Embed Size (px)

Citation preview

Canada | India | Netherlands | Singapore | UK | USA

▪ Supply chain disruption

▪ Lack of mobility of workforces

▪ Shortage of raw materials

▪ Lack of demand for non-essential products

▪ Liquidity crunch

▪ Consolidation of losses or significant reduction in revenues for certain industries

▪ Temporary relocation of business function to minimize the negative impact

Opening Remarks / Background

Canada | India | Netherlands | Singapore | UK | USA

Transfer Pricing Issues Arising out of COVID-19

▪ Impact on Limited Risk / Routine Entities (LRD/ LRM/ LRSP)

▪ Location / People Disruption Related Transfer Pricing Issues

▪ Revisiting / Renegotiating Intercompany Agreements

▪ Compensation for Royalty and Management Charges

▪ Intragroup Financing Arrangement

▪ Comparability Analysis and Transfer Pricing Documentation

▪ Future Controversies

▪ Advance Pricing Agreements (‘APA’) and Dispute Resolution

3

Canada | India | Netherlands | Singapore | UK | USA

IMPACT ON LIMITED RISK / ROUTINE ENTITIES (LRD/ LRM/ LRSP)

4

• What are your views on impact of COVID-19 on transfer pricing for routine entities such as low risk distributors, low risk contract manufacturers or even low risk service providers?

• Is there any possibilities for MNEs to lower the mark-up percentage or for that matter even change the transfer pricing methodology?

???

Canada | India | Netherlands | Singapore | UK | USA

Impact on Limited Risk / Routine Entities (LRD/ LRM/ LRSP)

▪ Impact of COVID-19 on routine entities

• Generally, limited risk entities are insulated from both the upside and downside impacts of majority ofbusiness risks

• Compensation for such entities are on a cost-plus mark-up basis under normal course of business

• Limited risk entities are not risk-free entities

• Reduced mark-up or zero mark-up or pass on losses- what is possible?

• Whether limited risk entities can ever incur losses?

o Para 1.129 of the OECD Guidelines – “Of course, associated enterprises, like independent enterprises, can sustaingenuine losses, whether due to heavy start-up costs, unfavourable economic conditions, inefficiencies, or otherlegitimate business reasons.”

o IRS FAQs on transfer pricing documentation - The documentation should thoroughly explain how the unforeseenbusiness circumstances experienced by the company caused the observed financial results and how the losseswere not caused by intercompany prices.

▪ Possibility of change in transfer pricing methodology:

• Change in method reflects the change in functional profile of the parties involved in the transactions

• Long term implications should not be ignored

Canada | India | Netherlands | Singapore | UK | USA

LOCATION / PEOPLE DISRUPTION RELATED TRANSFER PRICING ISSUES

6

• COVID-19 related travel restrictions / lockdowns have led to many employees being stranded in locations for time longer than envisaged. Do you foresee any Permanent Establishment implications that may arise? Also, what may be the potential transfer pricing implications of the same?

???

Canada | India | Netherlands | Singapore | UK | USA

▪ Permanent Establishment implications:

• Due to lockdown / travel restrictions, employees may be forced to perform services or habitually conclude a

contract in non-employment countries

• The extended stay may lead to permanent establishment and tax residency risks for employees and MNEs

• OECD’s paper on ‘Analysis of Tax Treaties and the Impact of the COVID-19’ –

o Due to force majeure and/ or Government directives, the employees are working in the other countries for

a temporary period

o The activities carried out are not in the nature of regular activities performed from that country

o The temporary change in location, where employment is exercised, should not create a new PE for the

employer

o The exceptional circumstances such as this, should not cause meaningful changes in the tax position under

a tax treaty, of employees’ residence and the taxation of employment income.

• In case Permanent establishment is newly created in any jurisdiction, transfer pricing will need to be

considered to determine profit attributable to that permanent establishment.

Location / People Disruption Related Transfer Pricing Issues

Canada | India | Netherlands | Singapore | UK | USA

REVISITING / RENEGOTIATING INTERCOMPANY AGREEMENTS

8

• COVID-19 has led business to relook at inter-company arrangements. What are the areas that multinational companies needs to take into consideration while revisiting / renegotiating intercompany agreements?

???

Canada | India | Netherlands | Singapore | UK | USA

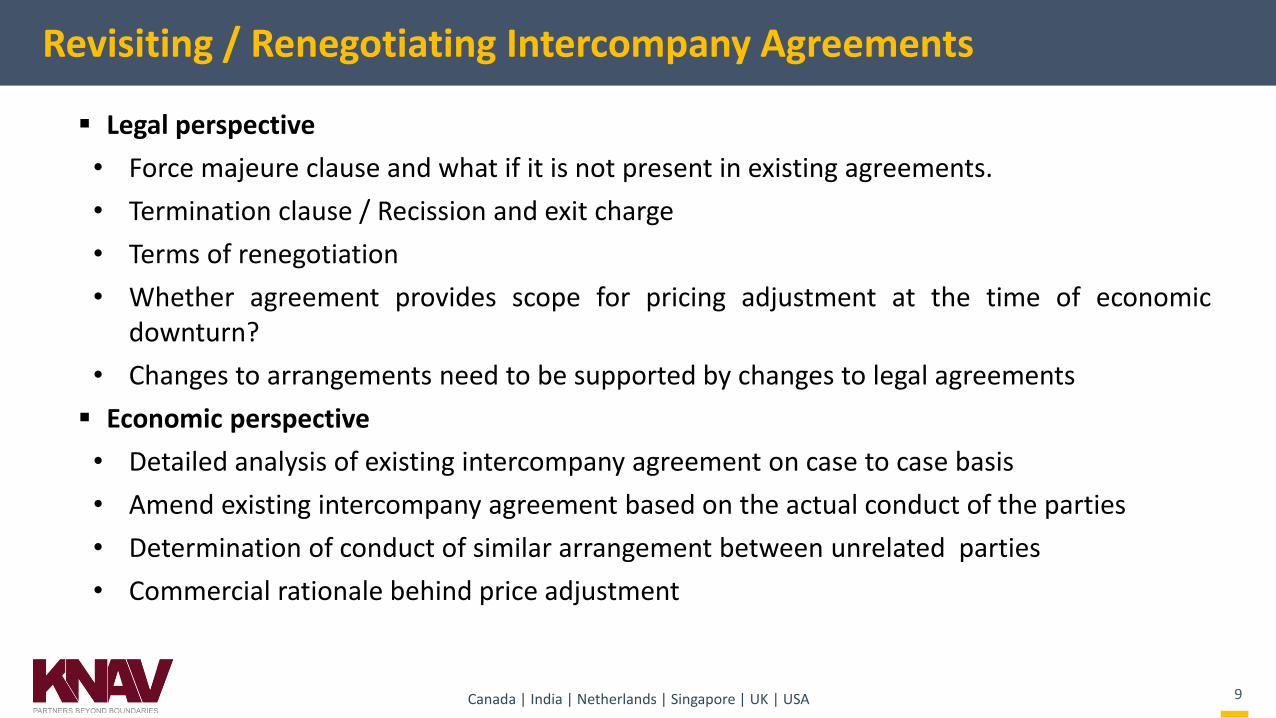

Revisiting / Renegotiating Intercompany Agreements

▪ Legal perspective

• Force majeure clause and what if it is not present in existing agreements.

• Termination clause / Recission and exit charge

• Terms of renegotiation

• Whether agreement provides scope for pricing adjustment at the time of economicdownturn?

• Changes to arrangements need to be supported by changes to legal agreements

▪ Economic perspective

• Detailed analysis of existing intercompany agreement on case to case basis

• Amend existing intercompany agreement based on the actual conduct of the parties

• Determination of conduct of similar arrangement between unrelated parties

• Commercial rationale behind price adjustment

9

Canada | India | Netherlands | Singapore | UK | USA

COMPENSATION FOR ROYALTY AND INTRAGROUP MANAGEMENT CHARGES

10

• Whether MNE should provide certain relief to loss-making licensee entities by way of waiver or reduction in fee or by granting moratorium period?

• Whether MNE group entities should pay for management services charges when the services were actually not received due to lockdown?

• Certain companies have established COVID-19 crisis management teams at corporate level and various measures are being taken. Should these costs be cross-charged to various group entities?

???

Canada | India | Netherlands | Singapore | UK | USA

Compensation for Royalty and Intragroup Management Charges

▪ Relief to loss-making licensee entities by way of waiver or reduction in fee or by granting moratorium period:

• Payment of royalties may put additional burden on cash flows of loss-making entities

• Whether a third party in similar circumstances would pay royalty when it was not able to utilise the IP andlicensee was not able to generate the revenue out of it?

• The regulations prevailing in both the service provider’s and service recipient's jurisdiction should beconsidered

• Any exceptions made for such payments need to be adequately thought through and documentedappropriately

▪ Management services charges when the services were actually not received due to lockdown:

• The benefits accrued from availing intragroup management services should typically justify the payments

• The Taxpayers are asked to demonstrate the need, benefit and rendition test

• Whether a third party would pay management charges when the services are not rendered by the serviceprovider and no benefits are received by the service recipient?

▪ COVID-19 crisis management expenses:

• Whether shareholder level expenses (considered towards stewardship function) or actual benefit beingpassed on to the group entities.

11

Canada | India | Netherlands | Singapore | UK | USA

INTRAGROUP FINANCING ARRANGEMENT

12

• What are the various aspects MNEs need to consider with respect to intragroup financial transactions?

• Should MNEs explore waiver / moratorium options available to them?

???

Canada | India | Netherlands | Singapore | UK | USA

Intragroup Financing Arrangement

▪ Various aspects MNEs need to consider with respect to intragroup financial transactions:

• Intercompany loans

o Recharacterization of loans to equity

o Reassessment of credit rating of borrower based on the updated financial projections

o Revisiting interest rates and repayment schedule

o Interest limitation rules in borrower’s as well as lender’s jurisdiction to avoid double taxation

o Exploring possibilities of providing reduced rate of interest or waiver or moratorium period

• Corporate guarantee

o Benefits to borrower - Improvement in credit rating and / or lower cost of borrowing, orenhancing borrowing capacity

o Assessment of risk of recharacterization in case of increase in the borrowing capacity

• Credit terms

o Extended credit terms - consistent with how they would transact with the third parties

13

Canada | India | Netherlands | Singapore | UK | USA

COMPARABILITY ANALYSIS AND TRANSFER PRICING DOCUMENTATION

14

• What are the challenges that may arise at the time of conducting benchmarking analysis?

• What aspects should be considered while preparing transfer pricing documentation considering COVID-19?

???

Canada | India | Netherlands | Singapore | UK | USA

Comparability Analysis and Transfer Pricing Documentation

▪ Various challenges that may arise at the time of conducting benchmarking analysis:

• Recent financial data will not reflect circumstances caused by COVID-19

• Selection of different time period analysis than the conventional three years

• Considering financial data of previous economic downturns

• Inclusion of loss-making comparable companies

• Economic adjustments on comparable companies such as idle capacity adjustment, workingcapital adjustment, adjusting fixed costs, etc.

• Treatment of extra-ordinary costs such as severance costs, inventory write-offs, businessrestructuring costs, lease breakage fees, contract termination settlement fees, assetimpairment, etc.

▪ Importance of robust Transfer Pricing Documentation:

• Maintaining contemporaneous documentation on real time basis

• Documenting the change in functional profile

• Industry overview

• Change in transfer pricing method should be substantiated

• Rationale for economic adjustment

15

Canada | India | Netherlands | Singapore | UK | USA

FUTURE CONTROVERSIES

16

• Do you foresee any future controversies surrounding transfer pricing and intercompany agreements? How should taxpayers prepare for it?

• How important will be the role of transfer pricing documentation in future litigations?

???

Canada | India | Netherlands | Singapore | UK | USA

Future Controversies

▪ Changes in business models and incidental transfer pricing leading to future taxlitigations

▪ Transfer pricing documentation issue -

• Taxpayers should ensure that corporate boards or managers properly andcontemporaneously document any changes to transfer pricing agreements.

• Taxpayers should ensure that corporate boards or managers properly andcontemporaneously document any changes to transfer pricing agreements.

17

Canada | India | Netherlands | Singapore | UK | USA

ADVANCE PRICING AGREEMENTS (‘APA’) AND DISPUTE RESOLUTION

18

• For the concluded APAs, whether Competent Authorities would be open to renegotiate the terms of APA? If yes, what should be the approach that MNEs should follow and what are the documents that MNEs need to maintain to strengthen their case?

???

Canada | India | Netherlands | Singapore | UK | USA

Advance Pricing Agreements (‘APA’) and Dispute Resolution

▪ Aspects related to concluded APAs:

• Renegotiate APAs in case of significant changes in the Critical Assumptions definedin the APA

• Experience from prior recessions / economic downturn

• Enhanced scrutiny on comparable companies, specially loss making comparables

• Expansion of time period for transfer pricing analysis

• Taxpayers should document how COVID-19 has impacted its business and criticalassumptions based on which the APA was entered into

• MNEs whose APA is at negotiation stage, should revisit their strategies based oncurrent economic circumstances

19

Canada | India | Netherlands | Singapore | UK | USA

Questions & Answers

20

21

OTHER OFFICES

21

INDIA OFFICE

Canada55 York Street, Suite 401, Toronto, ON M5J 1R7, Canada

NetherlandsFokkerstraat 12, 3833 LD Leusden, The Netherlands

Singapore60 Paya Lebar Road,#10-31 Paya Lebar Square, Singapore 409 051

UKGround floor, Hygeia Building, 66-68 College Road, Harrow, Middlesex HA1 1BE

USAOne Lakeside Commons, Suite 850, 990 Hammond Drive NE, Atlanta, GA 30328T: +1 678 584 1200

Canada | India | Netherlands | Singapore | UK | USA

For assistance, please contact [email protected] or visit us at: www.knavcpa.com

IndiaMumbai 201/202, Naman Centre, G-Block, Bandra-Kurla Complex, Bandra (East), Mumbai – 400 051T: +91 22 6164 4800

PuneA 401, Lotus Siddhi, Survey no. 162, D.P. Road, Aundh, Pune - 411007

Canada | India | Netherlands | Singapore | UK | USA

THANK YOU

22