Embed Size (px)

Citation preview

Tourism Corporation of Gujarat Limited

Block No. 16-17,

4th Floor, Udhyog Bhavan, Gandhinagar- 382 011

Phone: +91 79 23977211

Email ID: [email protected]

SELECTION OF CA FIRM FOR GST

CONSULTANCY, SOFTWARE DESIGNING &

HAND HOLDING, TRAINING TO STAFF OF TCGL

2

Disclaimer

The information contained in this request for proposal document (the “RFP”) or

subsequently provided to applicant(s), whether verbally or in documentary or any other

form, by or on behalf of the Tourism Corporation of Gujarat Ltd. (hereinafter referred to

as “TCGL”) or any of its employees or advisors, is provided to applicant(s) on the terms

and conditions set out in this RFP and such other terms and conditions subject to which

such information is provided.

This RFP is not an agreement and is neither an offer nor invitation by the TCGL to the

prospective Applicants or any other person. The purpose of this RFP is to provide

interested parties with information that may be useful in formulation of their application

for qualification and thus selection pursuant to this RFP (the “Application”). This RFP

includes statements, which reflects various assumptions and assessments arrived at by

the TCGL in relation to the event. Such assumptions, assessments and statements do not

purport to contain all the information that each Applicant may require. This RFP may not

be appropriate for all persons, and it is not possible for the TCGL, its employees or

advisors to consider the objectives, financial situation and particular needs of each party

who reads or uses this RFP. The assumptions, assessments, statements and

information contained in this RFP may not be complete, accurate, adequate or correct.

Each Applicant should therefore, conduct its own investigations and analysis and should

check the accuracy, adequacy, correctness, reliability and completeness of the

assumptions, assessments, statements and information contained in this RFP and obtain

independent advice from appropriate sources.

Information provided in this RFP to the Applicant(s) is on a wide range of matters, some

of which may depend upon interpretation of law. The information given is not intended to

be an exhaustive account of statutory requirements and should not be regarded as a

complete or authoritative statement of law. TCGL accepts no responsibility for the

accuracy or otherwise for any interpretation or opinion on law expressed herein.

TCGL, its employees and advisors make no representation or warranty and shall

have no liability to any person, including any Applicant or Bidder, under any law, statute,

rules or regulations or tort, principles of restitution or unjust enrichment or otherwise for

any loss, damages, cost or expense which may arise from or be incurred or suffered on

account of anything contained in this RFP or otherwise, including the accuracy,

adequacy, correctness, completeness or reliability of the RFP and any

assessment, assumption, statement or information contained therein or deemed to

form part of this RFP or arising in any way with selection of Applicants for

participation in the Bidding Process.

TCGL also accepts no liability of any nature whether resulting from negligence or

otherwise howsoever caused arising from reliance of any Applicant upon the statements

contained in this RFP. TCGL may, in its absolute discretion but without being under any

obligation to do so, update, amend or supplement the information, assessment or

assumptions contained in this RFP. The issue of this RFP does not imply that the TCGL is

bound to select and shortlist Applications and TCGL reserves the right to reject all or any

of the Applications or Bids without assigning any reasons whatsoever. The Applicant shall

bear all its costs associated with or relating to the preparation and submission of its

Application including but not limited to preparation, copying, postage, delivery fees,

expenses associated with any demonstrations or presentations which may be required by

TCGL or any other costs incurred in connection with or relating to its Application. All such

costs and expenses will remain with the Applicant and TCGL shall not be liable in any

manner whatsoever for the same or for any other costs or other expenses incurred by

an Applicant in preparation or submission of the Application, regardless of the

conduct or outcome of the Bidding Process.

3

Notification for Request of Proposal

To,

All Prospective Bidders

Sub: “Selection of Chartered Accountant Firm for GST Consultancy, Designing

Invoice Booking Software for All Properties of TCGL and Providing Training to Staff

of Tourism Corporation of Gujarat Limited”

Sir,

Tourism Corporation of Gujarat Limited (TCGL) invites proposals for “Selection of

Chartered Accountant Firm for GST Consultancy, Designing Invoice Booking

Software for All Properties of TCGL and Providing Training to Staff of Tourism

Corporation of Gujarat Limited”

The Background Information and Terms of Reference of the proposal are provided in

Chapter 2 of the Request for Proposal (RFP). This RFP is available to all eligible

Chartered Accountant Firms involved in accounting and financial management services.

A firm will be selected under Least Cost Method (LCS) and procedures described in this

RFP, in accordance with the policies of the Govt. of Gujarat.

The RFP includes the following documents:

Chapter 1 – Datasheet

Chapter 2 – Terms of Reference

Chapter 3 – Instruction to bidders

Chapter 4 – Submission & Evaluation of the Proposal

Chapter 5 – Technical & Financial Submission Forms

TCGL reserves the right to accept or reject any or all proposals, and to annul the

selection process and reject all proposals at any time prior to the award of contract,

without thereby incurring any liability or any obligation in any form to the affected firms

on any grounds.

Managing Director Tourism Corporation Gujarat Limited Block No.16-17, 4th Floor, Udhyog Bhavan,

Gandhinagar – 382 011

4

Chapter 1 Data Sheet

S.N. Information to Bidders

1 Name of the Client: Tourism Corporation of Gujarat Ltd. (TCGL), Govt. of

Gujarat (GoG)

Name of the Assignment: “Selection of Chartered Accountant Firm for

GST Consultancy, Designing Invoice Booking Software for All Properties of

TCGL and Providing Training to Staff of Tourism Corporation of Gujarat

Limited”

Details on the services to be provided: As Mentioned in Terms of

Reference (ToR) under Chapter 2 of the RFP.

2 Financial Proposal to be submitted Online only: Yes (To be submitted on

(n) Procure )

3 There shall be a Pre-bid Meeting as under: - Date and Time: 09-09-2019 at

3.00 pm.

Venue: Tourism Corporation of Gujarat Limited Office

The address for requesting clarifications is:

Managing Director

Block No.16-17, 4th Floor,

Udhyog Bhavan,

Gandhinagar – 382 011

Contact Person: Mr. Vindod Bhardarka

Ph: - +91 79 2397 7211

Email: [email protected]

4 Proposals must remain valid for 90 days from the submission date.

5 Earnest Money Deposit (EMD) amount is Rs. 1,00,000/- (One Lakh Rupees

only) and Bid Processing Fees is Rs. 2,500/- (Two Thousand Five Hundred

Rupees) in the form of Demand Draft in favour of “Tourism Corporation

of Gujarat Limited.” payable at Gandhinagar

6 Consortium and Joint Ventures with other firms for this assignment are NOT

permitted.

7 Under this contract the payments for the services of Chartered Accountants Firm

will be made as per the Terms of Reference (ToR). It is expected that Firm will

quote its fee after considering all requirements for satisfactory performance of the

services specified in this ToR.

8 Amounts payable by TCGL to the firm under the contract shall be subjected to

local taxes if any. The TCGL will pay GST, on prevailing rates as applicable on

the consultancy charges.

9 Proposals Physically must be submitted not later than the following date and

time:

Date: 16-09-2019, Time: up to 5.00 pm.

5

10 Eligibility Criteria: As mentioned in the ToR- Chapter 2

11 Evaluation Criteria: Technical Proposals shall be evaluated on the basis of the

criteria provided the RFP (refer to Chapter 2 & 4).

12 Method of selection: The selection is based on Least Cost Method (LCS) and

further details on the evaluation process are specified in Chapter 4.

13 Expected date for commencement of services: ----------------------------

14 The duration of the assignment: Initially for the period of Three Years and it

can be extendable for the further period of Two years depending on Performance.

The annual performance evaluation would be carried out by the TCGL at the end

of every 12 months and the continuation of its services shall be subject to

satisfactory performance of the Firm in the preceding completed 12 months.

Notwithstanding anything contained herein above, TCGL reserves the right to

discontinue the services of Chartered Accountant firm in the event their services

are evaluated as unsatisfactory at any time during the period of contract.

6

Chapter 2: Introduction 2.1 Introduction:

Tourism Corporation of Gujarat Limited is a Company completely belonging to Government of Gujarat established under Companies Act, 1956. This Corporation was established in the year 1975 and the Corporation started its commercial work from 1977-78. The Corporation undertakes commercial and promotional activities for development of tourism industry as Nodal Agency of State Government. As per audited report for the financial year 2017-18 the financial detail of the Corporation is as under:

Authorised Share Capital Rs.20.00 Crore

Paid up Share Capital Rs.19.99 Crore

Total Revenue receipts for the year 2017-18 Rs.97.19 Crore

Expenditure for the year 2017-18 Rs.35.94 Crore

Income tax paid for the year 2017-18 Rs.21.50 Crore

Grant to be received from Government are as under

1. From State Government for the year 2017-18 Rs.448.00 Crore

2. From Central Government for the year 2017-18 Rs.46.04 Crore

3. Other Government Bodies for the year 2017-18 Rs.27.54 Crore

TCGL is having approx. 11 self-run hotels along with fleet of vehicles, while another 17 TIBs (Tourist Information Bureau). Out of 17 TIBs, more than 10 TIBs are located outside Gujarat State. Apart from this, TCGL conducts various Fairs & Festivals, Exhibitions like Statue of Unity, Ranostav etc. List of Hotel Units/Tourist Information Bureau (TIB) Offices:

S.N. State Office Type

1 Gujarat Gandhi Ashram – Ahmedabad Toran Hotel & Restaurant

2 Gujarat Pavagadh Toran Hotel & Restaurant

3 Gujarat Saputara Toran Hotel & Restaurant

4 Gujarat Junagadh Toran Hotel & Restaurant

5 Gujarat Porbandar, Tourist Bunglows Toran Hotel & Restaurant

6 Gujarat Dwarka, Tourist Bunglows Toran Hotel & Restaurant

7 Gujarat Palitana, Hotel Sumeru Toran Hotel & Restaurant

8 Gujarat Vadnagar Toran Hotel & Restaurant

9 Gujarat Narayan Sarovar Toran Hotel & Restaurant

10 Rajasthan Mount Abu Toran Hotel & Restaurant

11 Gujarat Veraval Toran Hotel & Restaurant

12 Gujarat Gandhinagar Sector - 16 Tourist Information Bureau

13 Gujarat H K House – Ahmedabad Tourist Information Bureau

14 Gujarat Vadodara Tourist Information Bureau

15 Gujarat Surat Tourist Information Bureau

7

16 Gujarat Rajkot Tourist Information Bureau

17 Gujarat Bhuj Tourist Information Bureau

18 Rajasthan Jaipur Tourist Information Bureau

19 Maharashtra Mumbai Tourist Information Bureau

20 Tamilnadu Chennai Tourist Information Bureau

21 West Bengal Kolkata Tourist Information Bureau

22 Andhra Pradesh Hydrabad Tourist Information Bureau

23 Uttar Pradesh Lucknow Tourist Information Bureau

24 Karnataka Bengaluru Tourist Information Bureau

25 New Delhi New Delhi Tourist Information Bureau

26 Kerala Kochin Tourist Information Bureau

27 Chhattisgarh Raipur Tourist Information Bureau

28 Bihar Patna Tourist Information Bureau

As hotel business is taxable under GST, TCGL has taken GSTN in respective states. Every TIB accepts hotel booking for their hotels in Gujarat and provide ancillary services like vehicles, tours and specific events. Every TIB avails some GST Credit also on account of services and material received to run their offices. For compliance purpose, TCGL needs to maintain books of accounts, register as per GST at

every TIB office, train their accounting personnel and do return filling and other GST related compliance work. For ease in working, TCGL wants that billing and GST reporting system should be automated to ensure that all compliance has been fulfilled before time.

8

Scope of Work: 1. GST Compliance

A Generation of tax invoices and

i. Calculation of IGST, CGST and SGST liability on monthly basis

ii. Calculation of liability under reverse charge mechanism

iii. Ensure timely and correct calculation and availing of input tax credit

iv. Department representation, if required including assessment

v. Assistance in GST audit

vi. Filling of all returns including GST TDS Return for All units of TCGL

vii. The Consultant would be required to periodically match invoices populated in the GSTR- 2 with the invoices paid/booked in accounts by TCGL and report mismatches in time so that actions to sort out the issues can be initiated and loss of credit can be avoided.

viii. Proposing / recommending tax clauses for future contracts/ agreements in case of any major change in GST law.

ix. Ensure smooth compliances of GST laws applicable to TCGL and suggest changes / remedial action/ system changes where necessary for the entire period of contract

x. To update TCGL about various amendments taking place in GST laws/rules,

regulations, circulars, directions, etc. from time to time (compliance management), for enabling TCGL employees to be GST compliant.

xi. Providing opinion on applicability of GST on TCGL transactions as referred by employees as well as providing clarifications required to address customer complaints/ representations on GST related matters.

xii. Preparing replies to queries raised by GST authorities, statutory auditors, government auditors and internal auditors on time bound manner.

xiii. Provide opinion on applicability of GST TDS and ensure proper deduction from

eligible invoices

xiv. In-case any registration requirement pending then consultant will also help in suitable registration.

xv. Generation of e-way bill, if required

xvi. Generating GST TDS certificate to all vendors

xvii. Conduct GST Audit for All location of TCGL including TIB Offices wherever applicable as per GST Law

xviii. Filing of Annual GST return as per GST law.

xix. Addressing query/ complaint of its vendor on GST matter through email only

xx. Guide/advice for developing necessary tools for review, monitoring, reporting and compliance with report required under GST law

xxi. These GST services will be required at every state offices (Currently offices in 12 states)

xxii. Concerned person will visit state TIB office at least on monthly basis.

xxiii. State TIB office can call selected consultant as and when required

xxiv. No TA, DA separate fees will be paid for such visit

xxv. It is preferred that bidder have their own office in same state where TCGL has its TIB offices.

9

1. GST Compliance

B Automation of GST Process

i. Finalisation of SOP for every process that have impact on GST liability.

ii. Compilation of all register’s template that is required to maintain as per GST act.

iii. Designing of specialized software exclusively for the units of TCGL for standard accounting practices and procedures as per GST Laws.

iv. Designing of specialized software for all units of TCGL for generating Invoice with clear details about the GST.

v. Preparation of MIS report indicating GST liability, input tax credit and net liability.

vi. Necessary changes in the software in line with changes in GST act and applicable

to TCGL.

vii. Ensure integration with GSTN portal and ensure correct upload on return on GST

portal

viii. Conducting training session on how to use software till satisfaction of TCGL’s

personnel.

ix. Remote support during office hours to TCGL employee

x. Data hosting on cloud/ dedicated server provided by TCGL

xi. This software will be provided with perpetual license and free updation will be provided by the consultant during contract period.

xii. However AMC charges will be paid by TCGL that will be 20% of the quoted amount against software and will be paid on annual basis in advance after completion of first year of implementation.

2. Training to Staff of TCGL

A Training and Handholding exercises

i. Every TIB office has its own finance & accounts team that takes care of all sales and routine book keeping. Consultant need to study the entire process at each TIB office separately and provide signed copy of As-is Report.

ii. On the basis of As-is report, consultant will identify scope for BPR (business process re-engineering) and after discussion with state office, will initiate the same.

iii. On each process, separate stakeholder discussion will be held with concerned TIB office and state office and after confirmation of all stakeholder, approved process

will be adopted for further implementation.

iv. In the same line SOPs (Standard operating procedures) will be prepared for each TIB and for each process in every TIB.

v. After completion of SOP, same will be compiled into separate Accounting Process Manual.

vi. Consultant will provide the printed colour hard copy of accounting process manual to every TIB office at its own cost (expected 50 Copy)

vii. Accounting process manual will cover all part of financial management also

viii. On the basis of input and amendments happen in GST and other law applicable on TCGL, consultant will update the manual for one year.

ix. On the basis of final manual, consultant will arrange training session on monthly basis at every TIB offices.

x. Training session should be schedule at every TIB office on same day. In case there

10

is any practical difficulty on accounts of TCGL, timeline of same week should be strictly adhered.

xi. A separate report on training session including training need and evaluation will be submitted to state office.

xii. In such training session local person of the consultant who is responsible for GST compliance should be available in addition to trainer/ subject expert.

xiii. For better experience, consultant may be called upon external faculty however charges for the same will be borne by consultant only.

xiv. In case of external faculty of high repute, a common training session may also be organised after written approval of TCGL. Lodging, boarding of the same will be arranged by TCGL preferably in their own property.

xv. Every training session will be completed with feedback form of the participants that will be part of monthly training report. Format of the same may be agreed in first month of the training with state office.

xvi. For interest of the TCGL, if TCGL’s personnel need training on the other aspects of accounting/ financial management including GST, same should be provided by the consultant without any additional cost.

xvii. Photographs, Power point presentation preferably in common/ local language should

also be part of training report.

xviii. On yearly basis, all training PPT may be compiled into consolidated training manual, that may circulated to every TIB office in soft copy.

xix. Common forum will be created for finance department of each TIB, to maintain such forum and necessary update will be responsibility of the consultant.

xx. Frequently consultant will discuss the outcome of training session with state office and will implement remedial action as agreed in the meeting.

xxi. Minutes of such meeting will be part of next training report.

xxii. If any other type/training to be given to staff of TCGL then Consultant and Officials of TCGL may mutually decide.

Deliverables and timelines: as defined above there are two phases; deliverables of each phase is given as below:

a) Software development

S.N. Deliverables Due date Payment Cycle

1 Designing of Software for Invoice Generation of Bookings

Within 3 month from commencement of work.

1. SRS, UAT testing : 50% of quoted price against software

2. Final deployment and testing for 1 month: 50% of quoted price against

software

2 Designing of SOP for GST Work

Within 3 months

On Monthly basis against deliverable

3 Filing of GST Return Continuous On Monthly basis against

deliverable

4 Training and Guidance to Official of TCGL at Respective Unit/TIBs

Continuous On Monthly basis against deliverable

5 Submission of MIS for

GST Liability

Continuous On Monthly basis against

deliverable

11

b) Monthly compliance and capacity building: Fees will be paid on monthly basis after

submission of necessary reports and acknowledgement of each state office,

however fee will be paid by head office collectively for all TIB.

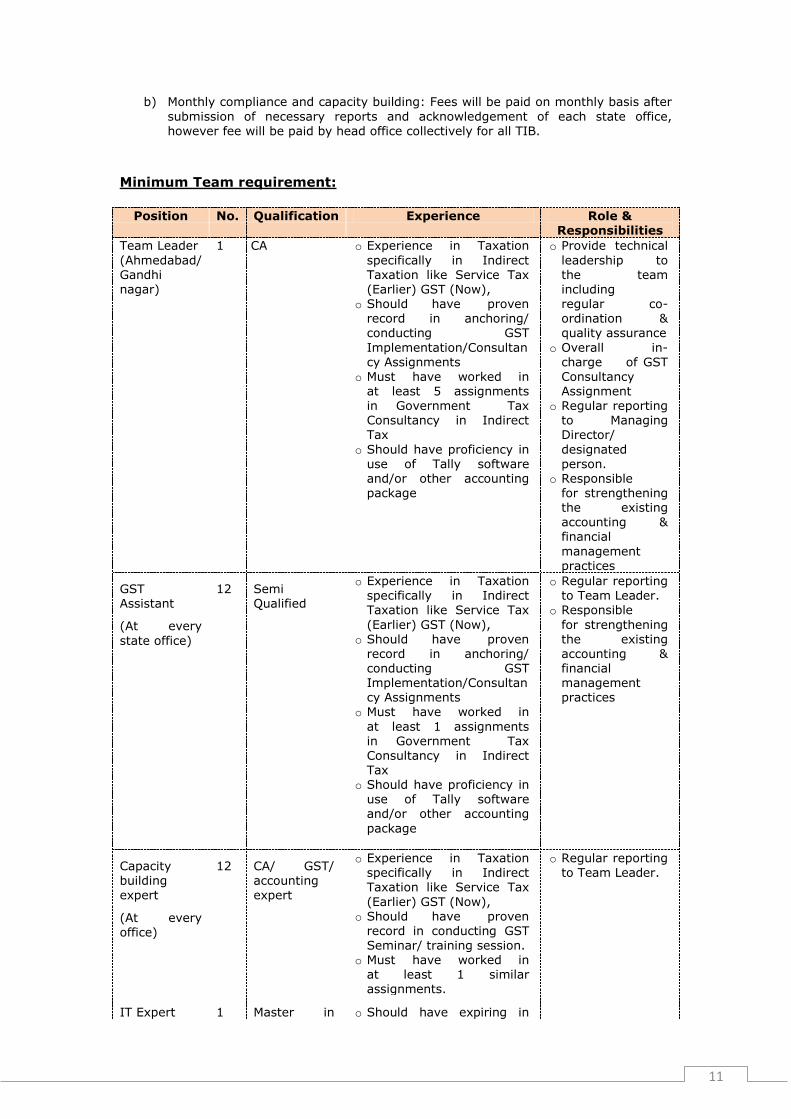

Minimum Team requirement:

Position No. Qualification Experience Role &

Responsibilities

Team Leader

(Ahmedabad/ Gandhi nagar)

1 CA o Experience in Taxation

specifically in Indirect Taxation like Service Tax (Earlier) GST (Now),

o Should have proven record in anchoring/ conducting GST

Implementation/Consultancy Assignments

o Must have worked in at least 5 assignments in Government Tax Consultancy in Indirect Tax

o Should have proficiency in use of Tally software and/or other accounting package

o Provide technical

leadership to the team including regular co- ordination & quality assurance

o Overall in-charge of GST

Consultancy Assignment

o Regular reporting to Managing Director/

designated person.

o Responsible for strengthening the existing accounting & financial

management practices

GST Assistant

(At every

state office)

12 Semi Qualified

o Experience in Taxation specifically in Indirect Taxation like Service Tax

(Earlier) GST (Now), o Should have proven

record in anchoring/ conducting GST Implementation/Consultancy Assignments

o Must have worked in

at least 1 assignments in Government Tax Consultancy in Indirect Tax

o Should have proficiency in use of Tally software and/or other accounting

package

o Regular reporting to Team Leader.

o Responsible

for strengthening the existing accounting & financial management practices

Capacity

building expert

(At every office)

12 CA/ GST/

accounting expert

o Experience in Taxation

specifically in Indirect Taxation like Service Tax

(Earlier) GST (Now), o Should have proven

record in conducting GST Seminar/ training session.

o Must have worked in at least 1 similar assignments.

o Regular reporting

to Team Leader.

IT Expert 1 Master in o Should have expiring in

12

(State office) technology software development

o Should understand financial management

o Has developed at least one software of similar nature

Accounting expert

(Head Office)

2 CA o Experience in Taxation

specifically in Indirect Taxation like Service Tax (Earlier) GST (Now),

o Should have proven record in anchoring/ conducting GST

Implementation/Consultancy Assignments

o Must have worked in at least 1 assignments in Government Tax Consultancy in Indirect

Tax o Should have proficiency in

use of Tally software and/or other accounting package

o Reporting to team leader

o Compilation of report from all state office

o Department representation

and other support

Software

developer

Will be deployed

at consultant office in case of software development

2.2 Support and inputs to the agency

TCGL shall provide adequate office space to the Agency to perform its services. In

terms of hardware and software support, TCGL shall provide necessary software(s),

data server and requisite hardware i.e. computers and printers to the Firm.

2.3 Performance Security

The Firm will furnish within 10 days of the issue of Letter of Acceptance (LOA), an Account Payee Demand Draft/ Fixed Deposit Receipt/ Unconditional Bank Guarantee (in TCGL format)/ in favour of “Tourism Corporation of Gujarat Limited” payable/en-cashable at Gandhinagar, from any nationalized or scheduled commercial Bank in India for an amount equivalent to 5% (five percent) of the total contract value

towards Performance Security valid for a period of six (6) months beyond the stipulated date of completion of services. The Bank Guarantee will be released after six months of successful completion of the assignment.

3. INSTRUCTION TO THE APPLICANTS 3.1 General

In preparing their Proposals, applicants are expected to examine in detail the documents comprising this RFP Document. Material deficiencies in providing the information

requested may result in rejection of an applicant. The Applicants are requested to submit the proposal and all their correspondence in English.

3.2 Proposal Validity

The Proposal shall remain valid for acceptance by the TCGL for a period of 90 days from

the last date of submission of proposals. If needed, TCGL may request the Applicants to extend the period of validity of their proposals on the same terms and conditions.

13

3.3 Amendment of RFP At any time prior to the Proposal Due Date, TCGL for any reason, whether on its

own initiative or in response to clarifications requested by a prospective applicant, may

modify and/or amend the RFP Document or part thereof by the issuance of an

amendment.

Any amendment thus issued shall form a part of the RFP Document and shall be

communicated in writing to all the Applicants who shall acknowledge receipt of such

amendment in writing to TCGL.

To give the prospective Applicants reasonable time in which to

take such amendments/modifications into account for preparing their Proposals, TCGL reserves the right to extend the Proposal Due Date.

3.4 Association of consultants and Sub-Consultants Associates or Joint Venture arrangement or Consortiums are not allowed under the

assignment. 3.5 Confidentiality Information relating to the examination, clarification, evaluation for selection, and recommendation of the Preferred Applicant / Successful Applicant shall not be disclosed

to any person who is officially not concerned with the Bidding Process or is not a retained professional advisor advising TCGL in relation to, or matters arising out of, or concerning the Bidding Process. TCGL shall treat all information submitted as part of Proposal as confidential and shall require all those who have access to such material to treat the same in confidence. TCGL shall not divulge any such information unless it is ordered to do so by any authority that has power under law to require its disclosure or is to enforce or assert any right or privilege of the statutory entity and/or TCGL.

3.6 Litigation History

Any entity which has been barred/blacklisted by the Central/ State Government, or any

entity controlled by it, from participating in any assignment/ project, and the bar subsists as on the date of Application (even if the litigation is pending on the same dispute (barred / blacklisted) under the jurisdiction / arbitration/ laws), would not be eligible

to submit Application, either individually or as an associate. 3.7 Conflict of Interest The Applicant shall not have a conflict of interest (the “Conflict of Interest”) that affects the Bidding Process. Any Applicant found to have a Conflict of Interest shall be disqualified. In the event of disqualification, TCGL shall be entitled to forfeit and

appropriate the Bid Security as mutually agreed genuine pre-estimated loss and damage likely to be suffered and incurred by the TCGL and not by way of penalty for, inter alia, the time, cost and effort of the TCGL, including consideration of such Applicant’s Application (the “Damages”), without prejudice to any other right or remedy that may be available to TCGL under the agreement or otherwise. 3.8 Fraud and Corrupt Practices

The Applicants and their respective officers, employees, agents shall observe the highest standard of ethics during the Bidding Process. Notwithstanding anything to the contrary contained herein, TCGL may reject an Application without being liable in any manner whatsoever to the Applicant if it determines that the Applicant has, directly or indirectly or through an agent, engaged in corrupt practice, fraudulent practice, coercive

practice, undesirable practice or restrictive practice in the Bidding Process. Without prejudice to the rights of TCGL hereinabove, if the Applicant is found by TCGL to have directly or indirectly or through an agent, engaged or indulged in any corrupt practice, fraudulent practice, coercive practice, undesirable practice or restrictive practice

14

during the Bidding Process, such Applicant shall not be eligible to participate in any RFP issued by TCGL during a period of 2 (two) years from the date such Applicant is found by TCGL to have directly or indirectly or through an agent, engaged or indulged in

any corrupt practice, fraudulent practice, coercive practice, undesirable practice or restrictive practice, as the case may be. For the purposes of this, the following terms shall have the meaning hereinafter

respectively assigned to them: a. “corrupt practice” means (i) the offering, giving, receiving, or soliciting, directly or indirectly, of anything of value to influence the actions of any person connected with the Bidding Process (for avoidance of doubt, offering of employment to, or employing, or engaging in any manner whatsoever, directly or indirectly, any official of the TCGL who is or has been associated in any manner, directly or indirectly, with the Bidding Process

or the LOA or has dealt with matters concerning the agreement or arising there from, before or after the execution thereof, at any time prior to the expiry of one year from the date such official resigns or retires from or otherwise ceases to be in the service of the TCGL, shall be deemed to constitute influencing the actions of a person connected with the Bidding Process); or (ii) engaging in any manner whatsoever, whether during the Bidding Process or after the issue of the LOA or after the execution of the

agreement, as the case may be, any person in respect of any matter relating to the

Project or the LOA or the agreement, who at any time has been or is a legal, financial or technical adviser of the TCGL in relation to any matter concerning the Project; b. “fraudulent practice” means a misrepresentation or omission of facts or suppression of facts or disclosure of incomplete facts, in order to influence the Bidding Process;

c. “coercive practice” means impairing or harming or threatening to impair or harm, directly or indirectly, any person or property to influence any person’s participation or action in the Bidding Process; d. “undesirable practice” means (i) establishing contact with any person connected with or employed or engaged by the TCGL with the objective of canvassing, lobbying or in any manner influencing or attempting to influence the Bidding Process; or (ii) having a Conflict

of Interest; and e. “restrictive practice” means forming a cartel or arriving at any understanding or

arrangement among Applicants with the objective of restricting or manipulating a full and fair competition in the Bidding Process.

Chapter 4. SUBMISSION OF & EVALUATION OF THE PROPOSAL

4.1 Submission of Proposal The Proposal shall be submitted in sealed envelopes as marked below. The Applicant shall submit its Proposal in the following covers: Envelope 1 – “Technical Proposal for Selection of Chartered Accountant Firm for GST

Consultancy, Designing Invoice Booking Software for All Properties of TCGL and Providing Training to Staff of Tourism Corporation of Gujarat Limited” Envelope 2 – Bid security in the form of Demand Draft

The information “Technical Proposal” and “Bid Security” should be specifically mentioned on the cover of respective envelopes. The format of covering letter for technical and financial proposal is given in Chapter 5.

All parts of the Proposal (sealed Envelope 1 and 2) marked as above, shall be placed in a sealed outer envelope or a box, with the following inscription: “Selection of Chartered Accountant Firm for GST Consultancy, Designing Invoice Booking Software for All Properties of TCGL and Providing Training to Staff of Tourism Corporation of Gujarat Limited”

15

Submitted by: (Name & address of the firm) Submitted To:

The Managing Director, Tourism Corporation of Gujarat Limited Block No.16-17, 4th Floor Udhyog Bhavan,

Gandhinagar – 382 011 Ph: - +91 79 2397 7211, Email: [email protected]

The Applicant can submit the Proposal by registered post/ courier or submit the same in person, so as to reach the designated address by the time and date stipulated. No delay in the submission of the Proposal for any reason will be entertained. Any Proposal received by TCGL after the deadline for submission of the Proposals stipulated, shall not be opened.

4.2 Content of the Proposal

4.2.1 Technical Proposal

The Technical Proposal shall necessarily comprise the following:

o Profile of the firm

o Experience in providing accounting and financial management services/GST

Consultancy Service/Designing Software

o Detailed profile of proposed team members

o Turnover of the firm

o Approach & methodology for handling accounting and financial management

services

The formats of the Technical Proposal to be submitted as per the requirement of the Technical & Financial formats provided in Chapter 5 of the RFP. In case of non-compliance with the formats marks may be deducted.

4.3 Evaluation Method

The detailed evaluation methods for Technical and Financial proposal are specified below. 4.3.1 Evaluation of Technical Proposal Technical proposals of all the firms which meet the basic requirements (i.e. timely submission, bid security, sealing of application, Pass/ Fail criteria etc.) would be taken up

for detailed evaluation as per the technical bid evaluation criteria. All firms scoring 70 or above marks would be technically qualified and would only move into the next stage of Financial evaluation. The Applications shall be first evaluated on the basic requirements parameters. Those Applicants, who meet the basic requirements, shall be evaluated further as part of Technical Evaluation. Criteria is given in para 2.5 of chapter 2. Detailed evaluation of the proposals shall be undertaken for those Firms which qualify the above

basic requirements.

16

Eligibility Criteria:

A. General Criteria:-

Firm of CA which fulfills the following criteria may apply:

Chartered Accounts firm should have Head Office/Branch Office either in

Ahmedabad/Gandhinagar.

CA Firm should have a valid GST Registration Number.

CA Firm must be empanelled with C & AG.

CA firm should have conducted training session on financial management

to government organization.

CA Firm Should have at least 10 Years of Experience.

CA Firm should have at least 15 Chartered Accountants including

Partners

CA Firm should have experience of Work with Government

Organization/Undertaking as Accounting and Financial Management/Tax

Consultant in at least 10 assignments

CA Firm should have Average Annual Professional receipt of last 3 years

i.e. F.Y.2015-16, 2016-17 & 2017-18 at least Rs.50 Lakh

Table Showing Technical Marks allocation:

S.N. Criteria Marks

A Years of Existence of the CA firm as on 01.01.2019 5

(i) More than 10 Years but up to 15 Years 1

(ii) More than 15 Years but up to 25 Years 3

(iii) More than 25 Years 5

B Team Strength - Nos of Chartered Accountants including Partners

5

(i) More than 15 but up to 25 3

(ii) More than 25 5

C Experience of Work with Government

Organization/Undertaking as Accounting and Financial Management/Tax Consultant

5

(i) Up to 10 Assignments 1.25

(ii) More than 10 but up to 20 Assignments 2.5

(iii) More than 20 Assignments 5

D Average Annual Professional receipt of last 3 years i.e. F.Y.2015-16, 2016-17 & 2017-18.

5

(i) More than Rs. 50 Lakh but up to Rs. 200 Lakh 1.25

(ii) More than Rs. 200 Lakh but up to Rs. 500 Lakh 2.50

(iii) More than Rs. 500 Lakh but up to Rs. 1000 Lakh 3.75

(iv) More than Rs. 1000 Lakh 5

17

E Working experience 20

(i) National Level Assignment- At least one 5

(ii) Accounting/Tax experience in state tourism corporation/ department 5

(iii) Training and capacity building session- at least 2 government client 5

(iv) Software implementation & maintenance- at least one government client

5

F Nos. of Branches of CA Firms covering TIBs outside Gujarat State as per ICAI Records on 01.04.2019

10

(i) Covering 8 TIBs 8

(ii) Covering 9 TIBs 9

(iii) Covering 10 TIBs 10

G Quality Accreditation 10

(i) CAG empanelment under major category 2.5

(ii) Peer Review 2.5

(iii) ISO certification 2.5

(iv) Net worth more than 50 Lakh 2.5

H Proposed Manpower 20

(i) Team Leader (5 each) 5

(ii) Accounting expert (2.5 each) 5

(iii) IT Expert (4 each) 4

(iv) Capacity building expert (0.5 each) 6

I Work Approach and Methodology 20

Total 100

4.3.2 Opening and Evaluation of Financial Proposal

The envelope containing the financial proposal shall not be opened till the technical evaluation is complete. The financial proposal of only such Applicants will be opened who obtain minimum qualifying 70 or above Marks prescribed. Out of the technically qualified applicants, the final selection shall be based on Least Cost method (LCS).

4.4 Last date of submission of the Proposal

The Proposals must be received by the Managing Director, TCGL not later than 16-09-2019 up to 5.00 pm. 4.5 Proposal opening The Applicants who qualify as per technical evaluation would be intimated in the due

course. The financial proposals of the Applicants who qualify as per technical evaluation

18

will be opened in the TCGL office, Gandhinagar in the presence of Concern Officials of TCGL. The authorized representatives of the firms (Applicants) may choose to attend the financial proposal opening with authorization letter from their firms.

4.6 Award of contract The firm will sign the contract after fulfilling all the formalities/pre-conditions mentioned

in the standard form of contract of TCGL, within 30 days of issuance of the letter of intent. The firm is expected to commence the Assignment/job on the date and at the location specified in the contract. 4.7 Duration of Contract:

The Contract will be awarded for 3 initially and extendable for further 2 years depending on performance of consultant.

19

Chapter 5 SUBMISSION FORMS - TECHNICAL & FINANCIAL

Form Tech - I: Technical Proposal Covering Letter

FORM TECH I

(To be placed in the sealed cover containing technical proposal)

[Location, Date]

To

The Managing Director,

Tourism Corporation of Gujarat Limited

Dear Sir,

We, the undersigned, offer to provide the services for [Insert title of

assignment] in accordance with your Request for Proposal dated [Insert Date] and our

Proposal. We are hereby submitting our Proposal, which includes this Technical

Proposal, sealed under an envelope.

We are submitting our Proposal in our own individual capacity without entering into any

association / as a Joint Venture. We hereby declare that all the information and

statements made in this Proposal are true and accept that any misinterpretation

contained in it may lead to our disqualification.

If negotiations are held during the period of validity of the Proposal, i.e., before the

date indicated in the RFP, we undertake to negotiate on the basis of the proposed

personnel. Our Proposal is binding upon us and subject to the modifications resulting

from Contract negotiations.

We undertake, if our Proposal is accepted, to initiate the consulting services related to

the assignment not later than the date indicated in the RFP (Please indicate date).

We understand you are not bound to accept any Proposal you receive. We remain.

Yours sincerely,

Authorized Signature [In full and initials]:

Name and Title of Signatory:

Name of Firm:

Address:

20

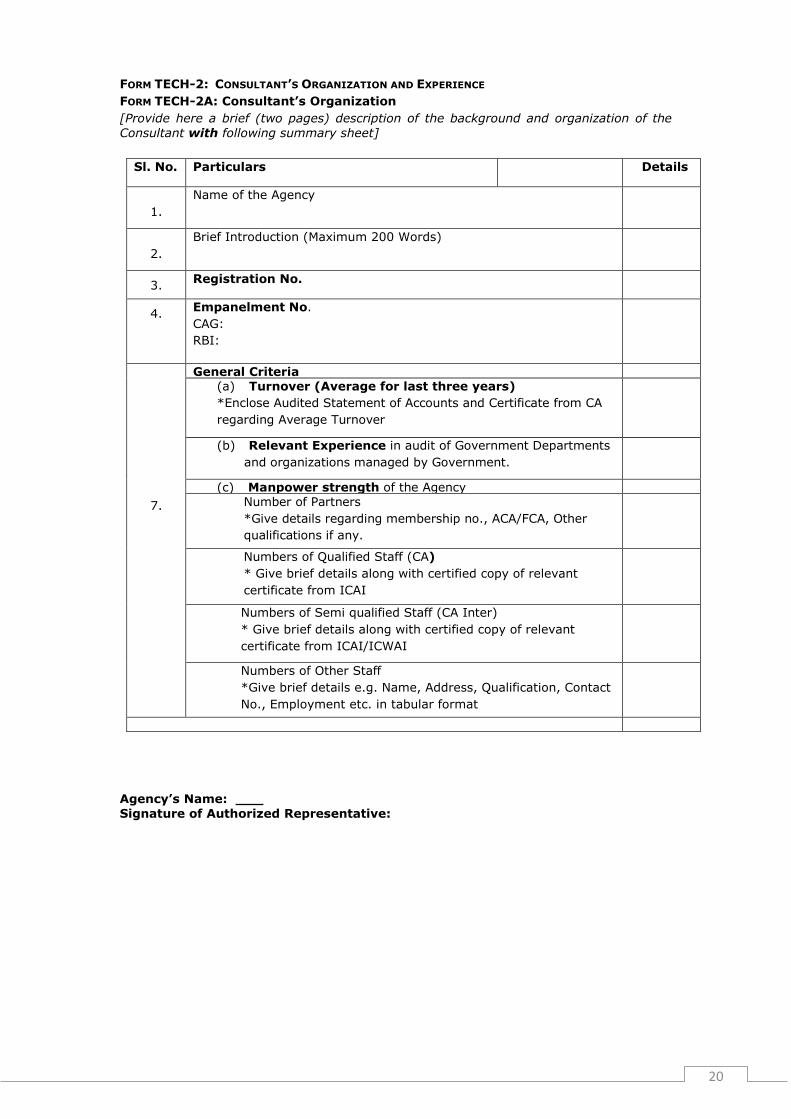

FORM TECH-2: CONSULTANT’S ORGANIZATION AND EXPERIENCE

FORM TECH-2A: Consultant’s Organization

[Provide here a brief (two pages) description of the background and organization of the

Consultant with following summary sheet]

Sl. No. Particulars Details

1.

Name of the Agency

2.

Brief Introduction (Maximum 200 Words)

3. Registration No.

4. Empanelment No.

CAG:

RBI:

7.

General Criteria (a) Turnover (Average for last three years)

*Enclose Audited Statement of Accounts and Certificate from CA

regarding Average Turnover

(b) Relevant Experience in audit of Government Departments

and organizations managed by Government.

(c) Manpower strength of the Agency Number of Partners

*Give details regarding membership no., ACA/FCA, Other

qualifications if any.

Numbers of Qualified Staff (CA)

* Give brief details along with certified copy of relevant

certificate from ICAI

Numbers of Semi qualified Staff (CA Inter)

* Give brief details along with certified copy of relevant

certificate from ICAI/ICWAI

Numbers of Other Staff

*Give brief details e.g. Name, Address, Qualification, Contact

No., Employment etc. in tabular format

Agency’s Name:

Signature of Authorized Representative:

21

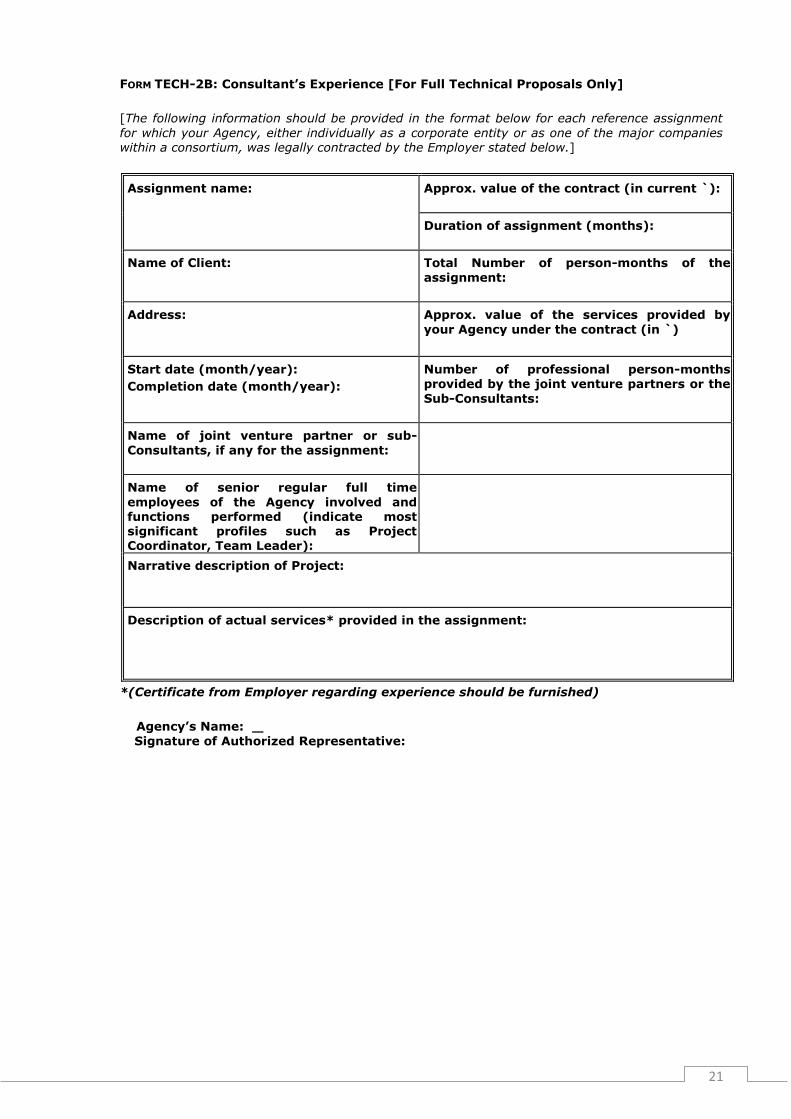

FORM TECH-2B: Consultant’s Experience [For Full Technical Proposals Only]

[The following information should be provided in the format below for each reference assignment

for which your Agency, either individually as a corporate entity or as one of the major companies within a consortium, was legally contracted by the Employer stated below.]

Assignment name: Approx. value of the contract (in current `):

Duration of assignment (months):

Name of Client:

Total Number of person-months of the

assignment:

Address:

Approx. value of the services provided by

your Agency under the contract (in `)

Start date (month/year):

Completion date (month/year):

Number of professional person-months

provided by the joint venture partners or the

Sub-Consultants:

Name of joint venture partner or sub-

Consultants, if any for the assignment:

Name of senior regular full time

employees of the Agency involved and functions performed (indicate most significant profiles such as Project Coordinator, Team Leader):

Narrative description of Project:

Description of actual services* provided in the assignment:

*(Certificate from Employer regarding experience should be furnished)

Agency’s Name:

Signature of Authorized Representative:

22

Form TECH-3: Description of Approach, Methodology and Work Plan for Performing the Assignment [As per the details mentioned in the NARRATIVE EVALUATION CRITERIA]

Technical Approach and Methodology,

Work Plan, and

Organization and Personnel,

a) Technical Approach and Methodology. In this chapter you should explain your

understanding of the objectives of the assignment, approach to the services, methodology for carrying out the activities and obtaining the expected output, and the degree of detail of such output. You should highlight the problems being addressed and their importance, and explain the technical approach you would adopt to address them. You should also explain the methodologies you propose to adopt and highlight the compatibility of those methodologies with the proposed approach.

b) Work Plan. In this chapter you should propose the main activities of the

assignment, their content and duration, phasing and interrelations, milestones (including interim approvals by the Client), and delivery dates of the reports. The proposed work plan should be consistent with the technical approach and methodology, showing understanding

of the TOR and ability to translate them into a feasible working plan. A list of the final documents, including reports, drawings, and tables to be delivered as final output, should be included here. The work plan should be consistent with the Work Schedule of Form TECH-7.

c) Organization and Personnel. In this chapter you should propose the structure and

composition of your team. You should list the main disciplines of the assignment, the key

expert responsible and proposed technical and support personnel.

23

FORM TECH-4: TEAM COMPOSITION, TASK ASSIGNMENTS AND SUMMARY OF CV

INCORMATION

Team Leader and Key Professionals

Surname, First Name

Agency Acronym

Area of Expertise

Position Assigned

Task Assigned

Employment Status with Agency (full-time/

other)

Education/ Degree (Year / Institution)

No. of years of relevant project

experience

CV signature (by expert/by

other)

Support Staff

Sl No Surname, Name Position Task Assignment

24

FORM TECH-5: CURRICULUM V ITAE (CV) FOR PROPOSED EXPERTS

[Summary of CV: Furnish a summary of the above CV. The information in the summary

shall be precise and accurate. The information in the summary will have bearing on the

evaluation of the CV]

1. Proposed Position[only one candidate shall be nominated for each position]:

2. Name of Firm [Insert name of firm proposing the expert]:

3. Name of Expert [Insert full name]:

4. Date of Birth: Citizenship:

5. Education [Indicate college/university and other specialized education of

expert, giving names of institutions, degrees obtained, and dates of obtainment]:

6. Membership of Professional Associations:

7. Other Training [Indicate significant training since degrees under 5 - Education

were obtained]: 8 Publication:[List of details of major technical reports /papers published in

recognized national and international journals]

9 Languages [For each language indicate proficiency: good, fair, or poor in

speaking, reading, and writing]:

9. Employment Record [Starting with present position, list in reversed order, every

employment held. List all positions held by staff member since graduation, giving dates, names of employing organization, title of positions held and location of assignments. For experience period of specific assignment must be clearly

mentioned, also give Employer references, where appropriate.]:

From [Year]: To [Year]: Employer:

Positions held:

12. Certification: I, the undersigned, certify to the best of my knowledge and belief that:

(i) This CV correctly describes my qualifications and my experience.

(ii) I am not employed by the Executing/ Implementing Agency. [(iii) I am /I am not in regular full-time employment with the Consultant /Sub-

Consultant.]

(iv) In the absence of medical incapacity, I will undertake this assignment for the duration and in terms of the inputs specified for me in the Personnel Schedule in Form TECH-6 provided team mobilization takes place within the validity of this proposal or any agreed extension thereof.

(v) I am willing to work on the project and I will be available for entire duration of

the project assignment and I will not engage myself in any other assignment during the currency of this assignment on the project

(vi) I, the undersigned, certify that to the best of my knowledge and belief, this bio-data correctly describes myself my qualification and my experience

I am committed to undertake the assignment within the validity of Proposal.

(vi) I did not write the terms of reference forth are consulting services assignment.

11A. Detailed Tasks Assigned

[List all tasks to be performed

under this assignment]

11B. Work Undertaken that Best Illustrates Capability to

Handle the Tasks Assigned[Among the assignments in which

the expert has been involved, indicate the following

information for those assignments that best illustrate the

expert’s capability to handle the tasks listed under point11.]

Name of assignment or project:

Year:

Location:

Client:

Main project features:

25

I understand that any wilful misstatement described herein may lead to my

disqualification or dismissal, if engaged.

Date: [Day/Month/Year]

[Signature of expert or authorized representative of the firm]

Full name of authorized representative:

1

This CV can be signed by a authorized representative of the Consultant or by the

expert.

26

No.

Name of Expert

/Position

Professional Expert input (in the form of a bar

chart)

Total person-months input

1 2 3 4 5 6 7 8 9 10 11 12 n Field2 Total

Expert

1

[Field]

2

3

N

Subtotal

Support staff

1

[Field]

2

N

Subtotal

Total

FORM TECH-6: PERSONNEL SCHEDULE

27

FORM TECH-7: WORK SCHEDULE

N° Activity1 Months2

1 2 3 n

1

2

3

4

5

1. Indicate all main activities of the assignment, including delivery of reports/ deliverables as

per Terms of Reference & Scope of Work (e.g.: inception, interim, and final reports), and

other benchmarks such as Client approvals. For phased assignments indicate activities,

delivery of reports, and benchmarks separately for each phase.

2. Duration of activities shall be indicated in the form of a bar chart.

28

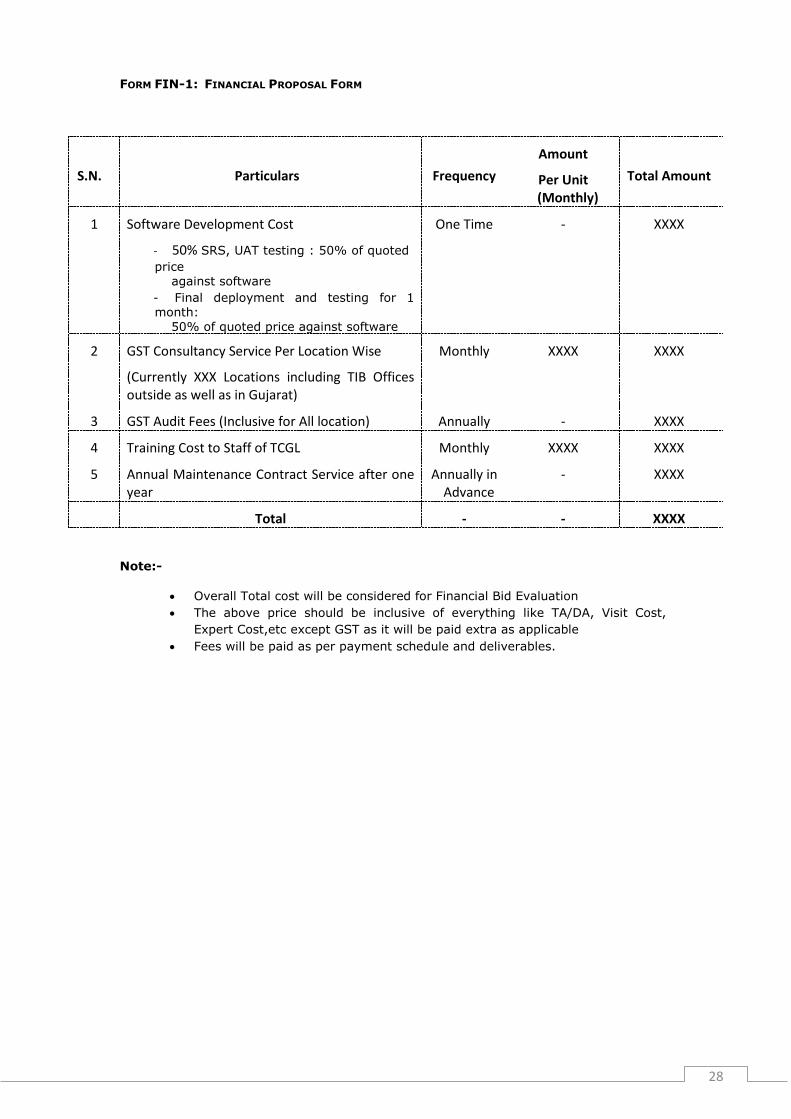

FORM FIN-1: FINANCIAL PROPOSAL FORM

S.N. Particulars Frequency

Amount

Per Unit (Monthly)

Total Amount

1 Software Development Cost

- 50% SRS, UAT testing : 50% of quoted

price against software

- Final deployment and testing for 1 month: 50% of quoted price against software

One Time - XXXX

2 GST Consultancy Service Per Location Wise

(Currently XXX Locations including TIB Offices outside as well as in Gujarat)

Monthly XXXX XXXX

3 GST Audit Fees (Inclusive for All location) Annually - XXXX

4 Training Cost to Staff of TCGL Monthly XXXX XXXX

5 Annual Maintenance Contract Service after one year

Annually in Advance

- XXXX

Total - - XXXX

Note:-

Overall Total cost will be considered for Financial Bid Evaluation

The above price should be inclusive of everything like TA/DA, Visit Cost,

Expert Cost,etc except GST as it will be paid extra as applicable

Fees will be paid as per payment schedule and deliverables.