Embed Size (px)

Citation preview

Mkt. Cap Price Cons. Current EPS Estimates Previous Est.Company Name Ticker (MM) Rating Price Target Next FY 2015 2016 2017 2016 2017 China Mobile Limited 941 HK $222,257.4 UNPF HK$84.20 HK$69.24 RMB5.29 RMB5.30 RMB5.45 RMB5.61 RMB5.45 RMB5.61China Telecom Corp Ltd. 728 HK $38,083.2 UNPF HK$3.65 HK$3.02 RMB0.25 RMB0.25 RMB0.25 RMB0.25 RMB0.25 RMB0.25China Unicom Ltd. 762 HK $27,816.1 UNPF HK$9.01 HK$7.26 RMB0.03 RMB0.44 RMB0.03 RMB(0.03) RMB0.03 RMB(0.03)

INDUSTRY NOTE

Assuming Coverage

China | Telecommunications | Telecom Services 21 November 2016

Telecom ServicesAssuming Coverage: Shareholder-unfriendlyPolicy Focus Drives Steep Downside

EQU

ITY R

ESEARC

H C

HIN

A

Source: OECD Digital Economy Outlook 2015,

company data, Jefferies

Source: Jefferies, company data

Source: IMF World Economic Outlook 2015,

www.dnaindia.com, company data, Jefferies

Source: Jefferies estimates

Edison Lee, CFA *Equity Analyst

+852 3743 8009 [email protected]

* Jefferies Hong Kong Limited

^Prior trading day's closing price unlessotherwise noted.

Key Takeaway

After multiple rounds of fund raising and restructuring, China's telecomindustry will likely be increasingly used as a tool to spur the growth of othersectors: supporting China's Internet+ and "Made in China 2025" initiatives.The government will likely continue pressing for lower prices, rapid coverageexpansion and ongoing technology and data speed upgrade. This will translateinto top line pressure and stubbornly high capex for all three telecomoperators.

With this report, Edison Lee assumes coverage of Jefferies’ telecoms coverage. We have anegative view on the sector driven by regulatory development.

Current industry structure seen as sustainable. After 20 years of partial privatization,multiple rounds of restructuring, fund raising and management reshuffles, we believe thegovernment sees the current industry structure as sustainable. In other words, the threeoperators are unlikely to get any asymmetric help or face any harm from the governmentin the near term.

Maximizing telecom profits no longer a priority. With no more equity fund raisingand restructuring required, the telecom policy focus in the next five years will likely be on1) lower prices, 2) rapid coverage expansion, and 3) continued data speed and technologyupgrade. This is to spur the growth of Internet services and encourage traditional industriesto utilize advanced IT technology.

Capex could remain stubbornly high. The three telecom operators’ capex to salesratios, which have stayed persistently high at 30% to 40%, are unlikely to fall substantiallywhile the telecoms revenue to GDP ratio will fall further (1.6%). Their top line growth willremain below GDP growth. The high capex explains why their EV/EBITDA multiples are low,and they may go even lower.

17% to 20% downside to the stock prices. Based on long-term capex to sales ratio of27% to 30%, our DCF-based TPs imply downside of 20%, 18% and 17% for China Unicom,China Mobile and China Telecom, respectively. Our 2017 earnings forecasts are also belowconsensus. Potential de-rating catalysts will be 1) weak EBITDA and profit growth in the nextfew quarters, 2) continued high capex guidance for 2017 (coming out in Mar/Apr 2017) and3) no dividend increase (for China Telecom and China Unicom) in the upcoming results. Inthe worst case, the market could revert to valuing these companies only on their dividends,and our DDM valuation is 32% to 61% below the current stock prices.

China Mobile - Its DCF is the least sensitive to capex because of its large cash pile. But itscontinued market dominance may invite more national services, and we see low likelihoodof a meaningful increase in dividend payout ratio.

China Telecom - Its DCF is the most sensitive to capex among the three operators. A rapidrise in capex in both fixed line and mobile, together with little EBITDA growth, will turn FCFnegative. Its ability to raise dividend is limited.

China Unicom - Its DCF is also very sensitive to capex because of its low operating margin.But its FCF will remain positive. Further margin pressure will likely force it to report a netloss in 2017.

Please see analyst certifications, important disclosure information, and information regarding the status of non-US analysts on pages 61 to 64 of this report.

Contents EXECUTIVE SUMMARY ................................................................................................................ 3 THE ART OF CHINESE REGULATION .............................................................................................. 9 FURTHER INDUSTRY CONSOLIDATION NOT IN SIGHT ................................................................. 12 WILL CAPEX EVER FALL? ............................................................................................................ 13 CONTINUED PRESSURE TO LOWER PRICES ................................................................................. 16 IS MOBILE DATA DEMAND IN CHINA PRICE ELASTIC? ................................................................. 18 LOW MORALE MAKES IMPROVEMENT EVEN HARDER ............................................................... 20 OUR VALUATION WORK SUGGESTS SIGNIFICANT DOWNSIDE .................................................... 21 CHINA MOBILE (941 HK) ............................................................................................................ 29

Entrenched market position as an incumbent ............................................................................ 29 A strong balance sheet allows rapid network build .................................................................... 29 Risk of asymmetric regulations is not all gone ............................................................................ 29 Dividend to exceed FCF; any big hike unlikely ............................................................................ 30 Valuation looks cheap but likely a value trap ............................................................................. 30

CHINA TELECOM (0728 HK) ........................................................................................................ 36 A large fixed line business has been a burden ............................................................................ 36 Margin will unlikely improve ...................................................................................................... 36 IDC, ICT and IPTV are bright spots, but not enough .................................................................... 36 FCF will be lower than forecast dividend payment ..................................................................... 37 DCF value highly sensitive to capex assumptions ....................................................................... 37

CHINA UNICOM (0762 HK) ......................................................................................................... 44 The new CEO could raise performance ....................................................................................... 44 Mobile is still a big challenge ...................................................................................................... 44 Fixed line is a smaller drag than at CT ......................................................................................... 44 Valuation unattractive on both DCF and multiples ..................................................................... 45 Excitement about PPP likely overdone ....................................................................................... 45

Telecommunications

Assuming Coverage

21 November 2016

page 2 of 64 , Equity Analyst, +852 3743 8009, [email protected] Lee, CFA

Please see important disclosure information on pages 61 - 64 of this report.

Executive Summary • With this report, Edison Lee assumes coverage of Jefferies’ telecom coverage. We have

a negative view on the sector driven by regulatory development.

• Chinese telcos’ profitability in the past 20 years has been heavily influenced by

government policies. Management has increased efficiency, streamlined operations and

improved governance. However, the magnitude of such an impact is small versus what

changes in regulations and policies have done.

• After 20 years of partial privatization, multiple rounds of restructuring, fund raising and

management reshuffle, we believe the government sees the current industry structure

sustainable. In other words, the three operators are unlikely to get any asymmetric help,

or face punishment, from the government in the near term.

• With no more equity fund raising and restructuring required, the telecom policy focus

in the next five years will likely be on 1) lower prices, 2) rapid coverage expansion, and 3)

continued data speed and technology upgrade. This is to support China’s Internet+ and

Made in China 2025 initiatives.

• In other words, Chinese telcos’ capex to sales ratio, which has been consistently high

(30% to 40%), will likely stay high longer term while the telecoms revenue to GDP ratio

will be low (1.6%). Their top line growth will remain below GDP growth. Owing to high

capex, their EV/EBITDA multiples are also justifiably low.

• We see many analysts’ high DCF valuations, driven by a fall in the long-term capex to

sales ratio to 20%-25% as very risky. We believe 27% to 30% is much more likely. Our TPs,

which are based on DCF estimates, imply downside of 20%, 18% and 17% for China

Unicom, China Mobile and China Telecom, respectively. Our 2017 earnings forecasts are

also below consensus. Potential de-rating catalysts will be 1) weak EBITDA and profit

growth in the next few quarters, 2) continued high capex guidance for 2017 (coming out

in Mar/Apr 2017) and 3) no dividend increase (for China Telecom and China Unicom) in

the upcoming results. The single biggest risk to our call is a massive cut in capex for these

operators in their 2017 guidance.

A more extreme, negative scenario is that the market may start valuing these stocks just

on the basis of the dividends, since investors may start feeling that minority shareholders

have no control over the use of these telcos’ FCF, and these SOEs are not for sale. That

could make DCF valuation less relevant for financial investors. On a DDM basis, our

valuation is 34% to 60% lower than the current stock prices.

Chart 1: Valuation Comparison

Source: Jefferies estimates, company data

Current 2016E Net

Stock Ticker stock px JEF rating JEF PT Mcap (US$m) 16E 17E 16E 17E 16E 17E 16E 17E 16E 17E 16E 17E Revenue EBITDA EPS debt to equity

China Mobile 941.HK 84.6 Upf 69.24 223,513 13.6 13.2 4.3 4.0 1.5 1.5 11.7% 11.4% 2.0 2.0 17.0% 16.9% 3.3% 2.3% -5.8% -43%

China Telecom 728.HK 3.65 Upf 3.02 38,117 13.0 12.6 3.5 3.3 0.8 0.8 6.4% 6.3% 0.9 0.8 5.8% 5.6% 2.5% 3.1% -1.0% 27%

China Unicom 762.HK 9.07 Upf 7.26 28,026 248.3 -266.4 4.1 4.2 0.8 0.9 0.3% -0.3% 1.1 1.1 1.1% 0.4% 2.3% 2.8% 9.9% 62%

P/B ROAE EV/IC ROIC CAGR 16E-19EPE EV/EBITDA

Government policies determine

telecom operators’ profitability in

China

Expect no more industry

restructuring

Regulatory focus is likely on lower

prices, wider network coverage and

ongoing tech and speed upgrade

Capex to sales will remain high;

telecom revenue to GDP will fall

Our LT capex to sales assumptions

are 27%-30%. Our DCF-based TPs

imply 17%-20% downside to stock

prices.

If capex remains high and dividends

do not grow, the worst case is to

revert to a DDM valuation.

Telecommunications

Assuming Coverage

21 November 2016

page 3 of 64 , Equity Analyst, +852 3743 8009, [email protected] Lee, CFA

Please see important disclosure information on pages 61 - 64 of this report.

Chart 2: China Mobile’s Valuation Summary

Source: Jefferies estimates, company data

Chart 3: China Mobile’s DCF Valuation

Source: Jefferies estimates, company data

Chart 4: China Telecom’s Valuation Summary

Source: Jefferies estimates, company data

Chart 5: China Telecom’s DCF Valuation

Source: Jefferies estimates, company data

Chart 6: China Unicom’s Valuation Summary

Source: Jefferies estimates, company data

Chart 7: China Unicom’s DCF Valuation

Source: Jefferies estimates, company data

Dec 31, Rmb m 2014A 2015A 2016E 2017E 2018E 2019E

Revenue 651,509 668,335 719,450 769,215 769,486 793,690

EBITDA 240,237 240,028 257,485 273,467 283,309 275,286

vs concensus 0.7% 0.5%

Net profit 109,218 108,539 111,521 114,799 111,832 93,078

Basic EPS (Rmb) 5.38 5.30 5.45 5.61 5.46 4.55

vs concensus 3.0% -2.3%

EPS growth -7.4% -1.5% 2.7% 2.9% -2.6% -16.8%

PE 13.8 14.0 13.6 13.2 13.6 16.3

EV/EBITDA 4.6 4.6 4.3 4.0 3.9 4.0

ROAE 13.0% 12.0% 11.7% 11.4% 10.4% 8.3%

ROIC 21.3% 15.7% 17.0% 16.9% 15.4% 11.3%

Dividend yield 3.1% 3.0% 3.42% 3.42% 3.42% 3.42%

P/B 1.7 1.6 1.5 1.5 1.4 1.3

EV/IC 2.6 2.2 2.0 2.0 1.9 1.8

FCF yield to market cap 2.8% 4.1% 3.9% 3.0% 2.2% 3.6%

WACC and Terminal Value Calculation

Risk free rate 1.40% Terminal growth rate 3.2%

Equity risk premium 7.80% Terminal FCF x 21.8

Beta 0.82 Terminal value 805,720

CoE 7.8% Terminal EV/EBITDA 3.0

Cost of debt NA

After-tax cost of debt NA

WACC 7.8%

DCF Valuation (Rmb m) 2016E 2017E 2018E 2019E 2020E

EBITDA 257,485 273,467 283,309 275,286 269,524

Change in working capital 23,035 4,283 (4,314) 20,113 (736)

Operating profit x tax rate (29,079) (29,670) (28,373) (22,331) (17,406)

Capex (186,000) (196,332) (209,574) (211,907) (215,499)

Unleveraged FCF 65,441 51,749 41,048 61,161 35,883

Unleveraged FCF + terminal value 65,441 51,749 41,048 61,161 841,603

Discount period 0 1 2 3 4

Discount factor 1.00 0.93 0.86 0.80 0.74

PV of unleveraged FCF 65,441 48,006 35,325 48,827 623,299

Enterprise value (Rmb m) 820,899

Less: net debt (end of 2016) (420,672)

Equity value (Rmb m) 1,241,572

Equity value per share (Rmb) 60.6

Equity value per share (HK$) 69.24

Dec 31, Rmb m 2014A 2015A 2016E 2017E 2018E 2019E

Revenue 324,394 331,202 358,486 373,456 383,507 386,073

EBITDA 94,853 94,106 98,134 102,804 106,706 107,400

vs consensus 1.6% 0.8%

Net profit 17,680 20,054 19,856 20,525 20,576 19,284

Basic EPS (Rmb) 0.22 0.25 0.25 0.25 0.25 0.24

vs consensus 2.2% -6.1%

EPS growth 0.8% 13.4% -1.0% 3.4% 0.2% -6.3%

PE 14.6 12.9 13.0 12.6 12.6 13.4

EV/EBITDA 3.6 3.6 3.5 3.3 3.2 3.2

ROAE 6.2% 6.7% 6.4% 6.3% 6.1% 5.5%

ROIC 5.8% 5.2% 5.8% 5.6% 5.3% 4.8%

Dividend yield 2.4% 2.4% 2.8% 2.8% 2.8% 2.8%

P/B 0.89 0.85 0.81 0.78 0.75 0.73

EV/IC 0.92 0.90 0.86 0.82 0.78 0.75

FCF yield to market cap 6.2% 2.6% 1.9% -0.9% -0.7% 1.6%

WACC and Terminal Value Calculation

Risk free rate 1.40% WACC 8.0%

Equity risk premium 7.80% Terminal growth rate 6.1%

Beta 1.05 Terminal FCF x 52.2

CoE 9.6% Implied terminal EV/EBITDA x 3.5

Cost of debt 4.0% Terminal value (Rmb m) 375,805

After-tax cost of debt 3.0%

WACC 8.0%

Rmb m 2016E 2017E 2018E 2019E 2020E

EBITDA 98,134 102,804 106,706 107,400 106,781

Change in working capital 14,260 1,187 (1,685) 1,068 1,207

Operating profit x tax rate (7,408) (7,452) (7,444) (7,080) (6,545)

Capex (97,000) (95,500) (95,632) (93,174) (94,246)

Unleveraged FCF 7,986 1,039 1,944 8,214 7,197

Unleveraged FCF + terminal value 7,986 1,039 1,944 8,214 383,002

Discount period 0 1 2 3 4

Discount factor 1.00 0.93 0.86 0.79 0.73

PV of unleveraged FCF 7,986 962 1,666 6,518 281,360

Enterprise value (Rmb m) 298,492

Less: net debt (end of 2016) 84,535

Equity value (Rmb m) 213,957

Equity value per share (Rmb) 2.64

Equity value per share (HK$) 3.02

Dec 31, Rmb m 2014A 2015A 2016E 2017E 2018E 2019E

Revenue 284,681 277,049 278,759 283,391 289,133 298,163

EBITDA 92,771 87,502 81,593 79,736 87,685 88,701

vs consensus -1.8% -10.9%

Net profit 12,055 10,562 766 (714) 2,781 1,016

Basic EPS (Rmb) 0.51 0.44 0.03 (0.03) 0.12 0.04

vs consensus -76% -110%

EPS growth 15.9% -13.7% -92.7% -193.2% -489.5% -63.5%

PE 15.6 18.1 248.3 (266.4) 68.4 187.2

EV/EBITDA 3.6 3.8 4.1 4.2 3.8 3.7

ROAE 5.4% 4.6% 0.3% -0.3% 1.3% 0.5%

ROIC 5.2% 2.9% 1.1% 0.4% 1.5% 0.7%

Dividend yield 2.5% 2.1% 2.5% 2.5% 2.5% 2.5%

P/B 0.84 0.82 0.84 0.86 0.86 0.88

EV/IC 1.2 1.2 1.1 1.1 1.2 1.3

FCF yield to market cap 9.7% -2.2% -5.9% 4.3% 8.3% 7.7%

WACC and Terminal Valuation Calculation

Risk free rate 1.40% WACC 5.1%

Equity risk premium 7.80% Terminal growth rate 2%

Beta 0.89 Terminal FCF x 31.8

CoE 8.3% Implied terminal EV/EBITDA x 3.5

Cost of debt 3.4% Terminal value (Rmb m) 305,043

After-tax cost of debt 2.6%

WACC 5.1%

Rmb m 2016E 2017E 2018E 2019E 2020E

EBITDA 81,593 79,736 87,685 88,701 88,141

Change in working capital (13,181) 6,306 8,951 6,899 (503)

Operating profit x tax rate (1,038) (355) (1,341) (618) 138

Capex (75,000) (73,920) (76,247) (77,289) (78,377)

Unleveraged FCF (7,625) 11,768 19,047 17,693 9,399

Unleveraged FCF + terminal value (7,625) 11,768 19,047 17,693 314,442

Discount period 0 1 2 3 4

Discount factor 1.00 0.95 0.90 0.86 0.82

PV of unleveraged FCF (7,625) 11,193 17,229 15,221 257,290

Enterprise value (Rmb m) 293,309

Less: net debt (end of 2016) 141,003

Equity value (Rmb m) 152,306

Equity value per share (Rmb) 6.4

Equity value per share (HK$) 7.26

Telecommunications

Assuming Coverage

21 November 2016

page 4 of 64 , Equity Analyst, +852 3743 8009, [email protected] Lee, CFA

Please see important disclosure information on pages 61 - 64 of this report.

Chart 8: China Mobile’s DCF Valuation Sensitivity to Capex to Sales Ratio

Source: Jefferies estimates, company data

Chart 9: China Telecom’s DCF Valuation Sensitivity to Capex to Sales Ratio

Source: Jefferies estimates, company data

Chart 10: China Unicom’s DCF Valuation Sensitivity to Capex to Sales Ratio

Source: Jefferies estimates, company data

Telecommunications

Assuming Coverage

21 November 2016

page 5 of 64 , Equity Analyst, +852 3743 8009, [email protected] Lee, CFA

Please see important disclosure information on pages 61 - 64 of this report.

China Mobile (941 HK)

The least risky of the three Key Takeaway

CM's strong incumbent advantages and net cash position of Rmb420bn makes

it the least risky stock to own among the three, in our view. Its mobile market

share has stabilized at around 67% since 2014. The convergence of TDD and

FDD in 4G has helped CM retain high-end subscribers. Its DCF value is the least

sensitive to any further capex rise (or fall).

4G helped CM maintain its incumbent advantages. CM's incumbent advantages

were weakened substantially when it was required to offer 3G services using the China-

developed TD-SCDMA standard. Those handsets cannot be used outside China, nor on

Unicom's or CT's networks. However, since TDD and FDD can converge in 4G, a large

number of multi-mode and multi-band handsets came out, which helped CM regain its

competitive edge, and stabilized revenue market share.

A strong balance sheet helped rapid network build. Its Rmb420bn cash on hand

has allowed CM to rapidly build its 4G coverage after it was awarded a license in

December 2013. By the end of 2015, it had 1.2m 4G base stations, versus 520K at CT and

400K at Unicom. That has enabled CM to achieve 312m 4G users (38% of its user base),

much higher than CT's 58.5m (30%) and Unicom's 44m (18%). Its advantage will likely

be repeated when 5G services are rolled out.

Meaningful dividend hike unlikely, to prepare for future investments. Despite

its massive net cash position, we do not believe management is motivated to

meaningfully hike its dividend payout ratio. Since it is hard to further reduce CM's market

dominance by industry restructuring, the government's likely solution is to keep asking

CM to perform national services, such as faster expansion, coverage in remote areas and

constant technology upgrade. Therefore, management, either at its own discretion or

under the government's influence, would like to keep as much cash as possible.

Valuation/Risks

CM is currently trading at 4.3x EV/EBITDA and 13.6x PE (or 10x excluding cash) for 2016.

While its earnings multiples look cheap, they would not fall as we forecast little growth in

EBITDA and profit. Its P/B of 1.5x and EV/IC of 2.0x is not particularly cheap either, against

1.5x ROAE/CoE and 2.2x ROIC/WACC. Our DCF value of HK$69.24 is based on a WACC of

7.8%, a terminal growth rate of 3.2% and a long-term capex to sales ratio of 30%.

Upside risks. The willingness of management to significantly increase dividend payout

for 2016 (even a one-time special dividend will be considered a disappointment) and a

large cut in capex guidance for 2017.

Downside risks. No capex cut and dividend increase in the upcoming 2016 result

announcement. Mobile data demand shows falling elasticity as prices continue to fall.

RMB Prev. 2015A Prev. 2016E Prev. 2017E Prev. 2018E

Rev. (MM) -- 668,335.0 -- 719,450.0 -- 769,215.0 -- 769,486.0

EBITDA (MM) -- 239,754.0 240,614.0 257,485.0 258,913.0 273,467.0 276,282.0 283,309.0

EV/EBITDA 4.6x 4.3x 4.1x 3.9x

Net Profit -- 108,539.0 -- 111,521.0 -- 114,799.0 -- 111,832.0

P/B -- 1.6x 1.9x 1.5x 1.8x 1.5x 1.7x 1.4x

ROE -- 12.0% -- 11.7% -- 11.4% -- 10.4%

ROIC -- 15.7% -- 17.0% -- 16.9% -- 15.4%

Div Yield -- 3.00% 2.20% 3.42% 2.50% 3.42% 2.80% 3.42%

Cons. EPS -- -- 5.34 5.29 5.85 5.74 6.49 6.23

EPS

FY Dec -- 5.30 4.78 5.45 5.35 5.61 5.89 5.46

FY P/E 14.2x 13.8x 13.4x 13.8x

U N D E R P E R F O R M

( f r o m B U Y )

P r ic e ta r g e t H K $ 6 9 .2 4

( f r o m H K $ 1 0 6 .8 0 )

P r ic e H K $ 8 4 .7 5

B lo o m b e r g : 9 4 1 H K

R e u te r s : 0 9 4 1 .H K

F in a n c ia l S u m m a r y

B o o k V a lu e ( M M ) : R m b 9 6 0 ,0 0 6 .0

B o o k V a lu e /S h a r e : R m b 4 6 .9 0

N e t D e b t ( M M ) : ( R m b 4 2 6 ,7 8 2 )

C a s h & S T In v e s t. ( M M ) : R m b 4 3 3 ,1 5 9 .0

M a r k e t D a t a

5 2 W e e k R a n g e : H K $ 9 9 .3 0 - H K $ 7 9 .0 0

T o ta l E n tp r s .V a lu e ( M M ) $ 1 6 1 .7 2 7 .2

M a r k e t C a p . ( M M ) : $ 2 2 3 ,6 8 7 .4

S h a r e s O u t. ( M M ) : 2 0 ,4 7 3 .0

F lo a t ( M M ) : 5 ,5 8 4 .1

A v g . D a ily V o l. : 1 4 ,0 0 7 ,6 3 0 .0

Price Performance

Source: Bloomberg

70

75

80

85

90

95

100

105

110

Nov-15 Feb-16 May-16 Aug-16

Telecommunications

Assuming Coverage

21 November 2016

page 6 of 64 , Equity Analyst, +852 3743 8009, [email protected] Lee, CFA

Please see important disclosure information on pages 61 - 64 of this report.

China Telecom (728 HK)

Most vulnerable to high capex Key Takeaway

CT became an integrated operator in 2008 by buying the CDMA business from

Unicom. It was awarded an FDD-LTE 4G license in 2015. Its capex has doubled

to Rmb105bn last year from 2012, driven by broadband expansion, 3G and

then 4G network build. Falling operating cash flow and still high capex will

cause FCF to turn negative. Our DCF valuation implies 17% downside, and it is

the most sensitive to capex assumptions among the three.

A large fixed line business is a burden. Being the incumbent fixed line operator in 21

southern provinces, revenue of fixed line voice accounted for as much as 30% of its

service revenue in 2010. Owing to mobile substitution, its revenue of fixed line voice has

fallen by Rmb32bn from 2010 to 2015, but fortunately it has been offset by growth in

broadband, IDC, ICT and leased line to produce overall flat growth in fixed line revenue.

In other words, all top-line growth has come from the mobile business.

Margin will unlikely improve. Since 2012, CT's mobile subscriber market share has

risen from 14.9% to 15.9%, but its revenue market share has impressively gone up from

11.8% to 15.1%, thanks to effective fixed-mobile bundling and rapid rollout of 3G and 4G

services. However, its revenue market share in mobile is still 80 bps below its subscriber

market share. That is due to CM's strong incumbent advantages. We do not forecast this

situation will change. Given CT has a large fixed line business, its EBITDA margin is the

lowest among the three operators. We forecast its EBITDA will remain the lowest and

continue to be under pressure.

Financially constrained to raise dividends. For 2015, CT generated enough FCF to

pay dividends. Its FCF in 2016 is forecast to fall by Rmb2.0bn, and it will be less than even

the 2015 dividend payment. Since we have factored in a 15% increase in DPS for all three

companies, its FCF in 2017 will fall short of projected dividend payment by Rmb2.3bn.

Moreover, CT will need to pay its parent Rmb61bn in 2017 as the last instalment for its

purchase of the CDMA network in 2012. Although that could be deferred, we see a real

risk of a dividend cut in 2018 and 2019.

Valuation/Risks

CT is trading at 13.0x PE and 3.5x EV/EBITDA for 2016, but against little growth in EBITDA

and net profit according to our forecasts. Its P/B of 0.81x and EV/IC of 0.86x are

unattractive against its ROAE/CoE ratio of 0.67x and ROIC/WACC ratio of 0.73,

respectively. Our DCF value of HK$3.02 per share is based on a WACC of 8%, a terminal

growth rate of 6% (translating into 3.5x EV/EBITDA) and a long-term capex to sales ratio

of 27%. Every one percentage point change in capex to sales will move the DCF value by

roughly HK$1.90 per share.

Upside risks. 1) a large capex cut in 2017, 2) a large dividend increase., 3) China Tower

Corp. is able to do an IPO at a very high valuation, and 4) a government-engineered

merger with Unicom

Downside risks. 2) little reduction in its 2017 capex guidance, 2) no dividend increase,

3) mobile data demand shows falling elasticity as prices continue to fall.

RMB Prev. 2015A Prev. 2016E Prev. 2017E Prev. 2018E

Rev. (MM) -- 331,202.0 -- 358,486.0 -- 373,456.0 -- 383,507.0

EBITDA (MM) -- 94,106.0 94,035.0 98,134.0 97,581.0 102,804.0 103,489.0 106,706.0

EV/EBITDA 3.6x 3.4x 3.3x 3.2x

Net Profit -- 20,054.0 -- 19,856.0 -- 20,525.0 -- 20,576.0

P/B -- 0.9x -- 0.8x -- 0.8x 0.7x 0.8x

ROE -- 6.7% -- 6.4% -- 6.3% -- 6.1%

EPS

FY Dec -- 0.25 0.24 0.25 0.24 0.25 0.27 0.25

FY P/E 13.0x 13.0x 13.0x 13.0x

U N D E R P E R F O R M

( f r o m B U Y )

P r ic e ta r g e t H K $ 3 .0 2

( f r o m H K $ 4 .4 0 )

P r ic e H K $ 3 .6 5

B lo o m b e r g : 7 2 8 H K

R e u te r s : 0 7 2 8 .H K

F in a n c ia l S u m m a r y

B o o k V a lu e ( M M ) : R m b 3 0 9 ,8 0 0 .0

B o o k V a lu e /S h a r e : R m b 3 .8 3

N e t D e b t ( M M ) : R m b 7 5 ,9 5 9

R e tu r n o n A v g . E q u ity : 5 .6 %

C a s h & S T In v e s t. ( M M ) : R m b 3 0 ,0 7 6 .0

M a r k e t D a t a

5 2 W e e k R a n g e : H K $ 4 .3 4 - H K $ 3 .2 8

T o ta l E n tp r s .V a lu e ( M M ) $ 4 9 ,1 1 0 .9

M a r k e t C a p . ( M M ) : $ 3 8 ,0 8 3 .2

S h a r e s O u t. ( M M ) : 8 0 ,9 3 2 .0

F lo a t ( M M ) : 1 3 ,8 7 7 .4

A v g . D a ily V o l. : 5 4 ,9 1 6 ,9 7 0 .0

Price Performance

Source: Bloomberg

3

3.2

3.4

3.6

3.8

4

4.2

4.4

Nov-15 Feb-16 May-16 Aug-16

Telecommunications

Assuming Coverage

21 November 2016

page 7 of 64 , Equity Analyst, +852 3743 8009, [email protected] Lee, CFA

Please see important disclosure information on pages 61 - 64 of this report.

China Unicom (762 HK)

A turnaround constrained by government policies Key Takeaway

Unicom's mobile business has faced tough challenges from both CM and CT.

CT has effectively bundled fixed line broadband with its mobile to take share

in higher-ARPU users in the 21 southern provinces. But Unicom's much

smaller fixed line business also created a smaller drag on return. We forecast

its FCF will exceed dividend payment, but its high gearing still makes

dividend increase unlikely. Recent excitement about a potential strategic

investor is overdone.

The new CEO could raise performance. In 2015, CT's CEO (Chairman Wang)

became Unicom's CEO under another government-directed reshuffle. Chairman Wang

has an excellent track record at both CT and CM. His rich experience allowed him to

quickly implement improvement initiatives at Unicom. However, many structural issues

and deep-rooted practices of Unicom cannot be changed just because of a new CEO.

After reporting good 1H16 results, its 3Q16 results were disappointing. The current lack

of financial incentives in the industry will also make significant improvements harder to

achieve.

Mobile is still a big challenge. Unicom's weak market position in mobile was driven

by its dual-network status and capital constraint at the start. Even though it sold its CDMA

business in 2008 and focused on the GSM-based network, the network quality and

coverage gap with CM will takes years to narrow. After Chairman Wang joined, he

accelerated the 4G rollout. However, Unicom's revenue market share in mobile in fact fell

from 17.4% in 2015 to 16.4% in 1H16. The mobile business remains an uphill battle for

Unicom.

Excitement about PPP likely overdone. Since Unicom was included by the NDRC in

the Public-Private-Partnership (PPP) pilot project, there has been rampant speculation that

one of the large Chinese Internet companies may take a stake in Unicom. We see limited

synergies in such a deal, and expect significant challenges in how the private investor can

influence Unicom's operations. Bear in mind Telefonica has yet to sell its remaining 1.5%

stake in Unicom (started at 9.6%), partly because there has been little tangible benefit

after seven years.

Valuation/Risks

Our DCF valuation of HK$7.26 per share is based on a WACC of 5.1%, a terminal growth

rate of 2% (3.5x EV/EBITDA) and a long-term capex to sales ratio of 30%. It is expensive

trading at 0.84x P/B against only 0.04x ROAE/CoE, and 1.1x EV/IC against.

Upside risks. 1) A large cut in its capex guidance for 2017, 2) a government-engineered

merger with CT, and 3) if a Chinese Internet company takes a strategic stake in Unicom at

a premium to the current stock price, Unicom’s stock price can rise in the short term.

Downside risks. 1) little reduction in its 2017 capex guidance, 2) no dividend increase

for 2016, 3) mobile data demand shows falling elasticity as prices continue to fall, 4) no

news in strategic investors nor merger with CT.

RMB Prev. 2015A Prev. 2016E Prev. 2017E Prev. 2018E

Rev. (MM) -- 277,049.0 -- 278,759.0 -- 283,391.0 -- 289,133.0

EBITDA (MM) -- 87,502.0 74,610.0 81,593.0 84,784.0 79,736.0 92,594.0 87,685.0

EV/EBITDA 3.7x 4.0x 4.1x 3.7x

Net Profit -- 10,562.0 -- 766.0 -- (714.0) -- 2,781.0

P/B 0.8x 0.8x 0.9x 0.9x

ROE -- 4.6% 1.0% 0.3% 3.2% -0.3% 4.8% 1.3%

ROIC -- 2.9% -- 1.1% -- 0.4% -- 1.5%

EPS

FY Dec -- 0.44 0.10 0.03 0.32 -0.03 0.49 0.12

FY P/E 18.3x NM NM 68.4x

U N D E R P E R F O R M

( f r o m H O L D )

P r ic e ta r g e t H K $ 7 .2 6

( f r o m H K $ 9 .0 0 )

P r ic e H K $ 9 .0 7

B lo o m b e r g : 7 6 2 H K

R e u te r s : 0 7 6 2 .H K

F in a n c ia l S u m m a r y

B o o k V a lu e ( M M ) : R m b 2 2 7 ,9 7 6 .0

B o o k V a lu e /S h a r e : R m b 9 .5 2

N e t D e b t ( M M ) : R m b 1 3 1 ,3 7 5

R e tu r n o n A v g . E q u ity : 4 .6 %

L o n g -T e r m D e b t ( M M ) : R m b 4 0 ,2 6 0 .0

C a s h & S T In v e s t. ( M M ) : R m b 2 1 ,2 1 4 .0

M a r k e t D a t a

5 2 W e e k R a n g e : H K $ 1 0 .2 6 - H K $ 7 .7 0

T o ta l E n tp r s .V a lu e ( M M ) $ 4 7 ,0 7 4 .4

M a r k e t C a p . ( M M ) : $ 2 8 ,0 0 1 .3

S h a r e s O u t. ( M M ) : 2 3 ,9 4 7 .0

F lo a t ( M M ) : 5 ,9 0 8 .6

A v g . D a ily V o l. : 5 3 ,6 9 8 ,7 8 0 .0

Price Performance

Source: Bloomberg

7

7.5

8

8.5

9

9.5

10

10.5

Nov-15 Feb-16 May-16 Aug-16

Telecommunications

Assuming Coverage

21 November 2016

page 8 of 64 , Equity Analyst, +852 3743 8009, [email protected] Lee, CFA

Please see important disclosure information on pages 61 - 64 of this report.

The Art of Chinese Regulation The regulatory environment mis-perceived to be stable

The stocks of China Mobile, China Telecom and China Unicom have been widely followed

by institutional investors and sell-side analysts. The consensus view seems to be generally

positive because valuation is “cheap” and the regulatory environment is “stable.” To

come up with a proper long-term view on these three stocks, we believe it is key to

examine the history of regulatory development in China, which will provide a sound basis

to predict where policy focus will be moving toward`. Historically, government policies

have had a significant influence on the operators’ profitability. Therefore, this exercise

could be more critical than analysis of revenue and cost on a quarterly basis.

Telecom has always been a regulated industry anywhere in the world, because spectrum

is a public resource and telephony services are considered a basic necessity. Government

policies do affect telecom operators’ profitability because they drive, for example, the

number of licenses (players) in the market, technology standards (neutral in most

markets), and how to create a level playing field for new entrants. In most countries, the

telecom regulator is pro-competition and pro-consumers.

The situation in China is, however, special because while China would like to create some

competition in the telecom industry, it has been more pre-occupied with its desire to

maintain absolute control over it, since it is a highly strategic industry and key to national

security. Therefore, telecom policies in China have always been a struggle to balance

investment needs, consumer benefits, operators’ profitability and other national priorities

from time to time (eg, the telecom equipment industry). At different times in the past, the

government has tended to stress one or two aspects over the others. To complicate

matters, various factions with vested interests tend to pressure the government or

telecom regulator to shift its policies in their favor.

In order for the government to maintain control over the industry, all three operators

(there were four at one time) continue to be majority state-owned, even though they are

publicly listed. That has several consequences: 1) the management are effectively civil

servants, who will do their best in maximizing efficiency but only within the overall

constraints imposed by the government, 2) these operators will have to accommodate

government objectives even if some objectives may not be the best commercial decisions,

and 3) the government may be interested in boosting their profitability, only if no other

more important priorities are present that conflict with that.

Need to look at regulatory history to

assess future direction

The regulator in China is far more

than just being pro-consumers

The government retains absolute

control over this strategic industry;

regulations aim to achieve a range of

objectives

All 3 operators are majority state-

owned; management always

accommodate government priorities

Telecommunications

Assuming Coverage

21 November 2016

page 9 of 64 , Equity Analyst, +852 3743 8009, [email protected] Lee, CFA

Please see important disclosure information on pages 61 - 64 of this report.

Chart 11: A Summary of China’s Telecom Regulatory Development since the

First Privatization

Source: Jefferies, company data

Month Year Major regulatory and corporate events Our interpretation of the government's policy focus

<1993

Telecom services were monopolized by China Telecom Group,

which belonged to the Ministry of Post and Telecoms

Jun 1994

State Council approved the creation of Unicom to provide

competition in the telecoms industry. Later China Jitong and China

Netcom were given licenses to operate data and Internet services.

China Railcom was allowed to provide all telecoms services other

than cellular.

1995

Unicom started using the structure of China-China-Foreign

ventures to build GSM networks in different cities and a

nationwide data and long distance network.

1997

China Telecom (Hong Kong) Ltd. (which has become the China

Mobile today) was established and raised US$4.2bn in an IPO. It

owned the parent's mobile operatios in two provinces (ie,

Guangdong and Zhejiang)

1998 State Council allowed Unicom to offer nationwide cellular services.

Feb 1999

Cellular services were split off from China Telecom Group. China

Mobile Communications Corp. was created to own all cellular

businesses previously owned by China Telecom Corp. China

Telecom Corp became a nationwide fixed line operator.

1999

MII approved the transfer of China Telecom's paging business to

Unicom. Unicom was authorized by the State Council to build a

nationwide CDMA network.

June 2000

China Uniom raised US$5.65bn in an IPO. Its parent started

building the CDMA network and leased capacity to the listco.

China Telecom (Hong Kong) Ltd. Changed its name to China

Mobile (Hong Kong) Ltd.

Dec 2001

China joined WTO. State Council promulgated Administrative

Regulations on Telecommunications Companies with Foreign

Investment to gradually reduce barriers for foreign investors to

enter China's telecoms industry.

May 2002

China Telecom, which operated China's nationwide fixed line

network, was split into north and south. China Netcom was formed

to take over northern operations of China Telecoms (10 provinces

in the northern part of China)

Nov 2002

China Telecom raised US$1.7bn in an IPO, initially with fixed line

operations in Shanghai, Guangdong, Jiangsu and Zhejiang.

Nov 2004

Management re-shuffle: CEO of China Mobile became CEO of

China Telecom, China Telecom's CEO became CEO of Unicom, and

Unicom's CEO became China Mobile's CEO

Nov 2004 China Netcom raised US$1.15bn in an IPO

Mar 2008

The MII was restructured to become the Ministry of Industry and

Information Technology (MIIT). The MIIT is responsible for

overseeing telecoms, Internet, broadcasting, telecoms equipment,

electronics and software industries.

Oct 2008

Unicom sold its CDMA biz to CT, and merged with China Netcom.

The merged company stays with the name China Unicom.

Dec 2008

The State Council gave go-ahead to the MIIT starting the process

of preparing for the issue of 3G license with a special objective to

support the TD-SCDMA standard.

Jan 2009

Unicom awarded a 3G license based on WCDMA technology; CT

awarded a 3G license based on CDMA2000 technology; China

Mobile was awarded a 3G license based on TD-SCDMA. China

Mobile's parent took on the job to build the TD-SCDMA network

and lease capacity to the listco.

Dec 2013

CM, CT and Unicom each awarded a 4G license based on TD-LTE

technology. CM immediately started building out the 4G network

at the listco level.

Jan 2014

MIIT lowered mobile interconnection rate CT/Unicom pay to CM to

Rmb0.06/min to 0.04/min; while that for CM to CT/Unicom traffic

remains at Rmb0.06/min

July 2014

All 3 operators entered into an agreement to set up China Tower

Corporation by contributing the majority of their existing towers to

that company.

Feb 2015

CT and Unicom each awarded a 4G license based on FDD-LTE

technology

May 2015

CT and Unicom started offering mobile users to roll over their

unused mobile data to the following month, under government

pressure to lower Internet prices.

Jun 2015

The three operators started phasing out domestic roaming and

national long distance charges (by introducing one-rate packages).

Aug 2015

Management re-shuffle: Shang Bing, Vice Minister of the MIIT,

became Chairman of China Mobile; CEO of China Telecom became

Unicom's CEO, Unicom's CEO (Chang Xiao Bing) became China

Telecom's CEO (but Chang was arrested a few months later for

corruption and China Telecom's President & COO was made CEO)

Oct 2015

China Mobile started offering mobile users to roll over their unused

mobile data to the following month.

Nov 2015

China Tower Corp. was officially established, which will centralize

telecoms tower maintenance and capex in the future. The

shareholding of CM, CT and Unicom in China Tower is 38%, 27.9%

and 28.1%, respectively.

Nov 2015 China Mobile acquired China Tie Tong (China Railcom)

2016-2020

Forecast

Expect no change to industry structure. Prepare for

commercialization of mobile 5G technology by 2020. Introduce

Private-Public Partnership at the parent of Unicom and CT to help

these two weaker players with funding and management

resources.

Support government's Internet+ and Made in

China 2025 strategic goals by encouraging A) faster

coverage expansion, B) continued drop in tariffs,

and C) ongoing technology upgrade.

1) Continued efforts to eliminate corruption and

promote rational competition at the three telcos, 2)

Premier Li Keqiang called for more affordable and

widely available Internet access, and a more

advanced digital system

Prepared for China's first privatization of major state-

owned industries. A key pilot project for China.

State Council and Ministry of Post and Telecoms

probably disagreed on how much competition

should be allowed ahead of this major act.

Ministry of Information Industry (Ministry of Post

and Telecoms prior to 1998) focused on creating an

attractive equity story for China Mobile to raise

equity and acquire remaining assets from its parent.

Rapid network expansion to accommodate rising

demand for mobile services, and to pre-empt

possible entry of foreign competition. State Council

probably more supportive of Unicom.

1) Restructured China Telecom to give China

Netcom a piece of the pie, and prepared them for

IPOs, 2) Commercialized China-developed TD-

SCDMA as one of the three global 3G standards,

and 3) Eliminated corruption and promoted more

rational competition at the three telcos.

1) Promoted TD-SCDMA 3G standard - China

Mobile had pulled away from Unicom so much that

it was asked to do the national service. 2) Created a

more sustainable industry structure by restructuring

CT and Unicom into two integrated operators.

1) Promoted buildout of 4G, 2) less biased toward

TD since TD-LTE and FDD-LTE can converge, 3) a

more balanced industry structure means no more

restructuring, but with ongoing tweaks of policies

to give some help to CT and Unicom (eg,

establishment of the Tower Co).

This table may be too hard to read,

but it outlines how the government

has engineered the industry’s

transformation since its first

privatization in 1997

Telecommunications

Assuming Coverage

21 November 2016

page 10 of 64 , Equity Analyst, +852 3743 8009, [email protected] Lee, CFA

Please see important disclosure information on pages 61 - 64 of this report.

Chart 1 outlines the historical development of regulatory changes and industry

restructuring in China’s telecoms industry since 1997, when the first privatization took

place. Our observations and conclusions are as follows:

1. Between 1995 and 2002 – Privatization and fund raising was the

focus. The government had focused on creating an attractive equity story for

the telcos so that they could raise money in the equity markets. The IPOs

achieved a few objectives for China: A) modernize management and improve

governance/efficiency, B) raise funds to rapidly roll out networks and improve

services (this was part of China’s modernization programs and they also helped

pre-empt competition from foreign entrants after China’s WTO entry), and C)

serve as a successful pilot program for China to privatize SOEs in other key

sectors in a similar fashion.

2. Between 2002 and 2008 – The Ministry of Information Industry (MII)

started acting more like an independent regulator, as the financial

ownership of the Chinese telcos had been transferred to the Ministry of Finance.

The regulatory focus was mainly on A) creating a more balanced and thus

sustainable industry structure, and B) developing 3G plans for China, with a

particular bias toward supporting the China-developed TD-SCDMA 3G standard.

On the other hand, with value-added and 2.5G services having taken off for

cellular operators both globally and in China, China Mobile had pulled away

from Unicom and the two fixed line operators. The result was that the

government decided to A) ask China Mobile to build a nationwide 3G network

based on TD-SCDMA to support the local equipment industry, and B)

restructure China Telecom, China Netcom and Unicom into two integrated

operators so they could compete effectively with China Mobile.

3. Between 2009 and 2015 – We characterized this period as the “heavy

investment” period for Chinese telcos. In 2008 the MII was restructured to

become the Ministry of Industry and Information Technology (MIIT). The MIIT’s

mandate is to oversee not just telecoms, but broadcasting, Internet, software,

telecom equipment and, effectively, the overall “knowledge economy” of China.

From this point and on, the policy focus on telecoms is not just supporting

telecoms, but related industries such as equipment and Internet. There has been

no more industry restructuring for telecom. The results are A) the issue of a 3G

license to China Mobile based on TD-SCDMA, B) the issue of a TD-LTE 4G license

to China Mobile and both TD-LTE and FDD-LTE 4G licenses to China Telecom

and Unicom, C) explicit and implicit pressure on the telecom operators to lower

data pricing (eg, data rollover in November 2015) to promote mobile Internet,

and D) the creation of a tower company to share maintenance cost and future

capex of tower construction, to lessen burden on the telecom operators.

For the next five years, we believe the policy focus will shift toward:

• More pressure for telecom operators to lower pricing on mobile data and

broadband services

• More pressure for operators to quickly expand 4G and broadband coverage

• Active R&D work and preparation for 5G technology, with a possible launch in

2019/20

• Ongoing efforts by telecom operators to upgrade data speed on both their

mobile and fixed line networks.

• Maintaining current structure of the telecom industry, but giving them some

help if the obligations prove to be too much to bear (there is no sign this is

necessary in the near term).

Between 1995 and 2002, three state-

owned telecom operators have all

been partially privatized and listed in

international stock markets

Between 2002 and 2008, the focus

was on issuing 3G licenses and

supporting the China-developed TD-

SCDMA standard

After 2009, the focus was on 3G

rollout and 4G licensing. The new

regulator, MIIT, oversees the entire

“knowledge economy” of China.

Over the next five years, the focus is

likely on 1) pushing for wide

coverage, 2) lower prices, 3)

ongoing tech upgrade, and 4)

preparing for 5G standard and

licensing

Telecommunications

Assuming Coverage

21 November 2016

page 11 of 64 , Equity Analyst, +852 3743 8009, [email protected] Lee, CFA

Please see important disclosure information on pages 61 - 64 of this report.

Our prediction of China’s regulatory focus on telecom is mainly driven by China’s two key

strategic initiatives: Internet Plus and Made in China 2025. China is in the midst of trying

to upgrade its manufacturing industry. It wants to transform itself from a “big industrial

country” to a “powerful industrial country.” It believes the rapid upgrade and

applications of broadband, mobile Internet, big data and cloud computing will 1) help

improve the efficiency of traditional industries, 2) create new businesses and business

models of various industries (eg, Internet finance), and 3) when combined with

manufacturing, speed up the transition from low value-add to high value-add through

innovations. We believe the two initiatives will work tightly together to achieve the

government’s long-term goal to transform China’s economy.

Premier Li Keqiang, who is in charge of China’s economic policies, has repeatedly said that

China would need more broadband coverage, higher data speed and more affordable

mobile Internet services in order to promote the use of the latest technology. The rise of

Alibaba, Tencent and Baidu in China has proven to the government that a better telecom

infrastructure could nurture a few entirely new industries.

Therefore, the government will likely continue to see telecom as a tool, or utility, to

achieve more important strategic goals for the economy. In this case, it will be hard to see

a policy focus allowing exciting returns to be achieved by the telecom operators.

Further Industry Consolidation not In

Sight Speculation about the merger of China Telecom and Unicom is misplaced

After three rounds of industry restructuring, we believe the government currently

considers the industry structure with three integrated operators as a sustainable one, at

least in the next few years. Between 2002 and 2008, China Mobile’s revenue share of the

industry had risen from 41.6% to 55.3%. More seriously, its EBITDA share of the industry

had skyrocketed from 44% to 58%. We believe that prompted the MII to merge China

Netcom with Unicom, and have Unicom sell the CDMA network to China Telecom in

2008 to create more effective competition for China Mobile. At the same time, China

Mobile was awarded a fixed line license and, subsequently, it took over China Tietong

(known as China Railcom) to expand into fixed line and broadband services.

Chart 12: Revenue Shares of Chinese Telcos

Source: Jefferies, company data

The key objective is to support the

“Internet+” and “Made in China

2025” initatives

Telecom is now the tool China uses

to upgrade the economy

Speculation about the merger of CT

and Unicom is unfounded

Telecommunications

Assuming Coverage

21 November 2016

page 12 of 64 , Equity Analyst, +852 3743 8009, [email protected] Lee, CFA

Please see important disclosure information on pages 61 - 64 of this report.

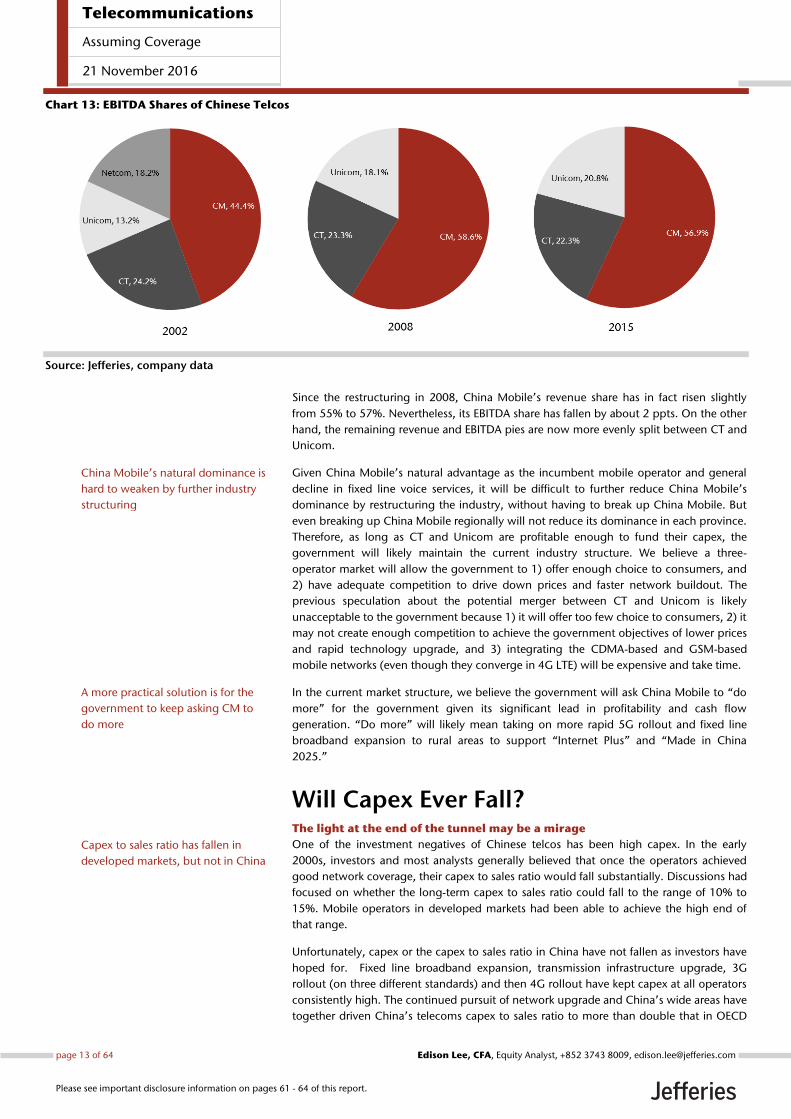

Chart 13: EBITDA Shares of Chinese Telcos

Source: Jefferies, company data

Since the restructuring in 2008, China Mobile’s revenue share has in fact risen slightly

from 55% to 57%. Nevertheless, its EBITDA share has fallen by about 2 ppts. On the other

hand, the remaining revenue and EBITDA pies are now more evenly split between CT and

Unicom.

Given China Mobile’s natural advantage as the incumbent mobile operator and general

decline in fixed line voice services, it will be difficult to further reduce China Mobile’s

dominance by restructuring the industry, without having to break up China Mobile. But

even breaking up China Mobile regionally will not reduce its dominance in each province.

Therefore, as long as CT and Unicom are profitable enough to fund their capex, the

government will likely maintain the current industry structure. We believe a three-

operator market will allow the government to 1) offer enough choice to consumers, and

2) have adequate competition to drive down prices and faster network buildout. The

previous speculation about the potential merger between CT and Unicom is likely

unacceptable to the government because 1) it will offer too few choice to consumers, 2) it

may not create enough competition to achieve the government objectives of lower prices

and rapid technology upgrade, and 3) integrating the CDMA-based and GSM-based

mobile networks (even though they converge in 4G LTE) will be expensive and take time.

In the current market structure, we believe the government will ask China Mobile to “do

more” for the government given its significant lead in profitability and cash flow

generation. “Do more” will likely mean taking on more rapid 5G rollout and fixed line

broadband expansion to rural areas to support “Internet Plus” and “Made in China

2025.”

Will Capex Ever Fall? The light at the end of the tunnel may be a mirage

One of the investment negatives of Chinese telcos has been high capex. In the early

2000s, investors and most analysts generally believed that once the operators achieved

good network coverage, their capex to sales ratio would fall substantially. Discussions had

focused on whether the long-term capex to sales ratio could fall to the range of 10% to

15%. Mobile operators in developed markets had been able to achieve the high end of

that range.

Unfortunately, capex or the capex to sales ratio in China have not fallen as investors have

hoped for. Fixed line broadband expansion, transmission infrastructure upgrade, 3G

rollout (on three different standards) and then 4G rollout have kept capex at all operators

consistently high. The continued pursuit of network upgrade and China’s wide areas have

together driven China’s telecoms capex to sales ratio to more than double that in OECD

China Mobile’s natural dominance is

hard to weaken by further industry

structuring

A more practical solution is for the

government to keep asking CM to

do more

Capex to sales ratio has fallen in

developed markets, but not in China

Telecommunications

Assuming Coverage

21 November 2016

page 13 of 64 , Equity Analyst, +852 3743 8009, [email protected] Lee, CFA

Please see important disclosure information on pages 61 - 64 of this report.

countries. In absolute amount, total telecom capex as reported by the listed telecom

companies has gone up from Rmb150bn in 2006 to almost Rmb450bn in 2015.

Chart 14: Total Telecoms Capex in China

Source: Jefferies, company data Note: CDMA capex incurred by Unicom’s parent in 2006 and 2007, and TD-SCDMA capex incurred by China Mobile’s parent between 2009 and 2013 is excluded. CDMA capex incurred by China Telecom’s parent between 2008 and 2013 is included.

Chart 15: Telecoms Capex to Sales Ratio

Source: OECD Digital Economy Outlook 2015, company data, Jefferies Note: CDMA capex incurred by Unicom’s parent in 2006 and 2007, and TD-SCDMA capex incurred by China Mobile’s parent between 2009 and 2013 is excluded. CDMA capex incurred by China Telecom’s parent between 2008 and 2013 is included.

Since the CDMA capex borne by Unicom’s parent (2006 and 2007) and the TD-SCDMA

capex borne by China Mobile’s parent has never been reported, we did not include these

numbers in the total telecom capex calculations. We estimate that the unreported capex

would be in the range of Rmb150bn to Rmb200bn, which would push up the capex to

sales ratio to 36% over the past ten years.

For 2016, the capex budget of all three telecoms operators will fall versus 2015, driven by

1) already extensive buildout of 4G in tier-one and tier-two cities, 2) establishment of

China Tower Corp., which will take over future capex of tower construction, and 3)

cooperation efforts between CT and Unicom on facilities and base station sharing. In

total, the budgeted 2016 capex of the three operators will fall by 18.5% from the 2015

Telecom capex in China has risen 3x

in the past 10 years

China’s telecom capex to sales ratio

has been more than double that of

OECD countries as a whole

These high capex to sales ratios did

not even include unreported capex

on CDMA and TD-SCDMA

Telecommunications

Assuming Coverage

21 November 2016

page 14 of 64 , Equity Analyst, +852 3743 8009, [email protected] Lee, CFA

Please see important disclosure information on pages 61 - 64 of this report.

level. However, the fall was mainly driven by the 44% fall at Unicom, which has

aggressively cut capex in 2G/3G, fixed line broadband network as well as infrastructure

and transmission.

Chart 16: Capex of Chinese Telcos: 2015 vs 2016 Budget (Rmb bn)

Source: company data, Jefferies

We agree that in the next two years the overall capex and capex to sales ratio in China will

likely fall moderately. However, to extrapolate that trend longer term and derive a DCF

valuation on the basis of a continued fall in absolute capex or the capex to sales ratio is

very risky.

As discussed in the first section of this report, we believe the policy focus in the next five

to seven years will be on pressing for faster network rollout and ongoing technology

upgrade. Therefore, the capex to sales ratio for the three Chinese telcos as a whole is

unlikely to be significantly below 30%. For China as a whole, we forecast total telecom

capex will rise slightly from Rmb1.2 trillion per year to Rmb1.3 trillion in the next four

years. The capex to sales ratio will stay roughly at 29%. Nevertheless, we believe it is

possible that the capex, as well as capex to sales ratio, starting from 2020 could rise

significantly above our current forecast should China decide to aggressively roll out 5G.

Chart 17: Total Capex Forecast and Capex to Sales Ratio Forecast

Source: company data, Jefferies

After aggressive 4G rollout, telecom

capex in China will likely fall

moderately in 2016

Longer term capex will go back up in

absolute terms

Capex to sales ratio will likely remain

closer to 30%

Telecommunications

Assuming Coverage

21 November 2016

page 15 of 64 , Equity Analyst, +852 3743 8009, [email protected] Lee, CFA

Please see important disclosure information on pages 61 - 64 of this report.

Continued Pressure to Lower Prices The government want lower and lower prices, to spur other industries

Competition has driven down telecom tariffs in China. However, the government has

from time to time given “indications” to telecom operators that they would like to see

faster fall in prices. Sometimes it is driven by consumer complaints; sometimes it is driven

by other priorities such as focusing on supporting the equipment industry.

Recently there have been strong signs that the telecom operators in China are under more

government pressure to cut prices:

• In June 2015, all three telecom operators introduced a data rollover

arrangement, where users can transfer unused mobile data in a particular month

to the following month.

• In mid-2016, CT and Unicom said they would phase out national roaming

charges (when a user makes or receives calls outside his/her home province) and

national long distance surcharges. China Mobile said in August 2016 that it

would start implementing a one-rate system for all local and national long

distance calls on its mobile networks.

• Premier Li Keqiang has said on several occasions that telecom pricing in China

needs to be more affordable to promote the popularity of mobile Internet and

mobile commerce.

The ongoing pressure for telecom operators to cut prices has caused China’s telecom

revenue to GDP ratio to continue falling in the past 10 years. In the early 2000s, many

analysts believed that telecom revenue would rise as a percentage of GDP as a country’s

income level increases. Therefore, the top line growth of Chinese telcos should continue

to exceed GDP growth. However, competition and government-led pressure to lower

prices from time to time have proved this theory wrong. It happened not only in China,

but also in India.

Chart 18: Telecom Revenue to GDP Ratio

Source: IMF World Economic Outlook 2015, www.dnaindia.com, company data, Jefferies

Using data in 2014 and 2015, we found that there is no longer any material correlation

between the level of GDP per capita and a country’s telecom revenue to GDP ratio.

Therefore, even if China’s GDP per capita is expected to rise further, China’s telecom

revenue to GDP ratio may continue to languish.

Government pressure to lower prices

sometimes is explicit, and sometimes

implicit

Both mobile voice and data pricing

has been the government’s target

Telecom revenue as a % of GDP was

thought to rise along with income

But in China it has been falling for

the past 10 years, as well as in India

Telecommunications

Assuming Coverage

21 November 2016

page 16 of 64 , Equity Analyst, +852 3743 8009, [email protected] Lee, CFA

Please see important disclosure information on pages 61 - 64 of this report.

Chart 19: Telecom Revenue to GDP Ratio vs. GDP per Capita

Source: IMF World Economic Outlook 2015, UK Ofcom International Report for 2014, Jefferies Note: Data for China, India and Korea are for 2015; others for 2014

Another bullish argument for top line growth is the rising penetration of 4G in China. By

the end of September, there were 677m of 4G mobile users in China, which accounted for

51% of total mobile users. The theory is that 4G users will spend more on mobile Internet

services and thus would help lift revenue growth for the three Chinese telcos. Globally

there is a positive, but weak, correlation between 4G penetration rate and the ratio of

telecom revenue to GDP. Nevertheless, China is significantly above the trend curve,

which means its telecom revenue to GDP ratio is much lower than its 4G penetration

would suggest. We believe it is because both voice and data prices in China are very low

and the continued pressure for the Chinese telcos to lower prices will likely keep its

telecom revenue to GDP ratio falling. In other words, telecom revenue in China will

continue to grow at a slower rate than the slowing GDP growth, in our view.

Chart 20: Telecom Revenue to GDP Ratio vs 4G Penetration

Source: IMF World Economic Outlook 2015, UK Ofcom International Report for 2014, Jefferies Note: Data for China, India and Korea are for 2015; others for 2014

There is no clear relationship

between telecom revenue as a % of

GDP and income level any more

Some argue rising 4G penetration

will lift the telecom revenue to GDP

ratio

China’s 4G penetration is already

high but telecom revenue to GDP

ratio is still low

Telecommunications

Assuming Coverage

21 November 2016

page 17 of 64 , Equity Analyst, +852 3743 8009, [email protected] Lee, CFA

Please see important disclosure information on pages 61 - 64 of this report.

Chart 21: Telecom Revenue to GDP Ratio – Global Comparison

Source: IMF World Economic Outlook 2015, UK Ofcom International Report for 2014, Jefferies Note: Data for China, India and Korea are for 2015; others for 2014

Is Mobile Data Demand in China Price

Elastic? We give it benefit of the doubt now, but early signs suggest risk

Some optimism has been expressed that lower mobile data prices will stimulate enough

usage growth that it is in fact positive for the three Chinese telcos. We believe mobile data

demand is price elastic when prices are relatively high. At this point, in fact we are worried

that the price elasticity in China has been exhausted. Any further fall in mobile data

pricing is likely a negative development for the revenue growth of the Chinese telecom

operators.

Examining the general trend of mobile data pricing versus total mobile data traffic in

China may lead one to the conclusion that mobile data demand showed high elasticity of

demand. In 2015, average revenue per MB of mobile data fell by 41% YoY but total

mobile data traffic rose by 119%. In 1H16, mobile data pricing dropped another 43% YoY

while total mobile data traffic increased by 128%. On the surface, mobile data demand

looks very price elastic.

China’s low telecom revenue to GDP

ratio on a global basis is likely due to

low pricing

Mobile data demand should be price

elastic

Telecommunications

Assuming Coverage

21 November 2016

page 18 of 64 , Equity Analyst, +852 3743 8009, [email protected] Lee, CFA

Please see important disclosure information on pages 61 - 64 of this report.

Chart 22: China’s Mobile Data Pricing vs Total Mobile Data Traffic – YoY

Change

Source: Company data, Jefferies

However, the total mobile data traffic growth has been a function of both organic usage

growth on the existing subscribers and new subscriber additions in 4G. The subscriber

growth was likely driven more by handset subsidies, promotion efforts and the general

need of faster data speed by consumers, rather than lower data pricing. We believe

examining the relationship between mobile data pricing and data of use (DOU) per 4G

subscriber will yield a more reliable estimate of price elasticity of demand for mobile data.

Using 1H16 data provided by CM and CT, we found that the elasticity of demand went

above -1, which means the percentage increase in DOU was smaller than the percentage

decrease in mobile data pricing. It is a significant cause of concern because if growth in

mobile data usage cannot offset the accelerating pricing pressure, revenue growth will

likely disappoint. That is also why we strongly believe China’s telecom industry revenue

growth will continue to lag GDP growth.

Chart 23: China Mobile’s Mobile Data Pricing vs DOU Per Subscriber – YoY

Change

Source: Company data, Jefferies Note: 2014 data reflect DOU per 3G subscriber, while data for 1H16 (vs 1H15) reflect DOU per 4G subscriber.

That seems to be supported by

examining total data traffic growth

vs. changes in data pricing

But total mobile data traffic growth is

driven by both subscriber growth

and organic usage growth

Focusing on organic growth of

mobile data traffic is more reliable,

and CM’s numbers in 1H16 suggest

some risk of that elasticity being

exhausted

Telecommunications

Assuming Coverage

21 November 2016

page 19 of 64 , Equity Analyst, +852 3743 8009, [email protected] Lee, CFA

Please see important disclosure information on pages 61 - 64 of this report.

Chart 24: China Telecom’s Mobile Data Pricing vs DOU Per Subscriber – YoY

Change

Source: Company data, Jefferies Note: 2012-2014 data reflect DOU per 3G subscriber, while data for 1H16 (vs 1H15) reflect DOU per 4G subscriber.

Low Morale Makes Improvement Even

Harder Compensation pressure and lack of stock options increase execution risks

In the first section, we discussed extensively why we think the current regulatory

environment is shareholder unfriendly. Those regulatory factors are specific to the telecom

industry. Outside of that, we also believe there are more general government policies that

are not helping minority shareholders.

Under President Xi’s leadership, the Chinese government started implementing an

aggressive anti-graft campaign in 2013, and it is still ongoing. The anti-grafting campaign

has two parts: A) investigate, arrest and prosecute corrupted government officials

(regardless of ranks, including SOE management), and B) promote frugality at all levels of

government and SOEs.

The anti-graft campaign has stormed through all major industries. In telecom, a number

of senior management members of China Mobile and China Telecom have been arrested

(and fired) for corruption. What is worse, the pursuit of frugality has resulted in both pay

freeze and pay cut at all three telecom operators.

In 2015, the total compensation of all three telecom operators’ top management has

fallen by 25% to 73%. Some may argue that this is only to create an impression that they

support the government’s initiative. However, we believe it has had real negative impact

on the level of compensation at middle management, especially at the provincial level.

Even though there has been generally no pay cut for middle management, it becomes

much more difficult for top management to justify salary increases and/or bonuses for

middle management. Consequently, the telecom operators’ middle management are

effectively having a compensation freeze.

CT’s numbers in 1H16 also suggest

the same risk

Government’s focus on frugality

means a very tight budget for SOEs

Several senior executives in the

telecom industry arrested for

corruption

The top management of all three

operators took significant pay cuts

Telecommunications

Assuming Coverage

21 November 2016

page 20 of 64 , Equity Analyst, +852 3743 8009, [email protected] Lee, CFA

Please see important disclosure information on pages 61 - 64 of this report.

Chart 25: Compensation Cut in 2015 vs 2014

Source: Company data, Jefferies

Moreover, since 2013, the government has banned the issue of stock options to SOE

employees. Even for previously issued options that remain outstanding, SOE management

has been expected not to exercise them. Therefore, with no stock options and little

prospect of improving salaries and bonuses, we believe the morale of the telecom

operators’ senior and middle management is currently quite low. This is in stark contrast

with the situation in the early 2000s, when the newly created SASAC decided to

incentivize SOE management to improve efficiency by giving them stock options, and

using profitability and return on capital as the major criteria for evaluating the

performance of SOEs’ top management.

Given the competitive nature of China’s telecom industry, both senior and middle

management of the telecom operators have many KPIs to meet. Therefore, their jobs are

stressful but there is little financial upside for them. The resulting low morale will make

any operational improvement at these companies even harder to achieve, and may even

eventually cause an exodus of young talents to private companies.

Our Valuation Work Suggests

Significant Downside Continued pricing pressure means slowing revenue growth

In 2H2015, the three operators introduced a data rollover program, which allows

customers to transfer the used mobile data in their packages to the following month. This

resulted in a significant slowdown in mobile revenue growth last year. In fact, both CT

and Unicom registered negative revenue growth in 2015. With a very low base in

2H2015, we forecast revenue growth will recover in 2016 for all three operators.

However, we believe the revenue growth rate in 2016 is not sustainable simply because

the government continued to put pressure on different fronts.

Mobile data pricing continued to fall at a rate of 30%+ in 1H2016. Competition was a

factor but the ongoing steep cut was partly done to satisfy what was perceived as

government expectation. In addition, in CM started phasing out national roaming charges

and domestic long distance rate premiums by introducing nationwide one-rate packages.

We believe aggressive, pro-active cuts in mobile data pricing, elimination of domestic

roaming and long distance price premium, and rising popularity of over-the-top services

such as WeChat calls will continue to pressure revenue growth at all three operators.

2014A 2015A YoY 2014A 2015A YoY 2014A 2015A YoY

CEO 1,994 574.9 -71% CEO 911 670 -26% CEO 1,076 696 -35%

CFO 1,812 521.5 -71% COO 807 593 -27% CFO 1,013 676 -33%

Exec Director 1 1,812 498.1 -73% Exec Director 1 808 608 -25% Exec Director 1 902 610 -32%

Exec Director 2 1,812 498.1 -73% Exec Director 2 815 601 -26% Exec Director 2 866 610 -30%

Exec Director 3 796 589 -26%

China Mobile China Telecom China Unicom

Top management lead by example

There are no stock options any more

Middle management under a lot of

pressure but not financially

incentivized enough

Data rollover in 1H15 only the start

of further pricing pressure

Mobile data pricing continued to fall

by 30%+ YoY after the data rollover

in1H15

Telecommunications

Assuming Coverage

21 November 2016

page 21 of 64 , Equity Analyst, +852 3743 8009, [email protected] Lee, CFA

Please see important disclosure information on pages 61 - 64 of this report.

Chart 26: YoY Growth in Service Revenue

Source: Company data, Jefferies

Our view that there will be no industry consolidation in sight means that the degree of

competition in the industry will not materially improve. Even though CT and Unicom

entered into an agreement to share some base stations, and China Tower Corp. was

created to centralize the maintenance and construction of towers, we believe price

competition on mobile voice, mobile data and wireline broadband will continue to be

intense, owing to limited differentiation of services. The three operators have rationally

cut back handset subsidies as a way to stimulate subscriber growth and upgrade. While

we believe handset subsidies will likely be restrained, general marketing and promotional

costs and network operations cost will likely continue to rise, pressuring the operators’

EBITDA margin.

Chart 27: EBITDA Margin Trend

Source: Company data, Jefferies

Established telecom companies are usually valued on the basis of discounted cash flow

(DCF), because the business is relatively stable (ie, non-cyclical) but has high capital

intensity. However, DCF’s major weakness is its high dependence on a few assumptions,

such as the weighted average cost of capital (WACC), the terminal growth rate and, in

case of telecoms companies, the long-term assumptions on capex. A small change in any

of these assumptions can swing the DCF results widely.

Chart 15 shows the summary results of our DCF valuation, which we also used as the

basis to set our target prices. We believe the most important assumption here is the capex

to sales ratio. Some analysts have derived a high DCF value for these three companies

Elimination of DLD price premium

and domestic roaming charges, and

further OTT substitution mean

further revenue growth pressure

No industry consolidation means a

moderate degree of price

competition will continue

We expect the EBITDA margin of all

three operators to fall more

We use DCF to value these

companies to capture their high

capex

But our assumption of capex to sales

at 27% to 30% is likely higher than

consensus

Telecommunications

Assuming Coverage

21 November 2016

page 22 of 64 , Equity Analyst, +852 3743 8009, [email protected] Lee, CFA

Please see important disclosure information on pages 61 - 64 of this report.

because the capex to sales ratio is assumed to fall quickly in the future. We have argued

above the telecoms capex in China will likely remain high, driven by the government’s

pressure to constantly expand coverage and upgrade technology and data speed. We

expect these three companies will start building 5G mobile networks by the end of 2019,

which will kick off another “up cycle” in capex. Therefore, the long-term average capex to