Embed Size (px)

Citation preview

Copyright © 2017 The Nielsen Company. Confidential and proprietary. Prepared by Nielsen Vietnam – April 2018

Copyright © 2017 The Nielsen Company. Confidential and proprietary.

3 Cop

yri

gh

t ©

20

17

Th

e N

iels

en

Com

pa

ny.

Co

nfid

en

tia

l a

nd

pro

pri

eta

ry.

4 Cop

yri

gh

t ©

20

17

Th

e N

iels

en

Com

pa

ny.

Co

nfid

en

tia

l a

nd

pro

pri

eta

ry.

Total Vietnam - Value Contribution by Super category in FMCG

5.8 5.7

6.7 6.5

15.9 15.8

14.0 13.8

16.0 16.3

20.1 19.7

19.0 19.7

2016 2017

Beer

Non-Alc Beverage

Food

Milk Base

Cigarette

Personal Care

Household Care

6%

10%

7%

7%

4%

5%

3%

4%

Total FMCG

Total Vietnam - Value Growth 2017 vs 2016

Source: Nielsen Retail Audit

5 Cop

yri

gh

t ©

20

17

Th

e N

iels

en

Com

pa

ny.

Co

nfid

en

tia

l a

nd

pro

pri

eta

ry.

3.0 3.7 1.5 -3.7

4.5 6.9 6.1

18.5

4.0 1.3 2.7

3.0

0.1

5.0 1.9

2.5

7.0 5.0 4.2

-0.7

4.6

11.9

8.0

21.0

Food Instant Noodles Soy & Oyster

Sauce

Fish Sauce MSG - Bouillon Biscuits Cake Pie Snack

Total Vietnam – Growth 2017 vs 2016

Value contribution to Food

29.7 3.5 11.8 18.9 12.2 8.9 14.9

Regular Categories

Impulse Categories

Volume Change Price Change Nominal Value Growth

Source: Nielsen Retail Audit

6 Cop

yri

gh

t ©

20

17

Th

e N

iels

en

Com

pa

ny.

Co

nfid

en

tia

l a

nd

pro

pri

eta

ry.

7 Cop

yri

gh

t ©

20

17

Th

e N

iels

en

Com

pa

ny.

Co

nfid

en

tia

l a

nd

pro

pri

eta

ry.

Manufacturers are willing to push new products, but less than 15% of them are sizeable

2.3 4.1

-1.8

4.4 9.0

6.2

17.5

2.8 0.1

1.1

0.3

2.9

1.8

3.5

5.0 4.2

-0.7

4.6

11.9

8.0

21.0

Instant Noodles Soy & Oyster

Sauce

Fish Sauce MSG - Bouillon Biscuits Cake Pie Snack

Value Growth contribution by Existing & New launch

Existing 2016

New launch 2017

REGULAR IMPULSE

Source: Nielsen Retail Audit | New launch is defined at variant level

7%

127 #No of New launch

% New launch

contribute 80% sales

19%

16

6%

172

6%

35

13%

981

13%

173

8%

675

8 Cop

yri

gh

t ©

20

17

Th

e N

iels

en

Com

pa

ny.

Co

nfid

en

tia

l a

nd

pro

pri

eta

ry.

New Value/Proposition Sizeable Need Distribution Effort

Source: Breakthrough Innovations – Winning with innovation in Asia Pacific

9 Cop

yri

gh

t ©

20

17

Th

e N

iels

en

Com

pa

ny.

Co

nfid

en

tia

l a

nd

pro

pri

eta

ry.

GENERAL PROFILE BREAKTHROUGH PROFILE

Kokomi Dai

Instant Noodles

Launch: Aug 2017

Distinctiveness

Chewy & Non-soggy texture Big

size

Relevance

0.8% share after 3 months

GENERAL PROFILE BREAKTHROUGH PROFILE

Chocopie Dark

Cake Pie

Launch: Oct 2017

Distinctiveness

70% more cocoa

Premium price

Relevance

2.5% share after 3 months

With clear differentiator and real consumer needs

10 Cop

yri

gh

t ©

20

17

Th

e N

iels

en

Com

pa

ny.

Co

nfid

en

tia

l a

nd

pro

pri

eta

ry.

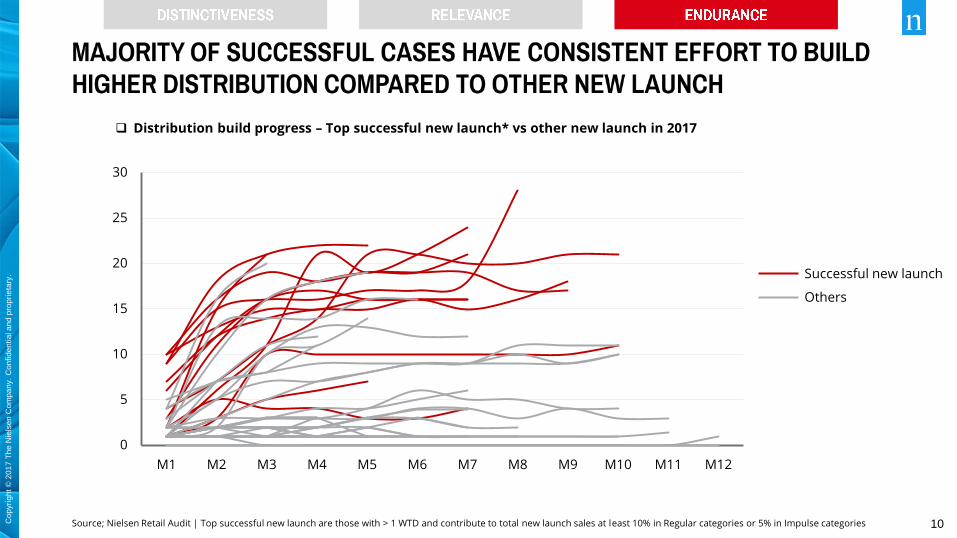

Distribution build progress – Top successful new launch* vs other new launch in 2017

Source; Nielsen Retail Audit | Top successful new launch are those with > 1 WTD and contribute to total new launch sales at least 10% in Regular categories or 5% in Impulse categories

0

5

10

15

20

25

30

M1 M2 M3 M4 M5 M6 M7 M8 M9 M10 M11 M12

Successful new launch

Others

11 Cop

yri

gh

t ©

20

17

Th

e N

iels

en

Com

pa

ny.

Co

nfid

en

tia

l a

nd

pro

pri

eta

ry.

12 Cop

yri

gh

t ©

20

17

Th

e N

iels

en

Com

pa

ny.

Co

nfid

en

tia

l a

nd

pro

pri

eta

ry.

Cop

yri

gh

t ©

20

17

Th

e N

iels

en

Com

pa

ny.

Co

nfid

en

tia

l a

nd

pro

pri

eta

ry.

WHAT CONSUMERS THINK HOW CONSUMERS ACT

37% consider

health as their concern,

ranked Top 2 as top

biggest concerns

80% concern about

long-term health impact of

artificial ingredients

(vs. 75% of global)

83% actively make

dietary choices to prevent

bad health conditions

(vs. 79% of global)

88% read packaging

labels carefully for nutrition

content

(vs. 75% of global)

89% willing to pay

more for foods that

promote health benefits

(vs. 76% of global)

Source; Nielsen Consumer Confidence Report Q3’17 | Global Ingredient and Dining-out Trends Report Aug’16 | Global Survey We are what we eat Jan’15

76% want to know

everything that is going into

their food

(vs. 74% of global)

13 Cop

yri

gh

t ©

20

17

Th

e N

iels

en

Com

pa

ny.

Co

nfid

en

tia

l a

nd

pro

pri

eta

ry.

Cop

yri

gh

t ©

20

17

Th

e N

iels

en

Com

pa

ny.

Co

nfid

en

tia

l a

nd

pro

pri

eta

ry.

Source: Nielsen Global Health Survey Q3’14.

Question: How willing are you to pay premium for foods that contain health attributes? How important are health attributes in influencing you to purchase more of a particular food/food products?

Top 15 attributes Vietnamese consumers consider when choosing healthy products

Calcium fortified

Vitamin fortified

Micronutrient fortified

Minerals fortified

Low / No cholesterol

Made from vegetables/ fruits

High in fiber

All natural

GMO free

Natural flavors

High in protein

No artificial colors

Organic

Ingredients sourced

sustainably/ fair trade

Low / No Fat

30

35

40

45

50

55

60

30 35 40 45 50 55 60

Impact on purchase intention (%)

Wil

lin

g t

o p

ay

pre

miu

m p

rize

fo

r (%

)

• Not differentiable

• Important/Expected attribute

• Differentiable

• Premium attribute

More is more

Less is more

Back to basic

14 Cop

yri

gh

t ©

20

17

Th

e N

iels

en

Com

pa

ny.

Co

nfid

en

tia

l a

nd

pro

pri

eta

ry.

Cop

yri

gh

t ©

20

17

Th

e N

iels

en

Com

pa

ny.

Co

nfid

en

tia

l a

nd

pro

pri

eta

ry.

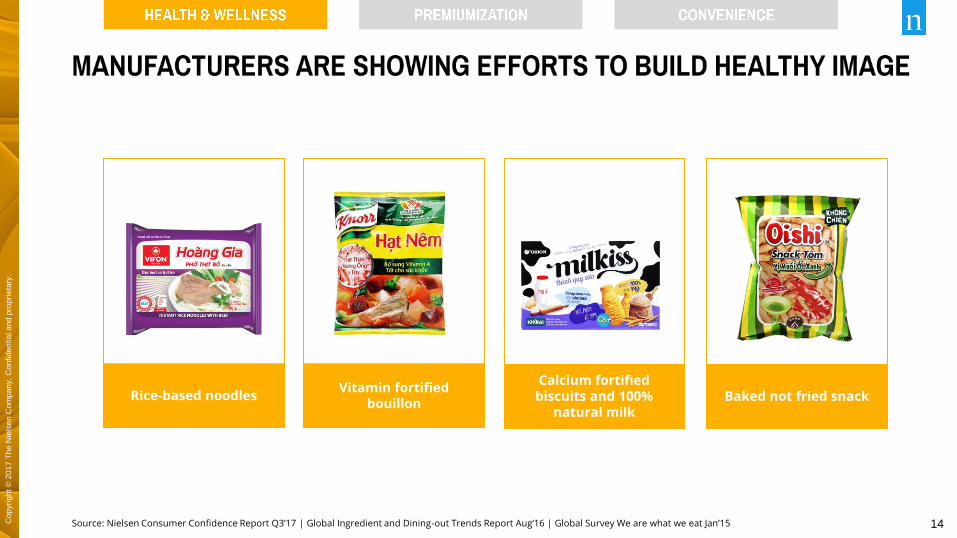

Source: Nielsen Consumer Confidence Report Q3’17 | Global Ingredient and Dining-out Trends Report Aug’16 | Global Survey We are what we eat Jan’15

Rice-based noodles Vitamin fortified

bouillon

Calcium fortified biscuits and 100%

natural milk Baked not fried snack

15 Cop

yri

gh

t ©

20

17

Th

e N

iels

en

Com

pa

ny.

Co

nfid

en

tia

l a

nd

pro

pri

eta

ry.

Cop

yri

gh

t ©

20

17

Th

e N

iels

en

Com

pa

ny.

Co

nfid

en

tia

l a

nd

pro

pri

eta

ry.

57%

63% 58%

60%

I trust health claims on food

packages

Health claims are just a way for

manufacturers to charge more

I feel more positively about

companies that are transparent

about how products were made

Global Vietnam

Source; Global Ingredient and Dining-out Trends Report Aug’16 | Global Survey We are what we eat Jan’15

73%

83%

16 Cop

yri

gh

t ©

20

17

Th

e N

iels

en

Com

pa

ny.

Co

nfid

en

tia

l a

nd

pro

pri

eta

ry.

Cop

yri

gh

t ©

20

17

Th

e N

iels

en

Com

pa

ny.

Co

nfid

en

tia

l a

nd

pro

pri

eta

ry.

Source; Nielsen Health Eating Survey, Ingredion Clean / Simple Label Report & Nielsen BASES

Clean + Concise + Traceable = Consumer Conviction

From CLEAN & CONCISE LABEL To TRACEABLE SOURCE

74% look for products

with simple & recognizable

list of ingredients

(vs. 64% of global)

Consumer Attraction Index

vs.

No/Untraceable claim

100 125

Traceable claim

Clean label Simple ingredients Trusted claim QRCode to trace

origin

17 Cop

yri

gh

t ©

20

17

Th

e N

iels

en

Com

pa

ny.

Co

nfid

en

tia

l a

nd

pro

pri

eta

ry.

Cop

yri

gh

t ©

20

17

Th

e N

iels

en

Com

pa

ny.

Co

nfid

en

tia

l a

nd

pro

pri

eta

ry.

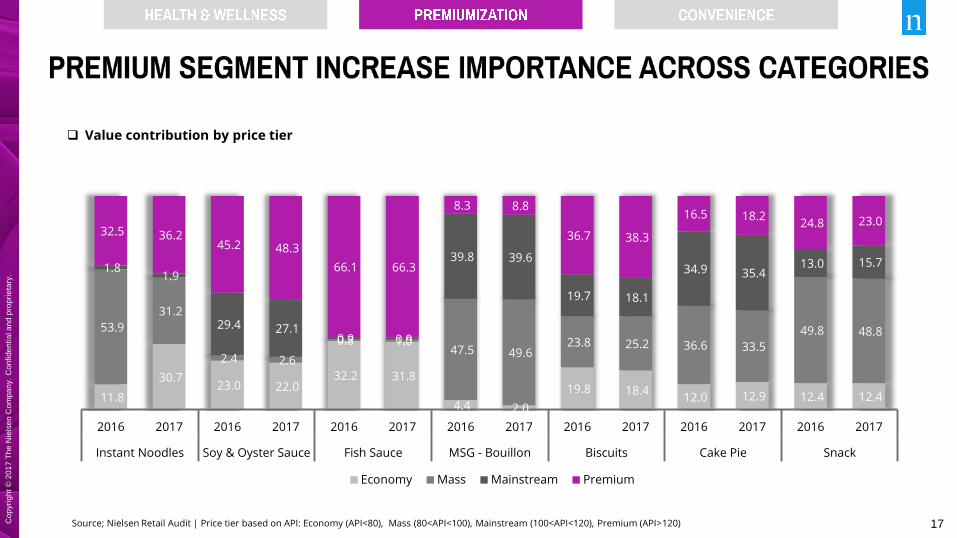

Source; Nielsen Retail Audit | Price tier based on API: Economy (API<80), Mass (80<API<100), Mainstream (100<API<120), Premium (API>120)

11.8

30.7 23.0 22.0

32.2 31.8

4.4 2.0

19.8 18.4 12.0 12.9 12.4 12.4

53.9

31.2

2.4 2.6

0.8 1.0 47.5 49.6

23.8 25.2 36.6 33.5

49.8 48.8

1.8 1.9

29.4 27.1 0.9 0.9

39.8 39.6

19.7 18.1

34.9 35.4 13.0 15.7

32.5 36.2 45.2 48.3

66.1 66.3

8.3 8.8

36.7 38.3

16.5 18.2 24.8 23.0

2016 2017 2016 2017 2016 2017 2016 2017 2016 2017 2016 2017 2016 2017

Instant Noodles Soy & Oyster Sauce Fish Sauce MSG - Bouillon Biscuits Cake Pie Snack

Economy Mass Mainstream Premium

Value contribution by price tier

18 Cop

yri

gh

t ©

20

17

Th

e N

iels

en

Com

pa

ny.

Co

nfid

en

tia

l a

nd

pro

pri

eta

ry.

Cop

yri

gh

t ©

20

17

Th

e N

iels

en

Com

pa

ny.

Co

nfid

en

tia

l a

nd

pro

pri

eta

ry.

Volume % Impact when SKU’s price change more than 5%

Source; Nielsen Retail Audit

Depending on one certain stage of the category, price adjustments have to be taken with caution

-40

26

-1

-17 -19 -23

-7

14

-9

-55

-35

-12

-38

21

1

0 -3

5 7 6 14

-80

-60

-40

-20

0

20

40

Instant Noodles Soy & Oyster Sauce Fish Sauce MSG - Bouillon Biscuits Cake Pie Snack

Price increase more than 5% Price decrease more than 5% No change in price

Price conscious

Premium thirst

New value seeker

New value seeker

New value seeker

New value seeker

Price conscious

*

* *

* Low base: Less than 1% share

PIE Share FY16 Share FY17 Contribution

to decline

Pie And Sponge Cake Thanh Hai Choco Pan Banh Mem Phu Socola Box 350 1X350 GM

10.4 0.0 -10

Pie And Sponge Cake An Pha Sweet Pandan Flavour Khay 210 1X210

GM 6.4 2.4 -5

Pie And Sponge Cake Orion Custas Milk Cream Box 184 1X184 GM 5.7 0.4 -5

Pie And Sponge Cake Nhat Viet Solote BBL Cuon Kem Vi Com Khay

270 1X270 GM 5.7 2.0 -4

Pie And Sponge Cake BK Hung Hanh Sapion Custard Cake Khay 225

1X225 GM 5.0 1.1 -4

Pie And Sponge Cake Bao Hung Custard (B.H) Custard Cake Khay 165

1X165 GM 3.5 1.1 -3

Pie And Sponge Cake G&G Sopitel Strawberry Cream Roll Khay 240

1X240 GM 3.0 0.1 -3

Pie And Sponge Cake BK Hung Hanh Sapion Strawberry Custard Cake

Khay 225 1X225 GM 2.7 3.6 0

BISC Share FY16 Share FY17 Contribution

to decline

Biscuits URC Tivoli Choco Coat Wafer Fill W Vani Soft Pack 369.6

1X369.6 GM 2.6 2.0 -1

Biscuits Tan Tien Phat Zone Banh Quy Kem Sau Rieng Soft Pack 8

1X8 GM 18.2 1.2 -17

MSG Share FY16 Share FY17 Contribution

to decline

Nestle Maggi Bouillon + Meal Maker Bouillon Granules Xuong Ham 3

Ngot Pork Bag 450 37.0 28.5 -19

Ha Anh Hoang Phu Cuong A Seasoning Powder (Bot Canh) Seasoning

Powder (Bot Canh) Bot Canh Shrimp & Chicken Bag 180 22.4 6.6 -18

Fish Sauce Share FY16 Share FY17 Contribution

to decline

Uniben 3 Mien (U.N) Regular PLBT 500 34.5 25.4 -23

Duc Vien Duc Tin (D.V) Regular PLBT 5000 3.1 5.1 -1

Decrease Increase

SOYSAUC Share FY16 Share FY17 Contribution

to growth

Oyster Nestle Maggi Regular PLBT 1X350 GM 22.8 21.2 4

Oyster Nestle Maggi Regular PLBT 1X820 GM 20.4 19.4 4

Soy Nuoc Cham Nam Duong Hang Viet Regular PLBT 1X495 ML 19.4 31.1 20

MSG Share FY16 Share FY17 Contribution

to decline

Unilever Knorr Bouillon + Meal Maker Bouillon Granules Shinbones

Tenderloin & Medulla Bag 400 44.1 49.6 -3

Uniben 3 Mien Bouillon + Meal Maker Bouillon Granules Thit & Xuong

Bag 400 14.1 16.5 0

Unilever Knorr Bouillon + Meal Maker Bouillon Granules Shinbones

Tenderloin & Medulla Bag 55 12.9 11.6 -3

Hifaco Jsc Awana Seasoning Powder (Bot Canh) Seasoning Powder

(Bot Canh) Bot Canh Shrimp Bag 200 9.7 7.3 -4

Saigon Ve Wong A-One Seasoning Powder (Bot Canh) Seasoning

Powder (Bot Canh) Bot Canh Iod Bag 200 1.8 0.3 -2

A Au A Au (A.A) Seasoning Powder (Bot Canh) Seasoning Powder (Bot

Canh) Bot Canh Chicken Bag 185 1.7 1.5 -1

Nguyen Binh Queen Msg Msg Msg Regular Bag 1000 1.5 0.5 -1

Saigon Ve Wong A-One Bouillon + Meal Maker Bouillon Granules Nuoc

Ham Xuong Bag 400 1.4 0.0 -1

BISC Share FY16 Share FY17 Contribution

to decline

Biscuits Cty 22 Huong Thao (Cty 22) Regular Soft Pack 235 1X235 GM 4.4 4.5 -1

Biscuits Mondelez Kinh Do Cosy Marie Regular Box 200 1X200 GM 3.3 3.8 0

Biscuits Tan Hoang Gia France (T.H.G) Butter France Soft Pack 400

1X400 GM 3.3 0.0 -3

Biscuits Mondelez Kinh Do Cosy Marie Regular Soft Pack 64 1X64 GM 2.0 0.5 -2

Biscuits Thien Hong Phat Thien Hong Phat Banh Quy Gac A+ Soft

Pack 180 1X180 GM 1.7 0.9 -1

Biscuits Kim Thien Phat Many Biscuits Soft Pack 320 1X320 GM 1.5 1.3 0

Biscuits Hoang Chien Thang HCT Banh Vong Vung Soft Pack 200

1X200 GM 1.4 1.1 0

Biscuits Bibica Cindy Assorted Biscuits Box 330 1X330 GM 1.3 1.3 0

Biscuits Thanh Do Dai Phat Loc (T.Do) Biscuits Soft Pack 180 1X180

GM 1.1 0.9 0

Biscuits URC Cream O Choco Sand.Cook W.Choco Soft Pack 54 1X54

GM 1.1 1.9 0

Biscuits HaiHaCo Soheart Banh Crack Kem Dua Bo Soft Pack 275

1X275 GM 1.0 0.4 -1

Biscuits Mondelez Kinh Do LU Petit Lu_Veritable Tin 600 1X600 GM 1.0 1.3 0

Biscuits Viet Long Dai Phat Loc (V.L) Banh Quy Soft Pack 180 1X180

GM 1.0 0.9 0

Biscuits Hoang Chien Thang New Star Banh Vong Vung Soft Pack 200

1X200 GM 1.0 0.4 -1

Biscuits Tan Hoang Gia France (T.H.G) Butter France Soft Pack 250

1X250 GM 1.0 3.0 1

Biscuits Dai Thang Dabico Wafer Choco Box 270 1X270 GM 1.0 0.2 -1

Biscuits Kelsen Copenhagen Danish Butter Cookies Tin 454 1X454 GM 0.9 0.3 -1

CAKEPIE Share FY16 Share FY17 Contribution

to decline

Pie And Sponge Cake Mondelez Kinh Do Solite Pandan Creamy Roll

Cake Khay 180 1X180 GM 25.9 30.0 -3

Pie And Sponge Cake Hoa Binh Confec Silate Pandan Roll Cake Khay

220 1X220 GM 4.3 0.3 -4

Pie And Sponge Cake BK Huu Nghi Huu Nghi Custard Cake Box 300

1X300 GM 4.1 3.6 -1

Pie And Sponge Cake Huong Giang Custard (H.G) Custard Cake Khay

210 1X210 GM 2.7 0.6 -2

Pie And Sponge Cake Hiep Thanh Loi Huro Custard Cake Khay 380

1X380 GM 2.7 0.2 -3

Pie And Sponge Cake Bibica Hura Deli BBL Kem Com Box 336 1X336

GM 2.4 0.3 -2

Pie And Sponge Cake Huong Giang Sogold Custard Cake Khay 320

1X320 GM 2.4 0.1 -2

Pie And Sponge Cake Biscafun Confec Nice (Biscafun) Chocolate Kem

Sau Rieng Soft Pack 216 1X234 GM 2.0 4.4 1

Pie And Sponge Cake Bibica Hura Strawberry Flavour Layer Cake

Khay 180 1X180 GM 1.9 0.8 -1

Pie And Sponge Cake Bibica Hura BBL Kem Com Box 300 1X300 GM 1.7 5.5 2

Pie And Sponge Cake BK Huu Nghi Salsa Sping Rice Fla Mini Roll

Cake Khay 180 1X180 GM 1.7 1.4 -1

Pie And Sponge Cake BK Huu Nghi Huu Nghi Custard Cake Khay 200

1X200 GM 1.7 0.2 -2

NOODLE Share FY16 Share FY17 Contribution

to decline

TP Thai Minh Mihamex Mi Shrimp Mi Soft Pack 1X70 GM 16.2 3.3 -14

Uniben Reeva Mi Beef Bo Ham Cai Chua Soft Pack 1X85 GM 15.2 17.7 -4

Masan Chin Su Mi Fish Xot Ca Hoi Chua Cay Soft Pack 1X75 GM 14.8 0.1 -15

Kinh Do An Hao Mi Chicken Ga La Giang Soft Pack 1X62 GM 5.9 0.1 -6

Uniben Reeva Mi Vegetable Lau Nam Chua Cay Soft Pack 1X85 GM 4.0 25.6 11

Masan Omachi Mi Beef Xot Spaghetti Xot Bo Bam Soft Pack 30X91

GM 3.3 4.4 -1

Afotech Cung Dinh Mi Shrimp Lau Tom Chua Cay Cup 1X80 GM 2.5 3.8 0

Masan Omachi Mi Shrimp Lau Tom Chua Cay Soft Pack 30X79 GM 2.4 2.7 -1

Uniben Reeva Mi Pork Suon Non Cai Chua Soft Pack 1X85 GM 2.3 1.2 -2

Ngoc Ha Tadico Mi Shrimp Mi Soft Pack 1X60 GM 2.1 1.6 -1

*

19 Cop

yri

gh

t ©

20

17

Th

e N

iels

en

Com

pa

ny.

Co

nfid

en

tia

l a

nd

pro

pri

eta

ry.

Cop

yri

gh

t ©

20

17

Th

e N

iels

en

Com

pa

ny.

Co

nfid

en

tia

l a

nd

pro

pri

eta

ry.

API range of premium products

Source; Nielsen Retail Audit | Most successful: Highest share premium variant’s API | Average: Weighted average API of premium variant based on sales value | Most common: Mode of all premium variants’ API

For some categories, there is mismatch between what manufacturers offer and what consumers accept

120

140

160

180

200

220

240

260

Instant

Noodles

Soy & Oyster

Sauce

Fish Sauce MSG -

Bouillon

Biscuits Cake Pie Snack

Most successful Average Most common Optimal range

• Most successful/

Average API: Indicate at

what API level

consumers have the

most support

• Most common API:

Indicate at what API level

manufacturers are

mostly pushing into

20 Cop

yri

gh

t ©

20

17

Th

e N

iels

en

Com

pa

ny.

Co

nfid

en

tia

l a

nd

pro

pri

eta

ry.

Cop

yri

gh

t ©

20

17

Th

e N

iels

en

Com

pa

ny.

Co

nfid

en

tia

l a

nd

pro

pri

eta

ry.

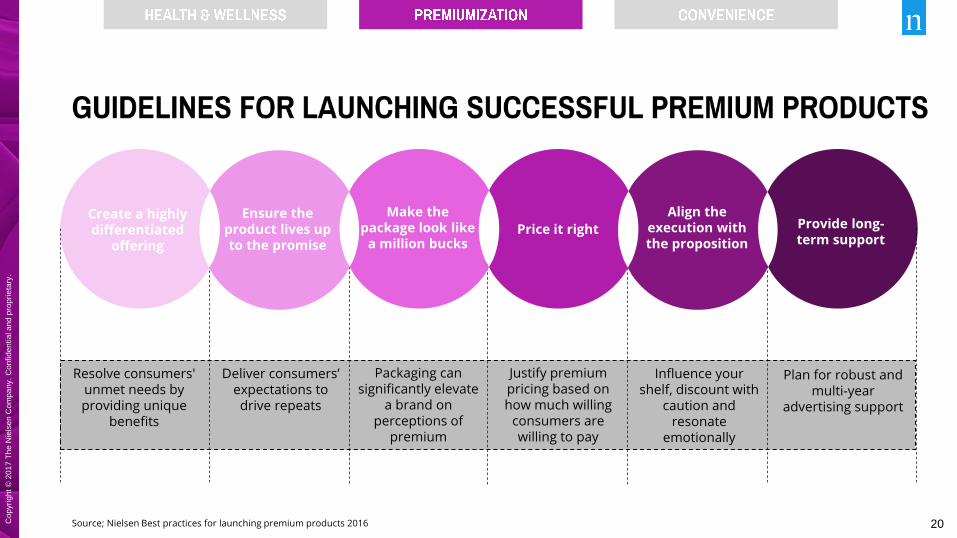

Resolve consumers' unmet needs by providing unique

benefits

Source; Nielsen Best practices for launching premium products 2016

Create a highly differentiated

offering

Ensure the product lives up to the promise

Make the package look like

a million bucks Price it right

Align the execution with the proposition

Provide long-term support

Deliver consumers’ expectations to drive repeats

Packaging can significantly elevate

a brand on perceptions of

premium

Justify premium pricing based on how much willing

consumers are willing to pay

Influence your shelf, discount with

caution and resonate

emotionally

Plan for robust and multi-year

advertising support

21 Cop

yri

gh

t ©

20

17

Th

e N

iels

en

Com

pa

ny.

Co

nfid

en

tia

l a

nd

pro

pri

eta

ry.

Cop

yri

gh

t ©

20

17

Th

e N

iels

en

Com

pa

ny.

Co

nfid

en

tia

l a

nd

pro

pri

eta

ry.

Source; United Nations, WUP, 2014 for population data. EIU for household & wage data.

Vietnam population dynamics 2015 – 2015

34% 40%

66% 60%

2015 2025

Urban Rural

% population by urbanity

% urban population by city size in people

49% 40%

3% 10%

6%

19% 26%

23% 23%

2015 2025

<300K 300k-500k 500k-1M

1M-5M 5M-10M 10M+

4.49 4.31

4.13 3.96 3.81 3.76 3.70 3.60 3.60 3.50 3.50

0

50

100

150

200

250

300

350

400

450

500

0.00

1.00

2.00

3.00

4.00

5.00

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

Average HH size (person) Average wages per month (USD)

Household size & Average wages per month

22 Cop

yri

gh

t ©

20

17

Th

e N

iels

en

Com

pa

ny.

Co

nfid

en

tia

l a

nd

pro

pri

eta

ry.

Cop

yri

gh

t ©

20

17

Th

e N

iels

en

Com

pa

ny.

Co

nfid

en

tia

l a

nd

pro

pri

eta

ry.

Number of Chained Convenient store & Minimart (stores)

Source: Retailers’ official website. CVS includes Circle K, B’s Mart, Family Mart, Shop & Go, Mini Stop, 7-eleven. MM includes: VinMart+, Coop Food, SatraFoods, Bach Hoa Xanh, Coop Smile, T-Mart, My Auchan. Nielsen Shopper Trend 2016 - Total Hanoi & Ho Chi Minh (All HM/SM shoppers n=1346)

700 699 711 728 731 745 744 774 783 788 795 818 827 823

1134 1281 1313 1227 1230 1278 1319 1358 1399 1456 1557

1726 1810 1817

0

500

1000

1500

2000

2500

3000

Convenient Store Minimart

Top 3 important attributes for shopping destination

(index)

Easy to find what I

need

Convenient to get to

Low prices

SUPERMARKET

CVS/MM

Efficient checkout Easy to find

what I need

Convenient to get to

7.7 6.6 5.7

9.7 9.0 7.8

23 Cop

yri

gh

t ©

20

17

Th

e N

iels

en

Com

pa

ny.

Co

nfid

en

tia

l a

nd

pro

pri

eta

ry.

Cop

yri

gh

t ©

20

17

Th

e N

iels

en

Com

pa

ny.

Co

nfid

en

tia

l a

nd

pro

pri

eta

ry.

WHAT IS HAPPENING HOW IT INDICATES

1

2

3

URBANIZATION

More and more people living

in Urban and high density

cities

HOUSEHOLD

Increase in single + non-

traditional households (with

more income and less

dependents)

RETAIL

Expansion of CVS/MM and

needs of convenience in

shopping occasions

• Focus on smaller packtype

• Capture demand for convenience, on-the-

go solutions

• Bridge gaps in consumer needs from

existing retail environment via E-commerce

and delivery options

• Create strategies to capture valued single

segment

• Explore premium and luxury opportunities

Source: Nielsen APAC – What’s next start now 2018

24 Cop

yri

gh

t ©

20

17

Th

e N

iels

en

Com

pa

ny.

Co

nfid

en

tia

l a

nd

pro

pri

eta

ry.

Cop

yri

gh

t ©

20

17

Th

e N

iels

en

Com

pa

ny.

Co

nfid

en

tia

l a

nd

pro

pri

eta

ry.

INSTANT NOODLES CUP

4.2

6.7

2016 2017

Value % Share

Value % Growth

69%

PRE-MIXED SOY SAUCE

11.9 12.1

2016 2017

Value % Share

Value % Growth

4%

BISCUITS (<= 150GM)

23.5 27.2

2016 2017

Value % Share

Value % Growth

30%

CAKE PIE (<= 150GM)

9.3 10.4

2016 2017

Value % Share

Value % Growth

21%

FROZEN FOOD/SAUSAGE

Source: Nielsen Retail Audit | Data for Total Vietnam exclude Frozen Food/Sausage is MT only

Value % Growth

9%

Frozen Food

26%

Sausage

25 Cop

yri

gh

t ©

20

17

Th

e N

iels

en

Com

pa

ny.

Co

nfid

en

tia

l a

nd

pro

pri

eta

ry.

26 Cop

yri

gh

t ©

20

17

Th

e N

iels

en

Com

pa

ny.

Co

nfid

en

tia

l a

nd

pro

pri

eta

ry.

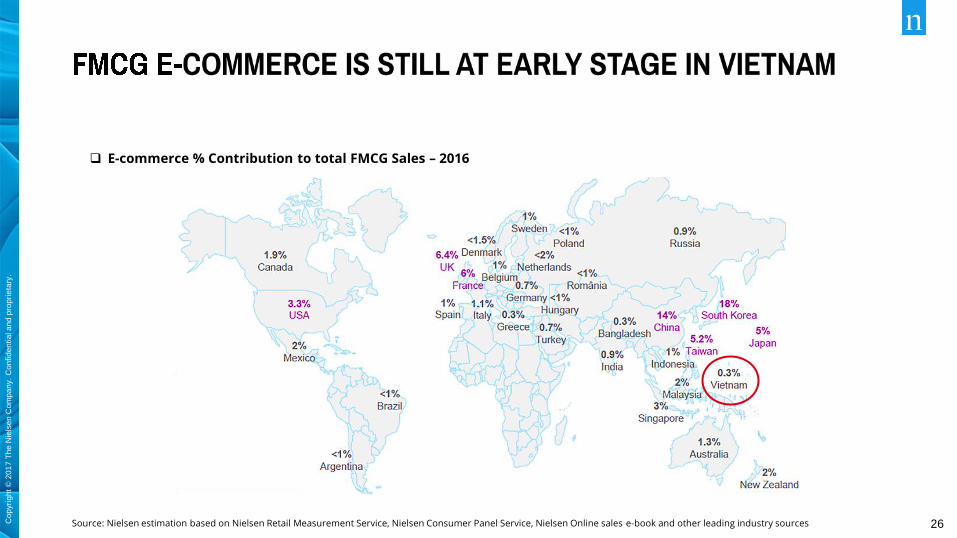

E-commerce % Contribution to total FMCG Sales – 2016

Source: Nielsen estimation based on Nielsen Retail Measurement Service, Nielsen Consumer Panel Service, Nielsen Online sales e-book and other leading industry sources

27 Cop

yri

gh

t ©

20

17

Th

e N

iels

en

Com

pa

ny.

Co

nfid

en

tia

l a

nd

pro

pri

eta

ry.

Vietnam FMCG E-commerce foundational elements

Source: CIA World Factbook; Nielsen: Cross Platform Insights 2016. *as compared to total 30 developed & developing countries – Nielsen global key drivers for Grocery E-commerce 2018

49 52 54 55

2017 2018 2019 2020

Minimum level for significant FMCG E-commerce size*

80

INTERNET PENETRATION

44 50

55 59

2017 2018 2019 2020

Minimum level for significant FMCG E-commerce size*

67

SMART PHONE PENETRATION

28 Cop

yri

gh

t ©

20

17

Th

e N

iels

en

Com

pa

ny.

Co

nfid

en

tia

l a

nd

pro

pri

eta

ry.

Have internet access Are willing to spend

discretionary income

WHO ARE THEY? HOW THEY ACT?

40 Million people in 2025 (x1.7 vs 2017)

99 Billion USD of annual spending in 2025 (x2.0 vs 2017)

48% Total consumer spending in 2025 (x1.3 vs 2017)

99 Normal Internet

User

117 Connected Spenders

Confidence Index

They stay connected with brands

Engage with other viewers on social media while

watching advertising

Appreciate learning about products through

advertising

Expect a relevant and personalized advertising

experience

77%

53%

54%

They review products online before making purchase

Read product

review and

feedbacks

73% Check

promotion

70% Check brand’s

reputation

and quality

Source: Demand Institutes, Nielsen Omni - Shopper Trend 2017

64%

29 Cop

yri

gh

t ©

20

17

Th

e N

iels

en

Com

pa

ny.

Co

nfid

en

tia

l a

nd

pro

pri

eta

ry.

Categories Vietnamese online shopper purchased in L3M

61

49 41 40 38 36 34 31 29 27 24 23

Fashion Cosmetics Personal

care

Books/

Stationary

IT & Mobile Consumer

electronics

Home care

products

Grocery

food

Travel Beverage Baby care

products

Event

tickets

Source: Nielsen Omni - Shopper Trend 2017 - All respondents Total (n=1005)

30 Cop

yri

gh

t ©

20

17

Th

e N

iels

en

Com

pa

ny.

Co

nfid

en

tia

l a

nd

pro

pri

eta

ry.

Actively engage with consumers throughout the

whole buying process via online platform,

especially during information searching and

purchase decision making

Ensure authentic products are sold on

online portals. Crackdown on counterfeit

products.

Invest in innovative and

personalized online

marketing experience for

consumers

FOOD E-COMMERCE

BUILD TRUST

DISRUPT PATH-TO-

PURCHASE

LEVERAGE BRANDING

OPPORTUNITIES

Source: Nielsen global key drivers for Grocery E-commerce 2018

Copyright © 2017 The Nielsen Company. Confidential and proprietary.

Top 3 fastest growing

super categories, but

growth is not common

across Regular and Impulse

Innovation is crucial, but

not easy to succeed.

Winning formula:

DISTINCTIVENESS +

ENDURANCE + RELEVANCE

Knowing what is healthy and how

to win consumer’s trust

Knowing how much is premium

and how to deliver premium

Knowing the need of

‘faster-and-smaller’ products

Manufacturers can

embrace E-commerce to

build trust, disrupt path-to-

purchase and leverage

branding opportunities

Copyright © 2017 The Nielsen Company. Confidential and proprietary.