Embed Size (px)

Citation preview

Vision and Objectives

22

OPRED

Wendy Kennedy

EUOAG

Offshore Petroleum Regulator

for Environment & Decommissioning

Chief Executive - Wendy Kennedy

Based in Aberdeen

OPRED’s aims are to regulate the offshore oil and gas industries in the context of sustainable

development; to achieve improved regulatory compliance without imposing an undue burden on the industry but nevertheless ensuring that it limits taxpayer liability.

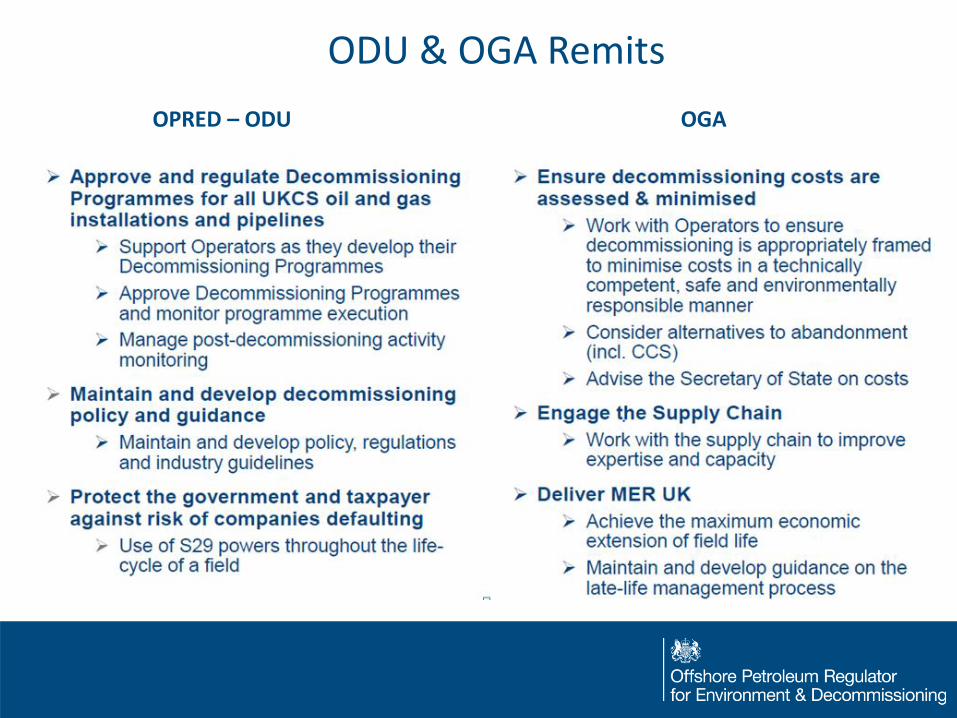

OPRED is responsible for:

• Developing, administering and enforcing the offshore oil and gas environmental regime

(including offshore gas unloading and storage and carbon dioxide storage). • handling domestic and international policy relating to developing the environmental

regulatory framework for offshore oil and gas. • the Department’s Strategic Environmental Assessment for offshore energy projects, which

allows the Oil & Gas Authority (OGA) to conduct offshore licensing rounds and facilitates offshore renewable energy developments.

• the oil and gas decommissioning regime and ensuring that the liability for such activity stays with the oil companies and does not transfer to the Department (total estimated cost currently sitting at £59 billion).

470 Installations - 58 Licensed Operators

• 10% floating

• 30% subsea

• 50% small steel

• 10% large steel or concrete – potential derogations for abandonment

Approximately 35,000 km pipelines

• 10,000 km major pipelines

What infrastructure is in the UKCS

Internationally, the UK has a number of obligations concerning the decommissioning of offshore installations.

Geneva Convention 1958 1958 Geneva Convention on the Continental Shelf. which determined that “any installations which are abandoned or disused must be entirely removed”. Convention on the Prevention of Marine Pollution by Dumping of Wastes and Other Matter 1972 The "London Convention" for short, is one of the first global conventions to protect the marine environment from human activities and has been in force since 1975. In 1996, the "London Protocol" was agreed to further modernize the Convention and, eventually, replace it. Under the Protocol all dumping is prohibited United Nations Convention on the Law of the Sea United Nations Convention on the Law of the Sea (UNCLOS) ratified by the UK in 1997. - Any installations or structures which are abandoned or disused shall be removed to ensure safety of navigation. UNCLOS(1982)

International Rules

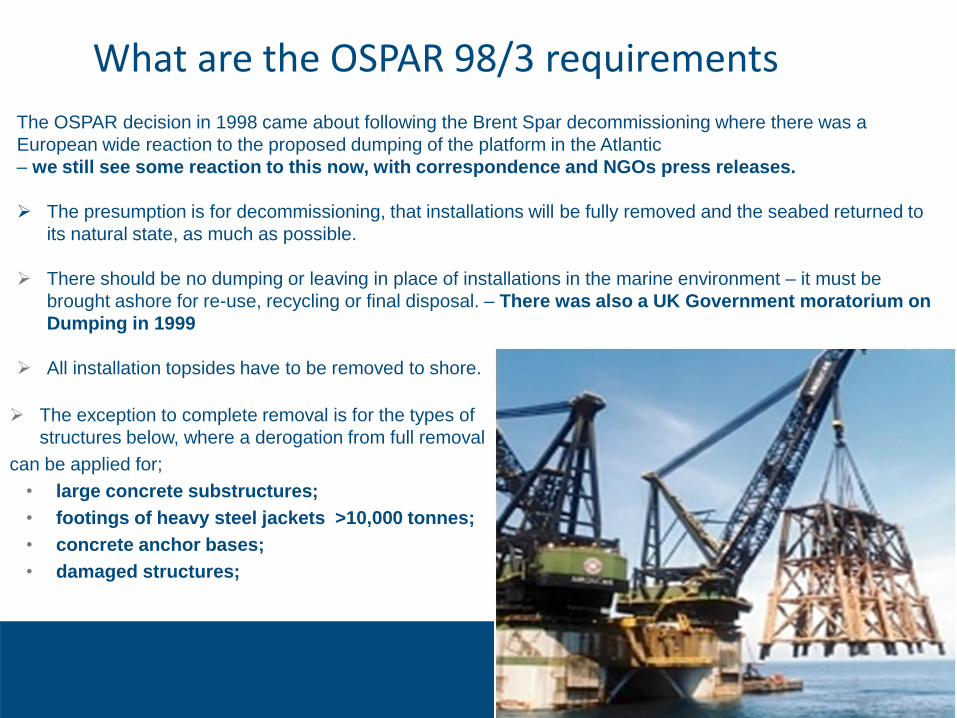

The OSPAR decision in 1998 came about following the Brent Spar decommissioning where there was a

European wide reaction to the proposed dumping of the platform in the Atlantic

– we still see some reaction to this now, with correspondence and NGOs press releases.

The presumption is for decommissioning, that installations will be fully removed and the seabed returned to

its natural state, as much as possible.

There should be no dumping or leaving in place of installations in the marine environment – it must be

brought ashore for re-use, recycling or final disposal. – There was also a UK Government moratorium on

Dumping in 1999

All installation topsides have to be removed to shore.

The exception to complete removal is for the types of

structures below, where a derogation from full removal

can be applied for;

• large concrete substructures;

• footings of heavy steel jackets >10,000 tonnes;

• concrete anchor bases;

• damaged structures;

What are the OSPAR 98/3 requirements

What does OSPAR cover?

GBS - 8

Platform name Jacket Weight Topside weight

Beryl A 200,000 32,500

Brent B 165,664 23,424– in consultation

Brent C 287,542 29,846– in consultation

Brent D 177,809 23,125 – now removed

Cormorant A 294,655 25,600

Dunlin A 228,611 19,350 – under discussion

Ninian Central 384,000 39,000

Ravenspurn 38,500 62,250

Heavy Steel jackets - 31

Platform name Jacket Weight Topside Weight

Britannia 20,000 18,500

Cormorant North 20,052 15,290

Magnus 37,057 34,600

Murchison 44,300 24,000 – in execution

Piper B 22,555 28,000

Tern 20,500 19,300

Thistle A 31,500 25,200

Alba Northern 17,000 25,534

Alwyn North NAA 18,500 21,400

Alwyn North NAB 14,500 15,000

Beryl B 13,250 21,800

Brae A 18,600 38,000– in consultation

Brae B 18,900 42,000– in consultation

Brent A 14,225 15,998– in consultation

Claymore A (CPP) 17,000 18,000

Clyde 10,400 17,900

Eider 17,100 11,200

Forties FA 12,310 10,551

Forties FB 14,152 10,551

Forties FC 14,152 10,551

Forties FD 14,152 10,551

Fulmar 12,400 24,000

Heather A 18,700 12,200

Miller 14,830 28,600 – Programme approved but platform not yet removed

Morecambe South CPP1 11,754 12,933

Ninian Northern 31,500 17,400 - In consultation

Ninian Southern 43,700 25,500

Saltire A 15,000 14,744

Scott JD 16,130 20,839

Tartan A 14,090 14,400

Tiffany 17,500 20,000

OSPAR Derogation candidates • 9 – Gravity based concrete structures in total, 8 remaining ( MCP 01 having been

decommissioned and the concrete jacket remaining in situ) • 32 – Heavy steel jackets over 10,000 tonnes, 31 remaining, (with North West Hutton

already removed).

• Miller platform has been approved and is about to be removed in the next couple of years

• Murchison topside removed and the jacket about to be removed in the next year. • The Brent A, B, C and D jacket programmes are up for consultation at the moment and

likely to go to OSPAR derogation consultation in late 2017, early 2018. • Brent Delta topside already approved and removed to shore for dismantlement. • Ninian North finished UK consultation and is about to go to OSPAR derogation in late

2017, early 2018 • Brae Alpha and Bravo, and up for consultation with Derogation consultation likely 2018. • Dunlin field Decommissioning programme currently in discussion and likely to go to UK

consultation in 2018.

What we ask operators to do:

• The Process and expectations are explained in published guidance – being updated to reflect learning and experience.

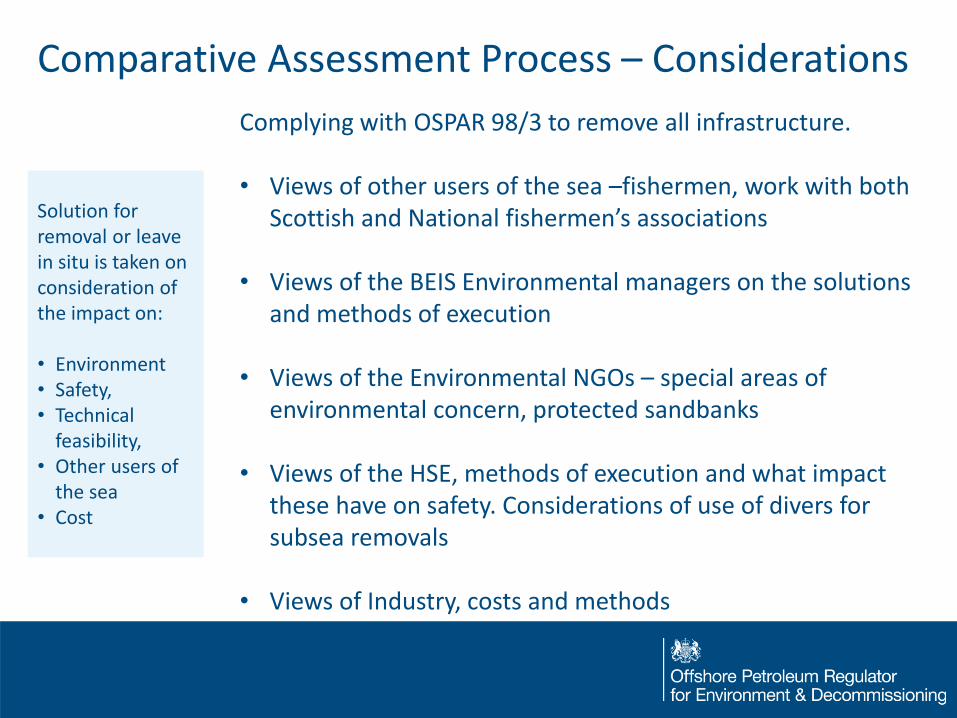

• We use a comparative assessment process to consider options using a set of criteria (safety, environment, technical feasibility, other users of the sea and economics) to determine the decommissioning solution, in respect of potential OSPAR derogation candidates

• Pipelines, many pipelines can be safely removed and but some are trenched at the time of installation and these are likely to remain.

• We also use the robust comparative assessment process detailed in OSPAR to consider how any Pipelines or related stabilisation features will be decommissioned

• Subsea infrastructure can be complex to remove and decisions consider the level of fishing activity, condition and burial as well as environmental conditions

Decommissioning in practice

Solution for removal or leave in situ is taken on consideration of the impact on: • Environment • Safety, • Technical

feasibility, • Other users of

the sea • Cost

Complying with OSPAR 98/3 to remove all infrastructure.

• Views of other users of the sea –fishermen, work with both Scottish and National fishermen’s associations

• Views of the BEIS Environmental managers on the solutions and methods of execution

• Views of the Environmental NGOs – special areas of environmental concern, protected sandbanks

• Views of the HSE, methods of execution and what impact

these have on safety. Considerations of use of divers for subsea removals

• Views of Industry, costs and methods

Comparative Assessment Process – Considerations

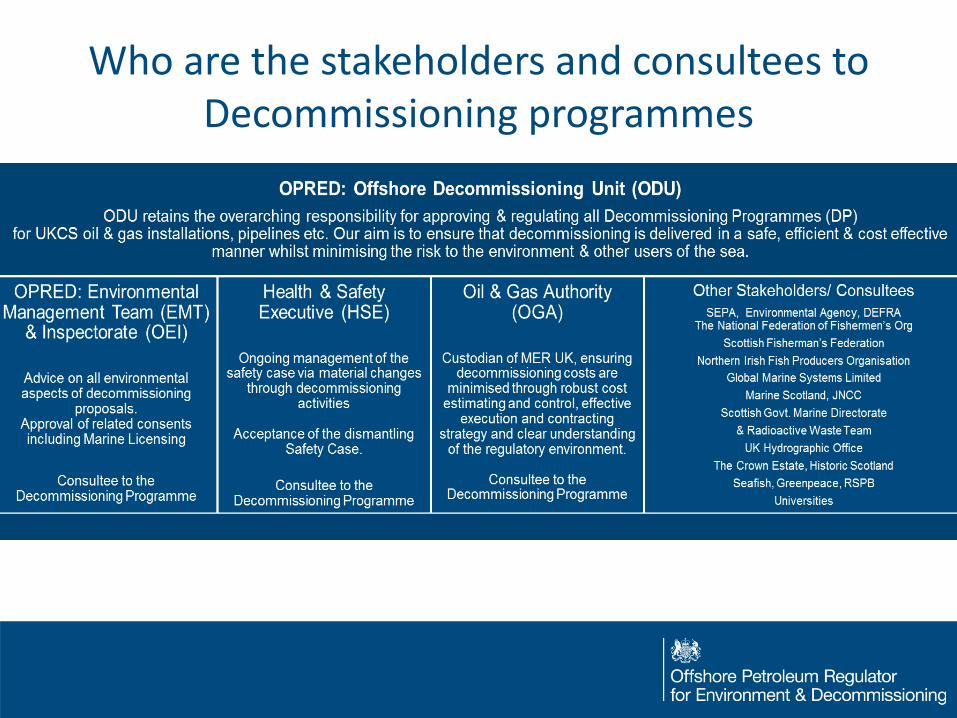

Who are the stakeholders and consultees to Decommissioning programmes

• It enacts the powers of the Oil and Gas Authority, and Imposes certain duties in regards to

decommissioning cost efficiency.

• In regard to BEIS, It places a duty on the Secretary of state to consult with the Oil and Gas

authority who will provide them with an assessment of arrangements in the decommissioning

programme to:

Ensure the programme is framed by means of timing of the measures or the inclusion of a

provision for collaboration that the cost of carrying it out is kept to the minimum that is

reasonably practicable in the circumstances

And consider alternatives to abandoning or decommissioning the installation or pipeline,

such as re-using or preserving it.

• As part of their preparation of the decommissioning programme there is a duty on operators to

consult the OGA and they must frame the programme so as to ensure (whether by timing of the

measures proposed, the inclusion of provision for collaboration, or otherwise) that the cost of

carrying the programme out is kept to the minimum that is reasonably practicable in the

circumstances.

Energy Bill 2016

ODU & OGA Remits

OPRED – ODU OGA

How is cost considered?

• Cost is a key consideration, but not the only or main one

• OGA provide us with a view on costs as a consultee

• Decommissioning in situ may not be the “cheapest” solution in all cases - e.g. Camelot field

Liability and risk assessment

• Operators decision’s on decommissioning are influenced by their appetite for risk

• Liability in perpetuity and the need for ongoing monitoring have a cost.

• Liability is hard to quantify, we are at the early stages in regard to the integrity of anything that has remained in situ or on P & Ad Wells.

Decommissioning in practice (1)

Liability for decommissioning rests with industry

• Principle of “polluter pays”

• Wide ranging regulatory powers to serve legal notices on those who have benefitted from the production of hydrocarbons – Petroleum Act 1998

• Potential to serve, withdraw and serve S34 notices to ensure that industry takes responsibility for decommissioning. Action must be proportionate – s29 and s34 of 1998 Act

• S29 and S34 are key tools in our financial risk mitigation processes

OSPAR principles underpin the decommissioning process

• Policy starting point is the expectation that operators will aim to restore the sea bed, described as a “clear sea bed”

Decommissioning in practice (2)

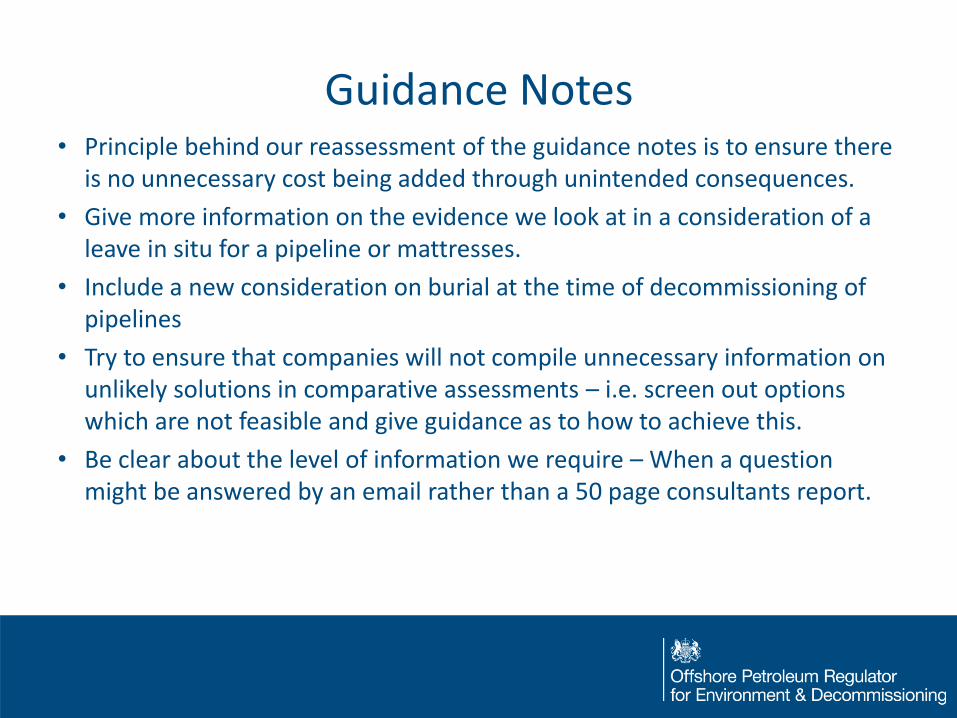

Guidance Notes • Principle behind our reassessment of the guidance notes is to ensure there

is no unnecessary cost being added through unintended consequences.

• Give more information on the evidence we look at in a consideration of a leave in situ for a pipeline or mattresses.

• Include a new consideration on burial at the time of decommissioning of pipelines

• Try to ensure that companies will not compile unnecessary information on unlikely solutions in comparative assessments – i.e. screen out options which are not feasible and give guidance as to how to achieve this.

• Be clear about the level of information we require – When a question might be answered by an email rather than a 50 page consultants report.

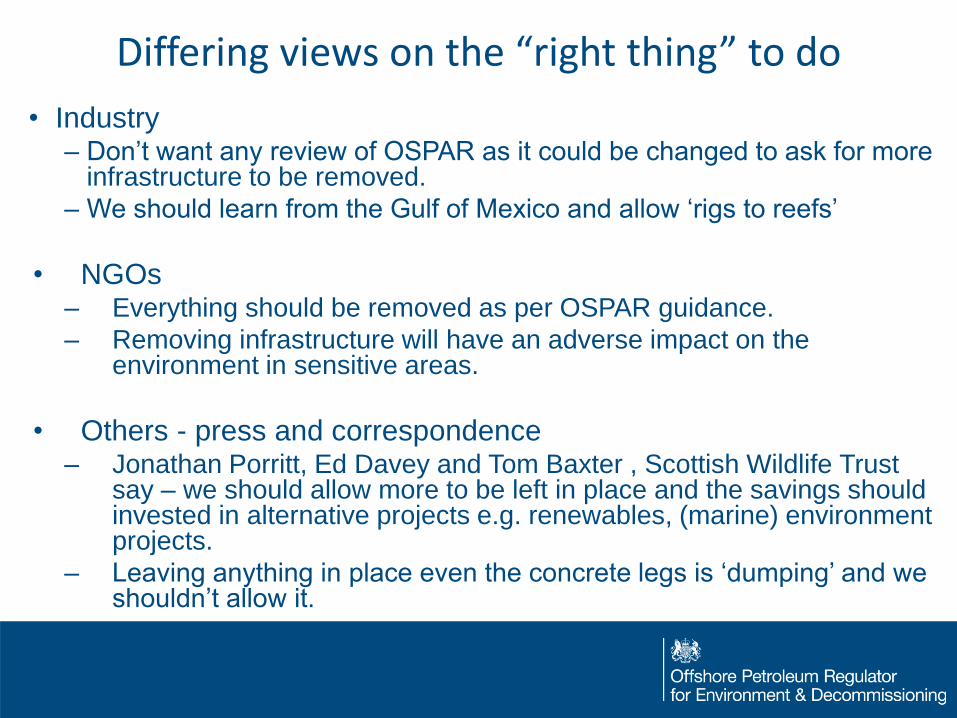

• Industry – Don’t want any review of OSPAR as it could be changed to ask for more

infrastructure to be removed.

– We should learn from the Gulf of Mexico and allow ‘rigs to reefs’

• NGOs – Everything should be removed as per OSPAR guidance.

– Removing infrastructure will have an adverse impact on the environment in sensitive areas.

• Others - press and correspondence – Jonathan Porritt, Ed Davey and Tom Baxter , Scottish Wildlife Trust

say – we should allow more to be left in place and the savings should invested in alternative projects e.g. renewables, (marine) environment projects.

– Leaving anything in place even the concrete legs is ‘dumping’ and we shouldn’t allow it.

Differing views on the “right thing” to do

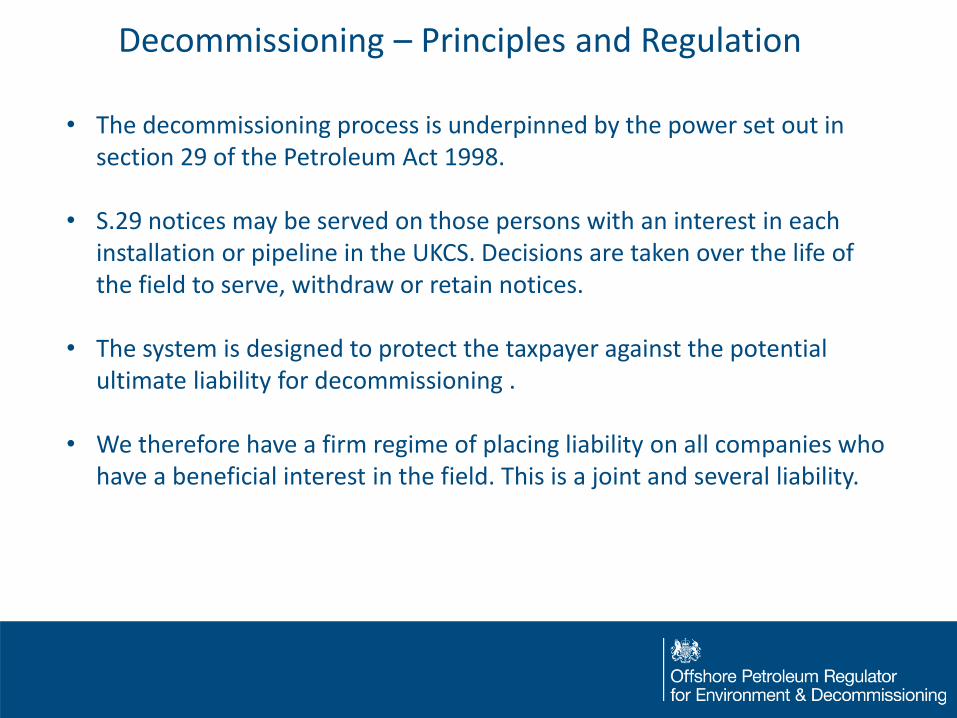

• The decommissioning process is underpinned by the power set out in section 29 of the Petroleum Act 1998.

• S.29 notices may be served on those persons with an interest in each

installation or pipeline in the UKCS. Decisions are taken over the life of the field to serve, withdraw or retain notices.

• The system is designed to protect the taxpayer against the potential

ultimate liability for decommissioning .

• We therefore have a firm regime of placing liability on all companies who have a beneficial interest in the field. This is a joint and several liability.

Decommissioning – Principles and Regulation

• Energy Act 2008 looked to enhance processes due to the increased participation by smaller companies which have fewer assets and as such bring increased risks that they might not be able to meet their decommissioning liabilities.

• Gave the Secretary of State power to require decommissioning security at any

time during the life of an oil or gas field if the risks to the taxpayer are assessed as unacceptable.

• Protecting the funds put aside for decommissioning, so in the event of insolvency of the relevant party, the funds remain available to pay for decommissioning and the taxpayers’ exposure is minimised.

Energy Act 2008

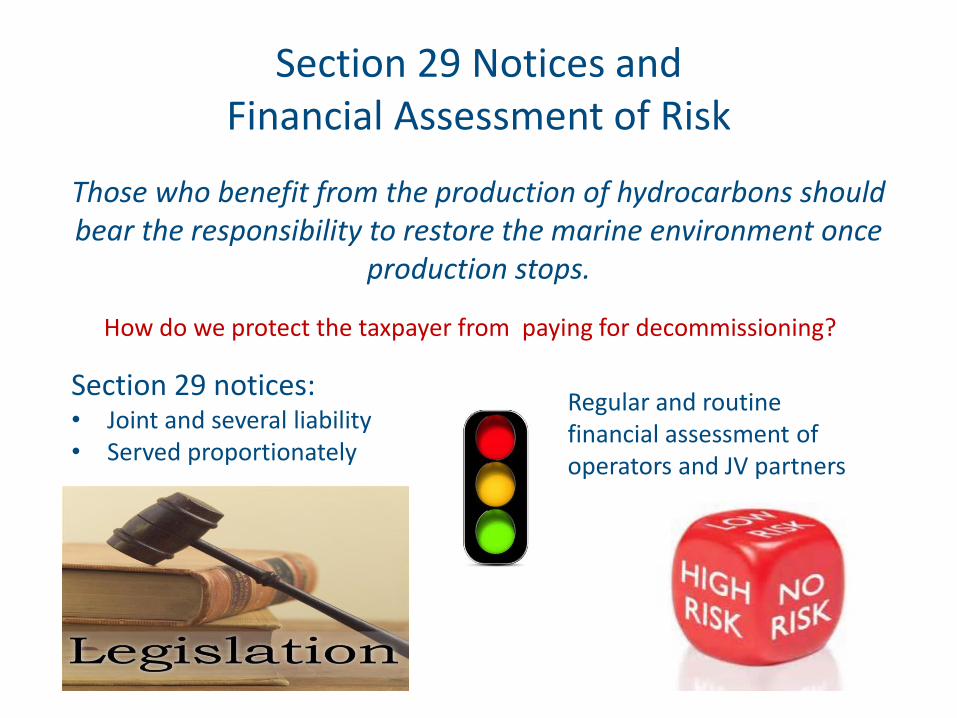

Section 29 Notices and Financial Assessment of Risk

Those who benefit from the production of hydrocarbons should bear the responsibility to restore the marine environment once

production stops.

How do we protect the taxpayer from paying for decommissioning?

Regular and routine financial assessment of operators and JV partners

Section 29 notices: • Joint and several liability • Served proportionately

Decommissioning – Financial Risk

• Key financial metric that has been used to assess risk and liability has been the company net worth as a comparison to their decommissioning liability.

• Key risk mitigation is that there are multiple bodies with a s29 notice on a field and liability is joint and several. Financial strength of all the s29 holders (even if they are no longer a current owner) informs the risk assessment of the field.

• Where risk is high we can request security is set aside to cover decommissioning liability (LOC or escrow). Statutory powers exist but we prefer to do this on a voluntary basis.

• The low oil price has increased the focus on decommissioning across Government, with the concern that HMG becomes responsible for decommissioning as a last resort.

• Our key role is to protect the taxpayer from this risk of default

How do we assess risk?

For every field we:

• Examine the finances of current and previous owners

Where we see a risk we will:

• Assess the NPV (Net Present Value or profitability) of the field

And may,

• Explore the presence of commercial decommissioning security agreements – Has security been posted?

– Does the Decommissioning Security Agreement (DSA) protect the taxpayer (in the event of failure of all of the parties)?

And in some circumstances we may even:

• Request a DSA between the operator and the Secretary of State, with appropriate security.

What would happen if an

operator failed? Who can be called

upon to pay for decommissioning?

What are the risks for the taxpayer? What can we

do to mitigate the risks?

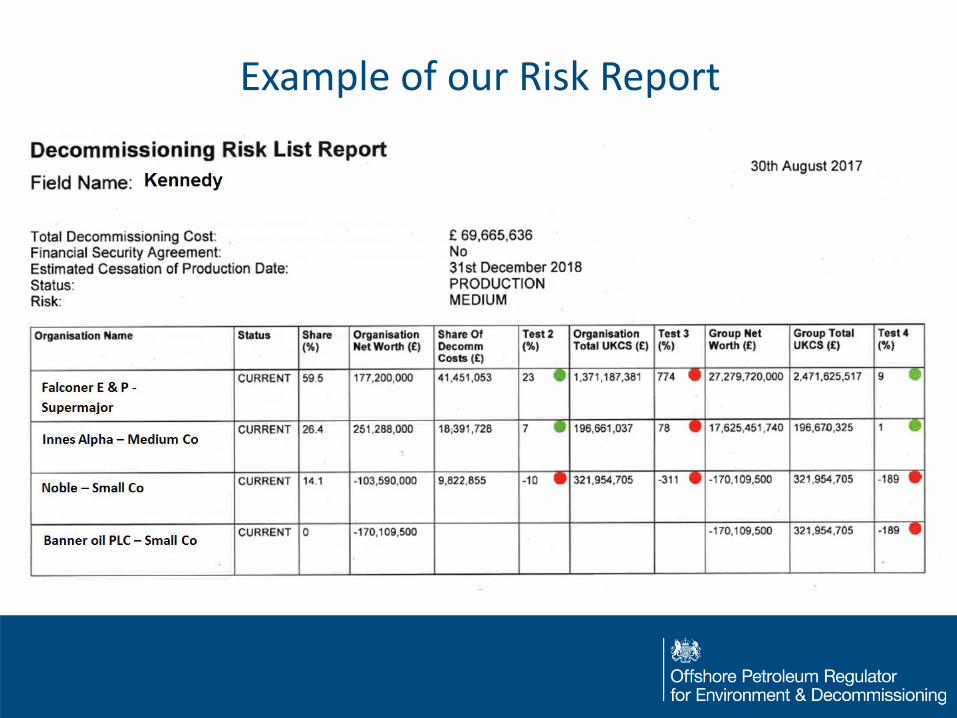

Example of our Risk Report

Decommissioning Security Agreements

• Decommissioning security agreement (previously called Financial security agreement) is a contract between the current and/or exited parties in a field to set aside security to cover the decommissioning costs in the field.

• BEIS has 8 instances where we are also signatories to these DSAs and security is posted, usually in the form of a letter of credit, held by the law debenture trust.

• A DSA should have a clause which protects these funds in the event of the company going into administration and ensures they can only be used for decommissioning.

• There are industry standard guidelines for DSAs however in practice the individual field DSAs are complex and negotiation on them is lengthy

Decommissioning costs and potential HMG exposure

• Over the whole UKCS we undertook an assessment of where we the risk was mitigated by a Supermajor or by a medium sized company which was financially stable.

• This led us to understand that 77% of the basin was covered either as a current or as an exited party by a supermajor.

• Following the estimate down to more risky companies with no larger companies to give comfort we have a top down assessment the risk of liability falling to HMG

Enhanced Financial Assessment

• Horizon Scanning: work with OGA, BEIS Commercial and UK Government Investments to identify companies at risk

• Refined risk categorisation – eight categories of risk

• Highest risk = field with one owner of low financial standing and no other legal notice holders

• Low risk = supermajor involved as current or ‘exited’ party

• Reviewed portfolio of assets owned by ‘high risk’ companies to determine scale and likelihood of risk to HM Government

• Identified information gaps in relation to commercial decommissioning security arrangements

Enhanced Financial Assessment

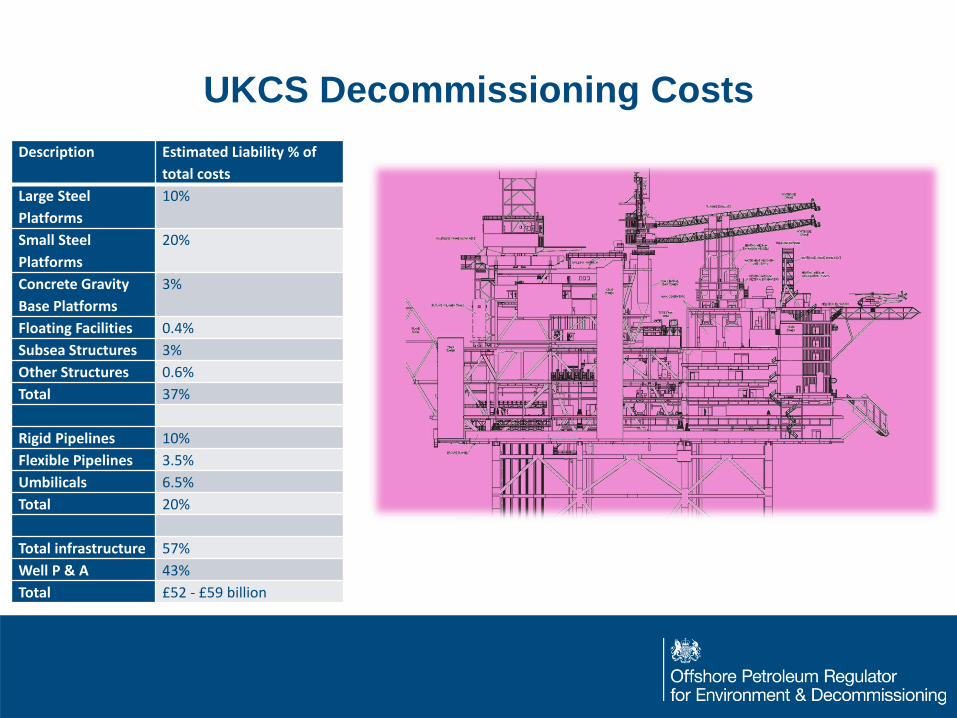

UKCS Decommissioning Costs

Description Estimated Liability % of

total costs

Large Steel

Platforms

10%

Small Steel

Platforms

20%

Concrete Gravity

Base Platforms

3%

Floating Facilities 0.4%

Subsea Structures 3%

Other Structures 0.6%

Total 37%

Rigid Pipelines 10%

Flexible Pipelines 3.5%

Umbilicals 6.5%

Total 20%

Total infrastructure 57%

Well P & A 43%

Total £52 - £59 billion

Decommissioning liability estimate of cost • Decommissioning liability cost estimation

– Inherently uncertain due to historical over runs and weather considerations, as well as differences in how industry come to their figure for each field.

– ODU method has been to use tonnage, estimated timings for removal etc translated into vessel costs per day and manhours per day, but with some determined positions on overruns and unpredictable delays.

– We consider each field/installation in the same way so any over/underestimates on unit costs are equal

– Use this method to have a cost per field broken down into the Work breakdown structure.

– Work breakdown structure looks at preparation, removal of modules, subsea removal etc.

– Estimate has a variance of around 50% +/-

• ODU liability estimate is £52billion

Decommissioning Cost • OGA’s remit is to ensure the costs of decommissioning are minimised and

provide advice to the SoS on how this will be achieved.

• They aim to achieve this by encouraging collaboration and by ensuring companies learn from others and implement learnings as part of their planning.

• OGA will benchmark companies on their decom costs, breaking down the individual parts of the work.

• ODU have supplied historical information on execution costs of decommissioning and are working closely on cost reduction.

• ODU are also working closely with the OGA and the OGA MER task force alongside the Treasury to provide confidence around a cost estimation.

• OGA cost estimate includes probability factors.

• OGA liability estimate is £59.7billion

Decommissioning costs

How can we have confidence in the liability estimate?

– We use other information to calibrate the estimate to ensure we have a

good understanding of the components which impact on the cost.

– Look at Operators estimates for individual fields against our estimate

– Look at estimated costs for fields against actual spend

– Look at each field individually in execution to see specifically where the cost overruns lie.

– Look at what has been learned to ensure our next estimate has these sensitivities included. We see all the programmes and can ask companies to share what they have found on P & A etc

Decommissioning Activity

• Large increase in Decommissioning activity.

• We see a substantial level of activity in the SNS as seen in the top graph.

• Level in the Northern North sea increasing in the 2020s

• Next 3 years appear to have the largest levels coming forward.

• We see programmes coming forward into execution around 2 years after Cessation of production.

Decommissioning Activity

• Decommissioning projects vary by size and complexity.

• Process starts 2-5 years before the project is approved.

• DP approval is a key milestone, but interest continues through execution, completion of work and post completion monitoring

• Activity levels are increasing. 24 projects with the potential to be approved this year, but only half this number anticipated.

• +20 projects in the pipeline in 2018

0

2

4

6

8

10

12

14

2010 2011 2012 2013 2014 2015 2016 2017(est)

Decommissioning Projects

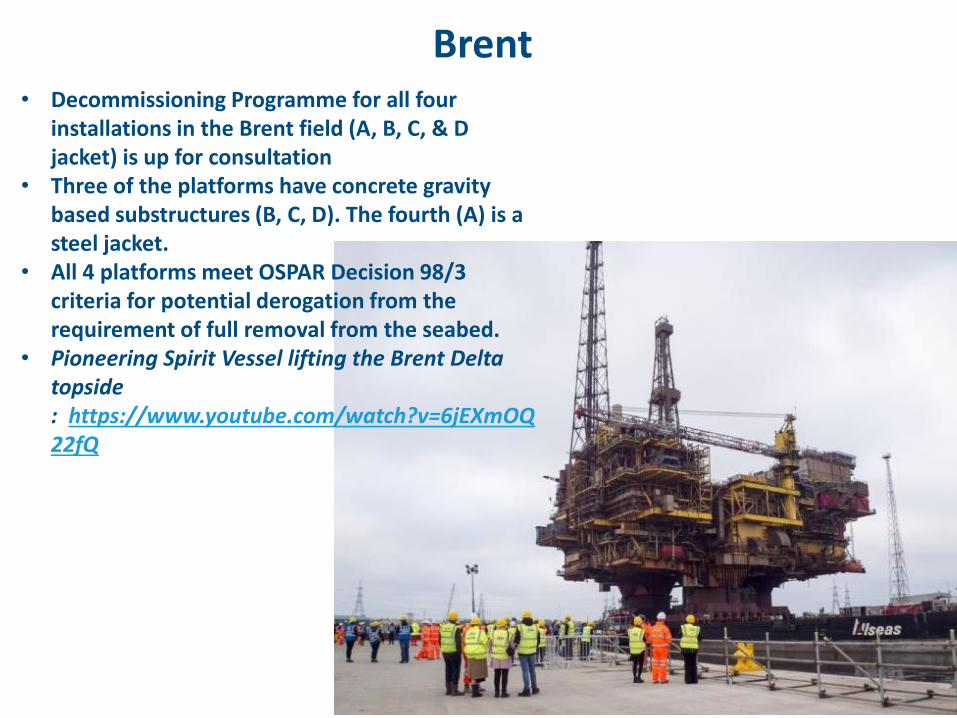

Brent • Decommissioning Programme for all four

installations in the Brent field (A, B, C, & D jacket) is up for consultation

• Three of the platforms have concrete gravity based substructures (B, C, D). The fourth (A) is a steel jacket.

• All 4 platforms meet OSPAR Decision 98/3 criteria for potential derogation from the requirement of full removal from the seabed.

• Pioneering Spirit Vessel lifting the Brent Delta topside : https://www.youtube.com/watch?v=6jEXmOQ22fQ

Brent - Largest decommissioning programme

“Legs up” Legs down” (-55m)

The proposal is to cut the concrete legs at the wave level and place navaids on the legs

This is the preferred option for the Scottish Fishermen’s association for navigation purposes. Shell also undertook some trials on how the legs could be cut and at the 95% of the cut phase found problems with stability of the concrete.

Thames – smaller decom programme

Footer text 35

Photo shows the first lift of a 500 tonne topside

Thames – small platforms but multifield Decommissioning programme

Footer text 36

• Thames consisted of 7 platforms and subsea tiebacks.

• Small platforms, of 500 tonnes.

• We are seeing more programmes with multiple fields coming forward, although these are small platforms there is a lot of complexity around the subsea infrastructure.

• The previous slide shows the first of the 5 mobilisations to dismantle one platform consisting of 4 modules.

• The whole Thames complex is being separated into 24 modules / lifts,

including the jackets. • These will be removed and go for onshore disposal to Vlissingen in the

Netherlands.