Embed Size (px)

Citation preview

By

Dr. Paul Cottrell

March 14, 2016

The 2016 International Meeting of the Academy of

Behavioral Finance & Economics

Dynamic Hedging Oil and Currency Futures Using

Receding Horizontal Control and Stochastic

Programming

Title

Chapter 1

• Introduction to the Study

Chapter 2

• Literature Review

Chapter 3

• Research Method

Chapter 4

• Results

Chapter 5

• Discussions, Conclusions, and Recommendations

Outline

Chapter 1 - Purpose

The purpose of this research is to fill the gaps in

the literature by providing a comprehensive study

on how to utilize and improve the performance of

the receding horizontal control and stochastic

programming (RHCSP) method pertaining to the

oil and currency markets.

Chapter 1 - Background

• Many investors were negatively affected by the financial crisis

of 2008.

• Many asset types fall together in a financial crisis creating

negative returns for investors.

• During a financial crisis the energy and currency markets

usually exhibit high volatility

• As geo-political instability increases and energy supplies

disrupted future prices also exhibit high volatility.

• The real-world problem is how to offset falling asset prices in a

dynamic way?

• There is a lack of scholarly literature, research, and

understanding in the area of hedging future contracts,

especially in illiquid or very volatile market conditions.

There is a lack of understanding for the reasons of

volatility in the oil or currency futures markets and how to

risk manage those volatility dynamics.

Chapter 1 - Problem Statement

Chapter 1 - Significance

• To improve portfolio performance in the oil and currency

markets and possible protection from black swan effects.

• RHCSP could be a better risk management tool for investors

and the banking industry.

• This study lends itself to how to reduce volatility epochs.

• In theory, governments might be able to use the RHCSP

techniques to smooth out price swings.

Similar to how the Federal Reserve affects interest rates.

Question #1:

Can the RHCSP hedging method improve hedging error compared to

the Black–Scholes, Leland, Whalley and Wilmott methods when

applied to a simulated market, oil futures market, and currency

futures market?

Chapter 1 - Research Questions

Question #2:

Can a modified RHCSP method significantly reduce hedging

error under extreme market illiquidity conditions when applied

to a simulated market, oil futures market, and currency futures

market?

Chapter 1 - Research Questions

Null Hypothesis:

There are no significant differences in hedging error among

RHCSP, modified RHCSP, Black–Scholes, Leland, Whalley

and Wilmott methods when applied to a simulated market, oil

futures market, and currency futures market.

Alternative Hypothesis:

There are significant differences in hedging error among

RHCSP, modified RHCSP, Black–Scholes, Leland, Whalley

and Wilmott methods when applied to a simulated market, oil

futures market, and currency futures market.

Chapter 1 - Null and Alternative Hypothesis

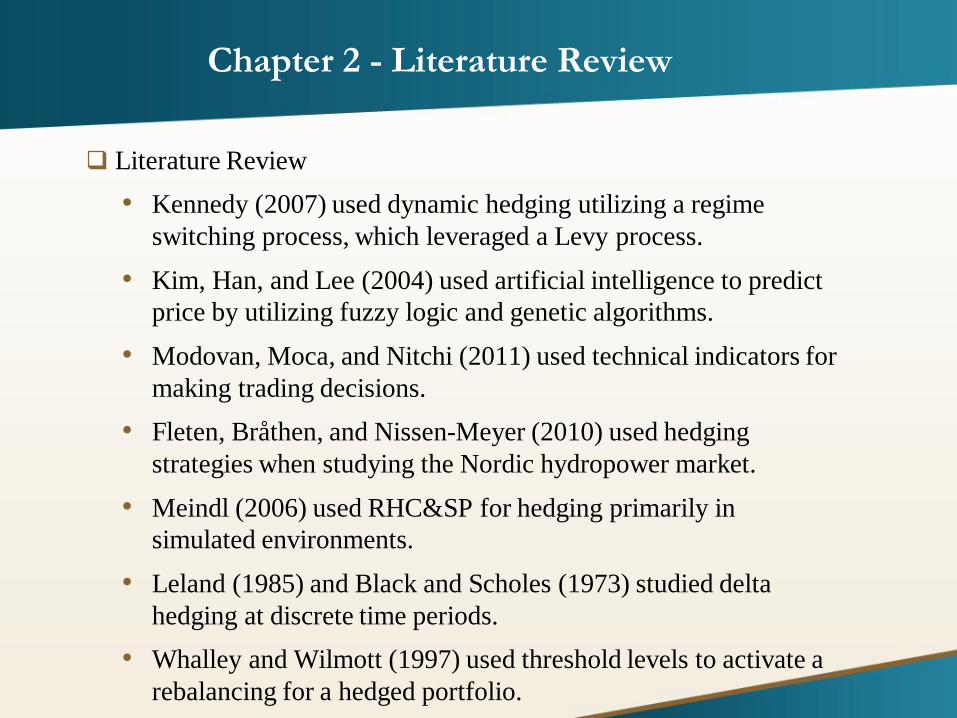

Literature Review

• Kennedy (2007) used dynamic hedging utilizing a regime

switching process, which leveraged a Levy process.

• Kim, Han, and Lee (2004) used artificial intelligence to predict

price by utilizing fuzzy logic and genetic algorithms.

• Modovan, Moca, and Nitchi (2011) used technical indicators for

making trading decisions.

• Fleten, Bråthen, and Nissen-Meyer (2010) used hedging

strategies when studying the Nordic hydropower market.

• Meindl (2006) used RHC&SP for hedging primarily in

simulated environments.

• Leland (1985) and Black and Scholes (1973) studied delta

hedging at discrete time periods.

• Whalley and Wilmott (1997) used threshold levels to activate a

rebalancing for a hedged portfolio.

Chapter 2 - Literature Review

Literature Gap

• Comprehensive study on how to utilize the performance of the

RHCSP method pertaining to oil and currency markets.

• Hedging performance in the full boom-bust-recovery cycle.

• Dynamic hedging strategies in an illiquid market.

• Hedging performance in the financial crisis of 2008.

• The utilization of London interbank offered rate (LIBOR) and

the Levy process to improve a dynamic hedging strategy.

Chapter 2 - Literature Gap

• Chaos theory and emergence

Oil and currency markets are nonlinear systems that

exhibit chaotic attributes (Mastro, 2013, p. 295).

To reduce portfolio variance, due to possible price

swings in the futures market, it is common practice to

implement a hedging strategy (Taleb, 1997, p. 3).

• Research used in this study pertains to risk management

techniques in corporate finance, but applies the assumption

that markets are not efficient because investors are not utility

maximizing throughout the whole investment time horizon.

Chapter 2 - Theoretical Foundation

Chapter 3 - Research Methodology

• Longitudinal quantitative method utilizing an

experimental design with simulated and historical asset

prices.

Chapter 3 - Research Design

• Two methods are utilized

Simulation

Historical backtesting

• Simulation method

To determine, in a stochastic simulated environment,

which hedging method performs the best in terms of

hedging error.

• Historical backtesting

To determine, in a real-world environment, which

hedging method performs the best in terms of hedging

error for the light sweet crude and EUR/USD future

contracts.

• Bias

Large price swings can produce biased averages.

Point of this research is not to eliminate outliers and to use simple averages to

determine hedging error in real-world conditions.

• Internal validity threat

Measuring instrument

o Simulation and historical backtesting should have similar hedging error

characteristics.

• External validity threat

Particular market relevance and application to the whole boom-bust cycle of

asset markets.

o This study uses two different asset classes and evaluates the hedging

performance through a boom-bust cycle.

• Ethics

Only using simulated and historical datasets of asset prices.

o No special ethical concern required.

Chapter 3 - Bias, Threats to Validity, and Ethics

• Stochastic simulation (primary sampling)

One price curve produced using the De Grawue and

Grimaldi (2006) model.

506 4-day average returns calculated

o Equals 8 years of daily returns

• Historical data (secondary sampling)

From datasets on light sweet crude and EUR/USD future

contracts.

506 4-day average returns calculated

o Equals 8 years of daily returns

January 1, 2005 to December 31, 2012

Chapter 3 - Sampling

Independent Variables:

• Two variables

Three markets

o Simulated, oil, and currency

Five Hedging method

o Black–Scholes

o Leland

o Whalley and Wilmott

o RHCSP

o Modified RHCSP

Dependent Variable:

• Absolute hedging error

Chapter 3 - Statistical Analysis

Research Question #1 and #2

• Two-way ANOVA

• Post hoc Tukey testing

• F-test and t-test

• Using 4-day absolute hedging error

Chapter 3 - Statistical Analysis

• Primary and secondary data

• SPSS

• 95% confidence interval, alpha value of 0.05

• Effect size 0.20

• Power 0.95

• With a sample size of 506 of hedging error calculations

Chapter 3 - Statistical Analysis

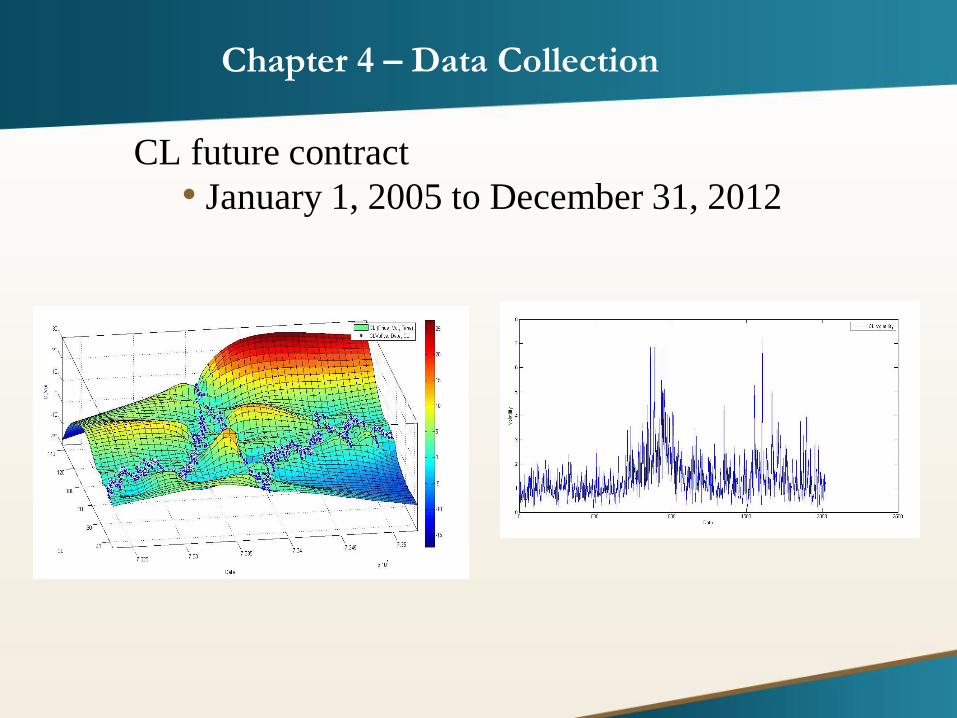

CL future contract

• January 1, 2005 to December 31, 2012

Chapter 4 – Data Collection

6E future contract

• January 1, 2005 to December 31, 2012

Chapter 4 – Data Collection

Simulated market

• January 1, 2005 to December 31, 2012

Chapter 4 – Data Collection

• Hedging error was calculated

For each hedging method

506 absolute hedging errors calculated

oA single sample was generated by

average of four daily absolute hedging

errors.

o Absolute hedging error

Value of position leg – Value of

hedged leg.

Chapter 4 – Data Collection

Chapter 4 – Descriptive Statistics

Chapter 4 – Results

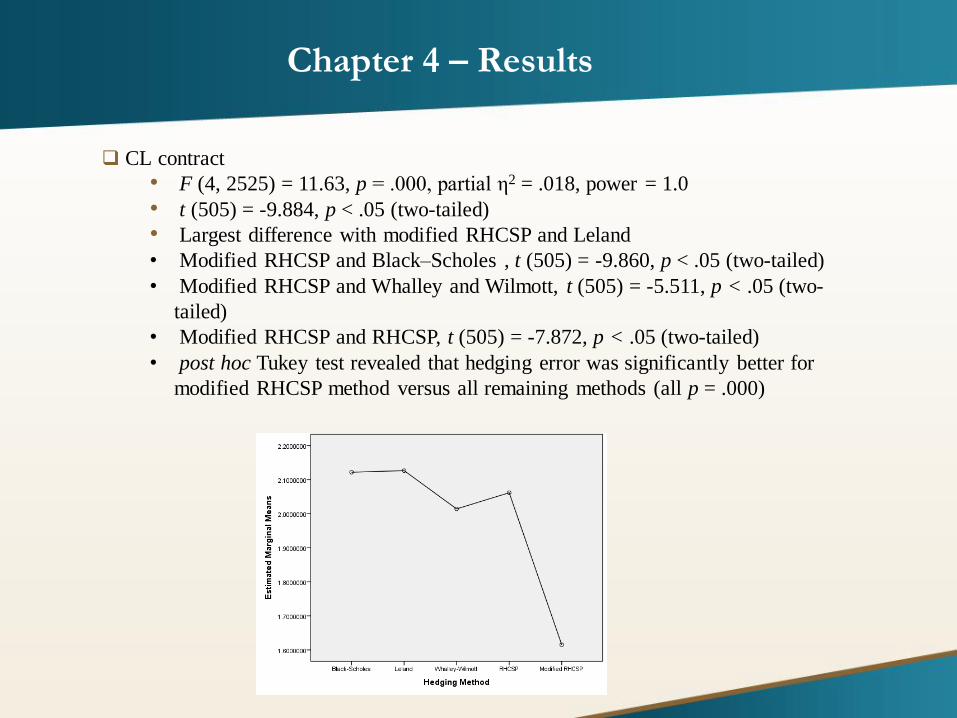

CL contract

• F (4, 2525) = 11.63, p = .000, partial η2 = .018, power = 1.0

• t (505) = -9.884, p < .05 (two-tailed)

• Largest difference with modified RHCSP and Leland

• Modified RHCSP and Black–Scholes , t (505) = -9.860, p < .05 (two-tailed)

• Modified RHCSP and Whalley and Wilmott, t (505) = -5.511, p < .05 (two-

tailed)

• Modified RHCSP and RHCSP, t (505) = -7.872, p < .05 (two-tailed)

• post hoc Tukey test revealed that hedging error was significantly better for

modified RHCSP method versus all remaining methods (all p = .000)

Chapter 4 – Results

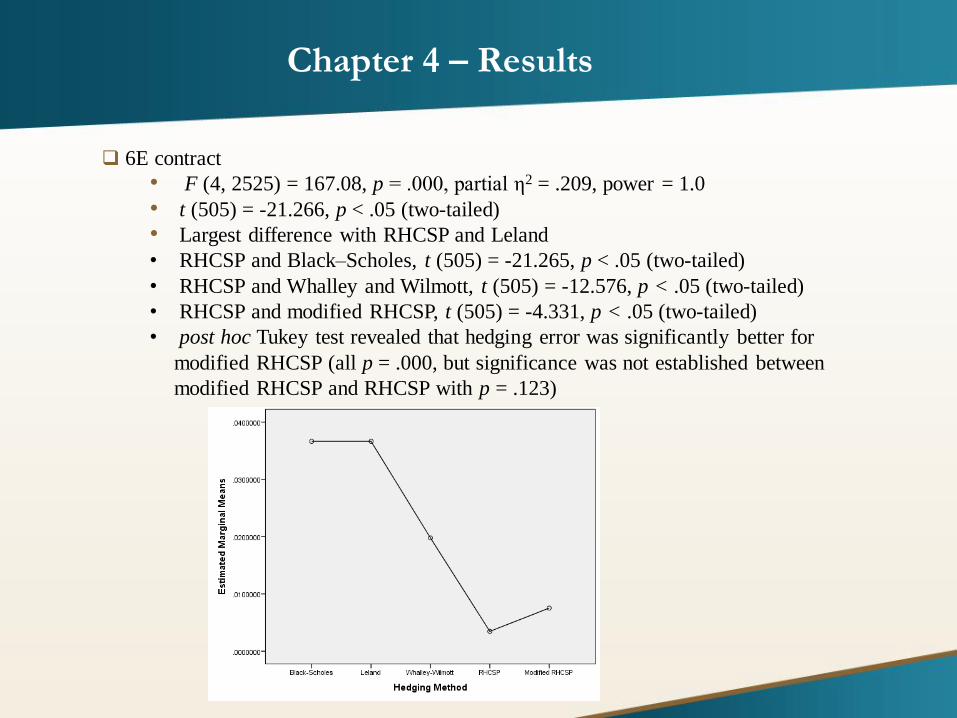

6E contract

• F (4, 2525) = 167.08, p = .000, partial η2 = .209, power = 1.0

• t (505) = -21.266, p < .05 (two-tailed)

• Largest difference with RHCSP and Leland

• RHCSP and Black–Scholes, t (505) = -21.265, p < .05 (two-tailed)

• RHCSP and Whalley and Wilmott, t (505) = -12.576, p < .05 (two-tailed)

• RHCSP and modified RHCSP, t (505) = -4.331, p < .05 (two-tailed)

• post hoc Tukey test revealed that hedging error was significantly better for

modified RHCSP (all p = .000, but significance was not established between

modified RHCSP and RHCSP with p = .123)

Chapter 4 – Results

Simulated market

• F (4, 2525) = 343.31, p = .000, partial η2 = .352, power = 1.0

• t (505) = -47.026, p < .05 (two-tailed)

• Largest difference with Leland and modified RHCSP

• Leland and Black–Scholes , t(505) = -1.00, p > .05, not significant, (two-tailed)

• Leland and Whalley and Wilmott, t(505) = -16.027, p < .05, (two-tailed)

• Leland and RHCSP, t(505) = -10.660, p < .05, (two-tailed)

• post hoc Tukey test revealed that hedging error was significantly better for Black–Scholes

and the Leland methods (all p = .000)

• Oil market

Modified RHCSP method significantly reduced

hedging error compared to hedging methods

investigated.

• Currency market

Either RHCSP or modified RHCSP significantly

reduced hedging error compared to other hedging

methods investigated.

• Simulated market

Black–Scholes or Leland methods performed

significantly better compared to the other methods

investigated.

Chapter 5 – Key Findings

Chapter 5 – Interpretations of Findings

• The volatility of the oil and currency markets can be tamed by using

the modified RHCSP method

• Dynamic hedging can help reduce return volatility and reduce

contingency claim risk.

• Investors can cap their risk by utilizing a dynamic hedging strategy

implemented with a modified RHCSP method.

• The modified RHCSP method works well in heteroskedastic

markets, but not in homoskedastic markets.

• When using a Levy process and LIBOR in the objective function,

significant reduction of hedging error is achieved in the oil and

currency markets.

Chapter 5 – Limitation of the Study

• Real-world data

Only the CL oil contract and 6E currency contracts

were studied.

• Studied homoskedastic simulation data.

• Other assets and a wider time period should be

investigated to strengthen external validity.

Chapter 5 – Future Research

Investigating modified RHCSP in

• Bond markets

reducing yield curve risk

• Natural gas futures

extremely volatile market

• Other major currency pairs

GBP/USD, USD/JPY, GBP/JPY

• Increase time frame of study

30-year history

• Uses regarding quantitative easing by a central bank.

Visualization tools utilizing modified RHCSP

• Neural network diagrams of systemic risk.

A better risk control on investment portfolios and how to

benefit from high volatility in markets, instead of being a

casualty of financial crises.

Risk managers can reduce counterparty risk in the oil and

currency markets by utilizing the modified RHCSP.

A possible framework for central banks to implement a

more stable monetary policy.

Can be utilized in software development which specializes

in financial trading.

Chapter 5 - Social Change Implications

Black, F., & Scholes, M. (1973). The valuation of options and corporate liabilities. Journal of Political Economy, 81(1), 637-654.

De Grauwe, P., & Grimaldi, M. (2006). The exchange rate in a behavioral finance framework. Princeton, NJ: Princeton University

Press.

Fleten, S. E., Bråthen, E., & Nissen-Meyer, S. E. (2010). Evaluation of static hedging strategies for hydropower producers in the

Nordic market. The Journal of Energy Markets, 3(4), 3-30.

Kennedy, J.S. (2007). Hedging contingent claims in markets with jumps. (Doctoral dissertation). Retrieved from ProQuest

Dissertations and Theses. (Accession Order No. NR35132)

Kim, M. J., Han, I., & Lee, K.C. (2004). Hybrid knowledge integration using the fuzzy genetic algorithm: Prediction of the Korea

stock price index. Intelligent System in Accounting, Finance and Management, 12(1). 43-60.

Leland, H.E. (1985). Option pricing and replication with transactions costs. The Journal of Finance, 15(5), 1283-1301.

References

Mastro, M. (2013). Financial derivative and energy market valuation: Theory and implementation in Matlab. Hoboken, NJ:

John Wiley & Sons, Inc.

Meindl, P. J. (2006). Portfolio optimization and dynamic hedging with receding horizon control, stochastic, and Monte Carlo

simulation (Doctoral dissertation). Retrieved from ProQuest Dissertations and Theses. (Accession Order No. 3242594)

Modovan, D., Moca, M., & Nitchi, Ş. (2011). A stock trading algorithm model proposal, based on technical indicators signals.

Informatica Economică (15)1, 183-188.

Taleb, N. (1997). Dynamic hedging: Managing vanilla and exotic options. New York, NY: John Wiley & Sons, Inc.

Whalley, A. E., & Wilmott, P. (1997). An asymptotic analysis of an optimal hedging model for option pricing with transaction

costs. Mathematical Finance, 7(3), 307-324.

References