Embed Size (px)

Citation preview

Royal Dutch Shell

Outlook 2020

Royal Dutch Shell

Cautionary note

2

The companies in which Royal Dutch Shell plc directly and indirectly owns investments are separate legal entities. In this

presentation “Shell”, “Shell Group” and “Royal Dutch Shell” are sometimes used for convenience where references are made

to Royal Dutch Shell plc and its subsidiaries in general. Likewise, the words “we”, “us” and “our” are also used to refer to

Royal Dutch Shell plc and its subsidiaries in general or to those who work for them. These terms are also used where no useful

purpose is served by identifying the particular entity or entities. ‘‘Subsidiaries’’, “Shell subsidiaries” and “Shell companies” as

used in this presentation refer to entities over which Royal Dutch Shell plc either directly or indirectly has control. Entit ies and

unincorporated arrangements over which Shell has joint control are generally referred to as “joint ventures” and “joint

operations”, respectively. Entities over which Shell has significant influence but neither control nor joint control are referred to

as “associates”. The term “Shell interest” is used for convenience to indicate the direct and/or indirect ownership interest held

by Shell in an entity or unincorporated joint arrangement, after exclusion of all third-party interest.

This presentation contains forward-looking statements (within the meaning of the U.S. Private Securities Litigation Reform Act of

1995) concerning the financial condition, results of operations and businesses of Royal Dutch Shell. All statements other than

statements of historical fact are, or may be deemed to be, forward-looking statements. Forward-looking statements are

statements of future expectations that are based on management’s current expectations and assumptions and involve known

and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those

expressed or implied in these statements. Forward-looking statements include, among other things, statements concerning the

potential exposure of Royal Dutch Shell to market risks and statements expressing management’s expectations, beliefs,

estimates, forecasts, projections and assumptions. These forward-looking statements are identified by their use of terms and

phrases such as “aim”, “ambition”, ‘‘anticipate’’, ‘‘believe’’, ‘‘could’’, ‘‘estimate’’, ‘‘expect’’, ‘‘goals’’, ‘‘intend’’, ‘‘may’’,

‘‘objectives’’, ‘‘outlook’’, ‘‘plan’’, ‘‘probably’’, ‘‘project’’, ‘‘risks’’, “schedule”, ‘‘seek’’, ‘‘should’’, ‘‘target’’, ‘‘will’’ and similar

terms and phrases. There are a number of factors that could affect the future operations of Royal Dutch Shell and could cause

those results to differ materially from those expressed in the forward-looking statements included in this presentation, including

(without limitation): (a) price fluctuations in crude oil and natural gas; (b) changes in demand for Shell’s products; (c) currency

fluctuations; (d) drilling and production results; (e) reserves estimates; (f) loss of market share and industry competition; (g)

environmental and physical risks; (h) risks associated with the identification of suitable potential acquisition properties and

targets, and successful negotiation and completion of such transactions; (i) the risk of doing business in developing countries

and countries subject to international sanctions; (j) legislative, fiscal and regulatory developments including regulatory

measures addressing climate change; (k) economic and financial market conditions in various countries and regions; (l)

political risks, including the risks of expropriation and renegotiation of the terms of contracts with governmental entities, delays

or advancements in the approval of projects and delays in the reimbursement for shared costs; and (m) changes in trading

conditions. No assurance is provided that future dividend payments will match or exceed previous dividend payments. All

forward-looking statements contained in this presentation are expressly qualified in their entirety by the cautionary statements

contained or referred to in this section. Readers should not place undue reliance on forward-looking statements. Additional risk

factors that may affect future results are contained in Royal Dutch Shell’s Form 20-F for the year ended December 31, 2018

(available at www.shell.com/investor and www.sec.gov). These risk factors also expressly qualify all forward-looking

statements contained in this presentation and should be considered by the reader. Each forward-looking statement speaks

only as of the date of this presentation, February 20, 2020. Neither Royal Dutch Shell plc nor any of its subsidiaries undertake

any obligation to publicly update or revise any forward-looking statement as a result of new information, future events or other

information. In light of these risks, results could differ materially from those stated, implied or inferred from the forward-looking

statements contained in this presentation.

We may have used certain terms, such as resources, in this presentation that the United States Securities and Exchange

Commission (SEC) strictly prohibits us from including in our filings with the SEC. U.S. investors are urged to consider closely

the disclosure in our Form 20-F, File No 1-32575, available on the SEC website www.sec.gov.

Royal Dutch Shell February 2020 3

2019 was also a year of record final investment decisions (FIDs), with 71 million tonnes of new capacity being sanctioned, indicating belief in long-term LNG demand. Increasing uncontracted and flexible supply is set to offer more options for customers in the future.

The last decade has seen rapid growth in energy demand and corresponding greenhouse gas emissions which have created the need for more and cleaner energy options. A combination of new policy, favourable economics and partnership with renewables is driving the momentum for coal-to-gas switching.

2019 saw record LNG supply growth as the recent wave of new LNG liquefaction projects nears completion. Most of this growth was absorbed by Europe. Year-on-year growth in Asian imports slowed from highs of 2017 and 2018, but Asia still remains a growth region. Increased liquidity, new spot trading mechanisms and a wider variety of indices being used for long-term contracts point towards LNG becoming an increasingly flexible commodity.

Gas continues to provide more and cleaner energy solutions

2019 was a year of record LNG supply growth

Record supply investment due to confidence in long-term LNG demand growth

01 02 03 LNG-powered cruise shipNigeria LNGSeoul

Overview

Royal Dutch Shell February 2020 4

Gas continues to provide more and cleaner energy solutions

01Queensland Curtis Island

Royal Dutch Shell

0510152025303540

02468

1012141618

CO

2 em

issio

ns (B

T)

Ener

gy c

onsu

mpt

ion

(mkt

oe)

Rest of world energy Asia energy

Global emissions (MtCO2)(RHS)

CO

2

25%

35%

45%

55%

65%

75%

85%

Urb

anisa

tion

leve

l

OECD East Asia & PacificSouth Asia

0100200300400500600700

Air

qual

ity (P

M 2

.5)

Average WHO safe level (10)

2019 range

6.5

6.7

6.9

7.1

7.3

7.5

7.7

0102030405060708090

Glo

bal p

opul

atio

n (b

ln)

Ann

ual p

opul

atio

n in

crea

se (m

ln)

Rest of world population Asia population

Global population (RHS)

Growing population and rising living standards drive demand for energy with lower emissions

February 2020 5

Source: Shell’s interpretation of Wood Mackenzie H1, World Bank, The World Air Quality Index 2019 data

Unsafe air quality

Increased urbanisation

Growing population

Rising energy demand & emissions

Royal Dutch Shell

0% 10% 20% 30% 40% 50% 60%

Global

North America

Europe

China

India

Share in the energy mix

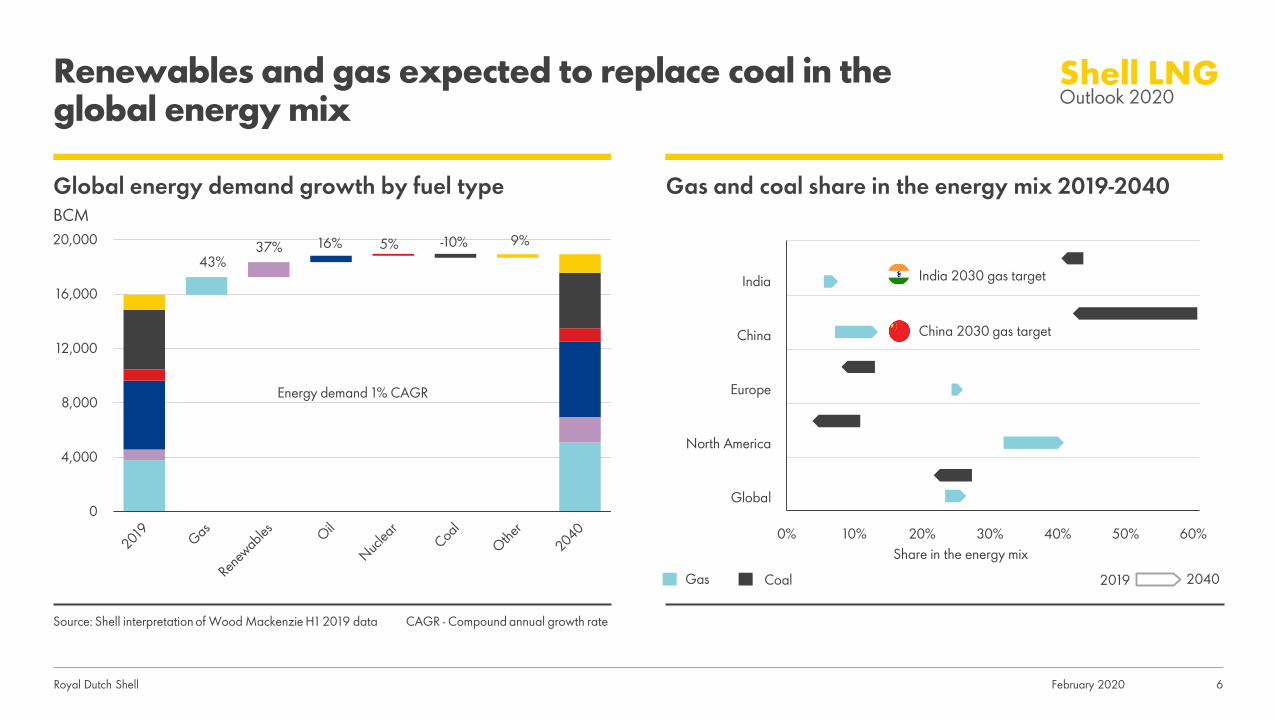

Renewables and gas expected to replace coal in the global energy mix

6

Source: Shell interpretation of Wood Mackenzie H1 2019 data CAGR - Compound annual growth rate

0

4,000

8,000

12,000

16,000

20,000

Energy demand 1% CAGR

43% 37% 16% 5% -10% 9%

Global energy demand growth by fuel typeBCM

Gas and coal share in the energy mix 2019-2040

February 2020

Gas Coal 2019 2040

India 2030 gas target

China 2030 gas target

Royal Dutch Shell

Coal-to-gas switching helping level global CO2 emissions

February 2020 7

-5

-4

-3

-2

-1

0

1

2

3

4

5

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

*Advanced economies Rest of world Global

Source: Shell interpretation of Wood Mackenzie, IEA World Energy Outlook, IEA Carbon Report 2019 data **Power sector coal-to-gas switching in Advanced economies only*Advanced economies include United States, European Union, Australia, Canada, Chile, Iceland, Israel, Japan, South Korea, Mexico, Norway, New Zealand, Switzerland & Turkey

CO2 change CO2 GT, 2010=0

Coal-to-gas switching CO2 savings CO2 MT, 2010=0

-700

-600

-500

-400

-300

-200

-100

0

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

United States China Europe

India Rest of world Global**

Equivalent to over 50% of

CO2 emissions from South America for a full year

-57%

CO2EMISSIONS

Royal Dutch Shell

Record coal phase-out and generation reduction in 2019Opportunity for more displacement of coal in the power sector

April 2019 8

Source: Shell interpretation of national government policy announcements, Carbon Brief, Global Energy Monitor, GlobalData plc and Wood Mackenzie 2019 data

Net change in global coal generationTWh

Global coal phase-out capacity announcements by dateGW

Power capacity by fuelGW

-400

-200

0

200

400

600

2001 2004 2007 2010 2013 2016 2019

0

20

40

60

80

2015 2016 2017 2018 2019

2020s 2030s 2040s

-

300

600

900

1,200

India China Europe NorthAmerica

Rest ofworld

Coal Gas Coal 2040 Gas 2040

Royal Dutch Shell

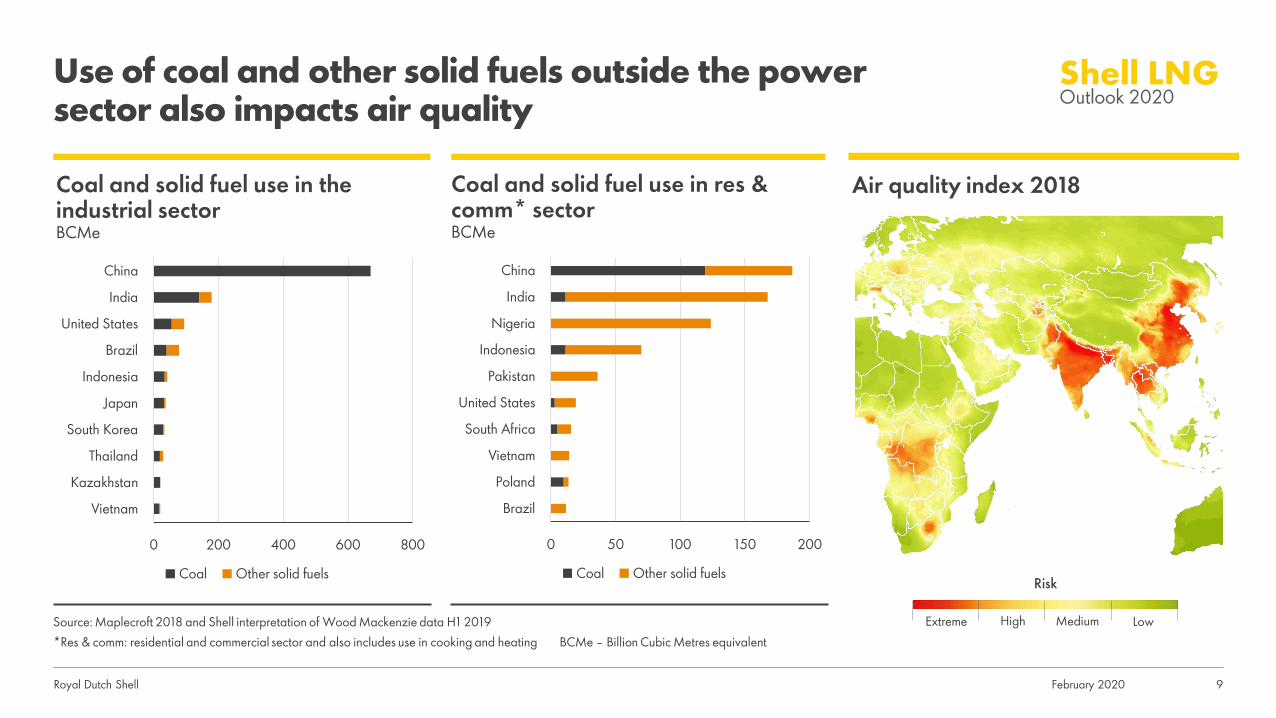

Use of coal and other solid fuels outside the power sector also impacts air quality

February 2020 9

0 200 400 600 800

Vietnam

Kazakhstan

Thailand

South Korea

Japan

Indonesia

Brazil

United States

India

China

Coal Other solid fuels

0 50 100 150 200

Brazil

Poland

Vietnam

South Africa

United States

Pakistan

Indonesia

Nigeria

India

China

Coal Other solid fuels

Source: Maplecroft 2018 and Shell interpretation of Wood Mackenzie data H1 2019*Res & comm: residential and commercial sector and also includes use in cooking and heating BCMe – Billion Cubic Metres equivalent

Coal and solid fuel use in res & comm* sectorBCMe

Coal and solid fuel use in the industrial sectorBCMe

Air quality index 2018

Extreme High Medium Low

Risk

Royal Dutch Shell

Coal-to-gas switching in the industrial sector can improve air quality

February 2020 10

Source: Shell’s interpretation of International Gas Union, Financial Times, Central Pollution Control Board (India) data 2018 and 2019 PM: particulate matter SO2: sulfur dioxide

Air quality levels in Morbi, Gujarat

μg/m3

Gas demand post-ban on coal units in Morbi industrial sector in 2019Mcm/d

Air quality in India

0

100

200

300

400

500

600

PM2.5 PM10 SO2

2017 2019

0

1

2

3

4

5

6

7

Morbi

Top 20 most polluted industrial clusters in 2018

0x 1x 2x 3x 4x 5x 6x 7x 8x 9x 10x 11x

Number of times above the WHO’s safe limit

Royal Dutch Shell

Growth of renewables favours gas in the power mix

February 2020 11

Source: Shell interpretation of Wood Mackenzie H1, national data and OpenNEM 2019 data

Average thermal load factorsThermal load factors

South Australia electricity supply December 2019MW

-1000

-500

0

500

1000

1500

2000

2500

3000

3500

4000

Batteries Renewables Gas Net interconnector

20%

30%

40%

50%

60%

70%

80%

90%

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

California UK Spain India

1%

11%

<1%

7%2%

28%

10%

<1%

Share of wind and solar in generation mix

Royal Dutch Shell

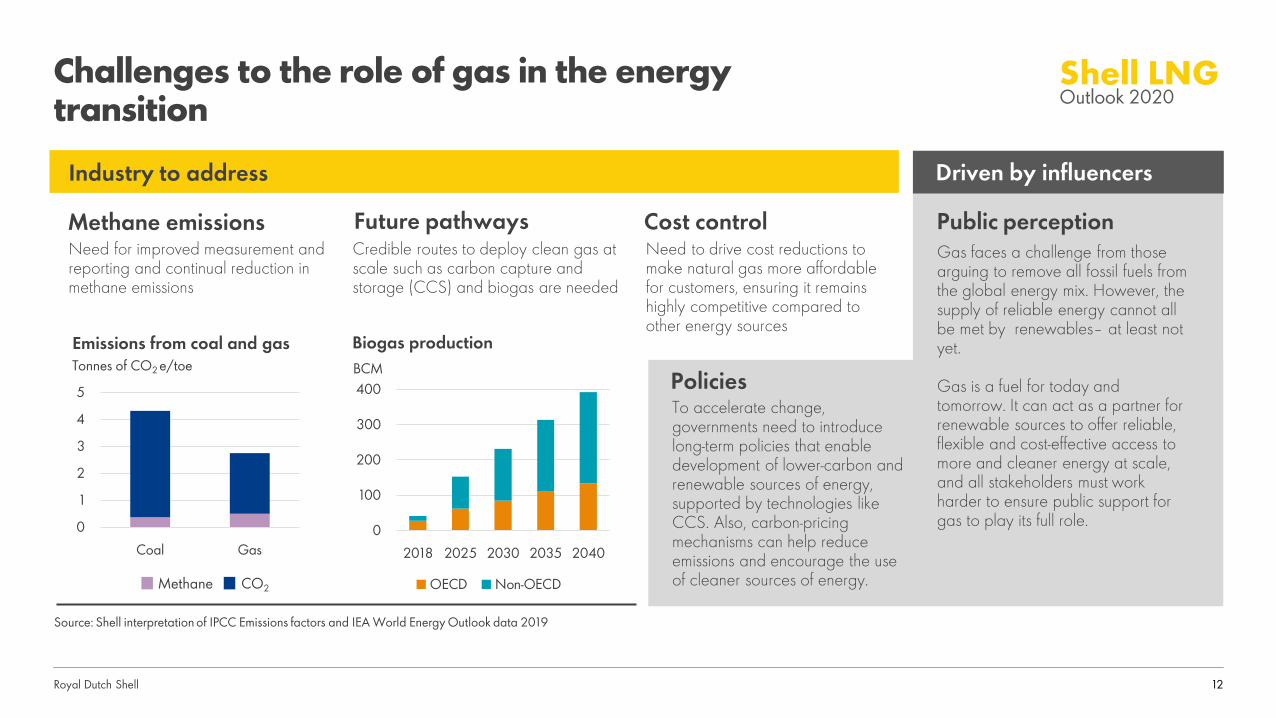

Challenges to the role of gas in the energy transition

February 2020

Need for improved measurement and reporting and continual reduction in methane emissions

Methane emissionsNeed to drive cost reductions to make natural gas more affordable for customers, ensuring it remains highly competitive compared to other energy sources

Cost controlCredible routes to deploy clean gas at scale such as carbon capture and storage (CCS) and biogas are needed

Future pathways

0

100

200

300

400

2018 2025 2030 2035 2040

Biogas production

OECD Non-OECD

Tonnes of CO2 e/toe

0

1

2

3

4

5

Coal Gas

Emissions from coal and gas

Source: Shell interpretation of IPCC Emissions factors and IEA World Energy Outlook data 2019

BCMPoliciesTo accelerate change, governments need to introduce long-term policies that enable development of lower-carbon and renewable sources of energy, supported by technologies like CCS. Also, carbon-pricing mechanisms can help reduce emissions and encourage the use of cleaner sources of energy.

Industry to address

12

CO2Methane

Public perceptionGas faces a challenge from those arguing to remove all fossil fuels from the global energy mix. However, the supply of reliable energy cannot all be met by renewables– at least not yet.

Gas is a fuel for today and tomorrow. It can act as a partner for renewable sources to offer reliable, flexible and cost-effective access to more and cleaner energy at scale, and all stakeholders must work harder to ensure public support for gas to play its full role.

Driven by influencers

Royal Dutch Shell

Gas to play a key role in reducing emissions from hard-to-electrify sectors

February 2020 13

Source: Shell interpretation of Wood Mackenzie H1 2019 data

Global gas demand growth by sectorBCM

Share of gas demand growth by sector 2019-2040Gas demand sectors

0

1,000

2,000

3,000

4,000

5,000

2019 Power Industry Res & comm Transport 2040

Gas demand 2% CAGR

40% 28%

23% 9%

-20% 0% 20% 40% 60% 80% 100% 120%

Transport

Res & comm

Industry

Power

Asia Europe FSU Americas Mid-East & Africa LNG bunker

Royal Dutch Shell

0

1,000

2,000

3,000

4,000

5,000

2019 Domesticproduction

Pipelineimports

LNGimports

2040

45% 15%

Gas demand 2% CAGR

40%

Asia set to be the key growth region for LNG

February 2020 14

Source: Shell interpretation of Wood Mackenzie H1 2019 data

Global gas supply by sourceBCM

LNG imports by regionBCM

LNG imports into AsiaBCM

0

200

400

600

800

1,000

2019 Asia Europe Americas Mid-East & Africa

2040

LNG demand 4% CAGR

74% 9% 8%

0

150

300

450

600

750

2019 China JKT SouthAsia

Rest ofAsia

2040

Asia LNG demand 4% CAGR

23% 1%

28%

48% 9%

Royal Dutch Shell February 2020 15

2019 was a year of record LNG supply growth

02 Gibraltar – small-scale LNG import terminal

Royal Dutch Shell

LNG trade volume growthMTPA (DES)

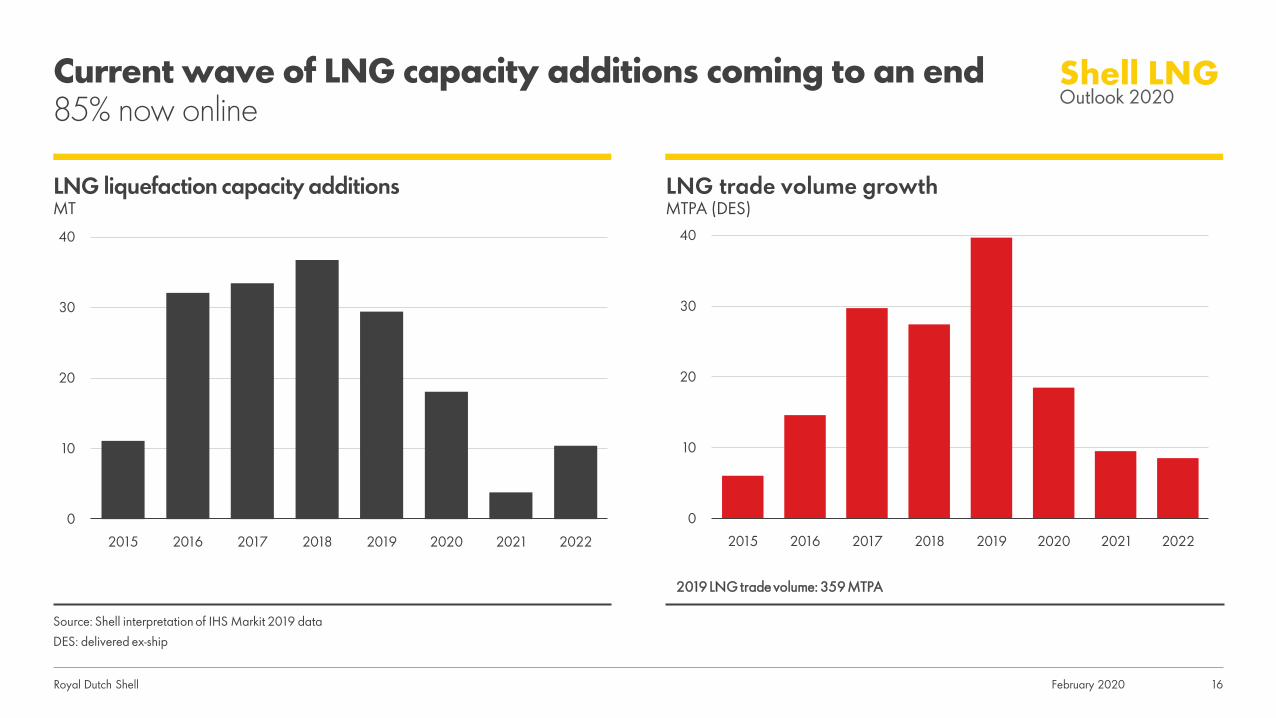

Current wave of LNG capacity additions coming to an end85% now online

February 2020 16

Source: Shell interpretation of IHS Markit 2019 dataDES: delivered ex-ship

LNG liquefaction capacity additionsMT

0

10

20

30

40

2015 2016 2017 2018 2019 2020 2021 2022

0

10

20

30

40

2015 2016 2017 2018 2019 2020 2021 2022

2019 LNG trade volume: 359 MTPA

Royal Dutch Shell

Record LNG supply growth absorbed mainly in Europe

February 2020 17

Source: Shell interpretation of IHS Markit, Wood Mackenzie, Poten & Partners Q4 2018 and 2019 data

LNG supply growth range by countryMTPA

LNG demand growth range by regionMTPA

Previous forecast range 2019

-10

0

10

20

30

40

Australia USA Russia Rest of world

-10

0

10

20

30

40

Asia Europe Americas Middle East & Africa

Actuals 2019

Royal Dutch Shell

LNG imports rise by 40 million tonnes in 2019China continues to be among top three global LNG growth markets

February 2020 18

Net imports: 2019 YoYMTPA (DES)

Source: Shell interpretation of IHS Markit, Wood Mackenzie and Poten & Partners 2018 and 2019 dataNote: Sweden, Canada, Colombia, Norway, Finland, Malta, Israel, Jamaica, Puerto Rico, Kuwait, Brazil, Panama, Poland and Dominican Republic are not included in the above chart as change is minimal

-8

-6

-4

-2

0

2

4

6

8

10

Previous forecast (consensus) Actuals

Royal Dutch Shell

0

25

50

75

100

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Pipeline import LNG import

0

100

200

300

400

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Gas demand Domestic production

LNG imports continue to meet China’s growing need for cleaner energy

February 2020 19

Source: Shell interpretation of NDRC 2019 data

China gas demand vs domestic productionBCMA

China LNG and pipeline gas importsBCMA

12%

7% 16%

34%

18%

Royal Dutch Shell

European LNG imports increased by 74% in 2019 with declining domestic production and pipeline imports …

February 2020 20

Domestic gas productionBCMA

Algerian and Russian pipeline salesBCMA

0

50

100

150

200

250

2015 2016 2017 2018 2019

UK NL Norway

0

50

100

150

200

250

2015 2016 2017 2018 2019

Algeria Russia

Source: Shell interpretation of Wood Mackenzie, S&P Global Platts and Gazprom Export LLC 2019 dataRussian sales volumes adjusted to reflect standard calorific value (40MJ/m3 at 15°C)

Gas balanceBCMA

400

450

500

550

Royal Dutch Shell

… and increased coal-to-gas switching in the power sector and storage due to mild winter

February 2020 21

Source: Shell interpretation of IHS Markit, Wood Mackenzie and Gas Infrastructure Europe (Aggregated Gas Storage Inventory) 2019 data

Coal-to-gas switching range$/MMBtu €/tonne CO2

Coal generation vs gas generationTWh

0

5

10

15

20

25

30

35

0

3

6

9

12

Jan-

16

Jul-1

6

Jan-

17

Jul-1

7

Jan-

18

Jul-1

8

Jan-

19

Jul-1

9

Range of coal-to-gas switching TTF gas

ARA coal European carbon price (RHS)

0

25

50

75

100

Jan-

15

Jun-

15

Nov

-15

Apr

-16

Sep-

16

Feb-

17

Jul-1

7

Dec

-17

May

-18

Oct

-18

Mar

-19

Aug

-19

Gas generation Coal generation

Year-end gas inventoryBCM

0

25

50

75

100

2015

2016

2017

2018

2019

NW Europe Southern Europe

CEE Storage capacity

Royal Dutch Shell

Growing industrial gas demand and declining domestic gas spurs LNG demand in South and South-east Asia

February 2020 22

230

240

250

260

270

2018 Domesticproduction

LNG 2019

-9%

109%

0%

25%

50%

75%

100%

0

10

20

30

40

LNG Imports Growth %

230

240

250

260

270

2018 Power Industry Res &comm

Transport 2019

22%

66% 8% 5%

Source: Shell interpretation of Wood Mackenzie and IHS Markit 2019 data

Gas demand growth by sectorBCMA

Gas supply growth by sectorBCMA

2019 LNG imports by countryBCMA Growth

>

Royal Dutch Shell

0

25

50

75

100

Japan South Korea

2018 2019

Higher nuclear availability and mild winters reduced imports into Japan and South Korea

February 2020 23

Source: Shell interpretation of IHS Markit, Japan Ministry of Economy, Trade and Industry, Korea Energy Economics Institute 2019 dataPower generation mix includes January through October data. *Winter months are from October through March.2020 includes YTD data

Power generation mix LNG importsMTPA

5%

7%

23%

26%

30%

29%

42%

41%

39%

38%

27%

25%

17%

18%

6%

7%

0% 20% 40% 60% 80% 100%

2018

2019

2018

2019

Japa

nSo

uth

Kore

a

Nuclear Coal Gas Oil Renewables Others

6

7

8

9

10

2015/2016

2016/2017

2017/2018

2018/2019

2019/2020

Winter* average temperatureDegree Celsius

Royal Dutch Shell

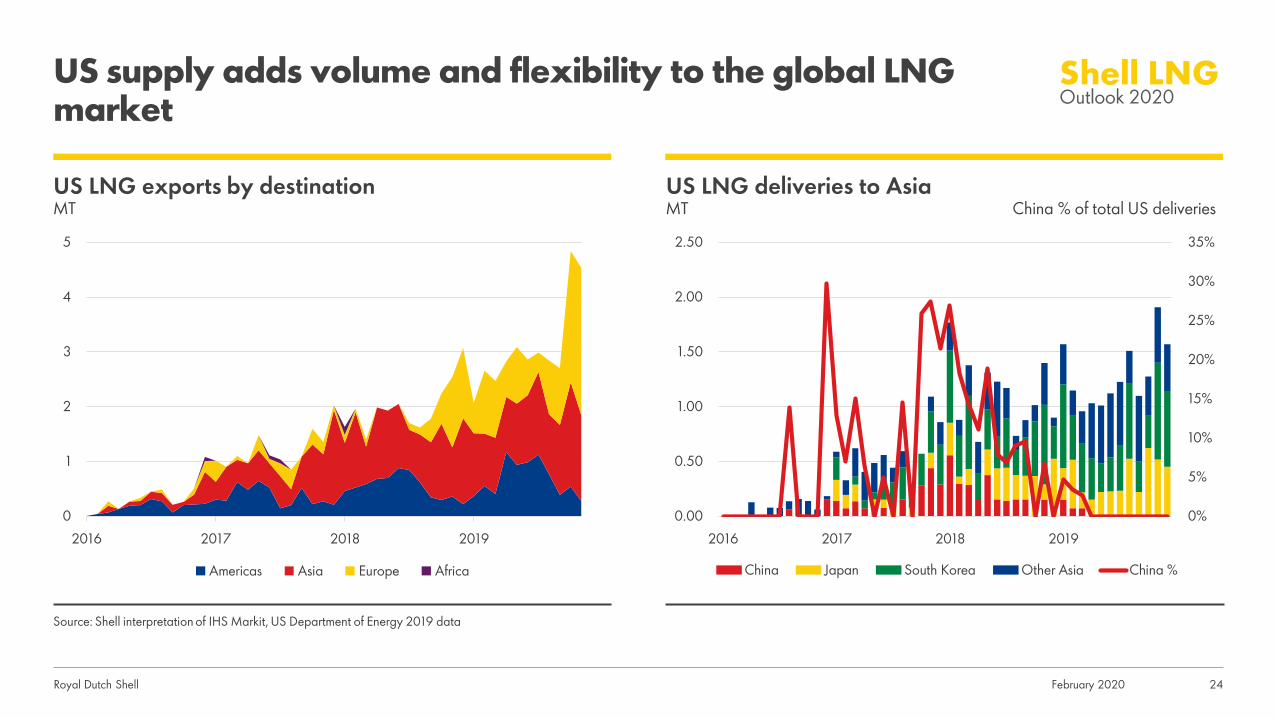

US supply adds volume and flexibility to the global LNG market

February 2020 24

Source: Shell interpretation of IHS Markit, US Department of Energy 2019 data

US LNG exports by destinationMT

US LNG deliveries to AsiaMT China % of total US deliveries

0

1

2

3

4

5

2016 2017 2018 2019

Americas Asia Europe Africa

0%

5%

10%

15%

20%

25%

30%

35%

0.00

0.50

1.00

1.50

2.00

2.50

2016 2017 2018 2019

China Japan South Korea Other Asia China %

Royal Dutch Shell

Global gas prices softened in 2019

February 2020 25

Source: Shell interpretation of ICE, CME, S&P Global Platts 2019 data

Global gas prices Asia spot price US LNG export margins*$/MMBtu

0

5

10

15

20

25

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

Dated Brent JKM TTF Henry Hub

$/MMBtu

0%

5%

10%

15%

20%

25%

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Range 2013-2018 2018 2019

JKM as % of Brent

-1

0

1

2

3

4

5

6

7

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

TTF Netback JKM Netback

2018

2019

netbacknetback

*Excludes liquefaction fee; netback calculated as: JKM and TTF minus regasification and transportation cost minus 115% Henry Hub

Royal Dutch Shell

Increasingly liquid and transparent spot market

February 2020 26

Source: Shell interpretation of IHS Markit, S&P Global Platts and ICE 2019 data

Spot LNG deliveriesCargoes % of total market

JKM eWindow/Market on CloseCargoes

ICE JKM LNG futuresCargoes ‘000 Lots*

0%

10%

20%

30%

0

250

500

750

1000

1250

1500

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

JKT China South AsiaMiddle East Europe Americas% spot

0

100

200

300

400

500

600

0

300

600

900

1200

1500

1800

2011

2012

2013

2014

2015

2016

2017

2018

2019

0

50

100

150

200

250

300

2018 2019

Bid Offer Trade

*About 300 lots is equal to 1 cargo

Royal Dutch Shell

Evolving contracting structures

February 2020 27

Source: Shell interpretation of Wood Mackenzie and IHS Markit 2019 data

Average volume and length of new contractsYears MTPA

New LNG contract volumes (by seller type)MT

Share of new LNG contract volumes (by price indexation)Share of total volume

0

0.5

1

1.5

2

0

4

8

12

16

2010 2012 2014 2016 2018

Average length Average volume (RHS)

0

200

400

600

800

1000

2010 2012 2014 2016 2018

Portfolio Project

0%

20%

40%

60%

80%

100%

2010 2012 2014 2016 2018

Oil-linked EU Gas Hub HH Hybrid JKM JLC

Royal Dutch Shell

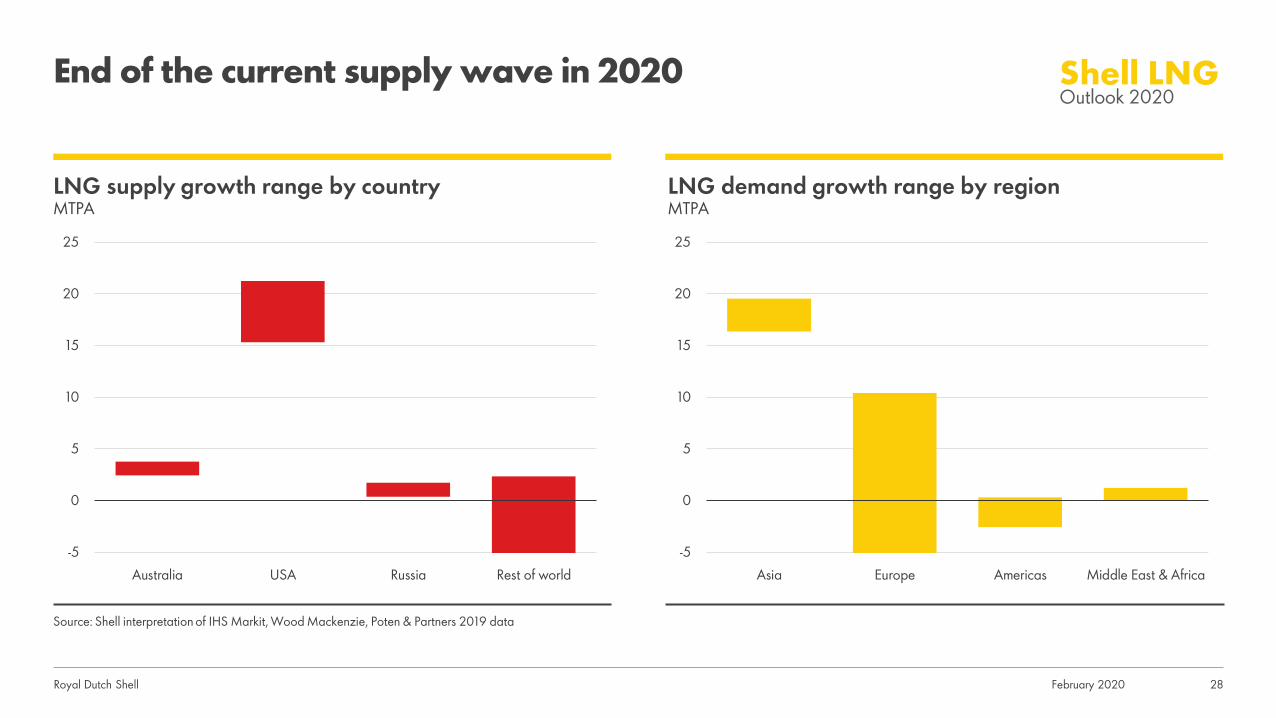

End of the current supply wave in 2020

February 2020 28

-5

0

5

10

15

20

25

Asia Europe Americas Middle East & Africa

Source: Shell interpretation of IHS Markit, Wood Mackenzie, Poten & Partners 2019 data

-5

0

5

10

15

20

25

Australia USA Russia Rest of world

LNG supply growth range by countryMTPA

LNG demand growth range by regionMTPA

Royal Dutch Shell

Global LNG market equilibrium expected to be restored

February 2020 29

LNG import growth by regionMT

Source: Shell interpretation of IHS Markit 2019 data

-5

0

5

10

15

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2016 2017 2018 2019 2020 2021

Asia Europe Americas Middle East

Royal Dutch Shell February 2020 30

03Record supply investment due to confidence in long-term LNG demand growth

LNG London bunkers a containership in Rotterdam

Royal Dutch Shell

Expected supply shortage in mid-2020s resulted in record FIDs

February 2020 31

Source: Shell interpretation of IHS Markit 2019 data

Investment in liquefaction capacity by contract typeMT

LNG equity offtake by buyer typeMT

0

20

40

60

80

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Project SPA Equity offtake

0

20

40

60

80

2010-2017 2018 2019

IOC NOC Other

Royal Dutch Shell

0

200

400

600

800

2000 2005 2010 2015 2020 2025 2030 2035 2040

Record FIDs delay expected supply-demand gapLNG demand estimated to double by 2040

February 2020 32

Source: Shell interpretation of IHS Markit, Wood Mackenzie, FGE and Poten & Partners Q4 2019 data

Emerging LNG supply-demand gapMTPA

Demand drivers for LNGMTPA

0

200

400

600

800

2000 2005 2010 2015 2020 2025 2030 2035 2040

Demand as LNG is the sole gas supply source

LNG demand supplements pipeline gas and/or domestic production

LNG demand due to declining domestic gas production

LNG demand from bunker fuel

LNG supply in operation

LNG supply under construction

Demand forecast central range

Potential Qatar expansion

Royal Dutch Shell

LNG bunkering demand accelerating

February 2020 33

Source: Shell interpretation of DNV GL, Woodmac, IHS Markit & IEA 2018 and 2019 data* Based on announcements with deliveries going out to 2027. Does not include 150 LNG-ready ships

385 LNG fuelled ships currently in operation/on order*

Confirmed LNG demand# of ships MTPA

LNG bunker demand projectionMTPA

0

10

20

30

40

50

2020 2025 2030 2035 2040Wood Mackenzie IHSMarkit

IEA (WEO 2019)On order

0 10 20 30 40

Car/Passenger ferriesContainer ships

Oil/Chemical tankersOffshore supply ships

Cruise shipsCrude oil tankers

Other vesselsRoPax

TugsGeneral cargo ships

Bulk carriersRo-Ro cargo ships

Car carriers

0.0

0.5

1.0

1.5

2.0

2.5

3.0

0

50

100

150

200

250

300

350

400

0 0 0 0 0 0 0 0 0 0 0 0 0

In operation On order ConsumptionIn operation

Royal Dutch Shell

China gas demand expected to double

April 2019 34

200

300

400

500

600

700

2019 Domesticproduction

Pipelineimports

LNGimports

2025 Domesticproduction

Pipelineimports

LNGimports

2040

52%

31%

200

300

400

500

600

700

2019 Power Industry Res &comm

Transport 2040

26%

19%

48% 7%

Source: Shell interpretation of Wood Mackenzie 2019 H1 data

China gas demand by sectorBCM

China supply by sourceBCM

17%

38%

33%

29%

Power of Siberia

Royal Dutch Shell

Growing gas demand expected in South and South-east Asia More LNG infrastructure investment needed

February 2020 35

Source: Shell interpretation of Wood Mackenzie and IHS Markit 2019 data

South Asia gas supply growth by sourceBCM

South-east Asia gas supply growth by sourceBCM

LNG demand and regasification capacityMT

0

50

100

150

200

250

2019 Domesticproduction

LNGimports

2040

India BangladeshPakistan Sri Lanka

0

50

100

150

200

250

2019 Domesticproduction

LNGimports

2040

Indonesia Malaysia Thailand

Vietnam Others

LNG demandRegas existingRegas under construction

0

50

2019 2040 Regas

India

0

50

2019 2040 Regas

Bangladesh

0

50

2019 2040 Regas

Indonesia

0

50

2019 2040 Regas

Thailand

0

50

2019 2040 Regas

Malaysia

0

50

2019 2040 Regas

Rest of SE Asia

0

50

2019 2040 Regas

Pakistan

0

50

2019 2040 Regas

Vietnam

Royal Dutch Shell February 2020 36

◼ European LNG imports increased by 74%◼ Higher nuclear availability and mild winters

reduced imports into Japan and South Korea◼ End of the current supply wave in 2020◼ Global LNG market equilibrium expected

to be restored

◼ Expected supply shortage in mid-2020s resulted in record FIDs

◼ Record FIDs delay expected supply demand gap

◼ LNG demand estimated to double by 2040

◼ 80% of energy demand growth expected to be met by renewables and gas

◼ Coal-to-gas switching helping level global CO2 emissions

◼ Record coal phase-out and generation reduction in 2019

Record supply investment due to confidence in long-term LNG demand growth

Gas continues to provide more and cleaner energy solutions

2019 was a year of record LNG supply growth

Summary

01 02 03