Embed Size (px)

Citation preview

1/24/18

1

Premium FinancingUnderstand the Risk & Rewards

Highland Capital Brokerage Platform

Presented by:

Robert W. Finnegan, J.D., CLU Mike Sapyta, CFP, CLU(518) 424-8928 610.945.1235 | Four Digit: [email protected] [email protected]

Today

I. The Rewards of Premium Financing

II. Understand Premium Financing

III. IUL & Understanding IUL Returns

IV. Aggressive Designs & Stress Test

V. The HCB Platform – Best Practices

1/24/18

2

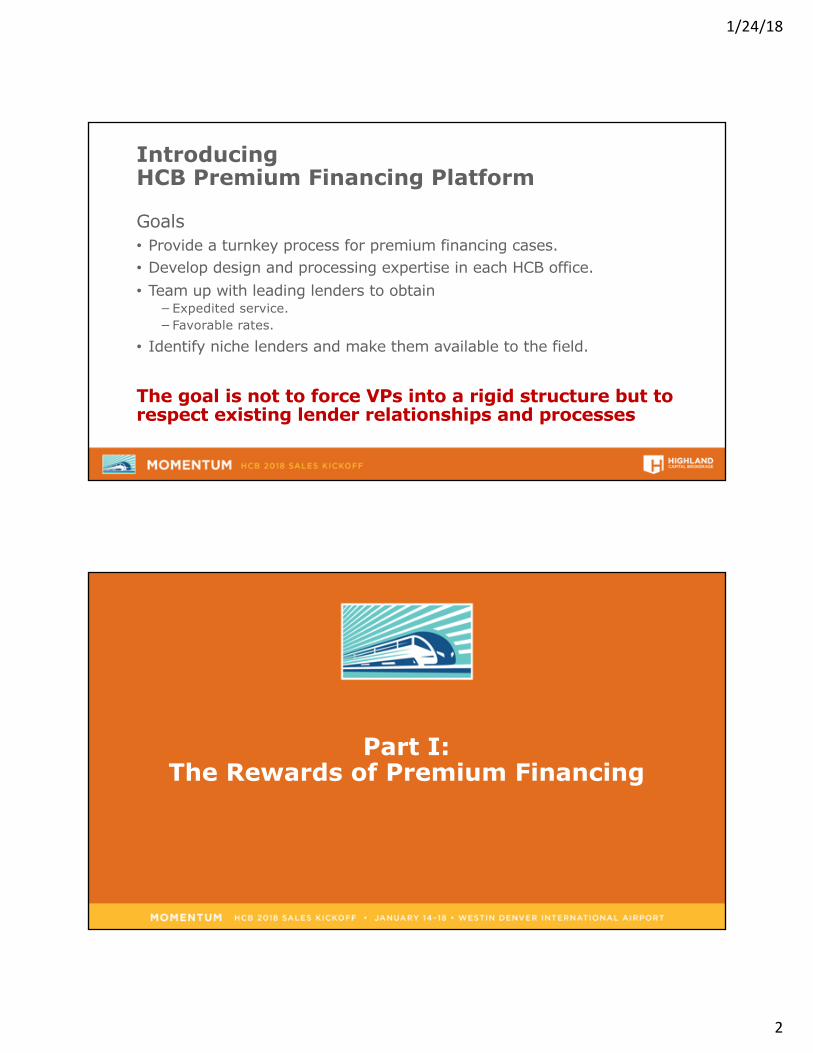

Introducing HCB Premium Financing Platform

Goals• Provide a turnkey process for premium financing cases. • Develop design and processing expertise in each HCB office.• Team up with leading lenders to obtain −Expedited service.−Favorable rates.

• Identify niche lenders and make them available to the field.

The goal is not to force VPs into a rigid structure but to respect existing lender relationships and processes

Part I: The Rewards of Premium Financing

1/24/18

3

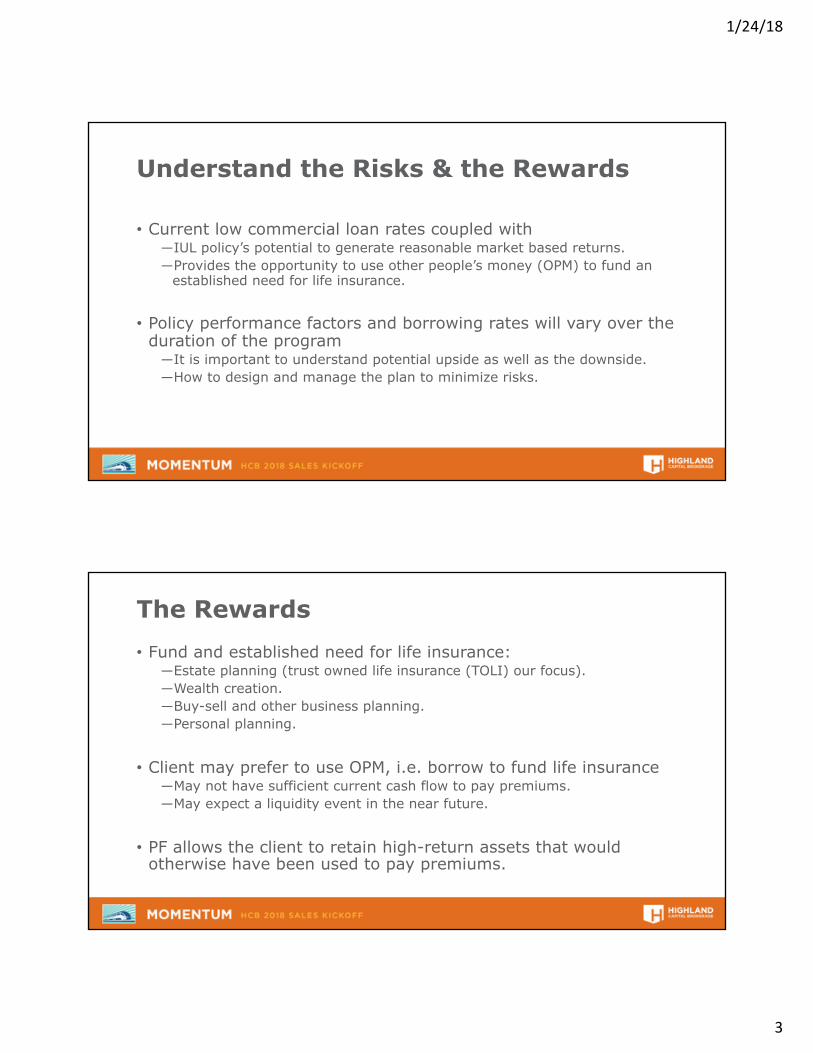

Understand the Risks & the Rewards

• Current low commercial loan rates coupled with ―IUL policy’s potential to generate reasonable market based returns. ―Provides the opportunity to use other people’s money (OPM) to fund an

established need for life insurance.

• Policy performance factors and borrowing rates will vary over the duration of the program―It is important to understand potential upside as well as the downside.―How to design and manage the plan to minimize risks.

The Rewards• Fund and established need for life insurance: ―Estate planning (trust owned life insurance (TOLI) our focus). ―Wealth creation.―Buy-sell and other business planning. ―Personal planning.

• Client may prefer to use OPM, i.e. borrow to fund life insurance―May not have sufficient current cash flow to pay premiums.―May expect a liquidity event in the near future.

• PF allows the client to retain high-return assets that would otherwise have been used to pay premiums.

1/24/18

4

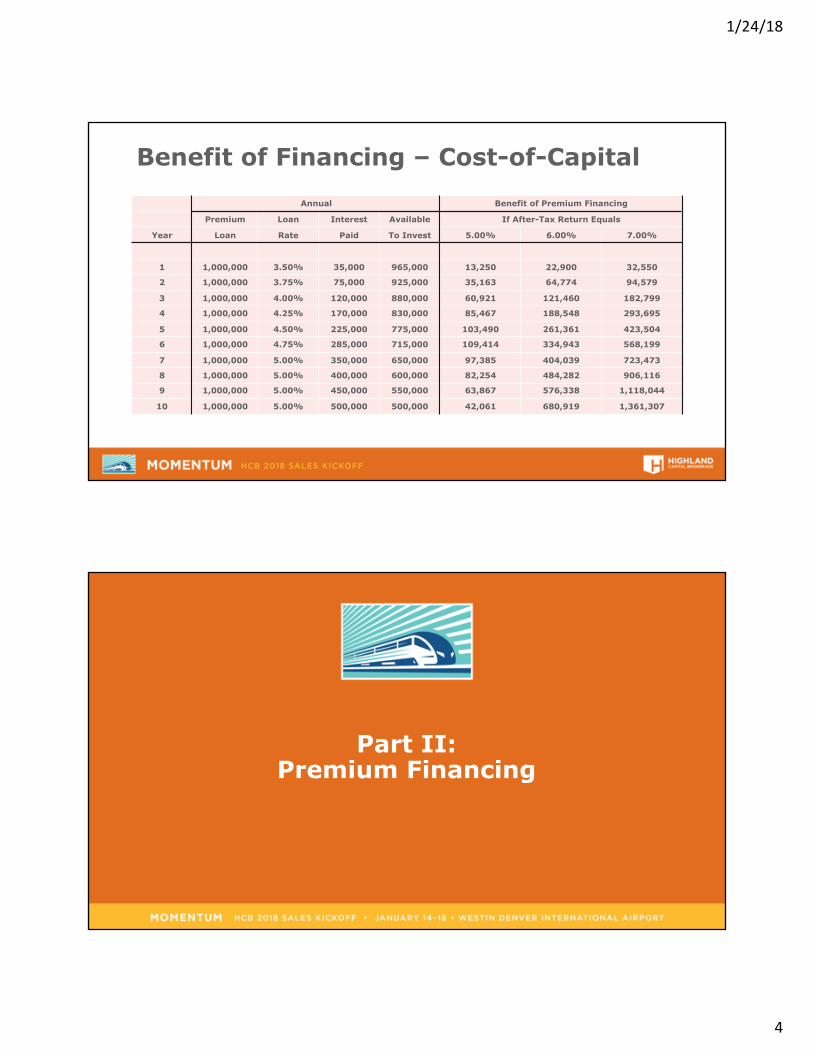

Benefit of Financing – Cost-of-CapitalAnnual Benefit of Premium Financing

Premium Loan Interest Available If After-Tax Return Equals

Year Loan Rate Paid To Invest 5.00% 6.00% 7.00%

1 1,000,000 3.50% 35,000 965,000 13,250 22,900 32,550

2 1,000,000 3.75% 75,000 925,000 35,163 64,774 94,579

3 1,000,000 4.00% 120,000 880,000 60,921 121,460 182,799

4 1,000,000 4.25% 170,000 830,000 85,467 188,548 293,695

5 1,000,000 4.50% 225,000 775,000 103,490 261,361 423,504

6 1,000,000 4.75% 285,000 715,000 109,414 334,943 568,199

7 1,000,000 5.00% 350,000 650,000 97,385 404,039 723,473

8 1,000,000 5.00% 400,000 600,000 82,254 484,282 906,116

9 1,000,000 5.00% 450,000 550,000 63,867 576,338 1,118,044

10 1,000,000 5.00% 500,000 500,000 42,061 680,919 1,361,307

Part II: Premium Financing

1/24/18

5

Typical Premium Financing Plan

• Policy approved based on full underwriting.

• Trust applies for & borrows premiums from a commercial lender.

• Loan interest is paid in cash with gifts from the client/insured.

• Sufficient collateral acceptable to the lender is posted so that the lender is fully secured at all times.

Typical Premium Financing PlanLender agrees to total loan for term of years (for ex. 5-years)

• Pays the 1st premium.

• On each anniversary provides an invoice for interest due, trues up collateral and offers the borrower the option to finance all or a portion of the next premium.

At the end of the loan term (5-years):

• The borrower may repay the loan or re-apply.

• If re-apply, the loan is re-underwritten (at current terms).

• If not renewed the loan is due and payable in full

1/24/18

6

Loan Interest• Typically based on the 12-month LIBOR plus a spread ranging

from approximately 100 to 350 basis points.

• The spread will depend upon the ―Lender.―Size of the loan.―Creditworthiness of the borrower. ―The spread is not guaranteed over the term of the loan.

• Loan rate adjusted annually based on current 12-month LIBOR plus the spread.

Note: Most lenders will offer a level multi-year loan rate at inception with an “interest rate swap” (+100 - 125 bps).

Collateral• The trust posts the policy cash surrender value as collateral. ―Typically, lenders will credit 90% - 100% of the policy CSV.―Insurance carrier must meet financial strength guidelines.

• Shortfall (Loan – CSV) secured by assets acceptable to the lender.

• Typically the grantor/insured pledges assets. ―Although there is no authority on point, most advisors feel that

posting of collateral is not considered a gift to the trust. ―Best practice is for the guarantor to charge a fee to the trust in

exchange for the guarantee.

1/24/18

7

Collateral• Most lenders will accept ―Cash.―Certificates of deposit from a highly rated bank.―Money market funds.―A letter of credit from a highly-rated bank. ―A portfolio of quality marketable securities.―Life insurance cash values and some annuities .

• For collateral other than cash and letters-of-credit―Lender will require a greater amount than the outstanding loan balance. ―The riskier or less liquid the collateral, the greater the margin.

• Lenders monitor collateral closely to ensure that the loan is not in default.

Gifts to Trust• Gifts to the trust to −Pay interest. −Repay the loan.−Collateral call.

• If it is a dynasty trust there will be GST implications.

• With all premium financing plans, it is important to carefully consider how −Loan interest will be paid −The loan will be repaid.

1/24/18

8

Exit Strategies• Death benefit

• Policy cash values ―This may however place too much strain on the policy.―Risk reduced death benefit or a policy lapse and phantom income.

• Implement PF plan in a funded trust with sufficient assets.

• Other assets may be transferred to the trust utilizing ―Gifts/sales to a defective grantor trust.―GRATs―Intra-family loans

Note: Transfers may not only backstop the loan, they may also generate cash flow to pay loan interest and simply constitute sound estate planning.

Premium Financing With Dynasty TrustClient (Grantor) Dynasty Trust (fbo Children, GC, GGC+)

1

1. Client Creates Irrevocable Trust.

4b. Client pledges collateral to cover shortfall.

5. Gifts to Trust to Pay Loan Interest.[Optional] Client Transfers Funds to

Trust.

- Cash Flow Pays Interest.- Assets Available to Repay Loan.

4a, 5, 6 2

Commercial Bank3

4b

55. Pays Loan Interest to Bank.6. Funds Available to Repay Loan.

a. Death Benefit

b. Cash Valuesc. Other Trust Assets

1. Trust fbo of Children, GC, GGC.

2. Trust policy approved (underwriting).

3. Trust Applies for Loan from Bank.

Bank Pays Premium to Carrier.4a. Trust pledges policy CV & DB as

collateral.

Life Insurance Income, Gift, Estate & GST tax free.

Assets in Multi-Generation Trust Avoid Repeat Estate Taxation.

Life Insurance & Other Assets in Dynasty Trust

Insurance Carrier

1/24/18

9

Indexed UL• A cash value general account product that is based on

• General account returns.• The returns of an Index Fund, typically the S&P 500 Index.

• The actual IUL return can vary substantially from the Index Fund’s return because the IUL return ―Excludes dividends on the stocks comprising the Index Fund. ―Subject to Participation rate, floor and cap.

• Premiums net of expenses and charges and Cash Value • Are not invested directly in the underlying Index Fund. • Are invested in the carrier’s general account• General account earnings create the options budget.

• The carrier employs hedging (option) strategies to achieve the IUL policy’s investment returns.

Part III: Indexed UL

Understanding IUL Returns

1/24/18

10

Indexed UL

Upon receipt of a premium, the carrier

• Deducts policy expenses, charges (including COIs) and loads.

• Invests excess premiums along with the policy’s cash values as part of its general account portfolio, −High grade bonds and mortgages. −The bonds and mortgages provide principal protection.−The portfolio income creates the “options budget” to purchase options to

meet the specific product’s cap, floor & participation rate.

IUL – Factors Affecting Performance• As with any current assumption UL product, the carrier could increase

or decrease the product’s costs and charges, including the COIs. • The options budget which is a function of a carrier’s general account

investment performance could increase or decrease. For example, − If interest rates rise, a carrier’s new investment in higher rate mortgages may

generate a larger options budget. −Conversely, continued downward pressure on carrier investment returns could

shrink the options budget.

• The cost of options hedging the cap and floor could increase or decrease.

• The carrier may increase or decrease −The non-guaranteed cap rate and/or participation rate.−Persistency bonuses (whether are guaranteed or not, carriers retain enough

control to manage risk).

1/24/18

11

Understanding IUL Returns

• How do IUL returns relate to the returns of the Index Fund.

• For a specific annual Index return, it is a simple matter to • Exclude dividends• Apply the cap, floor and participation rates.

• However, how do you put illustrated IUL returns in perspective taking into account the long-term performance of the Index Fund’s underlying stocks with their many and substantial ups and downs?

Understanding IUL Returns• Most carrier illustrations show how their parameters would affect

the historical Index Fund returns over the past 20-years. • A few carriers offer tools evaluating IUL RORs based on historical

equity returns. −VOYA offers a percentile model that calculates the probability of realizing

a specific IUL return based on historical S&P 500 returns. − annexus® offers the BGA IUL Crediting Strategy Comparison Tool

• Historical returns are of limited use however since −No IUL product has been inforce over the historical time frame.−The non-guaranteed cap, floor and participation rates might have varied

from those in the current product.−Investment managers not confident future returns will be as strong.−Historical rates cannot be used to predict future performance.

1/24/18

12

Understanding IUL Returns• John Hancock “Rate Translator Model” that is

• Based on the Capital Asset Pricing Model rather than on historical returns. • It “translates” a given or assumed equity Index Fund return into an

assumed IUL return. • It takes into account the long-term performance of the equities market

with its expected ups and downs (excluding dividends on the underlying stocks)

• Subjects those returns to the participation, cap and floor rates of the IUL product.

• A useful tool for −Understanding IUL returns in relation to Index Fund returns. −Comparing IUL returns among various products with different cap, floor

and participation rates.

• Verified the results of the translator model with a separate stochastic model that is based on the historical S&P 500 returns.

Index Fund Return vs. IUL Return0% Floor, 10.5% Cap, 100% Participation

(Excludes Persistency Bonuses)

Data

Point

If the Assumed

“Index Fund Return” is

Then the Assumed

“IUL Return” is

1 0.00% 4.01%

2 4.00% 4.90%

3 5.15% 5.15%

4 6.75% 5.50%

5 10.25% 6.30%

6 12.00% 6.70%

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

1 2 3 4 5 6

Chart I: Index Fund Return vs. IUL Return

S&P 500 Index Return IUL Return

S&P 500 Returns IUL Returns

Low High Spread Low High Spread

0.00% 12.00% 12.00% 4.01% 6.70% 2.69%

5.15% 12.00% 6.85% 5.15% 6.70% 1.55%

Cross

Over

1/24/18

13

Understanding IUL Returns

5.79%

6.03%

6.25%

6.46%

6.66%6.86%

7.05%

5.39%

5.60%

5.80%5.99%

6.17%6.35%

6.52%

4.98%5.17%

5.35%5.52%

5.69%5.85%

6.00%

4.50%

5.00%

5.50%

6.00%

6.50%

7.00%

7.50%

9.50% 10.00% 10.50% 11.00% 11.50% 12.00% 12.50%

IUL R

etur

n

IUL Cap Rate

Chart II. IUL Return Given 6, 8 or 10% Index Fund Return & IUL Cap

10% Index Fund Return 8% Index Fund Return 6% Index Fund Return

Part IV: Aggressive Designs

Stress TestWhat Could Go Worng?

1/24/18

14

Aggressive Premium Financing Plans

• The policy illustration is based on the highest illustrative rate allowed by the carrier (6.30% in our example below). • The loan remains in effect for the insured’s lifetime. • Loan interest is accrued and remains levels for all years. • With respect to the aggressive design:―It may look good and might live up to its promise―Substantial chance that it will not and that it could fail spectacularly. ―With some plans, the loan is repaid with a policy loan for example in the

15th year based on aggressive policy loan parameters.―Accrued loan interest is a substantial benefit.

Stress Testing and Aggressive Plan• M50 preferred with need for $10M of LI. • The agent proposes −IUL policy with an increasing death benefit. −Borrow 7 premiums of $562,270 from bank ($3,935,890 total). −Accrue loan interest. −Repay loan at death.

• Two Scenarios −Scenario I - No cost design, i.e. no out-of-pocket costs. −Scenario II stress tests the no-cost design

§ Reduce the IUL illustrative rate.§ Increase the assumed commercial loan rate.

1/24/18

15

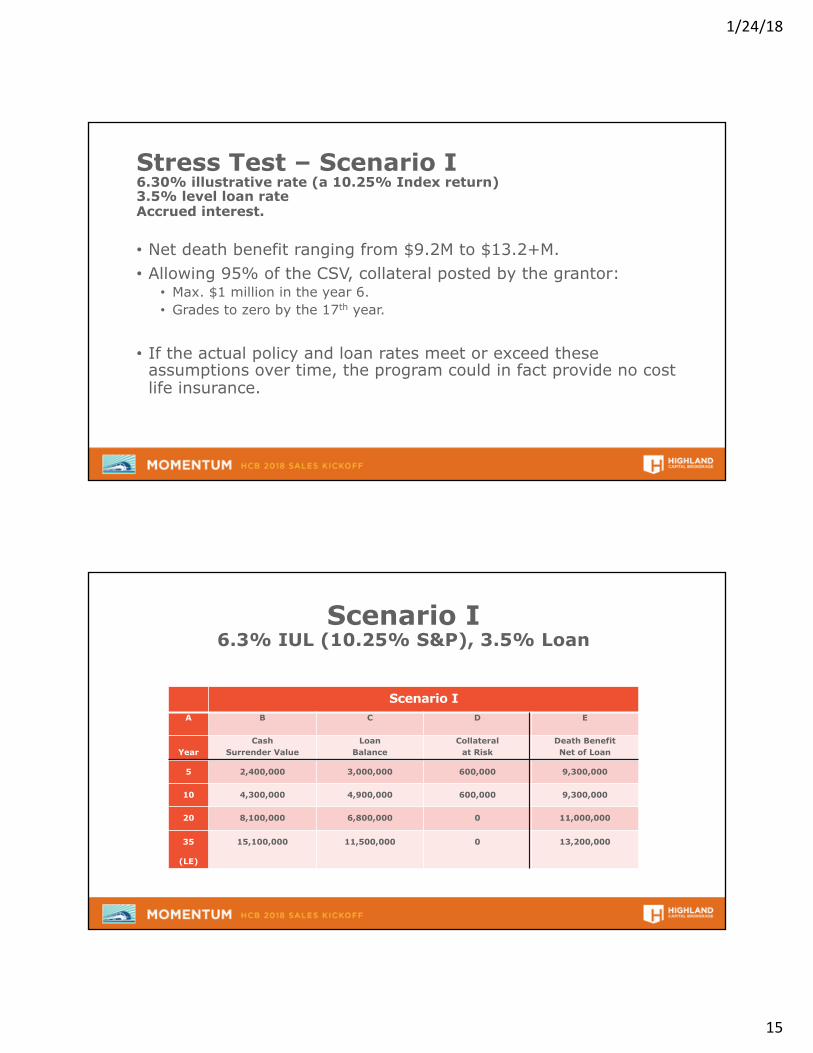

Stress Test – Scenario I6.30% illustrative rate (a 10.25% Index return)3.5% level loan rateAccrued interest.

• Net death benefit ranging from $9.2M to $13.2+M. • Allowing 95% of the CSV, collateral posted by the grantor:

• Max. $1 million in the year 6.• Grades to zero by the 17th year.

• If the actual policy and loan rates meet or exceed these assumptions over time, the program could in fact provide no cost life insurance.

Scenario I6.3% IUL (10.25% S&P), 3.5% Loan

Scenario IA B C D E

YearCash

Surrender Value Loan

BalanceCollateral

at RiskDeath BenefitNet of Loan

5 2,400,000 3,000,000 600,000 9,300,000

10 4,300,000 4,900,000 600,000 9,300,000

20 8,100,000 6,800,000 0 11,000,000

35

(LE)

15,100,000 11,500,000 0 13,200,000

1/24/18

16

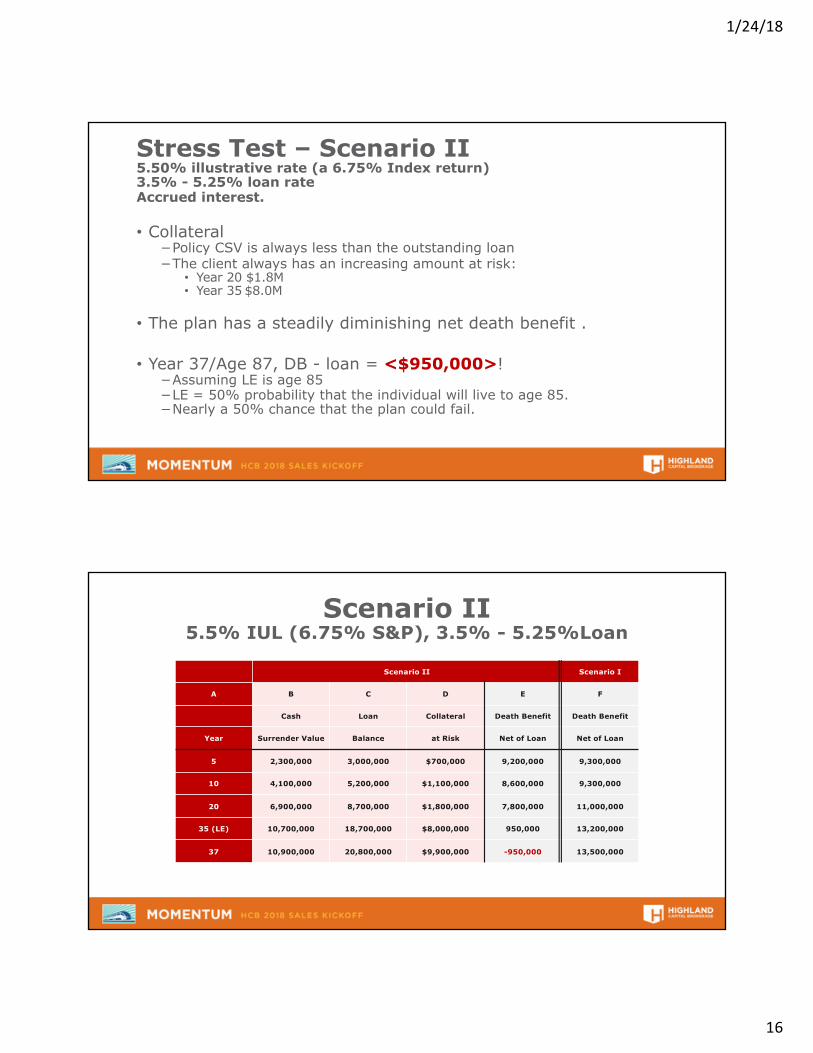

Stress Test – Scenario II5.50% illustrative rate (a 6.75% Index return)3.5% - 5.25% loan rateAccrued interest.

• Collateral−Policy CSV is always less than the outstanding loan −The client always has an increasing amount at risk:

• Year 20 $1.8M• Year 35 $8.0M

• The plan has a steadily diminishing net death benefit .

• Year 37/Age 87, DB - loan = <$950,000>! −Assuming LE is age 85 −LE = 50% probability that the individual will live to age 85.−Nearly a 50% chance that the plan could fail.

Scenario II5.5% IUL (6.75% S&P), 3.5% - 5.25%Loan

Scenario II Scenario I

A B C D E F

Cash Loan Collateral Death Benefit Death Benefit

Year Surrender Value Balance at Risk Net of Loan Net of Loan

5 2,300,000 3,000,000 $700,000 9,200,000 9,300,000

10 4,100,000 5,200,000 $1,100,000 8,600,000 9,300,000

20 6,900,000 8,700,000 $1,800,000 7,800,000 11,000,000

35 (LE) 10,700,000 18,700,000 $8,000,000 950,000 13,200,000

37 10,900,000 20,800,000 $9,900,000 -950,000 13,500,000

1/24/18

17

Stress Test Aggressive Plan Design

-2,000,000

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

16,000,000

5 10 20 35 37

Stress Test - Death Benefit Net of Loan

Scenario I

Scenario II

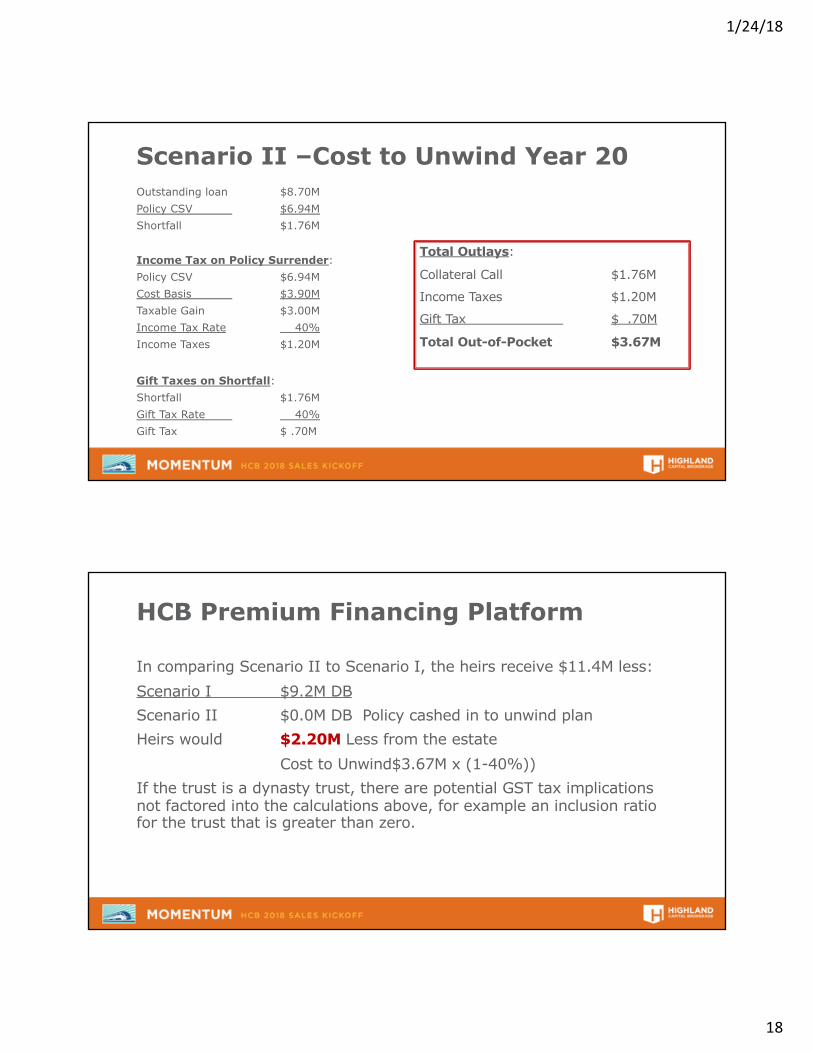

Scenario II –Cost to Unwind Year 20

Unwinding the loan in the 20th year • Based on Scenario II loan and policy assumptions.

• Trust is a defective grantor trust.

• Client does not have lifetime gift or GST exemption available.

• Income, gift and estate tax rates each equals 40%.

1/24/18

18

Scenario II –Cost to Unwind Year 20Outstanding loan $8.70M Policy CSV $6.94MShortfall $1.76M

Income Tax on Policy Surrender:Policy CSV $6.94MCost Basis $3.90M Taxable Gain $3.00MIncome Tax Rate 40%Income Taxes $1.20M

Gift Taxes on Shortfall:Shortfall $1.76MGift Tax Rate 40%Gift Tax $ .70M

Total Outlays:

Collateral Call $1.76M

Income Taxes $1.20M

Gift Tax $ .70M

Total Out-of-Pocket $3.67M

HCB Premium Financing Platform

In comparing Scenario II to Scenario I, the heirs receive $11.4M less: Scenario I $9.2M DBScenario II $0.0M DB Policy cashed in to unwind planHeirs would $2.20M Less from the estate

Cost to Unwind$3.67M x (1-40%)) If the trust is a dynasty trust, there are potential GST tax implications not factored into the calculations above, for example an inclusion ratio for the trust that is greater than zero.

1/24/18

19

Monitoring the Loan

• Prudent design• It is essential. • Avoids issues.

• Annual monitoring of plan performance • It is essential. • Uncover issues in the early stages when easier to address.

Part V: The HCB Platform

Best Practices

1/24/18

20

HCB Premium Financing Platform

Highland Advanced Planning is pleased to announce • Development of a robust premium financing platform.• Best practices −Design standards.−New business processing. −Monitoring existing cases.

• Team up with Lender(s)−Leader in the traditional premium financing.−Primary Lender (others still available).−Not exclusive – can use other lenders.

HCB Premium Financing Platform

Objectives• Clients and advisors understand risks & rewards.• Simplify – turnkey.• Compliant business.• Favorable rates.• Track results.

1/24/18

21

Choosing a Lender

It is important to carefully assess and compare each lender’s • Experience in the market.• Long-term commitment to the market.• The number and amount of premium financing loans in place.• Whether the loan has pre-payment penalties (the better

programs do not).• To carefully review the conditions under which the loan may be

called. ―The better lenders will only call the loan if it is in default.―Default - the loan balance exceeds combined collateral.―That shortfall has not been remedied following notification.

Select Carriers

• AXA• John Hancock• Lincoln• Minnesota Life• Pacific Life• Symetra

1/24/18

22

Client Requirements

Client must have

• An established life insurance need.

• Minimum net worth as defined by lender and HCB.

• Cash flow to pay all or portion of interest.

• Collateral acceptable to lender.

Best Practice - Design

Baseline Sales Illustration (reasonable illustrative and loan rates).• IUL illustrative rates −AG49 rate and −An alternate reasonable assumed IUL rates of return

• Loan interest.−Client proposal will be based on reasonable assumed loan rates. −For example, current loan rate (3.5%) increasing by 25-35 bps/year to

and leveling out at 4.5% or 5%. −Trust pays part or all of the loan interest. Establish source

§ Gifts of cash.§ Cash flow of assets transferred to trust (Gifts/sale, GRATs, etc.). § Existing funded trust.

Note: Accrued interest will be considered on an exception basis.

1/24/18

23

Best Practice - Design

Disclosure form to client and advisors including • Baseline Premium Financing Illustration.

• Outline the non-guaranteed nature of the program−Policy performance.−Loan elements of the program.−Carrier maintain minimum rating.

Best Practice – Processing the Loan

• Life underwriting must be complete before submitting loan application.Note: Informal underwriting may be acceptable on a case-by-case basis

• Submit all required information for loan underwriting (not piecemeal).

1/24/18

24

Best Practice – Processing the Loan• Credit Application - Individual Borrower−Cover letter−Signed credit application (Policy owner, Borrower, Guarantor, Insured)−Signed and dated personal financial statement (PFS)−Bank and brokerage statements to support liquid assets on PFS−Signed and dated 2-years of tax returns−Signed and dated premium finance illustration (don’t change once

application in process)−Signed and dated policy illustration (don’t change once application in

process)−Copy of driver’s license

• Illustration run at the guaranteed rate with current charges.• A copy of the trust, LLC, partnership or articles of incorporation

must be provided prior to closing.

Best Practice – Processing the Loan

• Credit Application - Business Borrower

• All of the above and −2-years consolidated business financial statements (balance sheet, cash

flow & income statement)−2-Years complete corporate tax returns

Note: A copy of the formation documents must be provided prior to closing.

1/24/18

25

Best Practice – Processing the Loan

Collateral• Discuss and identify amount required and source early on.• Must be approved by WinTrust−Brokerage house must approve and sign control agreement.

Note: WinTrust has agreements with 30 brokerage houses.−CD from an FDIC approved bank.−Letter of credit from a bank approved by WinTrust.

• Once loan is submitted, don’t change−Policy illustration.−Collateral.

Best Practice – Processing the Loan

WTLF Collateral Illustration• WTLF will require that the IUL illustration be run at the

guaranteed rate and current charges. • Initial collateral is determined by this illustration. • If the client is using a high early CSV rider, then collateral will be

based on the value this ride provides. (Rider must be approved in advance by WTLF.)• Client must sign this illustration.

1/24/18

26

Best Practice – Monitoring the Loan

• Annual monitoring of plan performance is essential.

• Uncover issues in the early stages when easier to address.

• Annual monitoring −Evaluates performance to date −Re-stress testing the plan parameters, projecting

§ Future policy performance with inforce ledgers § Current loan balance plus expected additional premium loans based upon

reasonable assumptions as to forward borrowing rates. −If the policy performance and/or loan rates are better than expected, then

it may be possible to skip premiums or utilize cash values to repay the loan without jeopardizing the policy.

Premium FinancingUnderstand the Risk & Rewards

Highland Capital Brokerage Platform

Presented by:

Robert W. Finnegan, J.D., CLU Mike Sapyta, CFP, CLU(518) 424-8928 610.945.1235 | Four Digit: [email protected] [email protected]