Embed Size (px)

Citation preview

Overview of the audit focus areas14 July 2015

2

The Auditor-General of South Africa has a constitutional mandate and, as the Supreme Audit Institution (SAI) of South Africa, exists to

strengthen our country’s democracy by enabling oversight, accountability and governance in the

public sector through auditing,

thereby building public confidence.

Our reputation promise

Our annual audits examine three areas

1 FAIR PRESENTATION AND RELIABILITY OF FINANCIAL STATEMENTS

2 RELIABLE AND CREDIBLE PERFORMANCE INFORMATION FOR PREDETERMINED OBJECTIVES

3 COMPLIANCE WITH KEY LEGISLATION ON FINANCIAL AND PERFORMANCE MANAGEMENT

Local government – our audits and messages – 2014/15

Financial statements Annual performance report

Compliance with key legislation

Required toreport on:

Development priorities

Quality of submitted

AFS

Quality of submitted

APR

SCM

HR Financial health

ICT

Roads infrastructure

Water and sanitation

• Effective leadership culture

• Oversight responsibility

• HR management

• Policies and procedures

• Audit action plans

• Proper record keeping

• Processing and reconciling controls

• Regular and reliable reporting

• IT systems controls

• Risk management

• Internal audit

• Audit committees

Strategic planning performance management

Budget management

Transfer of funds and conditional grants

Asset and liability management

Revenue management

Expenditure management (including UIFW)

Financial statement and annual report

Consequence management

HR management

Audit committees Internal audit

Procurement and contract management

From the audit process: Key controls

Risk areas

Coordinating departments –COGTA, treasuries and

Premier’s office

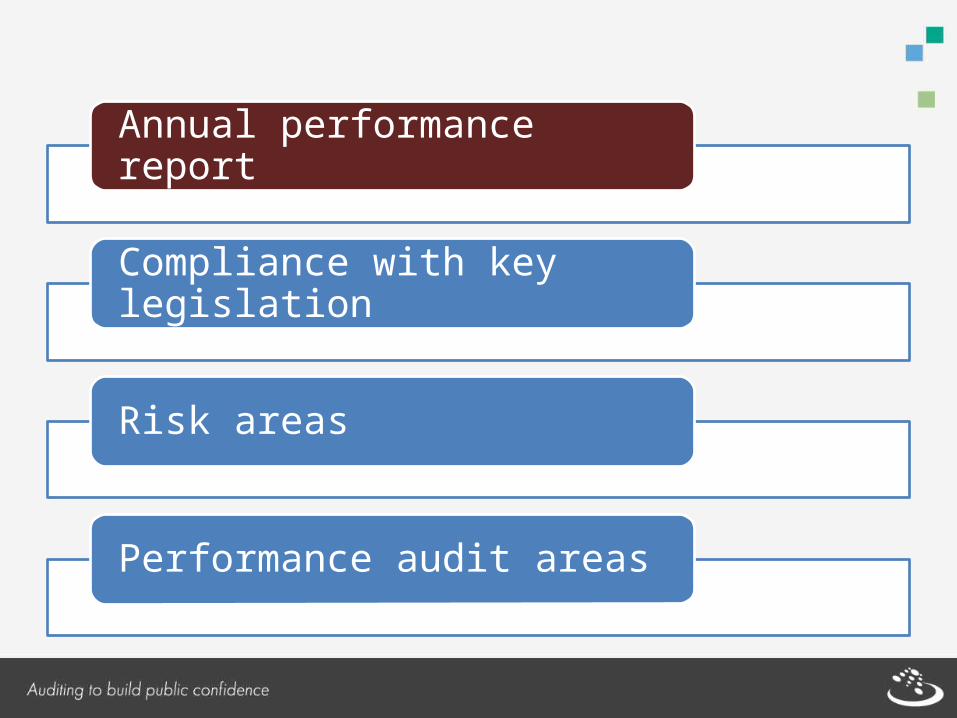

Annual performance report

Compliance with key legislation

Risk areas

Performance audit areas

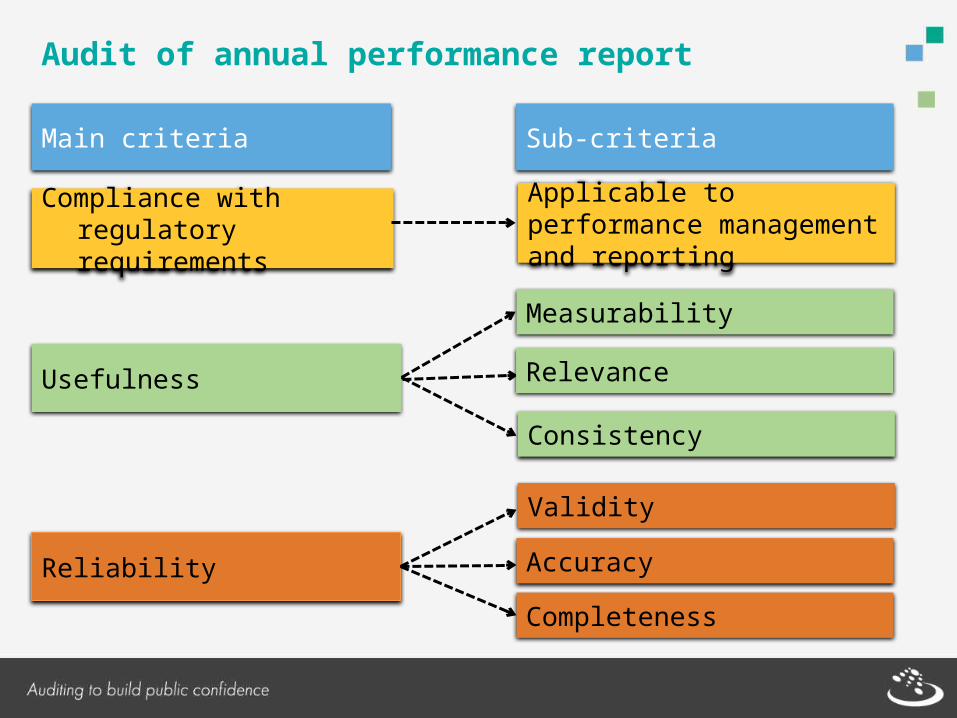

Audit of annual performance report

Main criteria Sub-criteria

Compliance with regulatory requirements

Applicable to performance management and reporting

Usefulness

Measurability

Relevance

Consistency

Reliability

Validity

Accuracy

Completeness

Good performance indicators

Well definedClear, unambiguous definition so that data will be collected consistently and easy to understand and use

VerifiablePossible to validate the processes and systems

Cost-effectiveUsefulness of the indicator must justify the cost of collecting the data

AppropriateAvoid unintended consequences and encourage service delivery improvements

RelevantRelate logically and directly to an aspect of the institution's mandate

ReliableAccurate enough for its intended use and respond to changes

* Source: NT FMPPI

SMART performance targets

S

M

A

R

T

PECIFIC

EASURABLE

CHIEVABLE

ELEVANT

IME BOUND

Nature and required level of performance can be clearly identified

Required performance can be measured

Realistic given existing capacity

Required performance is linked to achievement of goal

Time period/deadline for delivery is specified

* Source: NT FMPPI

Specific focus from 2014/15

Selection for audit - development priorities that addresses basic services:

• Water• Sanitation• Electricity• Waste removal

Inclusion of KPIs for basic services (as prescribed by MSA and regulations)

Annual performance report

Compliance with key legislation

Risk areas

Performance audit areas

Compliance focus areasStrategic planning performance management- IDP and SDBIP (including public

participation)- KPI requirements- Performance management system

Budget management- Approval (new budget)- Implementation and

monitoring (current budget)

Asset and liability management- Asset control (including capital assets)- Investments- Short and long terms debt- Guarantees and securities

Revenue management- Policies- Revenue collection - Property rates

Expenditure management- Expenditure control- 30 day payment- Prevention and reporting

of UIFW

Financial statement and annual report- Submission and quality

of AFS- Annual report processes

Consequence management- UIFW - Fraud and improper conduct in SCM- Financial misconductAudit committees

- Existence- Operations

Internal audit- Existence- Operations

UIFW = unauthorised, irregular, fruitless and wasteful

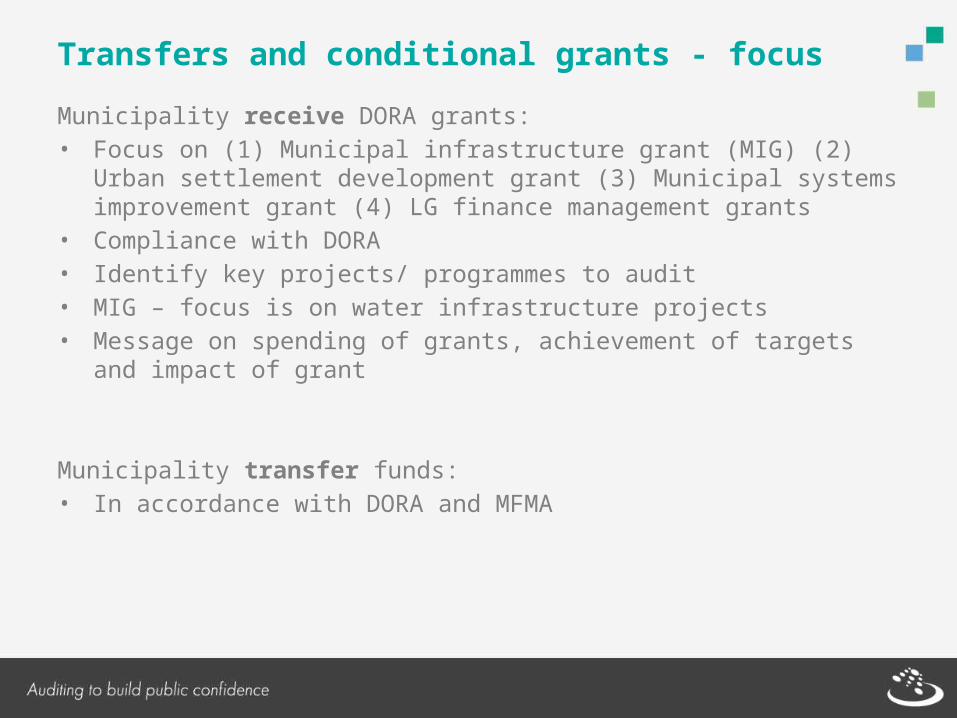

Transfers and conditional grants - focus

Municipality receive DORA grants:• Focus on (1) Municipal infrastructure grant (MIG) (2) Urban settlement

development grant (3) Municipal systems improvement grant (4) LG finance management grants

• Compliance with DORA• Identify key projects/ programmes to audit• MIG – focus is on water infrastructure projects• Message on spending of grants, achievement of targets and impact of grant

Municipality transfer funds:• In accordance with DORA and MFMA

Annual performance report

Compliance with key legislation

Risk areas

Performance audit areas

Quality of submitted

AFS

Quality of submitted

APR

SCM

HR Financial health

ICT

Quality of submitted AFS and APR

Material misstatements in submitted financial statements:• Material misstatements identified through audit process• Which could have been prevented or detected by auditee internal control system• Not isolated incident or UIFW identified in audit process• Non-compliance finding in audit report

Material misstatements in submitted annual performance report• Material misstatements identified through audit process• Which could have been prevented or detected by auditee internal control system• In audit report as “other matter”

Procurement and contract management (SCM)

Through audit we cover:• SCM internal controls• Payments to fictitious suppliers• Employees and councillors with interest in suppliers• Close family members of employees and councillors with interest in suppliers• Other state official with interest in suppliers• Prohibited suppliers• Prospective suppliers list • Quotation processes• Competitive bidding processes• Unsolicited bids• Contract management

Requirements from MFMA, SCM regulations, PPPFA and CIDB requirements

HR management and consultants

HR managementThrough audit we cover the compliance requirements for:• Appointments and acting positions• Suspensions• HR planning and organisation• Minimum competencies (effective)• Performance management

We also gather information on the following to assess control environment and report on in general report:• Whether there are senior managers made responsible for strategic planning and

for monitoring and evaluation• Vacancies and stability in positions of key officials – MM, CFO, HoS, senior

management, finance unit• Key official progress towards minimum competencies • Performance management aspects

HR management and consultants

Consultants:Through audit we assess the following processes in managing consultants:• Planning and appointment• Availability of internal capacity• Training and transfer of skills• Performance management and monitoring

We also gather information on the following to assess control environment and report on in general report:• The extent of use of consultants – particularly for financial reporting and

performance information• Whether the audit identified material findings in the areas consultants did work

and the reasons

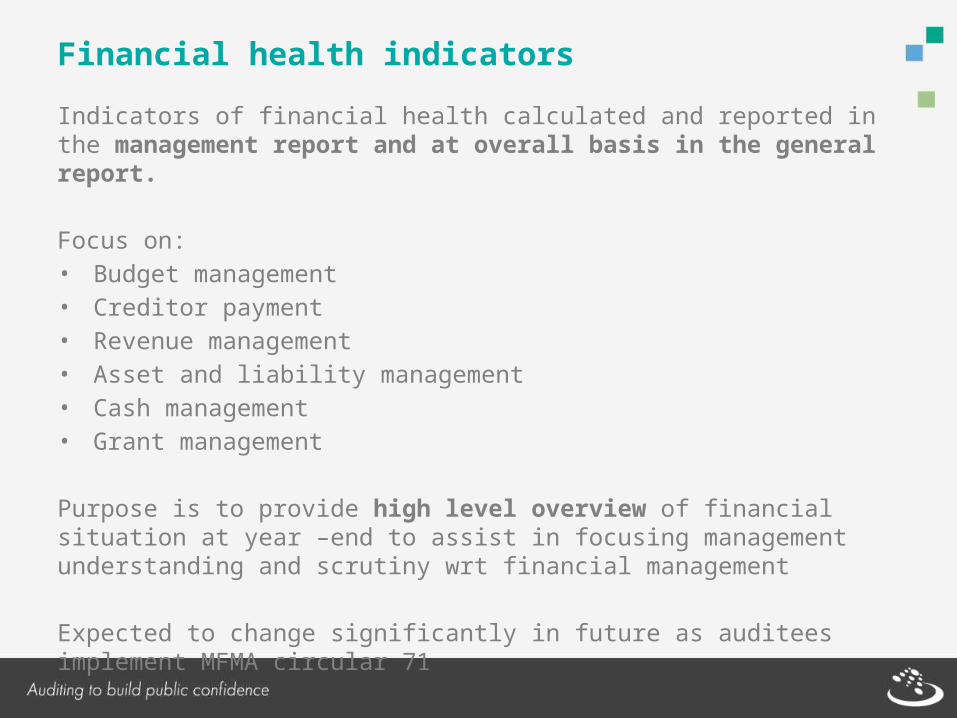

Financial health indicators

Indicators of financial health calculated and reported in the management report and at overall basis in the general report.

Focus on:• Budget management • Creditor payment• Revenue management• Asset and liability management• Cash management• Grant management

Purpose is to provide high level overview of financial situation at year –end to assist in focusing management understanding and scrutiny wrt financial management

Expected to change significantly in future as auditees implement MFMA circular 71

Information technology controls

ICT controls are assessed as part of audit process

Specific attention is given to:• IT governance• Security management• User access management• IT service continuity

Annual performance report

Compliance with key legislation

Risk areas

Performance audit areas

Performance audit areas

AGSA has discretion to also focus on additional areas that relate to service delivery through its mandate to do performance audits

In past 2 years there has been a gradual phasing in of work on the following two areas:• Water and sanitation• Roads infrastructure

Current focus is on planning and performance management processes.

Local government – our audits and messages – 2014/15

Financial statements Annual performance report

Compliance with key legislation

Required toreport on:

Development priorities

Quality of submitted

AFS

Quality of submitted

APR

SCM

HR Financial health

ICT

Roads infrastructure

Water and sanitation

• Effective leadership culture

• Oversight responsibility

• HR management

• Policies and procedures

• Audit action plans

• Proper record keeping

• Processing and reconciling controls

• Regular and reliable reporting

• IT systems controls

• Risk management

• Internal audit

• Audit committees

Strategic planning performance management

Budget management

Transfer of funds and conditional grants

Asset and liability management

Revenue management

Expenditure management (including UIFW)

Financial statement and annual report

Consequence management

HR management

Audit committees Internal audit

Procurement and contract management

From the audit process: Key controls

Risk areas

Coordinating departments –COGTA, treasuries and

Premier’s office