Embed Size (px)

Citation preview

1

POWER SECTOR DEVELOPMENTSIN BRAZIL

Mario Pereira

Workshop on Power Market Reformsand Global Climate Change

Stanford, January 27-28, 2005

2

Outline

• Brazilian system overview• Investment needs• Investment options• Market rules for new investments• The Bioelectricity initiative• Conclusions

3

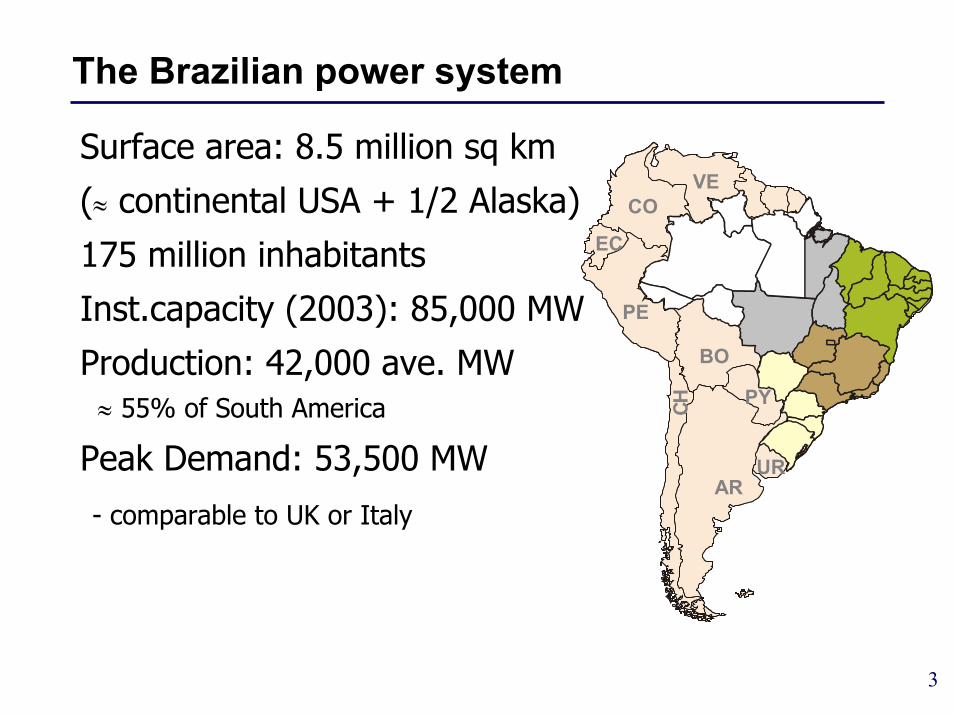

The Brazilian power system

Surface area: 8.5 million sq km

(≈ continental USA + 1/2 Alaska)

175 million inhabitants

Inst.capacity (2003): 85,000 MW

Production: 42,000 ave. MW≈ 55% of South America

Peak Demand: 53,500 MW

- comparable to UK or Italy

PEBR

URAR

PY

BO

EC

VECO

CH

PEBR

URAR

PY

BO

EC

VECO

CH

4

Current energy mix

• Thermal + interconnections (15%): combined- and open-cycle natural gas, coal, oil and nuclear

• Hydro (85%): large plants in cascade, in several basins

Maribondo1240

P.Colombia1227Ibitinga

909

N.Avanhandava911

C.I.Solteira914

PortoPrimavera

926

S.Dias Jupia919

A.SouzaLima908

Prom.910

BarraBonita907

CachoeiraDourada1514

Itumbiara1513

1515

CapimBranco1510

Miranda1509

1512

Camargos1207

EstreitoGrande1223

Masc.Moraes1222

Furnas1221

FunilGrande1212

Itutinga1208

V.GrandeGde. 1226

A.Vermelha1241

Jaborandi1243

A.E.Oliveira1237

Barretos1242

Caconde1233

Euclides daCunha1236

Viradouro1244

Serra

1493

1505

Bocaina1501

A. A. Layner602

Xavantes604

Capivara616

Rosana618

617

L.N.Garoez605

Canoas I606

Canoas II607

ItaipuBinac.620

NovaPonte1508

Igarapava1225

Jaguara1224

• all hydro plants are dispatched as a "portfolio", with"wetter" basins exporting energy to "drier" ones

Itaipu: 14,000 MWItaipu: 14,000 MW

5

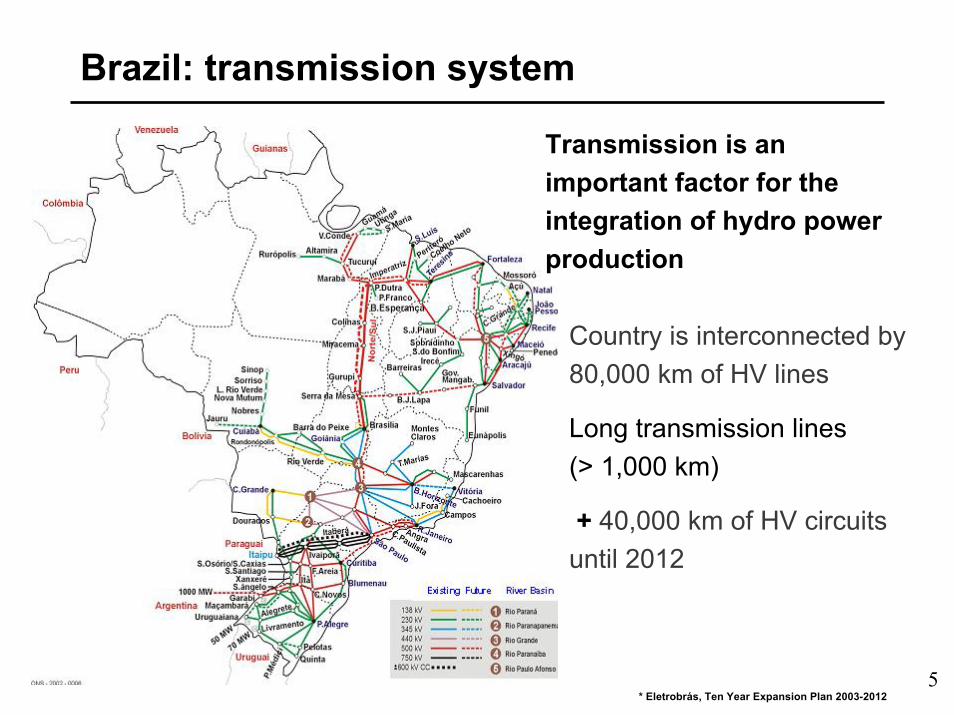

Brazil: transmission system

Country is interconnected by 80,000 km of HV lines

Long transmission lines(> 1,000 km)

+ 40,000 km of HV circuits until 2012

Transmission is an important factor for the integration of hydro power production

* Eletrobrás, Ten Year Expansion Plan 2003-2012

6

Power sector organization

• Regulatory agency (ANEEL)

• Nationwide ISO (ONS) and Wholesale Energy Market(CCEE), both private, under ANEEL supervision

• Generation– 11 gencos, 15% private (by energy produced) – total revenues (2003) : US$ 9 billion

• Transmission

– 26 transcos, 17 private

– total revenues (2003) : US$ 1.6 billion

• Distribution– 64 major discos, 80% private (by energy consumed)

– total revenues (2003): US$ 16 billion

7

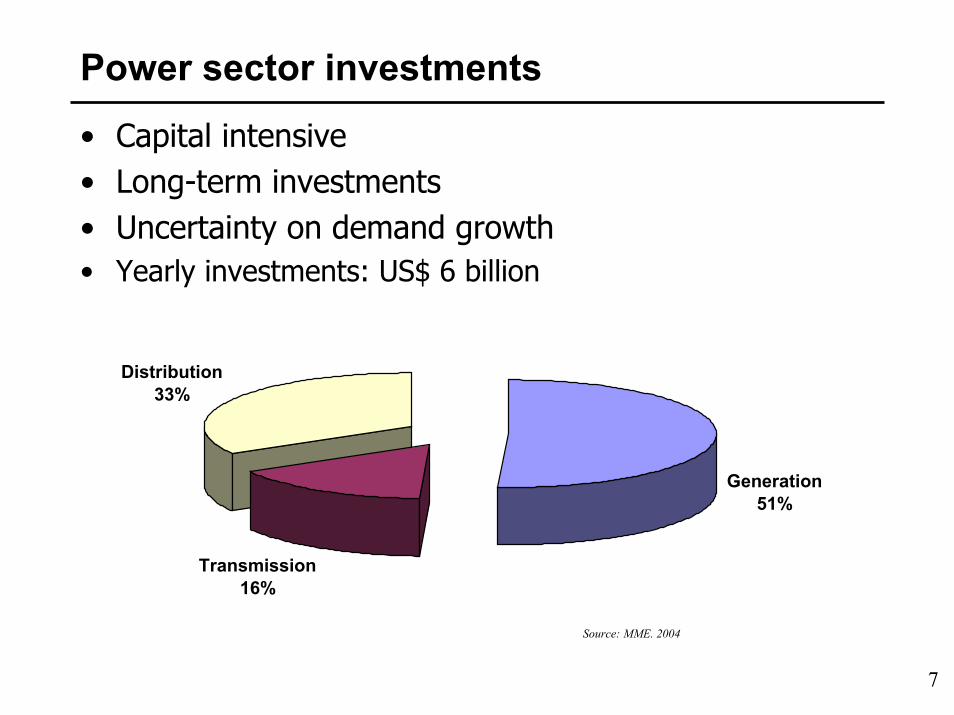

Power sector investments

• Capital intensive• Long-term investments• Uncertainty on demand growth• Yearly investments: US$ 6 billion

Generation51%

Transmission16%

Distribution33%

Source: MME. 2004

8

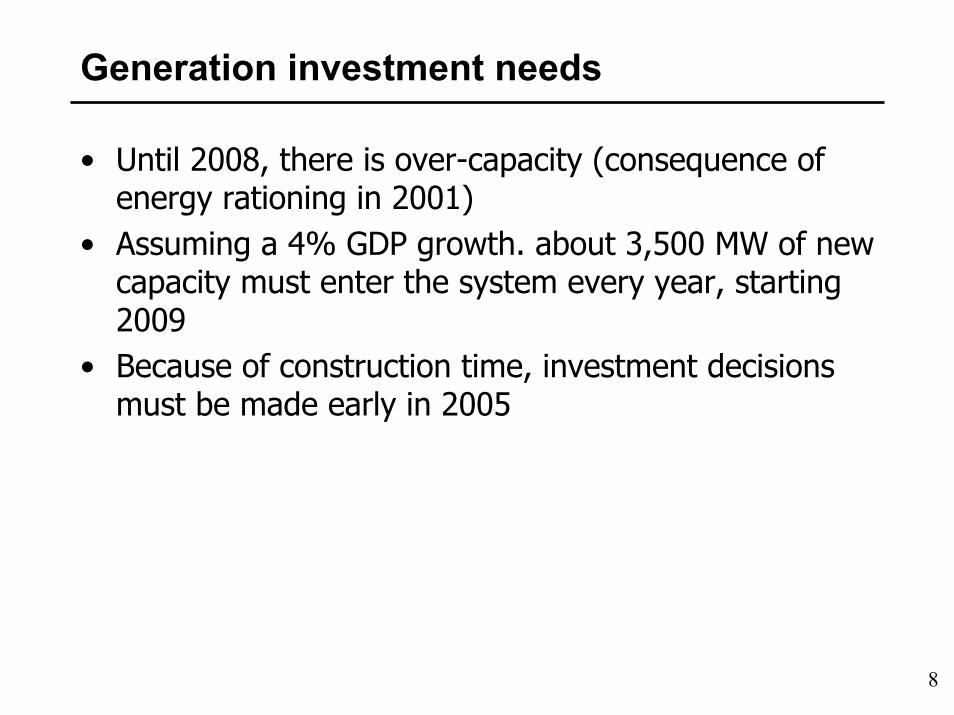

Generation investment needs

• Until 2008, there is over-capacity (consequence of energy rationing in 2001)

• Assuming a 4% GDP growth. about 3,500 MW of new capacity must enter the system every year, starting 2009

• Because of construction time, investment decisions must be made early in 2005

9

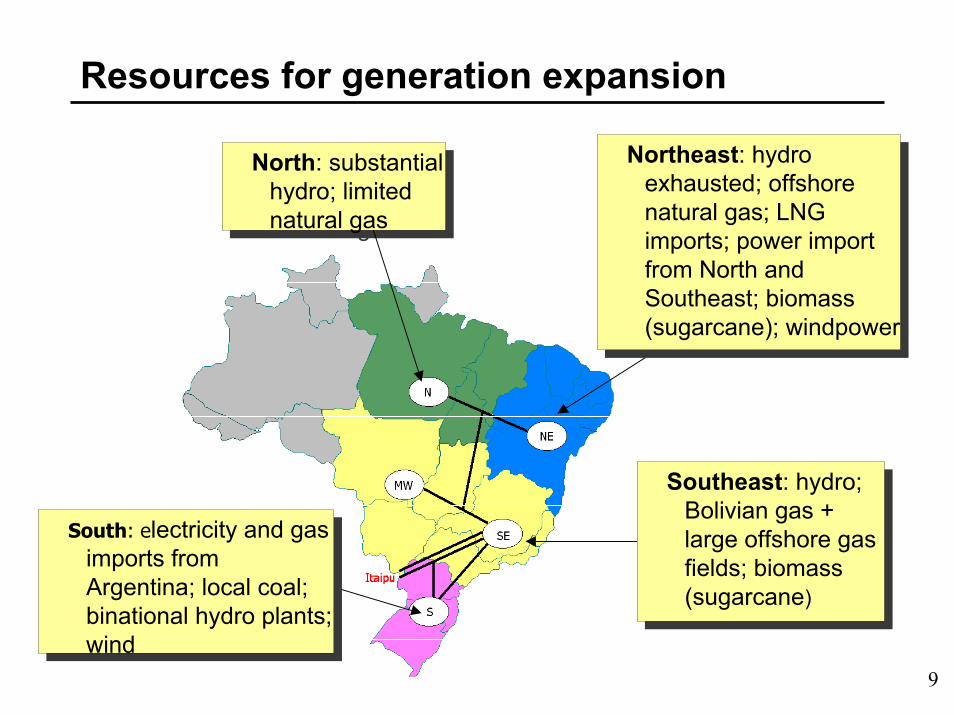

Resources for generation expansion

South: electricity and gas imports from Argentina; local coal; binational hydro plants; wind

South: electricity and gas imports from Argentina; local coal; binational hydro plants; wind

North: substantial hydro; limited natural gas

North: substantial hydro; limited natural gas

Northeast: hydro exhausted; offshore natural gas; LNG imports; power import from North and Southeast; biomass (sugarcane); windpower

Northeast: hydro exhausted; offshore natural gas; LNG imports; power import from North and Southeast; biomass (sugarcane); windpower

Southeast: hydro; Bolivian gas + large offshore gas fields; biomass (sugarcane)

Southeast: hydro; Bolivian gas + large offshore gas fields; biomass (sugarcane)

10

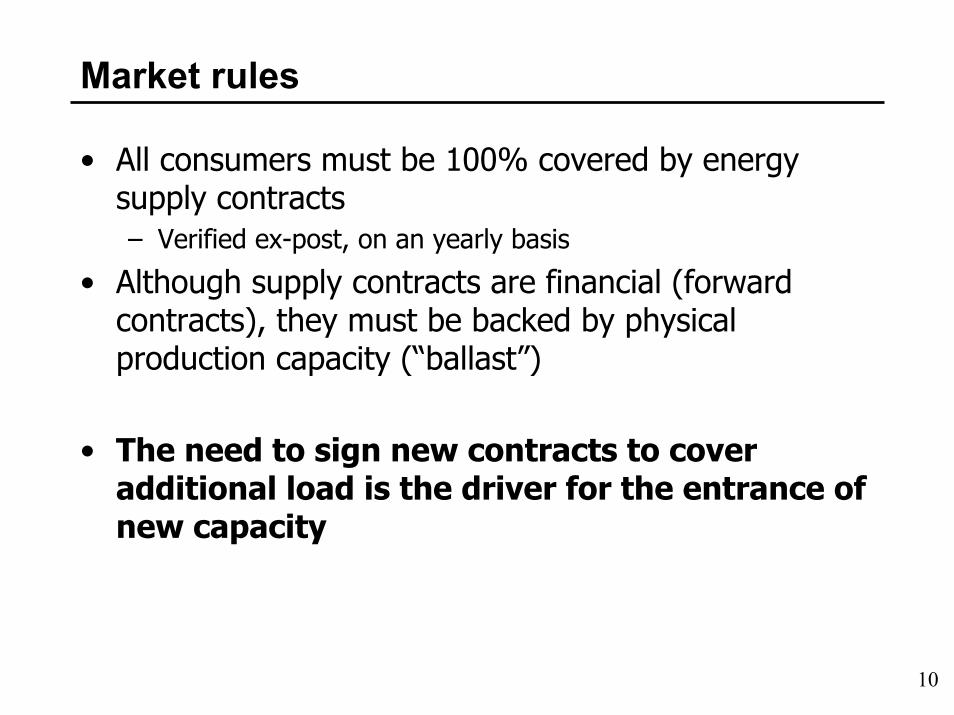

Market rules

• All consumers must be 100% covered by energy supply contracts– Verified ex-post, on an yearly basis

• Although supply contracts are financial (forward contracts), they must be backed by physical production capacity (“ballast”)

• The need to sign new contracts to cover additional load is the driver for the entrance of new capacity

11

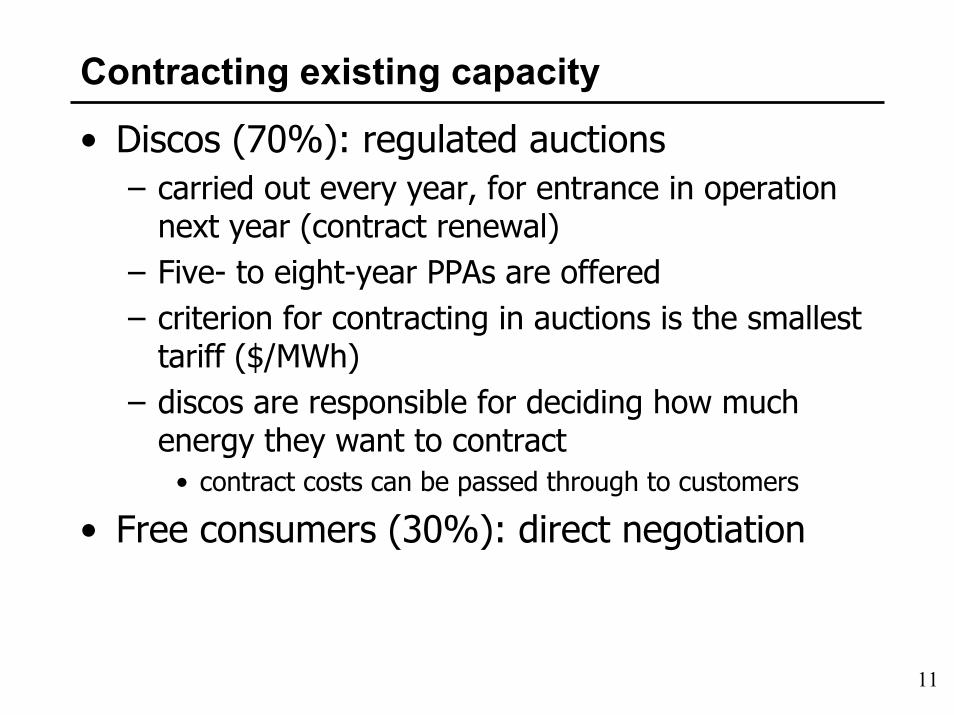

Contracting existing capacity

• Discos (70%): regulated auctions– carried out every year, for entrance in operation

next year (contract renewal)– Five- to eight-year PPAs are offered– criterion for contracting in auctions is the smallest

tariff ($/MWh)– discos are responsible for deciding how much

energy they want to contract• contract costs can be passed through to customers

• Free consumers (30%): direct negotiation

12

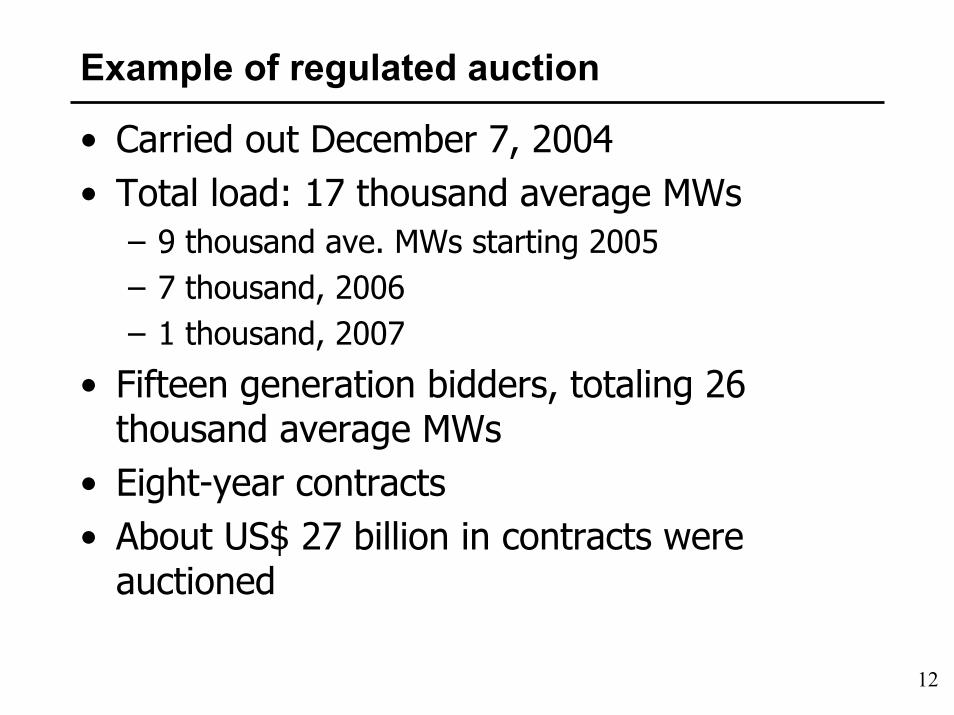

Example of regulated auction

• Carried out December 7, 2004• Total load: 17 thousand average MWs

– 9 thousand ave. MWs starting 2005– 7 thousand, 2006– 1 thousand, 2007

• Fifteen generation bidders, totaling 26 thousand average MWs

• Eight-year contracts• About US$ 27 billion in contracts were

auctioned

13

Contracting new capacity

• Discos: regulated auctions– carried out every year, for entrance in operation

five years later– 20-year PPAs are offered

• this allows auction winners enough time to build plants and to have project finance

– criterion for contracting in auctions is the smallest tariff ($/MWh)

– discos are responsible for deciding how much energy they want to contract

• contract costs can be passed through to customers

• Free consumers: direct negotiation

14

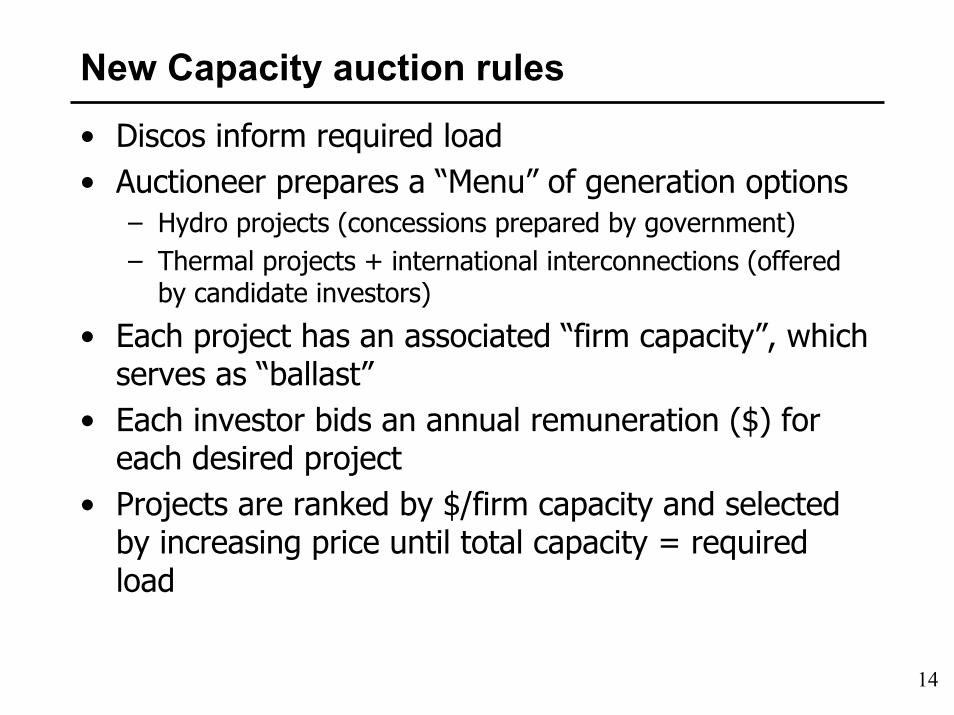

New Capacity auction rules

• Discos inform required load• Auctioneer prepares a “Menu” of generation options

– Hydro projects (concessions prepared by government)– Thermal projects + international interconnections (offered

by candidate investors)

• Each project has an associated “firm capacity”, which serves as “ballast”

• Each investor bids an annual remuneration ($) for each desired project

• Projects are ranked by $/firm capacity and selected by increasing price until total capacity = required load

15

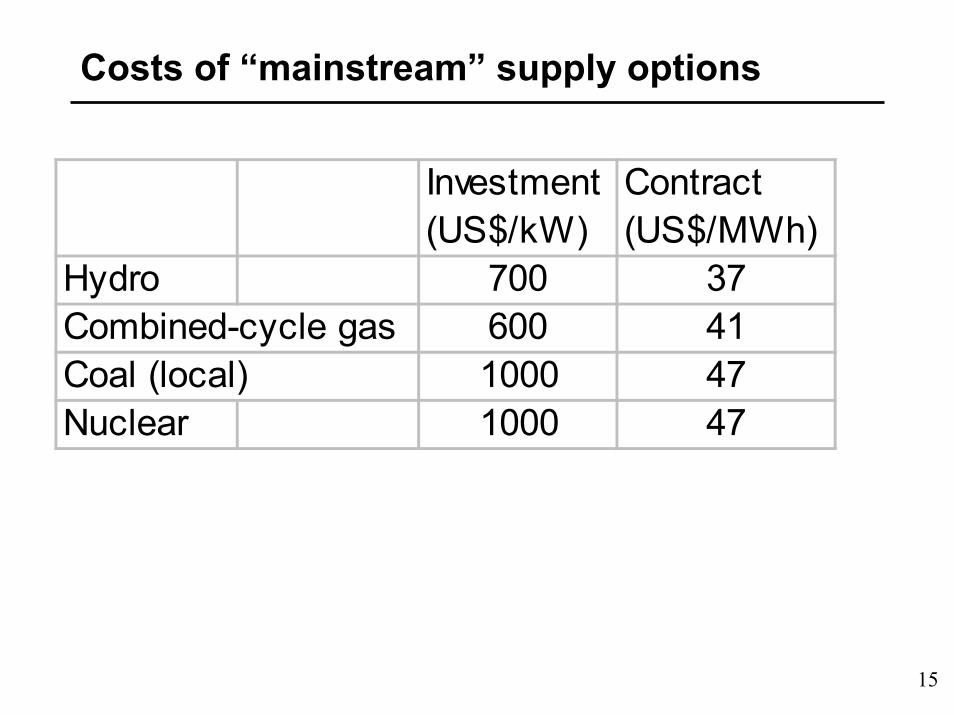

Costs of “mainstream” supply options

Investment (US$/kW)

Contract (US$/MWh)

Hydro 700 37Combined-cycle gas 600 41Coal (local) 1000 47Nuclear 1000 47

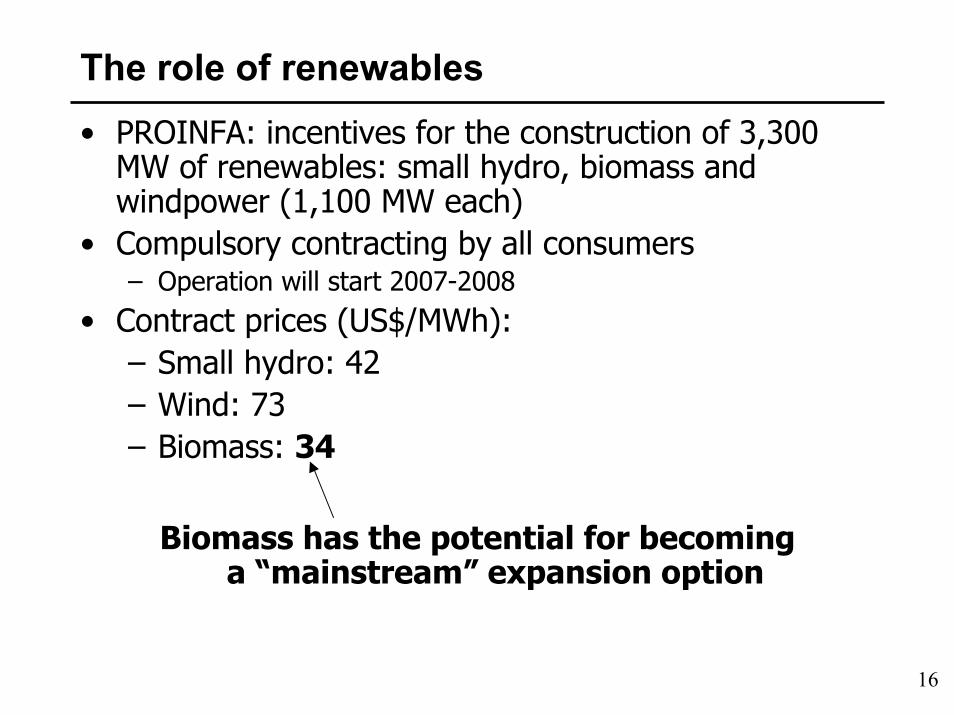

16

The role of renewables• PROINFA: incentives for the construction of 3,300

MW of renewables: small hydro, biomass and windpower (1,100 MW each)

• Compulsory contracting by all consumers– Operation will start 2007-2008

• Contract prices (US$/MWh):– Small hydro: 42– Wind: 73– Biomass: 34

Biomass has the potential for becominga “mainstream” expansion option

17

Sugarcane production - million tons

91

149

263303

350

0

50

100

150

200

250

300

350

400

1975 1980 1990 1995 2003

ProalcoolProalcool

Ethanol-run cars

Ethanol-run cars Sugar exports by

private sectorSugar exports by

private sector Flex-fuel cars and ethanol exports

Flex-fuel cars and ethanol exports

Source: Unica, Brazilian Sugar and Ethanol Market 2004, presentation by E.P.Carvalho, NY, March 2004

2010 projection: 540 million tons (50% increase)

18

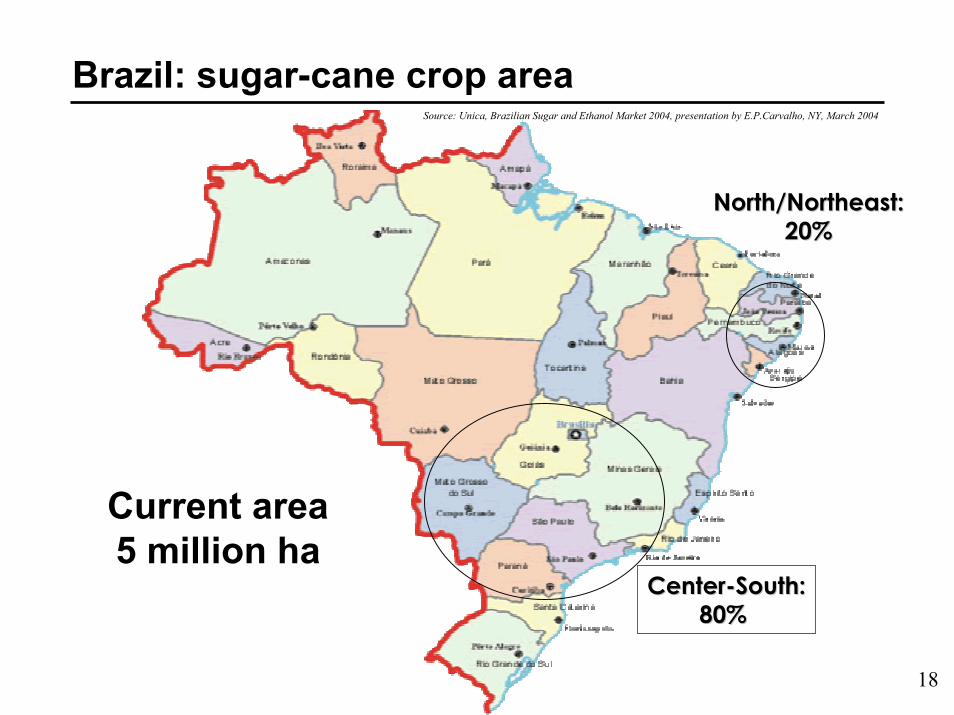

Brazil: sugar-cane crop area

Current area 5 million ha

North/Northeast: North/Northeast: 20%20%

CenterCenter--South:South:80% 80%

Source: Unica, Brazilian Sugar and Ethanol Market 2004, presentation by E.P.Carvalho, NY, March 2004

19

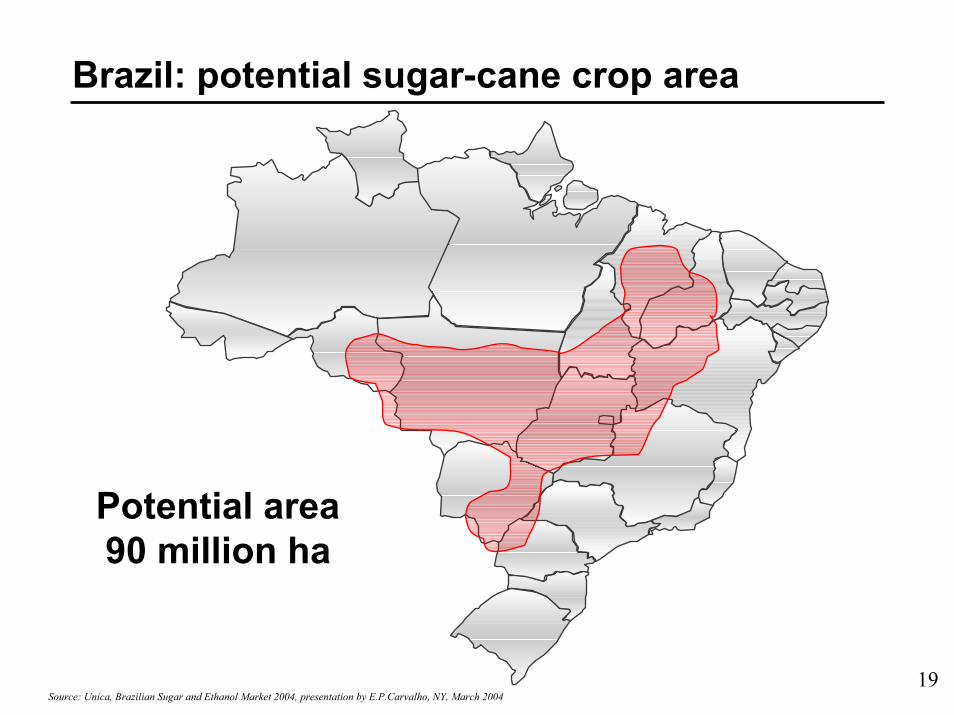

Brazil: potential sugar-cane crop area

Potential area 90 million ha

Source: Unica, Brazilian Sugar and Ethanol Market 2004, presentation by E.P.Carvalho, NY, March 2004

20

Economic advantages of Bioelectricity

• Shorter construction period– 2 years x 5 years for hydro– important due to uncertainty in load growth

• Natural “hedge” with sugar and ethanol production– greater competitiveness

• Location close to main load centers– reduction in transmission costs

• Synergy with hydro production pattern• Carbon credits

21

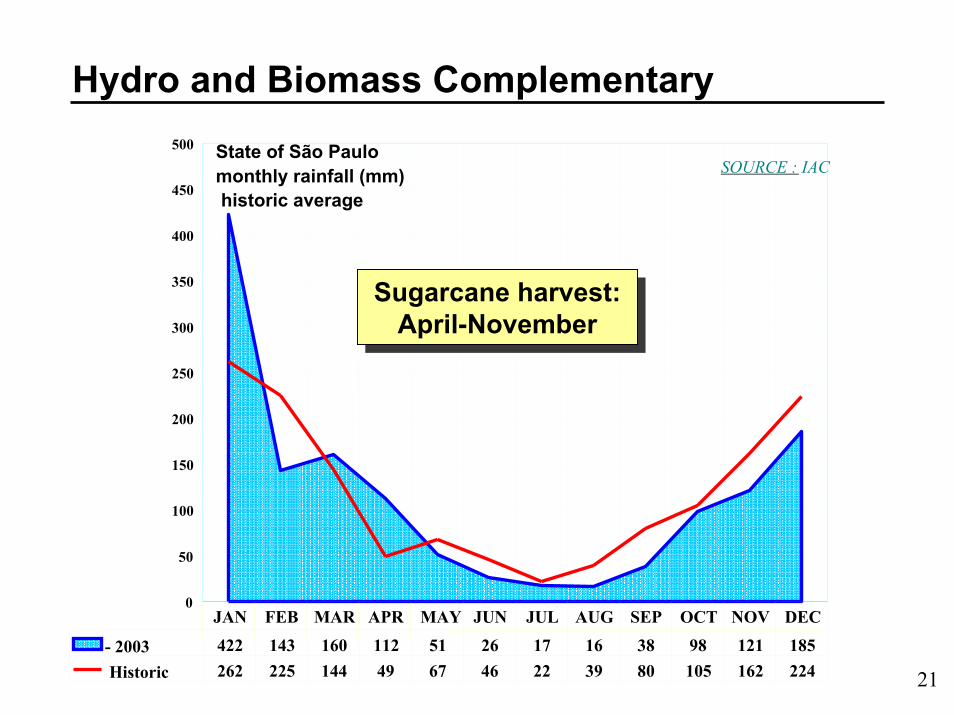

Hydro and Biomass Complementary

0

50

100

150

200

250

300

350

400

450

500

- 2003 422 143 160 112 51 26 17 16 38 98 121 185Historic 262 225 144 49 67 46 22 39 80 105 162 224

JAN FEB MAR APR MAY JUN JUL AUG SEP OCT NOV DEC

SOURCE : IACState of São Paulomonthly rainfall (mm)historic average

Sugarcane harvest:April-November

Sugarcane harvest:April-November

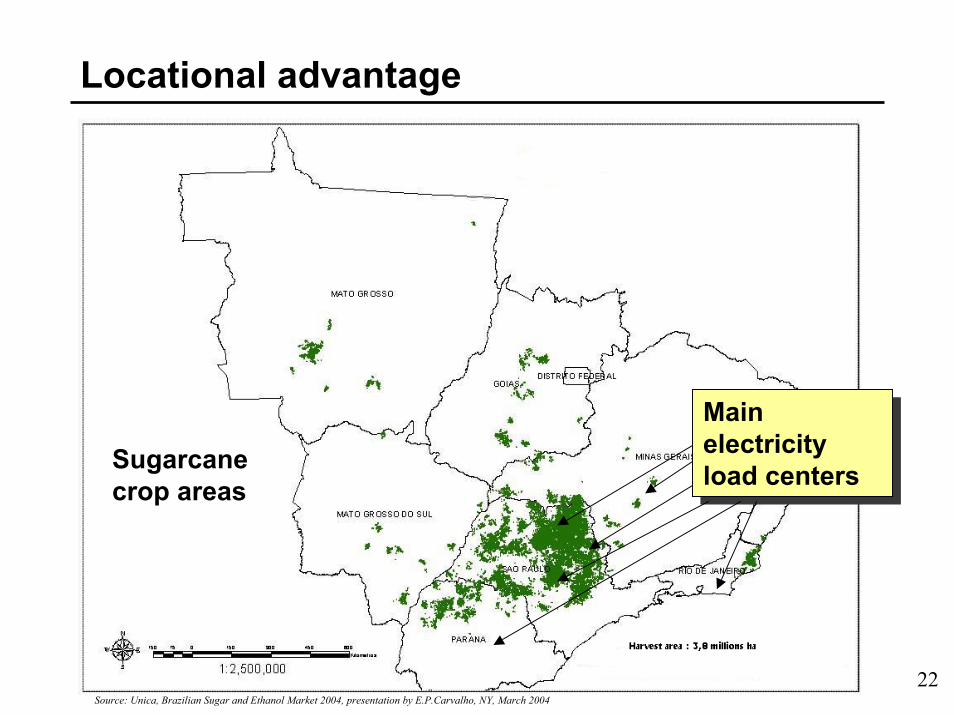

22

Locational advantage

Main electricity load centers

Main electricity load centers Sugarcane

crop areas

Source: Unica, Brazilian Sugar and Ethanol Market 2004, presentation by E.P.Carvalho, NY, March 2004

23

Additional Advantages of Bioelectricity

• Production in national currency• Wider range of investors• Job creation

24

The Biolectricity Initiative

• Joint endeavor of sugarcane producers and energy producers/traders

• Coordination with natural-based cogeneration initiative (COGEN)

25

Biolectricity objectives/actions

• Short-term objective: participate with at least 2500 MW in the new capacity action– Work with government (Ministry of Energy and

regulator) to finalize/detail power sector regulations

– Define with Ministry of Environment and Ministry of Energy a “baseline scenario” for carbon credits (Kioto rules)

– Additional negotiations with World Bank• Mid-term: explore additional opportunities

– Hydrogen from ethanol– Biorefineries

26

Conclusions

• Bioelectricity from sugarcane has the potential to become a “mainstream” energy option in the near future in Brazil

• “Window of opportunity” because of strong growth of sugar/ethanol sector, new power sector regulations and start of Kioto initiative