Embed Size (px)

Citation preview

Patrick & Dillon CERT!FIED PUBUC ACCOUNTANTS

327 West Fayette Street

Syracuse, NY 13202

Tel: (3 15) 471-1941

P. n Fax: (315) 471-1 949

~~~~~~~~~~~~~~~~~~~~~~

Independent Auditor's Report

September 19, 2008

To the Members of the City of Syracuse Industrial Development Agency

JOHN J. PATRICK, C.P.A . jpa tr ick@pa trick-dillon-cpa.com

EILEEN DILLON, C.P. A. edillon@patrick·dillon-cpa. com

We have audited the accompanying financial statements of the business-type activities, each major fund , and the aggregate remaining fund information of the City of Syracuse Industrial Development Agency (a Component Unit of the City of Syracuse, New York), as of and for the year ended December 31,2007, which collectively comprise the Agency's basic financial statements as listed in the table of contents. These financial statements are the responsibility of the City of Syracuse Industrial Development Agency's management. Our responsibility is to express an opinion on these financial statements based on our audit. The prior-year summarized comparative financial information has been derived from the Agency's 2006 financial statements and in our report dated August 17,2007, we expressed an unqua lified opinion on those financia l statements.

We conducted our audit in accordance with auditing standards generally accepted in the United States of America, and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assess ing the accounting principles used and significant estimates made by management, as we ll as evaluating the overall financia l statement presentation. We be lieve that our audit provides a reasonable basis for our opinion.

In our opinion, the financial statements referred to above present fairly, in all material respects, the respective financial position of the business-type activities, each major fund, and the aggregate remaining fund in formation of the City of Syracuse Industrial Deve lopment Agency as of December 31, 2007, and the respective changes in financial pos ition and cash flows thereof for the year then ended in conformity with accounting principles generally accepted in the United States of America.

In accordance with Government Auditing Standards, we have also issued our report dated September 19,2008 on our consideration of the City of Syracuse Industrial Development Agency 's internal control over financ ial reporting and our tests of its compliance with certain provisions of laws, regulations, contracts and grant agreements, and other matters. The purpose of that report is to describe the scope of our testing of internal control over financial reporting and comp liance and the results of that testing and not to provide an opinion on the internal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards and should be cons idered in conjunction with this report in considering the results of our aud it.

Page 2

To the Members of the City of Syracuse Industrial Development Agency September 19, 2008 Page 2

The Management' s Discuss ion and Analysis on pages 4 through 6 is not a req uired part of the basic fin ancial statements but is supplementary in formation req ui red by accounting principles generally accepted in the United States of America. We have applied certain limited procedures, which consisted principally of inqui ries of management regarding the methods of measurement and presentation of the required supplementary information. However, we did not audit the in fo rmation and express no opinion on it.

Our audit was conducted for the purpose of forming opinions on the financial statements that collectively comprise the City of Syracuse Industrial Development Agency's basic financial statements. The accompanyi ng Schedule of Expenditures of Federal Awards is presented for purposes of add it ional analysis as requi red by the United States Office of Management and Budget (OMB) Circular A-133 , "Audits of States, Local Govel'l1ments and Non-Profit Organizations" and, along with the additional supplementary schedules, the combining non major fund financial statements, the Supplemental Schedule of Industrial Revenue Bonds, and the Supplemental Schedule of Other Financing, are presented for purposes of additional analysis and are not a required part of the basic fi nancial statements. The Schedule of Expenditures of Federal Awards, the combining nonmajor fu nds financial statements, the Supplemental Schedule of Industrial Revenue Bonds, and the Supplemental Schedule of Other Financing, have been subjected to the aud iti ng procedures applied in the audi t of the basic financial statements and, in our opinion, are fairly stated, in all material respects, in relati on to the basic financial statements taken as a whole.

Page 3

CITY OF SYRACUSE INDUSTRIAL DEVELOPMENT AGENCY (a COlllponent Unit of the City of Syracuse, New York) Management's Discussion and Analysis for lite Year Ended December 31,2007 (Unaudiled)

As management of the Cily of Syracuse Ind llstrial Development Agency, we offer readers o/Ihis Agency's financial statements this narrative overview alld analysis of the finan cial nelivilies of tile Agency jar the fiscal year ended December 3/, 2007. We encourage readers 10 consider the informatioll pl'esellfed here il1 COlljUIICliol1 with additional in/ormatiol1

===-~==Ilrat we have1l1rnisheaTnlh~fil1ancial s afemenls.

FINANCIAL HIGHLIGHTS

• The assels of the Cily of Syracuse Indl/SI";al Development Agency exceeded ils liabilities 01 the close of ils mosl reeell/ fisca l year by $11,052,654 (net assels). This GII/ounlmay be used 10 meet (he Agency 's ongoing obligations to constituents alld creditors in accordance lVith the Agency's fund designation andfiscal policies.

• The Agency's 10lalnel assels increased by $4, 042,855 for Ihe 2007 fiscal year.

• During 2007, Ihe Agency received $855,000 ji'om Ihe City 0/ Syracuse 's COll1l1l1l1Jily Developmenl Block Grant f unds 10 s ubsidize HUD-108 10an payments, and $17,130,571 in /ees /or its role in various development projecls, The bl/lk of Ihe developmenl fees ($ 16,400,000) came fro m Ihe Desliny USA projecl, wilh $11, 000,000 of Ihis amol/nl passed Ihrol/gh by SIDA 10 Ihe City of Syracl/selOnondaga COI/nly, and $5, 400, 000 reslricled f or I/se by SI DA f or projecls il/ Ihe lakefrol/I area of Ihe Cily of Syracl/se.

• The Agency continued reducing ils HUD-10810ans during 2007 by making $ 1,378,000 ill principal payments.

• The Agency increased ils allowance for uncollectible loalls by $3,000,000 durillg 2007 to recognize the dOllbl/ul collec fibilily 0/0 portion of its loans to the Dey 's Centel1l1ial Plaza project,

OVEIIVIEW OF THE FINANCIAL STATEMENTS

This discllssion and analysis is intended to serve as all introduction to the Agency's bas ic financial statements. The Agency 's basic financial statements are comprised 0/ three components: I) agency-wide financial slatemenlS, 2) f und financial statements, and 3) notes 10 the financial statements. 11,;S report also cOl1tains olher sllpplementOlY in/ormalion in oddilion to the basic financial slatements themselves.

Agency-wide financial statements - The agency-wide finan cial statements are desig l1ed to provide readers with a broad overview 0/ the Agency 's finances. in a manner similar 10 a private-seclor business.

The Statemel1l of Net Assets presents in/ormation on all 0/ the Agency 's assets and liabilities, with the difference between the two reported as net assels. Over lime, increases 01' decreases inne! assets may serve as a lise/III indicator a/ whether the finanCial posilion o/Ihe Agency is improving or deteriorating,

The Statement 0/ Activities presents in/ormation showing how the Agency 's nel assets changed during the fiscal year. All changes in net assets are reported when the underlying event giving rise to the change occurs, regardless a/ the timing 0/ related cashfloll's. Thus, revenues and expemes are reported in this statement/or some items that will ol1ly result ill cash flows in the /I/Iltre fiscal periods (e.g.. accl'l/ed interesl),

Both a/the agencY-lI'idefil1ancial statements report only bUSiness-type (proprietOly) acti vities, since none a/ the Agency's activities are considered to be governmental acti vities supported primarily by laxes.

The agency-wide financial stalements call be /olll1d on pages 7 and 8 a/this report.

Page 4

CITY OF SYRACUSE INDUSTRIAL DEVELOPMENT AGENCY (a Component Unit of the City of Syracnse, New York) Mal/agemel/I's Discllssiol/al/d AI/alysis/or Iile Year EI/ded December 31,2007 (UI/alldited)

Fund jil1(wcinl statem ellts - A fund is a group ing of related accounts Ihal is used fa maillfain COl1lro/ over resources that have been segregated f or specific aclivities or objectives. The Agency, like olhel' component 1II1ilS of state and local govemmelllS, IIses fill1d accollnting 10 ensure Gnd demonstrafe compliance lI'ithjinance-related lega/requirements. All a/the funds of fil e Agency are currently treated as propl'ielmy funds.

______ Proprietary I" ll1i£=..J!r..Qj2fi£JOLY_flwds_m:..e_Ifsed to account fOl~essenl ially_the_same-!unctiolls reported as proprietaJ~_aClivil ies' ____ _ ill fh e agency-wide jinancial---stCiiemenlS:--However, unlike the agency-wlae ]moncial statements, proprietmy fimd financial statements /OC l/S on current sources and uses 0/ spendable resources, as well as 011 balances 0/ spendable resources available at the end o/the fiscal year. Such in/ormation may be lIse/ul in evaluating Ihe Agency's near-Ierm fin ancing requirements.

Becal/se the /OCllS 0/ proprielmy fill1ds is narrower Ihall that 0/ the agency-wide financial statements, it is IIsefiti 10 compare Ihe in/ormation presented / 0 1' proprietmy fi ll1ds with similar in/ormation presel1led f or proprietmy activities i" the agellcywide financial statements. By doing so, readers may beller understand the long -term impact 0/ the Agency's near-term financing decisions. 711e Agency maintaills fi \-'e proprietmy funds. In/ormation is presel1led separately in the Funds Financial S tatemellts / or the Operating Fund Gnd the HUD-108 Fund, both a/which are considered 10 be major fi ll1ds. Data/rom the other three fimds are combined illto a single, aggregated presentatiOn. bldividual fimd data for each 0/ these nonmajor proprietmy fimds is p rovided in the f orm 0/ combining statements and can be found on pages 28 and 29 0/ this report.

Notes to the Fil1(lIlcial Statements - The noles provide additional in/ormation thaI is essential to afitllunderstanding a/the data provided ill the agency-wide and/tmdjrnancial slatell1e11ls. The notes to the financial slalemellls can be /ound on pages 12 through 19 oj this report,

Other ill/ormation - 111 addition to the basic finanCial statemellls and accompanying notes, this report also colllains certain supplemenlmy in/ormation, which a) combines noumajor proprietmy /tmds, and b) supplies information all the Agency's projects required by the Office of the Nell' York State Comptroller. This, supplementGlY in/ormation call befoulld on pages 28 throl/gh 33 oJthis report,

AGENCY-WIDE FINANCIAL ANALYSIS

As noted earlier, net assets may serve over time as a IIseful indicator of the Agency 's financial position. 111 the case of Ihe City of Syracuse ludustrial Development Agency , assets exceeded liabilities by $ 11 ,052,654 as of December 31, 2007.

Cash alld 10al1s receivable constitute the largest portion of the Agency's l1el assets. These net asselS are available / or/lIIl1re repayment oft-lUD-108loans payable andforfiltllre economic developme11l projects.

All of the Agency 's fimds are treated as proprielGlY (business-type) /tmds. The / ollowing are summarized versions of the agency-wide financial sta/ell/ellls /01' 2007:

Statement orNet Assets

Cash and cash equivalents Receivables Inveslments ill properties Center ArmOlY garage Other assets

Total assets

HUD-1081oal1s payable Ce11ler ArmOlY garage bonds Payable to City oJ Syracl/se All other liabilities

Total liabilities

Net asse fs

Total liabilities alld lIet (Issets

PageS

$ 18,350,000 9,620,000

740,000 1,290,000

10,000

$ 30 OW 000

$ 13,565,000 1,645,000 2,040,000 1,710000

18,960,000

11,050,000

L.l1l.Jlli1.flflQ

CITY OF SYRACUSE INDUSTRIAL DEVELOPMENT AGENCY (a Component Unit of the City of Syracuse, New York) Mallagemellt's Discussioll alld Allalysis for lite Year Elided December 31, 2007 (Ullaudiled)

FillGllcillgjees Illterest income Loan subsidy (HUD) PILOT revenue

Statement ofA clivities

$ 17,130,000 1,470,000

855,000 830,000

============,------;lIll-01heL--;ncolll''--====;,--~-_=;====~=1.2',1;:{1QQ=====-~=====-95,000

TOlal income

Destiny USA fee 10 Cily of Syracuse/Onondaga Counly Interest expense Losses from lmcollecOble loolls Development cosls and public improvements All other expenses

Tolal expenses

Increase ill net assets

Nel nssels - beginning oj year

Nel assets - end of year

HUD-IOB DEBT

20,680,000

11,000,000 1,045,000 3,000,000

900,000 695,000

16,640,000

4,040,000

7,010,000

~ II Q~Q QQQ

The Agency has 1-/UD-I08 loans payable as of December 31, 2007 of $13,565,000. During 2007, Ihe Agency made principal payments of $ 1, 378,000. The resources needed 10 repay these loons will come from oj amolll1ls repaid by developers. b) a PILOT agreement assigned 10 fhe Agency, c) fee income, and d) allocations a/Community Developmelll Block Grant /ullds, which have been pledged to provide resources for these 10011 repoymellls. During 2007, Ihe Agency used Community Developl/,"1I1 Block Gralllfullds of$855,000 10 repay !-IUD-I 08 debl.

FINANCING FEES

As reporled earlier, SIDA received sllbslallliai developmelll fees from Ihe DeslillY USA projecl dl/rillg 2007: $5,400,000 for lise in development projects il1 the Syracllse lake/rollt area, and $ 11,000,000 to pass through to the City 0/ Syracllse/Onondaga COlmly /01' lise by them ill economic development. The SII ,OOO,OOO fee is part 0/0 len year/ee structure, 10laling $60,000,000, all ofll'hich lI'ill be passed Ihrough by SID;! 10 Ihe CilY ofSyracuselOllolldaga Counly.

RECEI VABLES

The Agency had approximately $8,800,000 (net) in 10al1s receivable, and $260,000 ill interest receivable 011 those loans olilstanding as 0/ December 31, 2007. ApprOXimately $8,000,000 0/ these receimbles are concentrated ill one project, Dey 's Centennial Plaza. The general partner o/Ihis project is the Syracllse Economic Developmelll Cmporation. which, like the City o/Syracuse Industrial Development Agency. is a compOnel1ll111i1 o/fhe City o/Syracuse.

IIEQUEST FOR INFORMA lION

This finanCial report is designed 10 provide readers wilh a general overview 0/ the Agency's finances. If you have questions about this report or need additional information, con/acl the Agency's board al Ihe City 0/ Syracuse Indus/rial Developmel1l Agellcy, 201 EasllVashillgloll Slreel, Room 605, Syracuse, NY /3202-1432.

Pnge6

CITY OF SYRACUSE INDUSTRIAL DEVE LOPMENT AGENCY (a Component Unit of the City of Syracuse, New York) Agency-widc Statemcnt of Net Assets December 31, 2007, with Comparative Fiuancia l luformation for December 31, 2006

2007 2006 ASSETS

Current assets: Cash and cash eq uiva lents $ 18,35 1,63 1 $ 12,404,344 InteresUeceLvable 258,24 28J,655 Loans rec eivable current portion 832,306 2,572,906 Other receivables 60 1,422 847,049 Investment in properties, at cost 737,160 727, 159 Prepaid expenses 10,944 10,857

Total current assets 20,79 1.705 16,845,970

Long-term assets: Loans receivable - long-term portion 7,932,556 8,755,708 Land and building, at cost, net of depreciation 1,288,74 1 1,40 I ,354 In terfund accounts

Total long-term assets 9,22 1,297 10,157,062

Total assets $ 30013 002 $ 27 003 lm

LIABILITIES AND NET ASSETS

Current liabilities: Accounts payable $ 1,362,44 1 $ 735 ,346 Accrued interest payable 345,829 376,652 Payable to City of Syracuse - current portion 347,842 41 9,448 Federal government loans - current portion 1,45 1,000 1,378,000 Bonds payable - current portion 120,000 11 0,000

Total current liabi lities 3,627, 112 3,01 9,446

Long-term liabilities: Payable to City of Syracuse - long-term portion 1,694,236 1,763,787 Federal government loans - long-term portion 12, 114,000 13,565,000 Bonds payable - long-term portion 1,525,000 1,645,000

Total long-term liabilities 15,333,236 16,973,787

Total liabili ties 18,960,348 19,993,233

Net assets: Invested in capital assets, net of re lated debt (349,344 ) (347,427)

Restricted for : Downtown Commercia l Rehabil itat ion Loans 290,277 290,277 Lakefront Development 5,400,000

Unrestricted 5,7 11 ,72 1 7,066,949

Total net assets 11 ,052,654 7,009,799

Total liabili ties and net assets $ 3Q 013 002 $ 22,Q03032

T he accompanying notes arc an integra l part of these fin ancia l statements.

Page 7

CITY OF SYRACUSE INDUSTRIAL DEVELOPMENT AGENCY (a Component Unit of the City of Syracuse, New York) Agency-wide Statement of Activities For the Year Ended December 31, 2007, with Comparative Summarized Financial Information for the Year Ended December 31,2006

Fees, In terest Income Operating

EXllenses and Relit Grants

Governmental activities: None $ $ $

Business-type activities: Destiny USA fcc to City of Syracuse/ Onondaga County 11 ,000,000 11,000,000

Economic Development 544,787 6, 130,571 Development projects 899,287 Loan programs 3,949,834 748,247 855,000 Parking garage 245,652 243,735

Total agency $ 16639560 $ 18, 122553 $ 855 000

General revenues: Interest on bank accounts PILOT revenue Other income

Total general revenues

Change in net assets

Net assets - beginning of year

Net assets - end of year

Net (Expense) Revenue and

ehangc in Net Assets 2007 2006

$ $

5,585,784 (475,080) (899,287 ) (303,491 )

(2,346,587 ) (1,939,279 ) (1,917) (11,982)

2,337,993 (2,729,832 )

720,055 509,256 832,127 457,787 152,680 85,434

1,704,862 I ,052,477

4,042,855 (1,677,355)

7,009,799 8,687.154

$ II Q:!2,ill $ 1002122

The accompa nying notes arc an integral part of these financial statements,

Pnge8

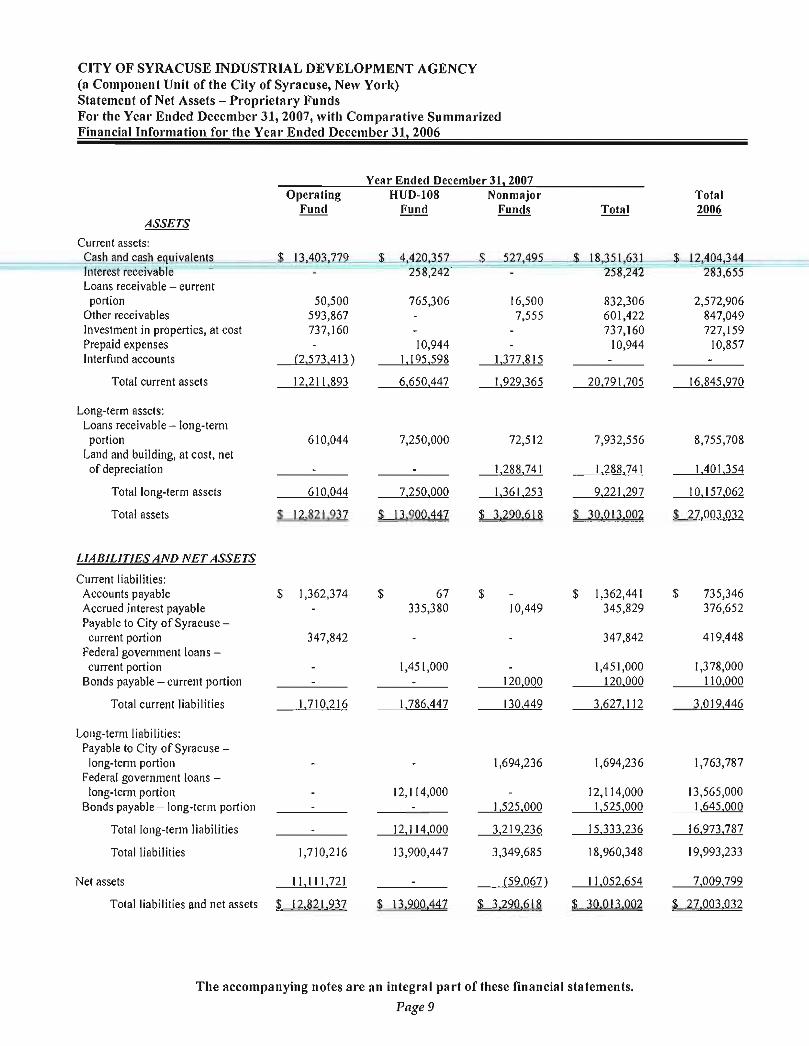

CITY OF SYRACUSE INDUSTRIAL DEVELOPMENT AGENCY (a Component Unit of the City of Syracnse, New Yor") Statement of Net Assets - Proprietary Fund s For the Yea r Ended December 31, 2007, with Com parative Summarized F iuanciallnformation fo r the Year Ended December 31, 2006

Year Ended December 31~ 2007 Operating HUD·t08 Nonmajor Total

Fu nd Fund Fu nds Total 2006 ASSETS

Current assets: Cash and cash cguivaients $ l3,4m.,Zl2 __ $~,420,35} __ L~27.495 __ $_ L8,3il,631 __ $_ 12,404,344 __ Interest receivable 258,242 258~242 283j;55 Loans receivable - current

portion 50,500 765,306 16,500 832,306 2,572,906 Other receivables 593,867 7,555 601,422 847,049 Investment in properties, at cost 737,160 737, 160 727, 159 Prepaid expenses 10,944 10,944 10,857 Interfund accounts (2,573,4 13 ) 1,195,598 1,377,8 15

Total current assets 12,2 11,893 6,650.447 1,929,365 20,791,705 16,845,970

Long-term assets: Loans receivable - long-term

portion 6 10,044 7,250,000 72,5 12 7,932,556 8,755,708 Land and building, at cost, net of depreciation 1,288,74 1 1,288,741 1,401,354

Total long-term assets 6 10,044 7,250,000 1,361,253 9,22 1,297 10,157,062

Total assets $ 12821937 $ 13900447 $ 3290618 $ 300 13002 $ 27 003 032

LIABILITIES AND NET ASSETS

Current liabilities: Accounts payable $ 1,362,374 $ 67 $ $ 1,362,441 $ 735,346 Accrued interest payable 335,380 10,449 345,829 376,652 Payable to City of Syracuse -current portion 347,842 347,842 419,448

Federal government loans -current port ion 1,45 1,000 1,45 1,000 1,378,000

Bonds payable - current portion 120,000 120,000 110,000

Total current liabil ities 1,710,216 1,786.447 130.449 3,627, 11 2 3,0 19.446

Long-term liabilities: Payable to City of Syracuse -

long-term portion 1,694,236 1,694,236 1,763,787 Federal government loans -

long-term portion 12, 11 4,000 12,1 14,000 13,565,000 Bonds payable - long-term portion 1,525,000 1,525,000 1,645,000

Total long-term liabilities 12,114,000 3,219,236 15,333,236 16,973,787

Total liabilities 1,710,216 13,900,447 3,349,685 18,960,348 19,993,233

Net assets 11,111,72 1 (59,067 ) 11 ,052,654 7,009,799

Total liabilities and net assets $ 12821231 $ 13 200,441 $ 3,220,618 $ 30 Q13,002 $ 21003032

T he accompanying notes are an intcgra l part of these financial statements.

Page 9

CITY OF SYRACUSE INDUST RIAL DEVELOPMENT AGENCY (a Component Unit of the C ity of Syracnse, New York) Statement of Revenues, Expenditures, and Changes in Fnnd Balances - Proprieta ry Funds Fo,' the Year Ended December 31, 2007, with Comparat ive Sunllnarized Financia l Information for the Year E nded December 31, 2006

Yea r Ended December 31 1 2007 Operating HUD-1 08 NO ll lllajor

Fund Fund "r'unds Revenue:

Financing fees $ 17, 130,57 1 $ $ PILOT revenue 349,966 482,16 1 Interest income 729,525 734, 155 4,622 Garage rent 243,735 Loan subsidy 855,000 Oth er income 11 6,803 35,877

Total revenue 18,326,865 2,071,3 16 284,234

Expenses: Development costs -Destiny USA ree to City of Syracuse! Onondaga County 11 ,000,000

Lakefront project 265,512 OM Edwards project 50,000

Public improvements 583,775 Interest 908,868 135,849 Losses from uncollectible loans 3,000,000 Legal fees 161,708 Professional fees 348,098 Depreciation 11 2,6 13 Miscellaneous 34,98 1 467 37,689

Total expenses 12.444.074 3,909.335 286, 151

Excess (deficiency) of revenue over expenses 5,882,791 (1,838,0 19) (1,917)

Transfers between funds ( 1,838,0 19 ) 1,838,019

Change in net assets 4,044,772 (1,9 17 )

Net assets - beginn ing of year 7,066.949 (57, 150)

Net assets - end of year $ II I II 121 $ !~20m

Total

$ 17, 130,57 1 832, 127

1,468,302 243,735 855 ,000 152,680

20,682.4 15

11 ,000,000 265,512

50,000 583,775

1,044,7 17 3,000,000

16 1,708 348,098 11 2,6 13 73, 137

16,639560

4,042,855

4,042,855

7,009,799

$ II 0~2 Q~1

T he accompanying notes a re an integra l pa rt of these fin ancia l statements.

Pngel0

ota 2006

$ 44,745 457,787

1,349,254 24 1,305

1,244,000 85,434

3.422,525

227,964 217

75,3 11 1, 124,178 3,000,000

311,983 186,5 19 11 2,6 13 6 1,095

5,099,880

(1,677,355)

(1,677 ,355 )

8,687,154

$ 1002,122

CITY OF SYRACUSE INDUSTRIAL DEVELOPMENT AGENCY (a Component Unit of the City of Syracuse. New Yorl,) Statemcnt of Cash Flows - Proprietary Fu nds For the Yea r Ended December 31. 2007. with Comparative Financia l Information for the Year Ended December 31. 2006

Cash flows from operating activities : Inflows -

Tota l Tota l 2007 2006

$ 805,91-5 ~~$~-618,28-1

8.155.112 1.288,745 ======~lll1nl!te~rest-receivedl=====----====,----~~===:ti:;;;",,:,

Loan fees and grants Rents and miscellaneous fees received Loan repayments Destiny USA fee

Outflows -Interest and financing fees Supplies and services Repayments to HUD Destiny USA fee to City of Syracuse/Onondaga County

Net cash provided by operating activities"

Cash flows from investing activities: Investment in property

Cash flows from financing activities: Payment on Center Armory Bonds

Net increase in cash and cash equ ivalents

Cash and cash equivalents - beginning of year

Cash and cash equivalents - end of year

*Reconciliation of changes in net assets to net cash provided by operat in g activities:

Change in net assets

Adjustments -Depreciation Decrease in loan principal and interest receivable Decrease (increase) in other receivables (Decrease) in loans payable to HUD (Decrease) increase in payable to City of Syracuse Increase in other payables and deferred revenue

Net adjustments

Net cash provided by operating activities

$

$

$

465,640 1,063,635 14 1,905 2,029,797

11 ,000,000

(1,072,730) (1 , 143,088) (1,050,555 ) (1,014,686) (1,378,000) (1,153,000)

( 11,000,000)

6.067,287 1.689,684

(10,000)

(110,000) (100,000)

5,947,287 1,589,684

12,404,344 10,814,660

18,ill,ill Lll,4Q4,ill

4.042,855 $ (1,677,355)

112,613 112.6 13 2.589. 165 3.855. 137

245,627 (29.333 ) (1,378,000) (1, 153,000)

( 141,157) 38,917 596,184 542,705

2,024,432 3,367,039

u,IIu7,287 $ 1,682,u8~

T he accompa nying notes are an integra l part of these financ ial statements.

Page 11

CITY OF SYRACUSE INDUSTRIAL DEVELOPMENT AGENCY (a Component Unit of the City of Syracuse, New Yorl,) Notes to Financial Statements December 31, 2007

Note 1 - Nature of the organization and significant accounting policies

Nature oftlte orgallilatioll

======-~TJle City_oLSyJ:acuse-IndustriaLDe"e lopment_~gency_(SIDA) is-a-publiG-benefit-agenc),-established-in- i9775,9,==;=-- - -::to enhance economic development act ivities in the City of Syracuse (New York). SIDA's programs include the issuing of industrial revenue bonds (Note 2) and the making of loans under the HUD Section 108 Program (Note 3), the Downtown Commercial Rehabilitation Loan Program (Note 4) and the SIDA Development Fund (Note 5). SIDA is treated by the City of Syracuse as a component unit and is integral to the overall economic development plans of the City.

The basic financial statements of the Agency have been prepared in accordance with accounting principles generally accepted in the United States of America as applied to government units. The Governmental Accounting Standards Board (GASB) is the accepted standard setting body for establishing governmental accounting and financial reporting principles. All of the Agency's funds are proprietary funds, and, therefore, include only business-type activities. There are no material differences between a) net assets and fund balances, and b) changes in net assets and changes in fund balances, and, therefore, no reconciliat ion schedu les of these items are included in this rep0l1.

Basis of pre selltati 011

Agellcy-wide fillallcial statemellts - The agency-wide financial statements include the Statement of Net Assets and the Statement of Activities. These statements report financial information for the Agency as a whole. Individual funds are not presented in the agency-wide fi nancial statements. The Agency has determined that all of its activities are business-type, which are predominantly or entirely financed with fees and loan repayments from external parties.

The Statement of Activities reports the expenses of a given function offset by program revenues directly connected with the functional program. A function is an assembly of similar acti vities and may include portions of a fund 01' summarize more than one fund to capture the expenses and program revenues associated with a distinct fu nctional activity. Program revenues include charges for services and grants and contributions. These revenues are subject to externally imposed restrictions to these program uses. PILOT revenue, gain on the sale of real property, and other revenue sources not properly included with program revenues are reported as general revenues.

FUlld fillall cial statemellts - Fund financial statements are provided to all of the Agency's funds. Major individual agency funds are rep0l1ed in separate columns with compos ite columns for nonmajor funds.

Measuremellt focus, basis of accoulltillg, al/{I fillallcial statemellt preselltatioll

The financial statements of the Agency are prepared in accordance with generally accepted accounting principles (GAAP). The Agency's report ing entity applies all relevant Governmenta l Accounting Standards Board (GASB) pronouncements. The agency-wide financial statements apply Financial Accounting Standards Board (FASB) pronouncements and Accounting Principles Board (APB) opinions issued on or before November 30, 1989, unless those pronouncements conflict wi th 01' contradict GASB pronouncements, in which case, GASB prevails.

Page 12

CITY OF SYRACUSE INDUSTRIAL DEVELOPMENT AGENCY (a Component Unit of the City of Syracuse, New Yorl,) Notes to Financial Statements December 31, 2007

Note 1 - Nature of the organization and significant accounting policies - continued

The agency-wide statements use the economic resources measurement focus and the accrual basis of accounti ng generally including the rec lassification or elimination of internal activity (between or within funds) . Revenues are recorded when earned and expenses are recorded when a liability is incurred, regard less of the

= ======cttiiming-ofTelare·d-clfslrilj)ws.-PILOT revenues are recognize<nlflhe year for wlliChtney are due whi"e"g"'r"'a""n"ts= ==---are recogni zed when grantor eligibility requirements are met.

Proprietary fund financial statements rep0l1 using the current financial resources measurement focus and the modified accrual basis of accou nting. Revenues are recognized when they are both measurable and avai lable. Available means collectible withi n the current period or soon enough thereafter to pay current li abilities. Expenditures are recorded when the related fund liability is incu rred.

Flllld types alld major jllllds

The Agency reports all its activities as proprietary funds, since all of its activi ties are financed in whole, or in substantial part, by fees, loan repayments, and grants.

The Agency reports the following major proprietary fund s:

Operatillg jillld - reports as the primary fund of the Agency. This fund is used to account for all financial resources not reported in other funds.

HUD-JOS jillld - reports all loan activi ty received and disbursed under Section 108 of the Housing and Community Development Act of 1974. The primary activity of this fund is borrowing from the Department of Housing and Urban Development, and reloaning of the borrowing proceeds to qualified developers.

The Agency also reports other (non major) proprietary funds in total on the funds financial statements, and provides detail s of these funds as supplemental information on the combining financial statements on pages 28 and 29 of this report. In addition, this report includes supplemental schedules of industrial revenue bonds and other financing on pages 30 through 33, which display the Agency's fina ncing activities that are not included in the Agency's basic financial statements.

S igllificallt accolllltillg policies

The attached financial statements have been prepared using the accrual basis of accounting.

Depreciation is calculated on a straight-line basis over the estimated useful lives of the assets.

SIDA's sole function is to enhance economic development activities through the making and facilitating of business loans. Virtually all of its expenses are incurred to fulfill this function . Management and general expenses and fund raising expenses are immaterial and are not segregated in the attached financial statements.

SIDA uses the allowance method to report loans of doubtful coll ectibility.

SIDA considers its lending activities, descri bed in Notes 3, 4 and 5, as operat ing activit ies for purposes of the statement of cash flows.

Cash and cash equivalents include all monies in banks and highly liqu id investments with maturity dates of less than three months. At various times during the year, SIDA's cash and cash equivalents balances exceeded the insured limi ts of the Federal Deposit Insurance Corporation. However, SIDA's accounts were fully collatera li zed by securit ies pledged by the depository bank.

Page 13

CITY OF SYRACUSE INDUSTRIAL DEVELOPMENT AGENCY (a Component Unit of the City of Syracuse, New York) Notes to Finaucial Statements December 31, 2007

Note 1 - Nature of the organization and significant accounting J)olicies - continued

The preparation of financial statements in conformity with generally accepted accounting principles requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts

.-=-----,=====;<o~lf revenues-and-expenses-during:the reporting-period. kctual-results-cllllltlOifferfrom those esliii'm;;;a"'e"s:::'. ======---::

Note 2 - Indush'ial Revenne Bonds/Other Financing

The City of Syracuse Industrial Development Agency is empowered to finance the acquisition, construction or reconstruction of manufacturing, warehousing, research, commercial, industrial and pollution control projects. SIDA raises funds to accomplish these purposes by issuing negotiable tax-exempt or taxable indust rial revenue bonds (lRB) and by participating in other financing arranged by/for the developers of the projects.

SlDA can provide up to 100% financing for an approved project including the cost of land, construction, equipment, planning and fees. Financing is generally provided at interest rates I Y, to 2% lower than conventional rates. SlDA finances individual projects by issuing revenue bonds in its own name. These bonds are secured by a mortgage on the property and a subsequent lease to the company. The company sell s the bonds to banks at a rate lower than the conventional interest rate. The bonds become an obligation of the company and are amortized by the revenue from the project. Typically, upon completion of a project, the facilities, improvements or equipment are leased to the company for a term equal to the term of the bond issue, which usually ranges from 10 to 25 years. The annual lease payments equal the annual principal and interest due on the bonds. At the end of the lease term, the company has the option of purchasing the project for one dollar. The assets and liabilities of these projects are not reflected in the attached financial statements, since SlDA treats the projects and bonds as assets and liabil ities of the individual developers.

SlDA does, however, own a project whose financial activity is refl ected in the attached financial statements, This project is more fully described in Note 6.

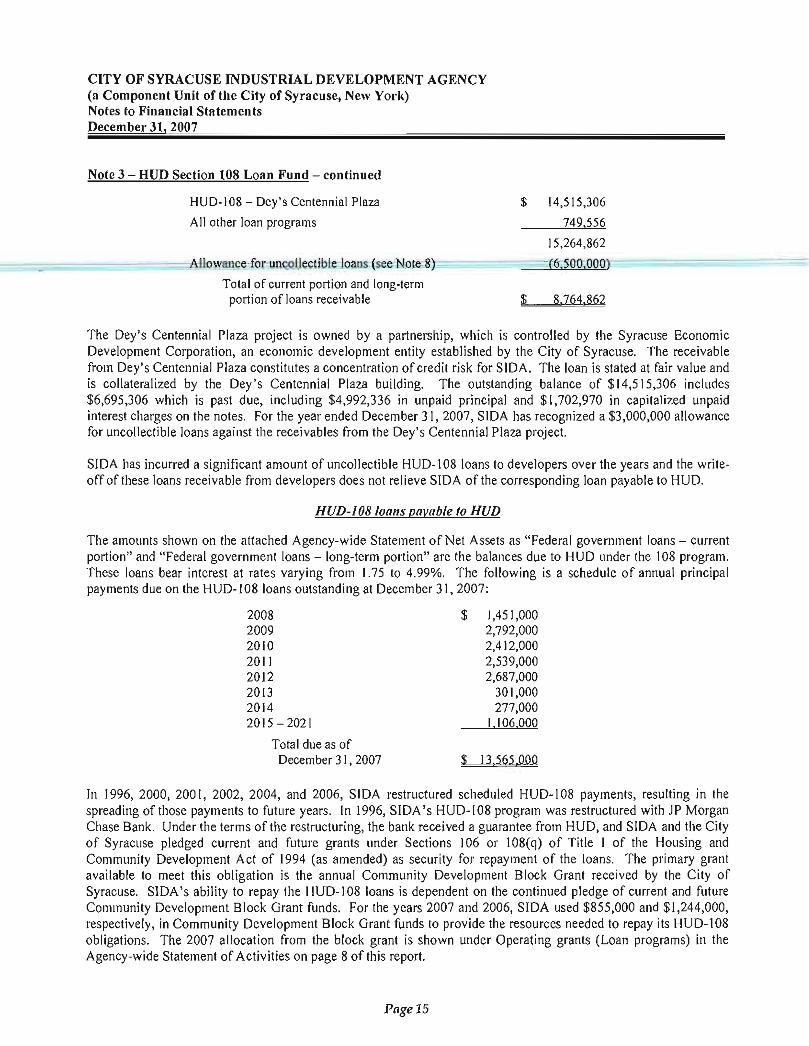

Note 3 - BUD Section 108 Loau Fund

Under Section 108 of the Housing and Community Development Act of 1974, SIDA receives loans from the Department of Housing and Urban Development (HUD) which it re-Ioans to industrial and commercial users for long-term fixed asset financing, The program is designed to stimulate private sector investment to retain and create permanent job opportunities for low and moderate income City residents by requiring a minimum of 50% private sector participation in each project. All funds received by SIDA under this program are payable back to HUD at interest rates of approximately 1% less than those charged by SlDA to developers. Any profit or loss generated in this fund is transferred to SlDA 's operating fund,

HUD-JOBloaus receivable (rom tlevelopers

The amounts shown as "Loans receivable - current portion" and "Loans receivable - long-term portion" in the attached Agency-wide Statement of Net Assets, are primarily made up of HUD-108 loans receivable from developers. As of December 31, 2007, one project-Dey's Centennial Plaza- accounts for all of SIDA 's HUD-108 loan receivables. The following is a summary of the receivable balances as of December 31, 2007:

Page 14

CITY OF SYRACUSE INDUSTRIAL DEVELOPMENT AGENCY (a Component Unit of the C ity of SY"acuse, New York) Notes to Financial Statements December 31, 2007

Note 3 - HUD Section 108 Loa n Fnnd - continued

HUD·I 08 - Dey's Centennial Plaza

All other loan programs

$ 14 ,5 15,306

749,556

15,264,862

(6500,000) ============A"'ll!l'lowa llce~for IInco llectib l"l oan s~(see Note~8~=====~;;;(Q;;~~ ,-~=======,-----

Total of current portion and long·term porti on of loans receivable $ 8 Z61862

The Dey's Centennial Plaza project is owned by a partnership, which is controlled by the Syracuse Economic Development Corporat ion, an economi c development enti ty establi shed by the City of Syracuse. The receivable from Dey's Centenni al Plaza constitutes a concentration of credit risk for SIDA. The loan is stated at fair value and is collateralized by the Dey' s Centennial Plaza building. The outstanding balance of $ 14,5 15,306 includes $6,695,306 which is past due, including $4,992,336 in unpaid principal and $ 1,702,970 in capitalized unpaid interest charges on the notes . For the year ended December 31,2007, SIDA has recogni zed a $3,000,000 allowance fo r uncollectible loans against the receivables from the Dey's Centenni al Pl aza project.

SIDA has incurred a significant amount of uncollectible HUD~ 108 loans to developers over the years and the write~ off of these loans receivable from developers does not re lieve SIDA of the correspond ing loan payable to HU D.

HUD~108 10{IIIS payable 10 HUD

The amounts shown on the attached Agency~wide Statement of Net Assets as "Federal government loans - current portion" and "Federal government loans - l ong~term portion" are the balances due to HUD under the 108 program. These loans bear interest at rates varying from 1.75 to 4.99%. The following is a schedule of annual principal payments due on the HUD~ I 08 loans outstanding at December 31,2007:

2008 $ 1,45 1,000 2009 2,792,000 2010 2,4 12,000 20 11 2,539,000 20 12 2,687,000 20 13 30 1,000 201 4 277,000 20 15 - 2021 1,106,000

Total due as of December 3 I, 2007 $ 13565QQQ

In 1996, 2000, 200 I, 2002, 2004, and 2006, SIDA restructured scheduled HUD~ I 08 payments, resulting in the spreading of those payments to futu re years. In 1996, SIDA's H UD~108 program was restructured wi th jp Morgan Chase Bank. Under the terms of the restructuring, the bank received a guarantee from HUD, and SIDA and the City of Syracuse pledged current and future grants under Secti ons 106 or 108(q) of Ti tle I of the Housing and Community Development Act of 1994 (as amended) as security fo r repayment of the loans. The primary grant available to meet this obligation is the annual Community Development Block Grant received by the City of Syracuse. SIDA's ability to repay the HU D·1 08 loans is dependent on the continued pledge of current and future Communi ty Development Block Grant fu nds. For the years 2007 and 2006, SIDA used $855,000 and $ 1,244,000, respectively, in Community Deve lopment Block Grant funds to provide the resources needed to repay its HUD~ 1 08

obl igations. The 2007 allocation from the block grant is shown under Operating grants (Loan programs) in the Agency~wide Statement of Activities on page 8 of this report.

Page l S

CITY OF SYRACUSE INDUSTRIAL DEVELOPMENT AGENCY (a Component Unit of the City of Syracuse, New York) Notes to Financial Statements December 31, 2007

Note 4 - Downtown Commercia l Rehabilitation Loan Fund

The Downtown Commercial Rehabilitation Loan Program was originally funded from the annual entitlement grant of the City of Syracuse's Depal1ment of Community Development and by the repayment of outstanding loans. The fund is used to provide rehabilitation assistance to owners of commercial or mixed-use buildings in the Downtown Special Assessment District. Loan repayments are restricted for use in future downtown commercial rehabi litation

====~~I·~ams~. ~~~~~~~~~~~~~~~~~~~~~~~~~~~=---~

Note 5 - SIDA Development Fund

SIDA has been designated by the City of Syracuse to receive, and subsequently loan for commercial use, funds collected by the City under a past tax amnesty program. Under this program, SIDA serves as a conduit between the loan recipient and the City of Syracuse. All earnings and potential losses from the activities in this fund revert back to the City, with the end result that SIDA has no net assets in the Development Fund.

Note 6 - Land and Bu ildings - Center Armory Garage Facility

The Center Armory Garage Facility is owned by SIDA and is located in the Armory Square historic district in downtown Syracuse. The project was financed by SIDA with revenue bonds, which included both bonds that are paid-off as they mature and bonds paid via sinking fund payments. As of December 31, 2007, only the bonds paid via sinking fund payments are still outstanding. The following is a schedule of current and future bond payments:

Sinking Funds Tax Exempt Taxable

(6.75%) (8.8%) Total

2008 $ 50,000 $ 70,000 $ 120,000 2009 50,000 75,000 125,000 2010 55,000 80,000 135,000 20 11 60,000 85,000 145,000 2012 65,000 90,000 155,000 2013 70,000 95,000 165,000 2014 75,000 100,000 175,000 2015 85,000 110,000 195,000 2016 90,000 115,000 205,000 2017 100,000 125,000 225,000

Total payments $ ZQQ QQQ $ 215 QQQ $ 1615 QQQ

SIDA leases the parking facilities to the Syracuse Economic Development Corporation (SEDCO), which subleases the facilities to the City of Syracuse (City). The lease and sublease, which expire on December 1,2017, call for rent payments to be made by the City to SIDA in an amount sufficient to pay the interest and principal due on the bonds and to maintain various bond reserve funds at required levels.

SIDA is depreciating the garage structure on a Slraight-line basis over an estimated usefu l life of twenty-five years. The following is a summary of the cost and accumu lated depreciation of the garage at December 31,2007:

Land

Building

Total

$

$

Cost

50,000

2,815,320

2865,12Q

Page 16

Accum ulated Den reciation

$

( 1,576,579)

U I 5Z65Z9)

Net

$ 50,000

1,238,74 1

$ 1,288,111

CITY OF SYRACUSE INDUSTRIAL DEVELOPMENT AGENCY (a Component Un it of the City of SyraclIse, New York) Notes to Financial Statements December 31, 2007

Note 7 - Other receivables

The amollnt shown as other receivables at December 31,2007 is made up of the following:

Masonic Lofts fee $ 40,543

Crouse.HospitaLfee 239;3 12

Onondaga County - Atrium Garage 105,980

Syrwil Associates (SIBLEY's) Payment in lieu of tax agreement (PI LOT) 120,540

Lakefront PILOT 87,492

Other 7,555

Total $ 60 I 122

Note 8 - Allowance for uncollectible loans

As of December 31, 2002, SlDA adopted a change in accounting policy for uncollectible loans. Prior to the change, SlDA used the direct write-off method for uncoll ectib le loans. SlDA continues to use the direct write-off method for immaterial loan balances. The change resulted in an addi tion to losses for uncollectible loans of $ 1,650,000 for the year ended December 3 I ,2002. Losses for uncollectible loans may be summarized as follows:

2004 2007 2006 2005 and 2003 2002

Direct write-offs $ $ $ $ 1,937 $ 392,523

Allowance (see Note 3) 3,000,000 3,000,000 500,000 1,650,000

Losses from uncollectible loans UQQQOQQ $ 3 QQQ QQO $ SQQ QQQ $ 1231 $ 2Q12 m

The $ 1,650,000 allowance was established in 2002 as a 100% reserve against loans due from Spectrum Medsystems, Inc. During 2003, SlDA determined that these loans were completely worthless and they were written-off against the allowance. SlDA seized the loans' co llateral, a building, and sold the building and land in 2004 for $825,02 1, with a gain on the sale transaction of $600,964.

For 2005, SlDA commenced recognition of the doubtful collectibility of a portion of its loans to the Dey's Centennial Plaza project (see Note 3), by record ing $500,000 in bad debt expense. For 2007 and 2006, SlDA recogni zed an add itional $3,000,000 each year in bad debt expense, and this amount is shown under the caption "Losses from uncollect ible loans" in the Statement of Revenue, Expenditures, and Changes in Fund Balances -Proprietary Funds, on page lO af this rep0l1. SlDA will continue evaluat ing the collectibility of these loans, and will increase or decrease the allowance for uncollectible loans in future years based on its analysis of the potential collectibility of its loans to the Dey's Centennial Plaza project.

Note 9 - Unused letter-of-credit

During 2000, SlDA established a letter-of-cred it wi th M & T Bank for $1,285,000. As of December 3 1, 2007, SlDA has not drawn on the letter-of-cred it. The letter-of-cred it is designed to provide collateral to HUD for a restructured H UD-I 08 loan payment.

Page 17

CITY OF SYRACUSE INDUSTRIAL DEVELOPMENT AGENCY (a Component Unit of the City of Syracuse, New Yorl,) Notes to Financial Statements December 31, 2007

Note 10 - Brownficlds Economic Development Inccntive (BEDn grants

In 1998 and 1999, SIDA received approval for (2) Brownfields Economic Development Incentive (BED I) grants in the amounts of $1 ,000,000 and $875,000, respective ly, for the City Crossroads project. As of December 3 1, 2007, SIDA had drawn down the following amounts on these grants:

Received in fisca l year BEOI grant ending December 31 1998 1999

2000 $ 400,101 $ 2002 599,899 293,940 2003 91,430

Total drawn $ I QQQ QQQ $ 38:l,lZQ

The remainder of the 1999 grant ($489,630) has not been drawn down by SIDA. The amounts that were drawn down were recorded as income in the year received .

Each of the granls contains a provision which requires SIDA to enter into HUD-I08 loans to development projects sited in the City Crossroads area. The required ratio of loans to grant dollars for each of the grants is as follows:

1998 grant 1999 grant

Ratio of loan $ to grant $

3: I

2.5: I

As of December 31,2007, SIDA had made $ 1,950,000 of HUD-I 08 loans to City Crossroads projects. Additional HUD-108 loans in the City Crossroads area would be needed to meet the required ratios of loan dollars to grant dollars noted above. As of December 31, 2007, the grant funds which have been "earned" by the issuance of loans is as fo llows:

BEOI grant 1998 1999 Total

Grant dollars received $ 1,000,000 $ 385,370 $ 1,385,370 Grant dollars "earned" by

making loans: 1998: $1,950,000 + 3 = 650,000 650,000 1999: $-0- + 2.5 = -0- -0-

Balance $ 35Q QQQ $ 38531Q $ 135,31Q

Management of SIDA is continuing to exp lore aclions needed to complete the requirements of these BEDI grants.

Note II - Destiny USA fees

Destiny USA Project- SIDA has participated in the financing of the Carousel Center Mall, holds nominal title to the project, and continues to be active in the financ ing of the project as it transforms from Carousel Center into Destiny USA. Financing information as of December 31, 2007 is shown on pages 31 and 32 of this report. In early 2007, the developer received fin ancing for Phase I of the conversion to Destiny USA, and commenced construction of a major expansion to the existing mall. In February, 2007, SIDA received a development fee of $5,400,000 for its participation in the financing of Ihe project. The use of this fee is restricted to development projects in the lakefront area near the mall . A separate $60,000,000 project fee is being paid to SIDA over ten years, with $11,000,000 paid to SIDA in February, 2007, and $11,000,000 in February, 2008. This separate fee is being passed through by SIDA to the City of Syracuse, New York and the County of Onondaga, New York to be used for general economic development purposes.

Page 18

CITY OF SYRACUSE INDUSTRIAL DEVELOPMENT AGENCY (a Component Unit of the City of Syracuse, New York) Notes to Fiuancial Statements December 31, 2007

Note 12 - Prior-year summarized comparative financial information

The financial statements include certain prior-year summarized comparative financial information in total but not by net asset class. Such information does not include suffi cient detail to constitute a presentation in conformity with generally accepted accounting principles. Accordingly, such information should be read in conjunction with

o----=~th·e-Agency'Sfinancial statements fori he year enaeaLlecember'J 1, 2006, from which the summarized information was derived.

Page 19