Embed Size (px)

Citation preview

171

Panaji, 9th May, 2013 (Vaisakha 19, 1935) SERIES I No. 6

Reg. No. GR/RNP/GOA/32 RNI No. GOAENG/2002/6410

PUBLISHED BY AUTHORITY

Suggestions are welcome on e-mail: dir–[email protected]

INDEX

Department Notification/Order/Corri. Subject Pages

1. Animal Hub. & Vet. Services Ord.- 2-13-93-AH/2013-14/ Revised rates for service charges. 172Dir. & ex officio Jt. Secy. /650

2. a. Finance Not- DA/Admn/11-12/2013- Rules for conducting the Initial Recruitment 174Rev. & Exp. Division -14/TR-304/17 Examination Training and Final ExaminationDirectorate of Accounts of the Accountants.Dir. & ex officio Jt. Secy.b. —do— Corri.- DA/Admn/11-12/ Correction done in the Notification Number. 175

/13-14/1563. a. Goa Legislature Secretariat Bills- LA/LEGN/2013/329 The Goa Tax on Infrastructure (First Amendment) 176

Bill, 2013.b. —do— LA/LEGN/2013/330 The Indian Stamp (Goa Amendment) Bill, 2013. 181c. —do— LA/LEGN/2013/331 The Goa Value Added Tax (Seventh Amendment) 198

Bill, 2013.d. —do— LA/LEGN/2013/332 The Goa Entertainment Tax (Amendment) Bill,2013. 225e. —do— LA/LEGN/2013/333 The Goa Tax on Entry of Goods (Amendment) 230

Bill, 2013.f. —do— LA/LEGN/2013/373 The Goa Land (Prohibition on Construction) 241

(Amendment) Bill, 2013.g. —do— LA/LEGN/2013/374 The Goa (Right of Citizens to Time-bound Delivery 244

of Public Services) Bill, 2013.h. —do— LA/LEGN/2013/382 The Goa Appropriation (No. 3) Bill, 2013. 252

4. Information Technology Ord.- 1(125)/DOIT/Contract Creation of posts– Dte. of Information Technology. 255Dir. & ex officio Jt. Secy. Appointment/2012/262

5. Labour Not.- 24/14/2012-Lab/209 Scheme for giving stipend to the trainees belon- 256Under Secretary ging to the SC/ST Community enrolled under

various Labour Welfare Centres in the State of Goa.

6. Law & Judiciary Not.- 8-36-2012-LD(Estt)/ Remission of fees for the registration of Deed of 257Law (Estt.) Division /689 Gift of Land.Under Secretary

7. Personnel Ord.- 15/7/2003-PER Results of Departmental Examination for Officers. 257Under Secretary

8. Public Health Ord.- 38/79/2013-I/PHD Change in name of Tisk Usgao Hospital. 258Under Secretary

9. Revenue Not.- 16-11-2009/RD(Part) Draft Rules— The Goa Land Revenue (Inspection, 258Under Secretary Search and Supply of Copies of Land Records)

(Amendment) Rules, 2013.

10. Transport Not.- D.Tpt/STA/1275/2013 Rates fixed for Self Employed Tourist Taxi 259Dte. of Transport Operators.Dir. & ex officio Addl. Secy.

11. a. Women & Child Devep. Not.- 2-98-2008/DW&CD/ Amendment to Retirement Benefit Scheme for 260 Dir. & ex officio Jt. Secy. /ICDS(3)/4234 Anganwadi Workers/Anganwadi Helpers.

b. —do— Ord.- 2-73-97-ICDS/Part-VI/ Revision of existing rate of honorarium to the 261/4235 Anganwadi Workers/Anganwadi Helpers.

c. —do— 2/279/LL/2012/DW&CD/4231 Laadli Laxmi Scheme. 262

OFFICIAL GAZETTE — GOVT. OF GOASERIES I No. 6 9TH MAY, 2013

172

GOVERNMENT OF GOADepartment of Animal Husbandry

Directorate of Animal Husbandry & Veterinary Services___

Order

2-13-93-AH/2013-14/650

The Government has approved the revision for Service Charges for various services providedby the Department of Animal Husbandry & Veterinary Services and the revised rates of theservices are hereby published for the information of the general public.

Sr. No. Item of Revenue Receipt Revised Rate

1. Sale of milk (cows) Rs. 36/- per litre(buffaloes) Rs. 40/- per litre

2. Sale of manure (cow dung) Rs. 500/- per M.T.

3. Sale of Green Fodder Re. 1/- per kg.

4. Sale of fruitsMango for 3 years(Auction) Rs. 65,000/-Coconut for 3 years(Auction) Rs. 30,000/-Cashew for 3 years(Auction) Rs. 10,000/-

5. Surplus animals Rate is variable de-pending on age,sex, stage of lacta-tion, breed etc.

6. Sale of poultry birds Rs. 30/- to Rs. 175/-depending uponthe age.

7. Culled poultry birds Rs. 75/- each.

8. Poultry manure Rs. 500/- per M.T.

9. Cess on fluid milk 0.15 paise per litreof milk sold.

LARGE ANIMALS INCLUDING GOATS, SHEEP & PIGS:

10. 1st visit for a new treatment case to the farmer’s house Rs. 20/-

and repeat visit for same case Rs. 10/-

11. Cases brought at the Centres (per visit) Rs. 5/-

12. Post bite anti-vaccine per shot per animal Rs. 20/-

13. Vaccination against infectious and contagious disease would continue toremain free —

14. No charges are to be collected when reports for infectious and contagiousdiseases are attended —

15. All artificial inseminations as many times required and treatment of infertilitycases will be provided free of cost to large animals —

16. Major Surgery Rs.100/-

17. Minor Surgery Rs. 50/-

18. Post operative care will be provided free of cost to large animals —

OFFICIAL GAZETTE — GOVT. OF GOA

SERIES I No. 6 9TH MAY, 2013

173

Sr. No. Item of Revenue Receipt Revised Rate

FOR PET DOGS, CATS, ETC.:

19. House visits are not to be encouraged. However, in emergency if a house visit isundertaken (for the first visit) Rs. 200/-and for subsequent visits Rs. 75/-

20. Treatment/Examination at the Hospitals & Dispensaries Rs. 50/-

21. In case of Anti-Rabies vaccine for dogs, for the first dose Rs. 100/-

22. And for subsequent dose (which includes the cost of vaccine) Rs. 60/-

23. Per post bite vaccine for pets at the centre (including cost of vaccine) Rs. 100/-

24. Post bite vaccine for pets outside centre (including cost of vaccine) Rs. 150/-

25. All other vaccines for dogs and the other pets brought by the owner at theHospital/Dispensary Rs. 50/-

26. Major Surgery Rs. 500/-

27. Minor Surgery Rs. 300/-

28. Post operative care Rs. 200/-

POULTRY:

29. Service charges for 100 birds inclusive of vaccines Rs. 20/-Any farmers having less than 100 birds will be entitled for free services —

GENERAL:

30. Radiography Examination (X’Ray) Rs. 500/-

31. Ultra Sonography Rs. 500/-

32. Euthanasia (for small and large animals also) Rs. 200/-

33. Processing fees for various Departmental Schemes Rs. 50/-

34. Issue of Health Certificates for transport of animals outside India Rs. 500/-

35. Issue of Health Certificates for transport of animals within India Rs. 300/-

36. Farm manure of Cattle and Piggery Farms (per metric tonne) Rs. 400/-

37. Per bundle of 25 kgs. of dry hay Rs. 100/-

DISEASE INVESTIGATION UNIT LABORATORY FINDINGS:

38. Medicines available in the Centres used for treatment, shall be free of cost —

39. Blood test, urine test, faecal examinations and skin scrapping etc., will be free in case of large animals -—

40. Blood test, urine test, faecal examinations and skin scrapping etc., in case ofpet/small animals Rs. 75/-

41. Post-mortem examination in case of small and large animals Rs. 300/-

42. Post-mortem for poultry birds Rs. 25/-

43. Meat samples examination (per tonne) and for issue of certificate Rs. 500/-

44. Culture with antibiotic sensitivity test Rs. 200/-

45. Test conducted by Biochemistry Analyser, SGOT, SGPT, Urea, Creatinine,Bilirubin Glucose, Protein Albumin, Na K, Cl, Ca, etc., each test Rs. 250/- per test

GOA ANIMAL PRESERVATION ACT, 1995:

46. Ante-Mortem charges for animals slaughtered for beef per animal Rs. 50/-

47. Inspection charges for beef or beef products brought in to Goa for sale per kg. wt. Rs. 2/-

OFFICIAL GAZETTE — GOVT. OF GOASERIES I No. 6 9TH MAY, 2013

174

Sr. No. Item of Revenue Receipt Revised Rate

48. Meat examined and certified for export including issue of certificate per kg. wt. Rs. 2/-

49. Animals belonging to Government Department and Dwarka Goseva Ashramwill be provided with free services —

ACCOMMODATION:

50. Self contained rooms for guests, other than STC/FTC trainee (Twin Sharing) Rs. 300/- per day

By order and in the name of the Governor of Goa.

Dr. B. Braganza, Director & ex officio Joint Secretary (AH).

Panaji, 2nd May, 2013.——— ———

Department of FinanceRevenue & Expenditure Division

Directorate of Accounts___

Notification

DA/Admn/11-12/2013-14/TR-304/17

Sub.: Rules for conducting the InitialRecruitment Examination Training and FinalExamination of the Accountants.

Read: Notification No. 4/18-2/66/Vol.II/1568

dated 25-12-1966.

In exercise of the powers conferred underRule 20 of the aforesaid Rules, the procedure,syllabus, scheme of examination and the

process of selection of Accountants containedin the relevant Rules, are hereby amended inrespect of filling up the post of Accountantsfrom amongst Departmental candidates i.e.Accounts Clerks/U.D.C. of the Directorate ofAccounts, as follows.

2. All Accounts Clerks/Treasurer Grade II &III of the Directorate of Accounts who havecompleted 02 years regular service in thegrade, shall be required to appear for writtenexamination to be conducted by theDirectorate of Accounts on such a date, venueand time as the Director may, by notification,prescribe.

3. The syllabus and pattern of examinationshall be as under:—

Subject Maximum marks Minimum qualifying

allotted marks

Paper (I)

Duration: 03 hours

Paper type: Subjective (90%) & Objective (10%)

English and General Knowledge

(a) Report Writing/Noting/Drafting 100 40

(b) Comprehension

(c) Precise

(d) Business Communication

(e) Essay/Composition

(f) Grammar

(g) General Knowledge

Paper (II)Duration: 02 hoursPaper type: Subjective (50%) & Objective (50%)

OFFICIAL GAZETTE — GOVT. OF GOA

SERIES I No. 6 9TH MAY, 2013

175

Subject Maximum marks Minimum qualifying

allotted marks

Section(A): Mathematics 30 15

Averages, Ratio & Proportion, Computation of Interest (Simpleand Compound Interest), Permutation & Combination, Linear& Simultaneous equations, Mensuration and Geometry,Statistics, Probability.

Section(B): Book keeping & Accountancy 20 10

Book keeping & Accountancy, Accounting Principles, AccountingStandards, Recording of transactions & Preparation of Trial Balance,Depreciation, Income tax calculations.

Section(C): Basic Service & Accounts Rules 50 25

FR/SR, TA/DA Rules, Medical Attendance Rules, Pay & OtherAllowances Rules, Leave Rules, L. T .C. Rules, Loans & Advances toGovernment Servants, GPF/LPS Rules, Works Manual.

the extent guidelines issued in this regard fromtime to time.

By order and in the name of the Governorof Goa.

G. S. Potekar, Director & ex officio JointSecretary (Accounts).

Panaji, 6th May, 2013.

_________Corrigendum

DA/Admn/11-12/13-14/156

Read: (1) Notification No. DA/Admn/11-12/13-

-14/01 dated 12-4-2013.

(2) Corrigendum No. DA/Admn/11-12/

/13-14/07 dated 12-4-2013.

In the above cited Notification theexpression “Read: Notification No. 4/13-2/66//Vol.II/1568 dated 25-12-1966 published inthe Official Gazette, Series I No. 39 dated29-12-1966,” shall be substituted as“Notification No. 4/18-2/66/Vol.II/1568 dated25-12-1966 published in the GovernmentGazette, Series I No. 39 dated 29-12-1966.”

The other contents of the order remainunchanged.

By order and in the name of the Governorof Goa.

Gurunath S. Potekar, Director & ex officioJoint Secretary (Accounts).

Panaji, 3rd May, 2013.

4. All departmental candidates who aredeclared successful as per the qualifyingcriteria laid down above shall be called for aviva-voce/oral interview to be conducted bythe Departmental Selection Committeecomprising of the Director of Accounts, thenext immediate senior officer of the Directorateof Accounts and the Under Secretary to theFinance Department, Government of Goa.

5. The selection criteria shall be as follows:

The written examination will carry aweightage of 85% while viva voce/oralinterview will carry a weightage of 15%. Themarks secured by the departmentalcandidates in written examination will becomputed proportionate to 85 marks andmaximum of 15 marks will be awarded at oralinterview stage. If the departmental candidatedoes not appear for the oral interview or scoreszero mark during oral interview shall not beconsidered for selection. Appearing for oral/viva voce is mandatory.

6. A merit list will be drawn for the purposeof selection and offer of appointment shall begiven as and when vacancies occur during therecruitment year.

7. The other condition for recruitment,reservation and procedure for application shallbe as defined by the Government and as per

OFFICIAL GAZETTE — GOVT. OF GOASERIES I No. 6 9TH MAY, 2013

176

Goa Legislature Secretariat__

LA/LEGN/2013/329

The following bill which was introducedin the Legislative Assembly of the State ofGoa on 29th April, 2013 is hereby publishedfor general information in pursuance of Rule--138 of the Rules of Procedure and Conductof Business of the Goa Legislative Assembly.

________

The Goa Tax on Infrastructure(First Amendment) Bill, 2013

(Bill No. 15 of 2013)

A

BILL

to amend the Goa Tax of Infrastructure Act,2009 (Goa Act 20 of 2009).

Be it enacted by the Legislative Assemblyof Goa in the Sixty-fourth Year of the Republicof India, as follows:—

1. Short title and commencement.— (1)This Act may be called the Goa Tax onInfrastructure (First Amendment) Act, 2013.

(2) It shall come into force on such dateas the Government may, by notification inthe Official Gazette, appoint.

2. Amendment of section 2.— In section2 of the Goa Tax on Infrastructure Act, 2009(Goa Act 20 of 2009) (hereinafter referred toas the principal Act),—

(i) clause (a) shall be re-numbered asclause (aa) and before clause (aa) so re-numbered, the following clause shall beinserted, namely:—

“(a) “built up area” means all areaswhich are built upon and essentiallyforming part of the building/buildings andincludes,—

(i) floor area i.e. covered area of thebuilding/buildings in all floor levelsadded together;

(ii) basement or cellar;

(iii) balcony/verandah/passages//lobby;

(iv) mezzanine floor;

(v) stilt area;

(vi) swimming pool whether coveredor uncovered;

(vii) staircases including fire escapestaircase, ramps (internal and/orexternal);

(viii) lift area at one level;

(ix) atrium/podium;

(x) terraces at intermediate floors; and

(xi) equipment room, generator room,security room; but does not include areasof open terraces on the top most floor ofthe building/buildings, un-storeyedporch, septic tanks, soak pits, sewagetreatment plants, man holes, drainage,gutters, chambers, wells, fountains,steps, water tanks, sumps, rain waterharvesting tanks, structures forhandling/sorting of waste having aheight of not more than 2.5 meters andhaving opening on at least two sides,pump house admeasuring an area notexceeding six square meters, swingframes, compounds and gates;”;

(ii) clause (d) shall be omitted;

(iii) after clause (i), the following clauseshall be inserted:—

“(ia) “other building” means abuilding or structure other thanresidential building, commercialbuilding or industrial building;”;

3. Amendment of section 3.— In section 3of the principal Act,—

(i) after sub-section (1), the followingsub-section shall be inserted, namely:—

“(1A) On any construction to beundertaken by any corporation orundertaking constituted under theCentral or State enactment, or any StateGovernment, or local bodies on any landspecified in the Schedule hereto, thereshall be levied and paid a service chargeon infrastructure at the rates specifiedin the said Schedule.”.

(ii) in sub-section (4), for the word “tax”,wherever it occurs, the words “tax orservice charge” shall be substituted;

OFFICIAL GAZETTE — GOVT. OF GOA

SERIES I No. 6 9TH MAY, 2013

177

(iii) in sub-section (5), for the word “tax”,wherever it occurs, the words “tax orservice charge” shall be substituted;

(iv) for sub-section (6), the following sub--section shall be substituted, namely:—

“(6) The tax and service chargecollected by the Competent Authorityshall be credited into the GovernmentTreasury and shall be utilized for worksidentified by the Government, such as,provision of water, power anddevelopment of other physicalinfrastructure.”.

4. Amendment of section 5.— In theprincipal Act,—

(i) in section 5 and in any other sections,for the word “tax” wherever it occurs, thewords “tax or service charge” shall besubstituted;

(ii) in section 5, for the words “industrialbuilding”, wherever it occurs, the words“industrial building or other building” shallbe substituted.

5. Amendment of section 6.— In sub--section (1) of section 6 of the principal Act,for the words “industrial building, whereverit occurs, the words “industrial building orother building” shall be substituted.

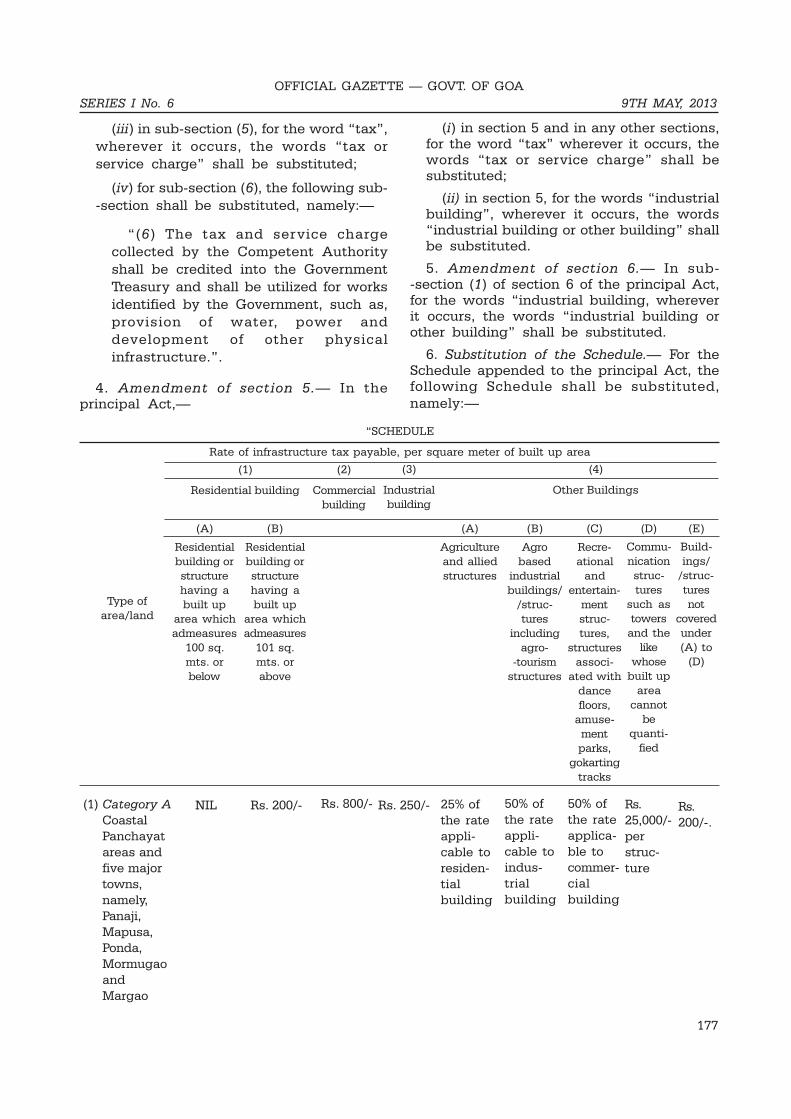

6. Substitution of the Schedule.— For theSchedule appended to the principal Act, thefollowing Schedule shall be substituted,namely:—

(C)

Recre-ational

andentertain-

mentstruc-tures,

structuresassoci-

ated withdancefloors,

amuse-mentparks,

gokartingtracks

Type ofarea/land

(A)

Residentialbuilding orstructurehaving abuilt up

area whichadmeasures

100 sq.mts. orbelow

(B)

Residentialbuilding orstructurehaving abuilt up

area whichadmeasures

101 sq.mts. orabove

(A)

Agricultureand alliedstructures

(B)

Agrobased

industrialbuildings/

/struc-tures

includingagro-

-tourismstructures

(D)

Commu-nicationstruc-tures

such astowers

and thelike

whosebuilt up

areacannot

bequanti-

fied

(E)

Build-ings/

/struc-turesnot

coveredunder(A) to

(D)

(1) Category ACoastalPanchayatareas andfive majortowns,namely,Panaji,Mapusa,Ponda,MormugaoandMargao

NIL Rs. 200/- Rs. 800/- Rs. 250/- 25% ofthe rateappli-cable toresiden-tialbuilding

50% ofthe rateappli-cable toindus-trialbuilding

50% ofthe rateapplica-ble tocommer-cialbuilding

Rs.25,000/-perstruc-ture

Rs.200/-.

“SCHEDULE

Rate of infrastructure tax payable, per square meter of built up area

(1)

Residential building

(2)

Commercialbuilding

(3)

Industrialbuilding

(4)

Other Buildings

OFFICIAL GAZETTE — GOVT. OF GOASERIES I No. 6 9TH MAY, 2013

178

Rate of infrastructure tax payable, per square meter of built up area.

(1)

Residential building

(2)

Commercialbuilding

(3)

Industrialbuilding

(4)

Other Buildings

(C)(A) (B) (A) (B) (D) (E)

(2) Category BOtherMunicipaltowns,Censustowns andVillagePanchayatsadjoiningor conti-guous tothe majortowns ofPanaji,Mapusa,Ponda,MormugaoandMargao

NIL Rs. 200/- Rs. 600/- Rs. 250/- 25% ofthe rateappli-cable toresiden-tialbuilding

50% ofthe rateappli-cable toindus-trialbuilding

50% ofthe rateappli-cable tocommer-cialbuilding

Rs.15,000/-perstruc-ture

Rs.200/-.

(3) Category COtherVillagePanchayatareas

(4) Servicecharge forbuildingscon-structedby anycorporationor under-takingconstitutedunder theCentral orStateenactment,or anyStateGovern-ment, orlocalbodies, inland/areaspecifiedabove

Rs. 200/-

75% ofthe ratespecifiedin respec-tivecategoryabove

Rs. 400/-

75% ofthe ratespecifiedinrespec-tivecategoryabove

Rs. 250/-

75% ofthe ratespecifiedinrespec-tivecategoryabove

25% ofthe rateappli-cable toresiden-tialbuilding

75% ofthe ratespecifiedinrespec-tivecategoryabove

50% ofthe rateappli-cable toindus-trialbuilding

75% ofthe ratespecifiedinrespec-tivecategoryabove

50% ofthe rateappli-cable tocommer-cialbuilding

75% ofthe ratespecifiedinrespec-tivecategoryabove

Rs.10,000/-perstruc-ture

75% ofthe ratespeci-fied inrespec-tivecat-egoryabove

Rs.200/-.

75%of therateappli-cabletoresi-dentialbuild-ing inrespec-tivecat-egoryabove.

NIL

NIL

OFFICIAL GAZETTE — GOVT. OF GOA

SERIES I No. 6 9TH MAY, 2013

179

charge collected under the said Act, for theworks identified by the Government, suchas, provision of water, power anddevelopment other related physicalinfrastructure.

Financial Memorandum

No financial implications are involved inthis Bill. However, the enhancement of therates of infrastructure tax, and levy of servicecharge, as per different geographicallocations and urbanization trend as proposedin this Bill would generate additional revenueof approximately Rs. 70 crores to theGovernment.

Memorandum Regarding DelegatedLegislation

No delegated legislation is involved in thisBill.

Porvorim Goa MANOHAR PARRIKAR

Dated: 23rd April, 2013. Chief Minister/

/Minister for TCP

Assembly Hall, N. B. SUBHEDAR

Porvorim Goa Secretary to the Legislative

Dated: 23rd April, 2013. Assembly of Goa.

_________

(Annexure to Bill No. 15 of 2013)......................................................................................................

The Goa Tax on Infrastructure Act, 2009.....................................................................................................

2. Definitions.— In this Act, unless the contextotherwise requires.—

(a) “classification of land” means theclassification assigned to land by zoning or use;

(b) “commercial building” means a buildingor structure consisting of shop, godown or officepremises, either on ground floor or any otherfloor, used wholly or partly for business activities;

(c) “competent authority” means suchauthority or officer of the Government, as theGovernment may, by notification in the OfficialGazette, specify;

(d) “floor area” means a floor area as definedin the Planning and Development Authority(Development Plan) Regulations, 2000, or anysubsequent regulations thereto made under theGoa (Regulation of Land Development andBuilding Construction) Act, 2008 (Act 6 of 2008),for the time being in force;

Statement of Objects and ReasonsThe Goa Tax on Infrastructure Tax Act, 2009

(Goa Act 20 of 2009) provides for levy ofinfrastructure tax as per the floor area of thebuilding. However, around 20% to 30% of thearea covered under stilt floors, basementfloors, mezzanine floors, balconies, passages,lobbies, stair cases, etc., are not coveredunder the “floor area”, as per the definitionof term “floor area” in the Goa LandDevelopment and Building ConstructionRegulations, 2010. These spaces are integralpart of the main building and also consumethe infrastructure facilities directly and assuch, it is felt necessary to bring the saidarea under the tax net. Hence, the Bill seeksto amend section 2 of the said Act so as todefine term “built up area” and omit clause(d) thereof.

Similarly, there are many constructionsother than residential, commercial andindustrial such as institutional buildings otherthan educational buildings, building andstructures for transportation andtelecommunication use, farm houses, dancefloors, etc. which need to be brought underthe taxation.

The Bill, therefore seeks to insert sub--section (1A) to section 3 of the said Act.

Goa has three physiographical regions,namely, the coastal area, midland areas andwestern ghats. Major developments andinfrastructure developments are concen-trated in the coastal areas and in the majortowns like Panaji, Mapusa, Ponda, Mormugaoand Margao. Commercial establishments likeshopping malls, arcades, hotels and resortsrequire major infrastructure facilities. Thevillage areas, contiguous to the major towns,many of which are identified as Census townsin the Census of India, are also showinghigher degree of urbanization and requiremore infrastructure facilities. Hence, the Billseeks to amend the Schedule to the said Act,so as to amend the said Schedule suitably.

The Bill also seeks to amend sub-section(6) of section 3 of the said Act so as toearmark and utilize the tax and service

OFFICIAL GAZETTE — GOVT. OF GOASERIES I No. 6 9TH MAY, 2013

180

(e) “Government” means the Government ofGoa;

(f) “industrial building” means any buildingor structure constructed for the purpose ofcarrying out medium and large scale industrialactivities within or outside the areas earmarkedand notified as industrial estates/areas, but doesnot include building constructed for carryingout small scale industrial activity;

(g) “infrastructure” means the provision ofpotable water, electricity and other amenitieslike roads, drains, foot paths, sewerage system,etc.;

(h) “local authority” means a MunicipalCouncil constituted under the GoaMunicipalities Act, 1968 (Act No. 7 of 1969) or aPanchayat constituted under the Goa PanchayatRaj Act, 1994 (Act No. 14 of 1994) or a MunicipalCorporation constituted under any law andincludes the Goa Industrial DevelopmentCorporation constituted under the GoaIndustries Development Act, 1965 (22 of 1965);

(i) “notification” means a notificationpublished in the Official Gazette;

(j) “prescribed” means prescribed by the rulesmade under the Act;

(k) “residential building” means any buildingor structure consisting either of a single selfcontained unit having built up area of morethan 100 square meters or more than oneindependent unit used for domestic purpose butdoes not include building constructed foreducational institution, orphanage, old agehome, home for spastic/retarded children or byany other non-profitable organization and suchother organizations as may be notified by theGovernment in public interest;

(l) “Schedule” means the Schedule appendedto this Act.

3. Tax on Infrastructure.— (1) On anyconstruction to be undertaken by any person onany land specified in the Schedule hereto, thereshall be levied and paid a tax on infrastructure atthe rates specified in the said Schedule.

(2) The Government may by notification in theOfficial Gazette, amend any entry in the Scheduleand the Schedule shall be deemed to have beenamended accordingly.

(3) Every notification made under sub-section(2) shall be laid as soon as may be after it is madeon the table of Legislative Assembly while it is in

session for a total period of thirty days which maybe comprised in one session or in two successivesessions, and if, before the expiry of the session inwhich it is so laid or the session immediatelyfollowing, the Legislative Assembly agrees inmaking any modification in the notification or theLegislative Assembly agrees that the notificationshould not be made and notify such decision inthe Official Gazette, the notification shall from thedate of publication of such decision have effectonly in such modified form or be of no effect, as thecase may be, so however that any such modificationor annulment shall be without prejudice to thevalidity of anything previously done or omitted tobe done under that notification.

(4) Where a licence for construction has alreadybeen issued to any person before thecommencement of this Act, the infrastructure taxshall be levied and paid at the time of the renewalof the construction licence or before the issuanceof the occupancy certificate/completion certificate,whichever is earlier, after carrying out assessmentof tax through the Competent Authority under thisAct.

(5) The tax on infrastructure payable under sub--section (1), shall be assessed and collected by theCompetent Authority at the time of approving theconstruction plan or at the time of issuingconstruction licence.

Explanation:— While assessing the said taxunder this Act,—

(a) where a building proposed to beconstructed is in a land earmarked forcommercial use/zone, the rate of tax applicablethereto shall be as applicable to commercialbuildings irrespective of its use;

(b) where a building proposed to beconstructed is in a land earmarked for other useor in zone other than commercial zone, in anyplan in force, such as residential or settlementzone, where commercial utilization of buildingis done partly on the ground floor or any otherfloor, the rate of tax applicable to commercialbuildings shall be changed only to the floorarea which is used for commercial purpose whilefor other area of the building which is used forresidential purpose, the rate applicable toresidential building shall be charged whileassessing infrastructure tax.

(6) The tax collected by the CompetentAuthority shall be credited into the GovernmentTreasury.

OFFICIAL GAZETTE — GOVT. OF GOA

SERIES I No. 6 9TH MAY, 2013

181

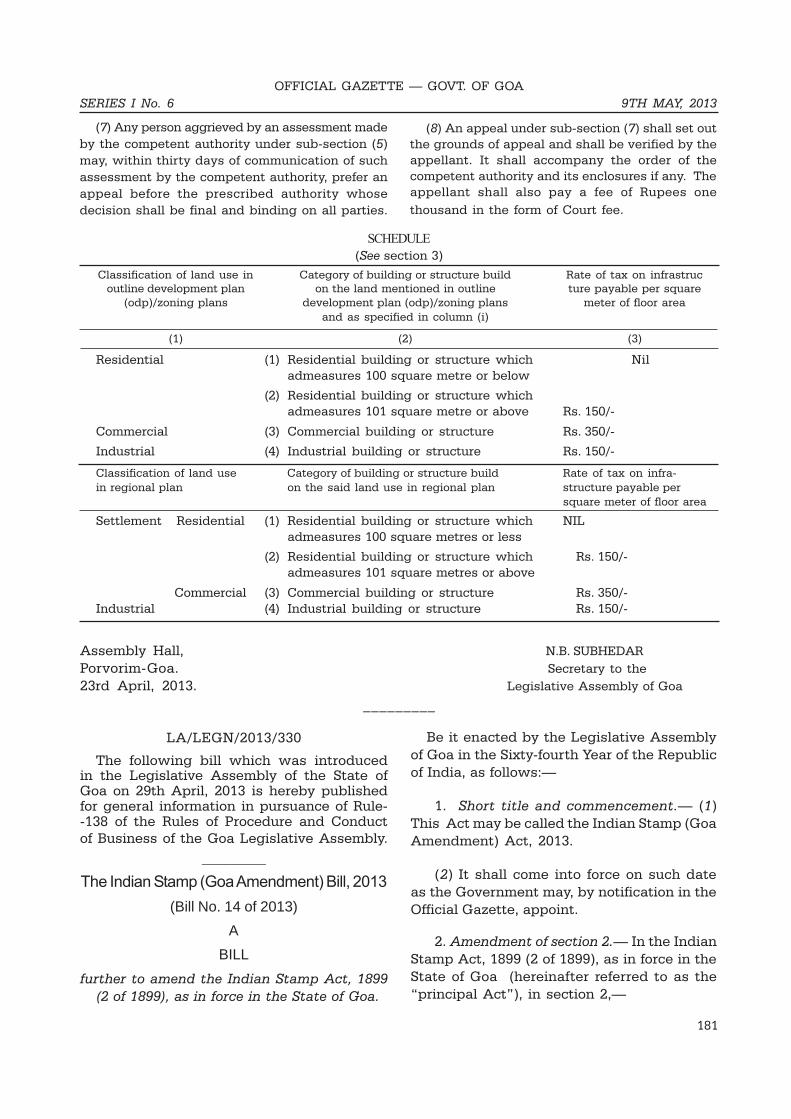

(7) Any person aggrieved by an assessment madeby the competent authority under sub-section (5)may, within thirty days of communication of suchassessment by the competent authority, prefer anappeal before the prescribed authority whosedecision shall be final and binding on all parties.

(8) An appeal under sub-section (7) shall set outthe grounds of appeal and shall be verified by theappellant. It shall accompany the order of thecompetent authority and its enclosures if any. Theappellant shall also pay a fee of Rupees one

thousand in the form of Court fee.

SCHEDULE(See section 3)

Classification of land use in Category of building or structure build Rate of tax on infrastrucoutline development plan on the land mentioned in outline ture payable per square

(odp)/zoning plans development plan (odp)/zoning plans meter of floor areaand as specified in column (i)

(1) (2) (3)

Residential (1) Residential building or structure which Niladmeasures 100 square metre or below

(2) Residential building or structure whichadmeasures 101 square metre or above Rs. 150/-

Commercial (3) Commercial building or structure Rs. 350/-

Industrial (4) Industrial building or structure Rs. 150/-

Classification of land use Category of building or structure build Rate of tax on infra-in regional plan on the said land use in regional plan structure payable per

square meter of floor area

Settlement Residential (1) Residential building or structure which NILadmeasures 100 square metres or less

(2) Residential building or structure which Rs. 150/-admeasures 101 square metres or above

Commercial (3) Commercial building or structure Rs. 350/-Industrial (4) Industrial building or structure Rs. 150/-

Assembly Hall, N.B. SUBHEDAR

Porvorim-Goa. Secretary to the

23rd April, 2013. Legislative Assembly of Goa

_________

LA/LEGN/2013/330

The following bill which was introducedin the Legislative Assembly of the State ofGoa on 29th April, 2013 is hereby publishedfor general information in pursuance of Rule--138 of the Rules of Procedure and Conductof Business of the Goa Legislative Assembly.

________The Indian Stamp (Goa Amendment) Bill, 2013

(Bill No. 14 of 2013)

A

BILL

further to amend the Indian Stamp Act, 1899(2 of 1899), as in force in the State of Goa.

Be it enacted by the Legislative Assemblyof Goa in the Sixty-fourth Year of the Republicof India, as follows:—

1. Short title and commencement.— (1)This Act may be called the Indian Stamp (GoaAmendment) Act, 2013.

(2) It shall come into force on such dateas the Government may, by notification in theOfficial Gazette, appoint.

2. Amendment of section 2.— In the IndianStamp Act, 1899 (2 of 1899), as in force in theState of Goa (hereinafter referred to as the“principal Act”), in section 2,—

OFFICIAL GAZETTE — GOVT. OF GOASERIES I No. 6 9TH MAY, 2013

182

(i) clause (1) shall be renumbered asclause (1A) and before clause (1A) sorenumbered, the following clause shall beinserted, namely:—

“(1) “Association” means anyassociation, exchange, organization orbody of individuals, whether incor-porated or not, established for thepurpose of regulating and controllingbusiness of the sale or purchase of, orother transaction relating to, any goodsor marketable securities;”;

(ii) for clause (10), the following clauseshall be substituted, namely:—

“(10) “Conveyance” includes,—

(i) a conveyance on sale;

(ii) every instrument;

(iii) every decree or final order of anyCivil Court;

(iv) every order made by the HighCourt under section 394 of the CompaniesAct, 1956 (Central Act 1 of 1956) inrespect of amalgamation or reconstruc-tion of companies; and every order madeby the Reserve Bank of India undersection 44 A of the Banking RegulationAct, 1949 (Central Act 10 of 1949) inrespect of amalgamation or reconstruc-tion of Banking Companies, by whichproperty, whether movable orimmovable, or any estate or interest inany property is transferred to, or vestedin, any other person, inter vivos, andwhich is not otherwise specificallyprovided for by Schedule I or by ScheduleI-A, as the case may be.

Explanation:— An instrumentwhereby a co-owner of any propertytransfers his interest to another co-ownerof the property and which is not aninstrument of partition, shall, for thepurposes of this clause, be deemed to bean instrument by which property istransferred inter vivos;”;

(v) after clause (16A), the followingclause shall be inserted, namely:—

“(16B) “market value”, in relation toany property which is the subject

matter of an instrument, means theprice which such property would havefetched if sold in open market on thedate of execution of such instrument,or the consideration stated in theinstrument, whichever is higher;”.

3. Amendment of section 3A.— In section3A of the principal Act, in sub-section (1), afterthe first proviso, the following provisos shallbe inserted, namely:—

“Provided further that in case of a mininglease for bauxite, the duty payable undersub-section (1) shall not exceed the amountin rupees arrived at by applying a rate of0.1 times annual extraction of mineralpermitted under the Environmentalclearance issued for such mining leaseunder the relevant law in force, multipliedby the period of the lease:

Provided further that in case of a mininglease for manganese, the duty payableunder sub-section (1) shall not exceed theamount in rupees arrived at by applying arate of hundred times annual extraction ofmineral permitted under the Environmentalclearance issued for such mining leaseunder the relevant law in force, multipliedby the period of the lease:

Provided further that in case of a mininglease for more than one mineral and havingEnvironmental clearance thereof the dutypayable shall be computed by taking intoaccount total stamp duty payable on eachof such minerals:”.

4. Insertion of new section 10A.— Aftersection 10 of the principal Act, the followingnew section shall be inserted, namely:—

“10A. Stock exchange etc., to deductstamp duty from trading member’saccount.— Notwithstanding anythingcontained in this Act, in case of transactionsthrough stock exchange or an associationas defined in clause (a) of section 2 of theForward Contracts (Regulation) Act, 1952(Central Act 74 of 1952), the stock exchange

OFFICIAL GAZETTE — GOVT. OF GOA

SERIES I No. 6 9TH MAY, 2013

183

or, as the case may be, an association, shallcollect the due stamp duty by deducting thesame from the trading member’s accountat the time of settlement of suchtransactions. The stamp duty so collectedshall be transferred to the GovernmentTreasury or Sub-Treasury in the mannerspecified by the Chief Controlling RevenueAuthority.

Explanation:— For the purpose of thissection, “stock exchange” means the stockexchange as defined in clause (j) of section2 of the Securities Contracts (Regulation)Act, 1956 (Central Act 42 of 1956).”.

5. Amendment of section 47A.— In section47A of the principal Act,—

(i) for the expression “conveyance,exchange or gift”, wherever it occurs,the expression “conveyance, exchange,gift, certificate of sale, deed of partition,power of attorney, deed of settlement ortransfer of lease by way of assignment”shall be substituted;

(ii) in sub-section (3), after the existing

proviso, the following proviso shall be

inserted, namely:—

“Provided that nothing in this sub-

-section shall apply to any instrument

of certificate of sale, deed of partition,

power of attorney, deed of settlement

or transfer of lease by way of

assignment registered before the date

of commencement of the Indian Stamp

(Goa Amendment) Act, 2013.”.

6. Amendment of Schedule I–A.— In

Schedule I-A of the principal Act,—

(i) against Article 2, in column (2), for thewords “Hundred rupees” and “fif tyrupees”, the words “Two hundred rupees”and “Five hundred rupees” shall berespectively substituted;

(ii) against Article 3, in column (2), for thewords “Fif ty rupees”, the words “Onethousand rupees” shall be substituted;

(iii) against Article 4, in column (2), forthe words “Twenty rupees”, the words“Fifty rupees” shall be substituted;

(iv) for Article 5, the following Article shallbe substituted, namely:—

“5. AGREEMENTOR MEMORANDUMOF AN AGREEMENT—

(a) if relating to thesale of a Bill ofexchange

(b) if relating to thepurchase or sale ofG o v e r n m e n tsecurity or sharein an incorporatedcompany or otherbody corporate

(c) if relating to anagreement for thesale of an immovableproperty

(d) if not otherwiseprovided for....

One hundredrupees.

Twenty paise forevery rupeesten or partthereof of valueof the security orshare.

2.9 percent ofthe market valueof the immova-ble property,subject to aminimum dutyof rupees onehundred androunded up tothe nearesthundred in itsm u l t i p l e sthereof.

One thousandrupees.

Exemptions

Agreement or memorandum of agreement—

(a) for or relating tothe sale of goods ormerchandise exclu-sively not being a NOTEor MEMORANDUMchargeable underArticle 42;

(b) made in the formof tenders to the Central

OFFICIAL GAZETTE — GOVT. OF GOASERIES I No. 6 9TH MAY, 2013

184

”;

The same duty asa Bond (Article15) for suchamount.

One hundredrupees.

”;

The same duty asis leviable on ac o n v e y a n c eunder clause (a)or (b), as thecase may be, ofArticle No. 22,on the totalmarket value ofthe propertiesexchanged.

”;

Government for orrelating to any loan;

AGREEMENT TOLEASE. See LEASE(Article 34).

(v) against Article 7, in column (2), forthe words “Fifty rupees”, the words “Onehundred rupees” shall be substituted;

(vi) against Article 8, in column (2), forthe words “Twenty rupees”, the words“Five hundred rupees” shall besubstituted;

(vii) against Article 9, in column (2), forthe words “Ten rupees”, the words “Onehundred rupees” shall be substituted;

(viii) against Article 17, in column (2),for the words “Fifteen rupees”, the words“One hundred rupees” shall besubstituted;

(ix) against Article 18, in column (2),for the expression “article 23 for aconsideration equal to the amount of thepurchase money”, the expression “Article22, on the market value of the property”shall be substituted;

(x) against Article 19, in column (2), forthe words “Ten rupees” the words “Onehundred rupees”, shall be substituted;

(xi) against Article 20, in column (2), forthe words “Thirty rupees” the words “Onehundred rupees” shall be substituted;

(xii) for Article 21, the following Articleshall be substituted, namely:—

“21. COMPOSITION--DEED,

that is to say anyinstrument executedby a debtor except anagreement, wherebyhe conveys hisproperty for the

benefit of his cre-ditors, or wherebypayment of a compo-sition or dividend ontheir debts is securedto the creditors, orwhereby provision ismade for the conti-nuance of the debtor’sbusiness under thesupervision of inspec-tors or under lettersof licence, for the be-nefit of his creditors.

(xiii) for Article 25, the following Articleshall be substituted, namely:—

“25. CUSTOMS-BOND OR EXCISE-BOND

(a) where the amountdoes not exceedRs. 2,500/-

(b) in any other case

(xiv) for Article 30, the following Articleshall be substituted, namely:—

“30. EXCHANGE OFPROPERTY-Instru-ment of–

EXTRACT – See Copy(Article 23)EXCISE BOND – SeeCustoms Bond orExcise Bond(Article 25).

Two hundredrupees.

OFFICIAL GAZETTE — GOVT. OF GOA

SERIES I No. 6 9TH MAY, 2013

185

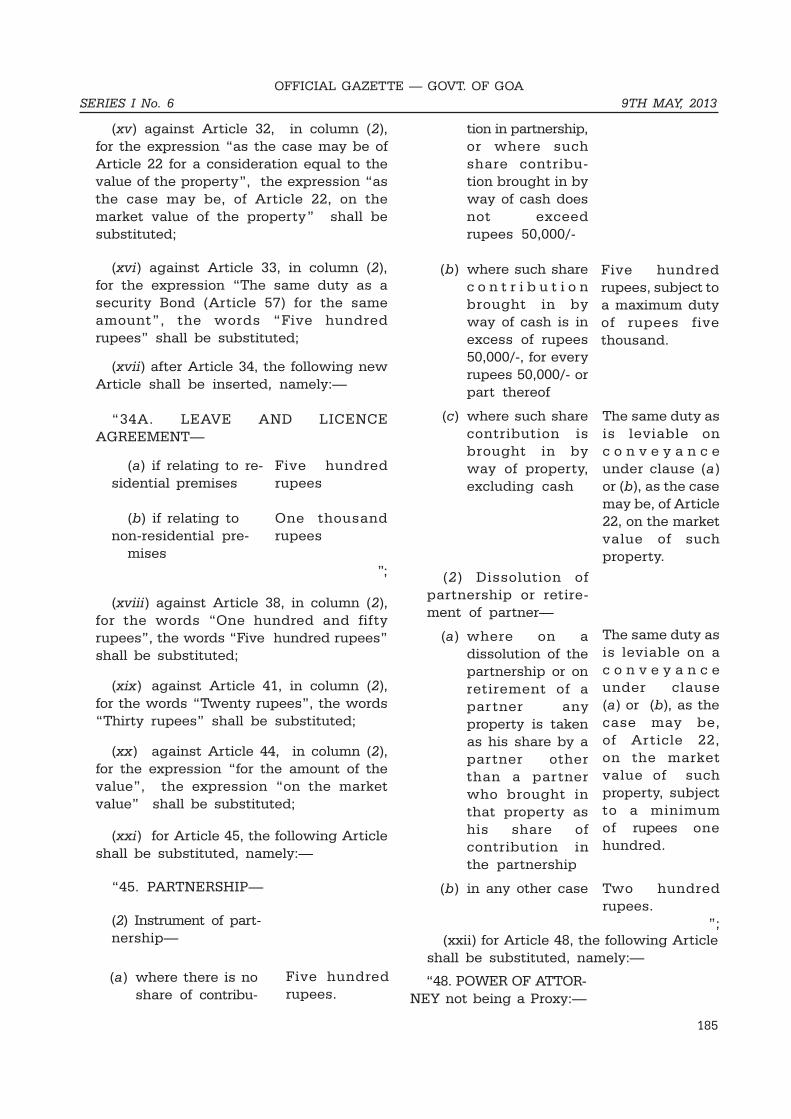

(xv) against Article 32, in column (2),for the expression “as the case may be ofArticle 22 for a consideration equal to thevalue of the property”, the expression “asthe case may be, of Article 22, on themarket value of the property” shall besubstituted;

(xvi) against Article 33, in column (2),for the expression “The same duty as asecurity Bond (Article 57) for the sameamount”, the words “Five hundredrupees” shall be substituted;

(xvii) after Article 34, the following newArticle shall be inserted, namely:—

“34A. LEAVE AND LICENCEAGREEMENT—

(a) if relating to re- Five hundredsidential premises rupees

(b) if relating to One thousandnon-residential pre- rupees

mises ”;

(xviii) against Article 38, in column (2),for the words “One hundred and fiftyrupees”, the words “Five hundred rupees”shall be substituted;

(xix) against Article 41, in column (2),for the words “Twenty rupees”, the words“Thirty rupees” shall be substituted;

(xx) against Article 44, in column (2),for the expression “for the amount of thevalue”, the expression “on the marketvalue” shall be substituted;

(xxi) for Article 45, the following Articleshall be substituted, namely:—

“45. PARTNERSHIP—

(2) Instrument of part-nership—

tion in partnership,or where suchshare contribu-tion brought in byway of cash doesnot exceedrupees 50,000/-

(b) where such sharec o n t r i b u t i o nbrought in byway of cash is inexcess of rupees50,000/-, for everyrupees 50,000/- orpart thereof

(c) where such sharecontribution isbrought in byway of property,excluding cash

(2) Dissolution ofpartnership or retire-ment of partner—

(a) where on adissolution of thepartnership or onretirement of apar tner anyproperty is takenas his share by apartner otherthan a partnerwho brought inthat property ashis share ofcontribution inthe partnership

(b) in any other case

Five hundredrupees.

Five hundredrupees, subject toa maximum dutyof rupees fivethousand.

The same duty asis leviable onc o n v e y a n c eunder clause (a)or (b), as the casemay be, of Article22, on the marketvalue of suchproperty.

The same duty asis leviable on ac o n v e y a n c eunder clause(a) or (b), as thecase may be,of Article 22,on the marketvalue of suchproperty, subjectto a minimumof rupees onehundred.

Two hundredrupees.

”;(xxii) for Article 48, the following Article

shall be substituted, namely:—

(a) where there is noshare of contribu-

“48. POWER OF ATTOR-NEY not being a Proxy:—

OFFICIAL GAZETTE — GOVT. OF GOASERIES I No. 6 9TH MAY, 2013

186

(a) when executed forthe sole purpose ofprocuring the regis-tration of one ormore documents inrelation to a singletransaction or foradmitting executionof one or more suchdocuments

(b) when required insuits or proceedingsunder the PresidencySmall Cause CourtsAct, 1882 (15 of 1882)

(c) when authorisingone person or moreto act in a singletransaction otherthan the case men-tioned in clause (a)

(d) when authorisingone person to act inmore than one transac-tion or generally

(e) when authorisingmore than oneperson to act insingle transaction ormore than one transac-tion jointly or severallyor generally

(f) when authorizing tosell or transfer immo-vable property,—

(i) if given to the father,mother, brother,sister, wife, husband,daughter, son, gran-dson, grand-dau-ghter or such otherclose relative; and

(ii) in any other case.

One hundredrupees.

One hundredrupees.

One hundredrupees.

One hundredrupees.

One hundredrupees.

Five hundredrupees.

The same dutyas is leviable ona conveyanceunder clause (a)

(g) when given to apromoter or developerby whatever namecalled, for constructionon, development of,or sale or transfer (inany manner what-soever) of, any immo-vable property

(h) in any other case

Explanation I.—Forthe purpose of thisArticle more personsthan one whenbelonging to the samefirm shall be deemed tobe one person.

Explanation II.— Theterm ‘registration’includes every operationincidental to registrationunder the RegistrationAct, 1908 (16 of 1908).

Explanation III.—Where under clause (f),duty has been paid onthe power of attorney,and a conveyancerelating to that propertyis executed in pursu-ance of power ofattorney between theexecutant of the powerof attorney and theperson in whose favourit is executed, the dutyon conveyance shall bethe duty calculated onthe market value of theproperty reduced byduty paid on the powerof attorney.

or (b), as thecase may be, ofArticle 22, onthe market valueof the property.

The same duty asis leviable on ac o n v e y a n c eunder clause (a)or (b), as thecase may be, ofArticle 22, on themarket value ofthe property.

One hundredrupees for eachperson authorised.

OFFICIAL GAZETTE — GOVT. OF GOA

SERIES I No. 6 9TH MAY, 2013

187

(xxiii) against Article 50, in column (2),for the words “Four rupees”, the words“One hundred rupees” shall besubstituted;

(xxiv) against Article 51, in column (2),for the words “Five rupees”, the words“One hundred rupees” shall besubstituted;

(xxv) against Article 54, in column (2),for the words “Fifty rupees”, the words“One thousand rupees” shall besubstituted;

(xxvi) after Article 54, the following newArticle shall be inserted, namely:—

“54A. RECORD OFT R A N S A C T I O N(Electronics or other-wise) effected by atrading member througha stock exchange or theassociation referred to insection 10A—

(a) if relating to sale orpurchase of Govern-ment securities

(b) if relating to pur-chase or sale ofsecurities, other thanthose falling underitem (a) above—

(i) in case of delivery

(ii) in case of non--delivery

(c) if relating to futuresand options trading

(d) if relating to forwardcontracts of commo-dities traded throughan association orotherwise

0.005 percent ofthe value ofsecurity.

0.005 percent ofthe value ofsecurity.

0.005 percent ofthe value ofsecurity.

0.005 percent ofthe value ofthe futures andoptions trading.

0.005 percent ofthe value of theforward contract.

Explanation I.— Forthe purpose of clause(b), “securities” meansthe securities as definedin clause (h) of section2 of the SecuritiesContract (Regulation)Act, 1956 (Central Act42 of 1956).

”;

(xxvii) for Article 55, the following Articleshall be substituted, namely:—

“55. RELEASE, that isto say, any instrument(not being an instru-ment as is provided bysection 23A) whereby aperson renounces aclaim upon other personor against any specifiedproperty,—

(a) if the release deed ofan ancestral propertyor part thereof isexecuted by or infavour of brother orsister (children ofrenouncer’s parents)or son or daughter orson of pre-deceasedson or daughter ofpre-deceased son orfather or mother orspouse of therenouncer or thelegal heirs of theabove relations

(b) in any other case

One thousandrupees.

The same duty asis leviable on ac o n v e y a n c eunder clause (a)or (b), as thecase may be, ofArticle 22, onthe market valueof the share,interest, part orclaim renounced.

”;

OFFICIAL GAZETTE — GOVT. OF GOASERIES I No. 6 9TH MAY, 2013

188

(xxviii) for Article 59, the followingArticle shall be substituted, namely:—

“59. SHARE WARRANTSto bearer issued under theCompanies Act, 1956 (1 of1956), for every rupees fivehundred or part thereof

ExemptionShare warrant when

issued by a company inpursuance of the provi-sions of section 114 of theCompanies Act, 1956 (1 of1956), to have effect onlyupon payment as compo-sition for that duty, to theCollector—

(a) one and a half percentum of the wholesubscribed capital ofthe company, or

(b) if any companywhich has paid thesaid duty or compo-sition in full subse-quently issues inaddition to itssubscribed capital,one and a half percentum of theadditional capital soissued.

SCRIP, See Certificate(Article 19).

”;

(xxix) against Article 60, in column (2),for the words “One rupee”, the words“One hundred rupees” shall besubstituted;

(xxx) for Article 61, the following Articleshall be substituted, namely:—

“61. SURRENDER OFLEASE including anagreement for surrender oflease—

(a) without any consi-deration

(b) with consideration

Explanation.— For thepurposes of this Article,return of money paid asadvance or securitydeposit by lessee to thelessor shall not betreated as considerationfor the surrender.

One thousandrupees.

The same dutyas is leviable ona conveyanceunder clause (a)or (b), as thecase may be, ofAr ticle 22, onthe amount ofconsideration.

”;

The same dutyas is leviable ona conveyanceunder clause (a)or (b), as thecase may be,of Article 22,on the marketvalue of theproperty, whichis the subjectmatter of transfer.

”;

Five rupees.

(xxxi) for Article 63, the following Articleshall be substituted, namely:—

“63. TRANSFER OFLEASE by way ofassignment and not byway of underlease or byway of decree or final orderpassed by any Civil Courtor any Revenue Officer

(xxxii) for Article 64, the following Articleshall be substituted, namely:—

“64. TRUST—A. Declara-tion of - of, or concerning,any property when madeby any writing not beinga Will,—

(a) where there is dis-position of property,—

OFFICIAL GAZETTE — GOVT. OF GOA

SERIES I No. 6 9TH MAY, 2013

189

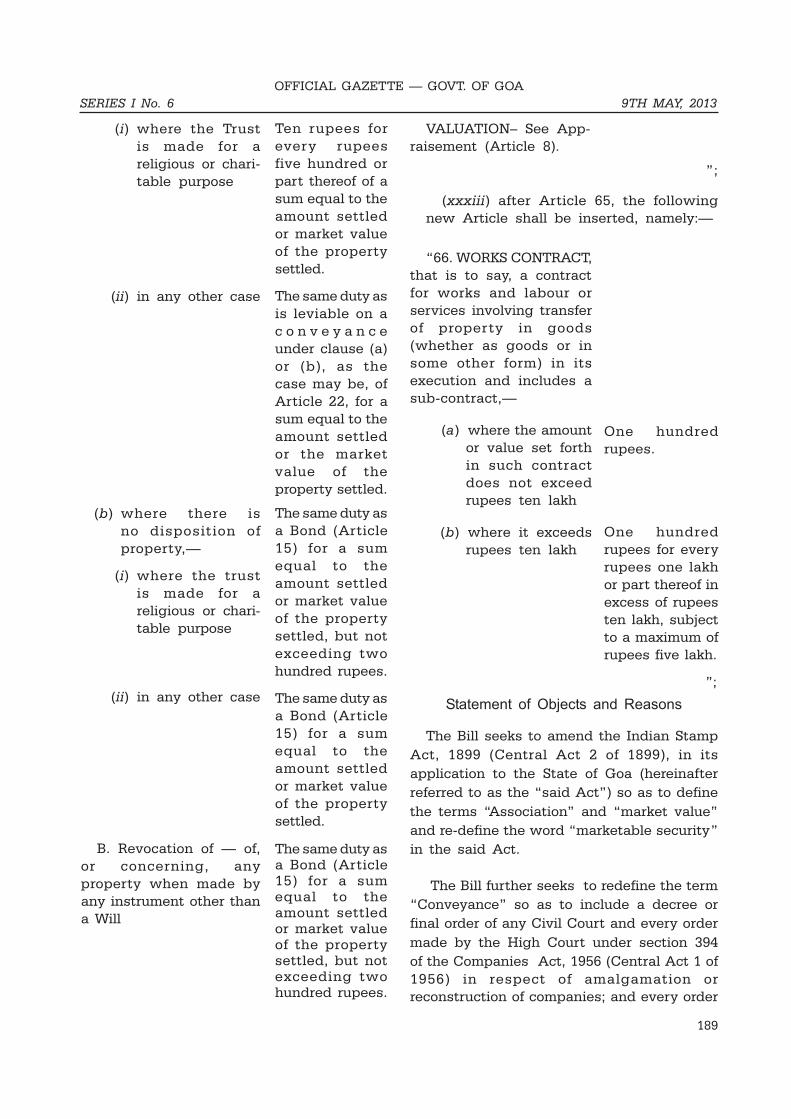

(i) where the Trustis made for areligious or chari-table purpose

(ii) in any other case

(b) where there isno disposition ofproperty,—

(i) where the trustis made for areligious or chari-table purpose

(ii) in any other case

B. Revocation of — of,or concerning, anyproperty when made byany instrument other thana Will

Ten rupees forevery rupeesfive hundred orpart thereof of asum equal to theamount settledor market valueof the propertysettled.

The same duty asis leviable on ac o n v e y a n c eunder clause (a)or (b), as thecase may be, ofArticle 22, for asum equal to theamount settledor the marketvalue of theproperty settled.

The same duty asa Bond (Article15) for a sumequal to theamount settledor market valueof the propertysettled, but notexceeding twohundred rupees.

The same duty asa Bond (Article15) for a sumequal to theamount settledor market valueof the propertysettled.

The same duty asa Bond (Article15) for a sumequal to theamount settledor market valueof the propertysettled, but notexceeding twohundred rupees.

VALUATION– See App-raisement (Article 8).

”;

(xxxiii) after Article 65, the followingnew Article shall be inserted, namely:—

“66. WORKS CONTRACT,that is to say, a contractfor works and labour orservices involving transferof property in goods(whether as goods or insome other form) in itsexecution and includes asub-contract,—

(a) where the amountor value set forthin such contractdoes not exceedrupees ten lakh

(b) where it exceedsrupees ten lakh

One hundredrupees.

One hundredrupees for everyrupees one lakhor part thereof inexcess of rupeesten lakh, subjectto a maximum ofrupees five lakh.

”;

Statement of Objects and Reasons

The Bill seeks to amend the Indian Stamp

Act, 1899 (Central Act 2 of 1899), in its

application to the State of Goa (hereinafter

referred to as the “said Act”) so as to define

the terms “Association” and “market value”

and re-define the word “marketable security”

in the said Act.

The Bill further seeks to redefine the term

“Conveyance” so as to include a decree or

final order of any Civil Court and every order

made by the High Court under section 394

of the Companies Act, 1956 (Central Act 1 of1956) in respect of amalgamation orreconstruction of companies; and every order

OFFICIAL GAZETTE — GOVT. OF GOASERIES I No. 6 9TH MAY, 2013

190

made by the Reserve Bank of India undersection 44 A of the Banking Regulation Act,1949 (Central Act 10 of 1949) in respect ofamalgamation or reconstruction of BankingCompanies, which has the effect oftransferring property.

The Bill further seeks to amend section 3Aof the said Act so as to fix separate stampduty for mining lease for Manganese, Bauxiteand mining lease for more than one minerals.

The Bill further seeks to insert section 10Ain said Act so as to enable the stockexchange or association to collect the stampduty by deducting the same from tradingmembers account and transfer the same tothe Government Treasury or Sub-Treasury.

The Bill further seeks to amend section 47Aof the said Act so as to make provision fordealing with instruments of conveyance, etc.which are undervalued.

The Bill also seeks to amend certainArticles of Schedule I-A since the stamp dutythereof is found to be very low and also toinsert some new Articles thereof.

The Bill seeks to achieve the above objects.

Financial Memorandum

No financial implications are involved inthis Bill, however, it would generateadditional revenue.

Memorandum Regarding DelegatedLegislation

Clause 1(2) of the Bill empowers theGovernment to issue notification forappointing the date to bring into force theAct.

This delegation is of normal character.

Porvorim, Goa. Adv. FRANCIS D’SOUZA

24th April, 2013. Minister for Revenue

Assembly Hall, N. B. SUBHEDAR

Porvorim, Goa. Secretary to the Legislative

24th April, 2013. Assembly of Goa.

Governor’s Recommendation under Article207 of the Constitution of India

In pursuance of Article 207 of the

Constitution of India, I, Bharat Vir Wanchoo,

Governor of Goa, hereby recommend the

introduction and consideration of the Indian

Stamp (Goa Amendment) Bill, 2013, by the

Legislative Assembly of Goa.________

ANNEXURE................................................................................................................................................

Extract of sections 2(1), 2(10), 2(16A), 10, 33 and47A of, and Articles 2, 3, 4, 5, 7, 8, 9, 17, 18, 19,20, 21, 25, 30, 32, 33, 34, 38, 41, 44, 45, 48, 50, 51,54, 55, 59, 60, 61, 63, 64 and 65 of the ScheduleI-A appended to, the Indian Stamp Act, 1899

(2 of 1899), as in force in the State of Goa........................................................................................................

Section 2(1)

2(1) “Banker” includes a bank and any personacting as a banker;

Section 2(10)

2(10) “Conveyance” includes a conveyance onsale and every instrument by which property,whether moveable or immovable, is transferred intervivos and which is not otherwise specificallyprovided for by Schedule I or by Schedule I-A, as thecase may be;

Section 2 (16 A)

(16A) “Marketable security” means a security ofsuch a description as to be capable of being sold inany stock market in India or in the United Kingdom;

Section 10

10. Duties how to be paid.— (1) Except asotherwise expressly provided in this Act, all dutieswith which any instruments are chargeable shallbe paid, and such payment shall be indicated onsuch instruments, by means of stamps—

(a) according to the provisions hereincontained; or

(b) when no such provision is applicablethereto—as the State Government may by ruledirect.

(2) The rules made under sub-section (1) may,among other matters, regulate,—

(a) in the case of each kind of instrument—thedescription of stamps which may be used;

OFFICIAL GAZETTE — GOVT. OF GOA

SERIES I No. 6 9TH MAY, 2013

191

(b) in the case of instruments stamped withimpressed stamps— the number of stamps whichmay be used;

(c) in the case of bills of exchange or promissorynotes the size of the paper on which they arewritten.

[“(2A) The Chief Controlling RevenueAuthority, may subject to such conditions ashe made deem fit to impose, authorise use offranking machine or any other machinespecified under sub-clause (d) of clause (13) ofsection 2, for making impressions oninstruments chargeable with duties toindicate payment on such instruments.

(2B)(a) Where the Chief Controlling RevenueAuthority is satisfied that having regard tothe extent of instruments executed and theduty chargeable thereon, it is necessary inpublic interest to authorise any person, bodyor organisation to such use of frankingmachine or any other machine, he may, by orderin writing, authorise such person, body ororganisation.

(b) Every such authorisation shall be subjectto such conditions, if any, as the ChiefControlling Revenue Authority may, by anygeneral or special order, specify in this behalf.

(2C) The procedure to regulate the use offranking machine or any other machine as soauthorised shall be such as the ChiefControlling Revenue Authority may, by order,determine.

(3) Notwithstanding anything contained insub-section (1), where the Government, in relationto any area in the State, is satisfied that on accountof temporary shortage of stamps in any area in theState, duly chargeable cannot be paid and paymentof duty cannot be indicated on instruments by meansof stamps, the Government, may, by notification inthe Official Gazette, direct that, in such area and forsuch period as may be specified in such notificationthe duty may be paid in cash or by demand draft orby pay order in any Government treasury ofGovernment sub-treasury or any other place as theGovernment may, by notification in the OfficialGazette, appoint in this behalf and the receipt orchallan therefore shall be given by the Officer incharge thereof. Such receipt or challan shall bepresented to the Chief Controlling RevenueAuthority who shall, after due verification that theduty has been paid in cash or by demand draft or by

pay order, make an endorsement to that effect onthe instruments to the following effect, aftercancelling such receipt or challan so that it cannotbe used again, namely:—

“Stamp duty of Rs............... paid in cash or bydemand draft or by pay order vide Receipt/ChallanNo. ........... dated the ....................

Signature of the Chief Controlling Revenue Authority

Provided that the period to be specified in thenotification shall not exceed a period of threemonths.

Explanation:— For the purpose of this sub--section, the expression “demand draft” and “payorder” mean the demand draft or pay order issuedby the State Bank of India constituted under theState Bank of India Act, 1955, or, a correspondingnew bank constituted under section 3 of the BankingCompanies (Acquisition and Transfer ofUndertakings) Act, 1970, or, under section 3 of theBanking Companies (Acquisition and Transfer ofUndertaking) Act, 1980, or, any, other bank being aScheduled Bank as defined in clause (e) of section2 of the Reserve Bank of India Act, 1934.

(4) An impression made under sub-section (2A),(2B) and (2C), or, as the case may be, an endorsementmade under sub-section (3), or any instrument shallhave the same effect as if duty of an amount equal tothe amount indicated in the impression or, as thecase may be, stated in the endorsement has beenpaid in respect of, such payment has been indicatedon such instrument by means of stamps, under sub--section (1).”.]

Section 33

33. Examination and impounding ofinstruments.— (1) Every person having by law orconsent of parties authority to receive evidence, andevery person in charge of a pubic office, except anofficer of police, before whom any instrument,chargeable, in his opinion, with duty, is produced orcomes in the performance of his functions, shall, if itappears to him that such instrument is not dulystamped, impound the same.

(2) For that purpose every such person shall

examine every instrument so chargeable and soproduced or coming before him in order to ascertain

OFFICIAL GAZETTE — GOVT. OF GOASERIES I No. 6 9TH MAY, 2013

192

whether it is stamped with a stamp of the value anddescription required by the law in force in whensuch instrument was executed or first executed:

Provided that––

(a) nothing herein contained shall be deemedto require any Magistrate or Judge of a criminalCourt to examine or impound, if he does not thinkfit so to do, any instrument coming before him inthe course of any proceeding other than aproceeding under Chapter XII or Chapter XXXVIof the Code of Criminal Procedure, 1898;

(b) in the case of a Judge of a High Court, theduty of examining and impounding anyinstrument under this section may be delegatedto such officer as the Court appoints in this behalf.

(3) For the purposes of this section, in cases ofdoubt,—

(a) the State Government may determine whatoffices shall be deemed to be public offices; and

(b) the State Government may determine whoshall be deemed to be persons in charge of publicoffices.

Section 47A

Articles 2, 3, 4, 5, 7, 8, 9, 17, 18, 19, 20, 21, 25,30, 32, 33, 34, 38, 41, 44, 45, 48, 50, 51, 54, 55,59, 60, 61, 63, 64 and 65 of the Schedule I-A

2. Administration Bond,including a bond given underthe Indian Succession Act,1925,or section 6 of the GovernmentSavings Banks Act, 1873—

(a) Where the amount doesnot exceed Rs. 2,000

(b) in any other case

3. Adoption Deed that is tosay, any instrument (other thana Will) recording an adoptionor conferring or purporting toconfer an authority to adopt

4. Affidavit, including anaffirmation or declaration in thecase of persons by law allowedto affirm or declare instead ofswearing

Exemptions

Affidavit or declaration inwriting when made-

(a) as a condition of enrol-ment in the Armed Forcesof the Union;

(b) for the immediate pur-pose of being filed orused in any Court orbefore the officer of anyCourt; or

(c) for the sole purpose ofenabling any person toreceive any pension orcharitable allowance.

5. AGREEMENT OR MEMO-RANDUM OF AN AGREEMENT-

(a) if relating to the sale ofa bill of exchange

(b) if relating to the sale orGovernment security orshare in an incorporatedcompany or other bodycorporate. Fifteen rupeessubject to maximum of fifteenrupees twenty paise for everyrupees 10.00 or part thereofof the value of the Security orshare

“(bb) if relating to anagreement for the sale of anImmovable property. Rupees100/- for property valued uptoRs. 1 lakh or part thereof andfor property valued inexcess of Rs. 1 lakh upto Rs.5lakhs, Rs. 500/- per lakh orpart thereof and for propertyvalued in excess of Rs. 5lakhs, Rs. 1,000/- per lakh orpart thereof.

(c) if not otherwiseprovided for

ExemptionsAgreement or memorandum

of agreement—

(a) for or relating to the saleof goods or merchandiseexclusively not being aNOTE or MEMORAN-DUM chargeable underNo. 42;

Hundred rupees

Fifty rupees.

Fifty rupees.

Twenty rupees.

Fifteen rupees.

Subject to maxi-mum of fifteenrupees twentypaise for everyrupees 10.00 orpart thereof ofthe value of theSecurity or share.

Rupees 100/- forproperty valuedupto Rs. 1 lakhor part thereofand for propertyvalued in excessof Rs. 1 lakh uptoRs. 5 lakhs, Rs.500/- per lakhor part thereofand for propertyvalued in excessof Rs. 5 lakhs,Rs. 1,000/- perlakh or partthereof.

Ten rupees.

OFFICIAL GAZETTE — GOVT. OF GOA

SERIES I No. 6 9TH MAY, 2013

193

(b) made in the form oftenders to the CentralGovernment for orrelating to any loan;

AGREEMENT TO LEASE.See LEASE (No. 34)

7. APPOINTMENT IN EX-ECUTION OF A POWER,whether of trustees or ofproperty, movable or immo-vable, where made by anywriting not being a Will

8. APPRAISEMENT OF VA-LUATION, made otherwisethan under an order of the Courtin the course of suit—

(a) where the amount or valuesecured does not exceedRs. 10/-

where it exceeds Rs. 10/-and does not exceed Rs. 50/-

where it exceeds Rs. 50/-and does not exceed Rs. 100/-

where it exceeds Rs. 100/-and does not exceed Rs. 200/-

where it exceeds Rs. 200/-and does not exceed Rs. 300/-

where it exceeds Rs. 300/-and does not exceed Rs. 400/-

where it exceeds Rs. 400/-and does not exceed Rs. 500/-

where it exceeds Rs. 500/-and does not exceed Rs. 600/-

where it exceeds Rs. 600/-and does not exceed Rs. 700/-

where it exceeds Rs. 700/-and does not exceed Rs. 800/-

where it exceeds Rs. 800/-and does not exceed Rs. 900/-

where it exceeds Rs. 900/-and does not exceed Rs.1000/-

(a) In any other case

Exemptions(a) Appraisement or valua-

tion made for the informa-tion of one party only

and not being on anymanner obligatory bet-ween parties either byagreement or operationof law.

(b) Appraisement of cropsfor the purpose ofascertaining the amountto be given to a landlordas rent.

9. APPRENTICESHIP DEED,including every writingrelating to the service or tuitionof any apprentice, clerk orservant placed with anymaster to learn any pro-fession, trade or employment,not being ARTICLES OFCLERKSHIP (No. 11)

Exemptions

Instrument of appren-ticeship executed by aMagistrate under theApprentices Act, 1961 or bywhich a person is apprenticedby, or at the charge of anypubic charity

17. CANCELLATION— instru-ment of (including anyinstrument by which anyinstrument previously execu-ted is cancelled), if attested andnot otherwise provided for.See also Release (No. 55),Revocation of Settlement(No. 58 B), Surrender of Lease(No. 61), Revocation of Trust(No. 64 B).

18. CERTIFICATE OF SALE(in respect of each property putup as a separate lot and sold)granted to the purchaser of anyproperty sold by public auctionby a Civil or Revenue Court, orCollector or other RevenueOfficer or by an Officer ofCustoms—

(a) where the purchasemoney does not exceedRs. 10/-

(b) where the purchasemoney exceeds Rs.10/- butdoes not exceed Rs. 25/-

Fifty rupees.

One rupee

One rupee

Two rupees

Three rupees

Five rupees

Six rupees

Seven rupees

Eight rupees

Nine rupees

Ten rupees

Eleven rupees

Twelve rupees

Twenty rupees

Ten rupees

Fifteen rupees

One rupee.

One rupee fiftypaise.

OFFICIAL GAZETTE — GOVT. OF GOASERIES I No. 6 9TH MAY, 2013

194

(c) in any other case

19. CERTIFICATE OR OTHERDOCUMENT, evidencing theright or title of the holderthereof, or any other person,either to any shares, script orstock in or any incorporatedcompany or other bodycorporate, or to becomeproprietor of charges, script orstock in or of any such companyor body

20. CHARTER-PARTY, that isto say, any instrument (exceptan agreement for the hire of atug steamer), where by a vesselor some specified principal partthereof is left for the specifiedpurposes of charter, whether itincludes a penalty clauses ornot

21. COMPOSITION-DEED,that is to say, any instrument(except an agreement wherebyhe convey his property for thebenefit of his creditors, orwhereby payment of acomposition or dividend ontheir debts is secured to thecreditors or whereby provisionis made for the continuance ofthe debtor’s business under thesupervision of inspectors orunder letters of licence, for thebenefit of his creditors—

25. CUSTOMS-BOND OREXCISE BOND—

(a) where the amountdoes not exceed Rs. 1,000/-

(b) in any other case

The same duty asis leviable underclause (a) or (b),as the case maybe, of article 23for a considera-tion equal to theamount of thepurchase money.

Ten rupees.

Thirty rupees.

Twenty-fiverupees.

The same dutyas a Bond(No. 15) for suchamount.

Fifteen rupees.

30. EXCHANGE OFPROPERTY— Instrument of—

EXTRACT— See Copy(No. 23)

EXCISE BOND— SeeCustoms Bond or Excise Bond(No. 25)

33. INDEMNITY—BOND.

INSPECTORSHIP DEED—See Composition Deed (No. 21).

INSURANCE— See Policy ofInsurance (No. 47)

34. LEASE, Including anunder-lease or sub-lease andany agreement to let or sublet.

(a) Where by such lease therent is fixed and nopremium is paid ordelivered—

(i) where the leasepurports to be for aterm of less than oneyear

(ii) where the leasepurports to be for aterm of not less thanone year, but notmore than five years

(iii) where the leasepurports to be for aterm exceeding fiveyears and notexceeding ten years

(The same duty asis leviable on aconveyance underclause (a) or (b), asthe case may be, ofarticle No. 22 for aconsideration equalto the value of theproperty of grea-test value as setforth in suchinstrument).

The same duty asa Security Bond(No. 57) for thesame amount.

Same amount.

Half of the dutypayable on a Bond(No. 15) for thewhole amount pay-able or deliverableunder such lease.

Half of the dutypayable on a Bond(No. 15) for theamount or value ofthe average annualrent reserved.

One third of theduty payable on aConveyance (No.22) (a) as levied bythis Act, for a consi-deration equal tothe amount orvalue of theaverage annualrent reserved.

OFFICIAL GAZETTE — GOVT. OF GOA

SERIES I No. 6 9TH MAY, 2013

195

(iv) where the leasepurports to be for aterm exceeding tenyears and notexceeding twentyyears

(v) where the leasepurports to be for aterm exceeding 20years, but notexceeding 30 years;

(vi) where the leasepurports to be for aterm exceeding 30years, but notexceeding 100 years

(vii) where the leasepurports to be for aterm exceeding 100years or in perpetuity

One third of theduty payable on aconveyance (No.22)(a) as levied bythis Act, for ac o n s i d e r a t i o nequal to twice theamount or valueof the averageannual rentreserved.

One third of theduty payable on aconveyance (No.22) (a) as levied bythis Act, for ac o n s i d e r a t i o nequal to threetimes the amountor value of theaverage annualrent reserved.

One third of theduty payable on aConveyance (No.22)(a) as levied bythis Act, for ac o n s i d e r a t i o nequal to fourtimes the amountor value of theaverage annualrent reserved.

One third of theduty payable on aconveyance (No.22) (a) as levied bythis Act, for ac o n s i d e r a t i o nequal in the caseof a lease grantedsolely for agricul-tural purposes to1/10th and in anyother case to1/6th of the wholeamount of rentwhich would bepaid or deliveredin respect of thefirst fifty years oflease.

(viii) where the leasepurport to be for anydefine term

(b) where lease is grantedfor a fine or premium orfor money advanced andwhere no rent isreserved

(c) where lease is grantedfor a fine or premium orfor money advanced inaddition to rent isreserved

Exemptions

Lease executed in the caseof a cultivator and for thepurposes of cultivation (inclu-

On third of theduty payable on aConveyance (No.22) (a) as levied bythis Act, for acons idera t ionequal to threetimes the amountor value of theaverage annualrent which wouldbe paid ordelivered for theten years if thelease continuedso long.

One third of theduty payable ona Conveyance(No. 22) (a) aslevied by thisAct, for acons idera t ionequal to theamount or valueof such fine orpremium oradvance as setforth in the lease.

One third of theduty payable on aConveyance (No.22) (a) as levied bythis Act, for acons idera t ionequal to theamount or valueof such fine orpremium oradvance as setforth in the lease,in addition to theduty whichwould have beenpayable on such alease if no fine orpremium oradvance hadbeen paid ordelivered.

OFFICIAL GAZETTE — GOVT. OF GOASERIES I No. 6 9TH MAY, 2013

196

ding a lease of trees for theproduction of food or drink)without the payment ofdelivery of any fine or premiumwhen a define term isexpressed and such term doesnot exceed one year, or whenthe average annual rentreserved does not exceed onehundred rupees.

In this exemption a lease forthe purposes of cultivationshall include a lease of land forcultivation together with ahomestead or tank.

Explanation I:— rent paid inadvance shall be deemed to bethe premium or moneyadvanced within the meaningof this article unless it isspecifically provided in thelease that rent paid in advancewill be set off towards the lastinstallment or installments ofrent.

Explanation II:— When alease undertakes to pay andrecurring charges such asGovernment revenue, land-lord’s share of ceases, orowner’s share of municipalrates of taxes, which is by lawrecoverable from the lessor andalso the cost repair andimprovements paid by thelessee; the amount so agreed tobe paid by the lessee shall bedeemed to be part of the rent.

38. MEMORANDUM OF ASSO-CIATION OF A COMPANY—

(a) if accompanied byarticle of associationunder section 26 of theCompanies Act, 1956

(b) if not so accompanied

Exemptions

Memorandum of anyassociation not formed for profitand registered under section25 of the Companies Act, 1956

One hundred andfifty rupees.

The same duty asis leviable onarticle of associa-tion under Article10 according tothe share capitalof the company.

41. NOTARIAL ACT, that isto say, any instrument, endor-sement, note, attestation,certificate of entry not being aProtest (No. 50) made or signedby a Notary Public in theexecution of the duties hisoffice, or by any other personlawfully acting as a NotaryPublic

See also Protest of Bill ornote (No. 50).

44.PARTITION Instrument ofas defined by section 2 (15)

Twenty rupees.

The same duty asa Bond (No. 15) forthe amount of thevalue of theseparated shareor shares of theproperty.

45. PARTNERSHIP—

A. Instrument of—

(a) where the capital of the partnership doesnot exceed Rs. 1,000/-.

Rs.1,000/- Five rupees.

Rs. 5,000/- Fifteen rupees.

Rs.10,000/- Twenty fiverupees.

Rs.15,000/- Fifty rupees.

Rs. 20,000/- Seventy fiverupees.

Rs. 25,000/- Hundred rupees.

(b) in any other case One hundred andfifty rupee.

B. Dissolution of PAWN Fifty rupees.OR PLEDGE, See Agreementrelating to Deposit of TitleDeeds, Pawn or Pledge (No. 6)

48. POWER OF ATTORNEYas defined in section 2

(21) not being a Proxy (No. 52)

(a) when executed for thesole purpose of procu-ring the registration ofone or more documentsin relation to a singletransaction or for admit-ting execution of onemore such document

Twenty rupees.

OFFICIAL GAZETTE — GOVT. OF GOA

SERIES I No. 6 9TH MAY, 2013

197

(b) when required in suits orproceedings under Presi-dency Small ClauseCourts Act, 1982

(c) when authorizing oneperson or more to act in asingle transaction otherthan the case mentionedin clause (a)

(d) when authorizing notmore than five persons toact jointly and severallyis more than onetransaction or generallyto act in a singletransaction other thanthe case mentioned inclause (a)

(e) when authorizing morethan five but not morethan 10 persons to actjointly and severally inmore than one transac-tion or generally

(f) when given for conside-ration and authoring theattorney to sell anyimmovable property

(g) in any other case

N. B.:— The term “registra-tion” includes every operationsincidental to registration underthe Indian Registration Act,1908.

Explanation:— For thepurpose of this article morepersons than one whenbelonging to the same firm shallbe deemed to be one person.

50. PROTEST OF BILL ORNOTE, that is to say, anydeclaration in writing made bya Notary Public or other personlawfully acting as such,attesting the dishonor of a billof exchange or promissory note

51. PROTEST BY THEMASTER OF A SHIP, that is tosay, any declaration of theparticulars of her voyage drawn

Twenty rupees.

Twenty rupees.

Forty rupees.

Fifty rupees.

The same duty asunder clause (a)or (b) as the casemay be of ArticleNo. 22 for theamount of consi-deration.

Twenty rupees.

Four rupees.

Five rupees.

up by him with a view to theadjustment of losses or thecalculation of averages andevery declaration in writingmade by him against thecharters or the consignors fornot loading or unloading theship, when such declaration isattested or certified by a NotaryPublic or other person lawfullyacting as such.

See also Note of Protest bythe Master of the Ship (No. 44).

54. RECONVEYANCE OFMORTGAGED PROPERTY—

(a) if the consideration forwhich the property wasmortgaged does not exceedRs. 1,000/-

(b) In any other case—

55. RELEASE, that is to say,any instrument (not being suchby release as is provided forsection 23A) whereby a personrenounces a claim uponanother person or against anyspecified property—

(a) if the amount or value ofthe claim does notexceed Rs.1,000/-

(b) In any other case

59. SHARE WARRANTS tobearer issued under theCompanies Act, 1956.

Exemptions

Share warrant when issuedby a Company in pursuance ofthe Company’s Act, 1956section 114, to have effect onlyupon payment, as compositionfor that duty, to the Collector ifStamp Revenue of—

The same duty isleviable on ac o n v e y a n c eunder clause (a)of Article 22 forthe amount ofsuch considera-tion as set forthin the reconve-yance.

Fifty rupees.

The same duty asa Bond (No.15) forsuch amount orvalue as set forthin the release.

Fifteen rupees.

OFFICIAL GAZETTE — GOVT. OF GOASERIES I No. 6 9TH MAY, 2013

198

(a) one-and-a-half per centumof the whole subscribedcapital of the company; or

(b) if any company which haspaid the said duty orcomposition in fullsubsequently issued anaddition to its scribedcapital, one and half percentum of the additionalcapital so issued.

SCRIP. See Certificate (No. 19).

60. SHIPPING ORDER for orrelating to the conveyance ofgoods on board of any vessel

61. SURRENDER OF LEASE—

(a) when the duty with whichthe lease is chargeabledoes not exceed tenrupees

(b) In any other case

Exemptions

Surrender of lease when suchlease is exempted from duty.

63. TRANSFER OF LEASE byway of assignment andnot by way of underlease

Transfer of any leaseexempt from duty.

64. TRUST—

(a) Declaration of— of, orconcerning any propertywhen made by anywriting not being a Will

(b) Revocation of— or concer-ning any property whenmade by any instrumentother than a Will

See also settlement (No.58).

VALUATION-See App-raisement (No. 8).