Embed Size (px)

Citation preview

OVERVIEW OF RECENT OVERVIEW OF RECENT ECONOMIC AND SOCIAL ECONOMIC AND SOCIAL

DEVELOPMENTS IN AFRICADEVELOPMENTS IN AFRICA

Adam ElHiraika,Adam ElHiraika,Director,Director,Macroeconomic Policy Division (MPD),Macroeconomic Policy Division (MPD),UNECAUNECA

KEY MESSAGES Africa’s growth remained robust despite slowing down from 5.7% in

2012 to 4.0% in 2013;

Export performance continued its post-2011 improvement in absolute terms, although intra-African trade remains low;

Despite improved export and fairly strong growth performance, Africa’s financing gap remains large. Yet, Africa’s economic transformation has to rely increasingly on domestic sources of finance.

Strong medium-term growth prospects despite downside risks and uncertainties;

Despite notable achievement, progress in social development remains below the level needed for Africa to achieve its social development goals; and

Africa needs development strategies that foster diversification, create jobs, reduce inequality and poverty and boost access to basic services in order to translate recent growth into sustained and inclusive development.

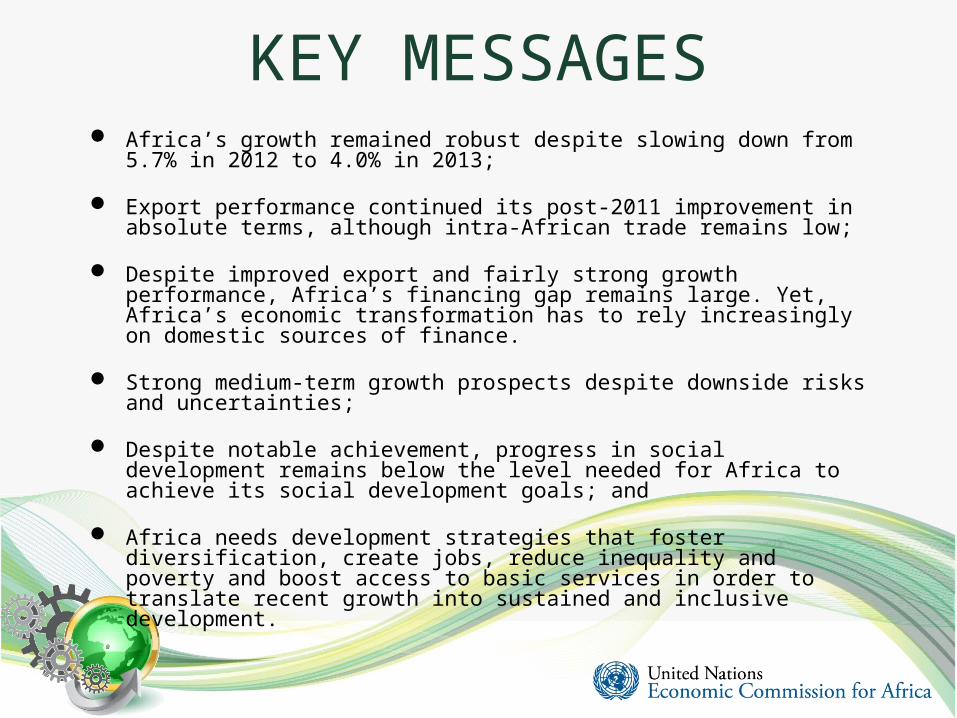

Global economic recovery remains slow

•Global growth decelerated to 2.1% in 2013, due to sluggish growth in global demand.

•Africa’s growth slowed down from 5.7% in 2012 to 4.0%, almost twice the global average, thanks mainly to:

Relatively high commodity prices;

Increased trade & investment ties with emerging economies;

Increased domestic demand.

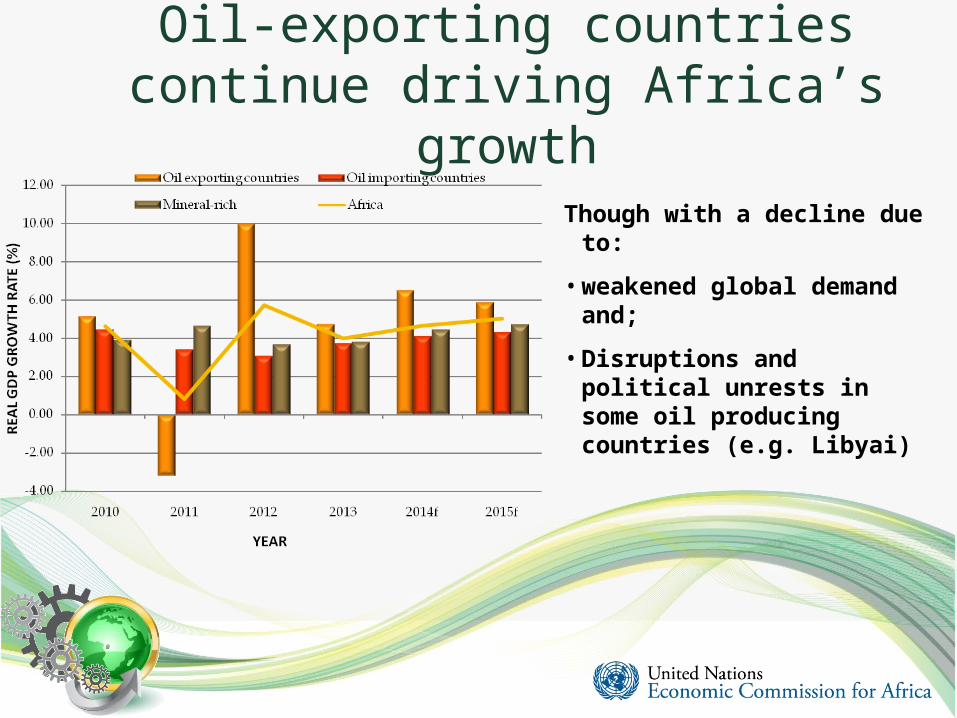

Oil-exporting countries continue driving Africa’s growth

Though with a decline due to:

•weakened global demand and;

•Disruptions and political unrests in some oil producing countries (e.g. Libyai)

Growth varied among sub-regions

With West Africa leading at 6.6% growth in 2013;

North Africa having the lowest at 2.3% mainly due to political instability and disruptions in oil production in the region;

Growth is expected to improve in all the subregions in the medium-term.

Declining inflationary pressure amid tight monetary policy in most

countries Inflation decelerated

from an avg. of 8.2% in 2012 to 8.0% in 2013;

Mainly due to: Subdued demand,

moderating international food and fuel prices; and

Tighter monetary policy in most countries.

Trade increased between Africa and its traditional partners

While growing in absolute terms, Africa’s exports have declined relative to aggregate output;

With diversification of its trade destinations, Africa’s exports to developing countries have increased (the BRICS becoming the second largest trading partners);

Intra-African trade remains more diversified and industrialized than the continent’s trade with the rest of the world;

Though not being regularly captured in many African countries, informal trade seems to command high proportions of total intra-African trade;

Implementation of CFTA and removal of remaining tariff barriers can see intra-Africa trade doubles in 10 years time.

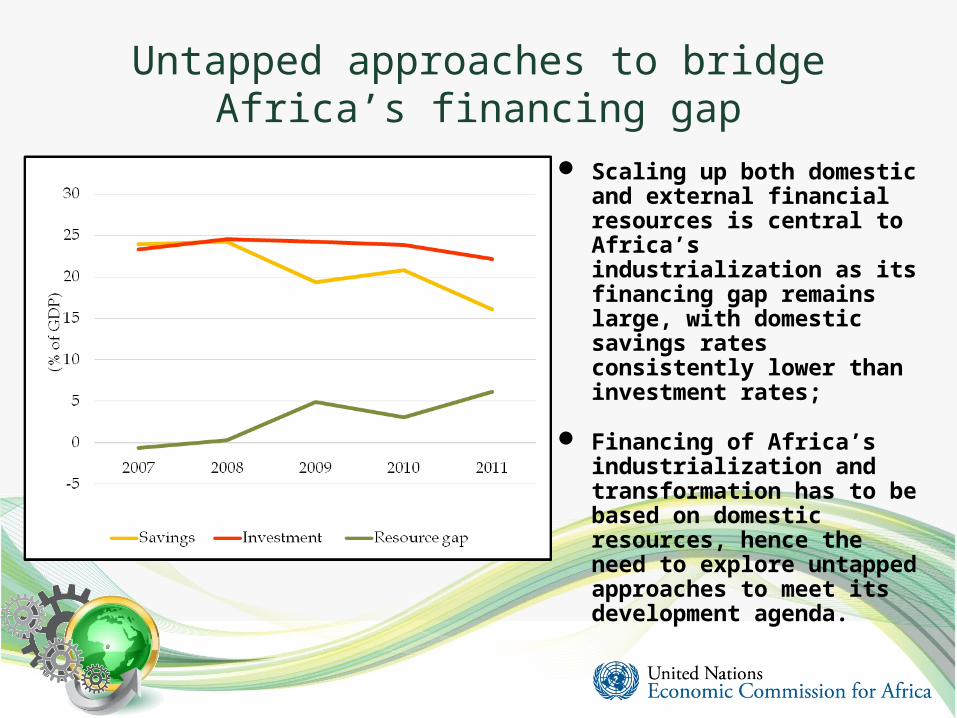

Untapped approaches to bridge Africa’s financing gap

Scaling up both domestic and external financial resources is central to Africa’s industrialization as its financing gap remains large, with domestic savings rates consistently lower than investment rates;

Financing of Africa’s industrialization and transformation has to be based on domestic resources, hence the need to explore untapped approaches to meet its development agenda.

Recent social developments

Some key social indicators are improving, but with tardy progress to meet the continent’s MDG targets.

While declining trend in many countries, poverty remains high on the continent at 48% and access to social services weak;

Increasing inequality in many countries, taking different forms, undermining efforts to reduce poverty and compromising opportunities for human development;

Labour market indicators are slowly improving, partly due to wage policies and harnessing of natural resources;

However, vulnerable employment remains stubbornly high compared with other regions (with 46.5 per cent of workers earning less than $1.25 a day in 2012), and highly skewed towards women and the youth.

Tardy labour-productivity gains hinder employment

Though labour productivity increased (2012-13), it has remained relatively low compared to East Asia;

Partly productivity growth is due to the shift of labour from agriculture to services;

Industry has remained stagnant over the past 12 years, hindering economic and employment prospects as most of the jobs (in agriculture and services) remain informal with low productivity.

Conclusions

Although robust, Africa’s growth remains below potential and has not translated into meaningful job creation and broad-based economic and social development needed to reduce poverty and inequality seen in many countries;

It is therefore essential that African countries embark on strategies to transform their economies through increased value addition to their commodities and diversify into higher-productivity employment-generating sectors, especially manufacturing and modern services.

African countries efforts to improve and sustain good macroeconomic management should be linked to long-term growth and structural transformation policies that promote inclusive development.