Embed Size (px)

Citation preview

ABB 08.03.07Sveinung Sletten, vice president external affairs, Petoro

Opportunities and challenges for the Norwegian Petroleum sector

• Petoro

• Opportunities and challengesfor the NCS

• Petoro’s strategy

• The Statoil-Hydro merger

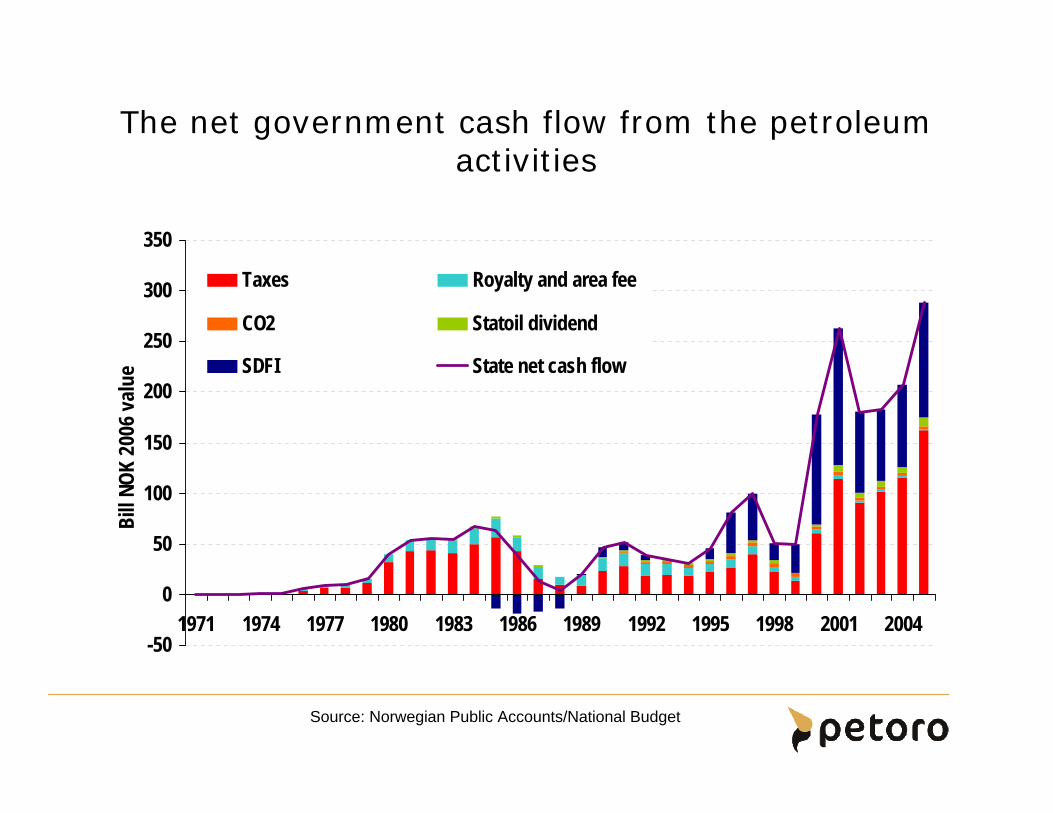

The net government cash flow from the petroleum activities

Source: Norwegian Public Accounts/National Budget

-50

0

50

100

150

200

250

300

350

1971 1974 1977 1980 1983 1986 1989 1992 1995 1998 2001 2004

Bill

NOK

2006

val

ue

Taxes Royalty and area fee

CO2 Statoil dividend

SDFI State net cash flow

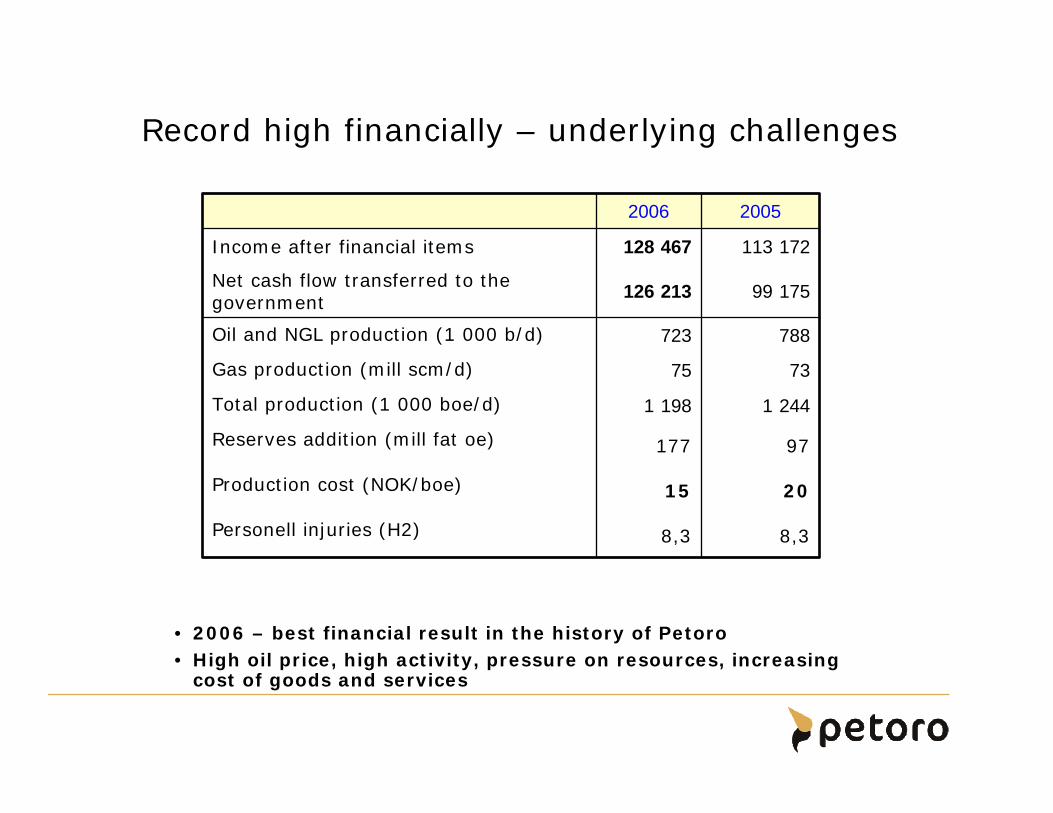

• 2006 – best financial result in the history of Petoro• High oil price, high activity, pressure on resources, increasing

cost of goods and services

Record high financially – underlying challenges

97177Reserves addition (mill fat oe)

2015Production cost (NOK/boe)

8,38,3Personell injuries (H2)

1 2441 198Total production (1 000 boe/d)

7375Gas production (mill scm/d)

788723Oil and NGL production (1 000 b/d)

99 175126 213Net cash flow transferred to the government

113 172128 467Income after financial items

20052006

12

6

19

24

256

6 2 °

6 0 °

5 8 °

T rondheim

Kristiansund

Ber genOslo

Stavanger

Harstad

5

5

1 23

4

1110987

15 16 17 18

26 27

32

31

29

3433 35

62026203

62046205

36

70 °

1 4 °

1 2 °

1 0 °

8 °

20 °22 °

2 4 °2 6 °

28 °30 °

18 °16 °

32 °

72 °

74 °

71207122

6 7 °

6 5 °

6 °

4 °2 °

TampenTampen

OsebergOseberg

TrollTroll

Norwegian SeaNorwegian Sea

Barents SeaBarents Sea

Southernmost NCSSouthernmost NCS

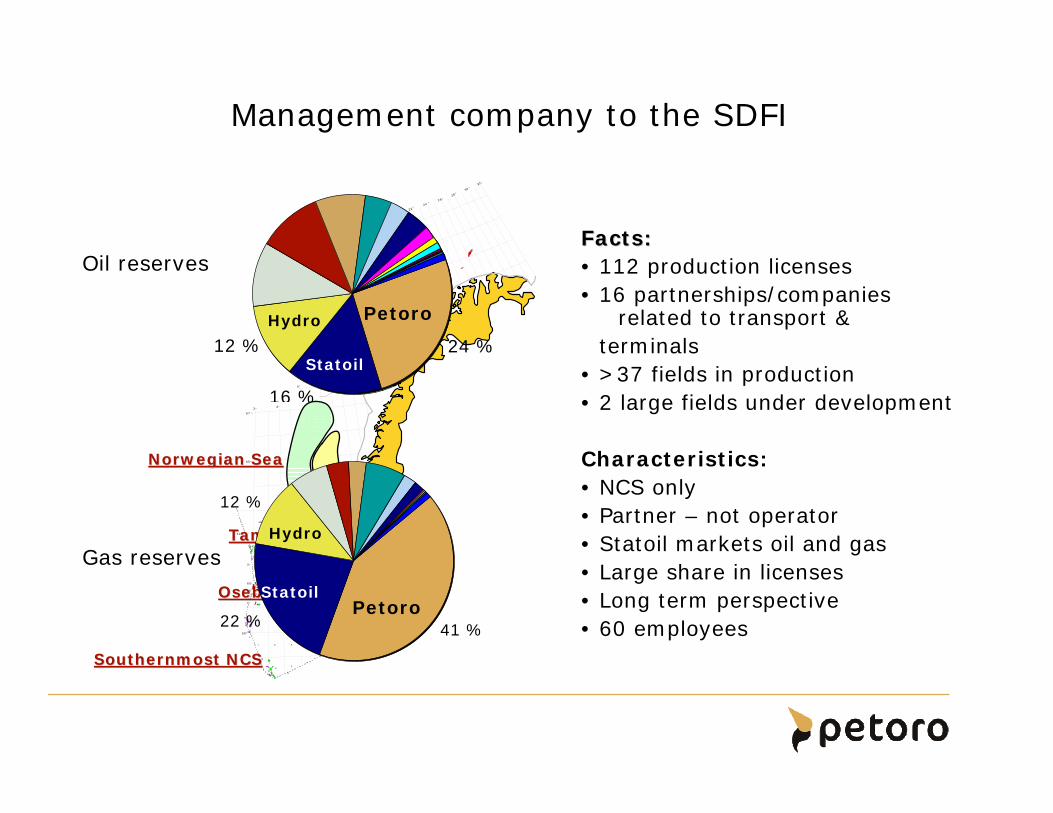

Management company to the SDFI

Facts:Facts:• 112 production licenses• 16 partnerships/companies

related to transport &terminals

• >37 fields in production• 2 large fields under development

Characteristics:• NCS only• Partner – not operator• Statoil markets oil and gas• Large share in licenses• Long term perspective• 60 employees

24 %

16 %

12 %

41 %22 %

12 %

Oil reserves

Gas reserves

PetoroStatoil

Hydro

PetoroHydro

Statoil

Opportunities and challenges

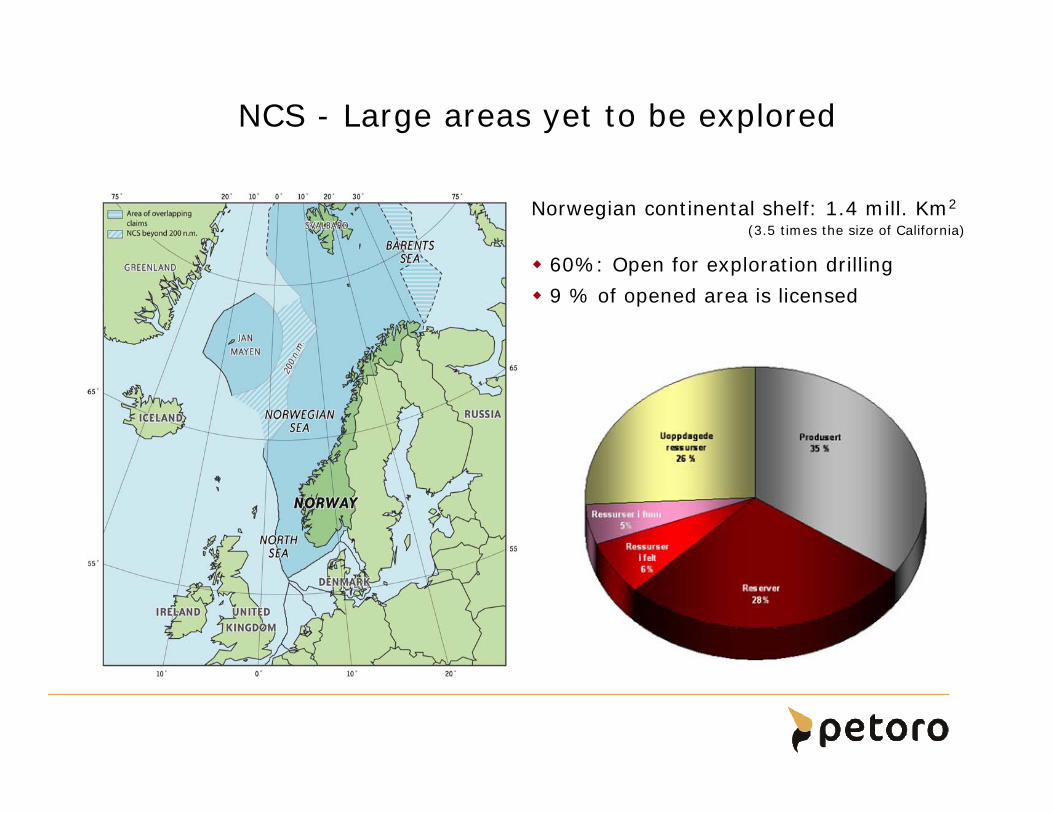

NCS - Large areas yet to be explored

Norwegian continental shelf: 1.4 mill. Km2

(3.5 times the size of California)

60%: Open for exploration drilling

9 % of opened area is licensed

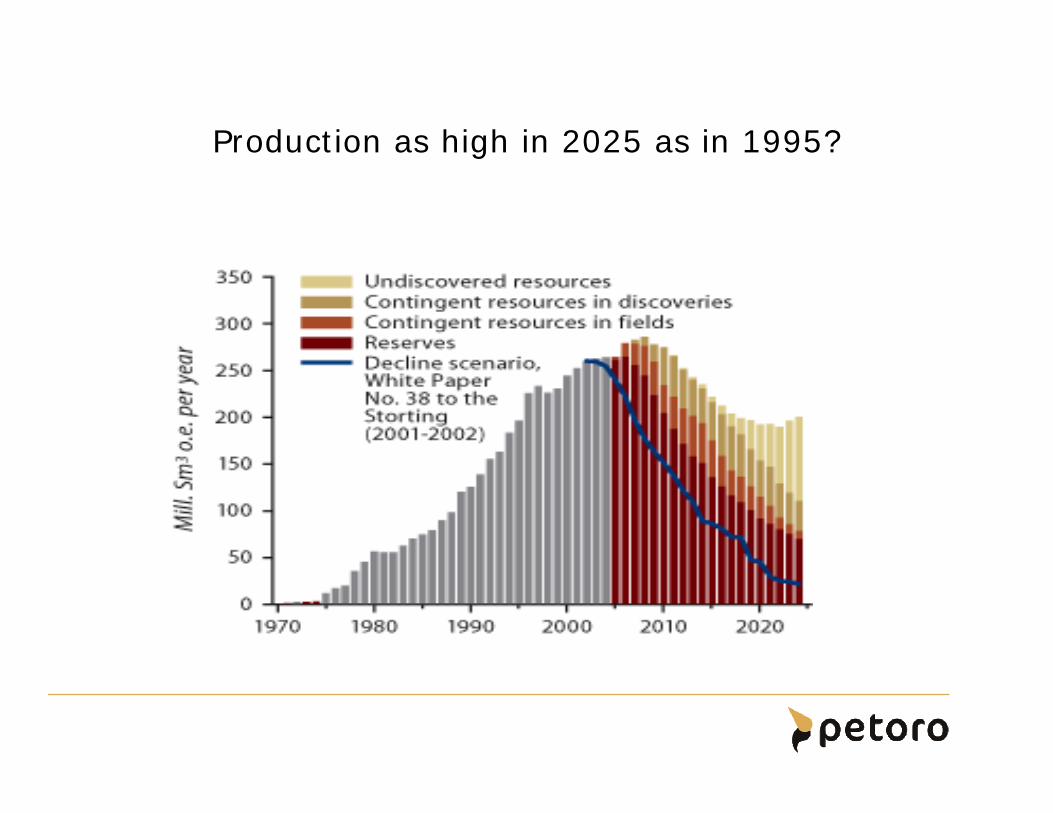

Production as high in 2025 as in 1995?

Source: NPD/MPE

Production level hinges on major fields

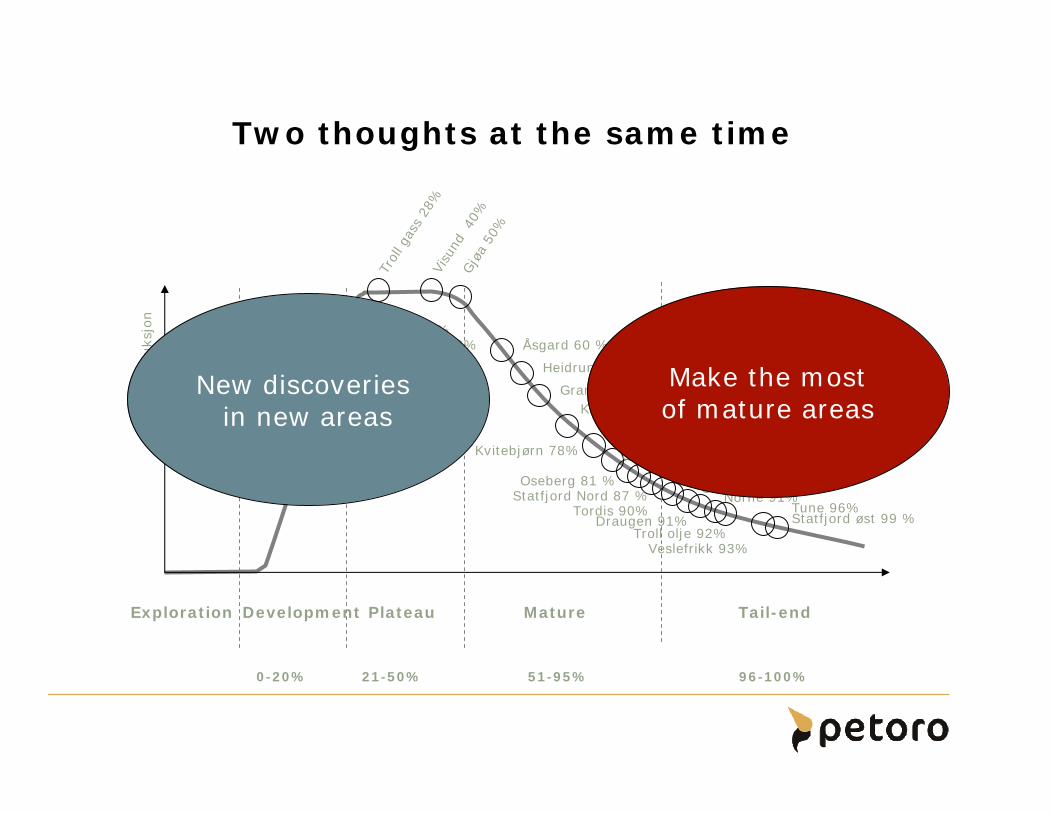

Two thoughts at the same timePr

oduks

jon

Exploration Development Plateau Mature Tail-end

0-20% 21-50% 51-95% 96-100%

Trol

l gas

s 28

%Vi

sund

40%

Gjø

a 50

%Statfjord Nord 87 %

Heidrun 64 %

Kristin 72%

Ormen Lange 13%Snøhvit 16 %

Åsgard 60 %

Statfjord øst 99 %

Oseberg 81 %

Tune 96%

Ekofisk 88%Gullfaks 89%

Grane 68 %

Kvitebjørn 78% Snorre 80%Vigdis 83%

Tordis 90%Draugen 91%

Norne 91%

Troll olje 92%Veslefrikk 93%

New discoveriesin new areas

Make the mostof mature areas

Trend: production decline, cost rise

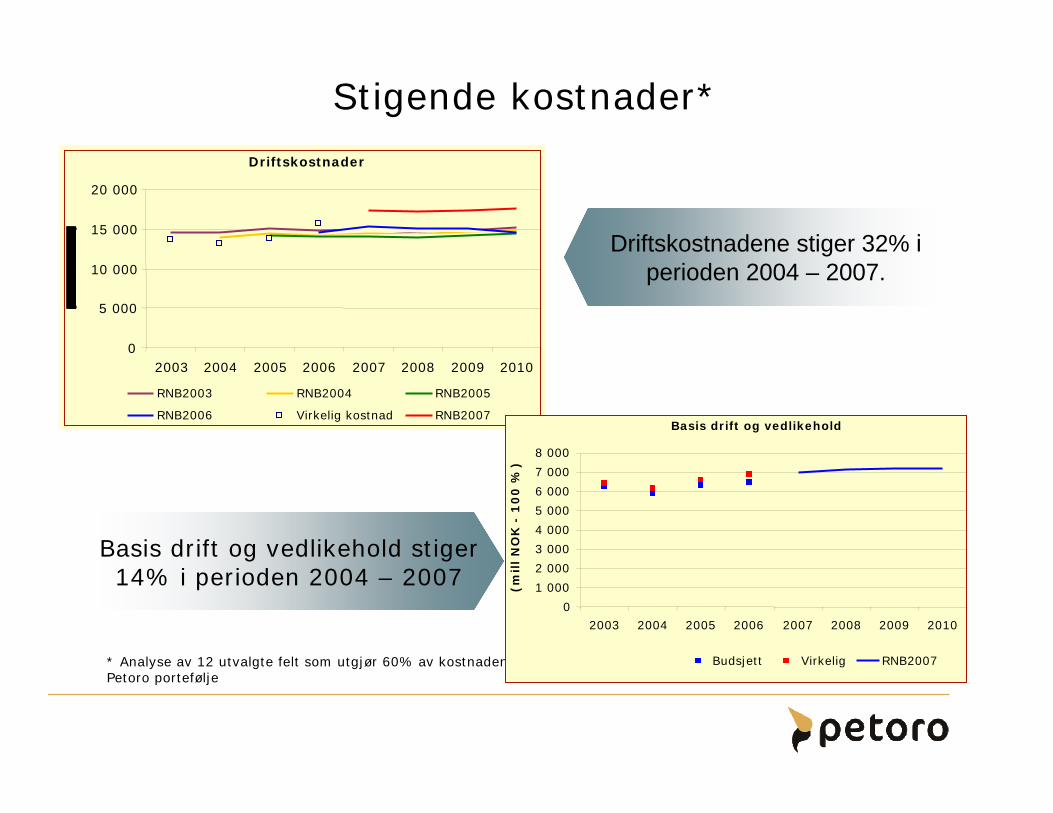

Stigende kostnader*

Driftskostnadene stiger 32% i perioden 2004 – 2007.

Basis drift og vedlikehold stiger 14% i perioden 2004 – 2007

* Analyse av 12 utvalgte felt som utgjør 60% av kostnadene i Petoro portefølje

Driftskostnader

0

5 000

10 000

15 000

20 000

2003 2004 2005 2006 2007 2008 2009 2010

RNB2003 RNB2004 RNB2005

RNB2006 Virkelig kostnad RNB2007Basis drift og vedlikehold

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

8 000

2003 2004 2005 2006 2007 2008 2009 2010

(mil

l N

OK

-1

00

%)

Budsjett Virkelig RNB2007

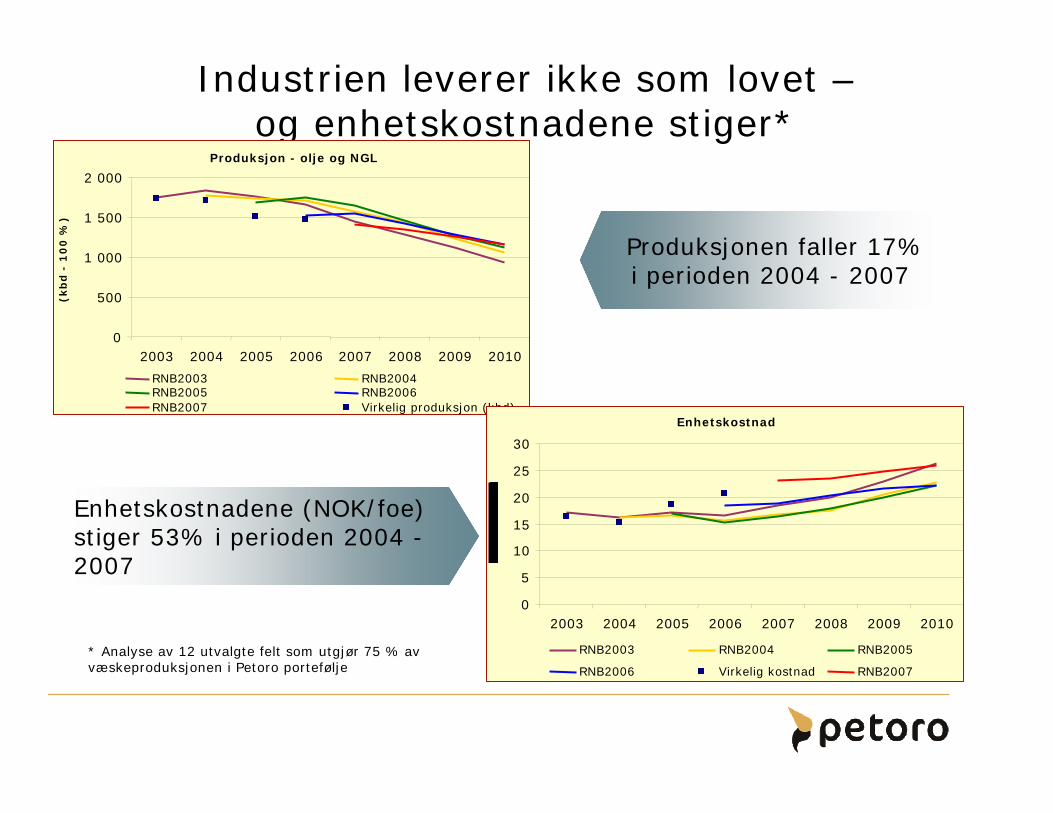

Industrien leverer ikke som lovet –og enhetskostnadene stiger*

Produksjonen faller 17% i perioden 2004 - 2007

Enhetskostnadene (NOK/foe) stiger 53% i perioden 2004 -2007

* Analyse av 12 utvalgte felt som utgjør 75 % av væskeproduksjonen i Petoro portefølje

Produksjon - olje og NGL

0

500

1 000

1 500

2 000

2003 2004 2005 2006 2007 2008 2009 2010

(kb

d-

10

0 %

)

RNB2003 RNB2004RNB2005 RNB2006RNB2007 Virkelig produksjon (kbd)

Enhetskostnad

0

5

10

15

20

25

30

2003 2004 2005 2006 2007 2008 2009 2010

RNB2003 RNB2004 RNB2005

RNB2006 Virkelig kostnad RNB2007

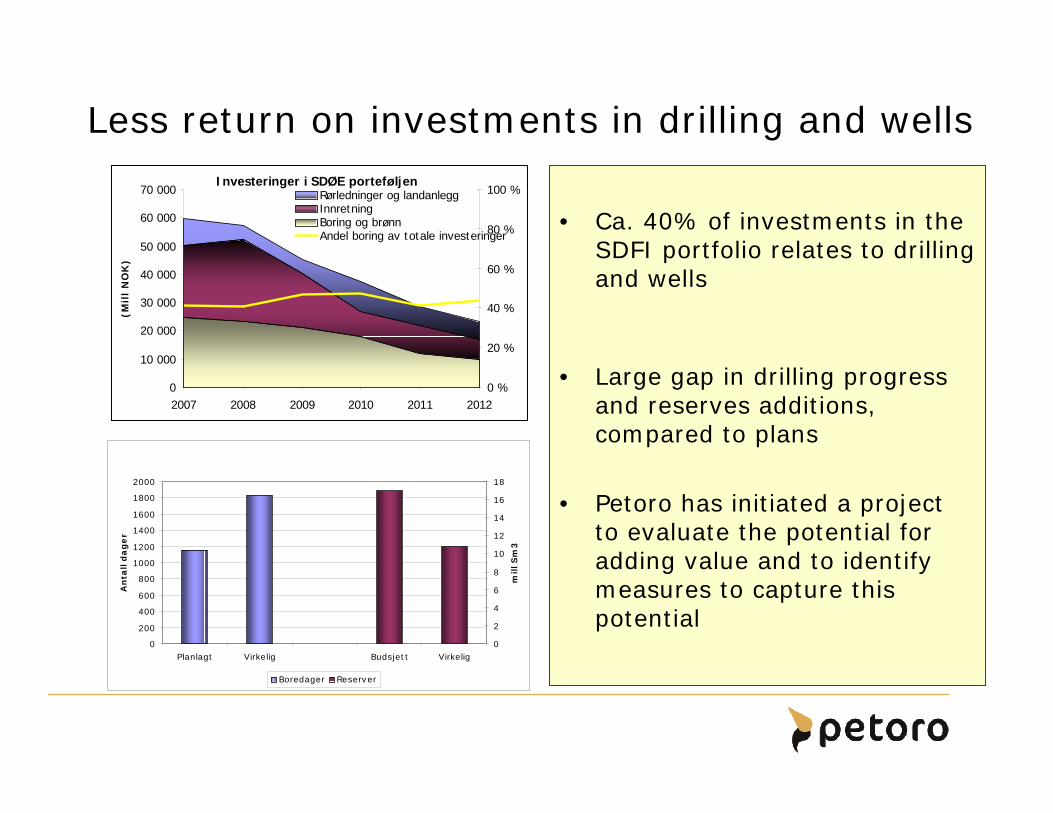

Less return on investments in drilling and wells

• Ca. 40% of investments in theSDFI portfolio relates to drilling and wells

• Large gap in drilling progress and reserves additions, compared to plans

• Petoro has initiated a projectto evaluate the potential for adding value and to identifymeasures to capture thispotential

Investeringer i SDØE porteføljen

0

10 000

20 000

30 000

40 000

50 000

60 000

70 000

2007 2008 2009 2010 2011 2012

(Mil

l N

OK

)

0 %

20 %

40 %

60 %

80 %

100 %Rørledninger og landanleggInnretningBoring og brønnAndel boring av totale investeringer

Oseberg

0

200

400

600

800

1000

1200

1400

1600

1800

2000

Planlagt Virkelig Budsjett Virkelig

An

tall d

ag

er

0

2

4

6

8

10

12

14

16

18

mill S

m3

Boredager Reserver

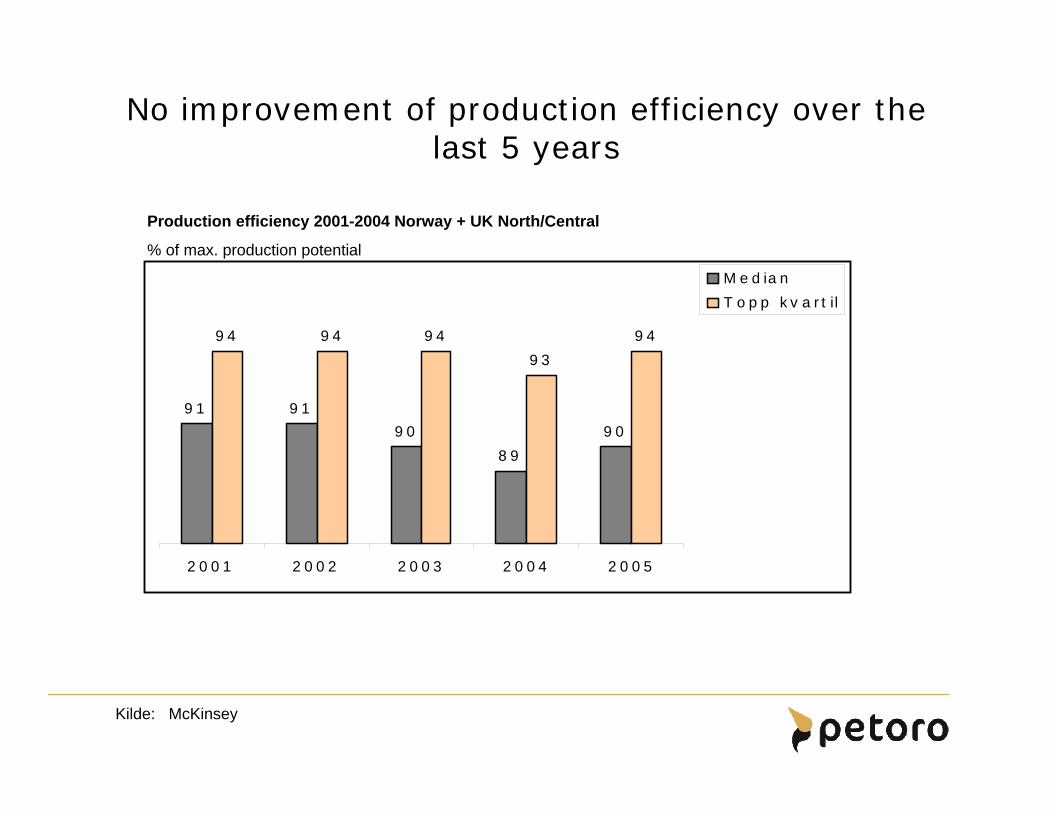

No improvement of production efficiency over thelast 5 years

Kilde: McKinsey

91 91

90

89

90

94 94 94

93

94

2001 2002 2003 2004 2005

M e d ia n

T o pp kv a rt il

Production efficiency 2001-2004 Norway + UK North/Central

% of max. production potential

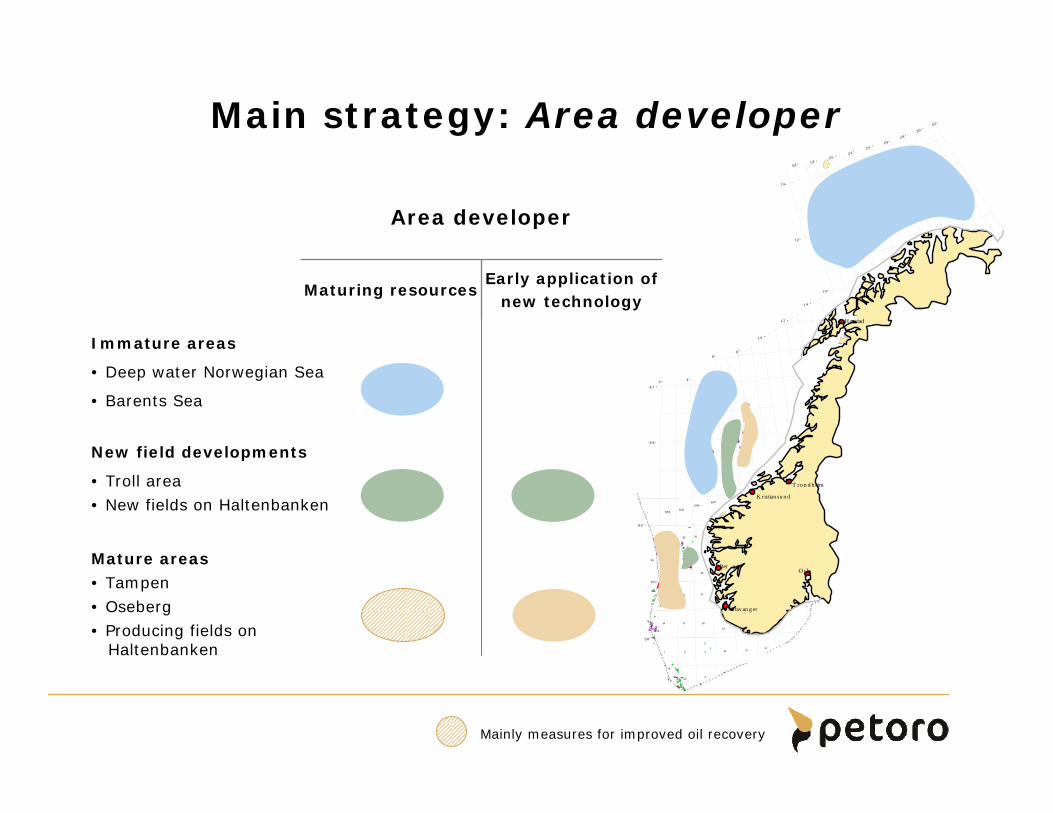

Petoro strategy: AREA DEVELOPER

MATURING RESERVES, EARLY APPLICATION OF TECHNOLOGY

Early application ofnew technology

Maturing resources

Area developer

Mature areas• Tampen • Oseberg• Producing fields on

Haltenbanken

New field developments

• Troll area• New fields on Haltenbanken

Immature areas

• Deep water Norwegian Sea

• Barents Sea

Main strategy: Area developer

12

6

19

24

256

6 2 °

6 0 °

5 8 °

T ro n d h eim

K ristian su n d

Ber g enOslo

Stav an g er

Harstad

5

5

1 23

4

1110987

15 16 17 18

26 27

32

31

29

3433 35

62026203

62046205

36

7 0 °

1 4 °

1 2 °

1 0 °

8 °

2 0 °2 2 °

2 4 °2 6 °

2 8 °30 °

1 8 °1 6 °

3 2 °

7 2 °

7 4 °

71207122

6 7 °

6 5 °

6 °

4 °2 °

Mainly measures for improved oil recovery

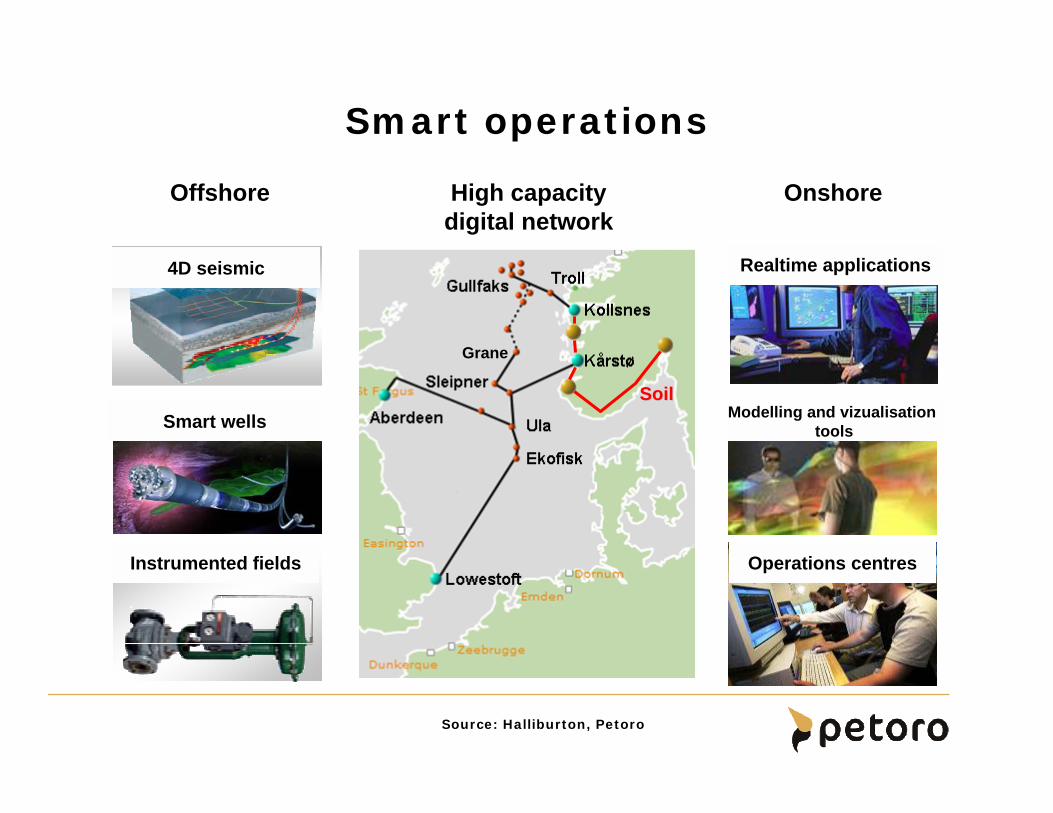

Smart operations

Offshore

4D seismic

Smart wells

Onshore

Operations centres

Modelling and vizualisation tools

Realtime applications

High capacitydigital network

SoilSoil

Grane

Instrumented fields

Source: Halliburton, Petoro

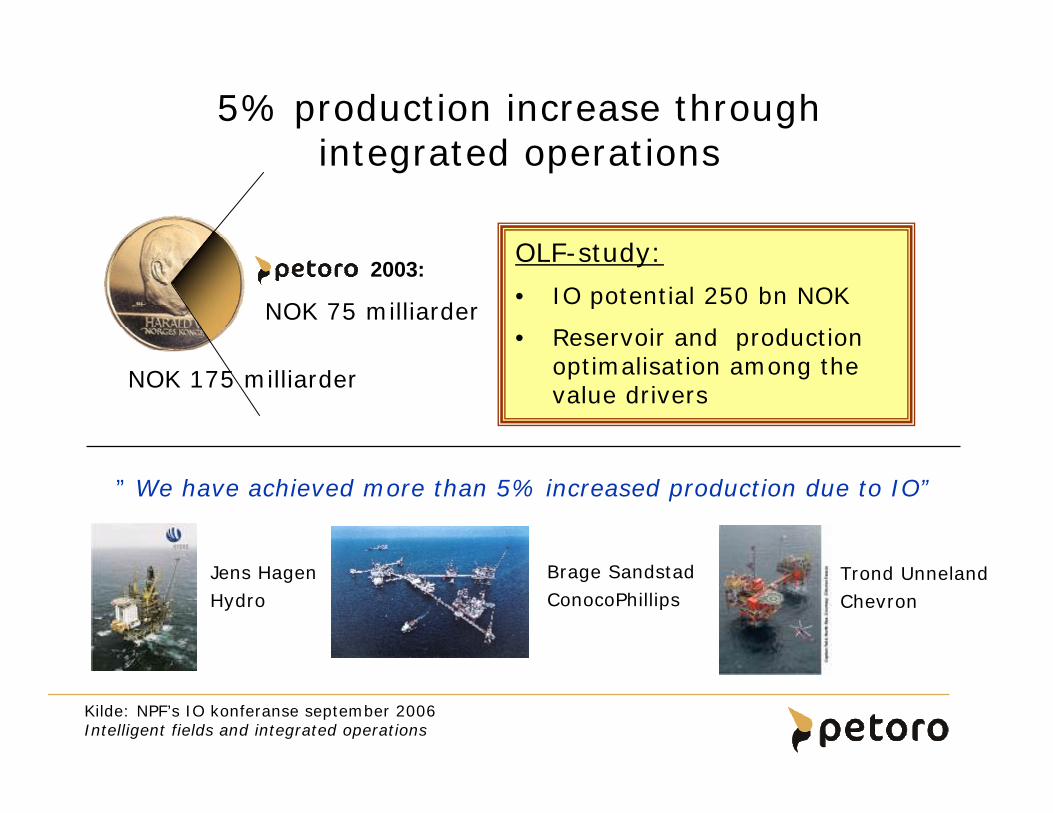

5% production increase throughintegrated operations

OLF-study:

• IO potential 250 bn NOK

• Reservoir and production optimalisation among the value drivers

Kilde: NPF’s IO konferanse september 2006Intelligent fields and integrated operations

” We have achieved more than 5% increased production due to IO”

Jens HagenHydro

Brage SandstadConocoPhillips

Trond UnnelandChevron

NOK 175 milliarder

NOK 75 milliarder

2003:

Statoil-Hydro merger

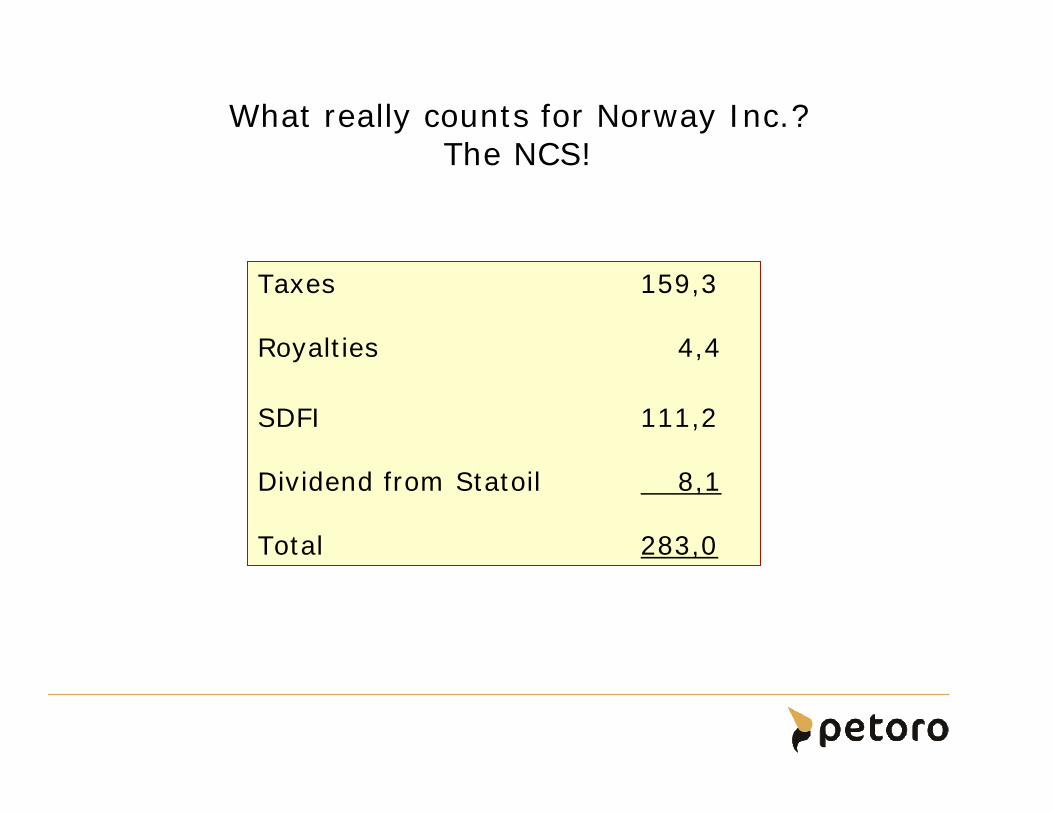

What really counts for Norway Inc.? The NCS!

Taxes 159,3

Royalties 4,4

SDFI 111,2

Dividend from Statoil 8,1

Total 283,0

12

6

19

24

256

62 °

60°

58°

Trondheim

Kristiansund

Ber genOslo

Stavanger

Harstad

5

5

1 23

4

1110987

15 16 17 18

26 27

32

31

29

3433 35

62026203

62046205

36

70°

14 °

12 °

10 °

8°

20 °22 °

24

18 °16°

72°

74°

71207122

67 °

65°

6°

4°2°

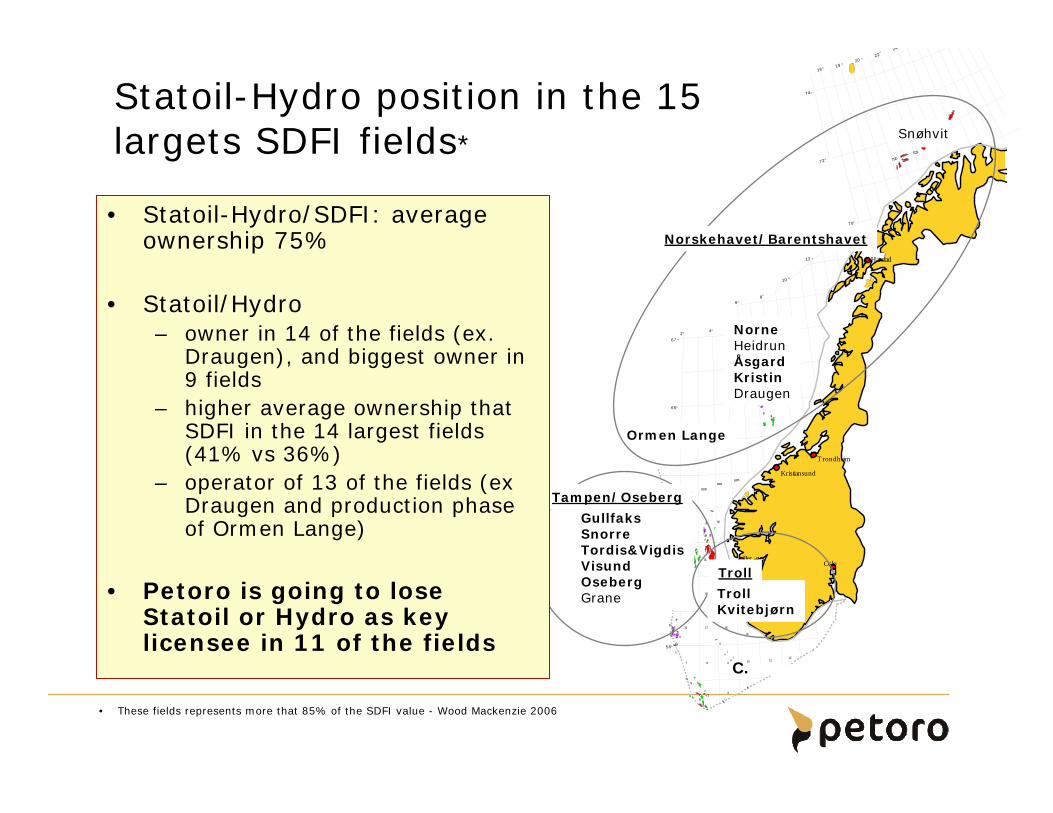

Statoil-Hydro position in the 15 largets SDFI fields* Snøhvit

C.

NorneHeidrunÅsgardKristinDraugen

GullfaksSnorreTordis&VigdisVisundOsebergGrane

Ormen Lange

Norskehavet/Barentshavet

TrollKvitebjørn

Tampen/Oseberg

Troll

• These fields represents more that 85% of the SDFI value - Wood Mackenzie 2006

• Statoil-Hydro/SDFI: averageownership 75%

• Statoil/Hydro– owner in 14 of the fields (ex.

Draugen), and biggest owner in 9 fields

– higher average ownership thatSDFI in the 14 largest fields(41% vs 36%)

– operator of 13 of the fields (ex Draugen and production phaseof Ormen Lange)

• Petoro is going to lose Statoil or Hydro as keylicensee in 11 of the fields

Future value creation on the NCS

• Statoil vs Hydro has produced strong solutions for the NCS

• Strong focus on NCS + best practices from abroad couldbenefit the NCS

• But reduced competition and diversity is a negative – gettingthe most out of a maturing NCS requires the efforts and results that diversity and competition can bring to the table

• The loss of S or H could to some degree be offset by strongerengagement by the mulitinationals - but will it happen?

• Management of SDFI at current levels requires a strengtheningof Petoro: – Primarily technical and commecial competence/capacity– Still partner – not a new operator– A limited budget for R&D could compensate for S-H dominance on

technology development

The best partner