Embed Size (px)

Citation preview

Premium FinancingTechnical Guide

2HCB Premium Financing Technical Guide

Table of Contents

3 Overview of Premium Financing

4 Uses of Premium Financing

4 Client Profile

5 Advantages of Premium Financing Plans

5 Disadvantages of Premium Financing Plans

6 Types of Policies Suitable for Premium Financing

6 Case Study

7 Pay Me Now, Pay Me Later

8 Exit Strategies

9 Risks & the Importance of Stress Testing

10 Gift, Estate and Income Tax Considerations

12 Other Considerations

3HCB Premium Financing Technical Guide

OverviewPremium financing is a strategy designed to help Clients acquire life insurance for which they have an established need by borrowing the funds necessary to pay the premiums from a commercial lender. The policy is pledged as collateral for the loan. To the extent that policy cash surrender values are insufficient to secure the loan, the client will post additional collateral. Should the insured(s) die prior to the repayment of the premium loan, the outstanding loan is repaid from the policy proceeds. In addition, in the estate planning context where the policy will be owned by a trust, it is recommended that an exit strategy be implemented in order to provide funds to repay the loan as well as pay ongoing premiums once the loan is repaid.

Loan interest is typically tied to an external measure such as 1-month or 12-month LIBOR or Prime lending rate plus a spread. The loan interest will fluctuate as the underlying benchmark rate fluctuates. For example, if a bank lends funds at 12-month LIBOR + 185 basis points, the loan rate will change on each anniversary tied to the then current LIBOR+ 185 basis points. Longer term fixed loan rate programs are available at higher level borrowing rates. Loan interest is typically paid annually in cash, although alternative designs such as accruing interest or a combination may be available.

The best use of premium financing is for short term financing, i.e. 3-5 years, or, as a rule of thumb, no longer than 15 years. An exit strategy for repaying the loan other than from policy values is strongly recommended for all plan designs.

Careful consideration should be made to determine whether premium financing is suitable for a Client. The client, and his or her legal and tax advisor, should determine the client’s risk tolerance and decide whether the concept is an acceptable risk.

4HCB Premium Financing Technical Guide

Uses for Premium Financing

Estate Planning Life insurance is a key component of many Clients’ estate plan with the policy owned by an irrevocable life insurance trust (ILIT or Trust) for the benefit of the Client’s spouse, children, grandchildren and subsequent generations. The question that must be addressed is, “What is the best way to pay for the coverage?” Premium financing can be an attractive funding strategy that compliments other non-life insurance estate planning strategies. During the early years of the plan, the annual loan interest is substantially less than paying the full annual premium, resulting in smaller initial gifts to the ILIT to fund the coverage.

Business Planning Businesses can use premium financing in a variety of different ways. A business might borrow the funds to obtain life insurance for key-person coverage, finance a non-qualified deferred compensation plan, set up a death benefit only plan for a key executive or obtain coverage for a buy/sell arrangement.

Client Profile

• High net worth ($10M for married couples, $5 million in the case of an individual)

• Need for substantial life insurance ($100k minimum initial loan available with some lenders)

• Insurable at favorable rates

• Sophisticated investor who understands complex financial transactions

- Understands the risks outlined below

- Understands the need for a rollout or exit strategy

• Has adequate assets acceptable to lender to post as collateral

- Cash

- CDs

- Marketable Securities

- Access to Letter of Credit

- High Cash Value non-MEC Life Insurance Policies from a Highly Rated Carrier

5HCB Premium Financing Technical Guide

Advantages of Premium Financing Plans

• The client can purchase life insurance with little initial impact on current cash flow or without having to liquidate existing investments (thus avoiding taxable gain upon liquidation). Note: See “Pay Me Now, Pay Me Later” discussion below.

• Premium financing can produce positive interest rate arbitrage if the after-tax growth in policy cash value and/or the growth in the Clients’ investments exceed the interest on the underlying loan.

• The client can take advantage of gift tax leveraging. Life insurance, with an immediate death benefit, compliments non-life insurance estate planning strategies that all take time to transfer substantial wealth. Premium financing can minimize short to mid-term gifting.

• If the policy is owned outside the insured’s estate, premium financing could eliminate the need to gift the entire premium. Only the loan interest may need to be gifted annually. Note: See “Pay Me Now, Pay Me Later” discussion below.

• If the lender allows the loan to be structured so that interest accrues and provide the policy performs very well, no gifting may be necessary.

Disadvantages of Premium Financing Plans

• Premium financing is a highly complex strategy that involves several risks (see more detailed discussion below):

- Policy performance risk

- Interest rate risk

- Policy lapse risk

- Collateral call risk

- Gift tax risk

- Income tax risk

• Over time, as each additional premium is borrowed, the interest cost increases and the net death benefit decreases by the amount of the outstanding loan. Note: See “Pay Me Now, Pay Me Later” discussion below.

• If the policy is owned outside the estate and interest is paid annually via gifts to the trust, gift tax issues could arise if the loan interest exceeds the client’s annual gift tax exclusions and lifetime exemption.

• Fluctuations in future interest rates could have a major impact on the life insurance policy and underlying premium loan.

6HCB Premium Financing Technical Guide

Types of Policies Suitable for Premium Financing

• Policies with strong cash values, whether survivorship or single life, are suitable for premium financing. Therefore, current assumption universal life (UL), Whole Life (WL) and indexed universal life (IUL) are good candidates. Because of current low crediting rates on current assumption UL and WL, for Clients who are comfortable investing in the stock market, IUL tends to be more attractive.

• Variable UL is not suitable because, as a security, it is subject to the margin loan rules limiting the amount of the loan that can be secured with policy cash values. (See below.)

• Guaranteed UL policies are generally not suitable due to the fact that cash values are very low or non-existent, requiring the Client to post substantially greater collateral.

• Term policies are generally not suitable for the same reason, i.e. cash values are non-existent, requiring the Client to post substantially greater collateral.

Case Study

Husband and Wife are each 60-years old and in excellent health. They have a substantial net worth acquired as real estate developers. Clients’ attorney has recommended $10 million of survivorship coverage for estate planning purposes with a $100,000 annual premium payable for lifetime owned by and payable to an irrevocable life insurance trust (ILIT). Client is heavily invested in real estate, and likes the concept of using other people’s money to fund the coverage. The Client expects to sell substantial properties in the next 3-5 years, freeing up funds to repay the loan and pay future premiums.

1. The Client or Clients create an ILIT.

2. The ILIT enters into a premium financing arrangement with a third part commercial lender (possibly the Client’s bank).

3. The ILIT will borrow each annual premium for up to seven years, pay the policy loan interest, posting the policy cash value and a portion of the death benefit as collateral.

4. To the extent that the policy cash value is insufficient to secure the loan, the Client posts collateral in the form of cash, marketable securities or a letter-of-credit acceptable to the lender.

5. Assuming the current loan rate is 5% (and will remain at that rate), loan interest on a $100,000 annual premium equals $5,000. The Client gifts $5,000 to the ILIT. Note: Borrowing rates typically vary at least annually. The level 5% rate is assumed for the sake of simplicity.

6. In the second year, an additional premium is borrowed for a total loan of $200,000, and the loan interest is $10,000. After 5-years, the total loan would equal $500,000 with an annual interest payments of $25,000.

7. At the same time that the ILIT purchases the policy, the Client gifts an interest in the discounted real estate that the clients expects to sell in the next 3-5 years. This acts as an exit strategy by providing a source of funds in the ILIT to repay the loan in the future and generate cash flow to pay future premiums.

8. Upon death, the policy proceeds are paid to the ILIT, net of the outstanding loan balance. Net proceeds or assets purchased from the estate with such proceeds are then managed and distributed according to the terms of the ILIT.

7HCB Premium Financing Technical Guide

“Pay Me Now, Pay Me Later” or The Importance of an Exit Strategy

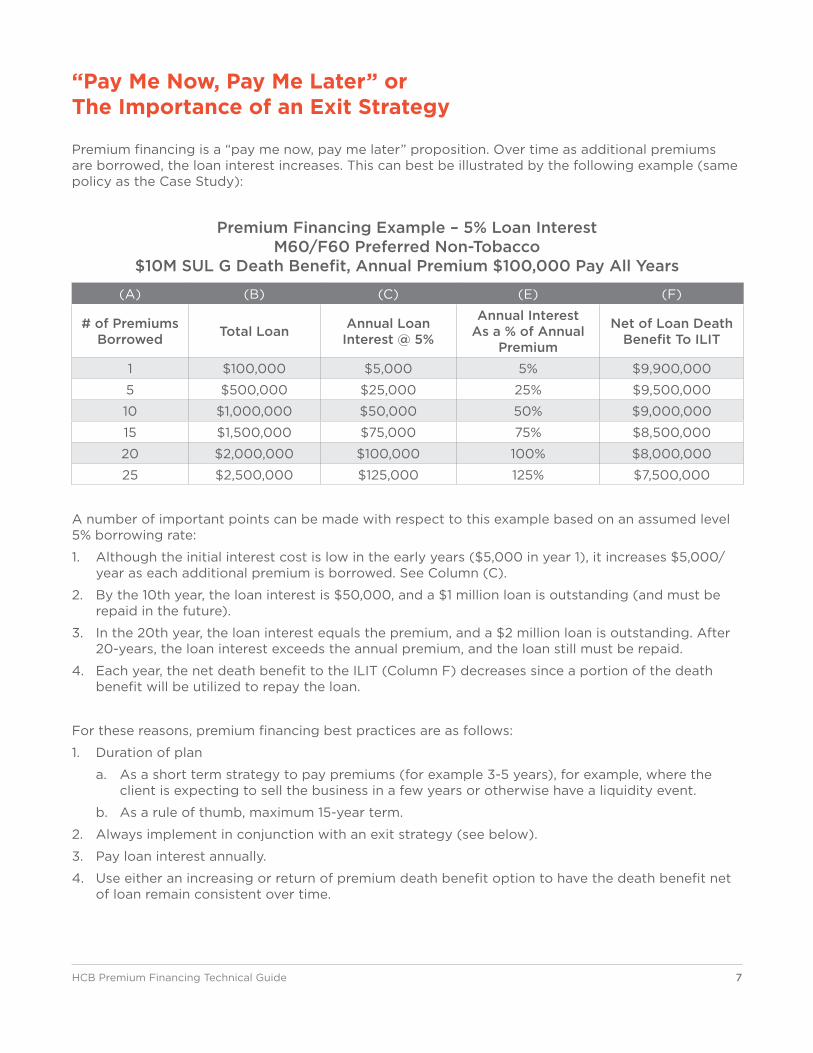

Premium financing is a “pay me now, pay me later” proposition. Over time as additional premiums are borrowed, the loan interest increases. This can best be illustrated by the following example (same policy as the Case Study):

Premium Financing Example – 5% Loan Interest M60/F60 Preferred Non-Tobacco

$10M SUL G Death Benefit, Annual Premium $100,000 Pay All Years

(A) (B) (C) (E) (F)

# of Premiums Borrowed Total Loan Annual Loan

Interest @ 5%

Annual Interest As a % of Annual

Premium

Net of Loan Death Benefit To ILIT

1 $100,000 $5,000 5% $9,900,000

5 $500,000 $25,000 25% $9,500,000

10 $1,000,000 $50,000 50% $9,000,000

15 $1,500,000 $75,000 75% $8,500,000

20 $2,000,000 $100,000 100% $8,000,000

25 $2,500,000 $125,000 125% $7,500,000

A number of important points can be made with respect to this example based on an assumed level 5% borrowing rate:

1. Although the initial interest cost is low in the early years ($5,000 in year 1), it increases $5,000/year as each additional premium is borrowed. See Column (C).

2. By the 10th year, the loan interest is $50,000, and a $1 million loan is outstanding (and must be repaid in the future).

3. In the 20th year, the loan interest equals the premium, and a $2 million loan is outstanding. After 20-years, the loan interest exceeds the annual premium, and the loan still must be repaid.

4. Each year, the net death benefit to the ILIT (Column F) decreases since a portion of the death benefit will be utilized to repay the loan.

For these reasons, premium financing best practices are as follows:

1. Duration of plan

a. As a short term strategy to pay premiums (for example 3-5 years), for example, where the client is expecting to sell the business in a few years or otherwise have a liquidity event.

b. As a rule of thumb, maximum 15-year term.

2. Always implement in conjunction with an exit strategy (see below).

3. Pay loan interest annually.

4. Use either an increasing or return of premium death benefit option to have the death benefit net of loan remain consistent over time.

8HCB Premium Financing Technical Guide

Exit Strategies

For premium financing plans, it is highly recommended that an exit (or rollout) strategy be designed and implemented at the same time as or in the early years of the premium financing plan. The following are examples of some of the most common exit strategies that can be used when an irrevocable life insurance trust (ILIT or trust) is a party to the premium financing arrangement.

Policy Death Benefit At death, the outstanding loan balance (including any accrued interest) is repaid to the lender and the net death benefit is paid to beneficiaries. This is generally considered a more aggressive strategy due to the risk of the insured(s) living too long with substantially increasing interest costs and a diminishing death benefit (net of the outstanding loan balance). Since it is not guaranteed, policy underperformance poses an additional risk.

Policy Values This rollout technique assumes the policy cash values will be sufficient at some point in the future so that the policyowner can make tax favored withdrawals from the policy (provided the policy is not a modified endowment contract) to pay all or a portion of the outstanding loan balance without causing the policy to lapse prior to the client’s death. Withdrawals are typically comprised of surrender of cash values up to cost basis, followed by policy loans.

While it may be possible to create a policy illustration that shows a rollout via policy values, it should be kept in mind that the illustrated policy values are not guaranteed. There is a risk that the cash value may not be sufficient to repay the loan plus accrued interest as projected. As a result, a client should consider other wealth transfer strategies (discussed below) to augment policy values and hedge policy underperformance.

In some premium financing programs, interest is not paid but rather it is accrued or “capitalized”. Accrual of loan interest increases the outstanding loan balance and, when policy cash values are being used as an exit strategy, puts a greater demand on policy when it comes time to repay the loan. This more aggressive strategy should only be entered into by clients with a full understanding of the potential risks and rewards of such a design. Stress testing the policy and lending assumptions is strongly advised.

Annual Exclusion and Lifetime Exemption Gifts Gifts can be an attractive wealth transfer strategy to compliment policy cash values in a premium financing program. The ILIT can use gifts to pay loan interest, invest excess gifts in a side fund and use those amounts to supplement policy cash values to repay the loan. The annual gift tax exclusion allows each individual to gift $15,000 annually to each child ($30,000 combined for a married couple). The lifetime gift exemption allows each individual to gift $11.18 million during their lifetime ($22.36 million combined for a married couple). Both the annual gift tax exclusion and the lifetime gift exemption allow gifts to be made directly to children and other beneficiaries or in trust for their benefit and are indexed for inflation.

Please note that the comments herein do not constitute legal or tax advice or a legal or tax opinion. Any decision to implement the ideas or comments discussed herein shall be made solely by the client on the advice of his or her legal and tax advisors. Highland Capital Brokerage and its employees are not engaged in the practice of law, are not acting as legal or tax advisors to clients nor are they establishing an attorney-client relationship with the client.

9HCB Premium Financing Technical Guide

Grantor Retained Annuity Trust (GRAT) The grantor retained annuity trust (GRAT) is a wealth transfer strategy that can be used as a rollout technique for premium financing. The GRAT pays a fixed amount each year to the grantor (the “retained annuity”) for a set term of years and, provided the grantor survives the GRAT term, distributes assets to the remainder beneficiary, typically children or a trust for their benefit. The higher the annual payout and the longer the payout term, the smaller the value of the gift to the remainder beneficiary. Funding the GRAT with discounted assets such as non-managing interests in a limited liability company (LLC) increases the efficiency of the GRAT as a wealth transfer vehicle.

As a premium financing exit strategy, at the end of the GRAT term, the ILIT (as the remainder beneficiary) receives any assets remaining. The ILIT can utilize those funds to repay all or part of the outstanding loan.

Note: The GRAT is a useful strategy when the insurance is owned by the ILIT for the benefit of children. When the insurance is also for the benefit of grandchildren and subsequent generations (i.e. in a Dynasty Trust), the sale to a defective trust discussed below is considered a superior strategy.

Gift and/or Sale to a Dynasty Trust Defective Grantor Trust Client creates an ILIT that is a Dynasty Trust, i.e. a trust that is for the benefit of children, grandchildren, and/or future generations. The trust is a defective grantor trust for income tax purposes. This means that all income taxes generated by the Trust are paid by the Client (the Grantor), and if the grantor sells appreciated assets to the Trust, no gain is recognized on the sale. The grantor gifts assets to the trust with the lifetime gift exemption ($11.18 million/$22.36 million combined for a married couple) or sells discounted assets to the trust. Assets appreciate in the Trust and can be used to 1) pay loan interest due, 2) terminate the premium financing arrangement by repay the outstanding loan balance, and 3) pay future premiums from cash flow.

Charitable Lead Unitrust or Annuity Trust (CLUT or CLAT) A Charitable Lead Annuity Trust (CLAT) pays a fixed amount to charity each year for a fixed term. At the end of the term, any remaining assets pass to the ILIT and can be used to 1) terminate the premium financing arrangement by repaying the lender the outstanding loan balance, and 2) paying future premiums from cash flow. The grantor is entitled to a charitable income tax deduction for the payouts to a qualified charity.

Risks & the Importance of Stress Testing

Policy Performance Risk Policy values of policies utilized with premium financing plans are not guaranteed. Those values could be impacted by deteriorating mortality, expense or crediting rate experience. Since policy cash values are pledged as collateral for the loan and may be used as a source for repaying all or a portion of the loan, it is important to understand that the policy could perform worse than current assumptions illustrate and have a significant effect on the financing plan.

Note: Conversely, an improvement in policy performance could have a positive impact on the program.

10HCB Premium Financing Technical Guide

Loan interest Rate Risk In securing a loan to pay premiums, the lender may offer a variable monthly or annual loan rate, or one that is guaranteed for a limited period of time. As a result, over time there could be substantial fluctuations and increases in loan interest rates. Changing rates can dramatically affect the performance and costs of a program as follows:

1. Higher interest costs.

2. Posting of a greater amount of supplemental collateral.

Note: If policy performance and loan interest rates worsen together and/or if loan interest is capitalized (i.e. accrued), the effect of higher interest rates on the outstanding loan and additional collateral required is even more dramatic.

Collateral Call Risk The lender’s primary concern is security of the borrowed funds. In a typical premium financing arrangement, the ILIT pledges the life insurance policy as collateral to the loan. To the extent that cash surrender value is insufficient to secure the loan, the grantor pledges supplemental collateral. In the event of a loan default, the lender could call both forms of collateral. The surrender of the policy to repay the lender could trigger substantial income tax gain and the collateral call of the supplemental collateral posted by the grantor would create a taxable gift to the ILIT.

Loan Qualification Risk Loans are typically for a specified term, e.g., one, five or 10 years. At the conclusion of the loan term, the borrower must re-qualify for a new loan term. If the borrower is unable to re-qualify for a new loan term, then the borrower will have to either repay the loan or find another lending institution. If new financing cannot be obtained, then the negative results outlined above could occur.

The Importance of Stress Testing In order to educate advisors and clients on the risks inherent in a premium financing program, it is important to “Stress Test” the proposed plan. Stress testing involved the following:

1. Illustrating the program with reasonable and typically increasing future borrowing rates.

2. Illustrate the policy with lower crediting rates.

3. Illustrate the combined effect of 1 and 2.

Gift, Estate and Income Tax Considerations

Gift Tax Considerations Gift tax issues can arise when a trust is the owner of the life insurance policy involved in premium financing, particularly upon payment of loan interest and loan collateral guarantees.

Borrowing by an ILIT to pay premiums does not constitute a gift to the Trust. Most premium financing cases are designed where the Trust pays the loan interest each year. Since most ILITs are unfunded (i.e. they don’t have assets other than the insurance policy), the client must make gifts to the Trust in order to provide the funds needed to pay loan interest.

Those gifts may qualify for the annual gift tax exclusion. To qualify for the annual gift tax exclusion ($15,000 for 2018 and indexed for inflation) the gift must be of a present interest. The trust should have Crummey powers that give the beneficiary the right, for a limited period of time, to withdraw any gifts in order to facilitate the present interest treatment. If the client wishes to have all interest

11HCB Premium Financing Technical Guide

payments qualify for the gift tax exclusion, he or she will need to ensure that the trust has enough Crummey beneficiaries to cover the interest payments.

As an alternative, the client may decide to use lifetime gift exemptions (in 2018, $11.18 million per person, i.e. $22.36 million husband and wife combined) to shelter gifts to the Trust to pay interest. If the ILIT is a Dynasty Trust (a trust for the benefit of children, grandchildren and subsequent generations), the client is more likely to use lifetime gift exemptions and will be required to us generation skipping transfer tax (also, $11.18 million per person, i.e. $22.36 million husband and wife combined).

Lifetime gift (and GST exemptions) are also more likely to be utilized with the selected exit strategy (see above). In addition, income producing assets transferred to fund an exit strategy could very well produce sufficient income to pay loan interest (for example, if commercial real estate interests with strong cash flow were gifted to the Trust).

In the majority of premium financing transactions involving estate planning, a trust owns the policy and obtains the loan to pay premiums, pledging the policy as the primary collateral. Normally the cash surrender value accumulates over time. However, the policy values are almost always insufficient to fully secure the loan in the early years. In most cases the lender might require the client to guarantee the loan on behalf of the trust.

Although this constitutes a gray area, the consensus is that the mere guarantee is not a taxable gift to the Trust. The IRS and courts have offered no clear guidance regarding the tax consequences of such a guarantee in the premium financing setting. In PLR 9409018, the IRS withdrew an earlier ruling (PLR 9113009) holding that a father’s guarantee of his child’s loan constituted a taxable gift to the borrower. The only court decision that addressed the gift taxation of a loan guarantee was Bradford v. Comm., 34 T.C., a 1960 ruling that held that a taxpayer’s guarantee of another person’s debt was not a taxable gift. IRC §2501 assesses gift taxation on transfers of property. The theory is that the loan guarantee is not an actual transfer of property, only a promise to pay in the future. Thus no gift taxation exists until the collateral actually has to be paid to the lender.

A more conservative position might be for the ILIT to pay the grantor a fee (for example 25-50 basis points of the amount guaranteed each year), or for the guarantor to declare a gift equal to the cost of obtaining a letter of credit in an arm’s length transaction.

In all cases, the client should consult his or her tax or legal advisor before proceeding.

Estate tax As with any life insurance, the insured must avoid holding any “incidents-of-ownership” in the policy to avoid inclusion of the death benefit in his or her estate (IRC Code §2042). Incidents of ownership include the right to change the beneficiary, to surrender or cancel the policy, to assign the policy, to revoke an assignment, to pledge the policy for a loan and to obtain a policy loan [Treas. Reg. §20.2042-1(c)(2)]. If the Trust is the owner and beneficiary of the policy from the outset, then the insured should not have any incidents of ownership.

An issue that frequently arises is whether an insured’s guarantee of a premium financing loan causes inclusion of the death benefit in his or her estate. Since a guarantee does not constitute an incident of ownership, it should not cause any estate inclusion. In PLR 9809032, the IRS indicated that the insured’s loans to a trust to pay premiums did not create an incident-of-ownership. If the insured’s own premium loans to the trust do not constitute an incident-of-ownership, then it would appear that the insured’s guarantee of a loan taken by the trust from a third party would also not create one either.

12HCB Premium Financing Technical Guide

Income tax Generally, there are no income tax consequences with premium financing. Any monies the client gives with regard to annual loan interest payments by the trust on the loan are subject to gift taxation and applicable annual exclusions. Provided there has not been a transfer-for-value, the life insurance policy proceeds at death are received income tax-free pursuant to IRC §101(a).

However, if the bank requires supplemental collateral from the client as an additional guarantee on the loans associated with the premium financing transaction, a collateral call could subject the client to income tax consequences as a result of the gains triggered in the collateralized property.

Likewise, a collateral call by the lender requiring the Trust to surrender the policy could trigger taxable gain to the extent that the policy cash value plus any outstanding loans exceed the Trust’s cost basis in the policy.

Loan interest to finance life insurance is not deductible. IRC §264.

Modified Endowment Contracts (MECs) Typically in a premium financing transaction, the policy is used as collateral to secure the loan. A policy that is a MEC should not be used as collateral. The moment the client pledges a MEC policy as collateral to secure the premium financing loan, any taxable gain built into the policy will be triggered. (IRC §72(e)(4)(A)(ii) indicates that if the client “assigns or pledges (or agrees to assign or pledge) any portion or value of such contract,” the assignment is treated as a distribution.)

If gain is triggered on a MEC policy and the policy owner has not attained age 59 ½, the distribution will be subject to the 10 percent penalty assessed on MEC policies if distributions occur. There are some exceptions to the penalty, for example, if the taxpayer becomes disabled, attains age 59 ½ or if the distribution is part of a series of substantially equal periodic payments made for the taxpayer’s life or life expectancy. If the Trust is a defective grantor trust, the age of the grantor (the owner of the policy for income tax purposes) controls. However, with a non-grantor trust, the trust is the taxpayer. Since the trust is a non-natural person the penalty will apply.

Other Considerations

Variable Life Products SEC Rule 11(d)(1) generally prohibits a broker-dealer from directly or indirectly arranging for financing for the purpose of purchasing securities.

Impact of final Split-dollar Regulations Premium financing, specifically third party arrangements, could fall under the broad definition of split-dollar arrangements. Under Treasury Reg. Sec 1.61-22(b), a split-dollar arrangement is defined as “an arrangement between an owner and non-owner of a life insurance contract …” where “either party to the arrangement pays, directly or indirectly, all or any portion of the premiums on the life insurance contract, including a payment by means of a loan to the other party that is secured by the life insurance contract … At least one of the parties to the arrangement paying premiums … is entitled to recover (either conditionally or unconditionally) all or any portion of those premiums and such recovery is to be made from, or is secured by, the proceeds of the life insurance contract.”

The regulations divide split-dollar arrangements into two categories: a loan regime and an economic benefit regime. Assuming that the split-dollar regulations apply, premium financing would fall under the loan regime. Adverse tax consequences would occur if the loan to pay premiums is considered to be a below-market loan. IRC §7872 would assess a tax on the difference between the below- market interest rate and the Applicable Federal Rate.

13HCB Premium Financing Technical Guide

However, regulations for IRC §7872 exempt loans that “are made available by the lender to the general public on the same terms and conditions which are consistent with the lender’s primary business practices” [Reg. 1.7872-5T(b)(1)]. So as long as the bank or other third party lender offers loans for premium financing transactions that they would offer to others and are consistent with their business practices, IRC §7872 should not apply.

All guarantees subject to the claims paying ability of the issuing insurance company.

The hypothetical case study results are for illustrative purposes only and should not be deemed a representation of past or future results. This example does not represent any specific product, nor does it reflect sales charges or other expenses that may be required for some investments. No representation is made as to the accurateness of the analysis.

Trusts should be drafted by an attorney familiar with such matters in order to take into account income and estate tax laws (including the generation-skipping tax). Failure to do so could result in adverse tax treatment of trust proceeds.

This material is for informational purposes only and is not meant as Tax or Legal advice. Please consult with your tax or legal advisor regarding your personal situation.

Revised 5/11/18 HCB00362