Embed Size (px)

Citation preview

Postville Community School District

Independent Auditor's Reports Basic Financial Statements

And Supplementary Information Schedule of Findings

June 30, 2017

Officials Independent Auditor's Report Management's Discussion and Analysis

Basic Financial Statements: Government-wide Financial Statements:

Statement of Net Position Statement of Activities

Governmental Fund Financial Statements: Balance Sheet

Table of Contents

Reconciliation of the Balance Sheet-Governmental Funds to the Statement of Net Position Statement of Revenues, Expenditures and Changes in Fund Balances Reconciliation of the Statement of Revenues, Expenditures and Changes in Fund Balances

Governmental Funds to the Statement of Activities Proprietary Fund Financial Statements:

Statement of Net Position Statement of Revenues, Expenses and Changes in Fund Net Position Statement of Cash Flows

Fiduciary Fund Financial Statements: Statement of Fiduciary Net Position Statement of Changes in Fiduciary Net Position

Notes to Financial Statements

Required Supplementary Information: Budgetary Comparison Schedule of Revenue, Expenditures/Expenses And Changes in Balances-

Budget and Actual · All Governmental Funds and Proprietary Funds Notes to Required Supplementary lnfonnation-Budgetary Reporting Schedule of the District's Proportionate Share of the Net Pension Liability Schedule of District Contributions Notes to Required Supplementary Infonnation - Pension Liability Schedule of Funding Progress for the Retiree Health Plan

Supplementary Information: Non-major Governmental Funds:

Combining Balance Sheet Combining Schedule of Revenues, Expenditures and Changes In Fund Balances

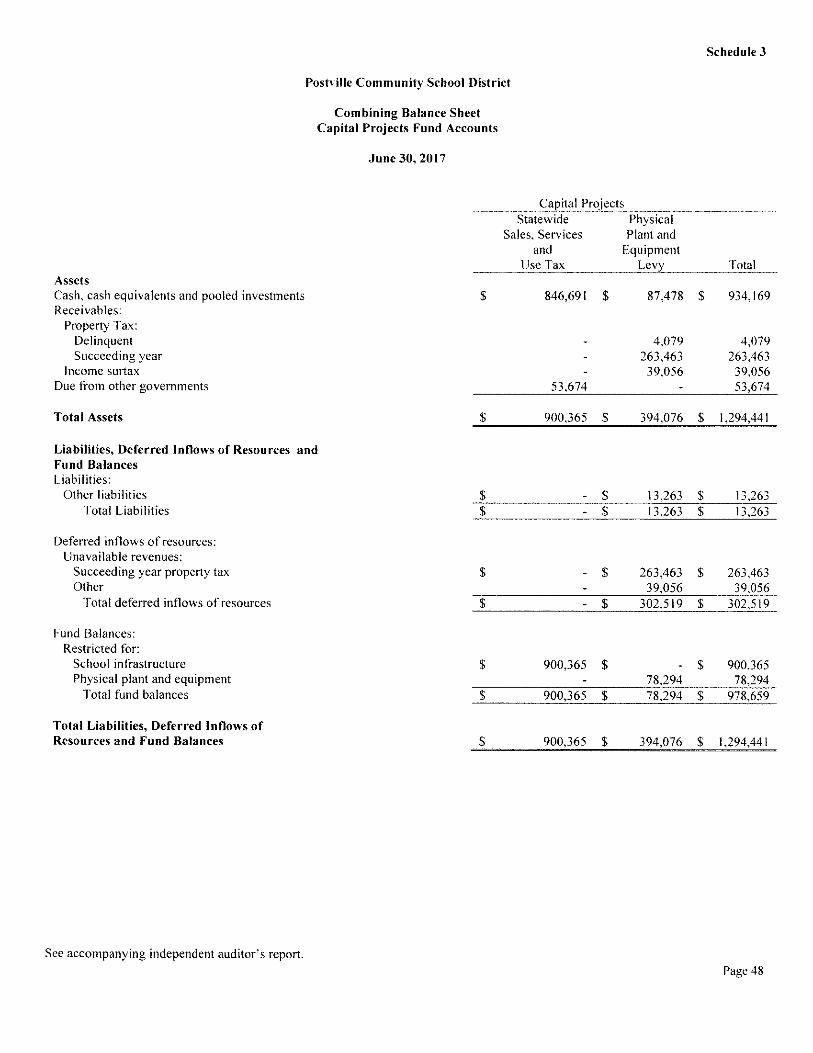

Capital Projects Fund Accounts: Combining Balance Sheet Combining Schedule of Revenues, Expenditures and Changes in Balances

Schedule of Changes in Special Revenue Fund-Student Activity Accounts Schedule of Changes in Fiduciary Assets and Liabilities-Agency Funds-Summary Schedule of Changes in Fiduciary Assets and Liabilities-Agency Funds-Detail Schedule of Fiduciary Net Position-Private Purpose Trusts Schedule of Change in Fiduciary Net Position-Private Purpose Trusts Schedule of Revenues by Source and Expenditures by Function-All Governmental Funds Schedule of Expenditures of Federal Awards

Independent Auditor's Report on Internal Control over Financial Reporting and on Compliance and Other Matters Based on an Audit of Financial Statements Performed in Accordance with Government Auditing Standards

Independent Auditor's Report on Compliance for Each Major Federal Program and on Internal Control over Compliance required by the Uniform Guidance

Schedule of Findings Summary Schedule of Prior Audit Findings Corrective Action Plan

Exhibit

A B

C D E

F

G H I

J K

Schedule

I 2

3 4 5 6 7 8 9 10 11

Page I

2-3 4-IO

11-12 13-14

15 16

17-18

19

20 21 22

23 24

25-39

40 41 42 43 44 45

46 47

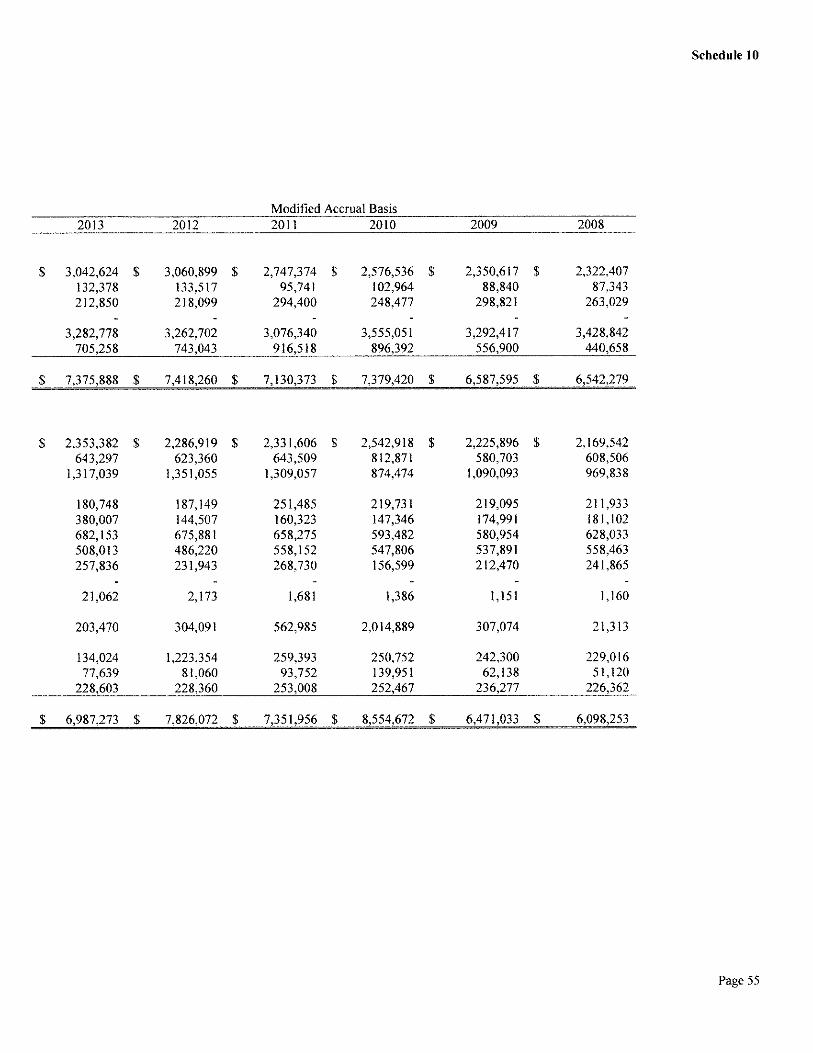

48 49 50 51 52 53 54 55

56-57

58-59

60-61

62-72 73 74

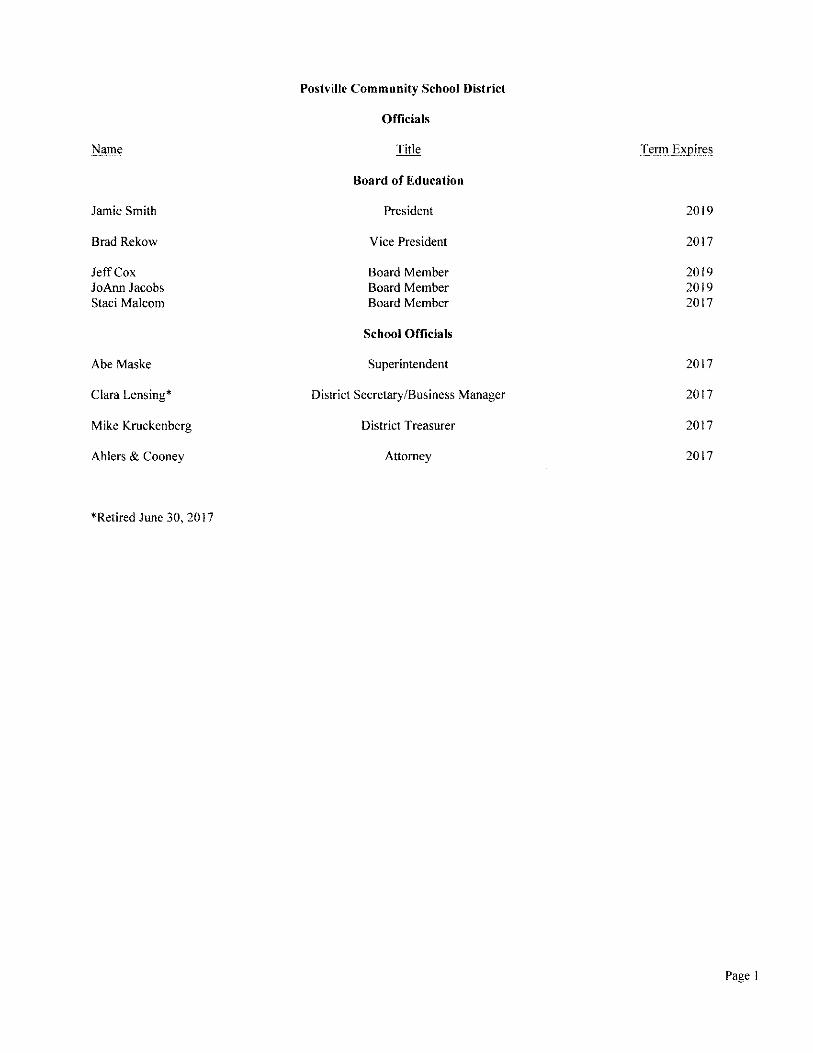

Postville Community School District

Officials

Name Title Term Expires

Board of Education

Jamie Smith President 2019

Brad Rekow Vice President 2017

Jeff Cox Board Member 2019 JoAnn Jacobs Board Member 2019 Staci Malcom Board Member 2017

School Officials

Abe Maske Superintendent 2017

Clara Lensing* District Secretary/Business Manager 2017

Mike Kruckenberg District Treasurer 2017

Ahlers & Cooney Attorney 2017

*Retired June 30, 20 I 7

Page I

Keith Oltrogge, CPA, P.C.

To the Board of Education of Postville Community School District:

Report on the Financial Statements

Independent Auditor's Report

20 l Eost /v\oin SlreFi

PO.Bo,310 Deroer, iuNCJ _':i0622

[319) 984 529? F!,X 13 !9, 98'16408

I have audited the accompanying financial statements of the governmental activities, the business type activities, each major fund and the aggregate remaining fund information of Postville Community School District, Postville, Iowa, as of and for the year ended June 30, 2017, and the related Notes to Financial Statements, which collectively comprise the District's basic financial statements listed in the table of contents.

Management's Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in accordance with U.S. generally accepted accounting principles. This includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement whether due to fraud or error.

Auditor's Responsibility

My responsibility is to express opinions on these financial statements based on my audit. I conducted my audit in accordance with U.S. generally accepted auditing standards and the standards applicable to fmancial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States. Those standards require that I plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor"s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the District's preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the District's internal control. Accordingly, I express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

l believe the audit evidence l have obtained is sufficient and appropriate to provide a basis for my audit opinions.

Opinions

In my opinion, the financial statements referred to above present fairly, in all material respects, the respective financial position of the governmental activities, the business type activities, each major fund and the aggregate remaining fund information of Postville Community School District, as of June 30, 2017, and the respective changes in its financial position and, where applicable, its cash flows thereof for the year then ended in accordance with lJ.S. generally accepted accounting principles.

/v\EfIBFR: b.tm Srxie1y of Certified Pubiic Accoun1ants • Minnesoro Society of Ce11ified Public Accounlonts • A.rn1:-ricon lnc,tilute of Co21Llied Accounlon!s ~ Divisio'l for CP/1. Firms ~ P1i,mte Companies Proc!ice Section

Page 2

Other Matters

Required Supplement my Jnf(Jrmation

U.S. generally accepted accounting principles require Management's Discussion and Analysis, the Budgetary Comparison Information, the Schedule of the District's Proportionate Share of the Net Pension Liability, the Schedule of District Contributions and the Schedule of Funding Progress for the Retiree Health Plan on pages 4 through IO and 40 through 45 be presented to supplement the basic financial statements. Such infonnation, although not a part of the basic financial statements, is required by the Governmental Accounting Standards Board which considers it to be an essential part of financial reporting for placing the basic financial statements in an appropriate operational, economic or historical context. I have applied certain limited procedures to the required supplementary information in accordance with U.S. generally accepted auditing standards, which consisted of inquiries of management about the methods of preparing the infonnation and comparing the information for consistency with management's responses to my inquiries, the basic financial statements and other knowledge I obtained during my audit of the basic financial statements. I do not express an opinion or provide any assurance on the information because the limited procedures do not provide me with sufficient evidence to express an opinion or provide any assurance.

Supp/ementwy Information

My audit was conducted for the purpose offo1111ing opinions on the financial statements that collectively comprise Postville Community School District's basic financial statements. I previously audited, in accordance with the standards referred to in the third paragraph of this report, the financial statements for the nine years ended June 30, 2016 (which are not presented herein) and expressed unmodified opinions on those financial statements. The supplementary information included in Schedules 1 through 11, including the Schedule of Expenditures of Federal Awards required by Title 2, U.S, Code of Federal Regulations, Part 200, Uniform Administrative Requirements, Cost Principles and Audit Requirements for Federal Awards (Uniform Guidance), is presented for purposes of additional analysis and is not a required part of the basic financial statements.

The supplementary information is the responsibility of management and was derived from and relates directly to the underlying accounting and other records used to prepare the basic financial statements. Such information has been subjected to the auditing procedures applied in the audit of the basic financial statements and certain additional procedures, including comparing and reconciling such information directly to the underlying accounting and other records used to prepare the basic financial statements or to the basic financial statements themselves, and other additional procedures in accordance with U.S. generally accepted auditing standards. In my opinion, the supplementary information is fairly stated in all material respects in relation to the basic financial statements taken as a whole.

Other jleporting Re_quired by Government Auditing Standards

In accordance with Government Auditing Standards, I have also issued my report dated January 19, 2018 on my consideration of Postville Community School District"s internal control over financial reporting and on my tests of its compliance with certain provisions of laws, regulations, contracts and grant agreements and other matters. The purpose of that report is solely to describe the scope of my testing of internal control over financial reporting and compliance and the results of that testing, and not to provide an opinion on the effectiveness of the District's internal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards in considering Postville Community School District's internal control over financial reporting and compliance.

Keith Oltrogge Certified Public Accountant

January 19, 20 I 8

Page 3

Post, ille Community School District

Manai:ement's Discussion and Analysis

For Fiscal Year Ended June 30, 2017

Postville Community School District provides this Management's Discussion and Analysis of its financial statements. This narrative overview and analysis of the financial activities is for the fiscal year ended June 30, 20 l 7. We encourage readers to consider this information in conjunction with the Districfs financial statements, which follow.

2017 FINANCIAL HIGHLIGHTS

• General Fund revenues increased from $7,2 I 9,957 in fiscal 2016 to $7,719,346 in fiscal 2017, and General Fund expenditures increased from $7,669,832 in fscal 2016 to $8,289,983 in fiscal 2017. The District's General Fund balance decreased from $2,306,217 in fiscal year 20 6 to $1,746,930 in fiscal year 2017, a 24.3% decrease.

• The increase in General Fund revenues was ,lttributable to an increase in local and state revenue in fiscal year 2017. The increase in expenditures was due primarily t1) an increase in instruction and support services costs.

• The District's solvency ratio decreased from 16.7% at June 30, 2016 to 9.4% at June 30, 2017. A District's solvency level indicates a District is able to meet unforeseen financing requirements and presents a sound risk for the timely repayment of short-term debt obligations.

lJSING THIS ANNlJAL REPORT

The annual report consists of a series of financial statements and other information, as follows:

Management's Discussion and Analysis ntroduces the basic financial statements and provides an analytical overview of the District's financial activities.

The Government-wide Financial Statements consist ofa Statement of Net Position and a Statement of Activities. These provide information about the activities uf Postville Community School District as a whole and present an overall view of the District's finances.

The Fund Financial Statements tell how governmental services were financed in the short term as well as what remains for future spending. Fund financial state11ents report Postville Community School District's operations in more detail than the government-wide financial statements by providing information about the most significant funds. The remaining financial statements provide information about activities for which Postville Community School District acts solely as an agent or custodian for the benefit of thos1! outside of the District.

Notes to Financial Statements provide additional information essential to a full understanding of the data provided in the basic financial statements.

Required Supplementary Information further explains and supports the financial statements with a comparison of the District's budget for the year, the Distric1's proportionate share of the net pension liability and related contributions, as well as presenting the Schedule of Fundilg Progress for the Retiree Health Plan.

Supplementary Information provides detailed information about the non-major governmental funds. In addition, the Schedule of Expenditures off ederal Aw irds provides details of various federal programs benefiting the District.

Page 4

REPORTING THE DISTRICT'S FINANCIAL ACTIVITIES

Government-wide Financial Statements

The government-wide financial statements report information about the District as a whole using accounting methods similar to those used by private-sector companies. The Statement of Net Position includes all of the District's assets, deferred outflows of resources, liabilities and deferred inflows of resources, with the difference reported as net position. All of the current year's revenues and expenses are accounted for in the Statement of Activities. regardless of when cash is received or paid.

The two government-wide financial statements report the District's net position and how it has changed. Net position is one way to measure the District's financial health or financial position. Over time, increases or decreases in the District's net position is an indicator of whether financial position is improving or deteriorating. To assess the District's overall health, additional non-financial factors, such as changes in the District's property tax base and the condition of school buildings and other facilities, need to be considered.

In the government-wide financial statements, the District's activities are divided into two categories:

• Governmental activities: Most of the District's basic services are included here, such as regular and special education, transportation and administration. Property tax and state aid finance most of these activities.

• Business type activities: The District charges fees to help cover the costs of certain services it provides. The District's school nutrition program is included here.

Fund Financial Statements

The fund financial statements provide more detailed information about the District's funds, focusing on its most significant or "major" funds - not the District as a whole. Funds are accounting devices the District uses to keep track of specific sources of funding and spending on particular programs.

Some funds are required by state law and by bond covenants. The District establishes other funds to control and manage money for particular purposes, such as accounting for student activity funds, or to show it is properly using certain revenues, such as federal grants.

The District has three kinds of funds:

I) Governmental funds: Most of the District's basic services are included in governmental funds, which generally focus on (I) how cash and other financial assets that can readily be converted to cash flow in and out and (2) the balances left at year-end that are available for spending. Consequently, the governmental fund statements provide a detailed short-term view that helps detennine whether there are more or fewer financial resources that can be spent in the near future to finance the District's programs.

The District's governmental funds include the General Fund, the Special Revenue Funds, the Debt Service Fund and the Capital Projects Fund.

The required financial statements for governmental funds include a Balance Sheet and a Statement of Revenues, Expenditures and Changes in Fund Balances.

2) Proprietary fimds: Services for which the District charges a fee are generally reported in proprietary funds. Proprietary funds are reported in the same way as the government-wide financial statements. The District's Enterprise Fund, one type of proprietary fund, is the same as its business type activities, but provides more detail and additional information, such as cash flows. The District currently has three Enterprise Funds, the School Nutrition Fund, the Student Construction Fund and the Pirate Enterprise Fund.

The required financial statements for proprietary funds include a Statement of Net Position, a Statement of Revenues, Expenses and Changes in Fund Net Position and a Statement of Cash Flows.

Page 5

3) Fiduchuyfimds: The District is the trustee, or fiduciary, for assets that belong to others. These funds include Private Purpose Trust and Agency Funds, as follow~:

• Private Purpose Trust Fund - The District accounts for outside donations for scholarships for individual students in this fund.

• Agency Funds - These are funds through which the District administers and accounts for certain federal and/or state grants as a fiscal agent.

The District is responsible for ensuring the assets reported in the fiduciary fonds are used only for their intended purposes and by those to whom the assets belong. The District excludes the,:e activities from the government-wide financial statements because it cannot use these assets to finance its operations.

The required financial statements for fiduciary funds includes a Statement of Fiduciary Net Position and a Statement of Changes in Fiduciary Net Position.

Reconciliations between the government-wide financ·a1 statements and the governmental fund financial statements follow the governmental fund financial statements.

GOVERNMENT-WIDE FINANCIAL ANALYSIS

Figure A-1 below provides a summary of the Districts net position at June 30, 2017 compared to June 30, 2016.

Figure A-1 Condensed Statement of Net Position

Governmental Business Type Total Activi1ies Activities District June :,0, June 30, June 30,

Total Change June 30,

2017 2016 2017 2016 2017 2016 2016-2017

Current and other assets $7, I 02,463 $7,884,210 $106,272 $121,442 $7,208,735 $8,005,652 -10.0% Capital assets 9,765,470 9,4 I 8,185 80,414 54,389 9,845,884 9,472,574 3.9~/()

Total assets $16,867,933 $ I 7,302,395 $186,686 $175,831 $17,054,619 $17,478,226 -2.4%

Deferred outflows of resources $1,761,724 $921,505 $60,309 $32,335 $1,822,033 $953,840 91.0%

Long-term liabilities $5,468,280 $4,896,445 $130,219 $100,804 $5,598,499 $4,997,249 12.0% Other liabilities 1,183,027 I, 127,502 6,472 9,783 I, 189,499 1,137,285 4.6%

Total liabilities $6,651,307 $6,023,947 $136,691 $110,587 $6,787,998 $6,134,534 10,7%

Deferred in1lows of resources $2,345,883 $2,898,128 $1,554 $23,472 $2,347,437 $2,921,600 -19.7%

Net position Net investment in capital assets $8,234,602 $7,675,881 $80,414 $54,389 $8,315,016 $7,730,270 7,6% Restricted 2,741,906 2,976,194 2,741,906 2,976,194 -7.8% Unrestricted -1,344,041 -1,350,250 28,336 19,718 -1,315,705 -1,330,532 1.1% Total net position $9,632,467 $9,301,825 $108,750 $74,107 $9,741,217 $9,375,932 3.9%

The District's combined net position increased 3.9%, or $365,285, from the prior year. The largest portion of the District's net position is invested in capital assets (e.g., land, infrasiructure, buildings and equipment), less the related debt. The debt related to the investment in capital assets is liquidated with sources other than capital assets.

Restricted net position represents resources subject to external restrictions, constitutional provisions or enabling legislation on how they can be used. The District's restricted net positio, decreased $234,288 or 7.8% from the prior year.

Page 6

Unrestricted net position - the part of net position that can be used to finance day-to-day operations without constraints established by debt covenants, enabling legislation or other legal requirements - increased by $14,827, or 1.1 %,. This increase in unrestricted net position was primarily a result of the District's increase in revenues.

Figure A-2 shows the changes in net position for the year ended June 30, 2017 compared to the year ended June 30, 2016.

Figure A-2 Changes in Net Position

Governmental Business Type Total Activities Activities Total District Change

2017 2016 2017 2016 2017 2016 2016-2017 Revenues: Program revenues: Charges for service $262,672 $250,626 $59,984 $62,470 $322.656 $313.096 3.1% Operating grants, contributions and restricted interest 1,872,948 1,713,048 429,458 415,979 2,302,406 2,129,027 8.1%

Capital grants, contributions and restricted interest

General revenues: Property tax 2,229,068 2,212,855 2,229,068 2,212.855 0.7% Income surtax 315,064 263,573 315,064 263,573 19.5% Statewide sales, services and use tax 644,866 628,257 644,866 628,257 2.6% Unrestricted state grants 3,707,343 3,480,091 3,707,343 3,480,091 6.5% Unrestricted investment earnings 14,253 14.728 JOO 79 14,353 14,807 -3.1% Other 80,023 70,734 80,023 70,734 13.1%

Total revenues $9,126.237 $8,633,912 $489,542 $478,528 $9,615,779 $9,112,440 5.5%

Program expenses: Governmental activities:

Instruction $5,931,782 $6,254,536 $3 $- $5,931,785 $6,254,536 -5.2% Support services 2,4 I 8,623 2,138,120 16,065 17,118 2,434,688 2,155,238 13.0'% Non-instructional programs 53,548 42,988 438,831 455,153 492,379 498,141 0.7% Other expenses 405,089 362,151 405,089 362,151 11.9% Total expenses $8,809,042 $8,797,795 $454,899 $472,271 $9,263,941 $9,270,066 -0.1%

Change in net position before sale of assets $317,195 -$ I 63,883 $34,643 $6.257 $351,838 -$157,626 323.2% Sale of assets 13,447 19,493 13,447 19,493 -13.0% Change in net position $330,642 -$ 144,390 $34,643 $6,257 $365,285 -$138,133 364.4%

Net position beginning of year $9,301,825 $9,448,346 $74,107 $67,850 $9,375,932 $9,516,196 -1.5% Prior period adjustment -2, 131 -2, 13 I 100.0% Adjusted net position beginning of Year $9,301,825 $9,446,215 $74,107 $67,850 $9,375,932 $9,514,065 -1.5%

Net position end of year $9,632,467 $9,301,825 $108,750 $74,107 $9,741.217 $9,375.932 3.9%

In fiscal year 2017, property tax and unrestricted state grants accounted for 61.7% of governmental activities revenue while charges for service and operating grants, contributions and re~.tricted interest accounted for 99.9% of business type activities revenue. The District's total revenues were approximately $9.6 mil lion, of which approximately $9.1 million was for governmental activities and less than $0.5 million was for business type activities

As shown in Figure A-2, the District as a whole experienced a 5.5% increase in revenues and a 0.1 % decrease in expenses. Property tax increased approximately $16,000.

Page 7

Governmental Activities

Revenues for governmental activities were $9,126,237 and expenses were $880,942 for the year ended June 30, 2017. In a difficult budget year, the District was able to balance the budget by trimming expenses to match available revenues.

The following table presents the total and net cost of:he District's major governmental activities, instruction, support services, noninstructional programs and other expenses for the year ended June 30, 2017 compared to those expenses for the year ended June 30. 2016.

Instruction Support services Non-instructional programs Other expenses

Totals

For the year ended June 30, 2017:

Figure A-3 Total and Net Cost of Governmental Activities

Total Cost Net Cost of Services Change of Services

2017 2016 2016-2017 2017 2016

$5,931,782 $6,254,536 -5.2% $3,802,275 $4,302,582 2,418,623 2,138,120 13.1% 2,412,510 2,126,400

53,548 42,988 24.6% 53,548 42,988 405,089 362,151 11.9% 405,089 362,151

$8,809,042 $8,797,795 0.1% $6.673,422 $6,834,121

• The cost financed by users of the District's ~rograms was $322,656.

Change 2016-2017

-11.6% 13.5% 24.6% 11.9%

-2.4%

• Federal and state governments subsidized certain programs with grants and contributions totaling $2,302,406.

• The net cost of governmental activities was tinanced with $2,544,132 of property and other taxes and $3,707,343 of unrestricted state grants.

Business Type Activities

Revenues for business type activities during the year ,,nded June 30, 2017 were $489,542 representing a 2.3% increase over the prior year, while expenses totaled $454,899, a 3.7% decrease from the prior year. The District's business type activities include the School Nutrition and Pirate Enterprise Funds. Revenues of these activities were comprised of charges for service, federal and state reimbursements and investment income.

INDIVIDUAL FUND ANALYSIS

As previously noted, Postville Community School Dhtrict uses fund accounting to ensure and demonstrate compliance with financerelated legal requirements.

The financial perfonnance of the District as a whole i~ reflected in its governmental funds, as well. As the District completed the year, its governmental funds reported a combined fund balance of$9,632,467, above last year's ending fund balances of$9,301,825.

Governmental Fund Highlights

• The District's decrease in General Fund financial position is the result of many factors. The decrease during the year in tax and other local sources resulted in a decreasr in revenues. The increase in expenditures and the decrease in revenue resulted in the decrease in the General Fund.

• The General Fund balance decreased from $1,306,217 to $1,746,930 due, in part, to the expenditures exceeding revenue.

• Capital Projects Funds balance decreased fr,m $1,308,063 to $978,659, due in part to expenditures exceeding revenue.

Page 8

Proprietary Fund Highlights

School Nutrition Fund net position increased from $73,789 at June 30, 2016 to$ I 07,425 at June 30, 2017. representing an increase of approximately 45.6%. The Private Enterprises Fund net position increased from $257 at June 30, 2016 to $1,264 at June 30, 2017, representing an increase of 392.0%

BUDGETARY HIGHLIGHTS

Over the course of the year, Postville Community School District amended its budget one time to reflect additional expenditures in instruction and other expenditures.

The District's total revenues were $117,284 less than total budgeted revenues, a variance of 1.2%. The most significant variance resulted from the District receiving less in federal sauces than originally anticipated.

Total expenditures were less than budgeted, due primarily to the District's budget for the General Fund. It is the District's practice to budget expenditures at the maximum authorized spenjing authority for the General Fund. The District then manages or controls General Fund spending through its line-item budget. As a result, the District's certified budget should always exceed actual expenditures for the year.

CAPITAL ASSETS AND DEBT ADMINISTRATION

Capital Assets

At June 30, 2017, the District had invested $9,845,884, net of accumulated depreciation, in a broad range of capital assets. including land, buildings, athletic facilities, computers, audio-v sual equipment and transportation equipment. (See Figure A-4) This represents a net increase of 3.9% from last year. More detailed information about the District's capital assets is presented in Note 5 to the financial statements. Depreciation expense for the year was $709,383.

The original cost of the District's capital assets was $22,029,939. Governmental funds accounted for $21,912,949, with the remainder of $116.990 accounted for in the Proprieta,y, School 'Jutrition Fund.

Land Construction in process Buildings Improvements other than

buildings Furniture and equipment

Totals

Governmental Activities June 30,

2017 2016

$89,000 $89,000 78,673 108,489

8,261,786 7,645,164

283,559 294,390 1,052,452 1,281,142

$9,765,470 $9,418,185

Figure A-4 Capital Assets, net of Depreciation

Business Type Total Activities District June 30, June 30,

2017 2016 2017 2016

$- $- $89,000 $89,000 78,673 I 08,489

8,261,786 7,645,164

283,559 294,390 80,414 54.389 I, 132,866 1,335,531

$80,414 $54,389 $9,845,884 $9,472,574

Total Change June 30,

2016-2017

-27.5% 8.1%

-3.7% -15.2% 3.9%

Page 9

Long-Term Debt

At June 30, 2017, the District had $1,530,868 in other long-term debt outstanding. This represents a decrease of 12. I% from last year. (See Figure A-5) Additional information about the District's long-term debt is presented in Note 6 to the financial statements.

The District continues to carry a general obligation bond rating of Aa3 assigned by national rating agencies to the District's debt since 1997. The Constitution of the State of Iowa limits the amount of general obligation debt districts can issued to 5% of the assessed value of all taxable property within the District. The District's outstanding general obligation debt is significantly below its constitutional debt limit of approximately $17.0 milli,,n.

Revenue bonds Capital lease

Totals

Figure A-5 Outstanding Long-term Obligations

Total Total District Change June 30, June 30,

2017 2016 2016-2017

$1,200,000 $1,300,000 -7.7% 330,868 442,304 -25.2%

$ I ,530,868 $1,742,304 -12.1%

ECONOMIC FACTORS BEARING ON THE DISTRICT'S FUTURE

At the time these financial statements were prepared and audited, the District was aware of existing circumstances which could significantly affect its financial health in the future:

• Funding to local school districts from federal and state agencies needs to be monitored closely, as possible decreases will result in less funding and may require budget adjustments in some areas in the future.

CONTACTING THE DISTRICT'S FINANCIAL MANAGEMENT

This financial report is designed to provide the District's citizens, taxpayers, customers, investors and creditors with a general overview of the District's finances and to demonstrate the District's accountability for the money it receives. If you have questions about this report or need additional financial information, contact Melissa Fettkether, District Secretary, Postville Community School District, P.O. Box 717, Postville IA 52162.

Page 10

Basic Financial Statements

Exhibit A Postville Community School District

Statement of Net Position

June 30, 2017

Govern- Business mental Type

Activities Activities Total Assets Cash, cash equivalents and pooled investments $ 4,233,466 $ 104,794 $ 4,338,260 Receivables:

Property tax: Delinquent 34,960 34,960 Succeeding year 2,300,485 2,300,485

1 ncome surtax 292,918 292,918 Accounts 24,979 251 25,230

Due from other governments 212,761 212,761 Due from other funds 2,894 2,894 Inventories 1,227 1,227 Capital assets, net of accumulated depreciation/amortization 9,765,470 80,414 9,845,884

Total Assets $ 16,867,933 $ 186,686 $ 17,054,619

Deferred Outnows of Resources Pension related deferred outflows $ 1,761,724 $ 60,309 $ 1,822,033

Liabilities Accounts payable $ 107,796 $ $ 107,796 Salaries and benefits payable 734,349 734,349 Other liabilities 13,263 13,263 Advances from grantors 68,965 68,965 Due to other governments 6,600 6,600 Accrued interest payable 8,939 8,939 Unearned revenue 6,472 6,472 Long-term liabilities:

Portion due within one year: Revenue bonds 100,000 100,000 Capital lease 113,081 113,081 Early retirement 30,034 30,034

Portion due after one year: Revenue bonds 1,100,000 1,100,000 Capital lease 217,787 217,787 Early retirement 30,000 30,000 Net pension liability 3,803,881 130,219 3,934,100 Net OPEB liability 316,612 316,612 Total Liabilities $ 6,651,307 $ 136,691 $ 6,787,998

Deferred Inflows of Resources Unavailable property tax revenue $ 2,300,485 $ $ 2,300,485 Pension related deferred inflows 45,398 1,554 46,952

Total deferred inflows of resources $ 2,345,883 $ 1,554 $ 2,347,437

Page 11

Net Position Net investment in capital assets Restricted for:

Categorical funding Debt service Capital projects Management levy purposes Student activities Physical plant and equipment

Unrestricted

Total Net Position

See notes to financial statements.

Postville Community School District

Statement of Net Position

,June 30,2017

$

Govern-mental

Activities

8,234,602 $

970,783 177,825 900,365 607,082

7,557 78,294

-1,344,041

$ 9,632,467 $

Exhibit A

Business Type

Activities Total

80,414 $ 8,315,016

970,783 177,825 900,365 607,082

7,557 78,294

28,336 -1,315,705

108,750 $ 9,741,217

Page 12

Poshille Community School District

Statement of Activities

Year Ended June 30, 2017

Program Revenues Operating Capital

Grants, Grants. Contributions Contributions

Charges and and for Restricted Restricted

Exr:enses Services Interest Interest Functions/Programs Governmental Activities:

Instruction: Regular instruction $ 4,043,736 $ 126,934 $ 1,189,180 $ Special instruction 1,224,034 35,610 62.714 Other instruction 664,012 95,333 619.736

$ 5,931,782 $ 257,877 $ 1,871,630 $ Support Services:

Student services $ 297,827 $ $ 1,318 $ Instructional staff services 607,894 Administration services 612,815 Operation and maintenance of plant services 634,697 4,695 Transportation services 265,390 100

$ 2,418,623 $ 4,795 $ 1,318 $

Non-instructional programs $ 53,548 $ $ $

Other Expenditures: Facilities acquisition $ 45,697 $ $ $ Long-term debt interest 67,087 A EA flow-through 292,305

$ 405,089 $ $ $

Total Governmental Activities $ 8,809,042 $ 262,672 $ 1,872,948 $

Business Type Activities: Non-Instructional Programs:

Food service operations $ 438,831 $ 58,974 $ 429,458 $

Instructional: Pirate enterprise $ 3 $ 1,010 $ $

Support Services: Administration services $ 15,529 $ $ $ Operation and maintenance of plant services 536

$ 16,065 $ $ $

Total Business Type Activities $ 454,899 $ 59,984 $ 429,458 $

Total $ 9,263,941 $ 322.656 $ 2,302,406 $

$

$

$

$

$

$

$

$

$

$

$

$

$

$

Net (Expense) Revenue And Chanoes in Net Position

Governmental Activities

-2,727,622 -1,125,710

51,057 -3,802,275

-296,509 -607,894 -612,815 -630,002 -265,290

-2.412,510

-53,548

-45,697 -67,087

-292,305 -405,089

-6,673,422

-

-

-6,673,422

$

$

$

$

$

$

$

$

$

$

$

$

$

$

Business Type

Activities

49,601

1,007

-15,529 -536

-16,065

34,543

34,543

$

$

$

$

$

$

$

$

$

$

$

$

$

$

Exhibit B

T)tal

-2,727,622 -1.125,710

51,057 -3,802,275

-296,509 -607,894 -612,815 -630,002 -265,290

-2,412,510

-53,548

-45,697 -67,087

-292,305 -405,089

-6,673,422

49,601

1,007

-15,529 -536

-16,065

34,543

-6,638,879

Page 13

General Revenues: Property Tax Levied For:

General purposes Capital outlay

Income surtax Statewide sales, services and use tax Unrestricted state grants Unrestricted investment earnings Other

Total General Revenues

Change in net position before sale of assets

Sale of assets

Change in net position

Net position beginning of year

Net Position End of Year

See notes to financial statements.

Postville Community School District

Statement of Activities

Year Ended June 30, 2017

Expenses

Charges for

Services

Program Revenues Operating

Grants, Contributions

and Restricted Interest

Capital Grants,

Contributions and

Restricted Interest

$

$

$

$

$

Net (Expense) Revenue And Changes in Net Position

Governmental Activities

1,969,651 259,417 315,064 644,866

3,707,343 14,253 80,023

6,990,617

317,195

13,447

330,642

9,301,825

9,632,467

$

$

$

$

$

Business Type

Activities

100

100

34,643

34,643

74,107

I 08,750

$

$

$

$

$

Exhibit B

Total

1,969,651 259,417 315,064 644,866

3,707,343 14,353 80,023

6,990,717

351,838

13,447

365,285

9,375,932

9,741.217

Page 14

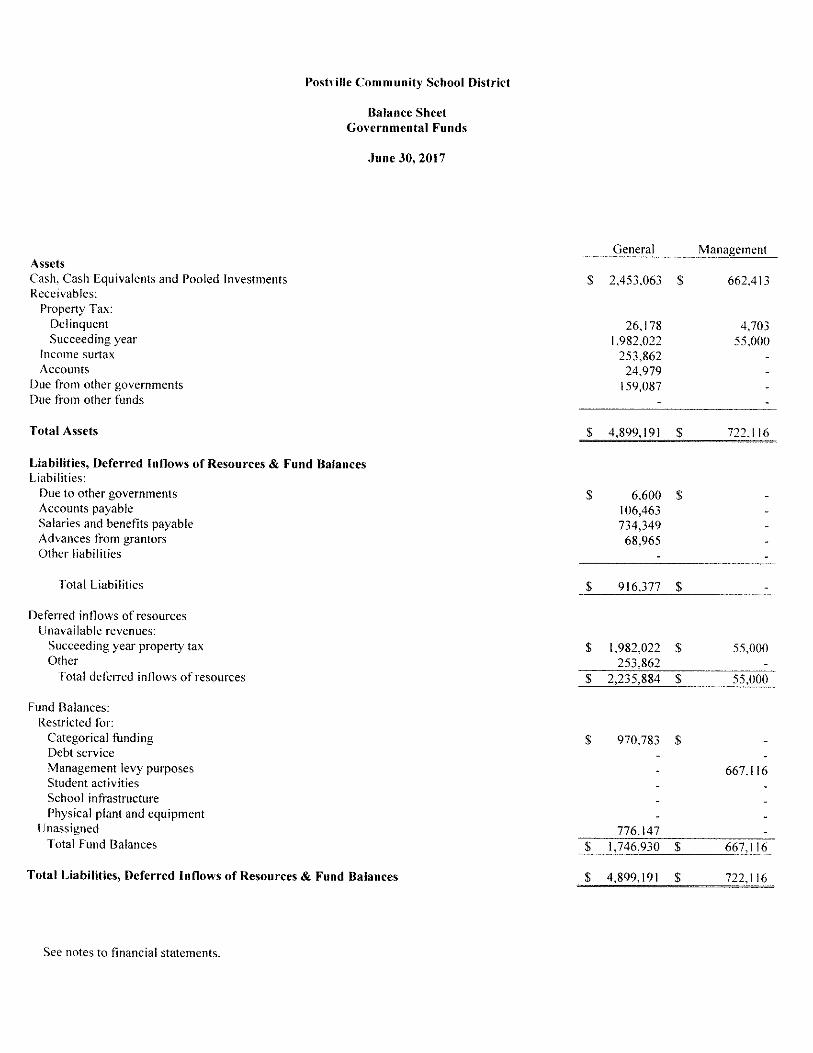

Assets Cash, Cash Equivalents and Pooled Investments Receivables:

Property Tax: Delinquent Succeeding year

Income surtax Accounts

Due from other governments Due from other funds

Total Assets

Poshille Community School District

Balance Sheet Governmental Funds

June 30, 2017

Liabilities, Deferred Inflows of Resources & Fund Balances Liabilities:

Due to other governments Accounts payable Salaries and benefits payable Advances from grantors Other liabilities

Total Liabilities

Deferred inflows of resources Unavailable revenues:

Succeeding year property tax Other

Total deferred inflows of resources

Fund Balances: Restricted for:

Categorical funding Debt service Management levy purposes Student activities School infrastructure Physical plant and equipment

Unassigned Total Fund Balances

Total Liabilities, Deferred Inflows of Resources & Fund Balances

See notes to financial statements.

General Management

$ 2,453,063 $ 662,413

26,178 4,703 1,982,022 55,000

253,862 24,979

159,087

$ 4,899,191 $ 722,116

$ 6,600 $ 106,463 734,349 68,965

$ 916,377 $

$ 1,982,022 $ 55,000 253,862

$ 2,235,884 $ 55,000

$ 970,783 $

667,116

776,147 $ 1,746,930 $ 667,116

$ 4,899,191 $ 722,116

$

$

$

$

$

$

$

$

$

Capital Projects

934,169 $

4,079 263,463

39,056

53,674

1,294,441 $

$

13,263

13,263 $

263,463 $ 39,056

302,519 $

$

900,365 78,294

978,659 $

1,294,441 $

Non-Major Funds

183,821

2,894

186,715

1,333

1,333

177,825

7,557

I 85,382

186,715

Total

4,233,466

34,960 2,300,485

292,918 24,979

212,761 2,894

$ 7,102,463

$ 6,600 107,796 734,349 68,965 13,263

$ 930,973

$ 2,300,485 292,918

$ 2,593,403

$ 970,783 177,825 667,116

7,557 900,365

78,294 776,147

$ 3,578,087

$ 7, I 02,463

Exhibit C

Page 15

Poshille Community School District

Reconciliation of the Balance Sheet - Governmental Funds To the Statement of Net Position

June 30, 2017

Total fund balances of governmental funds (page 15)

Antou11ts reported for gm1er11me11tal activities in the Statement of Net Position are d{fferent becau,'ie:

Capital assets used in governmental activities are not financial resources and, therefore, are not reported as assets in the govemmen:al funds

Other long-term assets, including income surtax receivable, are not available to pay current year expenditures and, therefore, are recognized as deferred inflows of resources in the governmental funds.

Accrued interest payable on long-term liabilities is not due and payable in the current year and, therefore, is not reported as a liability in the governmental funds

Pension related deferred outflows of resources and deferred inflows of resources are not due and payable in the current year and, therefore, are not reported in the governmental funds, as follows:

Deferred outflows of resources Deferred inflows of resources

Long-term liabilities, including bonds and notes payaJle, early retirement, other postemployment benefits payable and net pension liability are not due and payable in the current year and, therefore, are not reported in the governmental funds

Net position of governmental activities (page 12)

See notes to financial statements.

$ 1,761,724 -45,398

Exhibit D

3,578,087

9,765,470

292,918

-8,939

1,716,326

-5,711,395

$ 9,632,467

Page 16

Exhibit E

Posl\ille Community School District

Statement of Revenues, Expenditures and Changes in Fund Balances Governmental Funds

Year Ended June 30, 2017

Non-Capital Major

General Management Projects Funds Total Revenues:

Local Sources: Local tax $ 1,934,424 $ 299,966 $ 300,147 $ $ 2,534,537 Tuition 160,625 160,625 Other 52,692 12,726 36,135 94,769 196,322

Intermediate sources State sources 4,929,205 4,710 648,842 5,582,757 Federal sources 642,400 642,400

Total Revenues $ 7,719,346 $ 317,402 $ 985,124 $ 94,769 $ 9,116,641

Expenditures: Current:

Instruction: Regular instruction $ 3,753,824 $ 30,398 $ $ $ 3,784,222 Special instruction 1,291,140 1,291,140 Other instruction 588,698 103,927 692,625

$ 5,633,662 $ 30,398 $ $ 103,927 $ 5,767,987 Support Services:

Student services $ 296,276 $ 1,484 $ $ $ 297,760 Instructional staff services 452,930 2,370 17,300 472,600 Administration services 752,722 2,891 1,000 756,613 Operation and maintenance of

plant services 56 I ,044 44,431 28,853 634,328 Transportation services 250,450 12,830 263,280

$ 2,313,422 $ 64,006 $ 47,153 $ $ 2,424,581 Non-instructional programs $ 50,594 $ 1,496 $ $ $ 52,090 Other Expenditures:

Facilities acquisition $ $ $ 989,630 $ $ 989,630 Long-Term Debt:

Principal 211,436 211,436 Interest and fiscal charges 68,295 68,295

AEA flow-through 292,305 292.305 $ 292,305 $ $ 989,630 $ 279,731 $ 1,561,666

Total Expenditures $ 8,289,983 $ 95,900 $ 1,036,783 $ 383,658 $ 9,806,324

Excess (deficiency) of revenues over (under) expenditures $ -570,637 $ 221,502 $ -51,659 $ -288,889 $ -689,683

Other Financing Sources (Uses): Operating transfers in $ $ $ $ 279,842 $ 279,842 Operating transfers out -2,097 -277,745 -279,842 Sale of equipment 13,447 13,447

Total Other Financing Sources (Uses) $ 11,350 $ $ -277,745 $ 279,842 $ 13,447

Page 17

Poshille Community School District

Statement of Revenues, Expenditures and Changes in Fund Balances Governmental Funds

Year Ended June 30, 2017

Capital General Management Projects

Change in fund balances $ -559,287 $ 221,502 $ -329,404

Fund balances beginning of year 2,306,217 445,614 1,308,063

Fund Balances End of Year $ 1,746,930 $ 667,116 $ 978,659

See notes to financial statements,

Exhibit E

Non-Major Funds Total

$ -9,047 $ -676,236

194,429 4,254,323

$ 185,382 $ 3,578,087

Page 18

Post, ille Community School District

Reconciliation of the Statement of Revenues, Expenditures and Changes in Fund Balances - Governmental Funds

T> the Statement of Activities

Year Ended June 30, 2017

Change in fund balances - total governmental funjs (page 18)

Amou11t.\· reported for governme11tal activities ill the Statement of Activities are different hecau.5e:

Capital outlays to purchase or build capital assets are reported in governmental funds as expenditures. These costs are not rep01ted in the Stat=ment of Activities but they are allocated over the estimated useful lives of the capital assets as depreciation expense in the Statement of Activities. Capital outlay expenditures exceeded dep··eciation expense in the current year, as follows:

Expenditures for capital assets Depreciation expense

Income surtax revenue not received until several months after year end is not considered available revenue and is recognized as deferred inflows ofreso.1rces in the governmental funds.

Proceeds from issuing long-term liabilities provide ctrrent financial resources to governmental funds, but issuing debt increases long-term liabilities in the Statement of Net Position. Repayment of long-term liabilities is an expenditure in the goverr-mental funds, but the repayment reduces long-term liabilities in the Statement of Net Position. Current year repayments exceeded issuances as follows:

Repaid

Interest on long-term debt in the Statement of Activifes differs from the amount reported in the governmental funds because interest is recorded as ar expenditure in the governmental funds when due. In the Statement of Activities, interest expense j5 recognized as the interest accrues, regardless of when it is due.

The current year District IPERS contributions are rep)rted as expenditures in the governmental funds but are reported as deferred outflows of resources in the Statement of Net Position.

Some expenses reported in the Statement of Activities do not require the use of current financial resources and, therefore, are not reported as expenditures in the governmental funds, as follows:

Early retirement Pension expense Other postemployment benefits

Change in Net Position of Governmental Activitie, (page 14)

See notes to financial statements.

$

$

1,046,919 -699,634

-59,556 90,566

-35,724

$

$

Exhibit F

-676,236

347,285

9,596

211,436

1,208

442,067

-4,714

330,642

Page 19

Exhibit G

Postville Community School District

Statement of Net Position Proprietary Funds

June 30, 2017

School Student Pirate Nutrition Construction Enterprise Total

Assets Current assets: Cash and cash equivalents $ 103,469 $ 61 $ 1,264 $ 104,794 Accounts receivable 251 251 Inventories 1,227 1,227

Total Current Assets $ 104,947 $ 61 $ 1,264 $ 106,272

Non-current assets: Capital assets, net of accumulated depreciation $ 80,414 $ $ $ 80,414

Total non-current assets $ 80,414 $ $ $ 80,414

Total Assets $ 185,361 $ 61 $ 1,264 $ 186,686

Deferred Outflows of Resources Pension related deferred outflows $ 60,309 $ $ $ 60,309

Liabilities Current liabilities: Unearned revenue $ 6,472 $ $ $ 6,472

Total Current Liabilities $ 6,472 $ $ $ 6,472

Non-current liabilities: Net pension liability $ 130,219 $ $ $ 130,219

Total non-current liabilities $ 130,219 $ $ $ 130,219 Total Liabilities $ 136,691 $ $ $ 136,691

Deferred Inflows of Resources Pension related deferred inflows $ 1,554 $ - $ $ 1,554

Net Position Net investment in capital assets $ 80,414 $ $ $ 80,414 Unrestricted 27,01 I 61 l,264 28,336

Total Net Position $ 107,425 $ 61 $ 1,264 $ 108,750

See notes to financial statements. Page 20

Exhibit H

Post, ille Community School District

Statement of Revenues, Expenses and Changes in Fund Net Position Proprietary Funds

Year Ended June 30, 2017

School Student Pirate Nutrition Construction Enterprise Total

Operating revenues: Local sources: Charges for service/product $ 58,974 $ $ 1,010 $ 59,984

Operating expenses: Instruction:

Other $ $ $ 3 $ 3 Support services:

Administration services $ 15,529 $ $ $ 15,529 Operation and maintenance of plant services 536 536

$ 16,065 $ $ $ 16,065

Non-instructional programs: Food service operations: Salaries $ 148,247 $ $ $ 148,247 Benefits 35,722 35,722 Purchased services 5,565 5,565 Supplies 239,548 239,548 Depreciation 9,749 9,749

$ 438,831 $ $ $ 438,831 Total operating expenses $ 454,896 $ $ 3 $ 454,899

Operating income (loss): $ -395,922 $ $ 1,007 $ -394,915

Non-operating revenues: State sources $ 3,631 $ $ $ 3,631 Federal sources 425,827 425,827 Interest income 100 100 Total non-operating revenues $ 429,558 $ $ $ 429,558

Increase (Decrease) in net position $ 33,636 $ $ 1,007 $ 34,643

Net position beginning of year 73,789 61 257 74,107

Net Position End of Year $ I 07,425 $ 61 $ 1,264 $ I 08,750

See notes to financial statements.

Page 21

Posh ille Community School District

Statement of Cash Flows Proprietary Funds

Year Ended June 30, 2017

Cash flo\VS from operating activities: Cash received from sale of products and donations Cash received from sale of lunches and breakfasts Cash paid to employees for services Cash paid to suppliers for goods or services

Net cash provided (used) by operating activities

Cash flows from non-capital financing activities: State grants received Federal grants received Net cash provided by non-capital financing activit es

Cash flows from capital and related financing activitii!s: Acquisition of capital assets

Cash flows from investing activities: Interest on investments

Net increase (decrease) in cash and cash equivalents

Cash and cash equivalents beginning of year

Cash and Cash Equivalents End of Year

$

$

$

$

$

$

$

$

Reconciliation of operating income (loss) to net c,sh provided (used) by operating activities: Operating income (loss) $ Adjustments to reconcile operating income (loss) to net cash provided

(used) by operating activities: Commodities used Depreciation Decrease in inventories Decrease in accounts receivable (Decrease) in accounts payable (Decrease) in salaries and benefits payable Increase in unearned revenue Increase in net pension liability (Increase) in deferred outflows of resources (Decrease) in deferred inflows of resources

Net Cash Provided (Used) by Operating Activities $

Non-cash investing, capital and financing activitiei;: During the year ended June 30, 2017, the District received $38,520 of federal commodities.

See notes to financial statements.

Exhibit I

School Pirate Nutrition Enterprise

$ 1,010 61,035

-222,718 -207,055 -3 -368,738 $ 1,007

3,631 $ 396,383 400,014 $

-35, 774 $

100 $

-4,398 $ 1,007

107,867 257

103,469 $ 1.264

-395,922 $ 1,007

38,520 9,749 1,706

997 -273

-4,102 1,064

29,415 -27,974 -21,918

-368,738 $ 1,007

Page 22

Assets

Cash, cash equivalents and pooled investments Accounts receivable

Total Assets

Liabilities Due to other funds Other accounts payable Accounts payable

Total liabilities

Net position

Restricted for scholarships

See notes to financial statements.

Poshille Community School District

Stat<ment of Fiduciary Net Position Fiduciary Funds

June 30, 2017

$

$

$

$

$

Private Purpose Trust

Scholarships

22,109 $

22,109 $

$

$

22,109 $

Exhibit J

Agency

16,147

16,147

2,894 1.369

I 1.884

16,147

Page 23

Additions: Local sources:

Interest income

Deductions: Instruction:

Regular instruction: Scholarships awarded

Change in net position

Net position beginning of year

Net Position End of Year

See notes to financial statements.

Postville Community School District

Statement of Changes in Fiduciary Net Position Fiduciary Funds

Year Ended June 30, 2017

$

$

$

$

Private Purpose Trust

Scholarships

249

400

- I 5 I

22,260

22,109

Exhibit K

Page 24

Pos1'ille Community School District

Notes to Financial Statements

June 30, 2017

(I) Summary of Significant Accounting Polic1es

Postville Community School District is a po itical subdivision of the State oflowa and operates public schools for children in grades kindergarten through twelve. Additionally, the District either operates or sponsors various adult education programs. These courses include remedial education as well as career and technical and recreational courses. The geographic area served includes the City of Postville, Iowa and portions of the predominately agricultural territories in Allamakee, Clayton, Fayette and Winneshiek Counties. The District is governed by a Board of Education whose members are elected on a nonpartisan basis.

The District's financial statements are prepared in conformity with U.S. generally accepted accounting principles as prescribed by the Governmental Accounting Standards Board.

A. Reporting Enti!}'.

For financial reporting purposes, Postville Community School District has included all funds, organizations, agencies, boards, commissions and authorities. The District has also considered all potential component units for which it is financially accountable and other organizations for which the nature and significance of their relationship with the District are such that exclusion would cause the District's financial statements to be misleading or incomplete. The Governmental Ac,:ounting Standards Board has set forth criteria to be considered in determining financial accountability. These crit~ria include appointing a voting majority ofan organization's governing body and (I) the ability of the District to impose its will on that organization or (2) the potential for the organization to provide specific benefits to or impose specific financial burdens on the District. The District has no component units which meet the Governmental Accounting Standards Board criteria.

Jointly Governed Organization The District participates in a jointly governed organization that provides services to the District but does not meet the c1iteria of a joint venture since there is no ongoing financial interest or responsibility by the participating governments. The District is a member of the County Assessor's Conference Board.

B. Basis of Presentation

Government-wide Financial Statements~ The Statement of Net Position and the Statement of Activities report information on all of the non-fiduci ,ry activities of the District. For the most part, the effect of interfund activity has been removed from these statements. Governmental activities, which normally are supported by tax and intergovernmental revenues, are reriarted separately from business type activities, which rely to a significant extent on fees and charges for service.

The Statement of Net Position presents the District's non-fiduciary assets, deferred outflows of resources, liabilities and deferred inflows of resources, with the difference reported as net position. Net position is reported in the following categories:

Net investment in capital l.Ssets, consists of capital assets, net of accumulated depreciation/amortization and reduced by outstanding ba ances for bonds, notes and other debt attributable to the acquisition, construction or improvement of those a;sets.

Restricted net position results when constraints placed on net position use are either externally imposed or are imposed by law through constitutional provisions or enabling legislation. Enabling legislation did not result in any restricted net position

Unrestricted net position consists of net position not meeting the definition of the preceding categories. Unrestricted net position ii, often subject to constraints imposed by management which can be removed or modified.

Page 25

The Statement of Activities demonstrates the degree to which the direct expenses of a given function or segment are offset by program revenues. Direct expenses are those clearly identifiable with a specific function. Program revenues include (I) charges to customers or applicants who purchase, use or directly benefit from goods, services, or privileges provided by a given function and (2) grants, contributions and interest restricted to meeting the operational or capital requirements of a particular function. Property tax and other items not properly included among program revenues are reported instead as general revenues.

Fund Financial Statements - Separate financial statements are provided for governmental, proprietary and fiduciary funds, even though the latter are excluded from the government-wide financial statements. Major individual governmental funds are reported as separate columns in the fund financial statements. All remaining governmental funds are aggregated and reported as non-major governmental funds. Combining schedules are also included for the Capital Projects Fund accounts.

The District reports the following major governmental funds:

The General Fund is the general operating fund of the District. All general tax revenues and other revenues not allocated by law or contractual agreement to some other fund are accounted for in this fund. From the fund are paid the general operating expenditures, including instructional, support and other costs.

The Management Fund is used to account for all resources used for the cost of employment benefits, early retirement benefits and insurance agreements.

The Capital Projects Fund is used to account for all resources used in the acquisition and construction of capital facilities and other capital assets.

The District reports the following major proprietary fund:

The Enterprise, School Nutrition Fund is used to account for the food service operations of the District.

The District also reports fiduciary funds which focus on net position and changes in net position. The District's fiduciary funds include the following:

The Private Purpose Trust Fund is used to account for assets held by the District under trust agreements which require income earned to be used to benefit individuals through scholarship awards.

The Agency Fund is used to account for assets held by the District as an agent for individuals, private organizations and other governments. The Agency Fund is custodial in nature, assets equal liabilities, and does not involve measurement of results of operations.

C. Measurement Focus and Basis of Accounting

The government-wide, proprietary and fiduciary fund financial statements are reported using the economic resources measurement focus and the accrual basis of accounting. Revenues are recorded when earned and expenses are recorded when a liability is incurred, regardless of the timing of related cash flows. Property tax is recognized as revenue in the year for which it is levied. Grants and similar items are recognized as revenue as soon as all eligibility requirements imposed by the provider have been satisfied.

Governmental fund financial statements are reported using the current financial resources measurement focus and the modified accrual basis of accounting. Revenues are recognized as soon as they are both measurable and available. Revenues are considered to be available when they are collectible within the current period or soon enough thereafter to pay liabilities of the current period. For this purpose, the government considers revenues to be available if they are collected within 60 days after year-end.

Page 26

Property tax, intergovernmental revenues (shared revenues, grants and reimbursements rrom other governments) and interest associated with the current fiscal period are all considered to be susceptible to accrual. All other revenue items are considered to be measurable and available only when cash is received by the District.

Expenditures generally are recorded when a liability is incurred, as under accrual accounting. However, principal and interest on long-term debt, claims and judgments and compensated absences are recognized as expenditures only when payment is due. Capital asset acquisitions are reported as expenditures in governmental funds. Proceeds of general long-term debt and acquisitions under capital leases are reported as other financing sources.

Under the terms of grant agreements, the District funds certain programs by a combination of specific costreimbursement grants and general revenues. _Thus, when program expenses are incurred, there are both restricted and unrestricted net position available to finance the program. It is the District's policy to first apply costreimbursement grant resources to such programs and then general revenues.

When an expenditure is incurred in governmental funds which can be paid using either restricted or unrestricted resources, the District's policy is generally to first apply the expenditure toward restricted fund balance and then to less-restrictive classifications - committed, assigned and then unassigned fund balances.

Proprietary funds distinguish operating revenues and expenses rrom non-operating items. Operating revenues and expenses generally result rrom providing services and producing and delivering goods in connection with a proprietary fund's principal ongoing operations. The principal operating revenues of the District's Enterprise Funds is charges to customers for sales and services. Operating expenses for Enterprise Funds include the cost of sales and services, administrative expenses and depreciation on capital assets. All revenues and expenses not meeting this definition are reported as non-operating revenues and expenses.

The District maintains its financial records on the cash basis. The financial statements of the District are prepared by making memorandum adjusting entries to the cash basis financial records.

D. Assets, Deferred Outflows of Resources, Liabilities, Deferred Inflows of Resources and Fund Equity

The following accounting policies are followed in preparing the financial statements:

Cash, Cash Equivalents and Pooled Investments -The cash balances of most District funds are pooled and invested. Investments are stated at fair value.

For purposes of the Statement of Cash Flows, all short-term cash investments that are highly liquid are considered to be cash equivalents. Cash equivalents are readily convertible to known amounts of cash and, at the day of purchase, have a maturity date no longer than three months.

Property Tax Receivable - Property tax in governmental funds is accounted for using the modified accrual basis of accounting.

Property tax receivable is recognized in these funds on the levy or lien date, which is the date the tax asking is certified by the Board of Education. Delinquent property tax receivable represents unpaid taxes for the current and prior years. The succeeding year property tax receivable represents taxes certified by the Board of Education to be collected in the next fiscal year for the purposes set out in the budget for the next fiscal year. By statute, the District is required to certify its budget in April of each year for the subsequent fiscal year. However, by statute, the tax asking and budget certification for the following fiscal year becomes effective on the first day of that year. Although the succeeding year property tax receivable has been recorded, the related revenue is deferred in both the government-wide and fund financial statements and will not be recognized as revenue until the year for which it is levied.

Page 27

Property tax revenue recognized in these funds become due and collectible in September and March of the fiscal year with a I½% per month penalt:1 for delinquent payments; is based on January 1, 2015 assessed property valuations; is for the tax accrual period July I, 2016 through June 30, 2017 and reflects the tax asking contained in the budget certified to the County Board of Supervisors in April 2016.

Due from Other Governments - Due from other governments represents amounts due from the State of Iowa, various shared revenues, grants and reimbursements from other governments.

Inventories Inventories are valuec. at cost using the first-in, first-out method for purchased items and government commodities. Inventories of proprietary funds are recorded as expenses when consumed rather than when purchased or received.

Capital Assets~ Capital assets, which include property, furniture and equipment, are reported in the applicable governmental or business type acth-ities columns in the government-wide Statement of Net Position. Capital assets are recorded at historical cost. Donated capital assets are recorded at acquisition value. Acquisition value is the price that would have been paid to acquire a capital asset with equivalent service potential. The costs of normal maintenance and repair that do not :1dd to the value of the asset or materially extend asset lives are not capitalized. Capital assets are defined by the Di;trict as assets with an initial, individual cost in excess of the following thresholds and estimated useful lives in excess of two years.

Asset Class Land Buildings Improvements other than building:; Furniture and equipment:

School Nutrition Fund equipment Other furniture and equipment

Capital assets are depreciated using the straight-line method over the following estimated useful lives:

Asset Class Buildings Improvements other than building:; Furniture and equipment

Amount $ 2,000

10,000 10,000

500 2,000

Estimated Useful Lives

(In Years) 50 years

20 - 50 years 5 - 15 years

Deferred Outflows of Resources--· DefeJTed outflows of resources represent a consumption of net position applicable to a future year(s) which will not b, recognized as an outflow of resources (expense/expenditure) until then. Deferred outflows of resources con:;ist of unrecognized items not yet charged to pension expense and contributions from the District after the measurement date but before the end of the District's reporting period.

Salaries and Benefits Payable Pa,roll and related expenditures for teachers with annual contracts corresponding to the current school year, which are ,ayable in July and August, have been accrued as liabilities.

Advances from Grantors ~ Grant proceeds which have been received by the District but will be spent in a succeeding fiscal year.

Long-Tenn Liabilities In the govtTnrnent-wide financial statements, long-term debt and other long-term obligations are reported as liabilitie; in the governmental activities column in the Statement of Net Position.

Pensions For purposes of measuring the net pension liability, deferred outflows of resources and deferred inflows of resources related to pensions and pension expense, information about the fiduciary net position of the Iowa Public Employees' Retirement System (!PERS) and additions to/deductions from !PERS' fiduciary net position have been determined on the same basis as they are reported by !PERS. For this purpose, benefit payments including refunds of employee contributions are recotnized when due and payable in accordance with the benefit terms. Investments are reported at fair value. The net rosition liability attributable to the governmental activities will be paid primarily by the General Fund.

Page 28

Deferred Inflows of Resources Deferred inflows of resources represent an acquisition of net position applicable to a future year(s) which \Vill not be rtcognized as an inflow of resources (revenue) until that time. Although certain revenues are measurable, they are not available. Available means collected within the current year or expected to be collected soon enough thereafter to be used to pay liabilities of the current year. Deferred inflows of resources in the governmental fund financial statements represent the amount of assets that have been recognized, but the related revenue has not been recognized since the assets are not collected within the current year or expected to be collected soon enough thereafi:er to be used to pay liabilities of the current year. Deferred inflows of resources consist of property tax receivable and other receivables not collected within sixty days after year-end.

Deferred inflows of resources in the Statement of Net Position consist of succeeding year property tax receivable that will not be recognized until the year for which it is levied and the unamortized portion of the net difference between projected and actual earnings on pension plan investments.

_Fund Eguity - In the governmental fund financial statements, fund balances are classified as follows:

Restricted Amounts restricted to specific purposes when constraints placed on the use of the resources are either externally imposed by creditors, grantors or state or federal laws or imposed by law through constitutional provisions or enabling legislation.

Committed·- Amounts which can be used only for specific purposes determined pursuant to constraints formally imposed by the Board of Education through resolution approved prior to year end. Those committed amounts cannot be used for any other purpose unless the Board of Education removes or changes the specified use by taking the same action it employed to commit those amounts.

Unassigned All amounts not included in the preceding classifications.

E. Budgets and Budgetary Accounting

The budgetary comparison and relaced disclosures are reported as Required Supplementary Information.

(2) Cash, Cash Equivalents and Pooled Investments

The District's deposits in banks at June 30, ,017 were entirely covered by federal depository insurance or by the State Sinking Fund in accordance with Chapter I 2C of the Code of Iowa. This chapter provides for additional assessments against the depositories to insure there will be no loss of public funds.

The District is authorized by statute to invesr public funds in obligations of the United States government, its agencies and instrumentalities; certificates of deposit or 01her evidences of deposit at federally insured depository institutions approved by the Board of Education; prime eligible bankers acceptances; certain high rated commercial paper; perfected repurchase agreements; certain registered open-end maragement investment companies; certain joint investment trusts; and warrants or improvement certificates of a drainage distrkt.

The District had no investments meeting the disclosure requirements of Governmental Accounting Standards Board Statement No. 72.

(3) Inter-fund Transfers

The detail of inter-fund transfers for the yeai ended June 30, 2017 is as follows:

Transfer to Debt Service Debt Service Special Revenue - Student Activity

Total

Transfer from Capital Projects-· Physical Plant and Equipment Levy Capital Projects - Statewide Sales, Services, and Use Tax General Fund

$

$

Amount 120,33 I 157,414

2,097 279,842

Transfers generally move revenues from the fund statutorily required to collect the resources to the fund statutorily required to expend the resources.

Page 29

(4) Due From and Due to Other Funds

The detail of inter-fund receivables and payables at June 30, 2017 is as follows:

Receivable Fund Pa~able Fund Amount Special Revenue - Student Activity Agency Fund $ 2,894

The Agency Fund owes the Special Revenue - Student Activity Fund for negative cash. The balance is to be repaid by June 30,2018.

(5) Capital Assets

Capital assets activity for the year ended June 30.2017 was as follows:

Balance Balance Beginning End Of Year Increases Decreases Of Year

Governmental Activities: Capital assets not being depreciated: Land $ 89,000 $ $ $ 89,000 Construction in process 108,489 78,673 108,489 78,673 Total capital assets not being depreciated $ 197,489 $ 78,673 $ 108,489 $ 167,673

Capital assets being depreciated: Buildings $ 14,119,592 $ 918,717 $ $ 15,038,309 Improvements other than buildings 730,460 16,072 746,532 Furniture and equipment 5,8 l 8,489 141,946 5,960,435 Total capital assets being depreciated $ 20,668,541 $ 1,076,735 $ $ 21,745,276

Less accumulated depreciation for: Buildings $ 6,474,428 $ 302,095 $ $ 6,776,523 Improvements other than buildings 436,070 26,903 462,973 Furniture and equipment 4,537,347 370,636 4,907,983 Total accumulated depreciation $ 11,447,845 $ 699,634 $ $ 12,147,479

Total capital assets being depreciated, net $ 9,220,696 $ 377,101 $ $ 9,597,797

Governmental Activities Capital Assets, Net $ 9,418,185 $ 455,774 $ 108,489 $ 9,765,470

Balance Balance Beginning End Of Year Increases Decreases Of Year

Business type activities: Furniture and equipment $ 95,887 $ 35,774 $ 14,671 $ 116,990 Less accumulated depreciation 41,498 9,749 14,671 36,576

Business Type Activities Capital Assets, Net $ 54,389 $ 26,025 $ $ 80,414

Page 30

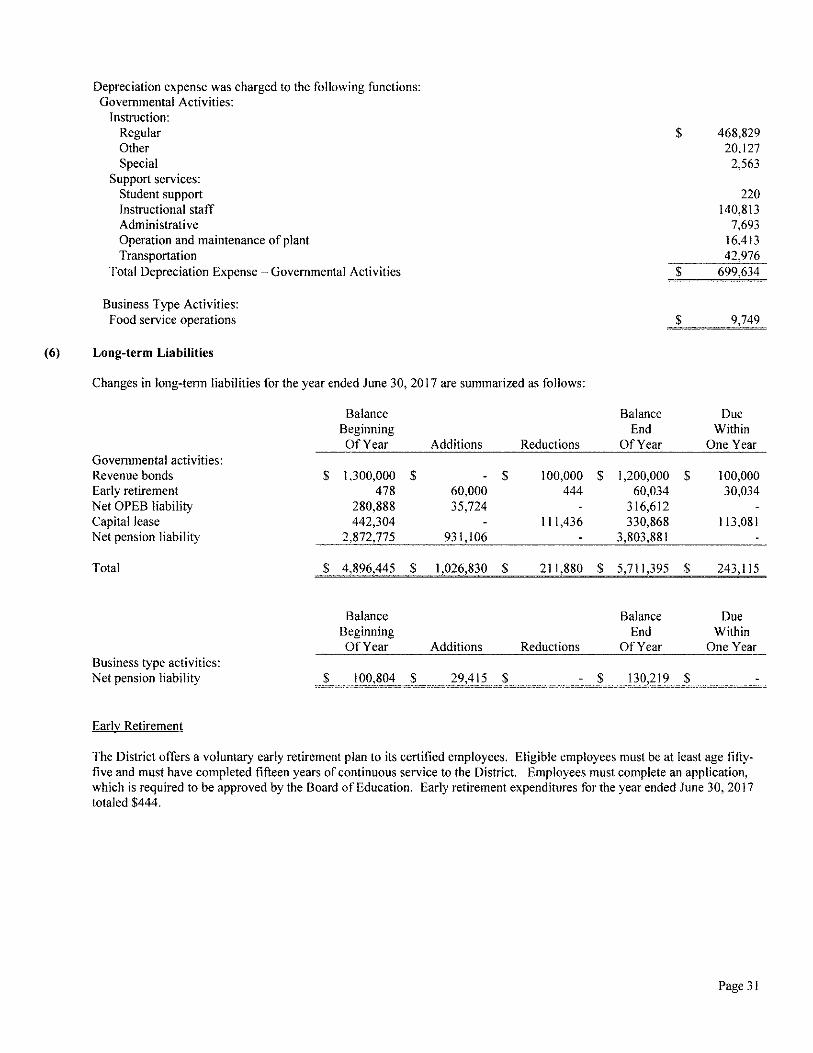

Depreciation expense was charged to the following functions: Governmental Activities:

Instruction: Regular Other Special

Support services: Student support Instructional staff Administrative Operation and maintenance of plant Transportation

Total Depreciation Expense - Governmental Activities

Business Type Activities: Food service operations

(6) Long-term Liabilities

Changes in long-term liabilities for the year ended June 30, 2017 are summarized as follows:

Governmental activities: Revenue bonds Early retirement Net OPEB liability Capital lease Net pension liability

Total

Business type activities: Net pension liability

Early Retirement

$

$

$

Balance Beginning Of Year

1,300,000 478

280,888 442,304

2,872,775

4,896,445

Balance Beginning Of Year

100,804

Additions Reductions

$ $ 100,000 60,000 444 35,724

111,436 931,106

$ 1,026,830 $ 211,880

Additions Reductions

$ 29,415 $

$

$

$

Balance End

Of Year

$ 1,200,000 $ 60,034

316,612 330,868

3,803,881

$ 5,711,395 $

Balance End

Of Year

$ 130,219 $

468,829 20,127

2,563

220 140,813

7,693 16,413 42,976

699,634

9,749

Due Within

One Year

I 00,000 30,034

113,081

243,115

Due Within

One Year

The District offers a voluntary early retirement plan to its certified employees. Eligible employees must be at least age fiftyfive and must have completed fifteen years of continuous service to the District. Employees must complete an application, which is required to be approved by the Board of Education. Early retirement expenditures for the year ended June 30, 2017 totaled $444.

Page 31

Capital Lease

The District entered into a capital lease with Apple Inc. to purchase computers for $61,740 with a 5.32% interest rate. Annual lease payments are $16,876.43 endir g July 15, 2018. Details of the Capital Lease are as follows:

Capital Lease Issued July 15, 2015

Year Ending Interest June 30, Rate Principal Interest Total

2018 5.32% $ 15,215 $ 1,662 $ 16,877 2019 5.32% 16,024 852 16,876

$ 31,239 $ 2,514 $ 33,753

The District entered into a capital lease with Apple Inc. to purchase computers for $396,619 with a 2.47% interest rate. Semi-annual lease payments are $51,727.23 ending January 15, 2020. Details of the Capital Lease are as follows:

Capital Lease Issued Februa12 4, 2016

Year Ending Interest June 30, Rate Principal Interest Total

2018 2.47% $ 97,866 $ 5,588 $ I 03.454 2019 2.47% 99,863 3,592 I 03.455 2020 2.47% 101,900 1,554 I 03,454

$ 299,629 $ 10,734 $ 310,363

Revenue Bonds

Details of the District's June 30, 2017 StateHide Sales, Services and Use Tax Revenue indebtedness are as follows:

Issued July I, 2009 Year Ending Interest

June 30, Rates Principal Interest Total 2018 4.0% $ 100,000 $ 53,800 $ 153,800 2019 4.0% 100,000 49,800 149,800 2020 4.2% 100,000 45,800 145,800 2021 4.2% 100,000 41,600 141.600 2022 4.4% 100,000 37,400 137,400

2023-2027 4.4%-4.8% 500,000 119,600 619,600 2028-2029 4.9% 200,000 14,700 214,700

Total $ 1,200,000 $ 362,700 $ 1,562,700

The District has pledged future statewide sales, services and use tax revenues to repay the $1,675,000 of bonds issued in July 2009. The bonds were issued for the purpos, of financing a portion of the costs of the Niches Project. The bonds are payable solely from the proceeds of the statewide sal~s, services and use tax revenues received by the District and are payable through 2029. The bonds are not a general obligation of the District. However, the debt is subject to the constitutional debt limitation of the District. Annual principal and interest payments on the bonds are expected to require approximately 12% of the statewide sales, services and use tax revenues. The total principal and interest remaining to be paid on the bonds is $1,562,700. For the current year,$ 100,000 principal and $57,400 of interest was paid on the bonds and total statewide sales, services and use tax revenues were $644,86{.

Page 32

The resolution providing for the issuance of the statewide sales, services and use tax revenue bonds includes the following provisions:

a) $161,130 of the proceeds from the issuance of the revenue bonds shall be deposited to a reserve account to be used solely for the purpose of paying prncipal and interest on the bonds if insufficient money is available in the sinking account. The balance of the proceeds shall be deposited to the project account.

b) All proceeds from the statewide sal,s, services and use tax shall be placed in a revenue account.