Embed Size (px)

Citation preview

November 2014

Europe Outlook

Europe Outlook, November 2014

Section 1

Slow motion recovery and bumpy road ahead

Section 2

The drivers of growth: further policy measures to prevent headwinds

Section 3

Forecast: downward revision

Section 4

Some imbalances have been corrected, but the growth potential is reduced

Annex

Country breakdown

Index

Page 2

Europe Outlook, November 2014

Main messages

Page 3

1

2

The global expansion goes on slower than expected except in the US (and Mexico)

The likelihood of the risk scenario increases due to geopolitical risks and the lower traction of support policies

Volatility, extremely low until now, has increased a bit, quickly over a very short period. Warrants monitoring

Global GDP growth (%) Source: BBVA Research

How do we assess the growth stance in BBVA’s footprint?

US EMU Spain Mex

Latam-5

Turkey China Em. Asia Arg Ven Andean C.

2014 ↓↓ ↓↓ ↓↓ ↓↓

2015 ↓↓ ↓↓ ↓↓ ↓↓ ↓↓ ↓↓

No change:

Bias without change in the forecast:

Forecast revision relative to July’s MC:

2,9

-0,3

5,3

3,9

3,2 3,2 3,2

3,7

-4

-3

-2

-1

0

1

2

3

4

5

6

2008 2009 2010 2011 2012 2013 2014 2015

Developed Emerging World BBVA footprint

3

Europe Outlook, November 2014

The economic conditions are in place for growth: suitable funding conditions and less stringent fiscal policy

Page 4

Fiscal Stimulus General Government. Annual change (multiplied by -1) of the Cyclically Adjusted Primary Balance, pp of Potential GDP Source: BBVA Research with IMF Fiscal Monitor data. Oct-14

Central Banks, Balance Sheet, % GDP Source: BBVA Research with Haver data

-2,0

-1,5

-1,0

-0,5

0,0

0,5

1,0

United States Euro area Emerging Economies(G20)

2013 2014-15 (f)

Fiscal Stimulus

Fiscal Tightening

0%

10%

20%

30%

40%

50%

60%

Sep-0

8

Jun-0

9

Mar

-10

Dec

-10

Sep-1

1

Jun-1

2

Mar

-13

Dec

-13

Sep-1

4

BoJ ECB BoE Fed

Europe Outlook, November 2014

Page 5

BBVA Financial Stress Index Source: BBVA Research

Economic Surprises vs Consensus Citigroup Index (*) Source: Haver and Citigroup

(*) A positive (negative) reading of the Economic Surprise Index suggests that economic releases have on balance beating (below) Bloomberg consensus.

-70

-35

0

35

70

08

-Jan

-20

14

05

-Feb-2

01

4

05

-Mar

-20

14

02

-Ap

r-2

01

4

30

-Ap

r-2

01

4

28

-May

-20

14

25

-Jun-2

01

4

23

-Jul-2

01

4

20

-Au

g-2

01

4

17

-Sep-2

01

4

15

-Oct

-20

14

USA eurozone Emerging Markets

Positive surprises

Negative surprises -0.07

-0.05

-0.03

-0.01

0.01

-0.7

-0.5

-0.3

-0.1

0.1

0.3

8-J

an-1

4

5-F

eb-1

4

5-M

ar-

14

2-A

pr-

14

30-A

pr-1

4

28-M

ay-1

4

25-J

un-1

4

23-J

ul-14

20-A

ug-1

4

17-S

ep-1

4

15-O

ct-1

4

USA eurozone Emerging Markets, right

As of late volatility has increased from extremely low levels due to disappointing economic expectations …

Europe Outlook, November 2014

BBVA World Conflict Heat-map (3Q-2014) (Number of conflict / Total events) Source: www.gdelt.org & BBVA Research

Ukraine-Russia

IS advances in M. East

Ebola Outbreak

Social Unrest in Asia

Ceasefire in place but still fragile.

Sanctions 2.0 in place

Waiting for the Winter

Stop the IS advance: The Coalition strikes

A rapid spread but regional

The real “Black Swan”

Turkey’s low profile but key role

Thailand’s “déjà vu”

Democratic demands in Hong Kong

… and an accumulation of potential disruptions due to geopolitical tensions could impact on the economic scenario

Page 6

Europe Outlook, November 2014

Page 7

All in all, current indicators still point to an improvement in global economic growth in the second half of 2014

Global GDP growth based on BBVA-GAIN (QoQ %) Source: BBVA Research

… given: supportive funding conditions and confidence, both coherent with an easing mood from fiscal and monetary policies.

However, if volatility continues, there is a risk that further readings worsen

0,0

0,2

0,4

0,6

0,8

Ju

l 1

4

Cu

rre

nt

Est

Ju

l 1

4

Cu

rre

nt

Est

2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14

Actual data Forecast

Indicators continue to point out towards a modest recovery in global growth, although probably heterogeneous) …

Europe Outlook, November 2014

US: Strong rebound in 2Q14 to be followed by growth over 2.5% in 2H14

Page 8

US: GDP growth (YoY Source: BBVA Research, BEA

US: BBVA Weekly Activity index % change Source: BBVA Research

-3

0

3

5

8

10

24

May-1

3

5 J

ul-

13

16

Au

g-1

3

27

Se

p-1

3

8 N

ov-1

3

20

De

c-13

31

Ja

n-1

4

14

Mar-

14

25

Ap

r-14

6 J

un

-14

18

Ju

l-14

29

Au

g-1

4

10

Oct-

14

2,22,0

2,5

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

2013 2014 2015

Oct-14 Jul-14

Europe Outlook, November 2014

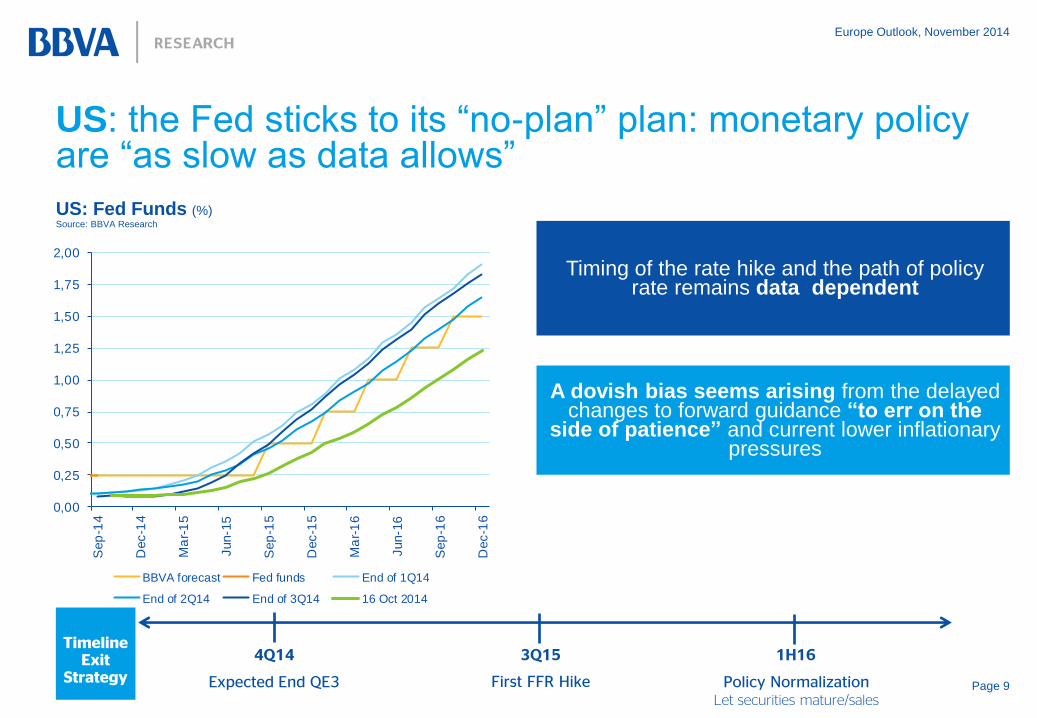

US: the Fed sticks to its “no-plan” plan: monetary policy are “as slow as data allows”

Page 9

US: Fed Funds (%) Source: BBVA Research

Timing of the rate hike and the path of policy rate remains data dependent

A dovish bias seems arising from the delayed changes to forward guidance “to err on the

side of patience” and current lower inflationary pressures

0,00

0,25

0,50

0,75

1,00

1,25

1,50

1,75

2,00

Sep

-14

Dec-1

4

Ma

r-1

5

Jun-1

5

Sep

-15

Dec-1

5

Ma

r-1

6

Jun-1

6

Sep

-16

Dec-1

6

BBVA forecast Fed funds End of 1Q14

End of 2Q14 End of 3Q14 16 Oct 2014

4Q14

Expected End QE3

3Q15

First FFR Hike

1H16

Policy Normalization Let securities mature/sales

Timeline

Exit Strategy

Europe Outlook, November 2014

Page 10

China: manufacturing confidence and activity Source: BBVA Research, PMI

China: total social financing monthly level %, CNY100mn Source BBVA Research

3

6

9

12

15

18

21

36

40

44

48

52

56

60

Ma

r-0

7

Dec-0

7

Sep

-08

Jun-0

9

Ma

r-1

0

Dec-1

0

Sep

-11

Jun-1

2

Ma

r-1

3

Dec-1

3

Sep

-14

PMI Industrial Activity (rhs)

China: some negative surprises on activity and credit growth during the summer

Industry production fell sharply in August, due to sluggish domestic demand

The July-August adjustment in the new funding was driven by real estate

slowdown and shadow banking tighter control

4.000

8.000

12.000

16.000

20.000

Ma

r-1

0

Dec-1

0

Sep

-11

Jun-1

2

Ma

r-1

3

Dec-1

3

Sep

-14

Europe Outlook, November 2014

China: The baseline scenario unchanged expecting policy support

Page 11

China: GDP Growth (%, y-o-y) Source: BBVA Research

7,7

7,2 7,0

0

1

2

3

4

5

6

7

8

9

2013 2014 2015

Oct-14 Jul-14

Economic rebalancing from investment to consumption will continue, but slowly

Policies will need to support economic activity:

• Expected easing in monetary policy (RRR

cuts or liquidity injection)

• More balanced fiscal policy (expansionary at the central gov. level; consolidation at the local level)

• Push forward structural reforms.

Negative bias from foreign demand: Japan’s tax tightening and eurozone downward revision

Europe Outlook, November 2014

Section 1

Slow motion recovery and bumpy road ahead Section 2

The drivers of growth: further policy measures to prevent headwinds Section 3

Forecast: downward revision Section 4

Some imbalances have been corrected, but the growth potential is reduced Annex

Country breakdown

Index

Page 12

Europe Outlook, November 2014

What’s new in Europe

1) Incoming data: some downside risks materialized, both external (geopolitical) and idiosyncratic

Page 13

2) External environment: Ukraine crisis weighs on confidence and, therefore, on investment (Germany), and on exports, to a lesser extent

3) Credit: more evidence of a demand issue in the current situation, more than a supply one

5) Exchange rate: Euro depreciation after the ECB’s new measures and is projected to continue over the medium term and support growth

6) Monetary policy: higher likelihood of QE

4) France and Italy: deterioration in confidence; some progress in the reform agenda, but slower than expected

7) Fiscal policy: open debate about French, Italian and German deficits and investment in infrastructures. Less restrictive stance.

Europe Outlook, November 2014

1) Incoming data: weak growth in 3Q (0.2% QoQ)

Better-than-expected performance of the French economy

Growth driven by positive private consumption behavior; investment still weak

GDP growth (% QoQ) Source: BBVA Research

Eurozone: quarterly GDP growth (%) by components

4Q13 1Q14 2Q14

3Q14

Observed

BBVA

Research

GDP 0,3 0,3 0,1 0,2 0,1

Private consumption -0,1 0,2 0,3

Public consumption -0,2 0,7 0,2

Investment 0,3 0,6 -0,9

Inventories (1) -0,2 0,2 -0,2

Domestic demand (1) 0,0 0,4 0,0

Exports 1,1 0,3 1,3

Imports 0,4 0,6 1,3

Net exports (1) 0,3 -0,1 0,1

(1) Contributions to QoQ GDP growth.

Sources: Eurostat and BBVA Research

Page 14

-0,4

-0,2

0,0

0,2

0,4

0,6

0,8

EMU Germany France Italy Spain

3Q13 4Q13 1Q14 2Q14 3Q14

Europe Outlook, November 2014

1) Incoming data: recovery set back in 2H14

Significant fall in confidence over the summer across countries and sectors, linked to

geopolitical tensions

Disappointing hard data

In October the deterioration of confidence has stopped

Page 15

GDP Jun

Private consumption Jun

Public consumption Jun

Investment Jun

Exports Jun

Imports Jun

ESI Oct

Industrial confidence Oct

Consumer confidence Oct

Export order books Oct

Order books Oct

Unemployment expectations Oct

PMI manufacturing Oct

PMI services Oct

Industrial production Sep

Domestic new orders Aug

Foreign new orders Aug

Passenger car registration Sep

Retail Sales Sep

Exports of goods Aug

China Aug

USA Aug

Imports of goods Aug

Based on quarterly growth rates. For the latest

data, the average of available months in the

quarter is taken. For confidence data,

standarized values are used, and the growth

and fall are related to the mean.

2012 2013 2014

Nati

onal

acco

unts

So

ft d

ata

Hard

data

Europe Outlook, November 2014

1) Incoming data: very weak recovery in 2H14

MICA-BBVA GDP short term model (% QoQ) Sources: Haver and BBVA Research

Growth expected stable at 0.2% in 4Q; but data are very limited

By country, feeble growth across the region…

… except for Spain and Ireland

Forecast by country

Page 16

Germany France Italy Spain

0,3 0,2 0,1 0,5

-0,6

-0,4

-0,2

0,0

0,2

0,4

0,6

0,8

1,0

1,2

1Q

10

2Q

10

3Q

10

4Q

10

1Q

11

2Q

11

3Q

11

4Q

11

1Q

12

2Q

12

3Q

12

4Q

12

1Q

13

2Q

13

3Q

13

4Q

13

1Q

14

2Q

14

3Q

14

4Q

14

Series3 Series9 Series4 ObservedCI 20% CI 40% CI 60%

Europe Outlook, November 2014

2) Geopolitical tensions persist: trade channel (lower growth in Russia), but also impact on confidence

The eurozone exports to Russia are relatively small (4,5% goods, 3,3% services)

Russian GDP forecasts have been slashed about 2,5pp since the beginning of the conflict

Page 17

-15

-10

-5

0

5

10

Goods Services Average exports 3Q13-1Q14 (% YoY)

Eurozone: exports to Russia Source: ECB and BBVA Research

Export share

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

2014 2015 2016

Nov-13 Feb-14 Jun-14 Oct-14

Russia: annual GDP growth forecasts (%) Source: FocusEconomics

Europe Outlook, November 2014

2) And weak demand from developed countries

UEM: Exports by destination (%3m/3m) Source: BBVA Research

Page 18

Volatile but weaker exports lately

Exports to the UK and the rest of the EU have

maintained the tone

Weak demand from emerging markets

-2

-1

0

1

2

3

4

1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14

Other European Union Other EuropeanAfrica AmericaAsia OceaniaRest Total

Europe Outlook, November 2014

Eurozone (% YoY) Note: Retail loans is the sum of loans to households and companies up to 1M€ Sources: BCE, Eurostat and BBVA Research

The new credit to large companies is still falling, partly because of their increased use of

the market

3) The new credit to households and small businesses has not taken off...

Page 19

-25

-20

-15

-10

-5

0

5

10

15

20

25

-6

-4

-2

0

2

4

6

Sep

-04

Ma

r-0

5

Sep

-05

Ma

r-0

6

Sep

-06

Ma

r-0

7

Sep

-07

Ma

r-0

8

Sep

-08

Ma

r-0

9

Sep

-09

Ma

r-1

0

Sep

-10

Ma

r-1

1

Sep

-11

Ma

r-1

2

Sep

-12

Ma

r-1

3

Sep

-13

Ma

r-1

4

Sep

-14

GDP

New RETAIL loans (t-2) (RHS)

Stock TOTAL loans (RHS)

The new credit and real variables (consumption and investment) are flows and are strongly

correlated (correlation of 0.9, compared to 0.6 with the stock of credit)

The new consumer credit and for small and medium enterprises has been growing for half a

year, but with some doubts

Europe Outlook, November 2014

3) … despite lower credit constraints

Page 20

-60

-40

-20

0

20

40

60

-0.015

-0.010

-0.005

0.000

0.005

0.010

0.015

1Q

20

03

3Q

2003

1Q

20

04

3Q

20

04

1Q

20

05

3Q

20

05

1Q

20

06

3Q

20

06

1Q

20

07

3Q

20

07

1Q

20

08

3Q

2008

1Q

20

09

3Q

20

09

1Q

20

10

3Q

20

10

1Q

20

11

3Q

20

11

1Q

20

12

3Q

20

12

1Q

2013

3Q

20

13

1Q

20

14

model error (LHS) credit standards (inverted, RHS)

-20

-15

-10

-5

0

5

10

15

20

-60

-40

-20

0

20

40

60

Q1

-04

Q3

-04

Q1

-05

Q3

-05

Q1

-06

Q3

-06

Q1

-07

Q3

-07

Q1

-08

Q3

-08

Q1

-09

Q3

-09

Q1

-10

Q3

-10

Q1

-11

Q3

-11

Q1

-12

Q3

-12

Q1

-13

Q3

-13

Q1

-14

Q3

-14

Credit standards (t-5) Loan demand (t-5)

Flow NFC (% YoY, RHS)

Eurozone: Flow , credit standards and loan demand Source: ECB and BBVA Research

Eurozone: Demand model estimation error and credit standards Source: ECB and BBVA Research

Higher correlation between credit flows and loan demand than with credit supply.

In 2008 and 2012, supply factors could explain a larger fall in credit to private sector.

Currently, limit evidence on supply constraints

Europe Outlook, November 2014

4) Italy / France: Lower growth momentum linked to internal issues

• GDP contracted in 2Q14 (-0,2% QoQ) and weak data for 3Q14

• The electoral and institutional reforms broadly on track (to be completed by February)

• Labour market reform launched (flexible dismissal), but details to be adopted throughout 2015

• Spending review delayed

• Growing internal impatience for the slowness of reforms

• Reduction of corporate and labour taxes to regain competitiveness

• € 50bn spending cut expected in 3 years (2.5% of GDP), but still to be detailed

• Launch of reforms in retail opening hours and professional services (December 2015)

• Deteriorated political landscape despite the government reshuffling.

Page 21

Italy

Fra

nce

Europe Outlook, November 2014

5) Stronger depreciation should help sustain the recovery in 2015…

The euro depreciation is due to: (a) Increasing cyclical divergence with US

(b) Increasing differences in monetary policy

Page 22

1.100

1.150

1.200

1.250

1.300

1.350

1.400

Ja

n-1

4

Ap

r-1

4

Ju

l-1

4

Oct-

14

Ja

n-1

5

Ap

r-1

5

Jul-1

5

Oct-

15

Ja

n-1

6

Ap

r-1

6

Ju

l-1

6

Oct-

16

Ja

n-1

7

Ap

r-1

7

Ju

l-1

7

Oct-

17

Jun-14 Sep-14

Dollar/Euro exchange rate Source BBVA Research

9% both in 2015 and 2016

Europe Outlook, November 2014

5) …with differenciated effects across countries

Projected impact: 0.3pp in 2015

Page 23

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

2014 2015 2016

Area Wide model ECM model (Max) OECD model

Eurozone: effect of euro depreciation on annual GDP growth (pp) Source OECD and BBVA Research

Larger impact on Italy and Germany than in Spain or France

Effect of euro depreciation on annual GDP growth (pp). ECM model Source BBVA Research

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

20

14

20

15

20

16

20

14

20

15

20

16

20

14

20

15

20

16

20

14

20

15

20

16

20

14

20

15

20

16

Germany France Italy Spain Eurozone

Min Max

Europe Outlook, November 2014

6) ECB: how to increase significantly its balance sheet? Running out of options

• Disappointing liquidity take up in September (€ 82.6bn). We

have to wait to December (higher demand expected).

• Next quarterly auctions will be correlated with credit (eg

growth)

• Difficult to quantify the volume and impact (particularly the

ABS program for the lack of details, such as the purchasing

conditions of the tranches with the higher risk)

TLTRO (4 years since

Sept 2014)

ABS and CB (2 years since

Q414, no target)

• More likely given recent data (activity and inflation

expectations), and difficulties to significantly expand the

balance with other measures.

• German opposition

QE ??

Liquidity

Purchase of

privates

assets

Purchase of

government

bonds?

Europe Outlook, November 2014

Mid

2017

• Details of the ABSPP and CBPP: • It did not announce a target size for the

private asset buying programmes • The programmes will last for at least two

years and they will commence in the fourth quarter of 2014

• Pending eligibility criteria for guaranteed mezzanine tranches

• The door remains open for (full scale) QE.

• Draghi said that: the ECB's balance sheet was just an instrument to achieve its inflation mandate.

• Recent comments continue to show discrepancies with the GC on next steps to be taken (full-scale QE)

ECB

Latest What do we expect? Policy pause until

BB

VA

Expect

ed

Tim

eline

18 Sept14

First rate hike

TLTROs

11 Dec14 Mar15 Jun15 Sep15 Dec15 Mar16 Jun16 Jun 17 TLTRO1

EUR 82,6 bn)

TLTRO2

TLTRO3 TLTRO4

TLTRO5 TLTRO6

TLTRO7 TLTRO 8

Purchase program of private assets (ABS and covered bonds)

Oct 14. CBPP starts

• We believe that the ECB´s commitment to increase significantly its balance sheet is credible, but current measures will not be enough. Consequently, a full-scale QE (i.e, purchase of government bonds) will be needed to fill the gap.

• The probability of QE has risen slightly above 50% in our baseline scenario.

• We postpone the ECB´s first rate hike to June 2017

6) The ECB in a wait and see stance

Europe Outlook, November 2014

7) Fiscal policy is less restrictive than in previous years...

Strucrural deficit adjustment 2010-2015 (% GDP) Source: BBVA Research

The adjustment of the structural deficit will be lower in 2014 than in previous years

The structural deficit after 2015 will remain positive and need further adjustment to meet

the fiscal rules

Page 26

-2

0

2

4

6

8

10

12

14

16

Portugal Ireland France Spain Italy Greece

Post 2015 2015 2014 2013 2012 2011

Intense debate on fiscal policy:

1. Room for Germany 2. Deficit in France and Italy 3. Junker’s plan on infrastructures

Europe Outlook, November 2014

Section 1

Slow motion recovery and bumpy road ahead Section 2

The drivers of growth: further policy measures to prevent headwinds Section 3

Forecast: downward revision Section 4

Some imbalances have been corrected, but the growth potential is reduced Annex

Country breakdown

Index

Page 27

Europe Outlook, November 2014

-10

-8

-6

-4

-2

0

2

4

6

2008 2009 2010 2011 2012 2013 2014 2015

Domestic Demand Exports Imports Net exports GDP

Forecast: weaker than expected growth both in 2014 and 2015

EMU: annual GDP growth contributions (pp) Sources: Eurostat and BBVA Research

2012 2013

2014

(f)

2015

(f)

Activity

REAL GDP (% YoY) -0,7 -0,4 0,8 1,3

Private consumption -1,3 -0,6 0,7 1,3

Public consumption -0,2 0,2 0,9 0,4

Investment -3,2 -2,4 0,6 1,8

Domestic demand (contr. %) -2,1 -0,8 0,8 1,1

Exports 2,6 1,1 3,7 5,1

Imports -1,0 1,2 4,1 5,2

Net exports (contr. %) 1,4 0,4 0,0 0,2

Current account balance(% GDP) 1,2 2,3 2,2 2,1

Public deficit (% GDP) -3,6 -2,9 -2,8 -2,6

CPI, % average 2,5 1,4 0,5 1,0

Page 28

Europe Outlook, November 2014

GDP forecast by country (%) Sources: Eurostat and BBVA Research

By country: downward revisions in the three largest countries

• Germany continues to lead the recovery but

with downward revision

• France doesn’t gain momentum yet

• Recently, positive measures have been

adopted to regain competitiveness and

reduce public spending

• Italy: still in recession in 2014

• Extensive reform plans, that need to be

materialized

Page 29

-0,7

-0,4

0,8

1,3

0,6

0,2

1,3 1,4

0,4 0,4 0,4

1,1

-2,3

-1,9

-0,3

0,8

-3,0

-2,5

-2,0

-1,5

-1,0

-0,5

0,0

0,5

1,0

1,5

2,0

2,5

20

12

20

13

20

14

20

15

20

12

20

13

20

14

20

15

20

12

20

13

20

14

20

15

20

12

20

13

20

14

20

15

EMU Germany France Italy

New projection (Oct-14) Last projection (Jul-14)

Europe Outlook, November 2014

Inflation is expected to stay at very low rates

Eurozone: inflation (% YoY) Sources: Eurostat and BBVA Research

Page 30

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Dec-08

May-09

Oct-09

Mar-10

Aug-10

Jan-11

Jun-11

Nov-11

Apr-12

Sep-12

Feb-13

Jul-13

Dec-13

May-14

Oct-14

Mar-15

Aug-15

20% 40% 60% 80% 95%

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Ja

n-0

4

Jul-0

4

Ja

n-0

5

Ju

l-0

5

Ja

n-0

6

Ju

l-0

6

Ja

n-0

7

Ju

l-0

7

Ja

n-0

8

Ju

l-0

8

Ja

n-0

9

Jul-0

9

Ja

n-1

0

Ju

l-1

0

Ja

n-1

1

Ju

l-1

1

Ja

n-1

2

Ju

l-1

2

Ja

n-1

3

Ju

l-1

3

Ja

n-1

4

Jul-1

4

Core HICP (% YoY) Core HICP at constant tax (% YoY)

1stre

ce

ssio

n

2n

dre

cess

ion

Eurozone: core inflation (% YoY) Source: Eurosat and BBVA Research

Inflation moderation over 3Q14 reflected falling prices of food and energy.

Core inflation broadly stable at low levels (0.8%)

Projected acceleration to only 1% due to the euro depreciation

Europe Outlook, November 2014

Inflation expectations worsened, increasing the risk of de-anchoring

Eurozone: inflation (% YoY) Source: BBVA Research

Page 31

Eurozone: 5Y5Y inflation swaps Source: BBVA Research

-1

0

1

2

3

4

5

Oct

-04

Apr-

05

Oct

-05

Apr-

06

Oct

-06

Apr-

07

Oct

-07

Apr-

08

Oct

-08

Apr-

09

Oct

-09

Apr-

10

Oct

-10

Apr-

11

Oct

-11

Apr-

12

Oct

-12

Apr-

13

Oct

-13

Apr-

14

Oct

-14

CI95 CI80 CI60

CI40 CI20 Optimal trim

HICP inflation Core inflation

1,70

1,80

1,90

2,00

2,10

2,20

5Y5Y EZ Inflation swap fwd

Eurozone 2Q GDP

Draghi at Jackson Hole

ECB meeting

ECB meeting

German trade data

Sell-off

Europe Outlook, November 2014

Risks

1. Lower growth abroad (China)

2. Impact from a problematic Fed exit

3. Geopolitical risks

1. AQR surprises

2. Risk of deflation and the burden of a recovery

with very low inflation

3. Lack of effectiveness of ECB’s measures and

market reversion

External

Domestic

Page 32

Old

1. Fed intolerance to dollar appreciation

2. Prolonged conflict with Russia

1. Rebound in confidence

2. More activism in European authorities

3. Further delays with reforms

4. Political risks (Catalonia, Le Pen, etc)

5. True secular stagnation

New

Europe Outlook, November 2014

Section 1

Slow motion recovery and bumpy road ahead Section 2

The drivers of growth: further policy measures to prevent headwinds Section 3

Forecast: downward revision Section 4

Some imbalances have been corrected, but the growth potential is reduced Annex

Country breakdown

Index

Page 33

Europe Outlook, November 2014

Low potential growth

Eurozone: potential GDP growth (%) and factors’ contribution (pp) Sources: Eurostat and BBVA Research

US and EZ projected potential GDP growth (pp) Sources: Eurostat and BBVA Research

The crisis has reduced the potential below 1%, but should recover to 1.5% Lower potential than in US

Page 34

-1

0

1

2

3

4

5

6

19

66

19

68

19

70

19

72

19

74

19

76

19

78

19

80

19

82

19

84

19

86

19

88

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

20

08

20

10

20

12

20

14

20

16

20

18

20

20

20

22

20

24

Capital Participation rate Active Population

Nairu TFP Potential

0,0

0,5

1,0

1,5

2,0

2,5

3,0

2014-2022 2014-2022

Capital Labour TFP

EMU

US

Europe Outlook, November 2014

The impact of the crisis: US vs core vs periphery

GDP Note: Q1-2008=100

Sources: Eurostat, Haver and BBVA Research

Components Note: Q1-2008=100

Sources: Eurostat, Haver and BBVA Research

Page 35

97,6

102,9

101,1

90,7

93,4

107,5

90

95

100

105

110

Ma

r-0

8Jun-0

8S

ep

-08

Dec-0

8M

ar-

09

Jun-0

9S

ep

-09

Dec-0

9M

ar-

10

Jun-1

0S

ep

-10

Dec-1

0M

ar-

11

Jun-1

1S

ep

-11

Dec-1

1M

ar-

12

Jun-1

2S

ep

-12

Dec-1

2M

ar-

13

Jun-1

3S

ep

-13

Dec-1

3M

ar-

14

Jun-1

4

Eurozone Germany France

Italy Spain USA

-60

-50

-40

-30

-20

-10

0

10

20

30

Euro area Germany France Italy Spain USA

Consumption Investment (w/o construction)

Investment in construction Exports

Europe Outlook, November 2014

Heat map of macroeconomic imbalances

Excluding aid to the financial sector **Data for France: 4Q-2012 Source: Eurostat, BCE, Haver and BBVA Research Page 36

Public DebtPublic Deficit*

Unemploy-ment Rate

Current Account

Net International Investment

Position

Real Effective Exchange

Rate

Nominal Unit Labour

Cost Household Debt

Non-Financial Corporations

Debt

% of GDP % of GDP % of GDP % of GDP 3-yr % chg. 3-yr % chg. % of GDP % of GDP

Q4-2013 2013 Latest 2013 Q4-2013** Sep. 2013 Latest Latest Latest

Eurozone 92,7 -2,8 11,8 2,4 -12,2 1,0 3,9 63,9 81,5

GER 78,4 0,0 5,1 7,5 48,3 0,1 6,1 58,2 48,5

FRA 93,5 -4,3 10,4 -1,4 -21,2 -0,7 5,2 56,7 84,0

AUT 74,5 -0,9 4,9 2,7 3,4 2,2 7,3 54,5 92,9

BEL 101,5 -2,8 8,5 -1,6 44,0 0,5 8,6 56,5 92,4

NED 73,5 -2,5 7,2 10,4 53,0 1,5 6,4 127,9 91,5

FIN 57,0 -2,1 8,5 -1,1 15,8 1,9 8,5 65,4 92,5

ITA 132,6 -3,1 12,7 1,0 -30,0 2,0 4,3 45,3 81,0

SPA 93,9 -6,6 25,3 0,8 -98,2 0,8 -5,3 81,3 114,0

POR 129,0 -4,5 15,2 0,5 -118,7 0,2 -1,3 86,8 130,8

IRE 123,7 -6,7 11,8 6,6 -104,9 -2,4 -3,4 105,1 201,3

GRC 175,1 -2,1 26,5 0,7 -119,0 -3,9 -11,1 64,5 64,8

DEN 44,5 -0,9 6,5 7,3 39,6 -1,4 3,8 139,2 97,9

SWE 40,6 -1,1 8,1 6,2 -4,8 3,1 6,2 83,4 121,2

U.K. 90,6 -5,7 6,7 -4,4 -1,3 3,9 6,2 93,1 83,8Colour criterion:

Higher than 130 Lower than -6 Higher than 16 Lower than -6 Lower than -100 Greater than 6 Greater than 9 Greater than 110 Greater than 140

110/130 -6/-5 13/16 -6/-4 -100/-50 4/6 6/9 90/110 120/140

90/110 -5/-4 10/13 -4/-2 -50/0 2/4 3/6 75/90 100/120

60/90 -4/-3 7/10 -2/0 0/20 0/2 0/3 60/75 80/100

Lower than 60 Higher than -3 Lower than 7 Greater than 0 Greater than 20 Lower than 0 Lower than 0 Lower than 60 Lower than 80

Europe Outlook, November 2014

Public and private debt 2005-2015 (% GDP) Sources: Eurostat and BBVA Research

Deleveraging isn’t in process yet, with exceptions

Private debt has stabilized and begun to fall in Spain

The peripheral countries have experienced much larger increases in debt than the core

during the crisis

Page 37

Spain

Portugal

France

Greece

Italy

Germany

Netherlands

0

20

40

60

80

100

120

140

160

180

80 130 180 230

Pu

blic

deb

t (%

GD

P)

Private debt (% GDP)

MacroeconomicImbalancesLimits

2005 X 2015

Europe Outlook, November 2014

Peripheral countries have reduced public deficits but public debts continue to grow

Government debt and deficit 2005–2015 Source: FMI

The adjustment of the deficit has been huge, especially in the countries subject to the

program

But debt levels have not begun to fall yet

The return to growth and higher inflation are key to rapid deleveraging

Page 38

Spain

France

Italy

Greece

Portugal

20

40

60

80

100

120

140

160

180

200

-16 -11 -6 -1 4

Genera

l G

overn

ment D

ebt

(% o

f G

DP

)

General Government Deficit (% GDP)

Maastricht deficit and debt limits

2005 X 2015

Europe Outlook, November 2014

Unit labour costs adjustment, 2009-2013 (%) Sources: Haver y BBVA Research

Unit labor costs have been adjusted rapidly in the periphery

In some countries this was due to increased productivity caused by the decline in

employment

Wage moderation has also played an important role, especially in comparison with the core

countries

Page 39

-20

-15

-10

-5

0

5

10

15

Gre

ece

Irela

nd

Sp

ain

Port

ug

al

EA

17

De

nm

ark

Ge

rma

ny

Ita

ly

Fra

nce

Ne

therl

and

s

Un

ite

d K

ing

dom

Au

str

ia

Fin

lan

d

Be

lgiu

m

Labour Productivity (Sign switched) Wages Unit Labour Cost

Europe Outlook, November 2014

Current account (% GDP) Sources: Eurostat and BBVA Research

The current account deficits have disappeared very fast

Current account (% GDP) Sources: Eurostat and BBVA Research

Most countries in the euro zone are now in surplus (except for France)

Part of the adjustment is due to the recession (less imports), but exports have also played an

important role

Page 40

-15,0

-10,0

-5,0

0,0

5,0

10,0

15,0

Mar-

01

Mar-

02

Mar-

03

Mar-

04

Mar-

05

Mar-

06

Mar-

07

Mar-

08

Mar-

09

Mar-

10

Mar-

11

Mar-

12

Mar-

13

Mar-

14

Germany France ItalySpain Portugal Netherlands

-20

-15

-10

-5

0

5

10

15

20

NLD

GE

R

IRL

AU

T

ITA

SP

A

GR

C

PO

R

FIN

FR

A

BE

L

Exports Imports Other items

Current account: 1Q08 Current account: 4Q13

Europe Outlook, November 2014

Unemployment since the beginning of the crisis (%) Sources: Haver and BBVA Research

The high unemployment remains the main problem of economic policy

The unemployment rate is well above that of 2008 (except in Germany)

Even so, it has begun to decrease earlier than in other recessions

Page 41

0

5

10

15

20

25

30

EA

18

GER

FR

A

AU

T

BEL

NLD

FIN

ITA

SPA

PO

R

IRE

GR

C

CYP

SLV

SLK

DEN

SW

E

UK

Last Feb-08 Feb-13

Europe Outlook, November 2014

Section 1

Slow motion recovery and bumpy road ahead Section 2

The drivers of growth: further policy measures to prevent headwinds Section 3

Forecast: downward revision Section 4

Some imbalances have been corrected, but the growth potential is reduced Annex

Country breakdown

Index

Page 42

Europe Outlook, November 2014

Germany: deterioration in the industrial sector 3Q14

Confidence indicators worsened over 3Q14

International conflicts have affected companies’ propensity to investment

2012 2013 2014 (f) 2015 (f)

Activity

REAL GDP (% YoY) 0,6 0,2 1,3 1,4

Private consumption 0,6 0,9 1,2 1,3

Public consumption 1,2 0,7 1,1 0,9

Investment 0,1 -0,6 3,2 3,3

Domestic demand (contr. %) -0,8 0,7 1,5 1,5

Exports 3,5 1,7 3,4 4,1

Imports 0,4 3,2 4,3 4,9

Net exports (contr. %) 1,4 -0,5 -0,1 0,0

External sector

Current account balance (% GDP) 7,2 7,3 6,7 7,1

Public finances

General Govt. Balance (% GDP) 0,1 0,1 0,0 0,0

Prices

CPI, % avg. 2,1 1,6 0,9 1,5

Page 43

GDP JunPrivate consumption JunPublic consumption JunInvestment JunExports JunImports Jun

ESI OctIndustrial confidence OctConsumer confidence OctService confidence Oct

Volume export order books OctVolume of order books OctUnemployment expectations Oct

Gfk consumer climate NovIfo business climate OctPMI manufacturing OctPMI services OctIndustrial production Sep

Domestic new orders SepForeign new orders Sep

Retail Sales SepExports of goods Aug

Intra EU AugExtra EU Aug

Imports of goods Aug

Based on quarterly growth rates. For the latest

data, the average of available months in the

quarter is taken. For confidence data,

standarized values are used, and the growth

and fall are related to the mean.

No DATAStronger growthGrowthFallDeeper fall

2012 2013 2014

Nati

on

al

acco

un

tsSo

ft d

ata

Hard

data

Europe Outlook, November 2014

Germany: slower growth with medium-term concerns

Ifo confidence, composite PMI and manufacturing orders from abroad Source: BBVA Research

Growth continues but at a slower pace than initially expected

Private consumption does not grow at rates consistent with the favorable labor market

conditions

The liberalization of some services sectors would help boost consumption and domestic

growth

Page 44

-10

-5

0

5

10

15

20

-1,0

-0,5

0,0

0,5

1,0

1,5

2,0

Jul-11

Sep-1

1

Nov-1

1

Jan-1

2

Mar-

12

May-1

2

Jul-12

Sep-1

2

Nov-1

2

Jan-1

3

Mar-

13

May-1

3

Jul-13

Sep-1

3

Nov-1

3

Jan-1

4

Mar-

14

May-1

4

Jul-14

Sep-1

4

Ifo confidence indexPMI CompositeForeign Manufacturing Orders (YoY, rhs)3-per M.A. (FMO)

Europe Outlook, November 2014

France: recovery doesn’t gain momentum

Confidence indicators fell sharply in Q3

Domestic demand continues to sustain the slow recovery

2012 2013 2014 (f) 2015 (f)

Activity

REAL GDP (% YoY) 0,4 0,4 0,4 1,1

Private consumption -0,4 0,3 0,2 1,1

Public consumption 1,7 2,0 1,7 0,5

Investment 0,3 -0,8 -0,6 1,1

Domestic demand (contr. %) -0,3 0,3 0,4 0,9

Exports 1,2 2,4 2,6 3,2

Imports -1,2 1,9 2,5 2,6

Net exports (contr. %) 0,7 0,1 0,0 0,1

External sector

Current account balance (% GDP) -2,1 -1,3 -1,7 -1,6

Public finances

General Govt. Balance (% GDP) -4,9 -4,1 -4,4 -4,3

Prices

CPI, % avg. 2,2 1,0 0,7 0,9

Page 45

GDP JunPrivate consumption JunPublic consumption JunInvestment JunExports JunImports Jun

ESI OctIndustrial confidence OctConsumer confidence Oct

Service confidence OctExport order books OctTotal order books OctUnemployment expectations Oct

Business Climate (INSEE) OctBusiness sentiment (BdF) OctPMI manufacturing OctPMI services OctIndustrial production SepDomestic turnover AugForeign turnover Aug

Capacity utilization (Industry) NovConsumer spending SepRetail Sales SepExports of goods Sep

Intra EU SepExtra EU Sep

Imports of goods SepBased on quarterly growth rates. For the latest

data, the average of available months in the

quarter is taken. For confidence data,

standarized values are used, and the growth

and fall are related to the mean.

No DATA

Stronger growth

Growth

Fall

Deeper fall

2012 2013 2014

Nati

onal

acco

unts

So

ft d

ata

Hard

data

Europe Outlook, November 2014

France: political instability slows reform process

Unit labour costs (2005=100) and current account balance Note: Unit labour costs normalized to 100 in 2005 Source: BBVA Research

The loss of competitiveness is the main issue in the medium term

The planned cuts in the tax burden on employment should be financed by lower public

spending

Page 46

But the government is negotiating to ease fiscal consolidation

-2,5

-2,0

-1,5

-1,0

-0,5

0,0

95

100

105

110

115

120

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

FRA Current Acc. Balance (%GDP) RHS

Eurozone

France

Germany

Spain

Europe Outlook, November 2014

Italy: the recession continues in 2014

Last confidence indicators have clearly worsened

Net exports no longer support the weak recovery

2012 2013 2014 (f) 2015 (f)

Activity

REAL GDP (% YoY) -2,3 -1,9 -0,3 0,8

Private consumption -4,1 -2,7 0,0 0,5

Public consumption -1,5 -0,7 0,0 -0,3

Investment -7,5 -5,4 -2,1 1,5

Domestic demand (contr. %) -5,0 -2,8 -0,4 0,6

Exports 1,6 0,9 2,0 3,8

Imports -8,2 -2,6 1,6 3,4

Net exports (contr. %) 2,6 0,9 0,2 0,3

External sector

Current account balance (% GDP) -0,2 1,0 0,9 0,9

Public finances

General Govt. Balance (% GDP) -3,0 -2,8 -3,0 -2,7

Prices

CPI, % avg. 3,3 1,3 0,3 0,7

Page 47

GDP JunPrivate consumption JunPublic consumption JunInvestment JunExports JunImports Jun

ESI OctIndustrial confidence OctConsumer confidence OctService confidence Oct

Export order books OctTotal order books OctUnemployment expectations Sep

Consumer confidence (ISTAT) OctBusiness confidence (ISTAT) JanPMI manufacturing JulPMI services JunIndustrial production Sep

Domestic new orders AugForeign new orders Aug

Capacity utilization rate SepPassenger car registrations OctRetail Sales AugExports of goods Aug

Intra EU AugExtra EU Sep

Imports of goods Aug

Fall

Deeper fall

Based on quarterly growth rates. For the latest

data, the average of available months in the

quarter is taken. For confidence data,

standarized values are used, and the growth

and fall are related to the mean.

2012 2013 2014

Nati

onal

acco

unts

So

ft d

ata

Hard

data

No DATA

Stronger growth

Growth

Europe Outlook, November 2014

Italy: reforms needed to increase the growth potential

GDP/working age population (2000=100) Source: BBVA Research In fiscal policy, the main problem is the high

volume of public debt (132.6%), while the deficit reduction is slower than expected

The growth potential is very slow …

…but could recover, should fiscal and labour market reforms underway be approved

Page 48

90

95

100

105

110

115

120

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

Italy Spain Eurozone

Europe Outlook, November 2014

Spain: recovery at a healthy pace

The growth will be driven by domestic and external factors, despite the lack of dynamism

in European demand

The trend in recent data points to a practical stabilization of growth around 0.5% in 3Q14

2012 2013 2014 (f) 2015 (f)

Activity

REAL GDP (% YoY) -2,1 -1,2 1,3 2,0

Private consumption -3,0 -2,3 2,1 1,8

Public consumption -3,7 -2,9 1,0 0,9

Investment -8,3 -3,7 0,7 4,2

Domestic demand (contr. %) -4,3 -2,7 1,6 2,0

Exports 1,2 4,3 3,7 5,3

Imports -6,3 -0,5 4,8 5,0

Net exports (contr. %) 2,5 1,5 0,0 5,5

External sector

Current account balance (% GDP) -0,3 1,4 1,2 2,1

Public finances

General Govt. Balance (% GDP) -6,6 -6,3 -5,5 -4,2

Prices

CPI, % avg. 2,4 1,4 0,0 1,0

Page 49

GDP JunPrivate consumption JunPublic consumption JunInvestment JunExports JunImports Jun

ESI OctIndustrial confidence OctConsumer confidence OctService confidence Oct

Export order books OctTotal order books OctUnemployment expectations Oct

Private cons. (synth. indicator) SepPMI manufacturing OctPMI services OctIndustrial production SepIndustrial new orders AugCapacity utilization rate NovMotor vehicle registrations OctRetail Sales SepExports of goods Aug

Intra EU JulExtra EU Jul

Imports of goods Aug

Stronger growth

Growth

Fall

Deeper fall

No DATA

2012 2013 2014

Nati

onal

acco

unts

So

ft d

ata

Hard

data

Based on quarterly growth rates. For the latest

data, the average of available months in the

quarter is taken.

For soft data, standarized values are used, and

the growth and fall are related to the mean.

Europe Outlook, November 2014

Spain: Investment in machinery & equipment (Real ratios, 2008 prices) Source: BBVA Research from INE

The recent increase in investment in machinery and equipment is consistent with the change in the production model oriented to the external

sector

The most urgent and important challenge is the sustained job creation, of the highest quality

possible

Need to take measures to improve productivity, competitiveness and human and technological

capital, among others

Spain: improvement in the labor market, but major imbalances persist

Page 50

4

5

6

7

8

9

10

Dec-8

1

Dec-8

3

Dec-8

5

Dec-8

7

Dec-8

9

Dec-9

1

Dec-9

3

Dec-9

5

Dec-9

7

Dec-9

9

Dec-0

1

Dec-0

3

Dec-0

5

Dec-0

7

Dec-0

9

Dec-1

1

Dec-1

3

Dec-1

5

% of GDP % of national demand

![When Lightning Strikes: Hadley v. Baxendale Probability ......15_O'GORMAN FINAL.DOCX (DO NOT DELETE) 4/1/2016 9:19 AM 2016] When Lightning Strikes 861 third (win, place, and show)](https://img.dokumen.tips/doc/110x75/60365441c550fc04ef6a3feb/when-lightning-strikes-hadley-v-baxendale-probability-15ogorman-finaldocx.jpg)