chair split, etc.

Strategy: Board engagement in the strategy-setting process.

Succession: approach to executive and its own succession

planning.

Risk: oversight of risk management, including emerging,

complex and reputational ones.

Remuneration: the linkage between Company strategy,

executive compensation philosophy and pay plan design.

Financial oversight: oversight of financial matters as

external audit, internal audit, financial controls.

Sustainability: understanding the real indicators that create

value through integrated thinking.

Activism: more openness to activist investors and increased

engagement to long-term institutional investors.

• Board transparency is the pillar.

• Board effectiveness becomes the key-driver.

• This brings more responsibility for Board as

a whole and its Directors.

• Director’s role has changed and many new

tasks and responsibilities should be

addressed.

• Long-term thinking should be applied in the

boardroom, disclosed and promoted to all

stakeholders.

2.0

···

Italian AGMs:

the context

Fiduciary’s Duty | 24.02.2017

10 2 .0 ITAL IAN AGMS: THE CONTEXT

PANEL FTSE MIB The subject of this analysis consists in a panel composed of the FTSE Mib companies as of June 2017, except :

• Companies that have the registered office abroad (CNH Industrial, Exor, Ferrari, FCA, Stmicroelectronics,

Tenaris);

• Mediaset and Mediobanca, which have not held the AGM 2017 yet;

The chart below shows the Market Cap level of the Companies analysed from the largest to the smallest.

-

10.000

20.000

30.000

40.000

50.000

60.000

Market Cap

Fiduciary’s Duty | 24.02.2017

11 2 .0 ITAL IAN AGMS: THE CONTEXT

AVERAGE QUORUM

AGM PARTICIPATION % OUTSTANDING SHARE CAPITAL

• Record date: average participation by institutional

investors +160% in six years.

• New context: greater investors’ participation and

binding proposals (remuneration) created a positive

momentum for CG best practices implementation.

54,3% 52,3%

61,7% 65,3% 65,2% 66,6% 65,1%

10,7%

19,3% 20,6% 21,1% 25,4% 26,1% 27,6%

2009 2010 2011 2012 2013 2014 2015 2016

Average Quorum Minority Shareholders

47,5% 44,6%

41,2% 39,0% 39,0%

8,3%

20,7%

25,4% 26,1% 27,6%

2005 2013 2014 2015 2016

Controlling Shareholders Minority Shareholders

FTSE Mib 2016 % OUTSTANDING SHARE CAPITAL

• Active approach towards non-financial matters

(ESG): due to greater investments by international

investors on Italian corporations.

Fiduciary’s Duty | 24.02.2017

12 2 .0 ITAL IAN AGMS: THE CONTEXT

QUORUM IMPACT

MINORITY

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Minority Shareholder Controlling Shareholder

The charts below shows the Minority shareholders weight in the last AGM.

• The average participation of Minority Shareholders is 47.6% of the Quorum.

• Prysmian is the only company whose Minority Shareholders represents almost 100% of the Quorum.

Fiduciary’s Duty | 24.02.2017

22

% 22

%

23

%

29

%

S.Ferragamo

MINORITY PARTICIPATION - FOREIGN INVESTORS

13 2 .0 ITAL IAN AGMS: THE CONTEXT

• 2012 • 2013 • 2014 • 2015

21

%

26

%

33

% 30

%

Unicredit

25

%

27

%

32

%

43

%

Intesa S

24

% 13

%

24

% 23

%

Snam

24

% 22

%

27

%

55

%

Telecom It

26

%

31

% 28

%

35

%

Eni

13

%

15

%

23

% 21

%

Saipem

9

%

12

%

15

%

17

%

Generali

22

% 17

%

32

%

35

%

Atlantia

5

%

14

% 11

%

12

%

Luxottica

13

%

20

%

27

%

46

%

Leonardo

SUBSTANTIAL INCREASING PARTICIPATION AT ITALIAN AGMS (% ISC) SINCE 2012

Fiduciary’s Duty | 24.02.2017

7

%

17

% 15

%

16

%

Luxottica

23

%

27

%

41

% 33

%

Saipem

25

%

30

% 28

%

34

%

S.Ferragamo

34

% 25

%

49

% 37

%

Snam

29

%

2

%

41

%

43

%

Atlantia

21

%

26

%

33

%

44

%

Generali

46

%

51

% 47

%

48

%

Eni

45

%

49

%

49

%

56

%

Telecom It

48

%

48

%

56

%

60

%

Unicredit

29

%

39

%

45

%

48

%

Leonardo

44

% 43

%

53

%

63

%

Intesa

MINORITY PARTICIPATION – INTERNATIONAL

INVESTORS

14 2 .0 ITAL IAN AGMS: THE CONTEXT

• 2012 • 2013 • 2014 • 2015

• 50% of the quorum is now usually held by foreign investors

• extraordinary resolutions are no longer routine exercise.

3.0

···

The players of the market

Fiduciary’s Duty | 24.02.2017

16 3 .0 THE PLAYERS OF THE MARKET

WHO ARE THE MAIN PLAYERS INVOLVED?

INSTITUTIONAL INVESTORS

• Many have CG teams.

• Have clear voting policies.

• Are generally happy to engage.

• Prefer to engage directly with Top Management,

not Investor Relations.

• Open to over-rule voting decision.

PROXY ADVISORS

• ISS and Glass Lewis – most influential.

• Recommend investors on how to vote.

• More rigid rather than their clients.

• Biased by Governance aspects only.

• Have a strong influence over many investors.

• Most are happy to engage but timing is important.

Fiduciary’s Duty | 24.02.2017

17 3 .0 THE PLAYERS OF THE MARKET

THE VOTING CHAIN

JP Morgan

Northern

BONY

UK Pension

Fund

US College

Fund

UK Pension

Fund

US Mutual

Fund

ISS

State

Street

HSBC

ECGS

Global

Custodian

Beneficial

Owner

Local

Custodians

Investment

Advisor

Proxy Voting

Agent

Proxy

Advisor

BLACKROCK

US Mutual

Fund

Glass

Lewis

Company

BNP Paribas

DB

Intesa

San Paolo

ISS

Broadridge

Fiduciary’s Duty | 24.02.2017

18 3 .0 THE PLAYERS OF THE MARKET

VOTING PROCESS FOR INVESTORS

Corporation

Fiduciary’s Duty | 24.02.2017

19 3 .0 THE PLAYERS OF THE MARKET

MAIN PROXY ADVISORS

• 500 analysts, 1700

institutional clients

which manage around

$26 trillion.

• 40.000 AGMs under

review each year.

• 300 analysts, 900

institutional clients

which manage around

$15 trillion.

• 23.000 AGMs under

review each year.

OTHER PROXY ADVISORS

4.0

···

Regulatory context

Fiduciary’s Duty | 24.02.2017

21 4 .0 REGULAT OR Y CONTEX T

INVESTORS AND CORPORATIONS: THE

REGULATORY CONTEXT

GROWING ENGAGEMENT BY INVESTORS OVER THE CORPORATIONS THEY INVEST ON

The engagement by investors on their investee Companies is constantly growing due to:

• Intention to promote governance implementations and financial performance of corporations through:

— Board election

— Say on pay

— ESG engagement.

• The “Vote with your feet” approach may generate an excessive risk-taking for big institutional investors.

• Local and supra-national regulatory initiatives (i.e. financial sectors).

• Institutional investors are much more “accountable” towards their end-investors - clients (fiduciary duty).

• Recent scandals in poor Governance (Enron, BP, Volkswagen, …) proved that an appropriate governance

model is a risk-mitigation factor.

Fiduciary’s Duty | 24.02.2017

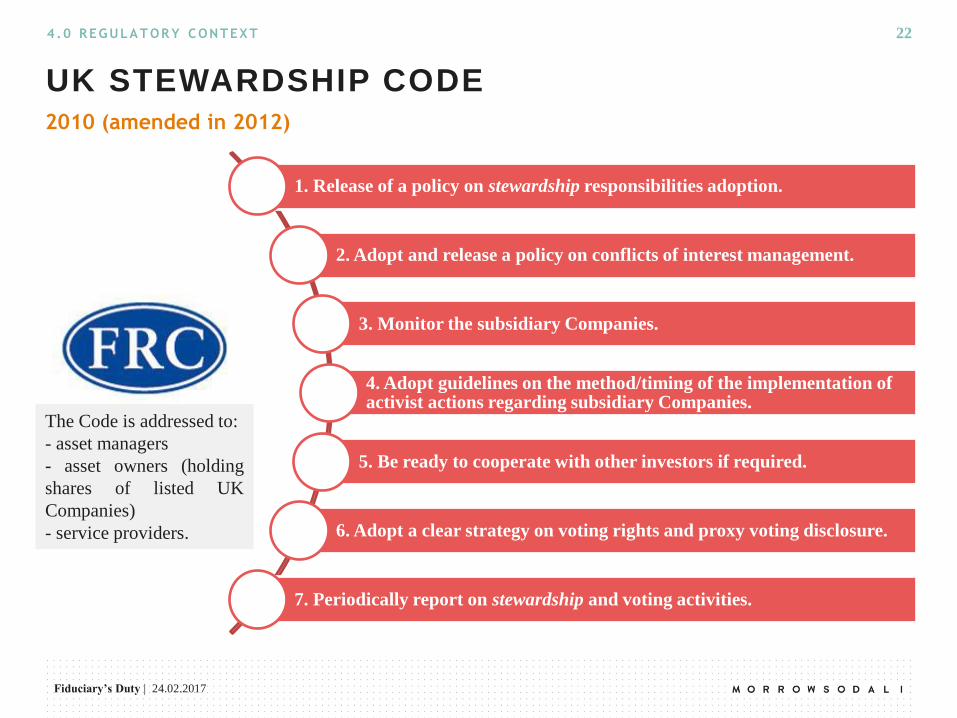

22 4 .0 REGULAT OR Y CONTEX T

UK STEWARDSHIP CODE

2010 (amended in 2012)

1. Release of a policy on stewardship responsibilities adoption.

2. Adopt and release a policy on conflicts of interest management.

3. Monitor the subsidiary Companies.

4. Adopt guidelines on the method/timing of the implementation of activist actions regarding subsidiary Companies.

5. Be ready to cooperate with other investors if required.

6. Adopt a clear strategy on voting rights and proxy voting disclosure.

7. Periodically report on stewardship and voting activities.

The Code is addressed to:

- asset managers

- asset owners (holding

shares of listed UK

Companies)

- service providers.

Fiduciary’s Duty | 24.02.2017

1. The Company should release a public policy on ownership responsibilities.

2. Monitor subsidiary Companies.

3. Adopt guidelines on method/timing of implementation of activist actions on subsidiaries, to protect investment and increase its value.

4. Take into consideration to cooperate with other investors if required, complying with any «agreement action» policy.

5. Consciuos exercise of the voting rights.

6. Report on the ownership and voting right exercise in subsidiary Companies, and implement an engagement activities policy.

23 4 .0 REGULAT OR Y CONTEX T

EFAMA CODE FOR EXTERNAL GOVERNANCE

2011

The Code is mainly

addressed to Investment

management companies.

Fiduciary’s Duty | 24.02.2017

24 4 .0 REGULAT OR Y CONTEX T

ITALIAN STEWARDSHIP CODE

2013 (amended in 2015)

1. The Companies adopt a publicly available policy regulating the exercise of rights on financial instruments pertaining OICR and administered portfolios.

2. The Companies monitor the listed subsidiary Companies.

3. 3. Adopt guidelines on method/timing of implementation of activist actions on listed subsidiaries, to protect investment and increase its value.

4. Evaluate the opportunity to cooperate with other investors if appropriate, taking careful attention to «agreement action» regulation.

5. The Companies consciously exercise the voting rights on financial instruments pertaining to OICR and administered portfolios.

6.The Companies mark the exercise of those rights on financial instruments pertaining to OICR and administered portfolios, and adopt a policy on external governance information disclosure.

The Code is manily

addressed to Asset

management Companies.

Fiduciary’s Duty | 24.02.2017

25

CONFLICTS OF INTEREST

Only the Stewardship Code recommends

the adoption of a policy to manage the

conflicts of interest.

PRE-AGM ENGAGEMENT

Only the Stewardship Code recommends to

communicate to the subsidiary Companies

the willingness to vote against or abstain

(motivated).

POST-AGM ENGAGEMENT

Only the Stewardship Code recommends

reporting the voting exercise in subsidiary

Companies.

INFORMATION ON PROXY

ADVISOR USE

The Italian Code does not mention any

disclosure on proxy advisory services

engagement.

4 .0 REGULAT OR Y CONTEX T

A COMPARISON ACROSS GOVERNANCE CODES

5.0

···

Board diversities

Fiduciary’s Duty | 24.02.2017

27 5 .0 BOARD D IVERS IT I E S

BOARD OVERSIGHT TRENDS

ADVANTAGES FROM DIVERS IT IES

Risk mitigation

• A proper mix of diversities in the Boardroom is

not only the driver to the effectiveness of the

Board but also an efficient tool to mitigate

growing risks to Board members.

Risk monitoring

• Wider, diversified and up-to-date expertise and

skills ensure the appropriate coverage of risks and

help directors pursuing their fiduciary duty.

Value creation

• Appropriate mix of skills ensures the Board

functions efficiently and supports strategically the

management to pursue a long-term value creation

for shareholders.

Objectives of the diversities policy

Boards should adopt diversities policy with the aim of:

• Finding a proper director’s skill set and variety of

perspectives which take into account company’s

culture & needs integrated with business &

economical context Board should face in the long-

term.

• Performing an in-depth assessment of Board

strengths, weaknesses and needs through an

effective Board evaluation.

• Achieving optimal balance between refreshing the

board and retaining valuable experience.

• Creating long-term value through injecting a

variety of informed perspectives into the

boardroom conversation.

• Defining a genuine Board appointments process to

ensure broader reach-out to identify and recruit

capable people of different backgrounds and life

experience.

Fiduciary’s Duty | 24.02.2017

28 5 .0 BOARD D IVERS IT I E S

TRENDS IMPACTING DIVERSITIES

More important trends will impact board diversities in

2017:

• Shareholders’ community has a strong say on

directors’ election.

• Disclosure on Board functioning is becoming

more important than composition, size or

independence.

• More transparency regarding Directors’

nomination process and functioning become

imperative.

• A greater and diverse diversities’ framework is

imperative for Boards to face long-term

challenges.

• Specialist and behavioral diversities should

enter in the Boardroom to minimize risks.

• Independence and thought diversity is critical

to compete today.

• Transition from a compliance exercise to ensuring

a sustainable long-term vision and mitigation of

risks.

• Principles are fundamental but attention to

company’s own culture, mission, values and

history should be integrated.

• Board succession plan help to ensure the

appropriate set of diversities to face future

challenges.

• Proper tenure mix to ensure continuity and

innovation.

• Integration of ESG factors within the business

strategy become the meaningful tool to ensure a

sustainable, profitable and less riskier business.

• Promote an effective integrated reporting.

• Stakeholder Governance becomes the new

approach.

Fiduciary’s Duty | 24.02.2017

29 5 .0 BOARD D IVERS IT I E S

WHAT DO DIRECTORS THINK ABOUT

DIVERSITIES?

34% agreed that the boards

on which they served fully

comprehended their

companies’ strategies.

Stephen Murray – President and Ceo of CCMP

Capital: “The whole activist industry exists

because public boards are often seen as

inadequately equipped to meet shareholder

interests”.

Lou Gerstner – Former Ceo of IBM: “In anything

other than a protected industry, longevity is the

capacity to change, not to stay with what you’ve

got, … . Companies that last 100 years are never

truly the same company, … . They’ve changed 25

times or 5 times or 4 times over that 100 years”.

Sir David Walker – Former Chairman of Barclays:

“The first question I would ask boards is whether

they are spending enough time and effort

assessing the organization’s long-term strategy, …

. If they are honest, the answer will almost always

be no.”

34

%

22

%

16

%

* Extract from Improving Board Governance: McKinsey Global

Survey results 2013.

Only 22% said their boards

were completely aware of

how their firms created

value.

Just 16% claimed that their

boards had a strong

understanding of the

dynamics of their firms’

industries.

Fiduciary’s Duty | 24.02.2017

30 5 .0 BOARD D IVERS IT I E S

BASIC VS ADVANCED BOARD

THE BAS IC BOARD

• Independence

• Tenure policy

• Gender

• Age

• Business expertise

• Financial expertise

• International expertise

• Audit expertise

• Risk management

• Familiarity with CG best practices

• Marketing & Sales

THE ADVANCED BOARD

• Attitude to change

• Dialogue skills within the Board

• Leadership experience

• Global mind-set

• Inter-market experience

• Crisis or turn-around experience

• New markets expertise

• Industry regulatory skills

• Governmental & Geo-political experience

• Cyber Security

• Information technology

• Digital & Media

• Race & Demography

• Environmental and Social factors

• Stakeholders’ culture

• Integrated thinking

Fiduciary’s Duty | 24.02.2017

20

14

14

13

13

13

13

12

11

10

10

10

9

9

8

7

Portugal

Germany

Italy

France

Ireland

Luxembourg

Spain

Belgium

Austria

Denmark

Sweden

UK

Norway

Switzerland

Finland

Netherlands

S IZE

31 5 .0 BOARD D IVERS IT I E S

• Italian “Independent Chairman” average level, 21%, is not aligned with

Nordics and Anglo-Saxons model.

• Not many CEO - Chair combined positions (14%).

• Italian “Non independent Chairman” average level is 34%.

COMPOSIT ION

94%

65%

56%

56%

50%

44%

40%

38%

38%

34%

32%

29%

21%

5%

2%

7%

9%

2%

24%

19%

3%

5%

6%

17%

11%

7%

15%

19%

17%

24%

14%

7%

6%

7%

3%

26%

39%

22%

17%

44%

47%

38%

44%

36%

41%

57%

34%

29%

50%

19%

2%

6%

33%

8%

4%

14%

60%

50%

56%

Netherlands

UK

Denmark

Finland

Portugal

Ireland

Norway

Belgium

Germany

Switzerland

Sweden

Austria

Italy

France

Luxembourg

Spain

Independent Chairman Executive Chairman Chairman former CEO

Non Independent Chiarman Combines Chiarman-CEO

• Italian Boards size average level, 1.4,

is in line with the Peers.

STATISTICS: SIZE & COMPOSITION

* Extract from ECGS 2014 Composition & Remuneration of Boards of Directors

11: EU average

Fiduciary’s Duty | 24.02.2017

80%

69%

62%

58%

58%

52%

49%

46%

44%

42%

41%

34%

33%

33%

32%

31%

3%

4%

29%

24%

8%

2%

7%

8%

19%

12%

11%

17%

29%

17%

27%

9%

18%

34%

46%

51%

47%

48%

39%

47%

66%

56%

50%

38%

69%

Switzerland

Finland

Spain

Norway

Luxembourg

Sweden

Denmark

France

Portugal

Belgium

UK

Ireland

Germany

Italy

Austria

Netherlands

Independent NED Executive Directors Not Independent NED

32 5 .0 BOARD D IVERS IT I E S

• Italian boards average independence level is 42%

• Italian executives on board average level is 19%

STATISTICS: INDEPENDENCE

* Extract from ECGS 2014 Composition & Remuneration of Boards of Directors

• EU independence rate is 34%

• 40% EU boards are below 50% level

[VALO

RE] [VALO

RE]

14%

Independent NED

Executive Directors

Not Independent NED

[VALOR

E] 18%

21%

27%

29%

4%

0%

<33%

33-49%

50-66%

67-99%

100%

Fiduciary’s Duty | 24.02.2017

33 5 .0 BOARD D IVERS IT I E S

STATISTICS: WOB & TENURE

* Extract from ECGS 2014 Composition & Remuneration of Boards of Directors

38%

31%

29%

29%

25%

24%

22%

21%

20%

20%

20%

18%

14%

13%

12%

5%

Norway

France

Finland

Sweden

Denmark

Italy

Netherlands

Belgium

Austria

Germany

UK

Spain

Switzerland

Ireland

Luxembourg

Portugal

WOMEN ON BOARD

TENURE

22%: EU average

• Italian gender average level, 24%, is over EU

level but behind Nordics Peers.

7,7

7,6

7,6

7

6,9

6,7

6,6

5,9

5,9

5,7

5,3

5,2

5,1

5

4,7

4,6

Belgium

Spain

Luxembourg

Ireland

Switzerland

Sweden

France

Germany

Portugal

Austria

UK

Denmark

Italy

Netherlands

Norway

Finland

• Italian EU tenure average level is 5.1 years.

5.9: EU average

Fiduciary’s Duty | 24.02.2017

3,5

2,1

1,13

2

1,7

Italia

Francia

Spagna

Uk

Norvegia

34 5 .0 BOARD D IVERS IT I E S

STATISTICS: OTHER INDICATORS

* Extract from Spencer Stuart 2015 Italia Board Index

58,9

59,7

60

57,5

55,3

Italia

Francia

Spagna

Uk

Norvegia

8%

33%

13%

32%

30%

Italia

Francia

Spagna

Uk

Norvegia

• The Italian level is in line

with European countries.

• Nonetheless, only France

shows older Boards.

AGE

• Italian Board-seats excessive

if compared to other

European countries.

• More than three times the

smallest average, registered

in Spain.

• The Italian level remains

below European countries.

• Specifically, it is the lowest

and ¼ of the best performing

country, Uk.

SEATS INTERNATIONALITY

Fiduciary’s Duty | 24.02.2017

35 5 .0 BOARD D IVERS IT I E S

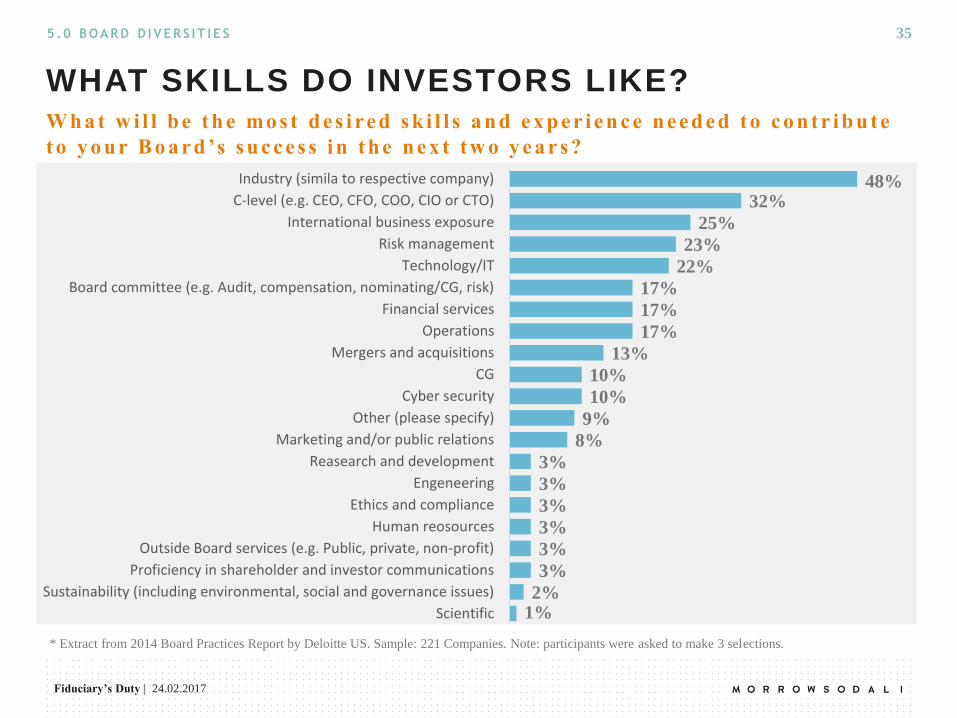

WHAT SKILLS DO INVESTORS LIKE?

* Extract from 2014 Board Practices Report by Deloitte US. Sample: 221 Companies. Note: participants were asked to make 3 selections.

48% 32%

25%

23%

22%

17%

17%

17%

13%

10%

10%

9%

8%

3%

3%

3%

3%

3%

3%

2% 1%

Industry (simila to respective company)

C-level (e.g. CEO, CFO, COO, CIO or CTO)

International business exposure

Risk management

Technology/IT

Board committee (e.g. Audit, compensation, nominating/CG, risk)

Financial services

Operations

Mergers and acquisitions

CG

Cyber security

Other (please specify)

Marketing and/or public relations

Reasearch and development

Engeneering

Ethics and compliance

Human reosources

Outside Board services (e.g. Public, private, non-profit)

Proficiency in shareholder and investor communications

Sustainability (including environmental, social and governance issues)

Scientific

W h a t w i l l b e th e mo s t d e s i re d s k i l l s a n d e x p e r i e n c e n e e d e d to c o n tr i b u te

t o y o u r B o a r d ’s s u c c e s s i n th e n e x t tw o y e a r s ?

Fiduciary’s Duty | 24.02.2017

36 5 .0 BOARD D IVERS IT I E S

BASIC VS ADVANCED BOARD

THE BAS IC BOARD

• Independence

• Tenure policy

• Gender

• Age

• Business expertise

• Financial expertise

• International expertise

• Audit expertise

• Risk management

• Familiarity with CG best practices

• Marketing & Sales

THE ADVANCED BOARD

• Attitude to change

• Dialogue skills within the Board

• Leadership experience

• Global mind-set

• Inter-market experience

• Crisis or turn-around experience

• New markets expertise

• Industry regulatory skills

• Governmental & Geo-political experience

• Cyber Security

• Information technology

• Digital & Media

• Race & Demography

• Environmental and Social factors

• Stakeholders’ culture

• Integrated thinking

Fiduciary’s Duty | 24.02.2017

37 5 .0 BOARD D IVERS IT I E S

WHAT SKILLS DO INVESTORS LIKE?

CALPERS: “The Board should consist of Directors with

the requisite range of skills, competence, knowledge,

experience and approach, as well as a diversity of

perspectives, to set the context for appropriate Board

behaviors and to enable it to discharge its duties and

responsibilities effectively”.

TIAA-CREF INVESTMENT MANAGEMENT:

“The Board should be composed of individuals who can

contribute expertise and judgment, based on their

professional qualifications and business experience. The

Board should reflect a diversity of background and

experience”.

CPP INVESTMENT BOARD: “The experience,

qualifications and character of Directors is of utmost

importance. The Board as a whole must have general

business acumen (including specific qualifications in

finance, accounting and governance matters) and relevant

industry expertise”.

Investors’ policies are based on principles and refrain

from being prescriptive … up to Boards decide the

proper mix!

• Adequate mix of competences (80%)

• Financial experience (70%)

• Banking regulation skill (70%)

• Accounting skill (60%)

• Risk & control experience (50%)

• Technology skill (40%)

• Management expertise (30%)

• Human resources skill (20%)

• Industrial skill and experience (20%)

MorrowSodali directly surveyed a target of

institutional investors to define the list of preferred

diversities for banking industry’s Boards

Fiduciary’s Duty | 24.02.2017

38 5 .0 BOARD D IVERS IT I E S

BOARD COMPOSITION

TRENDS ON DISCLOSURE

• Calls for improving disclosure of Board composition.

• Provide investors with more meaningful disclosure that will help them in their voting decisions by better

enabling them to determine whether and why a Director candidate is an appropriate choice for a particular

Company.

Specifically, as to current Board members:

• Basic biographical information that sheds little light on the board’s thinking about what each individual brings

to the Boardroom table.

• Any directorships of public companies and registered investment companies.

Specifically, as to Nominee Directors:

• Particular qualifications, attributes, skills or experience that led the board to conclude that the person should

serve as a Director.

• Clear understanding of how an individual’s background and qualifications relate to the company’s business and

strategy.

Board diversity policy:

Disclose whether and how Board considers diversity in the nomination process.

Fiduciary’s Duty | 24.02.2017

39 5 .0 BOARD D IVERS IT I E S

DISCLOSURE BEST PRACTICE

PROXY STATEMENT PRUDENTIAL

Fiduciary’s Duty | 24.02.2017

40 5 .0 BOARD D IVERS IT I E S

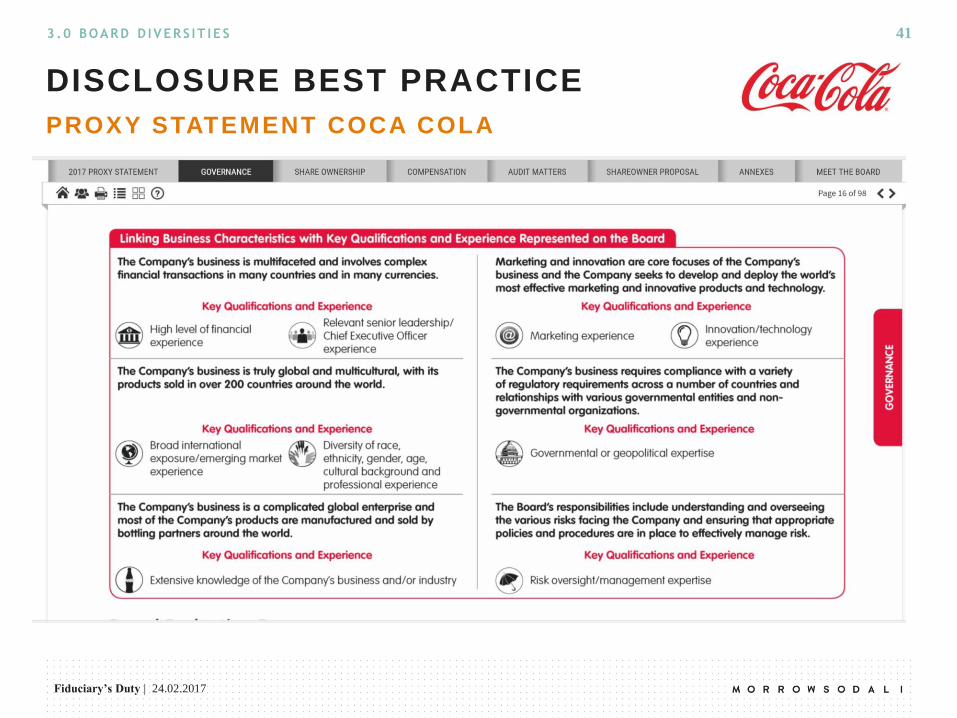

DISCLOSURE BEST PRACTICE

Business Characteristics Qualifications, Attributes, Skills and Experience

The Company’s business is multifaceted and involves

complex f inancial transactions in many countries and in

many currencies.

• High level of f inancial literacy

• Relevant Chief Executive Officer/President

experience

The Company’s business is truly global and

multicultural, w ith its products sold in over 200

countries around the w orld.

• Diversity of race, ethnicity, gender, age, cultural

background or professional experience

• Broad international exposure

The Company’s business is a complicated global

enterprise and most of the Company’s products are

manufactured and sold by bottling partners around the

w orld.

• Extensive know ledge of the Company’s business,

industry or manufacturing

Marketing is the core focus of the Company’s business

and the Company seeks to develop and deploy the

w orld’s most innovative and effective marketing and

technology.

• Marketing/marketing-related technology experience

The Company’s business requires compliance w ith a

variety of regulatory requirements across a number of

countries and relationships w ith various governmental

entities and non-governmental organizations.

• Governmental or geopolitical expertise

The Board’s responsibilities include understanding and

overseeing the various risks facing the Company and

ensuring that appropriate policies and procedures are

in place to effectively manage risk.

• Risk oversight/management expertise

PROXY STATEMENT COCA COLA

Fiduciary’s Duty | 24.02.2017

41 3 .0 BOARD D IVERS IT I E S

DISCLOSURE BEST PRACTICE

PROXY STATEMENT COCA COLA

6.0

···

Renewal of the Board

Fiduciary’s Duty | 24.02.2017

43

AGM RESOLUTIONS: BOARD ELECTION

SLATE SYSTEM MODEL

In Italy, the election of Boards of Directors and

statutory auditors applies a slate voting system called

“Voto di Lista”.

Voto di Lista

The Italian system historically features concentrated

ownership. The Slate voting (“Voto di Lista”) was

introduced to allow the representation of minority

shareholders in the Board.

It is a standard mechanism that ensures both Board

monitoring and the protection of Shareholders against

expropriation.

• • •

Condition:

Shareholders holding between

0.5%-4.5% of a Company’s share

capital are entitled to present a slate

of candidates ahead of the AGM.

• • •

6 .0 RENE WA L OF THE BOARD

Fiduciary’s Duty | 24.02.2017

44

AGM RESOLUTIONS: BOARD ELECTION

SYSTEM SLATE SYSTEM MODEL

The Italian Voto di Lista framework develops into 3 different systems:

6 .0 RENE WA L OF THE BOARD

Maggioritario puro: Company’s by-laws establish that the slate obtaining the highest number of votes appoints

the large majority of Board Members; the second most-votes list appoints the remaining directors.

i.e Exor: “all irectors except one shall be elected from the list that has obtained the highest number of votes, on the

basis of the numerical order in which they appear on the list; as provided by law, one director shall be elected from

the list that has obtained the second highest number of votes on the basis of the numerical order in which the

candidates appear on the list”.

Maggioritario proporzionale: Company’s by-laws establish that the slate obtaining the highest number of votes

appoints the large majority of Board Members; the remaining directors shall be appointed by the other slates.

i.e Enel : “7/10 of the Directors to be elected, rounding down any fraction to the unit, shall be drawn from the slate

that has obtained the most votes cast in the order in which they are listed on the slate; the remaining Directors shall

be drawn from the other slates; for this purpose, the votes obtained by these slates shall be divided successively by

one, two, three and so forth according to the number of Directors to be elected”.

Proporzionale: The votes obtained by the lists shall be divided subsequently by one, two, three, four and so on

according to the number of directors still to be elected.

i.e. Mediaset: “When the voting ends, the votes obtained by each list shall be divided by the integers from one to

the number of Directors to be elected”.

Fiduciary’s Duty | 24.02.2017

45

SLATE VOTING SYSTEM IN ITALY -1/2

SOME FACTS

Some analysis conducted by MorrowSodali shows

that:

• >50% Companies adopts a “maggioritario puro”.

• 15 Companies’ bylaws establish that minority

Shareholders have the right to appoint only one

member to the Board of Directors.

• Mediaset and Mediolanum adopt a “metodo

proporzionale”.

• Mps has a hybrid system which guarantees a high

level of representation for minority Shareholders;

the by-laws provide for 50% of members

appointed by the majority and the remaining 50%

appointed proportionally from minority slates.

• MEF Companies have a good representation of

minority Shareholders, the system foresees that

7/10 are appointed by the majority and 3/10 by

minorities translating effectively, for a Board

made up of 9 members (Eni, Enel, Snam) in a

33% appointed by minority Shareholders.

• Bper is the only Company adopting a staggered

Board.

6 .0 RENE WA L OF THE BOARD

ITALIAN LISTED COMPANIES: FTSE-MIB

• The number of Companies declaring at least one

minority Director is decreasing over time: 90, vs 93 in

2014 and 97 in 2013.

• The number of Companies with minority Directors is

quite stable (39%), because issuers diminished.

• The total number of minority Directors is 172 (vs 174 in

2014 and 191 in 2013). When present, they weight 18%

of the total (23% in the Supervisory Boards).

• The size of a Company matters in defining the number of

minority Directors (2,3 in the FTSE Mib; 1,9 in the Mid

Cap sector and 1,3 in the Small cap sector); industry is

another key factor (in the banking sector the number

reaches 2,6).

• The Board of Auditors across Companies has a more

homogeneous structure, almost always made up of 3

members, one of which represents the minority

Shareholders.

Fiduciary’s Duty | 24.02.2017

46

SLATE VOTING SYSTEM IN ITALY -2/2

CRITICAL ASPECTS

• Board members appointed by Minority

Shareholders: average 27%, excluding foreign-

domiciled Companies and Directors not elected

with the slate voting system.

• Board members appointed by Majority

Shareholders: average 73%, excluding foreign-

domiciled Companies and Directors not elected

with the slate voting system.

• Minority representation in Ftse Mib Companies

fueled the debate at the Italian conference on

Corporate Governance.

• In line with MorrowSodali analysis, it was

revealed that those investors whose weight in the

Italian market significantly increased in recent

years, currently suffer from under-representation.

6 .0 RENE WA L OF THE BOARD

SOME COMMENTS

• Remember that many important Italian

Companies still today allow only one minority

Director.

• Italian Companies should consider amending their

by-laws to strengthen market representation. It is

known that best practice should provide a

minority Shareholder representation ratio not

below a range between 1/4 and 1/3. The ratio

should always be compared to the International

institutional investors’ representation level in

terms of share capital.

Fiduciary’s Duty | 24.02.2017

85,47% 83,70%

73,75% 70,95%

62,07% 56,43% 55,63% 55,08%

49,98% 49,69%

14,45% 9,74%

25,64% 28,96% 37,06%

42,93% 44,20% 44,79% 49,43% 49,32%

0,08% 6,56%

0,61% 0,09% 0,87% 0,64% 0,17% 0,13% 0,59% 0,99%

PosteItaliane

A2A* Buzzi BPER Leonardo ENI Fineco Terna ENEL TelecomItalia

47

2017 BOARD RENEWAL: RESULTS INCLUDING REFERENCE SHAREHOLDERS

Quorum in

terms of

ISC

• The chart below shows the voting results of the FTSE Mib companies that renewed the Board in 2017 in

terms of issued share capital («ISC»).

For instance, concerning Terna the shareholders participation is equal to 63.65% ISC, of which 55.08% supporting Majority Slate,

44.79% supporting Assogestioni Slate and 0.13% Against/Abstain/not Voting.

Average

support of

Majority Slate:

64.27%

6 .0 RENE WA L OF THE BOARD

77.12% 40.19% 63.27% 63.65% 58.78% 58.36% 75.45% 67.43% 81.79% 70.94%

For Majority Slate For Assogestioni Slate Against/Abstain/Not Voting

*in A2A three slates have been presented. Majority and Assogestioni slates are displayed meanwhile the third one is included in Against/abstain/not voting part.

Fiduciary’s Duty | 24.02.2017

31,43% 31,31%

16,89% 16,43% 16,43% 16,43% 16,43% 15,42% 14,70% 12,88%

68,34% 67,12%

81,89% 82,59% 83,25% 82,59% 83,25% 84,34% 83,63% 86,64%

0,23% 1,57% 1,22% 0,99% 0,32% 0,99% 0,32% 0,24% 1,67% 0,48%

BPER Leonardo ENI ENEL Fineco Buzzi A2A Terna TelecomItalia

PosteItaliane

48

2017 BOARD RENEWAL: RESULTS MINORITY SHAREHOLDERS

Minority

Shareholders

Participation

(%ISC)

Average

support of

Majority

Slate: 18.8%

• The chart below shows the voting results of the FTSE Mib companies that renewed the Board in 2017

considering only the participation of minority shareholders in terms of issued share capital («ISC»).

For instance, concerning Leornardo the minority shareholders participation is equal to 37.23% ISC, of which 31.31% supporting

Majority Slate, 67.12% supporting Assogestioni Slate and 1.57% Against/Abstain/not Voting.

6 .0 RENE WA L OF THE BOARD

16.56% 35.18% 23.66% 33.80% 34.42% 12.86% 20.94% 40.06% 33.17% 37.23%

For Majority Slate For Assogestioni Slate Against/Abstain/Not Voting

Fiduciary’s Duty | 24.02.2017

49

CASE STUDY: TELECOM

• On April 16 2014, Telecom’s Shareholders

meeting was called to renew the Company’s

Board for the following three-years term.

• Telecom’s by-laws provided that: 4/5 of the Board

members chosen from the slate receiving the

highest number of votes, 1/5 from minority slates.

• 3 slates submitted:

— Slate 1 (Telco)

— Slate 2 (Findim)

— Slate 3 (SGRs, Institutional Investors).

The outcome of the voting process produced a hardly

foreseeable result:

• Slate 3 obtained 3.780.506.392 votes equal to

28,18%, thereby surpassing the main

Shareholder’s slate, which in theory is considered

to be the majority slate.

6 .0 RENE WA L OF THE BOARD

• Since the slate could not provide 10 elected members

awarded to the majority slate, according to the by-laws

when the voting process had ended, the 3 candidates

present on the majority slate were elected to the Board.

• For the remaining 7 Directors a second voting round

was carried out with the majority thresholds set by law

(i.e. absolute majority of votes in favor). 7 candidates

from Telco were elected while the foreign investors

representation left the Meeting without further

instructions to follow.

• Outcome: Shareholders representing ~20% of share

capital (minority in the Meeting) obtained 4/5 of

seats (majority in the Board); only l/5 of Directors

were elected from slates representing ~80% of

ordinary share capital of Telecom Italia.

Fiduciary’s Duty | 24.02.2017

50

CASE STUDY: UNICREDIT

• On May 13 2015, UniCredit’s Shareholders

Meeting was called to renew the Company’s

Board for the following three-years term.

• Two slates were submitted:

— Slate 1 (Allianz S.p.A. - Aabar Luxembourg

S.a.r.l. - Fondazione Cassa di Risparmio di Torino

- Carimonte Holding S.p.A. - Fincal S.p.A. –

Cofimar S.r.l.).

— Slate 2 (SGRs & institutional investors).

The outcome of the voting process produced a hardly

foreseeable result:

• Slate 1 obtained 1.371.406.336 votes in favor,

equal to 44,18%.

• Slate 2 (the minority shareholders list)

1.694.743.751 votes, equal to 54,60%.

6 .0 RENE WA L OF THE BOARD

The supposedly minority slate received the

majority of the votes. Nonetheless, UniCredit’s by-

laws provides that in case the majority slate does

not include enough candidates to elect the

corresponding number of Directors according to

the voting procedures under letter a), all candidates

from the majority slate will be elected to the

Board, while remaining Directors will be elected

from the minority slate that obtained the highest

number of votes.

The outcome of the aforementioned events was

the election of only one Director from the slate

that obtained 54% of the votes representing the

majority of UniCredit’s share capital.

Fiduciary’s Duty | 24.02.2017

SUPPORT TO L IST PROMOTED BY

THE REFERENCE SHAREHOLDERS

At Generali and Intesa Sanpaolo’s AGMs, those lists

promoted by the reference shareholders, competing

for the majority of the Board seats, have been strongly

supported by the minorities.

51

30,10%

21,21% 23,28%

3,75%

10,38%

14,43%

SNAM GENERALI INTESA

Azionista Strategico Minoranze

9,64%

37,66% 41,15%

Supporto minoranze

SNAM

The list promoted by institutionl investors through

Assogestioni became the majority list, in spite of the

list promoted by the controlling Shareholder.

• Only 3,75% of shares held by institutional

investors supported the list promoted by CDP

Reti.

6 .0 RENE WA L OF THE BOARD

9,64%

37,66% 41,15%

SNAM GENERALI INTESA

Snam Generali IntesaSupport by minorities ••• Reference shareholders ••• Minority

CASE STUDY: THE ELECTION YEAR 2016

Fiduciary’s Duty | 24.02.2017

52

%

6 .0 RENE WA L OF THE BOARD

Morrow Sodali directly surveyed a target of institutional investors to define what information

should be disclosed about Board composition to make an informed vote on director elections

BOARD ELECTION: TRENDS

7.0

···

Board evaluation

Fiduciary’s Duty | 24.02.2017

54

The Board Evaluation process has a key role in

determining and improving the Board effectiveness:

• The Board should undertake a formal and

rigorous annual evaluation of its own

performance and that of its committees.

• An effectiveness objective rather than a

compliance exercise.

• Regular use of an external facilitator could

improve Board evaluations by bringing an

objective perspective and sharing best practices

from other companies.

• Assessing its membership, organisation and

operation as a group, the competence and

effectiveness of each Board member and of the

Board committees.

7 .0 BOARD EVALUAT I O N

CONTEXT

• Assessing how well the board has performed

against any performance objectives set.

• The evaluation should also cover the quality and

timeliness of information received by the board

from the management.

• The board should state in the annual report

how performance evaluation of the Board, its

committees and its individual Directors has been

conducted.

• Outcome of the evaluation, including an action

plan on any necessary improvements increase the

accountability of the Board towards its own

performance, and is therefore expected by the

investor community.

Fiduciary’s Duty | 24.02.2017

55 7 .0 BOARD EVALUAT I O N

REGULATORY FRAMEWORK

Companies should “perform at least annually an evaluation of the performance of the

Board of Directors and its committees, as well as their size and composition, taking

into account the professional competence, experience, (including managerial

experience) gender of its members and number of years as Director. Where the

Board of Directors avails of consultants for such a self assessment, the Corporate

Governance Report shall provide information on their identity and other services, if

any, performed by such consultants to the issuer or to companies having a control

relationship with the issuer”.

CODICE DI AUTODISCIPLINA (1.C 1.G)

Fiduciary’s Duty | 24.02.2017

56

MAIN TRENDS

• 79% of Italian listed companies disclosed that a

Board evaluation has been performed.

• 88 listed companies used questionnaires, only 18

interviews with Directors.

• 92% of FTSE MIB provide disclosure on Board

evaluation (96% financial sector and 100%

insurance).

• FTSE Mib: 14 use questionnaires, 2 interviews, 9

both, 9 disclosed they performed a Board

evaluation without further disclosure on the

process.

7 .0 BOARD EVALUAT I O N

STATISTICS

* Italian Corporate Governance Council Report

EU-US trends

• External facilitator practice on board evaluation is

not factorized inside Italian boardrooms.

• An improvement towards EU-Anglo-Saxons Peers

may resulted in more effective board evaluation.

27%

35%

40%

98%

5%

47%

Italy

France

Uk

US

Russia

South Africa

INDEPENDENT CONSULTANTS FOR THE BOARD EVALUATION

Fiduciary’s Duty | 24.02.2017

57

UNILEVER

“Unilever’s Chairman leads the process whereby the Boards formally assess their own

performance with the aim of helping to improve the effectiveness of the Boards and

their Committees. The evaluation process consists of an internal exercise performed

annually with an independent third-party evaluation carried out at least once every three

years.

In 2012 we engaged an independent governance specialist to advise on our internal

evaluation process and help create three full and confidential online evaluation

questionnaires on our Boards, CEO and Chairman for all Directors to complete. The

detailed Board questionnaire invites comments on a number of key areas including

Board responsibility, operations, effectiveness, training and knowledge. The online

questionnaires were used again in 2013.

In addition, each year the Chairman conducts a process of evaluating the performance

and contribution of each Director which includes a one-to-one performance and

feedback discussion with each Director. The evaluation of the performance of the

Chairman is led by the Vice-Chairman/Senior Independent Director and the Chairman

leads the evaluation of the CEO, both using bespoke questionnaires. Committees of the

Boards evaluate themselves annually under supervision of their respective chairmen

taking into account the views of respective Committee members and the Boards.”

7 .0 BOARD EVALUAT I O N

DISCLOSURE OF THE PROCESS

MAIN TASKS ADDRESSED BY

UNILEVER BOARD

• Independent facilitator

• Questionnaires

• Peers to peers for directors

• Each committee Board

evaluation

Fiduciary’s Duty | 24.02.2017

58

BARCLAYS

“From the Board’s discussion of the review’s findings, the following areas for

action were agreed:

[…]

Greater awareness of the work of Board Committees: we agreed to give more

time, on a rolling basis, to Board Committee reporting to the Board, to allow all

Directors to gain a deeper understanding of the workings of each Board

Committee and their forward agendas;

Improvements to the Board appointments process: given the number of recent

changes to the Board, we agreed to ensure that all Board members are kept fully

informed of prospective candidates and potential appointments; and

Director induction: we agreed to improve the on-boarding process for new

Directors, including partnering new Directors, if appropriate, with longer-serving

Board members”.

7 .0 BOARD EVALUAT I O N

DISCLOSURE OF OUTCOME

IMPROVEMENTS

HIGHLIGHTED BY BARCLAYS

BOARD

• Functioning of Committees

• Board appointments

process

• Induction effectiveness

8.0

···

Succession Plans

Fiduciary’s Duty | 24.02.2017

60

ITALY**

• In 2015, only 20 Companies have adopted

executive succession plans.

• The number is constant since 2014; it has

increased from 2013 (16 Companies) and 2012 (7

Companies).

• Disclosure of succession plan adoption has

improved among the FTSE MIB Companies.

• Information about the existence of the plans is

provided in Ftse Mib from 100% of the

Companies, representing an increase compared to

previous years.

8 .0 SUCCE S S I O N PLANS

CONTEXT

*Extract from Deloitte “Board Practices reports 2014” - ** Assonime “Corporate Governance in italia 2014 ”

US*

• Us Companies have introduced succession plans.

• 58% of large cap companies review their CEO

succession plans yearly, while 32% review these

twice a year.

• At 30% of the companies the Board has full

responsibility for succession planning, at 29% the

responsibility is on the Compensation Committee,

at 21% on the Nomination/Corporate Governance

Committee and at 2% of the companies on the

independent Directors.

Issue: Succession plans seem insufficiently

structured/clear about who is performing the

planning. Meantime, investors call for involvement

of the entire Board in the process as well as more

clarity about the timeframe of the process.

Fiduciary’s Duty | 24.02.2017

61 8 .0 SUCCE S S I O N PLANS

SAMPLE

9.0

···

Board Induction

Fiduciary’s Duty | 24.02.2017

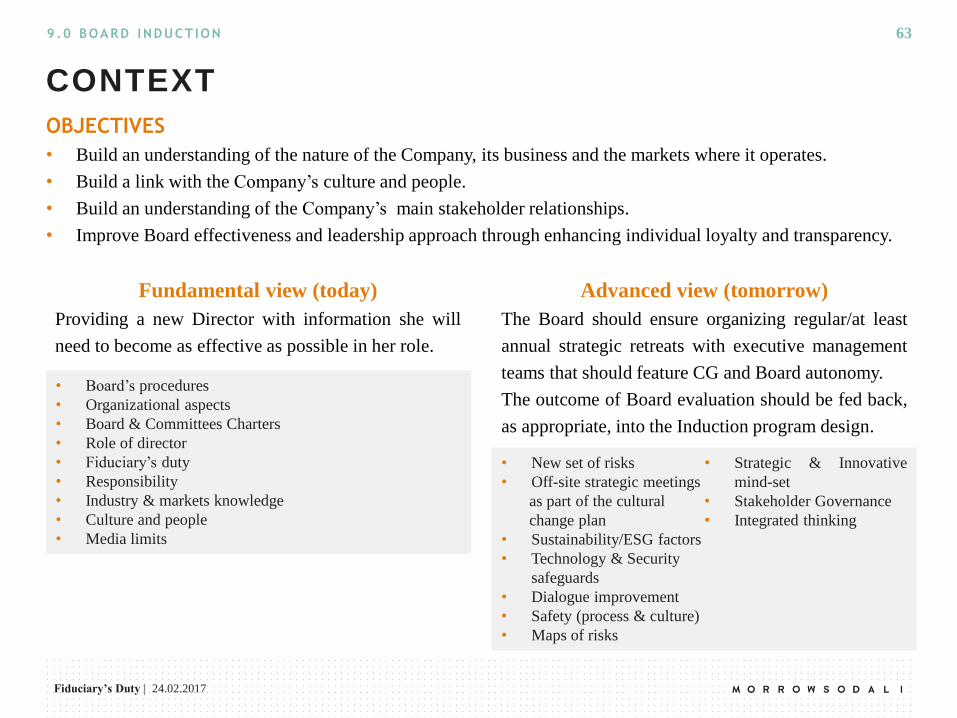

Advanced view (tomorrow)

The Board should ensure organizing regular/at least

annual strategic retreats with executive management

teams that should feature CG and Board autonomy.

The outcome of Board evaluation should be fed back,

as appropriate, into the Induction program design.

63

OBJECTIVES

• Build an understanding of the nature of the Company, its business and the markets where it operates.

• Build a link with the Company’s culture and people.

• Build an understanding of the Company’s main stakeholder relationships.

• Improve Board effectiveness and leadership approach through enhancing individual loyalty and transparency.

9 .0 BOARD INDUCT ION

CONTEXT

• Board’s procedures

• Organizational aspects

• Board & Committees Charters

• Role of director

• Fiduciary’s duty

• Responsibility

• Industry & markets knowledge

• Culture and people

• Media limits

• New set of risks

• Off-site strategic meetings

as part of the cultural

change plan

• Sustainability/ESG factors

• Technology & Security

safeguards

• Dialogue improvement

• Safety (process & culture)

• Maps of risks

• Strategic & Innovative

mind-set

• Stakeholder Governance

• Integrated thinking

Fundamental view (today)

Providing a new Director with information she will

need to become as effective as possible in her role.

10.0

···

Remuneration policy

Fiduciary’s Duty | 24.02.2017

65

CONTEXT & RECENT TRENDS

• A general but louder voice in executive

compensation without micro-management.

• Board and Compensation Committee engagement

with Shareholders ahead of the General Meeting.

• Alignment of Director interests with Shareholder

interests through adopting stock ownership

guidelines.

10 .0 REMUNE R AT IO N POL ICY

• Substantial and easy-to-understand disclosure of

pay to permit benchmarking by Shareholders.

• Independent Compensation Committee.

• Pay linked to performance and long-term value

creation for Shareholders.

• Top Management retention and talent attraction.

• Compensation reports should be written by the

Board and should explain how the compensation

program’s structure, performance metrics and

goals are designed to incentivize executives,

achieve business goals and maximize value

creation for Shareholders.

Fiduciary’s Duty | 24.02.2017

NON-EXECUTIVE COMPENSATION

• Review the best way to incentivize non-

executive Directors for increasing

responsibilities, time and duties dedicated to the

Board?

• Involvement of Directors should be 360°: inside

the boardroom and outside towards all identified

stakeholders.

• Less Directorships, more time dedicated to one

/few Boards and rewards aligned with time

commitment?

66

COMPENSATION – CONTEXT

EXECUTIVE COMPENSATION

• Executive compensation is still among the top key

concerns for the investor because it requires

alignment between the Management and the

Shareholders’ interests.

• Whilst the work of the Compensation Committee,

it is a responsibility of the whole Board.

A vote against the Remuneration Report is a

vote against the Board

• Increasing share of pay being at risk, in the form

of long-term compensation based on

performance rather than time-based.

Most of the compensation committees spend the

large majority of time on compensation, but

should also consider:

— management/leadership development

— succession planning.

10 .0 REMUNE R AT IO N POL ICY

Fiduciary’s Duty | 24.02.2017

67

%

10 .0 REMUNE R AT IO N POL ICY

Morrow Sodali directly surveyed a target of institutional investors to rank the issues in executive

remuneration from the most important to the least important

REMUNERATION: TRENDS

Fiduciary’s Duty | 24.02.2017

68

%

10 .0 REMUNE R AT IO N POL ICY

Morrow Sodali directly surveyed a target of institutional investors to define how important is it

for Remuneration Committees to disclose its decision-making process when defining executive

pay including the rationale for deciding on the structure and magnitude of overall executive pay

REMUNERATION COMMITTEE: TRENDS

Fiduciary’s Duty | 24.02.2017

DISCLOSURE

• Provide useful and easy-to-understand disclosure

of Company pay practices and decisions.

• Comprehensive, timely and transparent disclosure

of executive pay.

• Disclosure of individual executive and non-

executive Director compensation.

• Clearly explain the key decisions of the

Compensation Committee and their motivation.

• Clearly disclose and justify the performance

measures adopted and the related targets.

• Disclose the maximum amount of variable

compensation which can be paid to executive

Directors.

• Summarize the changes from the prior year.

69

COMPENSATION – BEST PRACTICES

PRINCIPLE

• Alignment to sustainable, long-term value

creation for Shareholders and stakeholders.

• Linking variable compensation with Company’s

financial and non-financial performance.

• Mix of performance-based short- and long-term

incentives.

• Rigorous objective targets corresponding to

results with a corresponding decrease in incentive

opportunity.

• Avoid significant retention awards without

assigning performance conditions.

• Maintain an independent and effective

compensation Committee, preferably fully

independent.

• Identify appropriate peer groups for performance

comparisons.

10 .0 REMUNE R AT IO N POL ICY

Fiduciary’s Duty | 24.02.2017

70

INTEGRATED APPROACH TO COMPENSATION

BOARD, REM.CO AND HR – A NEW ROLE

• Holistic approach to compensation decision-

making process.

• Internal optimal coordination: Board/Rem.Co -

Investor Relations/Legal - Human Resources.

• External market considerations - investor

engagement - stakeholder considerations.

• Ensure Company internal pay alignment as well

as responding to external stakeholder

requirements.

• Take into account the social context.

• Board becoming a driver to implement an

integrated thinking inside and outside of the

Boardroom.

• Drive the Board versus a holistic approach to

Shareholders through regular Engagement.

10 .0 REMUNE R AT IO N POL ICY

Fiduciary’s Duty | 24.02.2017

71

SHRD DIRECTIVE: UPDATE

Under the new rules, remuneration policy should

contribute to the business strategy, long-term interests

and sustainability of the company and should not be

linked to short-term objectives.

Directors' performance should be assessed using both

financial and non-financial performance criteria,

including where appropriate environmental, social

and governance factors.

Article 9a shareholder have the right to vote on the

remuneration policy at the general meeting( Member

States shall ensure that the vote by the shareholders at

the general meeting on the remuneration policy is

binding, however is possible to opt for an advisory

vote).

Shareholders will also have a right to vote on the

annual report on pay (art 9b).

Although is not establish a Ceo pay ratio the report

include “the annual change of remuneration, of the

performance of the company, and of average

remuneration on a fulltime equivalent basis of

employees of the company other than directors over at

least the five most recent financial

years, presented together in a manner which permits

comparison”.

10 .0 REMUNE R AT IO N POL ICY

Fiduciary’s Duty | 24.02.2017

72

GLOBAL CONTEXT OF “SAY ON PAY”

COUNTRY YEAR

ADOPTED* DIRECTORS OR

EXECUTIVES PAY POLICY OR STRUCTURE BINDING OR ADVISORY FREQUENCY

REQUIRED OR

VOLUNTARY

Spain 2014 Directors Pay Policy, Pay Structure Binding, Advisory Annually Required

France 2013 Executives Pay Policy, Pay Structure Binding, Advisory Annually Required

The Netherlands 2004 Executives Pay Policy Binding Upon Changes Required

Australia 2005 Directors Pay Structure Advisory Annually Required

Sweden 2006 Executives Pay Policy Binding Annually Required

Norway 2007 Executives Pay Policy Binding Annually Required

Denmark 2007 Executives Pay Policy Binding Upon Changes Required

United States 2011 Executives Pay Structure Advisory

Annually/

Biennially/

Triennially

Required

United Kingdom 2013 Directors Pay Policy, Pay Structure Binding, Advisory Annually Required

Switzerland 2013 Directors Pay Policy Binding Annually Required

Germany None Executives Pay Structure Advisory Annually Voluntary

Canada None Executives Pay Structure Advisory Annually Voluntary

10 .0 REMUNE R AT IO N POL ICY

Fiduciary’s Duty | 24.02.2017

• No empirical evidence yet.

• Regulation vs “Comply-or-explain” model.

• Complex matter affected by Company-specific

circumstances, market requirements and

willingness of Shareholders to commit resources.

• Substantial diversity in cultural approach to

compensation.

• Uncertainty where to go at Regulatory level.

• Controversial role of Proxy Advisory firms.

• Positive three-year trend (2012-2016) in FTSE

Mib company compensation results.

73

THE CURRENT DEBATE ON “SAY ON PAY”

What is more beneficial to financial

markets: a binding vote or an advisory

vote on pay?

10 .0 REMUNE R AT IO N POL ICY

Fiduciary’s Duty | 24.02.2017

74

MORROW SODALI SURVEY ON SAY-ON-PAY

QUESTION 11

In Say-on-Pay proposals, what negative vote should cause Directors to amend the

compensation plan? (Please choose one option only)

> 5%

3%

> 10%

21%

> 15%

28%

> 20%

28%

> 30%

21%

• According to 28% of investors, Companies

should consider amending the compensation

plan when they receive >15% of votes against

their say on pay (SOP) policy.

• A further 28% of investors suggests that changes

should be made when receiving more than

20% votes against the SOP.

10 .0 REMUNE R AT IO N POL ICY

Fiduciary’s Duty | 24.02.2017

75

%

10 .0 REMUNE R AT IO N POL ICY

Morrow Sodali directly surveyed a target of institutional investors to define the preference on the

Pay policy or rather, actual Pay-related decisions taken during the period under review (i.e.

Compensation report), or both

SAY ON PAY: TRENDS

Fiduciary’s Duty | 24.02.2017

The boxes below show the average level of support to Remuneration Policies proposed by FTSE Mib Companies

and the related average level of positive and negative recommendation issued by ISS.

The negative recommendations are often based on the following criteria:

• lack of disclosure

• excessive severance payments

• lack of disclosure on performance criteria for STI or LTI plans

• absence of risks adjustments mechanism.

76

RESULTS

Average level of

support to

Remuneration policies

on FTSE MIB

Level of positive

recommendation by

ISS (FTSE Mib).

88% 62.5%

37.5%

Level of negative

recommendation by

ISS (FTSE Mib).

REMUNERATION POLICY - FTSE MIB 2017

10 .0 REMUNE R AT IO N POL ICY

Fiduciary’s Duty | 24.02.2017

77

THE AGM RESOLUTIONS: REMUNERATION

POLICY

There has been a decreasing support for the FTSE MIB Companies’ Remuneration policies from the main proxy

advisor (ISS) in comparison with the previous two years.

62,5% 71,4% 68,8%

37,5% 28,6% 31,3%

0%

10%

20%

30%

40%

50%

60%

70%

80%

2017 2016 2015

FOR AGAINST

ISS - FTSE MIB (2017-2015)

10 .0 REMUNE R AT IO N POL ICY

Fiduciary’s Duty | 24.02.2017

78

PROXY ADVISORS AND SAY ON PAY

France and Italy registered high levels of concern during the last proxy season. Major issues still pertain to ex-

ante/post disclosure for targets and magnitude of severance agreements.

19,0%

41,0%

57,0% 62,5%

0,0 %

10, 0%

20, 0%

30, 0%

40, 0%

50, 0%

60, 0%

70, 0%

UK Spain France Italy

10 .0 REMUNE R AT IO N POL ICY

Fiduciary’s Duty | 24.02.2017

79

REMUNERATION PROPOSALS – ITALIAN

METRICS FTSE MIB - M INORITY SUPPORT (2017 -2015)

The approval rates in FTSE MIB Companies have decreased in comparison with the last two years.

69,4% 75,9% 75,2%

30,6% 24,1% 24,8%

0,0 %

10, 0%

20, 0%

30, 0%

40, 0%

50, 0%

60, 0%

70, 0%

80, 0%

90, 0%

100 ,0%

2017 2016 2015

FOR AGAINST/ABSTAIN

10 .0 REMUNE R AT IO N POL ICY

Fiduciary’s Duty | 24.02.2017

80

THE CONTEXT – INCLUDING REFERENCE SHAREHOLDERS

• The average approval rate is 88.1%.

• In fourteen cases, the support has been >95%.

• In four cases, the support has been <70%.

• In no case, the remuneration policy has been rejected.

SAY ON PAY APPROVAL RATES

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

For Against Abstain

10 .0 REMUNE R AT IO N POL ICY

Fiduciary’s Duty | 24.02.2017

81

THE CONTEXT

• The average approval rate is 69.4%.

• In eleven cases, the support by minority investors has been >90%.

• In nine cases, the support by minority investors has been <50%, proving a mis-alignment to market

expectations.

MINORITY SHAREHOLDERS VOTE ON SAY ON

PAY

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

For - Minority Shareholders Against - Minority Shareholders Abstein - Minority Shareholders

10 .0 REMUNE R AT IO N POL ICY

Fiduciary’s Duty | 24.02.2017

82

The chart below shows the average consensus expressed by Minority Shareholders in the last three years.

The blue line represents the average level of overall consensus including the reference shareholders, while the red

line only takes into account the consensus expressed by the minority shareholders on the remuneration report.

MINORITY SHAREHOLDERS: AVERAGE

SUPPORT ( 2 0 1 7 - 2015 )

20%

30%

40%

50%

60%

70%

80%

90%

100%

Average 2015-2017 Average 2015 - 2017 (only Minority Shareholders)

10 .0 REMUNE R AT IO N POL ICY

Fiduciary’s Duty | 24.02.2017

83

REMUNERATION PROPOSALS – US CONTEXT

SAY-ON-PAY-APPROVAL RATES IN 2015 *

Of the 94 Top 100 Companies that held a say-on-pay vote in 2015,

77% received approval rates in excess of 90% and 7% received

approval rates below 70%.

*Approval rates are calculated on the ratio of votes «for» over the sum of votes cast plus abstention, as reported in SEC filings.

10 .0 REMUNE R AT IO N POL ICY

11.0

···

AGM preparation:

why?

Fiduciary’s Duty | 24.02.2017

85

AGM PREPARATION & PLANNING

RECOMMENDATIONS FOR

COMPANIES

• Check the logistics of cross-border voting -

regulatory deadlines, unbundling, ADR votes, other

barriers to voting.

• Engagement with Proxy Advisors – act beforehand

to prevent negative recommendations.

• Engagement with investors: selection, access to the

right contact ("split-brain disease", comparison with

IR contact).

• Set a direct communication plan with investors to

neutralize potential activist behavior.

• Propose alternatives to the Board before publication

– estimate in advance the impact of the decision,

evaluate vulnerabilities, plan of action to maximize

support.

• Controlled “mobilization" of the Shareholders.

11 .0 AGM PREPARA T I O N: WHY?

Fiduciary’s Duty | 24.02.2017

86

STAKEHOLDER GOVERNANCE – CONTEXT

Companies increasingly face complex uncertainties

and risks related to Governance issues, but also

related to social, environmental and, generally,

Stakeholder issues.

• An Integrated approach is called for - Boards

have the responsibility of shaping the culture,

both within the boardroom and across the

organization as a whole, embedding good

corporate behavior.

• Board efforts should embrace a more strategic

and coordinated approach that pursues

transformational goals:

— effectively streamlining this approach within

the organization

— engaging multiple stakeholders as

management, employees, Shareholders,

competitors, suppliers, governments, and NGOs

— increasingly focusing on transformational,

strategic results.

Boards and Directors should re-think their

leadership-role, stakeholder governance and

integrated-thinking.

11 .0 AGM PREPARA T I O N: WHY?

Fiduciary’s Duty | 24.02.2017

87

STAKEHOLDERS – INSTITUTIONAL INVESTORS

RECOMMENDATIONS FOR

COMPANIES

Paul Polman – Ceo Unilever: “… to attract the right

longer-term Shareholders to our register”.

• Integrated Governance

• Sustainable growth over the long-term

• Re-consider earnings guidance

• Long-term cultural change

• Holistic approach to Shareholders

Board transparency is the most effective

form of prevention from activism and to

attract right longer-term Shareholders.

11 .0 AGM PREPARA T I O N: WHY?

Many other companies as Glaxo Smithkline or

General Electric decided to apply such cultural

change and devote more efforts in managing

efficiently their Shareholders trough periodic

engagement.

• Boards should be far more active in facilitating

dialogue with major long-term Shareholders.

• Boards need to regularly communicate the

company’s long-term strategy and performance to

key long-term Shareholders. This is the most

effective way to alleviate the pressure to

maximize short-term returns.

• The more powerful discussions occur when

Companies strive to communicate their strategies

for longer-term growth and their key metrics for

it, besides single-minded governance issues (such

as pay).

• Dialogue gives Directors the context and

confidence to carry out their fiduciary duty.

• Therefore there must be two-way communication

• Engagement.

Fiduciary’s Duty | 24.02.2017

88

ANTICIPATE INVESTORS ’ DISSENT

11 .0 AGM PREPARA T I O N: WHY?

AGM

• Shareholders Identification

• Voting policy analisys

• GAP analysis

INTELLIGENCE

• Proxy Advisor

• SRI Rating Agencies

• Institutional investors

PERCEPTION • Identify critical

factors

• Improvement plan

• Voting projection

STRATEGY

• Proxy Advisor

• Institutional investors

ENGAGEMENT

12.0

···

The engagement with Institutional

Investors

Fiduciary’s Duty | 24.02.2017

90

BOARD ENGAGEMENT VS INVESTORS

THE ADVANTAGES

• Mitigate Proxy Advisor influence

• Get an external perception of the Company, its

governance model and the management

• Get warning signal connected to potential

dissident actions

• Improve the governance level aligning to best

practices promoted by Shareholders

• Strengthen the Board authority versus its

Shareholders

• Better understanding of investors’ requests

mitigating the risks of activism.

12 .0 THE ENGAGE M E NT WITH INST ITU T I ON AL INVEST OR S

Fiduciary’s Duty | 24.02.2017

• • •

“We believe constructive

engagement regarding relevant

issues such as financial

performance, strategy, governance

and executive compensation

practices among shareholders, their

research providers and public