Embed Size (px)

Citation preview

Pillar 3 Disclosures as at 31 December 2014

BHF Kleinwort Benson

2

Contents

1. Introduction ................................................................................................................................................................ 5

Background ................................................................................................................................................................ 5

Overview of the regulatory framework ................................................................................................................. 5

Objective .................................................................................................................................................................... 5

Developments since last disclosure ....................................................................................................................... 6

Key Metrics ................................................................................................................................................................. 6

2. Scope .......................................................................................................................................................................... 7

BHF Kleinwort Benson Group SA (“BHF KB”) .................................................................................................... 8

BHF (“BHF”) ............................................................................................................................................................ 9

Kleinwort Benson Bank Limited (“KBBL”) .......................................................................................................... 9

Kleinwort Benson Channel Islands Holdings Limited and subsidiaries (“KBCIHL”) ................................... 9

Kleinwort Benson Investors Dublin Limited (“KBI”) .......................................................................................... 9

Differences in the basis of consolidation for accounting and prudential purposes .................................... 9

Pillar 3 process and approval policy ...................................................................................................................11

Basis and frequency of disclosures ......................................................................................................................12

Future Developments .............................................................................................................................................12

Location and verification ......................................................................................................................................12

3. Governance and Risk Management ..................................................................................................................13

BHF Kleinwort Benson Group SA ...........................................................................................................................13

BHF Bank ....................................................................................................................................................................13

Kleinwort Benson .....................................................................................................................................................19

Kleinwort Benson Wealth Management (“KBWM”) ....................................................................................19

KBI ..........................................................................................................................................................................26

4. Assessment of Group’s Risk Mitigation Policies and Assumptions ..................................................................29

Risk appetite .............................................................................................................................................................29

Risk Identification .....................................................................................................................................................29

Use of Credit Risk Mitigation Techniques ............................................................................................................31

BHF Kleinwort Benson Group (Management companies) ........................................................................31

BHF Bank ..............................................................................................................................................................31

Kleinwort Benson Wealth Management (“KBWM”) ....................................................................................32

KBI ..........................................................................................................................................................................32

5. Capital resources ....................................................................................................................................................33

Total Available Capital ..........................................................................................................................................33

BHF Kleinwort Benson

3

Indicators of global systematic importance ......................................................................................................33

Description of Capital Instruments .......................................................................................................................33

Common Equity Tier 1 (CET 1) Capital ...........................................................................................................33

Tier 2 (T2) Capital ................................................................................................................................................34

Capital Management ............................................................................................................................................34

6. Capital requirements ..............................................................................................................................................35

Internal Assessment of Capital Adequacy.........................................................................................................35

Capital Buffers ..........................................................................................................................................................35

7. Credit risk ...................................................................................................................................................................37

Credit Risk Exposures ...............................................................................................................................................37

Credit Limits for Exposures ......................................................................................................................................37

BHF Kleinwort Benson Group (Management companies) ........................................................................37

BHF Bank ..............................................................................................................................................................38

Kleinwort Benson Wealth Management (“KBWM”) ....................................................................................39

KBI ..........................................................................................................................................................................39

Netting Arrangements ............................................................................................................................................39

BHF Bank ..............................................................................................................................................................40

Kleinwort Benson Wealth Management (“KBWM”) ....................................................................................40

Geographical Analysis of Exposures ....................................................................................................................40

Maturity Analysis of Exposures ...............................................................................................................................40

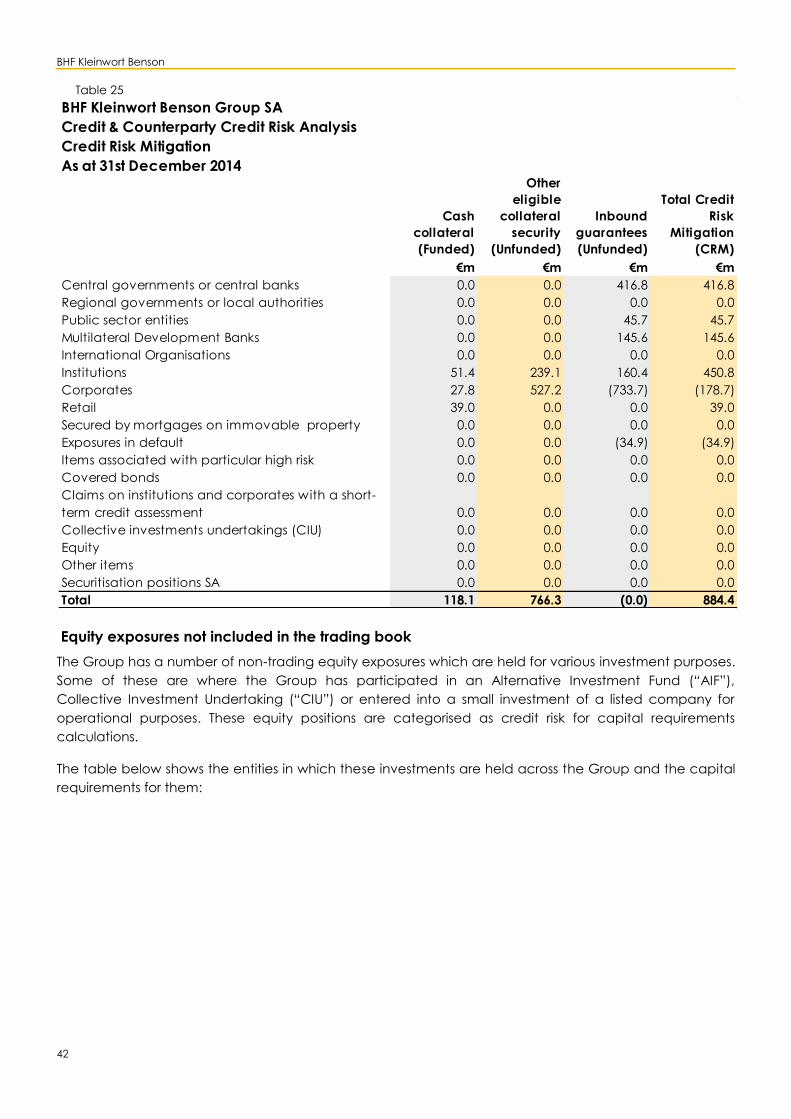

Credit Risk Mitigation (“CRM”) ..............................................................................................................................41

Equity exposures not included in the trading book ..........................................................................................42

BHF Bank ..............................................................................................................................................................43

BHF KB Group (Management companies) & Kleinwort Benson Wealth Management (“KBWM”) ...45

Impairment of Financial Assets and Past Due Items .........................................................................................45

Neither past due or impaired ..........................................................................................................................47

Past due but not impaired financial instruments .........................................................................................47

Impaired loans ....................................................................................................................................................47

Use of External Credit Assessment Institutions (“ECAI”) ....................................................................................49

8. Counterparty Credit Risk ........................................................................................................................................51

Settlement Risk .........................................................................................................................................................51

Derivatives & Financial Contracts ........................................................................................................................51

Counterparty Credit Limits .....................................................................................................................................51

Wrong-Way risk ........................................................................................................................................................51

Counterparty Credit Risk Mitigation ....................................................................................................................52

Potential Collateral Obligations ...........................................................................................................................53

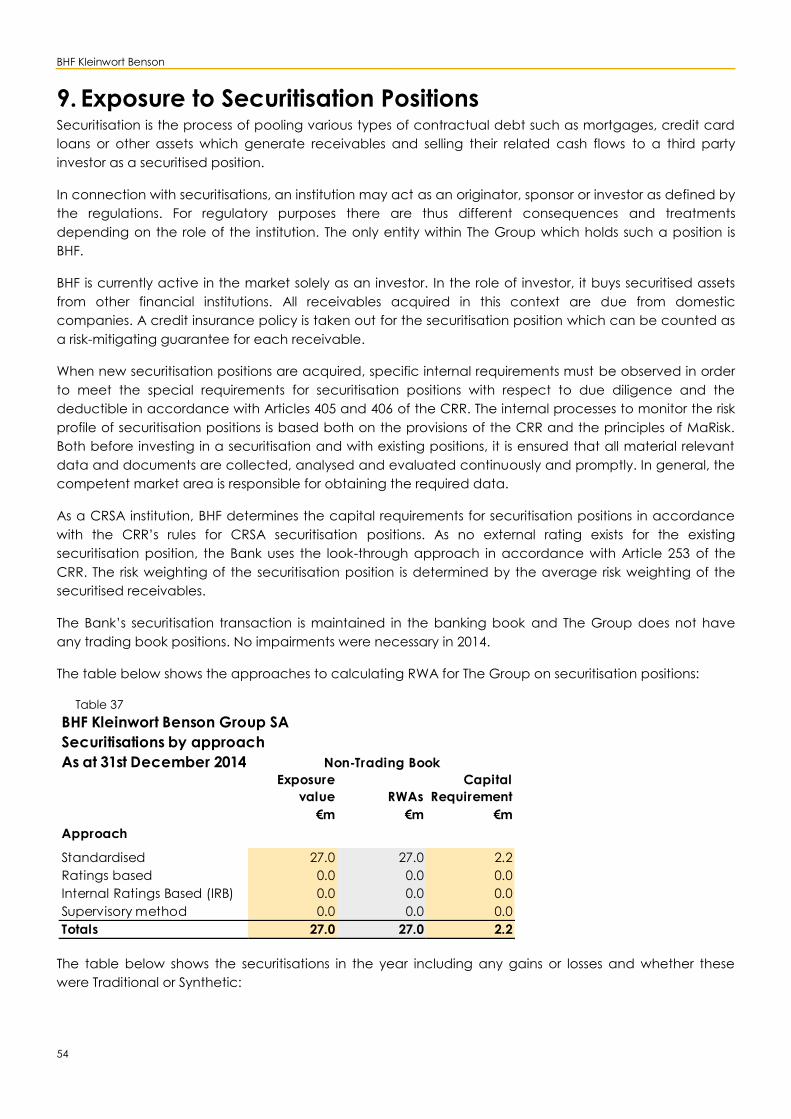

9. Exposure to Securitisation Positions ......................................................................................................................54

10. Market Risk ................................................................................................................................................................59

BHF Kleinwort Benson

4

Market Risk - BHF Bank ............................................................................................................................................59

Market Risk – Kleinwort Benson Wealth Management (“KBWM”) .................................................................61

Market Risk – Capital Requirements ....................................................................................................................61

Equity Market Risk (Trading Book) ........................................................................................................................62

Currency (“FX”) Risk ................................................................................................................................................62

Currency (“FX”) Risk – BHF Bank ......................................................................................................................62

Currency (“FX”) Risk – KBBL, KBCIHL, KBI & BHF KB Group management companies ..........................62

Interest Rate (Non-Trading Book) .........................................................................................................................63

Assumptions used in the calculation of the interest rate gap ..................................................................64

Debt instruments (Trading Book) ..........................................................................................................................64

VaR Model Based PRR ............................................................................................................................................65

SVar Model Based PRR ...........................................................................................................................................65

11. Operational Risk .......................................................................................................................................................67

BHF KB Group management companies ...........................................................................................................67

BHF Bank ....................................................................................................................................................................67

Kleinwort Benson Wealth Management (“KBWM”) ..........................................................................................67

KBI ...............................................................................................................................................................................68

BHF KB Group operational risk requirements ......................................................................................................69

12. Unencumbered Assets ...........................................................................................................................................70

13. Leverage ...................................................................................................................................................................72

14. Remuneration ..........................................................................................................................................................73

Governance .............................................................................................................................................................73

Scope ........................................................................................................................................................................73

Link between pay and performance ..................................................................................................................74

Determination of variable remuneration ......................................................................................................74

Cap on variable remuneration .......................................................................................................................74

Deferral of variable remuneration ..................................................................................................................74

Code staff remuneration .......................................................................................................................................75

15. Appendix – List of Acronyms .................................................................................................................................76

Terms ..........................................................................................................................................................................76

Entity names .............................................................................................................................................................77

BHF Kleinwort Benson

5

1. Introduction

Background

BHF Kleinwort Benson Group (“BHF KB”) is regulated as an institution in the UK by the Prudential Regulation

Authority (“PRA”). The PRA regulate BHF KB as a UK Consolidation Group and currently acts as the lead

regulator. The Financial Conduct Authority (“FCA”) regulates the UK financial services activities of the

Group via Kleinwort Benson Bank Limited (“KBBL”).

All disclosures within this report have been prepared from existing internal policies and documentation

reflecting BHF KB’s practices as at 31st December 2014, the Group’s last financial year end.

Overview of the regulatory framework

The PRA requires BHF KB to maintain sufficient financial resources, including own funds and liquidity

resources of an amount and quality to ensure there is no significant risk that its l iabilities cannot be met as

they fall due.

The Basel lll regulatory framework, which was implemented in Europe through the Capital Requirements

Directive IV (“CRD IV”), came into effect on 1 January 2014. The requirements of CRD IV build upon the

pre-existing regulations which divide the framework into three ‘pillars’ that leislate how a firm should

approach this responsibility:

Pillar 1 sets out quantitative minimum capital requirements to mitigate a firms’s credit, counterparty,

market and operational risk

Pillar 2 requires firms to carry out an ‘Individual Capital Adequacy Assessment Process’ (“ICAAP”), a

more qualitative internal review to assess its own risk profile and whether additional capital should be

held against those risks not adequately covered in Pillar 1. The firm’s view of the additional capital

requirement is also assessed by the GFSC during its ‘Supervisory Review and Evaluation Process’ (“SREP”)

and is used to determine the overall capital resources required by the bank

Pillar 3 rules are designed to promote market discipline by enhancing the level of disclosures made by

firms to their stakeholders, allowing them to assess a firm’s key risk exposures and the adequacy of the

Board’s risk management processes to mitigate these risks

All three pillars require that a firm has in place strategies, processes and systems to identify and manage

the major sources of risk relevant to the firm, given the nature and scale of its business, and to assess and

maintain financial resources that it considers adequate to cover the risks to which it is or might be

exposed.

The Pillar 3 disclosure requirements are set out in articles 429 to 455 of the Capital Requirements

Regulation (“CRR”).

Objective

This document comprises BHF KB’s Pillar 3 disclosures on capital and risk management as at

31 December 2014. It has two principal purposes:

To meet the regulatory disclosure requirements noted above

To provide stakeholders with further useful information on the capital and risk profile of the Group

BHF Kleinwort Benson

6

Developments since last disclosure

BHF KB has now fully transformed itself from an industrial holding company into a focused financial

services group by materially disposing of all legacy (non-financial) businesses. In addition to this, on

26th March 2014 BHF KB acquired BHF (“BHF”), which substantially increased BHF KB’s assets.

During the year RHJI International SA (“RHJI”) renamed itself as BHF Kleinwort Benson SA which was part of

simplifying the legal structure of The Group. This is explained on pages 2 - 9 of the BHF Kleinwort Benson

Group Annual report 2014. The Annual Report 2014 is located on BHF Kleinwort Benson’s website and can

be accessed via the following link:

http://www.bhfkleinwortbenson.com/investor-information/financial-information/financial-reports-

presentations/annual-reports?year=2014

Key Metrics

The Group’s performance in 2014 was in line with expectations following the acquisition of BHF and

changes to BHF KB’s structure. The key ratios and metrics that demonstrate The Group’s capital and

financial position are as follows:

Table 1

Common Equity

Tier 1 Capital

Common Equity

Tier 1 Ratio

€734.8m 17.0%

Tier 1 Capital Tier 1 Ratio

€734.8m 17.0%

Total Regulatory Capital Total Capital Ratio

€888.2m 20.5%

Total RWA's Total RWA Density

€,4333.6m 46.2%

Credit Risk RWA Credit Risk RWA Density

€,3363.3m 50.1%

Leverage Ratio

(As Per CRR)

7.2%

BHF Kleinwort Benson

7

2. Scope In line with CRR guidelines the Pillar 3 disclosures are presented at a BHF KB consolidated level. The basis

of consolidation is the same as for Capital Adequacy (Own Funds) reporting to the PRA.

While the BHF KB Annual Report 2014 is published in EUR, the capital adequacy reporting to the PRA is in

GBP. Therefore BHF KB will publish the Pillar 3 disclosures in both GBP & EUR currencies for consistency and

reconciliation purposes.

CRD4 regulation states that significant subsidiaries must also report limited Pillar 3 disclosures. The main

significant subsidiaries of the Group are BHF, Kleinwort Benson Channel Islands Holding Limited (“KBCIHL”)

and Kleinwort Benson Bank Limited (“KBBL”). These subsidiaries also disclose their own Pillar 3 disclosures

report.

The diagram below shows details of The Group structure as at 31st December 2014:

Table 2

BHF Kleinwort Benson

8

Kleinwort Benson Group Limited (“KBG”) is currently in the process of being collapsed into the parent

company BHF Kleinwort Benson Group SA to create a cost-efficient single-tier holding structure. This is part

of the Group’s legal reorganisation strategy, which is explained on page nine of BHF KB Group’s annual

report 2014. For this reason, further sections below will incorporate these two holding companies into a

single company where possible and refer to them as BHF KB Group (Management companies).

BHF KB Group (Management companies) has disposed of its legacy portfolio relating to investments in

industrial holdings, which historically would have been deducted as “Qualifying Holdings”. There is a small

transitional amount remaining which will also be liquidated into cash once it is strategically appropriate.

These items are shown at amortised cost for accounting purposes and not consolidated which is

consistent to their treatment for prudential purposes. These items are risk weighted as part of Equity Credit

Risk.

BHF KB Group (Management companies) continues to hold small holdings (€18m) in Financial Investments

which are not significant and equity accounted, which historically would have been deducted as

“Material Holdings”. These items are not consolidated for accounting purposes, which is consistent to

how they are treated for prudential purposes. These items are risk weighted as part of Equity Credit Risk.

During the year the Group acquired some new equity investments as part of the takeover of BHF. BHF

holds a small number of investments, which are predominantly in Funds and they are treated in the same

manner for both accounting and prudential reporting. These investments are not consolidated and risk

weighted as part of The Groups credit risk calculations. This is explained further in section 7.8 of this Pillar 3

document.

As at 31st December 2014 the Group’s basis for prudential consolidation is the same as the accounting

consolidation for the financial statements.

The entities within the business that fit one of the following descriptions have been included in the

Group’s prudential consolidation:

An institution (i.e. a bank, building society or investment firm)

A financial institution

An asset management company

A financial holding company

An ancillary services undertaking

The entities considered to be financial companies and within scope of consolidation include BHF, KBBL,

KBCIHL and Kleinwort Benson Investors Dublin Ltd (“KBI”). In addition investments in subsidiary

undertakings or participations that are financial companies are also consolidated for both accounting

and prudential purposes.

The Group does not have any transitional provisions or deductions in relation to ‘Material’ or ‘Qualifying

holdings’. No entities have been partially consolidated and after the changes in the legal structure as

explained on page 9 of the Annual Report 2014 there are no deductions in relation to ‘Minority Interests’.

BHF Kleinwort Benson Group SA (“BHF KB”)

The Group’s ultimate parent company BHF Kleinwort Benson Group SA is a financial holding company

incorporated under the laws of Belgium, having its registered office in Brussels, Belgium.

BHF KB combines the two traditional brands of BHF and Kleinwort Benson to create a client-centric

merchant bank with principle activities in private banking, asset management and financial markets &

corporates. BHF KB provides contemporary wealth management and corporate banking in Europe for

sophisticated private and corporate clients and family offices.

BHF Kleinwort Benson

9

As noted above, it is assumed that KBG is part of BHF KB for the purposes of the Pillar 3 disclosures.

BHF (“BHF”)

BHF is the modern private bank for discerning middle-market entrepreneurs and their families. The bank

has a clear strategic focus on wealth management and corporate advisory services. BHF's business

activities are focused on Private Banking and Asset Management along with Financial Markets &

Corporates. The close cooperation between Private Banking and a Corporate Finance unit that is clearly

geared to the needs of entrepreneurs in the 'Mittelstand' segment is one of the bank's hallmarks.

Headquartered in Frankfurt am Main, BHF has 12 locations in Germany and international offices in

Abu Dhabi, Geneva, Luxembourg and Zurich.

Kleinwort Benson Bank Limited (“KBBL”)

KBBL focuses on providing private banking and wealth management services. The target clients are high

net worth individuals, family offices and entrepreneurs primarily in the UK and selected international

markets. KBBL offers bespoke structuring of complex wealth solutions for high net worth clients as well as

in-house funds for the affluent sector whilst seeking to maintain a strong capital base and a liquid

balance sheet with little reliance on wholesale funding.

Kleinwort Benson Channel Islands Holdings Limited and subsidiaries (“KBCIHL”)

Kleinwort Benson’s offshore operations are focused on Guernsey and Jersey. Kleinwort Benson plays a

pivotal role in these key financial centres and was one of the first major banks to establish itself in the

Channel Islands, over 50 years ago. Jersey and Guernsey are on the G20’s White List and are classed as

having substantially implemented the internationally agreed tax standard along with the UK, US, France

and Germany.

In addition to providing private banking services, including Fiduciary, to wealth management clients,

KBCIHL delivers a business-to-business proposition to Trust Companies, assisting them in managing their

clients' assets, deposits and electronic banking, custody and investment services.

The Fiduciary, Fund Administration and Custodian Trustee divisions provide services to investment funds

and institutional clients including the administration of Funds, Employment Benefit Trusts, Special Purpose

Vehicles and the provision of Custodian Trustee services.

Kleinwort Benson Investors Dublin Limited (“KBI”)

KBI is an established institutional asset manager that has been managing assets for institutional investors

since 1980. It currently manages specialist strategies for public and corporate pension schemes, sub-

advisory investors and foundations/endowments. KBI offers investment services on both a segregated

and unitised basis, with the majority of its Assets under Management (“AuM”) relating to its international

clients. KBI’s primary goal is to enhance performance and meet clients’ investment expectations through

specialisation and innovation. KBI focus on two key strategies: global equities and environmental equities.

KBI has a global client base in Europe, North America, the UK, Ireland and Asia.

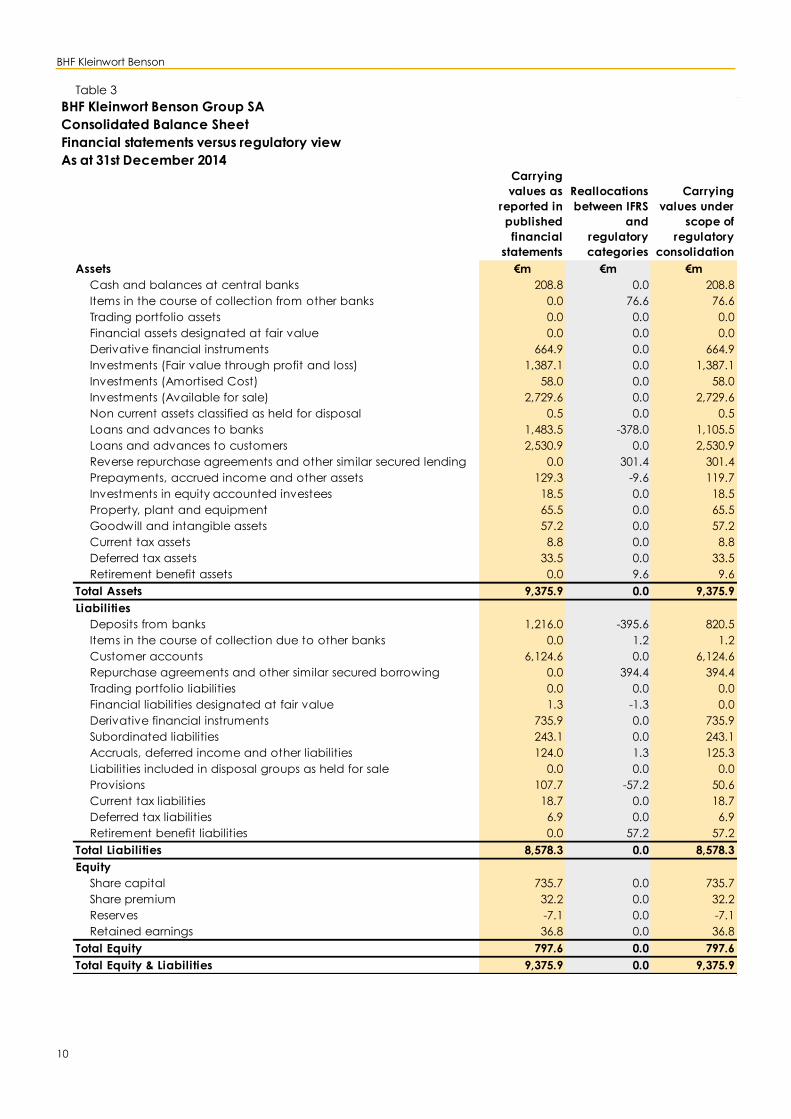

Differences in the basis of consolidation for accounting and prudential purposes

The Group’s basis for prudential consolidation is the same as the accounting consolidation in the

financial statements. In terms of presentation, some of the items are presented with different categories

for accounting and prudential reporting and the table below shows how these are reallocated.

BHF Kleinwort Benson

10

Table 3

BHF Kleinwort Benson Group SA

Consolidated Balance Sheet

Financial statements versus regulatory view

As at 31st December 2014Carrying

values as

reported in

published

financial

statements

Reallocations

between IFRS

and

regulatory

categories

Carrying

values under

scope of

regulatory

consolidation

Assets €m €m €m

Cash and balances at central banks 208.8 0.0 208.8

Items in the course of collection from other banks 0.0 76.6 76.6

Trading portfolio assets 0.0 0.0 0.0

Financial assets designated at fair value 0.0 0.0 0.0

Derivative financial instruments 664.9 0.0 664.9

Investments (Fair value through profit and loss) 1,387.1 0.0 1,387.1

Investments (Amortised Cost) 58.0 0.0 58.0

Investments (Available for sale) 2,729.6 0.0 2,729.6

Non current assets classified as held for disposal 0.5 0.0 0.5

Loans and advances to banks 1,483.5 -378.0 1,105.5

Loans and advances to customers 2,530.9 0.0 2,530.9

Reverse repurchase agreements and other similar secured lending 0.0 301.4 301.4

Prepayments, accrued income and other assets 129.3 -9.6 119.7

Investments in equity accounted investees 18.5 0.0 18.5

Property, plant and equipment 65.5 0.0 65.5

Goodwill and intangible assets 57.2 0.0 57.2

Current tax assets 8.8 0.0 8.8

Deferred tax assets 33.5 0.0 33.5

Retirement benefit assets 0.0 9.6 9.6

Total Assets 9,375.9 0.0 9,375.9

Liabilities

Deposits from banks 1,216.0 -395.6 820.5

Items in the course of collection due to other banks 0.0 1.2 1.2

Customer accounts 6,124.6 0.0 6,124.6

Repurchase agreements and other similar secured borrowing 0.0 394.4 394.4

Trading portfolio liabilities 0.0 0.0 0.0

Financial liabilities designated at fair value 1.3 -1.3 0.0

Derivative financial instruments 735.9 0.0 735.9

Subordinated liabilities 243.1 0.0 243.1

Accruals, deferred income and other liabilities 124.0 1.3 125.3

Liabilities included in disposal groups as held for sale 0.0 0.0 0.0

Provisions 107.7 -57.2 50.6

Current tax liabilities 18.7 0.0 18.7

Deferred tax liabilities 6.9 0.0 6.9

Retirement benefit liabilities 0.0 57.2 57.2

Total Liabilities 8,578.3 0.0 8,578.3

Equity

Share capital 735.7 0.0 735.7

Share premium 32.2 0.0 32.2

Reserves -7.1 0.0 -7.1

Retained earnings 36.8 0.0 36.8

Total Equity 797.6 0.0 797.6

Total Equity & Liabilities 9,375.9 0.0 9,375.9

BHF Kleinwort Benson

11

The table below shows how assets and liabilities as per the financial statements are presented or

disclosed for capital adequacy calculations in this Pillar 3 document.

Table 4

Pillar 3 process and approval policy

The Pillar 3 disclosures are completed annually as part of the overall Group regulatory reporting process.

Each business unit approves their components and validates the accuracy of the financial figures used in

the overall consolidation. All individual business unit and consolidated disclosures are checked and

validated against the relevant regulatory returns where possible to ensure the disclosures are consistent.

Sections of the Pillar 3 document are checked by Finance, Risk, Treasury, Legal, Compliance and

Corporate Governance representatives across each business unit. The component elements of the

disclosures have been reviewed and approved by local Executive Management of each subsidiary. The

consolidated Pillar 3 document is formally approved by the BHF KB Audit Committee before being

published.

The BHF KB Board believes these disclosures appropriately display the risk profile of The Group.

BHF Kleinwort Benson Group SA

Regulatory classifications of IFRS accounts

IFRS Classification Credit Risk

Counterparty

Credit Risk Market Risk 3

Assets £m £m £m

Cash and balances at central banks o o

Items in the course of collection from other banks o o

Trading portfolio assets o o

Financial assets designated at fair value o

Derivative financial instruments o o

Available for sale investments o o

Loans and advances to banks o o

Loans and advances to customers o o

Reverse repurchase agreements and other similar secured lending o o

Investments in equity accounted investees o o

Other Assets 1 o o

Liabilities

Deposits from banks o o o

Items in the course of collection due to other banks o o o

Customer accounts o o o

Repurchse agreements and other similar secured borrowing o o

Trading portfolio liabilities o o

Financial liabilities designated at fair value o o

Derivative financial instruments o o

Subordinated liabilities o o o

Other Liabilities 2o o o

1

2

3

Other Assets consist of Prepayments, Accrued Income, Other Assets, Property Plant and Equipment, Goodwill &

Intangibles, current tax assets, deferred tax assets & retirement benefit assets

Other Liabilities consist of Accruals, deferred income, other liabilities, Liabilities in disposal groups as held for

sale, provisions, current tax liabilities, deferred tax liabilities & retirement benefit liabilities

For market risk the table above indicates specific balance sheet items that are subject to market risk

fluctuations. It does not represent FX market risk which would impact the whole balance sheet.

BHF Kleinwort Benson

12

Basis and frequency of disclosures

The disclosures in this document have been completed in accordance with Articles 429 to 455 of the

CRR. Unless stated otherwise, all figures are as at the financial year-end, 31st December 2014. These

disclosures will be issued on an annual basis and prepared in conjunction with the Financial Statements.

Future Developments

The BCBS introduced a series of rules that form the basis of Basel III & CRD4 which became effective on

1st January 2014. Although CRD4 has been reflected in these Pillar 3 disclosures, some elements are being

phased in and will become effective over the course of the next few years. The impacts of the new rules

are summarised below:

Capital requirements and capital ratios will be gradually phased in as follows:

o Minimum Common Equity Tier 1 (“CET1”) requirement of 7% by 2019: This includes a 2.5%

Capital Conservation Buffer (“CCB”) which will be phased in from 01st January 2016 with

increments 0.625% per annum.

o Minimum Total Capital requirement of 10.5% by 2019 which also includes the CCB of 2.5%

being phased in from 01st January 2016 for CET1 ratio requirements.

o The Bank of England also has the option to introduce a Counter-Cyclical Capital Buffer

(“CCCB”)

New leverage ratio of 3% will be introduced for all UK regulated banks from January 2018 subject to

review in 2017.

New liquidity ratios:

o Intraday liquidity risk reporting will commence in 01st July 2015 and will be required on a

quarterly basis.

o Additional Liquidity Monitoring Metrics (ALMM) reporting will commence 01st July 2015.

The BCBS also published revised Pillar 3 disclosure requirements in January 2015 and these are planned to

take effect by year-end 2016.

Location and verification

The Pillar 3 disclosures for the consolidated group and its subsidiaries are located on the BHF Kleinwort

Benson website and can be accessed via the following link

http://www.bhfkleinwortbenson.com/investor-information/financial-information/financial-reports-presentations/other-

reports?year=2014

The disclosures are not subject to external audit and do not form part of BHF Kleinwort Benson Groups

financial statements.

BHF Kleinwort Benson

13

3. Governance and Risk Management

BHF Kleinwort Benson Group SA

The Group is a focused financial services business with principal activities in private banking and wealth

management, asset management and financial markets & corporates. These complementary businesses

are offered by various businesses:

Private banking and wealth management are offered by KBBL in the UK, KBCIHL in the Channel

Islands and by German-based BHF;

Asset management services are offered by KBI and BHF’s subsidiary Frankfurt Trust;

Financial markets and corporate banking services are mostly provided through BHF.

Through the combined businesses, the Group faces and accepts risks in order to generate returns for its

shareholders. The Group has set strategic objectives and its medium-term performance targets against

following qualitative risk appetite principles:

Maintenance of a strong capital position with sufficient regulatory capital surpluses which are at

the high-end of European peers, set in the context of the prevailing global economic environment,

market conditions, regulatory environment and reflecting the potential impact from several

appropriate stress tests.

Maintenance of a strong liquidity position ensuring that liabilities can be met, even under adverse

business and market conditions. The Company’s approach to liquidity is based on the

maintenance of highly liquid low-risk treasury portfolios and stable funding with limited reliance on

wholesale funding.

Conduct of business in accordance with the highest ethical standards aimed at maintaining an

excellent reputation with clients, employees, regulators and other stakeholders.

The above qualitative principles are translated into risk appetite statements with appropriate risk

tolerance levels and quantitative risk limits defined in comprehensive risk frameworks for each of the

Company’s businesses developed under the responsibility of their respective Board of Directors.

Please refer to the BHF KB’s Strategy and Business Review together with Corporate Governance sections

of the BHF KB’s Annual Report 2014 for further information on The Groups governance.

BHF Bank

BHF’s risk management, measurement and control processes ensure that significant risks are identified at

an early stage, fully evaluated and outlined adequately. The risk management objectives together with

the strategies and processes to manage risks are demonstrated in the diagram below:

BHF Kleinwort Benson

14

Table 5

BHF guarantees the viability and effectiveness of its risk management system through the clear,

functional organisation of its risk management process. As part of this approach, the individual bodies

are assigned clear tasks at strategic level:

The Supervisory Board plays a supervisory role in respect of all measures related to risk mitigation and

management at BHF. It approves the capital allocation proposed by the Board of Managing Directors of

BHF.

The Board of Managing Directors is responsible for proper organisation of the business and its continuous

development. This responsibility comprises (in cooperation with the Risk Committee and the Asset-Liability

Committee) the main activities of overall bank management on the basis of risk reports, overriding limit

concepts and risk-bearing capacity. This includes a clear definition of the strategies, the transaction

types, as well as the acceptable and unacceptable risks.

The members of the Board of Managing Directors in charge of finance and credit risk management bear

the responsibility for the risk management and control processes in relation to the risks entered into by

BHF.

The Risk Committee establishes the risk profile of BHF for the individual risk types within the framework of

the strategies determined by the Board of Managing Directors, for example, by volume and structure

control (achieved among other things by setting limits in the context of monitoring and limiting

concentration risks), by the establishment of risk management parameters and methods and by

determining measures to ensure ongoing compliance with internal and external guidelines.

The Asset Liability Committee (ALCO) of BHF assumes all responsibilities that exist in relation to the liquidity

management of the Bank and the Group. The ALCO ensures the liquidity position of BHF is efficiently

managed, that appropriate processes and guidelines exist for monitoring and limiting risks, and that

sufficient resources are available for evaluating and controlling the risks.

At BHF, the Head of Corporate finance carries out the risk controlling function pursuant to MaRisk AT 4.4.1,

which is responsible for the independent monitoring and communication of risks. It operates independent

of the market units and reports solely to the member of the Board of Managing Directors responsible for

finance. Its tasks, supported by the Risk Control department, include in particular:

- supporting the management in all risk-policy matters, especially in the development and

implementation of the risk strategy and in the design of a system for limiting risks,

BHF Kleinwort Benson

15

- implementing the risk inventory and creation of the overall risk profile,

- supporting management in the establishment and development of risk management and

control processes,

- establishing and developing a system of risk indicators and an early risk detection process,

- ongoing monitoring of the risk situation of the institution and the risk-bearing capacity as well

as compliance with established risk limits,

- preparing regular risk reports for management,

- assuming responsibility for the processes involved in the immediate forwarding to the

management, the responsible party and, where appropriate, the internal audit department

of information that is material in terms of risk.

As part of their risk control function, the Head of Corporate Finance has access to all information

necessary to perform his/her duties and is involved in all important risk-policy decisions.

The risk management and control processes ensure that material risks are identified at an early stage,

comprehensively recorded and mapped in an appropriate manner. The risk management and control

processes are adjusted promptly to take account of changing conditions. Interactions between the

various types of risk are taken into account where relevant and material.

Corporate Finance and Credit Risk Management submit a risk report to the Risk Committee, the Board of

Managing Directors and the Risk and Audit Committee of the Supervisory Board takes place at regular

intervals, but at least quarterly. This reporting also forms the basis for the presentation of risk data to the

supervisory authorities and rating agencies.

This comprehensive risk reporting, which includes appropriate stress tests and scenario analyses, ensures

that regular monitoring of all significant risks, especially in the lending and trading business, and taking

into account risk/return considerations, takes place both at the individual transaction level and at

portfolio level, and that appropriate control measures can be implemented at an early stage, if

necessary.

The comprehensive approach to risk management at BHF also guarantees timely and recipient-based

forwarding of all relevant information through appropriate measures. Defined communication channels

and corresponding information events ensure there is a regular exchange of information between those

involved in the various corporate divisions with respect to strategies, objectives and risks, in order to

prevent an accumulation of individual risks or the combination of risks that would lead to a risk that

threatens the existence of the company.

Ad hoc reporting includes the immediate forwarding to the responsible party of information that is

material in terms of risk (e.g. claims, relevant defects, specific suspicions of irregularities). In addition, the

involvement of Group Operational Risk Control is required in the event of claims or operational risks; it

informs the Board member responsible for risk controlling and the internal audit department to ensure

that appropriate measures or audit procedures can be initiated at an early stage.

The Management Information System (MIS) of BHF serves as the central strategic control, information and

early warning system. This enables the simultaneous description of profitability, its underlying value drivers

and the risks on the basis of both regulatory and economic risk measures. As part of the MIS reporting,

management and other decision-makers are provided with all information relevant to controlling on a

monthly basis, taking into account risk/return considerations. The control of BHF is subject to various

conditions. The most important conditions are the core and total capital ratio in accordance with CRR

and compliance with economic risk limits

The Board of Managing Directors of BHF has a business strategy and a consistent overall risk strategy,

including complementary sub-risk strategies adopted as frameworks for the BHF Group’s risk policy

orientation.

BHF Kleinwort Benson

16

The overall risk strategy defines, amongst other things, the individual risk types classified as material and

establishes the framework for dealing with these risks in the context of the risk-bearing capacity concept.

Specifically, the following points are defined and substantiated:

- the types of risk that are material for the Bank,

- the risk-bearing capacity concept,

- the transactions that can be executed,

- the regulations on activities in new products or in new markets,

- the procedures for risk assessment,

- the risk monitoring and communication in the context of risk reporting,

- the tasks of the internal audit department,

- the general conditions for the outsourcing of business activities,

- the requirements for organisational guidelines and for documentation and

- the information on the personnel and technical resources in the BHF Group.

The overall risk strategy is complemented by the individual sub-risk strategies for credit risk, market risk,

liquidity risk, operational risk, investment risk, business risk and reputational risk.

In its sub-risk strategy for credit risk, the Bank has laid down the conditions for entering into, monitoring,

controlling and reporting with respect to this type of risk. Under this strategy, the prerequisites for the

execution of credit transactions in BHF include, amongst others, the understanding of the transaction and

an individual assessment of the customer’s creditworthiness, including the establishment of risk-

appropriate conditions. The credit risk strategy also includes provisions for the identification and limitation

of risk concentrations.

The market risk strategy describes the fungible products and the related business objectives associated

with entering into market risks. In addition, the principles of market risk management, limit setting and

monitoring, including the principles of quantification of market risks, are defined.

In accordance with its liquidity risk strategy BHF pursues conservative liquidity management in order to

ensure that sufficient liquidity is always maintained within the BHF Group. The liquidity risk strategy

describes in detail the methods used to manage and measure liquidity risk, the main committees and the

contents of the regular reports.

In its sub-risk strategy for operational risks, the Bank defines the principles for the management and

limitation of operational risks. These include the definition of clear roles and responsibilities within the

framework of risk management. One principle of the sub-risk strategy is the emphasis on maintaining the

good reputation of the BHF Group in all business activities.

Risk management for investment risks (-> investment risk strategy) takes place at different levels. All

affiliated companies that are included in the consolidated financial statements are included in the

management information system (MIS) reports in order to ensure ongoing monitoring of business

developments. Moreover, the Corporate Development & Investment department regularly collects and

prepares information on investments. A monthly review of the recoverability of the carrying amounts of

investments is conducted on this basis.

The management of business risk (-> business risk strategy) is based on a qualitative approach through

regular reporting of results to the Board of Managing Directors and other stakeholders.

The information on value drivers, in particular income and expense margins, in the management

information system supports the identification, assessment and control of business risks.

BHF Kleinwort Benson

17

Besides monitoring and reporting, the Bank states in its sub-risk strategy for investment risks that

investments may be made for strategic reasons, for the provision of internal services or as compulsory

investments. The acquisition and disposal of investments may only be made with the approval of the

Board of Managing Directors. If the amount of the investment exceeds EUR 5 million, the Supervisory

Board also has to approve the acquisition or disposal.

The objective of BHF’s Group-wide risk management and early warning system is to ensure that losses

from the risks entered into at no time exceed the risk-bearing capacity in a liquidation approach. To this

end, the sum of the risk capital requirements for the risk types included in the risk-bearing capacity

(counterparty risk (credit risk), market risk, investment risk, operational risk and business risk) is compared

with the risk capital allocated to the individual business areas and portfolios. In parallel, the risk-bearing

capacity is also determined quarterly from a going-concern perspective as part of the risk reporting at

the overall bank level. A traffic light system is used in both control areas, which depicts limit utilisation at

an early stage.

Table 6

The adequacy of the methods used to assess the risk-bearing capacity is reviewed annually by the Risk

Controlling Department and the assumptions underlying them are justified in a clear manner.

The risk coverage is determined on a quarterly basis on the dates of the risk report. The allocated risk

capital as a percentage of the risk cover represents the potential amount of risks that can be entered

into in business activities. The calculation of risk coverage is oriented toward the balance sheet and profit

and loss and is based on the total IFRS equity of the BHF Group and the long-term, subordinated liabilities,

taking into account various deductions that are shown in the table below. In this way, the Bank takes into

account the fact that these deductible items will very likely not be available in the event of liquidation.

BHF has introduced a traffic light system with defined escalation measures in order to monitor and ensure

the risk-bearing capacity. One criterion within the traffic light concept considers the ratio of economic

capital to the IFRS capital. At the reporting date this ratio was 75%.

The risk assessment for counterparty risks and market risk is carried out on the basis of value-at-risk (VaR)

concepts and stress tests. For the other types of risk included in the risk-bearing capacity concept, the risk

utilisation is determined using indicator-based measurement methods.

BHF uses the depiction of risk-adjusted profitability ratios in the Management Information System to ensure

that the risk inherent in the business activities is taken into account in its control and monitoring processes.

BHF Bank

Risk bearing capacity and utilisation

2014 2013 Variance

€m €m €m

Available risk capital to cover assets 617.5 601.3 16.2

Free risk capital to not be quantified or allocated to risks (inc capital buffer) -177.5 -161.3 -16.2

Risk capital available for allocation (inc capital buffer) 440.0 440.0 0.0

Capital buffer -2.6 0.0 -2.6

Risk capital available for allocation (excl capital buffer) 437.4 440.0 -2.6

Risk capital utilised (Amount) 365.7 352.0 13.7

Risk capital utilised (%) 83.6% 80.0% 3.6%

Risk capital to cover for default risk 35.7 34.5 1.2

For individual impairment 20.5 21.4 -0.9

For collective impairment 15.2 13.1 2.1

Accruals for provisions 12.2 12.8 -0.6

BHF Kleinwort Benson

18

The Bank allocates risk capital to the individual sub-segments, portfolios and risk types and carries out its

controlling using risk-adjusted profitability indicators; the objectives of this approach are to limit risks to a

total amount that is consistent with the business strategy, to limit risk concentrations in a targeted way

and to maintain sufficient capital even in worst-case assumptions, transparency with regard to the level

of risks entered into by the individual sub-segments, the effective use of risk capital through the individual

sub-segments and the linking of risk management and overall bank management.

Table 7

The risk-bearing capacity is calculated quarterly and shown in the risk reports. The responsibility for this lies

with the Risk Control department of the Corporate Finance department.

BHF applies risk-reducing diversification effects (resulting from the correlation between the risk types) to

aggregate the individual risk contributions. The calculation of correlations is based on the Bank’s internal

time series and has an overall conservative orientation, as the correlations are determined based on

maximum values with respect to different timeframes. The final correlation values are determined using

the statistical bootstrapping method as the 95% percentile of the bootstrapping distribution.

In the event limits are exceeded, the Bank has processes in place to ensure an immediate reduction of

the limit utilisation. The possible measures include risk-reducing transactions, the redistribution of risk

capital set aside for the specific risk type within the sub-segments or portfolios and the distribution of a

capital buffer. Risk controlling is responsible for the monitoring of compliance with the limits that have

been set and informs the Board of Managing Directors if the limits are exceeded.

The Bank uses an emergency plan in the event of extremely unfavourable markets and heavy daily

losses, which may lead to limits being exceeded due to the utilisation of market risk limits. In this context,

the Bank uses an escalation process based on a traffic light concept, which should ensure an adequate

response in such a scenario and guarantee that risks can be reduced within one month. This applies in

particular to market risks arising from products that can be completely removed only by selling the

products. No escalation was required in the reporting year.

AT 4.1 item 9 MaRisk, in the version dated 14 December 2012, requires institutions to have a process of

planning for future capital requirements. The planning horizon should include a reasonably long, multi-

year period. According to the accompanying letter from BaFin dated 17 December 2012 on the MaRisk

BHF Bank

Risk bearing capacity and utilisation

Tota

l

Priva

te

Ba

nk

ing

Ass

et

Ma

na

ge

me

nt

Co

rpo

rate

s

Fin

an

cia

l

Ma

rke

ts

Inte

rna

l

ac

co

un

ts

Pe

nsi

on

s

Oth

ers

€m €m €m €m €m €m €m €m

Credit Risk 183.5 5.5 0.0 148.6 24.2 1.0 4.2 0.0

Market Risk 133.9 1.9 0.0 1.0 100.0 2.0 30.2 -1.2

Counterparty Risk 70.2 10.5 5.0 25.0 1.0 30.6 0.0 -1.9

Business Risk 49.1 13.4 4.0 5.0 7.9 18.8 0.0 0.0

Operational Risk 37.0 14.5 5.0 6.8 9.0 1.8 0.0 0.0

Diversification and Capital deductions -36.3 -3.0 -0.8 -13.4 -5.7 -0.8 -0.8 0.0

437.4 42.8 13.2 173.0 136.4 53.4 33.6 -3.1

Capital buffer 2.6

BHF Bank available risk capital 440.0

Risk capital utilised (Amount) 365.7 35.0 12.7 153.9 96.1 49.9 29.3

Risk capital utilised (%) 83.6% 81.8% 96.2% 89.0% 70.5% 93.4% 87.2% 0.0%

Risk capital utilised (%) Previous year 80.0% 88.4% 91.4% 84.4% 67.3% 90.4% 77.0% 0.0%

Risk capital available for allocation (excl

capital buffer)

BHF Kleinwort Benson

19

amendment, both internal and regulatory capital requirements must be determined. To do so, based on

its business plan BHF calculated the future development of its equity at the Group level and the

regulatory capital for the period 2015-2018, including taking into account a stress effect to identify

possible future capital requirements at an early stage and to take countermeasures.

Kleinwort Benson

Kleinwort Benson is the combination of KBBL, KBCIHL and KBI.

KBBL and KBCIHL are the Private Banking entities of Kleinwort Benson and form Kleinwort Benson Wealth

Management (“KBWM”). KBI is the Asset Management arm of Kleinwort Benson.

KBBL, KBCIHL and KBI are wholly owned subsidiaries of KBG as shown in the organisational chart in table 2

of this Pillar 3 disclosure report.

Kleinwort Benson Wealth Management (“KBWM”)

KBWM has a vision statement to provide a compelling relationship driven proposition to clients through a

focused high quality offering and state-of-the-art execution. KBWM reviews its business strategy annually

and it is presented to the KBBL and KBCIHL Boards for approval.

To achieve the strategy KBWM maintains a Risk Appetite and Framework (“The Risk Framework”) which is

approved by the KBBL and KBCIHL Management Committee and Strategic Risk Committee before being

approved by the Boards of KBBL, KBCIHL and KBCIL.

The Risk Framework sets out a comprehensive framework of high level limits to control key risks facing the

business but aligned to achieving the overall business strategy.

KBWM has a Treasury and Financial Risks Management Policy (T&FRMP) document which is an

overarching risk management framework. This document complements the Risk Framework setting out

strategies, policies and how to manage the risks within the business and stay within the risk appetite. This

document consists of the following key components:

The Board’s articulation of Kleinwort Benson Wealth Management‘s strategy and direction together

with the associated risk appetite. This is complemented by targets and risk limits set by executive

committees.

Clear roles, responsibilities, reporting lines, committees and mandates exist to achieve the strategy.

A comprehensive set of risk policies, processes and control procedures in place to provide bedrock

for an effective control environment.

Comprehensive and timely management reporting of risk exposures for decision making or

mitigating potential risk on the horizon.

BHF Kleinwort Benson

20

The following diagram illustrates how the KBWM Strategic review flows into the T&FRMP and the

underlying policies and procedures.

Table 8

Updated Risk Appetite

Business Strategy

Updated Risk Limits

Treasury Strategy

Treasury and Financial Risks

Management Policy

Market Risk

Interest Rate

Risk in

Banking Book

Liquidity Risk Operational

Risk

Credit and

Counterparty

Risk

Strategic Review

External Factors / Clients Needs/ Core Values / Internal Objectives/ Current Risk Appetite

Policies / Procedures / Limits

BHF Kleinwort Benson

21

The following diagram sets out the high level Board and Committee structure. It excludes details of

boards for subsidiary companies wholly owned by KBBL and KBCIHL.

Table 9

Strategic Risk Committee

The Strategic Risk Committee has responsibility for recommending The Risk Framework and overall Risk

Appetite to the boards of KBWM and their subsidiaries and considers how the external environment may

impact the current and future strategy of the businesses. The Committee consists of at least three

members, the majority of whom are independent non-executive directors and meets at least three times

per annum.

Nomination and Remuneration Committee

The Nomination and Remuneration Committee reviews the structure, size, function and composition of

the Kleinwort Benson Boards, having regard to gender representations, and makes recommendations to

the appropriate Kleinwort Benson Boards in relation to any changes deemed necessary, including the

identification and nomination of candidates for the approval of the appropriate Kleinwort Benson

Boards.

The Nomination and Remuneration Committee agrees with the Kleinwort Benson Boards and, as

appropriate, subsidiary company boards a general remuneration policy for the executive directors and

officers of Kleinwort Benson and/or subsidiary company and a group policy for other members of staff,

ensuring that they meet any legal and regulatory requirements.

In line with local regulations and guidance, KBI also has its own Remuneration Committee.

Audit Committee

The Audit Committee advises the board on meeting its external financial reporting obligations and

provides advice and guidance on all matters relating to internal and external audit, together with the

internal control systems of KBWM.

Kleinwort Benson

Nomination and

Remuneration

Committee

Kleinwort Benson

Strategic Risk

Committee

Kleinwort Benson

Audit Committee

Kleinwort Benson

Investors Dublin

Limited

Kleinwort Benson

Group Limited

Offshore

Management

Committee

EXCO

Client

Sub-Group

Management

Committee

Kleinwort Benson

Channel Islands

Holdings Limited

Kleinwort Benson

Bank Limited

BHF-BANK A.G.

BHF Kleinwort Benson

22

Management Committee

The Management Committee of KBWM has been given delegated authority for strategy and operational

management. The Committees primary responsibilities are to:

Define, recommend to the boards and promote Kleinwort Benson’s strategy, business plans and

annual budget

Set targets and goals across the business areas; and

Monitor performance against the strategic objectives and targets.

Alongside the Management Committee, the Offshore Management Committee independently

considers any group-wide policy, committee terms of reference or other material proposal regarding the

business strategy, management, operations and performance of the non-UK businesses and considers

whether or how it should be implemented having taken account of the legal and regulatory

requirements relating to the business carried out by KBCIHL and its subsidiaries.

The Management Committee has established the following sub-committees:

Table 10

Risk ManagementChange Management

CEO

Taskforce

Project

Board

CEO

Taskforce

Project

Board

Risk and

Compliance

Committee

Asset and

Liability

Management

Committee

Credit

Committee

New Products

and

Instruments

Committee

Management

Committee

Change Board

Cash

Management

Committee

Reputational

Risk

Committee

Policy

Committee

BHF Kleinwort Benson

23

The responsibilities of each of these committees are detailed in the table below:

Table 11

The KBWM Boards are firmly committed to sound and prudent risk management practices, given the

importance of such practices to achieving The Group’s strategic objectives. In line with its ordinary

activities, KBWM is exposed to a number of risks. KBWM has embedded a robust risk process into its risk

management practise. The firm has a five step approach to risk management as detailed in the following

diagram:

Committee Specific Responsibilities

Asset and Liability

Management

Committee

Monitoring liquidity and capital and determining the investment

policy for the treasury assets in the context of KBBL’s strategy and

market conditions

Cash Management

Committee

The design of and monitoring performance against the risk

framework around the product, “Kleinwort Benson Cash

Management Service.”

Change Board Monitoring progress with change projects and setting priorities.

Approving counterparty limits and investment grade rated credit

applications.

Considering the allowable non-property collateral

New Products and

Instruments Committee

Reviewing existing and proposed products, services and

instruments.

Monitoring compliance, risk and control issues across the business

and determining market risk limits.

Monitoring the adequacy of the performance of outsourcers

providing Credit, IT and Operational services

Reputational Risk

Committee

Determines the reputational risk appetite in relation to client or

business opportunities

Policy Committee

Responsible for the policy framework across the group, including

the review, recommendation and, in certain circumstances,

approval of policies

Credit Committee

Risk and Compliance

Committee

BHF Kleinwort Benson

24

Table 12

Risk Identification

This is the identification of all risks which could have a material impact on the operation of the business

and/or the achievement of the business’s strategy and objectives.

KBWM control functions undertake assessments in specialist areas, incorporating external drivers, e.g. new

legislation, to assist in risk identification. The internal audit, external audit, compliance and risk monitoring

processes, the business change process and the due diligence process also highlight new risks.

Regular internal business meetings also assist in risk identification, and new risks may be identified through

analysis of root causes of other (related) risks. Risk identification includes risks that are both internal and

which are caused by factors external to the firm.

Risk Assessment

The objective of risk assessment is to develop an understanding of each risk, including cause, potential

likelihood of occurrence and the impact on the business. The firm uses an impact v likelihood matrix to

quantify and prioritise the risk on the basis of financial, operational, reputational, and other loss

categories.

Risk Management

The risk management or risk mitigation process requires Kleinwort Benson to identify a range of options

around managing individual risks. Once agreed, this is then followed by mitigation planning and

implementation.

Risk Identif ication

Risk Assurance

Risk Management

Risk Reporting

Risk Monitoring

Risk

Culture

BHF Kleinwort Benson

25

Overall risk management strategy options include, but are not limited to:

Table 13

Risk reporting and Management Information

KBWM identifies and captures a wide range of information concerning events and activities, both internal

and external, that is relevant to achieving the strategic business aims of KBWM.

Providing the appropriate level of information to the relevant business and function heads, at the right

time enables KBWM to be better informed of the risks faced, as well as providing effective monitoring of

the key risks within KBWM.

Information is gathered centrally through a variety of business as usual mechanisms including, as new risks

on risk registers, as incidents occur, through local self-assessments, internal audit, external audit, post-

incident assessments and general risk reviews.

MitigationImplementation of new or revised policies and processes to ensure the risk is mitigated to

an appropriate level.

SharingRisk is reduced or spread across the organisation or external parties sharing risk, through

such sources as subcontracting, outsourcing or entering into partnerships or joint ventures

Avoidance By performing or not performing an action which prevents an initial risk materialising

Can be achieved through external assurance (ie insurance) or parental guarantees, use of

credit derivatives, selling positions or portfolios and use of collateral

In some cases the firm recognises that the risk exists and accepts it to accomplish business

objectives.

Acceptance In some cases the firm recognises that the risk exists and accepts it to accomplish business

objectives.

Risk Management Strategy Options

Transfer

BHF Kleinwort Benson

26

The following table provides an overview of the key management information provided to the Boards

and various committees which enable KBWM to manage it’s financial and risk exposures and mitigate or

take correcting actions for potential risks that may be on the horizon.

Table 14

KBI

The governance structure within KBI provides a clear overview of the basic principles of KBI’s risk

governance, the roles and responsibilities of each of the KBI Board and the various KBI Board sub-

committees, e.g. the Executive Committee and KBID Audit Committee and its decision making policies.

From a solvency risk perspective KBI’s capital is managed within this governance framework taking into

account the relevant regulatory requirements with which the KBI Board and subsidiary boards must

comply. There are regular checks and reviews of its adequacy to mitigate against such risk.

KBBL & KBCIHL

Boards

Strategic Risk

Committee

Asset & Liabilitee

Committee

Risk and

Compliance

Committee Credit Committee

Minimum three

meetings

per annum

Minimum three

meetings

per annum

Monthly Meetings Minimum nine

meetings

per annum

Quarterly meetings

Financial update Chief Risk Officer’s

report

Treasury portfolio

status and market

conditions

Compliance

breaches

Credit approvals

Strategic update Market conditions

and trends report

Balance sheets Regulatory findings

/ interactions

Loan book and

analysis

Capital status Liquidity report Margins Complaints Client ‘Watch List’

Liquidity status Lending report Capital position Major risk events Provisions and

losses against loans

Risk Appetite

(annually or on

change)

Risk Appetite

(annually or on

change)

Liquidity position Key risks per

business area

Regulatory issues

(where necessary)

Exceptions to Risk

Appetite

Exceptions to Risk

Appetite

Counterparty

exposure

Major initiatives Audit findings

(where necessary)

Strategic Risk

Committee report

Market Risks

exposure

Key risk indicators

for top enterprise

risks (quarterly)

Audit Committee

report

Compliance

Assurance status

and progress

against findings

Nomination and

Remuneration

Committee report

Internal Audit

status and progress

against findings

TCF/Conduct risk

metrics/report

BHF Kleinwort Benson

27

The chart below gives an overview of the KBI governance structure including sub-committees:

Table 15

The KBI Board

The KBI Board has adopted Principles of Corporate Governance, which provide an effective corporate

governance framework for KBI. The KBI Board meets at least on a quarterly basis and more frequently if

required. It is responsible for:

Setting the strategic goals of the company and for the overall oversight and supervision of the

affairs of the company;

Defining and documenting the risk strategy and the capital planning of the company;

Supporting the internal development of risk awareness within the organisation;

Delegating and overseeing the implementation of the ICAAP to the Executive Committee;

Approving the risk and capital policies as set out by the Executive Committee;

Delegating and overseeing the risk management function; and

Approving on a regular basis the risk and capital management processes of the company through

regular reporting by the Executive Committee.

The KBI Board maintains the following committees to assist in discharging its oversight responsibilities:

Remuneration Committee

Audit Committee

Executive Committee

Remuneration Committee

The Remuneration Committee advises and supports the Board in developing and managing a coherent,

fair and responsible remuneration policy aligned to the business strategy and the interests of relevant

stakeholders, and will oversee its implementation in a manner that does not encourage excessive risk-

taking.

Risk Committee IT Steering

Committee

Pricing

Committee

Audit

Committee

KBI Board of

Directors

Executive

Committee

Remuneration

Committee

Business

Continuity

Management

Committee

BHF Kleinwort Benson

28

Audit Committee

The Audit Committee assists the Board of Directors and does this by supervising on behalf of the Board,

the integrity, efficiency and effectiveness of risk management and the internal control measures in place,

paying special attention to correct financial reporting. The Audit Committee also oversees the

company’s processes to secure compliance with laws and regulations.

Executive Committee

The Executive Committee implements the strategies, policies and decisions of the Board and manages

the company and its subsidiaries from a day-to-day perspective. It is responsible for managing the

business and affairs of the company and for the leadership and operational management of the

company.

The Executive Committee maintains the following sub-committees to assist it in discharging its oversight

responsibilities:

Risk Committee

IT Steering Committee

Pricing Committee

Business Continuity Management Committee

BHF Kleinwort Benson

29

4. Assessment of Group’s Risk Mitigation Policies and

Assumptions

Risk appetite

The Group and its subsidiaries have a comprehensive and conservative medium-term plan which sets out

a three year strategy to manage the business in the face of the changing economic environment.

BHF KB sets its qualitative risk appetite principles that are then translated into a risk appetite statement for

each of the business units as explained in section three of this Pillar 3 document.

BHF has clearly defined its risk appetite as part if its business and risk strategy. The framework for this

appetite is set by BHF’s low-risk business model as such. The outcome of this process is as follows:

With respect to pillar 1 requests, BHF’s significantly high tier 1 and total capital ratios underline its

degree of risk-awareness.

With respect to ICAAP (pillar 2), the risk appetite is given by a set of buffers (i. e. only a part of the

adjusted own funds is allocated as risk capital) and consistent risk limits.

KBWM adopts a Risk Appetite and Framework (“The Risk Framework”) which is explained in section three

of this Pillar 3 document that is approved by the Boards. This is a comprehensive document which outlines

the nature and quantum of risk KBWM is prepared to tolerate in the process of achieving its strategic and