Embed Size (px)

Citation preview

Copyright © 2014 by A.M. Best Company, Inc. ALL RIGHTS RESERVED. No part of this report or document may be distributed in any electronic form or by any means, or stored in a database or retrieval system, without the prior written permission of the A.M. Best Company. For additional details, refer to our Terms of Use available at the A.M. Best Company website: www.ambest.com/terms.

ASEAN Non-Life & Life

Market Prospects Improve for Insurers Ahead of ASEAN IntegrationIntegration of insurance markets among the 10 member states of the Association of Southeast Asian Nations (ASEAN) has a way to go, though prospects for closer connectivity in a region presenting vibrant growth give insurers and regulators incentive to focus on boosting competitive strategies. This report looks at the relative strengths of regulatory systems, new business and capital attraction, and economic fundamentals, as well as their prospects for success in terms of market and business competitiveness.

ASEAN is a geopolitical and economic organization comprising Brunei, Cambodia, Myanmar, the Philippines, Laos, Indonesia, Malaysia, Singapore, Thailand and Vietnam. The proposed ASEAN Economic Community (AEC) slated for 2015 aims to create a competitive economic region with a single market and production base by facilitating the free flow of goods, services, investments, skilled labor and capital.

Regulations, economic conditions and ease of doing business differ greatly among ASEAN countries. That diversity extends to political systems, cultures, languages and religions, complicating the AEC project in practice. Complete insurance integration may be difficult in view of the region’s diverse backgrounds and market needs, compared with a developed market such as Singapore with its sophisticated re/insurance hub and attraction for international and regional businesses. In the longer term, less-developed countries may benefit from the accelerated pace of improvement in insurance regulation. Regulatory development leads to a stronger and more level playing field, which will create market consolidation and capital stress for some insurers on the way to achieving a well-functioning and standardized system.

With 600 million people, a relatively young population and aggregate gross domestic product of USD 2.4 trillion in 2013, ASEAN has promising insurance demand supported by persistent development of the region’s diverse economies. Compared with other emerging Asian markets, India reported GDP of USD 1.88 trillion and had a population of 1.25 billion in 2013. China’s GDP was USD 9.24 trillion with a population of 1.36 billion. Countries with stronger economic fundamentals such as Indonesia see greater attraction for new insurance investment. New frontier countries such as Cambodia and Myanmar also have drawn new insurance activity, although development of their markets is at a preliminary stage.

As the ASEAN market looks to be a production base for world markets, the ability to provide insurance capacity is vital for industry across the region. To this end, the seven member nations of Brunei, Cambodia, Indonesia, Malaysia, the Philippines, Singapore and Vietnam plan to further open their non-life and reinsurance markets by 2015, according to the AEC blueprint.

Insurance companies within ASEAN have limited capacity to write big commercial risks, impeding their competitiveness in light of market liberalization. To enhance the industry’s competitiveness, regulators have adopted initiatives to scale up measures such as capital requirements as a way to align industry standards with intra- and inter-regional norms.

With increasing global connectivity in the supply chain for goods and services, insurance regulations across ASEAN markets are becoming more compatible and standardized in support

Regulators, insurers see incentives for closer regional cooperation.

Market ReviewSeptember 29, 2014

Analytical ContactMoungmo Lee +852 2827 [email protected]

Researcher and Writer:Iris Lai+852 2827 3415

Editorial ManagementDavid Pilla

BEST’S SPECIAL REPORTOur Insight, Your Advantage.

2

Special Report ASEAN Non-Life & Life

of such changes. The Thailand floods of 2011, which created a confluence of disruptive influences on local and international insurance markets, pointed to the connectivity and ubiquity of commercial risks in both developed and developing markets.

Amid regulatory reforms and continuous economic growth, reinsurers benefit from the region’s growing primary insurance markets as most domestic players still rely on reinsurance for risk management, particularly on large-scale property and natural catastrophe risks. Long-established international reinsurers, emerging Asian companies and specialist writers have expanded their business in ASEAN, with Singapore as their regional hub.

Scaling Up RegulationASEAN countries have undergone regulatory transitions toward stricter requirements for capital and risk management. The proposed AEC in 2015, with its free-trade agreement across the region, has driven regulatory changes to enhance the market’s competitiveness.

Regulatory compatibility and transparency are prerequisites for liberalizing markets. Most ASEAN nations have updated their regulations or are upgrading insurance rules. The European Union’s Solvency II discussion over the past decade, together with increasing awareness of enterprise risk management (ERM), have helped this process.

Internationally, there has been greater incentive for regulators to work together to supervise the insurance industry. Regional alignments such as the AEC have accelerated this process. Less-developed markets will benefit from the experiences of developed markets (see Exhibit 1).

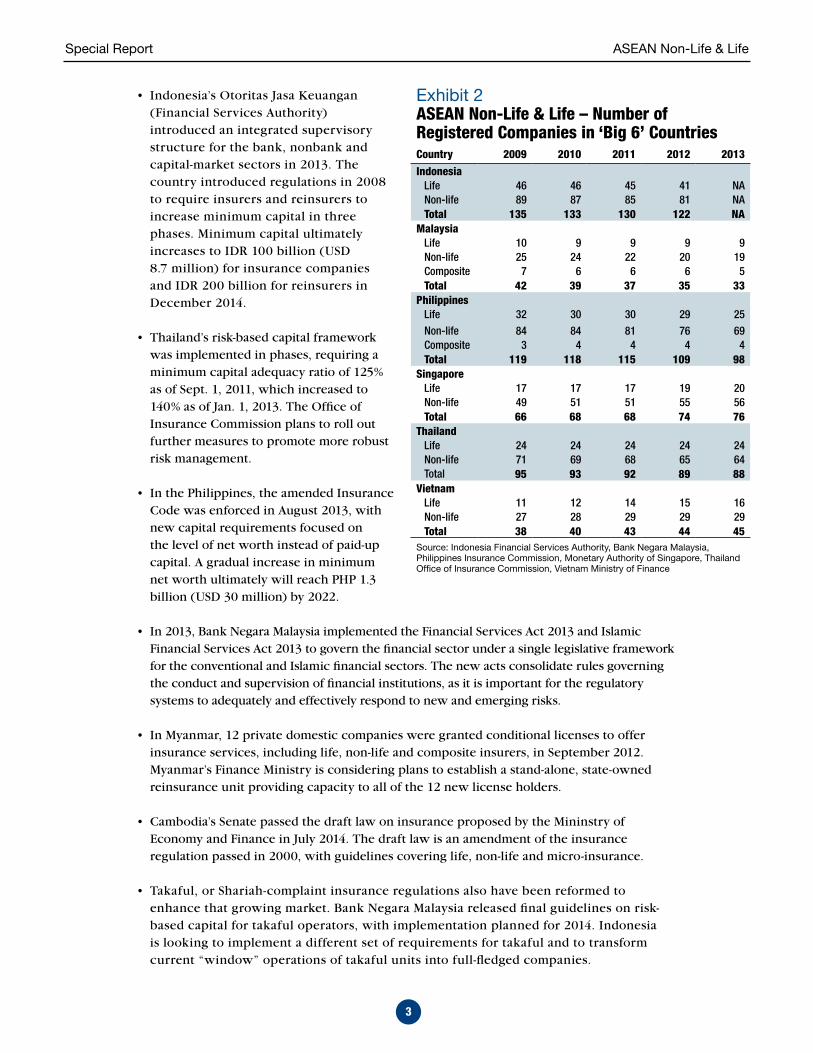

Indonesia, Malaysia, the Philippines, Singapore and Thailand have adopted a risk-based capital (RBC) framework, and Vietnam and Brunei adopted the solvency margin standard, while the rest of ASEAN nations having no particular system in place. Over the past few years, capital requirements have been raised in a bid to strengthen the industry’s capitalization, but this also has led to consolidation in some markets (see Exhibit 2). Thailand, Indonesia and the Philippines have raised capital requirements to scale up their regulatory standards and to enhance their markets’ competitiveness (see Exhibit 3).

Measures taken in various ASEAN markets include:

• In 2005, Singapore was the first regional country to introduce a more complex, risk-based capital framework. The Monetary Authority of Singapore is reviewing its RBC 2 proposals by introducing new ERM requirements, including those related to its own risk and solvency assessment. The new requirements are intended to improve the alignment of capital standards between banking and insurance.

Exhibit 1ASEAN Non-Life & Life – Regulatory Matrixes

Country Regulatory Body

Solvency Margin Requirement

Year Implemented

Brunei Monetary Authority of Brunei Darussalam (Autoriti Monetari of Brunei Darussalam), www.ambd.gov.bn

Solvency Margin

2006

Cambodia Ministry of Economy and Finance, www.mef.gov.kh

NA

Indonesia Financial Services Authority (Otoritas Jasa Keuangan (OJK)), www.ojk.go.id

RBC (Risk Based Capital)

2005

Laos Ministry of Finance, www.mof.gov.la

NA

Malaysia Bank Negara Malaysia, www.bnm.gov.my

RBC 2009

Myanmar Ministry of Finance and Revenue NA

Philippines Insurance Commission, www.insurance.gov.ph

RBC 2006

Singapore The Monetary Authority of Singapore, www.mas.gov.sg

RBC 2004

Thailand Office of Insurance Commission, www.oic.or.th

RBC 2011

Vietnam Ministry of Finance, www.mof.gov.vn

Solvency Margin

2007

Sources: AON Benfield Asia Pacific Solvency Regulation 2013; Norton Rose Fulbright; Insurance Regulators

3

Special Report ASEAN Non-Life & Life

• Indonesia’s Otoritas Jasa Keuangan (Financial Services Authority) introduced an integrated supervisory structure for the bank, nonbank and capital-market sectors in 2013. The country introduced regulations in 2008 to require insurers and reinsurers to increase minimum capital in three phases. Minimum capital ultimately increases to IDR 100 billion (USD 8.7 million) for insurance companies and IDR 200 billion for reinsurers in December 2014.

• Thailand’s risk-based capital framework was implemented in phases, requiring a minimum capital adequacy ratio of 125% as of Sept. 1, 2011, which increased to 140% as of Jan. 1, 2013. The Office of Insurance Commission plans to roll out further measures to promote more robust risk management.

• In the Philippines, the amended Insurance Code was enforced in August 2013, with new capital requirements focused on the level of net worth instead of paid-up capital. A gradual increase in minimum net worth ultimately will reach PHP 1.3 billion (USD 30 million) by 2022.

• In 2013, Bank Negara Malaysia implemented the Financial Services Act 2013 and Islamic Financial Services Act 2013 to govern the financial sector under a single legislative framework for the conventional and Islamic financial sectors. The new acts consolidate rules governing the conduct and supervision of financial institutions, as it is important for the regulatory systems to adequately and effectively respond to new and emerging risks.

• In Myanmar, 12 private domestic companies were granted conditional licenses to offer insurance services, including life, non-life and composite insurers, in September 2012. Myanmar’s Finance Ministry is considering plans to establish a stand-alone, state-owned reinsurance unit providing capacity to all of the 12 new license holders.

• Cambodia’s Senate passed the draft law on insurance proposed by the Mininstry of Economy and Finance in July 2014. The draft law is an amendment of the insurance regulation passed in 2000, with guidelines covering life, non-life and micro-insurance.

• Takaful, or Shariah-complaint insurance regulations also have been reformed to enhance that growing market. Bank Negara Malaysia released final guidelines on risk-based capital for takaful operators, with implementation planned for 2014. Indonesia is looking to implement a different set of requirements for takaful and to transform current “window” operations of takaful units into full-fledged companies.

Exhibit 2ASEAN Non-Life & Life – Number of Registered Companies in ‘Big 6’ Countries Country 2009 2010 2011 2012 2013

IndonesiaLife 46 46 45 41 NANon-life 89 87 85 81 NATotal 135 133 130 122 NA

MalaysiaLife 10 9 9 9 9Non-life 25 24 22 20 19Composite 7 6 6 6 5Total 42 39 37 35 33

PhilippinesLife 32 30 30 29 25Non-life 84 84 81 76 69Composite 3 4 4 4 4Total 119 118 115 109 98

SingaporeLife 17 17 17 19 20Non-life 49 51 51 55 56Total 66 68 68 74 76

ThailandLife 24 24 24 24 24Non-life 71 69 68 65 64Total 95 93 92 89 88

VietnamLife 11 12 14 15 16Non-life 27 28 29 29 29Total 38 40 43 44 45

Source: Indonesia Financial Services Authority, Bank Negara Malaysia, Philippines Insurance Commission, Monetary Authority of Singapore, Thailand Office of Insurance Commission, Vietnam Ministry of Finance

4

Special Report ASEAN Non-Life & Life

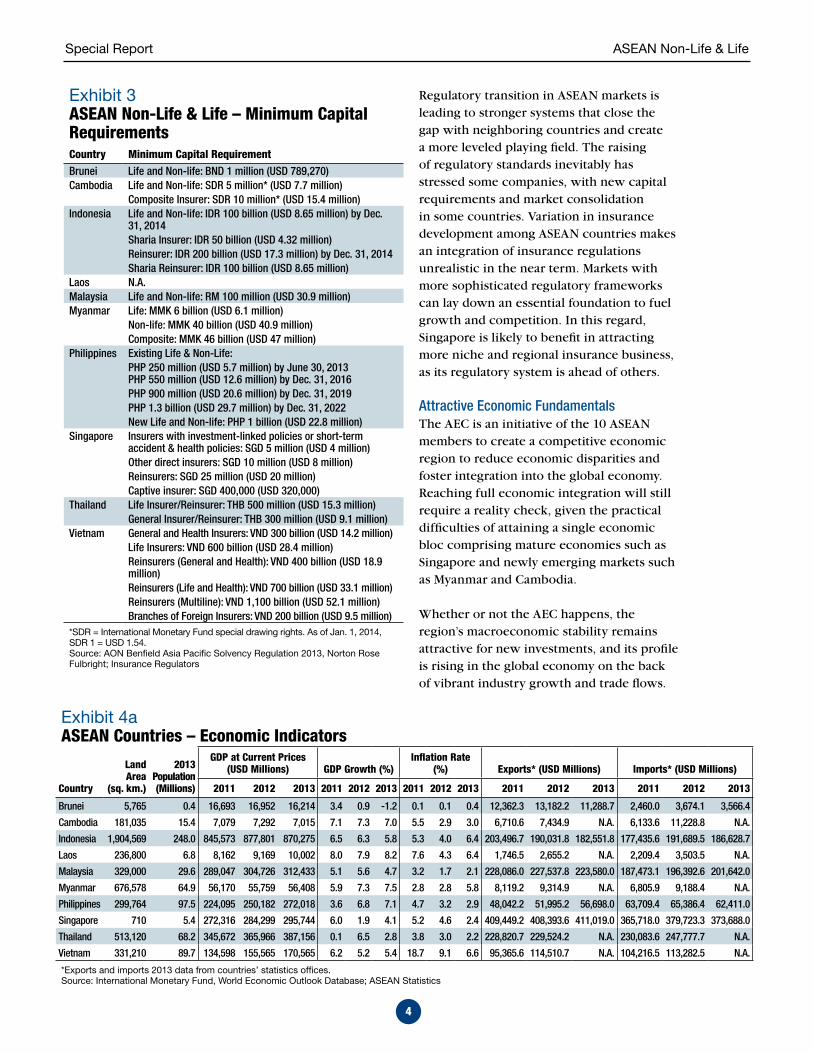

Regulatory transition in ASEAN markets is leading to stronger systems that close the gap with neighboring countries and create a more leveled playing field. The raising of regulatory standards inevitably has stressed some companies, with new capital requirements and market consolidation in some countries. Variation in insurance development among ASEAN countries makes an integration of insurance regulations unrealistic in the near term. Markets with more sophisticated regulatory frameworks can lay down an essential foundation to fuel growth and competition. In this regard, Singapore is likely to benefit in attracting more niche and regional insurance business, as its regulatory system is ahead of others.

Attractive Economic FundamentalsThe AEC is an initiative of the 10 ASEAN members to create a competitive economic region to reduce economic disparities and foster integration into the global economy. Reaching full economic integration will still require a reality check, given the practical difficulties of attaining a single economic bloc comprising mature economies such as Singapore and newly emerging markets such as Myanmar and Cambodia.

Whether or not the AEC happens, the region’s macroeconomic stability remains attractive for new investments, and its profile is rising in the global economy on the back of vibrant industry growth and trade flows.

Exhibit 3ASEAN Non-Life & Life – Minimum Capital RequirementsCountry Minimum Capital RequirementBrunei Life and Non-life: BND 1 million (USD 789,270)Cambodia Life and Non-life: SDR 5 million* (USD 7.7 million)

Composite Insurer: SDR 10 million* (USD 15.4 million)Indonesia Life and Non-life: IDR 100 billion (USD 8.65 million) by Dec.

31, 2014Sharia Insurer: IDR 50 billion (USD 4.32 million)Reinsurer: IDR 200 billion (USD 17.3 million) by Dec. 31, 2014Sharia Reinsurer: IDR 100 billion (USD 8.65 million)

Laos N.A.Malaysia Life and Non-life: RM 100 million (USD 30.9 million)Myanmar Life: MMK 6 billion (USD 6.1 million)

Non-life: MMK 40 billion (USD 40.9 million)Composite: MMK 46 billion (USD 47 million)

Philippines Existing Life & Non-Life: PHP 250 million (USD 5.7 million) by June 30, 2013PHP 550 million (USD 12.6 million) by Dec. 31, 2016PHP 900 million (USD 20.6 million) by Dec. 31, 2019PHP 1.3 billion (USD 29.7 million) by Dec. 31, 2022New Life and Non-life: PHP 1 billion (USD 22.8 million)

Singapore Insurers with investment-linked policies or short-term accident & health policies: SGD 5 million (USD 4 million)Other direct insurers: SGD 10 million (USD 8 million)Reinsurers: SGD 25 million (USD 20 million)Captive insurer: SGD 400,000 (USD 320,000)

Thailand Life Insurer/Reinsurer: THB 500 million (USD 15.3 million)General Insurer/Reinsurer: THB 300 million (USD 9.1 million)

Vietnam General and Health Insurers: VND 300 billion (USD 14.2 million)Life Insurers: VND 600 billion (USD 28.4 million)Reinsurers (General and Health): VND 400 billion (USD 18.9 million)Reinsurers (Life and Health): VND 700 billion (USD 33.1 million)Reinsurers (Multiline): VND 1,100 billion (USD 52.1 million)Branches of Foreign Insurers: VND 200 billion (USD 9.5 million)

*SDR = International Monetary Fund special drawing rights. As of Jan. 1, 2014, SDR 1 = USD 1.54.Source: AON Benfield Asia Pacific Solvency Regulation 2013, Norton Rose Fulbright; Insurance Regulators

Exhibit 4aASEAN Countries – Economic Indicators

Country

Land Area

(sq. km.)

2013 Population (Millions)

GDP at Current Prices(USD Millions) GDP Growth (%)

Inflation Rate (%) Exports* (USD Millions) Imports* (USD Millions)

2011 2012 2013 2011 2012 2013 2011 2012 2013 2011 2012 2013 2011 2012 2013

Brunei 5,765 0.4 16,693 16,952 16,214 3.4 0.9 -1.2 0.1 0.1 0.4 12,362.3 13,182.2 11,288.7 2,460.0 3,674.1 3,566.4

Cambodia 181,035 15.4 7,079 7,292 7,015 7.1 7.3 7.0 5.5 2.9 3.0 6,710.6 7,434.9 N.A. 6,133.6 11,228.8 N.A.

Indonesia 1,904,569 248.0 845,573 877,801 870,275 6.5 6.3 5.8 5.3 4.0 6.4 203,496.7 190,031.8 182,551.8 177,435.6 191,689.5 186,628.7

Laos 236,800 6.8 8,162 9,169 10,002 8.0 7.9 8.2 7.6 4.3 6.4 1,746.5 2,655.2 N.A. 2,209.4 3,503.5 N.A.

Malaysia 329,000 29.6 289,047 304,726 312,433 5.1 5.6 4.7 3.2 1.7 2.1 228,086.0 227,537.8 223,580.0 187,473.1 196,392.6 201,642.0

Myanmar 676,578 64.9 56,170 55,759 56,408 5.9 7.3 7.5 2.8 2.8 5.8 8,119.2 9,314.9 N.A. 6,805.9 9,188.4 N.A.

Philippines 299,764 97.5 224,095 250,182 272,018 3.6 6.8 7.1 4.7 3.2 2.9 48,042.2 51,995.2 56,698.0 63,709.4 65,386.4 62,411.0

Singapore 710 5.4 272,316 284,299 295,744 6.0 1.9 4.1 5.2 4.6 2.4 409,449.2 408,393.6 411,019.0 365,718.0 379,723.3 373,688.0

Thailand 513,120 68.2 345,672 365,966 387,156 0.1 6.5 2.8 3.8 3.0 2.2 228,820.7 229,524.2 N.A. 230,083.6 247,777.7 N.A.

Vietnam 331,210 89.7 134,598 155,565 170,565 6.2 5.2 5.4 18.7 9.1 6.6 95,365.6 114,510.7 N.A. 104,216.5 113,282.5 N.A.

*Exports and imports 2013 data from countries’ statistics offices.Source: International Monetary Fund, World Economic Outlook Database; ASEAN Statistics

5

Special Report ASEAN Non-Life & Life

ASEAN countries are at vastly different stages of development, presenting attractive prospects for a variety of life and non-life insurance business. Growing investment inflows, increasing infrastructure and manufacturing investments, rising affluence, favorable demographics and fast-growing consumer markets are fueling demand for insurance in both commercial and personal insurance segments. Correlated with these favorable economic fundamentals are opportunities to foster consumer markets for personal insurance in life, health, automobile and household property protection.

Foreign investment has focused on the manufacturing sector for cost benefits provided by a mixed supply of natural and human resources across ASEAN. Countries such as Cambodia and Vietnam, with ample and relatively cost-effective labor forces, have attracted production infrastructure for low-value goods such as garments. Myanmar has just begun to open its market but already is drawing substantial interest in its abundant natural resources and labor supplies. Established industrial countries such as Thailand and Malaysia remain competitive as global production sites for automobile, electronic and computer goods and parts. Vietnam also has started the production of high-end products such as mobile phones.

Among ASEAN countries’ economic factors (see Exhibits 4a and 4b), Indonesia appears to have a balanced pool of comparative advantages, delivering an attractive market size, substantial economies of scale, diversified commercial and personal business portfolios, promising foreign investments and robust trading activities.

As the largest ASEAN economy, Indonesia represents almost 40% of the ASEAN region’s economic output. It is the world’s largest exporter of natural resources such as palm oil and coal, and it takes an active role in global trade flows. Indonesia is projected to be the second-highest growth market in non-life premium in the world, with an estimated compound annual growth rate (CAGR) of 9.5% between 2014 and 2020, according to Munich Re. For life premium, Indonesia is forecasted to post a CAGR of 14.9% between 2014 and 2020.

ASEAN countries present distinctive comparative advantages correlated with their economic, political and social circumstances. Indonesia, Thailand and Malaysia are expected to benefit more from the AEC in terms of insurance growth, supported by compelling drivers in manufacturing and industrial growth, rising affluence and big consumer markets. Newly emerging markets such as Cambodia and Myanmar have drawn considerable interest in their gradual market liberalization and immense potential as they start from a low base.

In ASEAN, the nature of insurance companies varies from state-owned or captive insurers of government corporations in Vietnam, to family-controlled companies in Thailand, conglomerates in Indonesia and banking groups in Singapore and Malaysia. Multinationals tend to have a more diverse presence across the region in life, non-life and reinsurance businesses. International groups with established operations across different markets will benefit more from existing resources, networks and regional connections. Relatively, domestic players may find it more difficult to take advantage of closer economic integration.

Exhibit 4bASEAN Foreign Direct Investment Net Inflows(USD Millions)**

2011 2012

CountryIntra-

ASEANExtra-ASEAN Total

Intra-ASEAN

Extra-ASEAN Total

Brunei 67.5 1,140.8 1,208.3 N.A. N.A. N.A.Cambodia 223.8 667.9 891.7 523.0 1,034.1 1,557.1Indonesia 8,334.5 10,907.2 19,241.6 8,027.0 11,826.4 19,853.4Laos 54.0 246.8 300.7 73.6 220.7 294.4Malaysia 2,664.3 9,336.6 12,000.9 2,813.9 6,586.1 9,400.0Myanmar 210.7 1,846.3 2,057.0 118.0 1,034.3 1,152.3Philippines -74.1 1890.0 1,815.9 145.2 2,651.8 2,797.0Singapore 4,311.8 50,973.4 55,285.2 7,286.6 48,885.4 56,172.0Thailand 564.9 8,434.6 8,999.4 -89.7 10,786.7 10,697.0Vietnam 1,517.3 6,001.7 7,519.0 1,262.5 7,105.5 8,368.0** Foreign direct investment net inflow data not available for 2013.Source: International Monetary Fund, World Economic Outlook Database; ASEAN Statistics

6

Special Report ASEAN Non-Life & Life

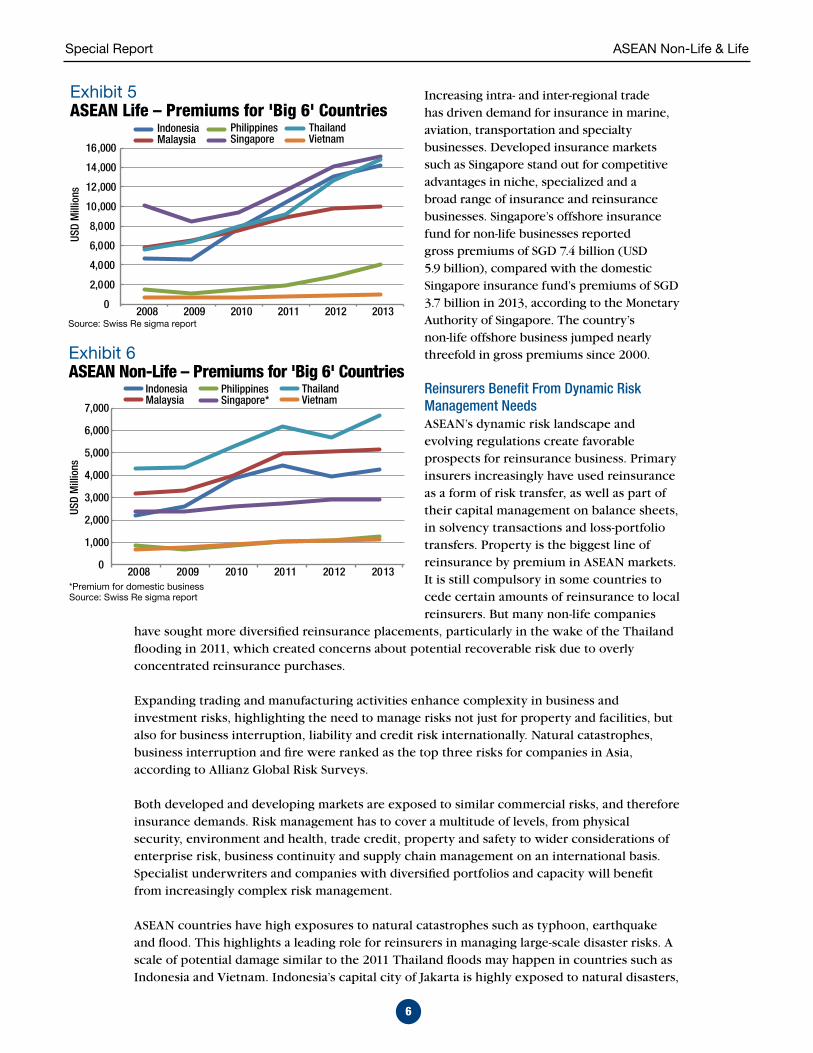

Increasing intra- and inter-regional trade has driven demand for insurance in marine, aviation, transportation and specialty businesses. Developed insurance markets such as Singapore stand out for competitive advantages in niche, specialized and a broad range of insurance and reinsurance businesses. Singapore’s offshore insurance fund for non-life businesses reported gross premiums of SGD 7.4 billion (USD 5.9 billion), compared with the domestic Singapore insurance fund’s premiums of SGD 3.7 billion in 2013, according to the Monetary Authority of Singapore. The country’s non-life offshore business jumped nearly threefold in gross premiums since 2000.

Reinsurers Benefit From Dynamic Risk Management NeedsASEAN’s dynamic risk landscape and evolving regulations create favorable prospects for reinsurance business. Primary insurers increasingly have used reinsurance as a form of risk transfer, as well as part of their capital management on balance sheets, in solvency transactions and loss-portfolio transfers. Property is the biggest line of reinsurance by premium in ASEAN markets. It is still compulsory in some countries to cede certain amounts of reinsurance to local reinsurers. But many non-life companies

have sought more diversified reinsurance placements, particularly in the wake of the Thailand flooding in 2011, which created concerns about potential recoverable risk due to overly concentrated reinsurance purchases.

Expanding trading and manufacturing activities enhance complexity in business and investment risks, highlighting the need to manage risks not just for property and facilities, but also for business interruption, liability and credit risk internationally. Natural catastrophes, business interruption and fire were ranked as the top three risks for companies in Asia, according to Allianz Global Risk Surveys.

Both developed and developing markets are exposed to similar commercial risks, and therefore insurance demands. Risk management has to cover a multitude of levels, from physical security, environment and health, trade credit, property and safety to wider considerations of enterprise risk, business continuity and supply chain management on an international basis. Specialist underwriters and companies with diversified portfolios and capacity will benefit from increasingly complex risk management.

ASEAN countries have high exposures to natural catastrophes such as typhoon, earthquake and flood. This highlights a leading role for reinsurers in managing large-scale disaster risks. A scale of potential damage similar to the 2011 Thailand floods may happen in countries such as Indonesia and Vietnam. Indonesia’s capital city of Jakarta is highly exposed to natural disasters,

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

2008 2009 2010 2011 2012 2013

IndonesiaMalaysia

PhilippinesSingapore

ThailandVietnam

USD

Mill

ions

Exhibit 5ASEAN Life – Premiums for 'Big 6' Countries

Source: Swiss Re sigma report

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2008 2009 2010 2011 2012 2013

IndonesiaMalaysia

PhilippinesSingapore*

ThailandVietnam

USD

Mill

ions

Exhibit 6ASEAN Non-Life – Premiums for 'Big 6' Countries

*Premium for domestic businessSource: Swiss Re sigma report

7

Special Report ASEAN Non-Life & Life

but a large part of the city’s economy remains uninsured. The protection gap between the economic and insured losses could amount to USD 10 billion if a major flood or earthquake hits Jakarta. The gap may triple to USD 28 billion by 2023 unless the city improves its disaster preparedness, according to a survey by Swiss Re.

In many ASEAN countries, the capital size of insurers, particularly in nations with similar concentrations of medium to small, local non-life players, is still not enough to retain large-scale risks such as natural catastrophe, commercial property and industry. This is also a factor driving demand for reinsurance as capital replacement or risk management for primary insurers. Most ASEAN non-life companies maintain low retention rates, particularly for higher risk exposures. For instance, Thailand’s worst class of flood-hit non-life business – industrial all risks – ceded more than 90% of its risk to reinsurers, which absorbed significant flood losses in international markets. The high use of reinsurance in most ASEAN countries has contributed to most non-life insurers’ stable underwriting results. On average, non-life insurers ceded about half of gross premium to reinsurance, particularly for commercial risks, divided among local and international markets and regional reinsurers.

Rising primary insurance premiums and direct insurers’ increasing appetite for alternative capital and risk management – all amid regulatory changes, natural catastrophe threats and the growing complexity of risks – present substantial prospects for reinsurance business in ASEAN. This is demonstrated by the influx of reinsurance capacity from international markets and the emergence of Asian reinsurers in the past few years. ASEAN economies’ growing connectivity and vigorous economic activity have attracted new reinsurance establishments in line with their global diversification strategies.

Malaysia’s Takaful LeadTakaful, or Islam-compliant insurance, is also a business prospect raised by both local and international insurers following increased regulatory and market integration. ASEAN countries represented one-quarter of global gross takaful contributions, with USD 3.5 billion in 2013. Malaysia has led in takaful business, accounting for 70.4% of ASEAN’s total gross takaful contributions, followed by Indonesia with 22.6% of takaful market share. The two countries’ large Muslim populations, along with initiatives on regulatory reform, have driven growth.

Malaysia is the second-largest takaful market in the world, with industry growth of 24.2% in 2013, and it is also the world’s largest family takaful market. The country’s low insurance penetration and young population present significant potential for growth, supported by favorable regulation to promote overall Islamic finance and more active participation of local and international players. Malaysia continues to lead as a regional center for global takaful in terms of business and regulatory development.

Indonesia’s attraction is its large Muslim population and current low insurance penetration. The industry grew 23.4% in 2013, with good prospects in the medium to long term as 80% of Indonesians are underinsured.

Market ProspectsThe AEC blueprint states that the process of liberalization should occur with due respect for national policy objectives and the levels of economic and financial development of individual members. It also identifies member countries with respect to specified progress in liberalizing financial services, including insurance sectors, by 2015. However, it is doubted that some members will be ready for liberalization by next year. A.M. Best believes it is premature to predict insurance integration, as market liberalization within ASEAN is in an

8

Special Report ASEAN Non-Life & Life

early stage. In reality, it is difficult for some ASEAN members to liberalize within a definite time frame as early as 2015, as the insurance sector plays a vital role in the economies of developing nations.

In the long run, A.M. Best expects liberalization to generate greater efficiency and supply of insurance capacity. This will subsequently benefit policyholders, as affordability is an issue in some ASEAN markets. The attraction of new entrants driven by liberalization will encourage efficient and alternative distribution to enhance market penetration and product development.

ASEAN countries continue to be attractive for insurance and reinsurance businesses, supported by buoyant industry growth, expanding urbanization and consumer markets, and dynamic risk management needs. There is a wide range of opportunities for insurers with scale, as well as niches for consumer, commercial and specialist businesses.

Newer insurance markets in the Indochina region such as Vietnam are attractive, with higher potential for growth and good profitability in the long term. Relatively, markets with longer histories, such as the Philippines and Indonesia, need to undergo structural changes to improve profitability for further potential growth. Key factors for success include efficient distribution and claims management, along with substantial economies of scale for cost-effective operations. Singapore stands out as a hub for regional and specialist business, drawing an increasing number of reinsurers and underwriters to write risks for the region.

Foreign capital continues to flow into the region as part of ASEAN markets’ diversification and overseas expansion strategies. They also will be able to offer competitive pricing, because the risks will be spread globally. In recent years, multinationals have created a more diverse presence across the region for life, non-life and reinsurance businesses.

Recent merger and acquisition activities highlight substantial interest from Japanese groups targeting big, high-potential markets such as Indonesia. Nippon Life, Sumitomo Life, Dai-ichi Life, Mitsui Sumitomo Insurance and Nipponkoa all entered or expanded in Indonesia in the past few years, with aggregate deal values of nearly USD 2 billion.

Against impressive growth, ASEAN markets are facing issues of both capital and qualified human resources. The relative size of insurance companies in some ASEAN markets is small, making it difficult for them to achieve economies of scale. Expense ratios in some ASEAN countries are much higher than those in East Asia, meaning ASEAN companies may face higher costs for expansion within ASEAN due to insufficient scale. A lack of compatible and stable human resources for multiple markets is also an issue for intra-regional expansion, particularly

Exhibit 7ASEAN Life & Non-Life – Insurance Penetration for ‘Big 6’ CountriesPremiums as % of gross domestic product

2008 2009 2010 2011 2012 2013

Country LifeNon-Life Total Life

Non-Life Total Life

Non-Life Total Life

Non-Life Total Life

Non-Life Total Life

Non-Life Total

Indonesia 0.92 0.43 1.34 0.85 0.48 1.33 1.10 0.54 1.64 1.23 0.55 1.78 1.42 0.53 1.94 1.60 0.50 2.10Malaysia 2.80 1.52 4.32 3.21 1.63 4.84 3.04 1.60 4.64 3.02 1.70 4.72 3.11 1.74 4.85 3.20 1.70 4.80Philippines 0.89 0.51 1.41 0.69 0.43 1.12 0.75 0.43 1.18 0.84 0.47 1.31 1.08 0.50 1.58 1.50 0.50 1.90Singapore 5.56 1.56 7.13 4.62 1.62 6.23 4.57 1.57 6.14 4.46 1.60 6.06 4.48 1.62 6.10 4.40 1.60 5.90Thailand 2.06 1.56 3.62 2.43 1.64 4.07 2.51 1.66 4.17 2.67 1.79 4.45 2.95 2.07 5.01 3.80 1.70 5.50Vietnam 0.70 0.74 1.44 0.64 0.74 1.38 0.70 0.86 1.56 0.63 0.81 1.44 0.63 0.79 1.42 0.60 0.70 1.40Source: Swiss Re sigma report

9

Special Report ASEAN Non-Life & Life

with the diverse nature of ASEAN nations. Currently, not many ASEAN companies actively venture out of their local markets.

With the AEC accession in mind, A.M. Best expects the region may see the emergence of strong players buoyed by increasing connectivity and strengthening standards. Interconnectivity of insurance business is likely greater with the relatively closer ties among companies in Malaysia and Singapore. In the future, there may be increasing connectivity among companies within the Mekong region countries of Vietnam, Cambodia, Laos and Myanmar, given their similarity in pace of development.

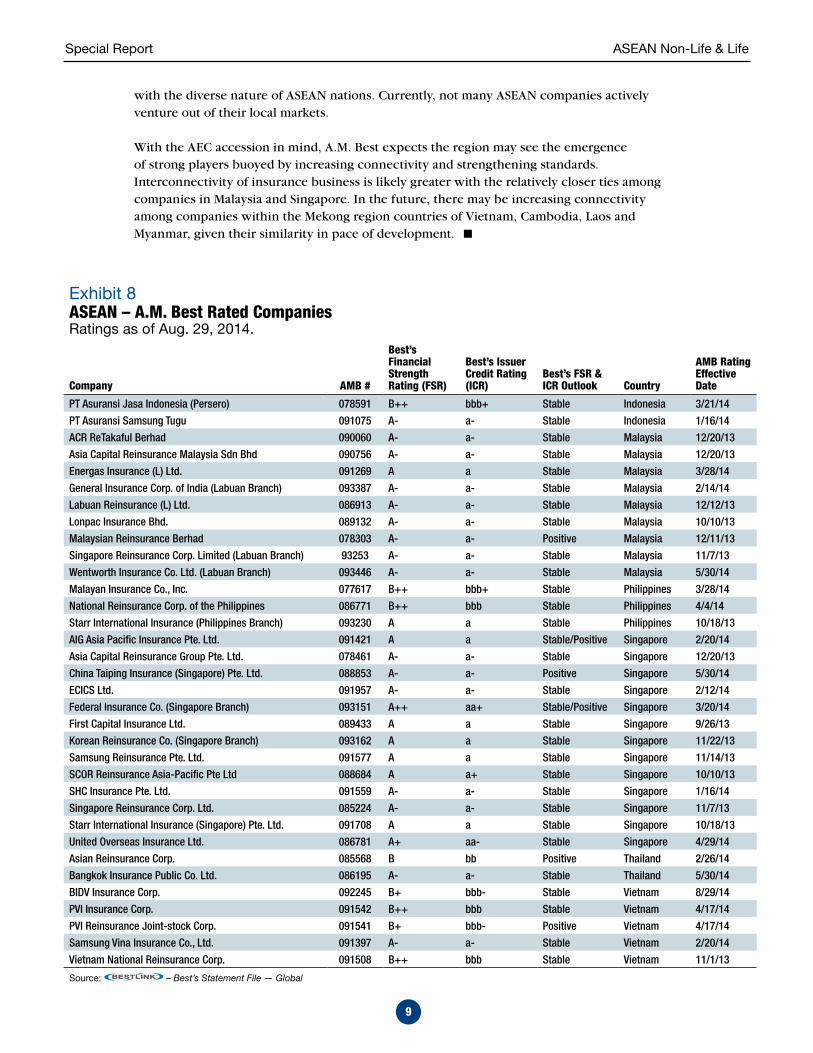

Exhibit 8ASEAN – A.M. Best Rated CompaniesRatings as of Aug. 29, 2014.

Company AMB #

Best’s Financial Strength Rating (FSR)

Best’s Issuer Credit Rating (ICR)

Best’s FSR & ICR Outlook Country

AMB Rating Effective Date

PT Asuransi Jasa Indonesia (Persero) 078591 B++ bbb+ Stable Indonesia 3/21/14

PT Asuransi Samsung Tugu 091075 A- a- Stable Indonesia 1/16/14

ACR ReTakaful Berhad 090060 A- a- Stable Malaysia 12/20/13

Asia Capital Reinsurance Malaysia Sdn Bhd 090756 A- a- Stable Malaysia 12/20/13

Energas Insurance (L) Ltd. 091269 A a Stable Malaysia 3/28/14

General Insurance Corp. of India (Labuan Branch) 093387 A- a- Stable Malaysia 2/14/14

Labuan Reinsurance (L) Ltd. 086913 A- a- Stable Malaysia 12/12/13

Lonpac Insurance Bhd. 089132 A- a- Stable Malaysia 10/10/13

Malaysian Reinsurance Berhad 078303 A- a- Positive Malaysia 12/11/13

Singapore Reinsurance Corp. Limited (Labuan Branch) 93253 A- a- Stable Malaysia 11/7/13

Wentworth Insurance Co. Ltd. (Labuan Branch) 093446 A- a- Stable Malaysia 5/30/14

Malayan Insurance Co., Inc. 077617 B++ bbb+ Stable Philippines 3/28/14

National Reinsurance Corp. of the Philippines 086771 B++ bbb Stable Philippines 4/4/14

Starr International Insurance (Philippines Branch) 093230 A a Stable Philippines 10/18/13

AIG Asia Pacific Insurance Pte. Ltd. 091421 A a Stable/Positive Singapore 2/20/14

Asia Capital Reinsurance Group Pte. Ltd. 078461 A- a- Stable Singapore 12/20/13

China Taiping Insurance (Singapore) Pte. Ltd. 088853 A- a- Positive Singapore 5/30/14

ECICS Ltd. 091957 A- a- Stable Singapore 2/12/14

Federal Insurance Co. (Singapore Branch) 093151 A++ aa+ Stable/Positive Singapore 3/20/14

First Capital Insurance Ltd. 089433 A a Stable Singapore 9/26/13

Korean Reinsurance Co. (Singapore Branch) 093162 A a Stable Singapore 11/22/13

Samsung Reinsurance Pte. Ltd. 091577 A a Stable Singapore 11/14/13

SCOR Reinsurance Asia-Pacific Pte Ltd 088684 A a+ Stable Singapore 10/10/13

SHC Insurance Pte. Ltd. 091559 A- a- Stable Singapore 1/16/14

Singapore Reinsurance Corp. Ltd. 085224 A- a- Stable Singapore 11/7/13

Starr International Insurance (Singapore) Pte. Ltd. 091708 A a Stable Singapore 10/18/13

United Overseas Insurance Ltd. 086781 A+ aa- Stable Singapore 4/29/14

Asian Reinsurance Corp. 085568 B bb Positive Thailand 2/26/14

Bangkok Insurance Public Co. Ltd. 086195 A- a- Stable Thailand 5/30/14

BIDV Insurance Corp. 092245 B+ bbb- Stable Vietnam 8/29/14

PVI Insurance Corp. 091542 B++ bbb Stable Vietnam 4/17/14

PVI Reinsurance Joint-stock Corp. 091541 B+ bbb- Positive Vietnam 4/17/14

Samsung Vina Insurance Co., Ltd. 091397 A- a- Stable Vietnam 2/20/14

Vietnam National Reinsurance Corp. 091508 B++ bbb Stable Vietnam 11/1/13

Source: – Best’s Statement File — Global

10

Special Report ASEAN Non-Life & Life

11

Special Report ASEAN Non-Life & Life

Special Report ASEAN Non-Life & Life

Published by A.M. Best Company

Special ReportCHAIRMAN & PRESIDENT Arthur Snyder III

EXECUTIVE VICE PRESIDENT Larry G. Mayewski

EXECUTIVE VICE PRESIDENT Paul C. Tinnirello

SENIOR VICE PRESIDENTS Douglas A. Collett, Karen B. Heine, Matthew C. Mosher, Rita L. Tedesco

A.M. BEST COMPANYWORLD HEADQUARTERS

Ambest Road, Oldwick, NJ 08858 Phone: +1 (908) 439-2200

WASHINGTON OFFICE830 National Press Building

529 14th Street N.W., Washington, DC 20045 Phone: +1 (202) 347-3090

A.M. BEST AMÉRICA LATINA, S.A. de C.V.Paseo de la Reforma 412

Piso 23Mexico City, Mexico

Phone: +52-55-5208-1264

A.M. BEST EUROPE RATING SERVICES LTD.A.M. BEST EUROPE INFORMATION SERVICES LTD.

12 Arthur Street, 6th Floor, London, UK EC4R 9AB Phone: +44 (0)20 7626-6264

A.M. BEST ASIA-PACIFIC LTD.Unit 4004 Central Plaza, 18 Harbour Road, Wanchai, Hong Kong

Phone: +852 2827-3400

DUBAI OFFICE (MENA, SOUTH & CENTRAL ASIA)Office 102, Tower 2

Currency House, DIFCPO Box 506617, Dubai, UAE

Phone: +971 43 752 780

A Best’s Financial Strength Rating is an independent opinion of an insurer’s financial strength and ability to meet its ongoing insurance policy and contract obligations. It is based on a com-prehensive quantitative and qualitative evaluation of a company’s balance sheet strength, oper-ating performance and business profile. The Financial Strength Rating opinion addresses the relative ability of an insurer to meet its ongoing insurance policy and contract obligations. These ratings are not a warranty of an insurer’s current or future ability to meet contractual obligations. The rating is not assigned to specific insurance policies or contracts and does not address any other risk, including, but not limited to, an insurer’s claims-payment policies or procedures; the ability of the insurer to dispute or deny claims payment on grounds of misrepresentation or fraud; or any specific liability contractually borne by the policy or contract holder. A Financial Strength Rating is not a recommendation to purchase, hold or terminate any insurance policy, contract or any other financial obligation issued by an insurer, nor does it address the suitability of any particular policy or contract for a specific purpose or purchaser.

A Best’s Debt/Issuer Credit Rating is an opinion regarding the relative future credit risk of an entity, a credit commitment or a debt or debt-like security. It is based on a comprehensive quantitative and qualitative evaluation of a company’s balance sheet strength, operating performance and business profile and, where appropriate, the specific nature and details of a rated debt security. Credit risk is the risk that an entity may not meet its contractual, financial obligations as they come due. These credit ratings do not address any other risk, including but not limited to liquidity risk, market value risk or price volatility of rated securities. The rat-ing is not a recommendation to buy, sell or hold any securities, insurance policies, contracts or any other financial obligations, nor does it address the suitability of any particular financial obligation for a specific purpose or purchaser.

Any and all ratings, opinions and information contained herein are provided “as is,” without any expressed or implied warranty. A rating may be changed, suspended or withdrawn at any time for any reason at the sole discretion of A.M. Best.

In arriving at a rating decision, A.M. Best relies on third-party audited financial data and/or other information provided to it. While this information is believed to be reliable, A.M. Best does not independently verify the accuracy or reliability of the information.

A.M. Best does not offer consulting or advisory services. A.M. Best is not an Investment Adviser and does not offer investment advice of any kind, nor does the company or its Rating Analysts offer any form of structuring or financial advice. A.M. Best does not sell securities. A.M. Best is compensated for its interactive rating services. These rating fees can vary from US$ 5,000 to US$ 500,000. In addition, A.M. Best may receive compensation from rated enti-ties for non-rating related services or products offered.

A.M. Best’s Special Reports and any associated spreadsheet data are available, free of charge, to all Best’s Insurance News & Analysis subscribers. Nonsubscribers can purchase the full report and spreadsheet data. Special Reports are available through our Web site at www.ambest.com/research or by calling Customer Service at (908) 439-2200, ext. 5742. Briefings and some Special Reports are offered to the general public at no cost. For press inquiries or to contact the authors, please contact James Peavy at (908) 439-2200, ext. 5644.

SR-2014-513