Embed Size (px)

Citation preview

1

Pakistan

Opportunities in

Telecommunications

Pakistan Telecommunications

Authority

September 2007

2

Come aboard!

Pakistan: the fastest growing market in Telecommunications 4 AM, Islamabad: Construction site of the 45 storey Grand Hyatt Hotel. The cell phone glows dimly as the laborer speaks to his wife hundreds of miles away, just before the work starts. 10 AM, Islamabad: The Mercedes of the Chairman glides on to the ramp overseeing the massive excavation of this hotel as the concrete pours. His Blackberry chirps with the e-mail about the paintings being procured for the Grand Ballroom. 11 AM, a small village, a hundred and fifty kilometers from Lahore: the small girl sits fascinated watching the pictures on the PC screen installed in the Telecenter, linked on Broadband via WiMAX to a site halfway across the world. 4 PM, Karachi: The frenetic construction activity outside the broadband Video Conferencing Room nearly drowns out the sound on the presence based conference linking Karachi, Hong Kong, Dubai and the software developers at MIT in Boston. 10 PM, Faisalabad: The cut and sew manager of a leading Textile mill, is uploading images of the new patterns of the curtains to Macy’s as he views the hurricane Dean rip across Jamaica on his converged platform of TV, WiFi , Telephones and Broadband just installed via optical fibre to the Gigabit Ethernet WAN of his company. 12 AM, Peshawar: the giggling young teens upload the pictures on Flickr via their EDGE enabled cell phones and await the responses from their sister in London. 1 AM: Quetta: the sisters never had it better. Speaking to each other across thousands of miles at less than 6 cents per hour on their Cell phones. 2 AM: Jacobabad: Finally the father reaches his son in Germany. At less than 2.5 cents a minute a call to Europe (or US) has never been so affordable. This is just a real life snippet of where Pakistan has come in Telecommunications in a very short time. It has changed the way communications is perceived and used: business, social, entertainment, education, governance, security. Its impact on the economy is considerable and the developments mirror the rapid economic growth of the country in the last few years.

GDP Growt h

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

9.00%

0 1 2 3 4 5 6 7 8

Ye a r s 2 0 0 0 - 2 0 0 8

3

Pakistan and its economy

1

Pakistan is the gateway to the energy rich Central Asian States, the financially liquid Gulf States and the economically advanced Far Eastern tigers. This strategic advantage alone makes Pakistan a marketplace teeming with possibilities. With three major international airports and thirty-eight domestic airports, Pakistan is accessible via fifty international airlines. Pakistan's geographical location, a rapidly expanding transportation and communications infrastructure and an environment conducive to business makes it an attractive destination for investors. With a predominantly young population of 160 million, a large portion speaks several Regional languages and English. The Central Board of Revenue has facilitated structural reform in tax and tariffs and the State Bank of Pakistan has invigorated the banking sector into high returns on investment. Pakistan provides relatively strong protection for foreign investors, it ranks 19

th worldwide on protecting

investors, according to World Bank report Doing Business in South Asia 2007. The capital markets are being modernized, and reforms have resulted in development of infrastructure in the stock exchanges of the country. The Securities and Exchange Commission has improved the regulatory environment of the stock exchanges, corporate bond market and the leasing sector. Current investment policies have been tailor made to suit investor needs. A concerted Policy and planning have been consistent, with liberalization, de-regulation, Privatization, and facilitation being its foremost cornerstones. With a consistent growth in GDP and a supportive

Fiscal and Regulatory infrastructure the growth in investments has been quite rapid in the last few years. The net impact of this has been a major surge in investments and growth of the telecom sector which constituted the major recipient of FDI

2 in the last two years and is set to maintain this

position in the foreseeable future. It is relatively easy to set up a company in Pakistan, be able to freely repatriate foreign exchange (profits, equity) by following easy processes. Foreign companies can own 100% equity with out any need for taking on local shareholders. Security concerns and Investment protection While it is a fact that Pakistan has got some bad press related to security issues, but this has been blown out of

1 Data in Annex

2 Foreign Direct Investment

Stock Exchange Index

0

2000

4000

6000

8000

10000

12000

14000

16000

2000-01 2001-02 2002-03 2003-04 2004-05 2005-06 2006-07

Stock Exchange Index

Investments

0

2000

4000

6000

8000

10000

12000

14000

16000

2000-

01

2001-

02

2002-

03

2003-

04

2004-

05

2005-

06

2006-

07

Millio

n U

S$

FDI (Million $) Foreign Investment (FDI+Public&Private Portfolio)

4

proportion by the media. Ask the companies who do their own clear headed due diligence and are consistently investing in Pakistan. About US$ 2 Billion has been invested yearly in Telecom alone in the last couple of years and this trend is growing as the networks expand the opportunities grow. In all the reported „turmoil‟ one shop front of one the companies was damaged in a country where there are over 60 Million Cell phones, 6 cell phone companies, 16 LDIs, many LL and WLL operators

3 and investors from

Europe, Middle and Far East. The Telecom Roadmap A coherent and forward looking Telecommunications Deregulation policy was created with the help of the World Bank and comprehensive consultations with all stake holders and announced on July 13, 2003. This covered Long Distance and International (LDI), Local Loop (LL, including Wireless Local Loop WLL). The other licenses which are issued are DNOP (Data Network Operator), ISP and other Value Added Licence (see www.pta.gov.pk for details). A transparent process for award of licenses and frequencies was adopted which resulted in two new Cellular companies as well as a number of LDI, WLL and LL licenses being issued. Most companies rolled out in an environment of perfect competition. A few key enablers made sure that not only a smooth roll out be effected but also least bureaucratic or regulatory hurdles got in the way. A light touch Regulatory régime is in effect, which facilitates not only the efficient growth but also protects the citizens their right to best services. This was done by enabling elements like CPP (Calling Party Pay), MNP (Mobile Number Portability), dynamic interconnect, reducing interconnection costs from the SMPs (Significant Market Powers). In order to enable development in un- and underserved areas, a USF (Universal Service Fund – www.usf.org.pk) has been formed which is funded by regulatory fees paid by the Operators as well as injections by the World Bank. This which would support the growth of local loops and rural voice and broadband communications. The Regulatory Environment The PTA (www.pta.gov.pk) has been tasked to set up a fair regulatory regime to promote investment, encourage competition, protect consumer interest and ensure high quality telecom services. It does so by adopting a light touch regulatory approach and in doing so tries to ensure a level playing field for large and small Operators by being even handed and transparent in its determinations, arbitration and push for Quality of Services. The major result of this strategy has been a controversy free, transparent, rapid deregulation of the sector in the last 24 months. Two key principles have guided the process: being supportive to the new entrants and letting the market forces drive the sector. In order to enable this to happen the PTA is structured in a way that enables efficient internal and external operations to take place. The structure to enable a smooth flow to happen is facilitated by various divisions of the PTA.

Law & Regulations

Coordination

Licensing

Enforcement

Industry Development

Finance

Commercial Affairs

Economic Affairs

3 LDI: Long Distance and International; LL: Local Loop; WLL: Wireless Local Loop

5

Regulatory Studies

Frequency Allocation Board

Administration Directorate

The Frequency Allocation Board (FAB) has been integrated into the PTA infrastructure so that the Licencing process is seamless. The PTA not only regulates the sector but also creates an environment which facilitates the induction of new technologies as well as development of direct and indirect industries and markets. The State of Telecommunications today Subsequent to the Policy declaration, the PTA set up a Transparent and open process for license acquisition and frequency auctions. The process was completed in a short time and within 3 months of licenses being issued, the companies started operations. In the last two years, a massive transformation of the Telecom landscape has taken place in Pakistan. In this short span of time the cellular connections have gone from less then 12 Million to over 60 Million. This coupled with the increase in WLL lines has rocketed the Tele-density from 2.2% to over 45% in this period. This is of considerable significance for the development of the market. As the short story line in the beginning of this document indicated (these are real scenarios) the segments being addressed will force the penetration to over 100 Million in a few years. What is significant is the large and diverse user base which will support the launch of Value Added Services, new operations as well as delivery of total solutions in the market – addressing different segments at the same time.

In parallel the growth of Broadband has increased considerably. The bandwidth required by the Cellular and other operators additionally is driving the market. Three new Nationwide optical fibre systems have been deployed having an aggregated capacity of over 4.5 Terabit/s expandable to over 45 Terabit/s (on 10 GigE).

Total Voice Telephony

-

10,000,000

20,000,000

30,000,000

40,000,000

50,000,000

60,000,000

70,000,000

2,004 2,005 2,006 2,007

Years

Users

Telephone lines (including WLL) Mobile phones Total

70%

60%

50%

40%

30%

20%

10%

Telephone Line Penetration

2004 2005 2006 2007

Teledensity

Total Voice Telephony

-

10,000,000

20,000,000

30,000,000

40,000,000

50,000,000

60,000,000

70,000,000

2,004 2,005 2,006 2,007

Years

Users

Telephone lines (including WLL) Mobile phones Total

70%

60%

50%

40%

30%

20%

10%

Telephone Line Penetration

2004 2005 2006 2007

Teledensity

Raiwind

PA

KIS

TA

N

Abbottabad

Peshawar

Taxila

Islamabad

Jhelum

Gujrat Sialkot

Sargodha

KalabaghBannu

Karak

D. I. Khan

Multan

D. G.

KHAN

I

N

D

U

S

GojraT. T. Singh

Lahore

Okara

Sahiwal

Khanewal

Bahawalpur

ThattaKarachi

Nooriabad

Hyderabad

Nawab Shah

Amirabad

Sukkur

Gawadar

Fort Sandeman

Chaman

Khuzdar

Quetta

Mach

Sibbi

D M J

Jacobabad

Fazilpur

Kand Kot

Shikarpur

Dadu

Kalari

Larkana

Gujranwala

Ahmadi

Banda

Mandi

Bhauddin

Rahim Yar Khan

Jhang

Landi

Kotal

Mardan

Faisalabad

Jamshoro

Rojhan

Khewra

Fort Abbas

Khokhropar

ARABIAN SEA

AF

GH

AN

IST

AN

IND

IA

JAMMU & KASHMIR

GILGIT

AGENCY

IRAN

Zahidan

Kandahar

Kabul

Amritsar

RIN

G-01

109 Km

104 Km

118 K

m

125 K

m

Dherki

120

Km

117 Km

84 Km

98

Km

90 K

m

104 Km

90 Km

100 Km

128 Km

80 K

m

67 Km

99 K

m

90

Km

94 K

m

72 K

m

71 K

m

80 Km

58

Km

50 Km

78 K

m

41 Km25 Km

59 Km

100

Km

79 Km

95 Km

41 Km

80 Km

46 Km

50 K

m

33 Km

76 K

m

64 K

m

70 Km

23 Km

46 Km

110 Km

65 Km

106 Km

65 K

m

55 Km

79 Km

Arifwala

Vehari

MailsiLodhran

Burewala

60 Km

52 K

m

42 Km

44 Km

35 Km

60

Km

25 Km

Kohat

Noshera

Kharian

Gujar Khan

58 Km

33 Km

Chicha Watni46 K

m

25 K

m

Qureshi

Chowk

Muzaffar

Garh

Mianwali

Bhakkar

Khushab

45 Km

140 K

m

35

Km

Kot Addu

Layyah

Liaquatpur

Chiniot

33 Km

36 Km

36 Km

20 Km

95 Km

40 Km

75 K

m

60 K

m

45 K

m

112

Km

92 Km

Pattoki Ferozpur

25 Km

RIN

G-05

RING-02

RING-03

RIN

G-04

Pakpattan

Kasur

Domestic Optical fibre Backbone Network

6

The actual fibre penetration is much deeper and over 550 locations have fibre access on the PTCL fibre a section of which is shown the diagram. The services now on offer include dark fibre, MPLS

4, Gigabit

Ethernet and other Value added services.

These new systems (in addition to the older PTCL system connect over 100 cities. Metro-rings in over 20 cities are being deployed by different operators (Islamabad has the first FTTH- (Fibre To The Home – system) where corporate and cellular back haul requirements are also being met. Companies like Wateen are creating triple play opportunities by deploying lanighaul and metro fibre systems and creating access via WiMAX. Others like Niyatel have deployed Pakistan‟s first FTTH

5 network in Islamabad and are planning

expansions to other cities. These operators are offering services ranging from Triple Play

6 to Dark

Fibres to a whole range of end users. The access pricing has dropped to less than US$ 12/month for a

512 Kb/s connection. A triple play bundle costs less than US$ 40/month. With the possibility of utilizing the 5 M land line network of the PTCL for DSL, new operators are driving the Broadband penetration quite aggressively. HFC

7 Cable operators are now upgrading

their networks in order to offer triple play services after acquiring requisite licenses from the PTA or entering into franchising relationships with existing operators.

4 Multiple Protocol Label Switching

5 FTTH: Fibre To The Home

6 Triple Play: Voice, Video and Data

7 HFC: Hybrid Fibre Coax

Long H

aul/M

PLS B

ackb

one

Metro Ring

Central POP

Legacy Circuit

Switched Network

Internet

CPE

CPE

WiMAX Access

Virtual

Hub

Long H

aul/M

PLS B

ackb

one

Metro Ring

Central POP

Legacy Circuit

Switched Network

Internet

Central POP

Legacy Circuit

Switched Network

Legacy Circuit

Switched Network

InternetInternet

CPE

CPE

WiMAX Access

CPE

CPE

CPE

CPE

WiMAX Access

Virtual

Hub

Virtual

Hub

Virtual

Hub

Virtual

Hub

SMW 4 International optical fibre links

Wateen Telecom

Niyatel

7

Broadband The demand for Internet and Broadband has been no less phenomenal. The growth over a 5 year period has been over 7,700% with over 10.5 Million active users

8

In recent months the Broadband sector on DSL has started expanding with the facilitatory régime in place for reduction in bandwidth prices, fair interconnect with the PTCL landline network and the issuance of licences for WiMAX in the 3.5 GHz band. The numbers of DSL users stands at over 100,000 with a target to hit 1.6 Million by 2009. This will be achieved by support from the Universal Service Fund for expansion of Broadband users, farming new frequencies in the 2.3, 2.5, 3.5 and other bands for WiMAX and other new wireless technologies. As mentioned earlier, the private sector licensees are laying metro fibre for HFC, Fibre access (FTTC, FTTH) in over 20 cities. The PTCL optical fibre reaches into the heartlands at over 550 locations. This will help open the rural markets as the new private sector owners expand and utilize the installed infrastructure. New access media are growing – EDGE, EVDO, WiFi Mesh, WiMAX, Optical Fibre, DSL and HFC are being deployed in different networks to capture this growing segment. In fact Pakistan is leading the international deployment of WiMAX across the country. Three operators (Mobilink, Wateen and Burraq) are deploying nationwide systems on the 802.16d/e standards. All this has resulted in a huge growth of international connected bandwidth as well as rapidly dropping prices. An E1 (2Mb/s) is available at US$1500/month and with competition heating up; it is expected to drop further to sub US$ 1000 levels.

New Undersea (and planned overland transnational Fibre systems) have ensured a degree of redundancy and reliability which was not present earlier.

8http://www.internetworldstats.com/

Total connected International Bandwidth

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

2003 2004 2005 2006 2007

Mb

/s

PTCL TW1 Total

Voice+Data

Multiple paths underseaMultiple paths undersea

8

The Deregulation and Privatisation Liberalisation of the Fixed Line Sector Pakistan inherited parts of Indian Telephone and Telegraph Department at the time of independence in 1947. Since then, it functioned as a government department for providing telecom services in Pakistan. In 1994, the government decided to transform it into public corporation and then in 1996 it was further restructured into public limited company under the title of Pakistan Telecommunication Company Limited (PTCL). The Pakistan Telecommunication Ordinance 1994 provided a 25-year license for incumbent operator, Pakistan Telecommunication Company Ltd (PTCL), to provide domestic and international telephone services. Keeping in view the inefficiencies of the basic telecom sector Government of Pakistan decided to move away from monopolized market structure to more deregulated and liberalized one. Government of Pakistan and Pakistan Telecommunication Authority, along with World Bank Consultants made concerted efforts to facilitate this process. Pakistan Telecommunication Authority (PTA) received applications from 95 companies for the grant of Local Loop (LL) and Long Distance International (LDI) licenses from the prospective investors. Out of these 39 companies opted for LL licenses while 23 opted for the award of LDI licenses. The PTCL was recently privatized and 26% shares with management rights sold to Etisalat at US$ 2.6 Bln. Award of FLL and LDI Licences So far PTA has issued 14 LDI Licenses to various National and Multinational Companies. PTA has also issued 84 Fixed-line Local Loop (FLL) Licenses to various companies for 14 telecom regions of Pakistan.

http://www.pta.gov.pk/index.p

hp?option=com_content&task=view&id=849&Itemid=625 Cellular Networks Five GSM operators

9 and one

(deploying) WCDMA operator are driving the cellular market in market in Pakistan. This is one of the fastest growing markets in the world and has brought about considerable social and economic change in the country. With facilities like CPP, fair interconnect, clear frequency band availability, trained manpower and financial and banking support, this sector has attracted the maximum investments into Pakistan in the last 3 years. Between the operators over 6000 cities, towns and villages are already covered and with the continuing aggressive roll out, it is expected that most of Pakistan (including the rural areas) will have cellular coverage in the next two to three years. The license fee determined by open auction was US$ 291 M for each operator.

9 See Annex

9

Investors Telecommunications has attracted investment from a wide variety of players. These range from Telenor Norway, Warid UAE, Etisalat UAE, Singtel Singapore, Orascom Egypt, QTel Qatar, Diallog Uzbekistan, etc. These are serviced by a range of vendors from Europe, USA, China, Canada, etc. The investment rules and regulations for FDI are very supportive and 100% foreign ownership is permitted as is unhindered repatriation of profits and equity. Key Players Due to the successful market opening and open competition, the Telecom landscape has changed dramatically. Over the last few years a few leaders have emerged and the dominance of the state owned Operator (PTCL) has been diluted. In Mobile networks, Mobilink (Orascom) has over 40% market share and has revenue streams in excess of US$ 1Bln. In the fixed line sector, PTCL still dominates in the wired and wireless (WLL) domain. However, the voice traffic (domestic and international) has migrated considerably to the private sector operators. In a similar manner there is a considerable shift of traffic in the bandwidth arena as well. With a new private sector (TWA1) undersea fibre in place, the PTCL has lost over 35% of the market. It is also expected that the new nationwide and metro fibres will migrate to these from the earlier monopoly. This dynamic has been described to illustrate the highly conducive environment for the new investors who can acquire a large market share with appropriate investments and a high quality offering of services. Mergers and Acquisitions Market consolidation is taking place in the changing competitive environment. Mergers and Acquisitions have been taken place which has created higher levels of competition. While this has created price pressures on the operators, they are striving for higher levels of quality and bringing in new services. This in turn has driven demand further, creating new ARPU opportunities.

Mergers in Telecom Sector

Foreign Companies who purchased shares

Local Companies who sold shares

Share purchased (%)

Amount paid US$ Million

1. Orascom, Egypt Mobilink 11.31% 290

2. Qtel, Qatar Buraq 75% 12.3

3. Singtel, Singapore Warid 30% 758

4. China Mobile, China Paktel 100% 764

5. Oman Tel, Oman World Call 60% 220

In addition to the International acquisitions, local companies have consolidated their positions by buying unused frequency spectrum (for WiMAX) from other operators and ISPs and Data Operators being merged into traditional voice operators (like the acquisition of World On Line by Orascom). Opportunities

10

While considerable licensing has been done for cellular, LL, WLL, LDI, ISP sectors, the government has plans of opening up frequencies for WiMAX in different frequency bands as well as issue new licenses for 3G cellular systems. Consultative processes are happening for setting up large Voice and Data Peering Points, Converged Networks, MVNOs, LMDS networks, etc. There is now a huge opportunity for operators or build on top of the competitive infrastructure which has been installed (and is expanding by the day) to bring in high yield Value Added Services. The next frontier is delivery of wired and wireless broadband services and the target is to hit at least 3 Million users in the next few years (30% of the Internet user base) and innovative solutions will be encouraged. With market consolidation taking place, there are new opportunities for Mergers and Acquisitions as has been evidenced in the last few months. Operators are diluting their equity in order to get institutional investors and others are doing this to acquire the technical expertise to enable more efficient operations. Jump Aboard! All this signals opportunities in the Traditional and Value Added sectors for not only creating new businesses by riding on these systems but also to be a part of new licenses which are being reviewed. These include MVNO

10,

Regional Hosting, Call Centers, Telecenters, Video Conferencing, Content aggregation, Converged networks, etc. On another plane, the Regulatory environment permits spectrum trading, Mergers and Acquisitions as well as entry via Private equity arrangements. The market opening has nearly doubled the sector revenues and this trend is expected to grow. The laws of Pakistan tightly protect foreign investment and in all the years since the market deregulation started: 1989 for cellular and 1993 when the first Payphone, Data and ISP licenses were issued, there has not been one instance which reflects anything contrary to this. New Government initiatives in Public Private Partnerships which depend on ICT infrastructures, not only create demand for these services but also create growth opportunities for new source of Revenue streams. New and growing rural markets are turning established conventional thought on its head and have forced the new operators to open out new and virgin areas. Clearly validating Pralahad‟s vision of “Fortune at the bottom of the Pyramid” Welcome Aboard.

10 MVNO: Mobile Virtual Network Operator

Sector Revenue Growth

-

0.50

1.00

1.50

2.00

2.50

3.00

3.50

2004 2005 2006

US

$ B

illio

n

Fixed Line Mobile Data, etc

11

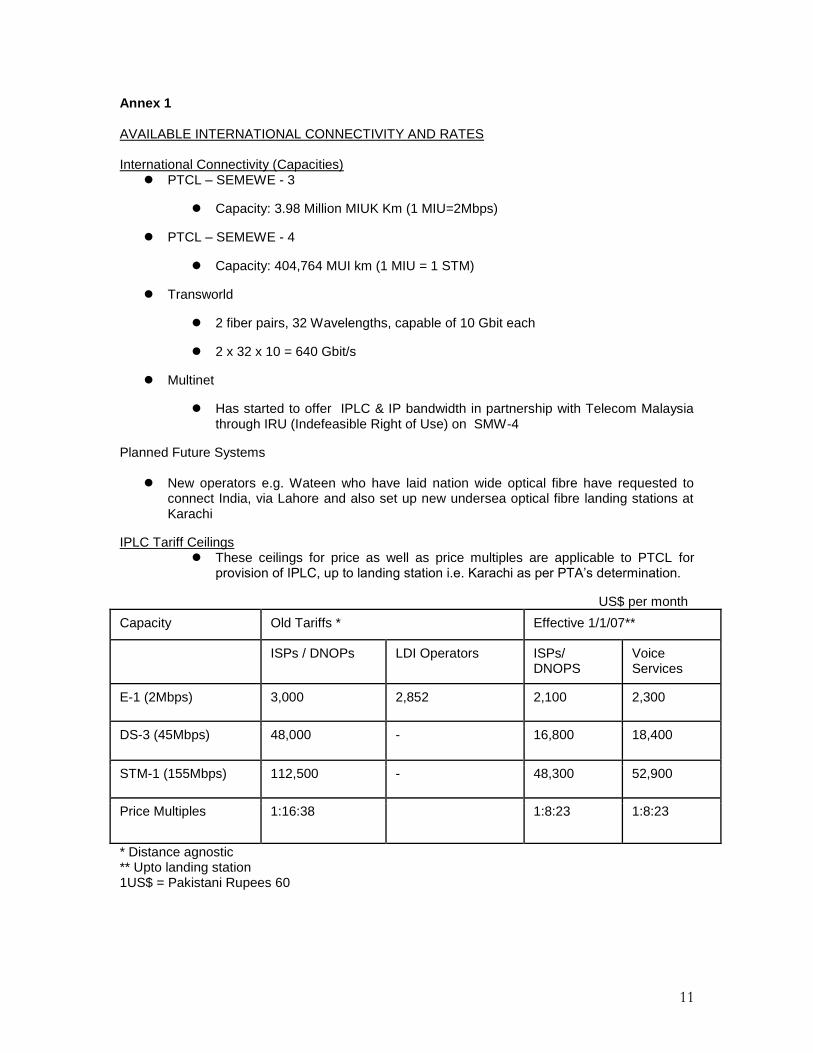

Annex 1 AVAILABLE INTERNATIONAL CONNECTIVITY AND RATES International Connectivity (Capacities)

PTCL – SEMEWE - 3

Capacity: 3.98 Million MIUK Km (1 MIU=2Mbps)

PTCL – SEMEWE - 4

Capacity: 404,764 MUI km (1 MIU = 1 STM)

Transworld

2 fiber pairs, 32 Wavelengths, capable of 10 Gbit each

2 x 32 x 10 = 640 Gbit/s

Multinet

Has started to offer IPLC & IP bandwidth in partnership with Telecom Malaysia through IRU (Indefeasible Right of Use) on SMW-4

Planned Future Systems

New operators e.g. Wateen who have laid nation wide optical fibre have requested to connect India, via Lahore and also set up new undersea optical fibre landing stations at Karachi

IPLC Tariff Ceilings These ceilings for price as well as price multiples are applicable to PTCL for

provision of IPLC, up to landing station i.e. Karachi as per PTA‟s determination.

US$ per month

Capacity Old Tariffs * Effective 1/1/07**

ISPs / DNOPs LDI Operators ISPs/ DNOPS

Voice Services

E-1 (2Mbps) 3,000 2,852 2,100 2,300

DS-3 (45Mbps) 48,000 - 16,800 18,400

STM-1 (155Mbps) 112,500 - 48,300 52,900

Price Multiples 1:16:38 1:8:23 1:8:23

* Distance agnostic ** Upto landing station 1US$ = Pakistani Rupees 60

12

Annex 2 WLL Auctions These auctions yielded over US$ 230 M in licensing fees for all the Regions.

S. # Regions 1.9 GHz US$ M

450 MHz US$ M.

479 MHz US$ M

3.5 GHz US$ M

Total

US$

1 Karachi (KTR)

60.2 4.4 0.5 4.3 69.4

2 Faisalabad (FTR)

21.3 3.4 0.1 0.5 25.1

3 Lahore (LTR)

17.7 2.8 0.1 1.3 21.8

4 Gujranwala (GTR)

14.8 4.0 0.4 0.1 19.2

5 Multan (MTR)

14.3 3.5 0.3 0.1 18.2

6 Islamabad (ITR)

14.5 1.1 0.1 0.8 16.5

7 Northern (NTR-I)

10.1 3.1 0.3 0.5 14.0

8 Rawalpindi (RTR)

10.0 3.2 0.3 0.1 13.5

9 Southern (STR-I)

6.7 2.0 0.1 0.1 8.9

10 Central (CTR)

6.1 1.8 0.0 0.0 7.9

11 Western (WTR)

3.8 1.9 0.2 0.1 5.8

12 Southern (STR-V)

4.0 1.6 0.2 0.1 5.8

13 Northern (NTR-II)

2.8 1.3 0.1 0.1 4.2

14 Haripur (HTR)

1.7 2.0 0.2 0.1 3.9

G.Total 187.6 35.9 2.9 7.9 234.3

13

Annex 3 WLL Spectrum ownership map In the recent months this has undergone a consolidation with large portions of spectrum for WiMAX being bought out by larger players from the smaller operators with fragmented markets.

14

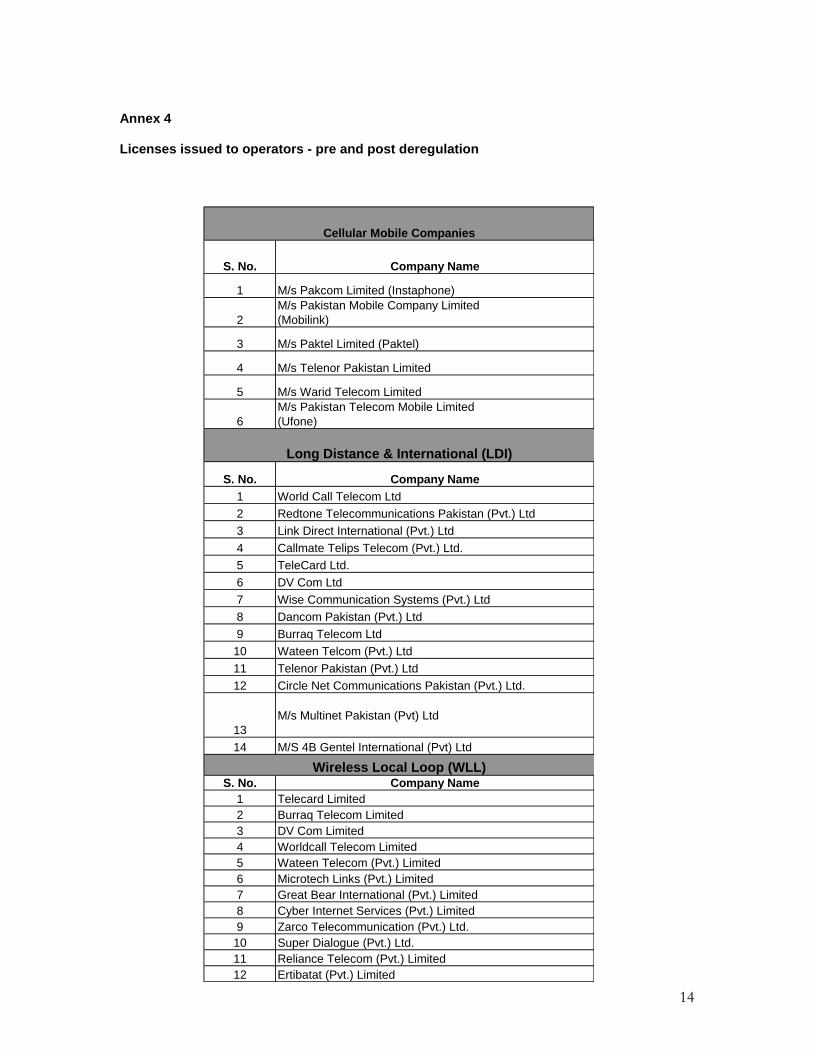

Annex 4 Licenses issued to operators - pre and post deregulation

S. No. Company Name

1 M/s Pakcom Limited (Instaphone)

2

M/s Pakistan Mobile Company Limited

(Mobilink)

3 M/s Paktel Limited (Paktel)

4 M/s Telenor Pakistan Limited

5 M/s Warid Telecom Limited

6

M/s Pakistan Telecom Mobile Limited

(Ufone)

S. No. Company Name

1 World Call Telecom Ltd

2 Redtone Telecommunications Pakistan (Pvt.) Ltd

3 Link Direct International (Pvt.) Ltd

4 Callmate Telips Telecom (Pvt.) Ltd.

5 TeleCard Ltd.

6 DV Com Ltd

7 Wise Communication Systems (Pvt.) Ltd

8 Dancom Pakistan (Pvt.) Ltd

9 Burraq Telecom Ltd

10 Wateen Telcom (Pvt.) Ltd

11 Telenor Pakistan (Pvt.) Ltd

12 Circle Net Communications Pakistan (Pvt.) Ltd.

13

M/s Multinet Pakistan (Pvt) Ltd

14 M/S 4B Gentel International (Pvt) Ltd

S. No. Company Name

1 Telecard Limited

2 Burraq Telecom Limited

3 DV Com Limited

4 Worldcall Telecom Limited

5 Wateen Telecom (Pvt.) Limited

6 Microtech Links (Pvt.) Limited

7 Great Bear International (Pvt.) Limited

8 Cyber Internet Services (Pvt.) Limited

9 Zarco Telecommunication (Pvt.) Ltd.

10 Super Dialogue (Pvt.) Ltd.

11 Reliance Telecom (Pvt.) Limited

12 Ertibatat (Pvt.) Limited

Cellular Mobile Companies

Long Distance & International (LDI)

Wireless Local Loop (WLL)

15

Annex 5 Licenses issued to operators - pre and post deregulation (contd)

S. No. Company Name

1 Dancom Pakistan (Pvt.) Ltd.

2 Easy Phone (Pvt.) Ltd.

3 Cyber-Soft Technologies (Pvt.) Ltd.

4 NetSol Connect (Pvt.) Ltd.

5 Air Track Telecommunication (Pvt.) Ltd.

6 Call 2 Phone (Pvt.) Ltd.

7 Web Concepts (Pvt.) Ltd.

8 Zari Telecommunications (Pvt.) Ltd.

9 Vision Telecom (Pvt.) Ltd.

10 Metrotel (Pvt.) Ltd.

11 Albadar Etisalat (Pvt.) Ltd.

12 Brain Ltd.

13 Hazara Communications (Pvt.) Ltd.

14 ION (Pvt.) Ltd.

15 Sohail & Inam (Pvt.) Ltd.

16 Telenex (Pvt.) Ltd.

17 Union Communications (Pvt.) Ltd.

18 Unified Technologies (Pvt.) Ltd.

19 Velocity (Pvt.) Ltd.

20 WorldCall Broadband Ltd.

21 WorldCall Multimedia Ltd.

22 Z-Communication (Pvt.) Ltd. (CCZ)

23 Eagle.Com (Pvt.) Ltd.

24 Naya Tel(Pvt.) Ltd.

25 City Links Communications Ltd.

26 Cyber House (Pvt.) Ltd.

27 Poleax Telecom (Pvt.) Ltd.

28 Multinet Pakistan (Pvt.) Ltd.

29 Whistler Telecom (Pvt.) Ltd.

30 Global Touch (Pvt.) Ltd.

31 Frontier Telecom (Pvt.) Ltd.

32 Stanley Telecom (Pvt.) Ltd.

33 Globecomm Wireless (Pvt.) Ltd.

34 Satcomm (Pvt.) Ltd.

35

IBEX Telecommunication

(Pvt.) Ltd.

S. No. Company Name

1

Pakistan Telecommunication Company Limited

(PTCL)

2 National Telecommunication Company (NTC)

3 Special Communication Orginisation (SCO)

PTCL, NTC SCO

Fixed Local Loop (FLL)

16

Annex 6 Pakistan – some economic facts Pakistan has an area of 796,096 square kilometers and population of 160 million. Strategically located in South Asia, Pakistan is at the crossroads between Eastern and Western Asia. Pakistan is the gateway to the energy rich Central Asian States, the financially liquid Gulf States and the economically advanced Far Eastern tigers. This strategic advantage alone makes Pakistan a marketplace teeming with possibilities. With three major international airports and thirty-eight domestic airports, Pakistan is accessible via fifty international airlines. Pakistan's geographical location, a rapidly expanding transportation and communications infrastructure and an environment conducive to business makes it an attractive destination for investors.

Pakistan Economic Facts 2007

Indicator 2002-03 2003-04 2004-05 2005-06 2006-07

Real GDP Growth (%) 4.7 7.5 9.0 6.6 7.0

Foreign Exchange Reserves US Billion 10.7 12.3 12.6 12.8 15.1

Per Capita Income US$ 586 669 733 833 925

Population (Million) 147 150 152 155 158

Economic Indicators (2006-2007)

Indicators 2000-01 2001-02 2002-03 2003-04 2004-05 2005-06 2006-2007 + (-) %

Exports (Billion $) 9.20 9.13 11.16 12.31 14.39 16.47 17.01 3

Imports (Billion $) 10.72 10.34 12.22 15.59 20.60 28.58 30.54 9

Trade Balance (Billion $) (1.52) (1.20) (1.06) (3.28) (6.21) (12.11) (13.53) 12

Net Revenue (Billion Rs.) 393.9 404.1 460.6 518.8 590.39 712.61 841.4 18

FDI (Million $) 322.40 484.70 798.00 949.40 1524 3,521 5,125 46

Foreign Investment (Million $) (FDI+Public&Private Portfolio)

182.00 475.00 820.00 922.00 1677 3,872 8,417 88

Workers Remittances (Billion $)

1.09 2.39 4.24 3.872 4.17 4.60 5.49 19

Forex Reserves (Billion $) 3.22 6.43 10.72 12.33 12.61 13.14 15.18 16

Exchange Rate (Rs./ US$) 58.4 61.0 57.7 57.92 59.66 60.16 60.5 1

Stock Exchange Index 1300 1520 3402 5279 7450 9,989 13,772 38

GDP Growth 2.6% 3.6% 5.1% 6.4% 8.4% 6.6% 7.0%

Inflation 4.4% 3.4% 3.3% 3.9% 9.3% 8% 7.9%