Embed Size (px)

Citation preview

Open Forum on Pan-European Instant

Payments

Frankfurt

3rd May 2016

Welcome

Wolfgang Ehrmann

Chairman

Euro Banking Association

Open Forum on Pan-European Instant Payments, 3rd May 2016

Introduction

Hansjörg Nymphius

Advisor to the Board

Euro Banking Association

Open Forum on Pan-European Instant Payments, 3rd May 2016

4Open Forum on Pan-European Instant Payments, 3rd May 2016

1. Welcome by EBA Chairman

Wolfgang Ehrmann, Chairman, Euro Banking Association

2. Introduction by the Open Forum Coordinator

Hansjörg Nymphius, Advisor to the Board, Euro Banking Association

3. Taking stock of current instant payment developments and

initiatives outside of Europe (followed by Q&A session)

Dr. Leo Lipis, CEO, Lipis Advisors

Coffee break & networking

Proposed agenda

5Open Forum on Pan-European Instant Payments, 3rd May 2016

4. Understanding the expectations of online merchants from a real-

time solution (followed by Q&A session)

Douwe Lycklama, Partner, Innopay

5. Discussion and exchange of views on non-scheme issues

As a part of the discussion, you are invited to share your views on

non-scheme issues, such as AML or fraud checks

6. Closing remarks

Hansjörg Nymphius, Advisor to the Board, Euro Banking Association

Proposed agenda

Taking stock of current instant payment

developments and initiatives outside of Europe

Dr. Leo Lipis

CEO

Lipis Advisors

Open Forum on Pan-European Instant Payments, 3rd May 2016

© 2016, Lipis Advisors GmbH. All rights reserved. Proprietary and confidential

Real-time payments initiatives beyond EuropeOpen Forum on Pan/European Instant Payments

Facilitated by the EBA Association

3 May 2016

8

© 2016, Lipis Advisors GmbH. All rights reserved. Proprietary and confidential

Agenda

Introduction to Lipis Advisors

Introduction to the Global Payment Systems Analysis (GPSA)

A look around real-time payments

Countries in scope

Volume trends in real-time payments

Participation and the role of regulation

Settlement methods

System speed and availability

Popular use cases

Large western economies and RT

Final thoughts

9

© 2016, Lipis Advisors GmbH. All rights reserved. Proprietary and confidential

About Lipis Advisors

Industry analysis

We have unparalleled

understanding with many

years of experience and

insider knowledge of the

industry.

Payments business strategy

We possess deep

experience in payment

strategy development,

planning and leadership.

Product development

We have extensive

experience in the

development products

uniquely tailored for

specific markets.

Market intelligence

Decades of expert

knowledge and a network

of international SMEs in

the payment industry

provide remarkable insight

into markets.

Operations consulting

We combine payment

strategies and market

knowledge with execution.

Payments systems research

We conduct continuous

research on the latest

payment developments

and analyze new trends

with market leading data

visualization tools.

Real-time payments experts

10

© 2016, Lipis Advisors GmbH. All rights reserved. Proprietary and confidential

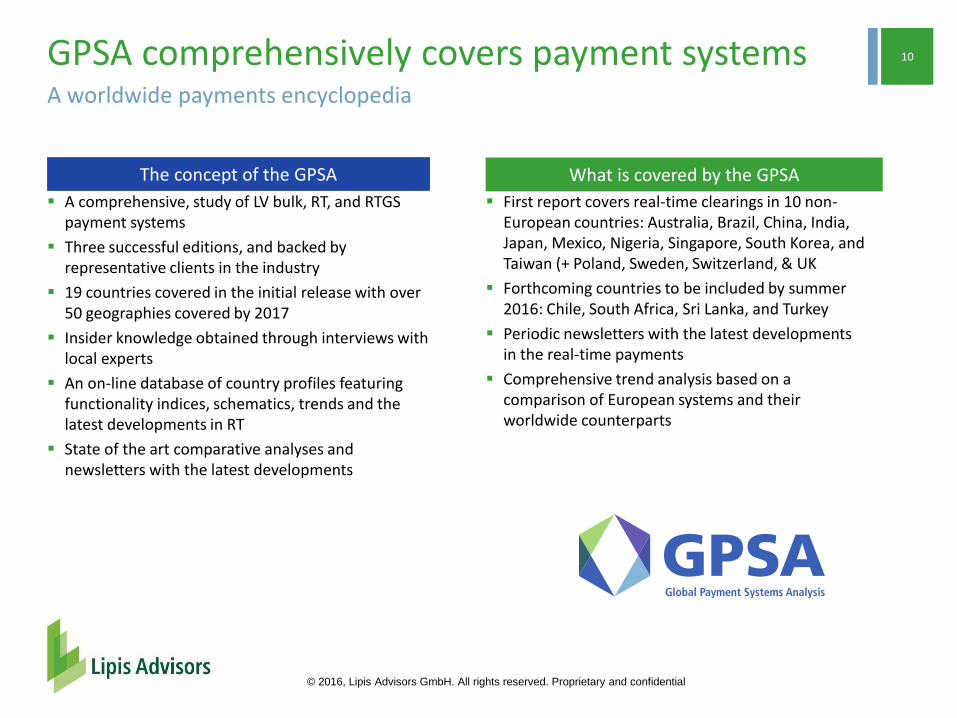

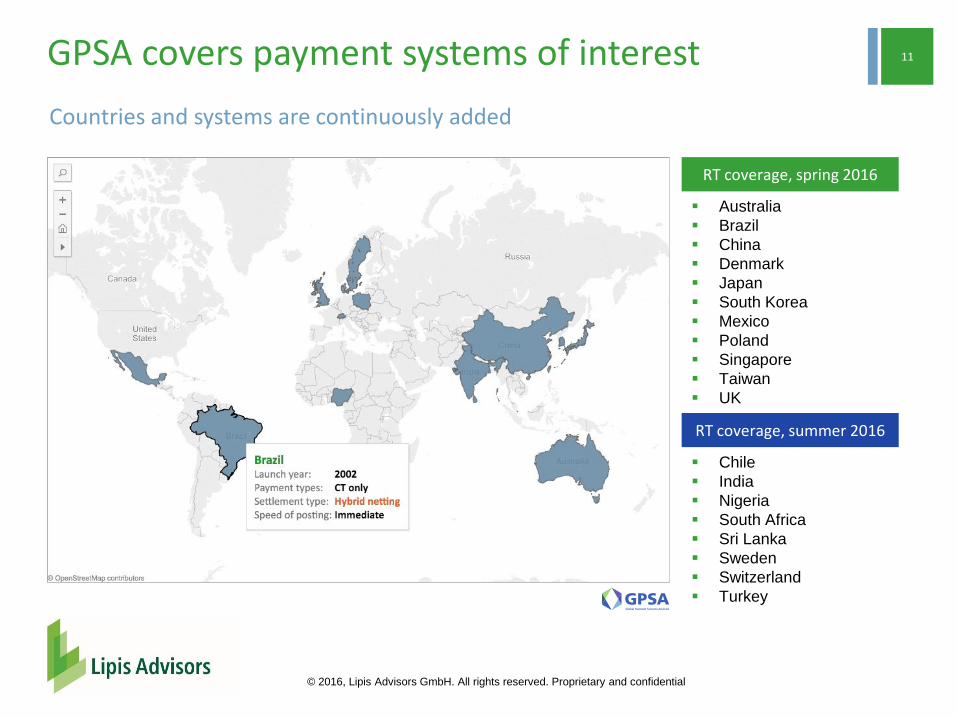

A worldwide payments encyclopedia

GPSA comprehensively covers payment systems

A comprehensive, study of LV bulk, RT, and RTGS payment systems

Three successful editions, and backed by representative clients in the industry

19 countries covered in the initial release with over 50 geographies covered by 2017

Insider knowledge obtained through interviews with local experts

An on-line database of country profiles featuring functionality indices, schematics, trends and the latest developments in RT

State of the art comparative analyses and newsletters with the latest developments

First report covers real-time clearings in 10 non-European countries: Australia, Brazil, China, India, Japan, Mexico, Nigeria, Singapore, South Korea, and Taiwan (+ Poland, Sweden, Switzerland, & UK

Forthcoming countries to be included by summer 2016: Chile, South Africa, Sri Lanka, and Turkey

Periodic newsletters with the latest developments in the real-time payments

Comprehensive trend analysis based on a comparison of European systems and their worldwide counterparts

The concept of the GPSA What is covered by the GPSA

11

© 2016, Lipis Advisors GmbH. All rights reserved. Proprietary and confidential

GPSA covers payment systems of interest

RT coverage, spring 2016

Australia

Brazil

China

Denmark

Japan

South Korea

Mexico

Poland

Singapore

Taiwan

UK

RT coverage, summer 2016

Chile

India

Nigeria

South Africa

Sri Lanka

Sweden

Switzerland

Turkey

Countries and systems are continuously added

12

© 2016, Lipis Advisors GmbH. All rights reserved. Proprietary and confidential

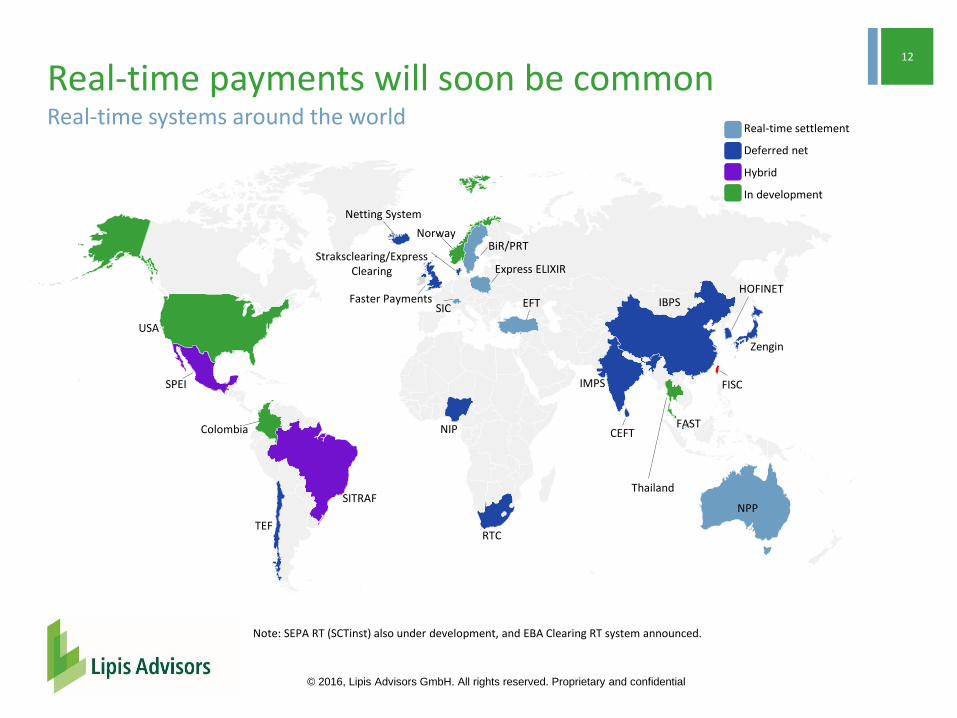

Real-time payments will soon be commonReal-time systems around the world

USA

SPEI

Colombia

SITRAF

TEF

NorwayBiR/PRT

Straksclearing/Express Clearing Express ELIXIR

SIC EFT

NIP

RTC

IMPS

IBPS

CEFT

HOFINET

Zengin

FISC

FAST

NPP

Faster Payments

Real-time settlement

Deferred net

Hybrid

In development

Note: SEPA RT (SCTinst) also under development, and EBA Clearing RT system announced.

Thailand

Netting System

13

© 2016, Lipis Advisors GmbH. All rights reserved. Proprietary and confidential

GPSA analysis show developing trendsAll real-time systems recorded growth

0

5

10

15

20

25

30

35

Nigeria India Mexico Brazil UK Japan China SouthKorea

Real-time system volume, 2013 and 2014

2013

2014

8.6%

13.8%

138.8

%

29.5%

836.5

%

17.5%

2.4% 130.8

%

Vo

lum

e in

Bill

ions

Some systems show quick adoption

Denmark and Singapore launched their

RT systems within the past 2 years:

Denmark recorded 5.13m

transactions in November and

December 2014.

Singapore’s FAST live since March

2014 but does not release

statistics.

Poland’s Express Elixir recorded 1.69m

in 2015 with a minority of banks in

Poland.

Drivers of growth

Volume is not driven by population but by

maturity and availability of alternatives

3 of the 4 top systems are >10 years old

Bottom 4 are in countries with larger

populations than the top 4 (except China)

Fastest growth is occurring in countries

with lowest base (except China)

14

© 2016, Lipis Advisors GmbH. All rights reserved. Proprietary and confidential

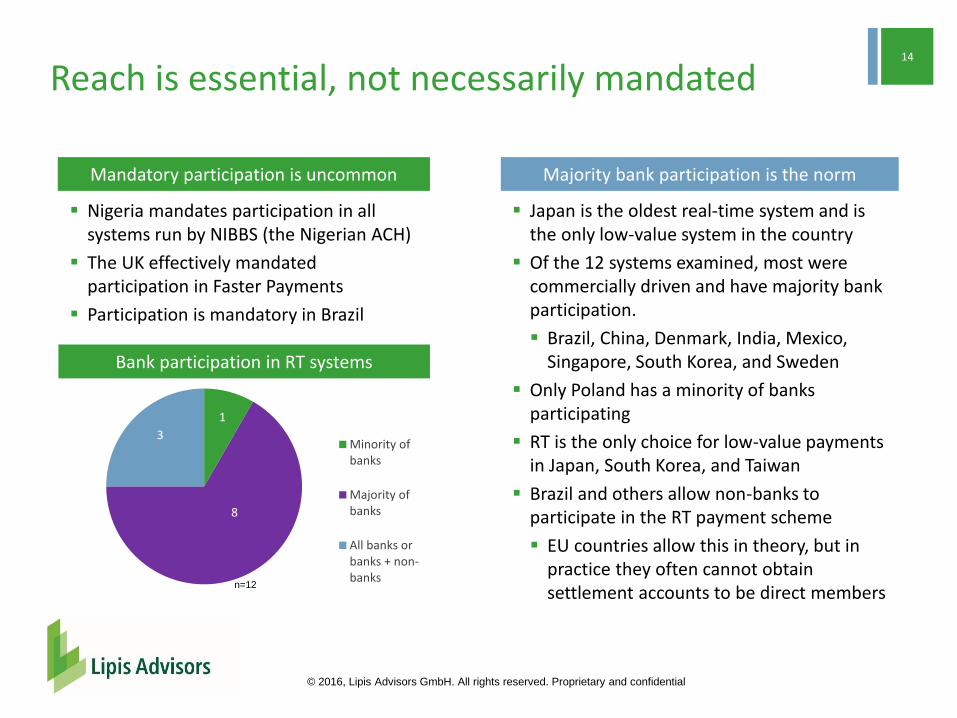

Majority bank participation is the norm

Japan is the oldest real-time system and is the only low-value system in the country

Of the 12 systems examined, most were commercially driven and have majority bank participation.

Brazil, China, Denmark, India, Mexico, Singapore, South Korea, and Sweden

Only Poland has a minority of banks participating

RT is the only choice for low-value payments in Japan, South Korea, and Taiwan

Brazil and others allow non-banks to participate in the RT payment scheme

EU countries allow this in theory, but in practice they often cannot obtain settlement accounts to be direct members

Mandatory participation is uncommon

Nigeria mandates participation in all systems run by NIBBS (the Nigerian ACH)

The UK effectively mandated participation in Faster Payments

Participation is mandatory in Brazil

Reach is essential, not necessarily mandated

1

8

3

Bank participation in real-time systems

Minority ofbanks

Majority ofbanks

All banks orbanks + non-banks

Bank participation in RT systems

n=12

15

© 2016, Lipis Advisors GmbH. All rights reserved. Proprietary and confidential

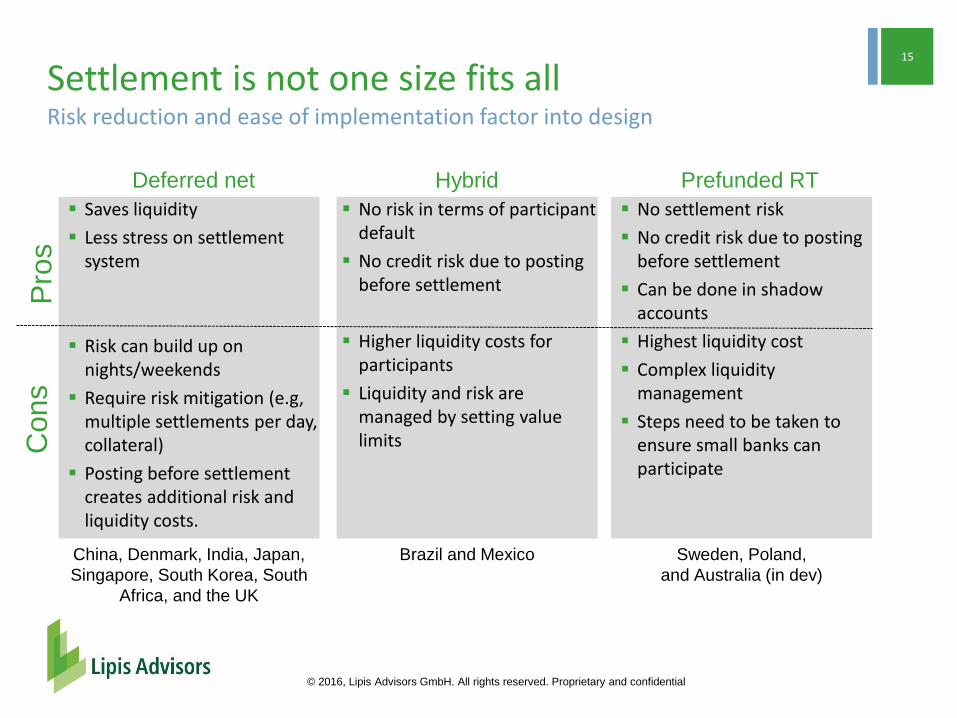

Settlement is not one size fits all

Saves liquidity

Less stress on settlement system

Risk can build up on nights/weekends

Require risk mitigation (e.g, multiple settlements per day, collateral)

Posting before settlement creates additional risk and liquidity costs.

Deferred net

No risk in terms of participant default

No credit risk due to posting before settlement

Higher liquidity costs for participants

Liquidity and risk are managed by setting value limits

Hybrid

No settlement risk

No credit risk due to posting before settlement

Can be done in shadow accounts

Highest liquidity cost

Complex liquidity management

Steps need to be taken to ensure small banks can participate

Prefunded RT

Pro

sC

on

s

Risk reduction and ease of implementation factor into design

China, Denmark, India, Japan,

Singapore, South Korea, South

Africa, and the UK

Sweden, Poland,

and Australia (in dev)

Brazil and Mexico

16

© 2016, Lipis Advisors GmbH. All rights reserved. Proprietary and confidential

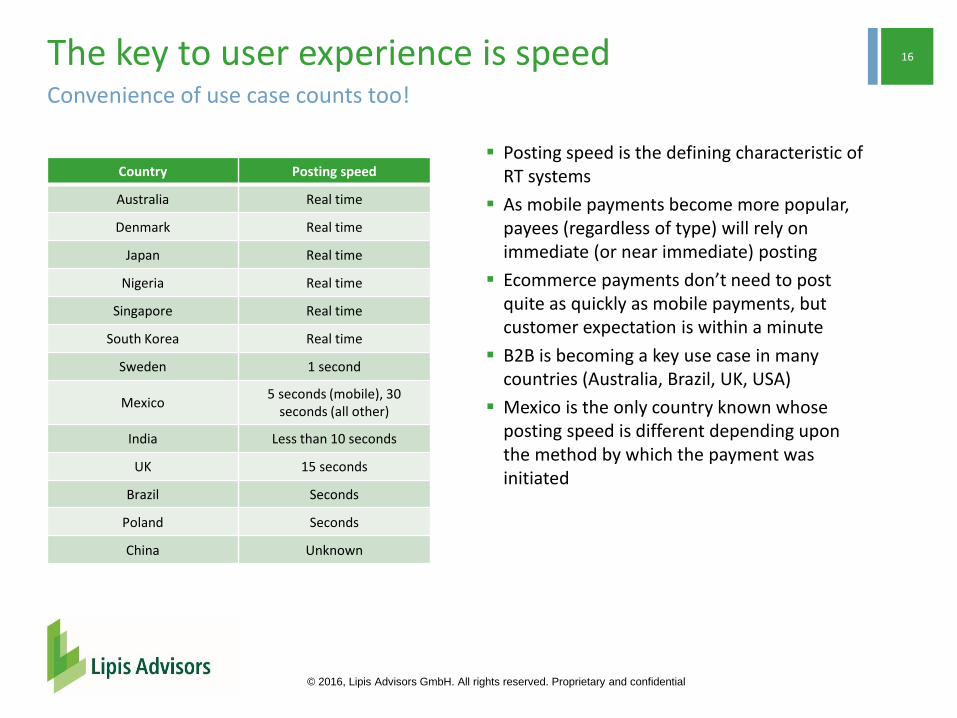

Convenience of use case counts too!

The key to user experience is speed

Country Posting speed

Australia Real time

Denmark Real time

Japan Real time

Nigeria Real time

Singapore Real time

South Korea Real time

Sweden 1 second

Mexico5 seconds (mobile), 30

seconds (all other)

India Less than 10 seconds

UK 15 seconds

Brazil Seconds

Poland Seconds

China Unknown

Posting speed is the defining characteristic of RT systems

As mobile payments become more popular, payees (regardless of type) will rely on immediate (or near immediate) posting

Ecommerce payments don’t need to post quite as quickly as mobile payments, but customer expectation is within a minute

B2B is becoming a key use case in many countries (Australia, Brazil, UK, USA)

Mexico is the only country known whose posting speed is different depending upon the method by which the payment was initiated

17

© 2016, Lipis Advisors GmbH. All rights reserved. Proprietary and confidential

Direct debits in real-time? Corporate use cases

China’s IBPS is an “Internet banking” platform. Customers access multiple accounts at multiple banks for real-time debit and credit transactions. Banks offer a range of products, including bill payments, direct debits, and internal corporate transfers.

Singapore’s FAST system will replace the IBG low-value system. Direct debit functionality was recently activated.

Sri Lanka is focused on developing and popularizing direct debit functionality for the real-time system. Risk management will entail determining maximum limits and transaction frequency, and setting criteria to initiate direct debits.

Australia’s NPP is focused on addressing corporate use cases.

Chinese corporates can manage collections contracts through the IBPS system. They can initiate real-time direct debits.

Real-time POS

The UK’s Pay by Bank app, which is in development, will enable real-time POS transactions via mobile devices utilizing Faster Payments.

Shifting the real-time product landscapeBeyond real-time credit transfers and P2P payments

18

© 2016, Lipis Advisors GmbH. All rights reserved. Proprietary and confidential

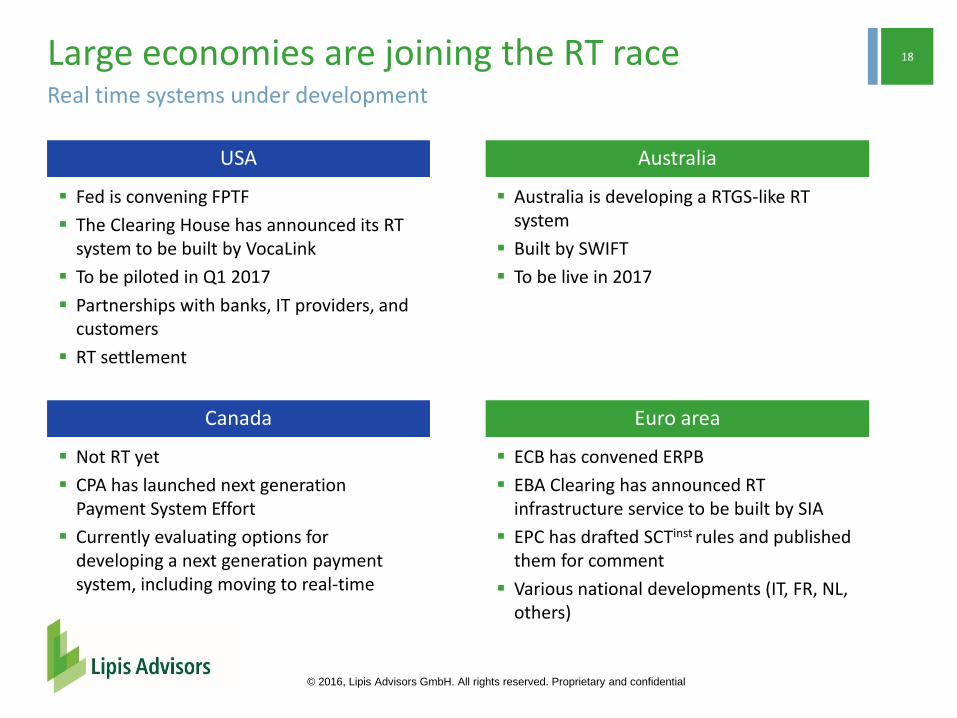

Real time systems under development

Large economies are joining the RT race

USA Australia

Fed is convening FPTF

The Clearing House has announced its RT system to be built by VocaLink

To be piloted in Q1 2017

Partnerships with banks, IT providers, and customers

RT settlement

Australia is developing a RTGS-like RT system

Built by SWIFT

To be live in 2017

Canada Euro area

Not RT yet

CPA has launched next generation Payment System Effort

Currently evaluating options for developing a next generation payment system, including moving to real-time

ECB has convened ERPB

EBA Clearing has announced RT infrastructure service to be built by SIA

EPC has drafted SCTinst rules and published them for comment

Various national developments (IT, FR, NL, others)

19

© 2016, Lipis Advisors GmbH. All rights reserved. Proprietary and confidential

RT payments are coming The future of RT

RT is coming

Historical trends show wide acceptance and a business case for it

There are national as well as regional initiatives to build RT capability

Use cases are broader than expected

Direct Debits in RT are unusual and possibly implausible in Europe given the regulatory landscape in the EU

Settlement models vary; in the EU it is dependent on the ECB’s stance on risk

The real-time revolution is underway

Reach / Participation and uniformity for experience for all users

Coordination / interoperability between national and regional initiatives

Legislative constraints

Settlement model harmony

Key points

Challenges

20

© 2016, Lipis Advisors GmbH. All rights reserved. Proprietary and confidential

For further informationLearn more about the GPSA and our real-time payments’ expertise

Leo Lipis

Lipis Advisors

lipisadvisors.com/gpsa/

Telephone +49 30 8892 2049

Mobile +49 172 990 5777

Knesebeckstrasse 61a

10719 Berlin

Germany

Coffee break & networking

Open Forum on Pan-European Instant Payments, 3rd May 2016

Open Forum on Pan-European Instant Payments, 3rd May 2016

Understanding the expectations of online merchants from a real-

time solution

Douwe Lycklama

Partner

Innopay

tomorrow’stransactionstoday

Themerchantview:frominstantpaymenttoinstantcommerce

Instantpayments

DouweLycklama(PartnerInnopay)– 3May2016Frankfurt

2 Themerchantview:frominstant paymenttoinstantcommerce©|Frankfurt3May2016InnopayBV.Allrightsreserved.

• Innopay:innovationexpertssince2002

• 30consultants

• OfficesinAmsterdamandFrankfurt

• Practices:Payments,DigitalIdentity,e-Business

• Services:Strategy,Co-creation,Transformation

• MemberofEBA,EPCAandECP

• FoundingmemberofHollandFintech

Introduction

3 Themerchantview:frominstant paymenttoinstantcommerce©|Frankfurt3May2016InnopayBV.Allrightsreserved.

CUSTOMER

MERCHANT

Timespaceconvergencehasarrivedtopayments…

Placesareseparatedbyabsolutedistanceandbytime.Withimprovementsincommunicationsystemsandmethodsoftransport,thistime-distancediminishes.Inessence,time–spaceconvergencemeansthatthefrictionofdistance—aconceptfundamentaltoconventionalcentralplacetheory,diffusiontheory,andlocationtheory—is lessening.

In1992,R.O'Brienpredicted‘theendofgeography’.Hewaswrong.Simson(2005)J.Transp.Geog.26,2writesthat ‘speedpermeatesthehistoryoftransportandmodernity,butitdoessoinmultipleways.

Thetime–spacecompressionnarrativeisnotadequatetoencompassthishistory.’Furthermore‘therearedifferentkindsoftechnologies,differentlevelsoftechnologicalchange,andeventhesametechnologycanbeuseddifferentlybydifferentpeople indifferentplaces’(N.Coeetal.2007).

Source:OxfordReference

4 Themerchantview:frominstant paymenttoinstantcommerce©|Frankfurt3May2016InnopayBV.Allrightsreserved.

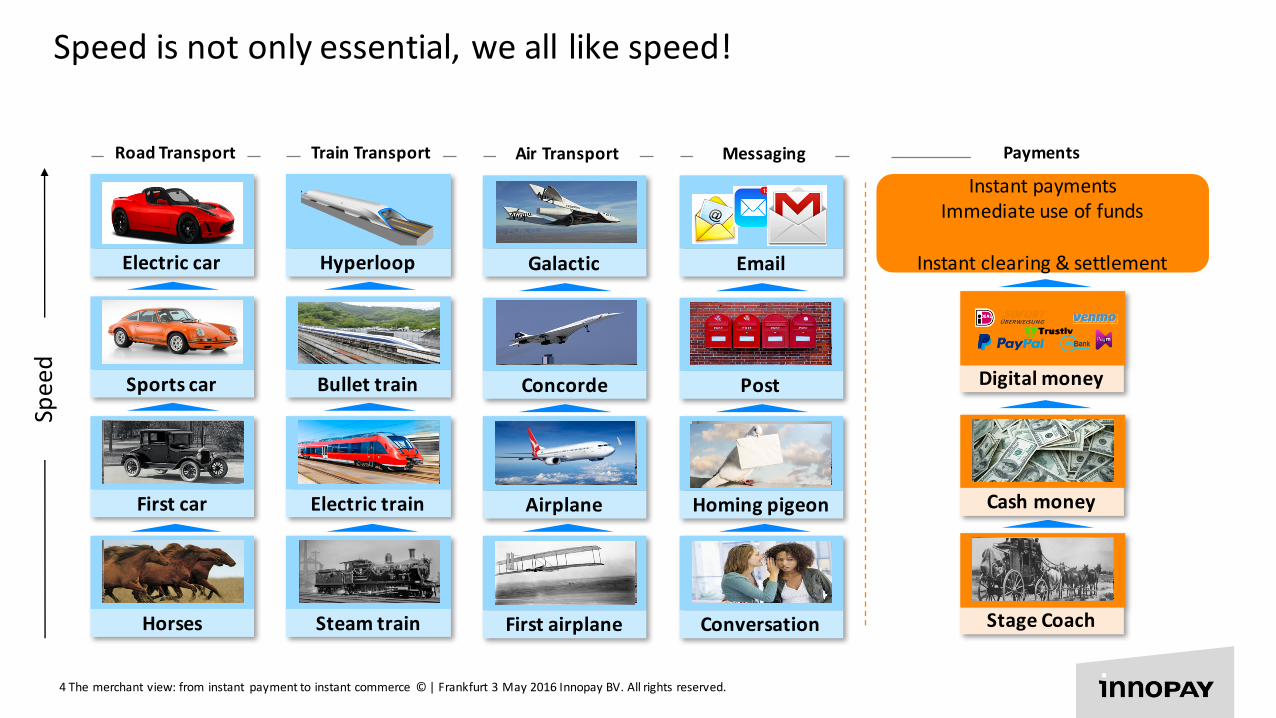

Speedisnotonlyessential,wealllikespeed!Speed

TrainTransport

Steamtrain

Electrictrain

Bullettrain

Hyperloop

RoadTransport

Horses

Firstcar

Sportscar

Electriccar

AirTransport

Firstairplane

Airplane

Concorde

Galactic

Messaging

Conversation

Homingpigeon

Post

Payments

StageCoach

InstantpaymentsImmediateuseoffunds

Instantclearing&settlement

Cashmoney

Digitalmoney

5 Themerchantview:frominstant paymenttoinstantcommerce©|Frankfurt3May2016InnopayBV.Allrightsreserved.

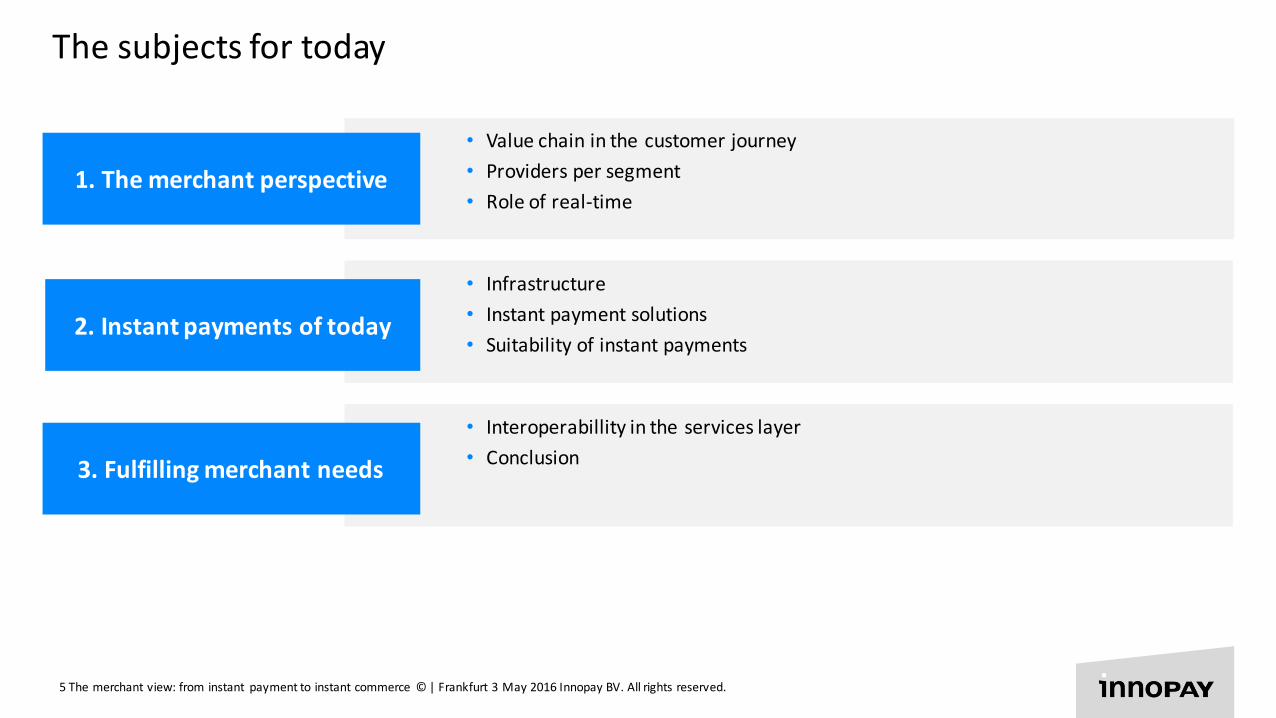

Thesubjectsfortoday

• Valuechaininthecustomerjourney• Providerspersegment• Roleofreal-time

• Interoperabillity intheserviceslayer• Conclusion3.Fulfillingmerchantneeds

• Infrastructure• Instantpaymentsolutions• Suitabilityofinstantpayments

2.Instantpaymentsoftoday

1.Themerchantperspective

6 Themerchantview:frominstant paymenttoinstantcommerce©|Frankfurt3May2016InnopayBV.Allrightsreserved.

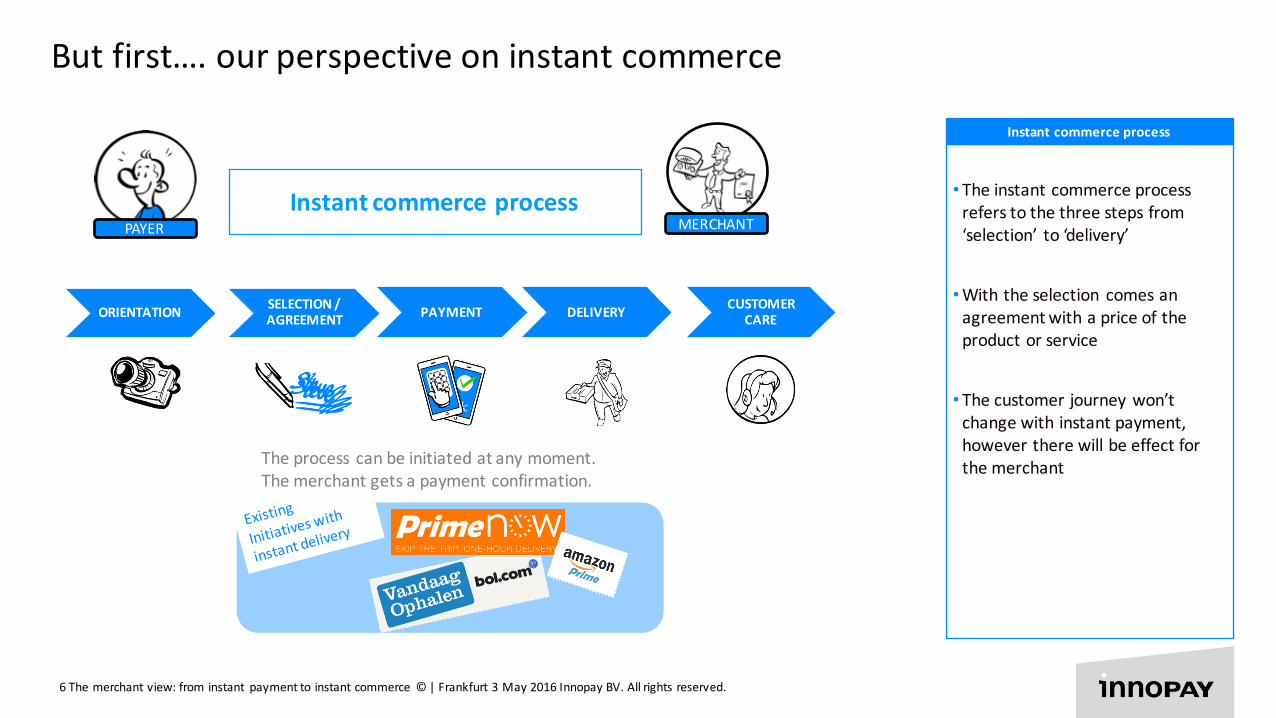

Butfirst….ourperspectiveoninstantcommerce

SELECTION/AGREEMENT PAYMENT DELIVERY

PAYER MERCHANTInstantcommerceprocess

CUSTOMERCAREORIENTATION

Instantcommerceprocess

• Theinstantcommerceprocessreferstothethreestepsfrom‘selection’ to‘delivery’

•Withtheselection comesanagreementwithapriceoftheproductorservice

• Thecustomerjourneywon’tchangewithinstantpayment,howevertherewillbeeffectforthemerchantTheprocess canbeinitiatedatanymoment.

Themerchantgetsapaymentconfirmation.

7 Themerchantview:frominstant paymenttoinstantcommerce©|Frankfurt3May2016InnopayBV.Allrightsreserved.

Customerjourney:orientation/selection,order/payment, deliveryandcustomercare

Webshop

Information Funds

SCT,SDD,Cards

ACH,Visanet,Banknet

RealTimeGrossSettlement

Instruments

Processing

Settlement

SEPA

ServicesInfrastructure

Custom

er

account

ISSUINGBANK ACQUIRINGBANK

CUSTOMER MERCHANT

Browser

Onlinebanking

Webshop

Routingservice

Onlinepymntprovider

Source:Innopayanalysis,Euro BankingAssociation(EBA),European CentralBank(ECB)

Merchant

account

Merchantsarealreadyinstantbecausecustomersexpectinstant

12

3

Mostservicesofthemerchantarealready instant

Merchantsoffersawidevarietyofstepsinordertomeetthecustomersrequirementof‘instantcommerce’

Legendofnumberedsteps:

1. Orientation&SelectionThecustomerstartshis/herorientationandselectionprocessfortherequiredproductorservice

2. Order&PaymentThecustomerchoosesapaymentmethod

3. DeliveryThemerchantstartswiththedeliveryprocess

4. CustomercareIfnecessarythecustomercancontactthemerchantforcustomercare

Cloudandinteroperabilitybetweensolutionsenablemerchantstobemoresuccessfulininstantcommerce

4

1Customerjourney steps

8 Themerchantview:frominstant paymenttoinstantcommerce©|Frankfurt3May2016InnopayBV.Allrightsreserved.

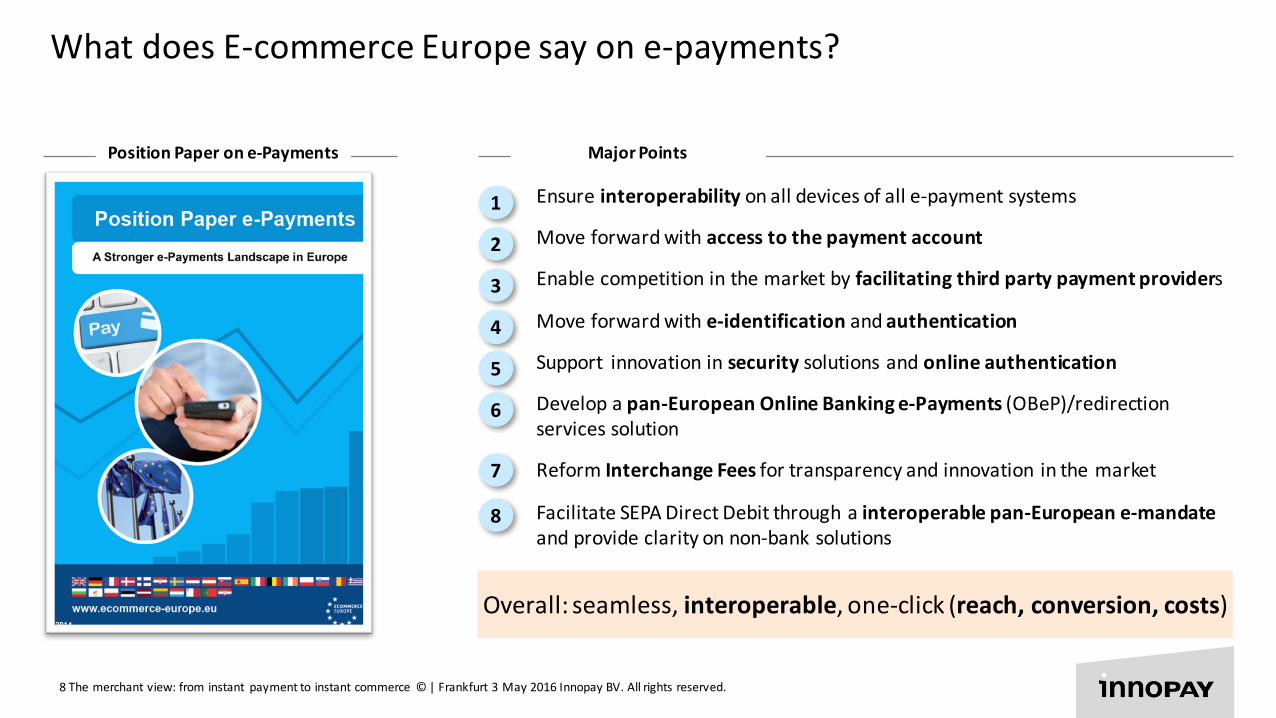

1. Ensureinteroperability onalldevicesofalle-paymentsystems

2. Moveforwardwithaccesstothepaymentaccount

3. Enablecompetitioninthemarketbyfacilitatingthirdpartypaymentproviders

4. Moveforwardwithe-identificationandauthentication

5. Support innovationinsecurity solutionsandonlineauthentication

6. Developapan-EuropeanOnlineBankinge-Payments(OBeP)/redirectionservicessolution

7. ReformInterchangeFeesfortransparencyandinnovationinthemarket

8. FacilitateSEPADirectDebitthroughainteroperable pan-Europeane-mandateandprovideclarityonnon-banksolutions

WhatdoesE-commerceEuropesayone-payments?

PositionPaperone-Payments MajorPoints

1

2

3

Overall:seamless,interoperable,one-click(reach,conversion,costs)

4

5

6

7

8

9 Themerchantview:frominstant paymenttoinstantcommerce©|Frankfurt3May2016InnopayBV.Allrightsreserved.

SuccessfulpaymentsolutionsprovideReachandConversionagainstfairCost

REACH

CONVERSION

COST

Visitors

Potentialbuyers

Customers

Profit

1

2

3

MERCHANT

ReachconversioncostKeycustomerrequirementsforpaymentsingeneral

1. ReachMerchantview:theshareofvisitorswhichcanpotentiallypayinashop,i.e.couldbecomepotentialcustomers.Consumerview:theshareofshopswherehecouldpayforapurchase

2. ConversionMerchantview:theshareofvisitorswhichactuallybecomeacustomerConsumerview:theeaseofuseofcompletingapurchase

3. CostThecostsassociatedwiththetransaction,whichhasadirectbottomlineeffectformerchantandconsumer.Thisgoesbeyondpuretransactioncosts,andincludeschargebacks,fraudandimplementation/onboardingefforts

10 Themerchant view:frominstant paymenttoinstantcommerce©|Frankfurt3May2016InnopayBV.Allrightsreserved.

REACH

CONVERSION

COST

Customersandmerchantsmostlywantthesame…

• Widelyaccepted&trustedpaymentmethods• Availabilityofpaymentsystems

• Easeofuse• Seamlessexperience

• Guaranteedsettlement• Instantconfirmationoffinality/irrevocability

• Costinsight• Banksidecharges• Merchant surcharge

• Costoffraud• Nomigrationcosts• Nochargeback

1

2

3

“Onlyonepaymentaccount toshoponlineacrossEurope” “Keepcheck-outsimpleandmitigaterisks”MERCHANTCUSTOMER

Source:Innopayanalysis

• Payafterorhavechargebackoption• Instantconfirmationofpurchase

• Lowcostpaymentmethods

11 Themerchant view:frominstant paymenttoinstantcommerce©|Frankfurt3May2016InnopayBV.Allrightsreserved.

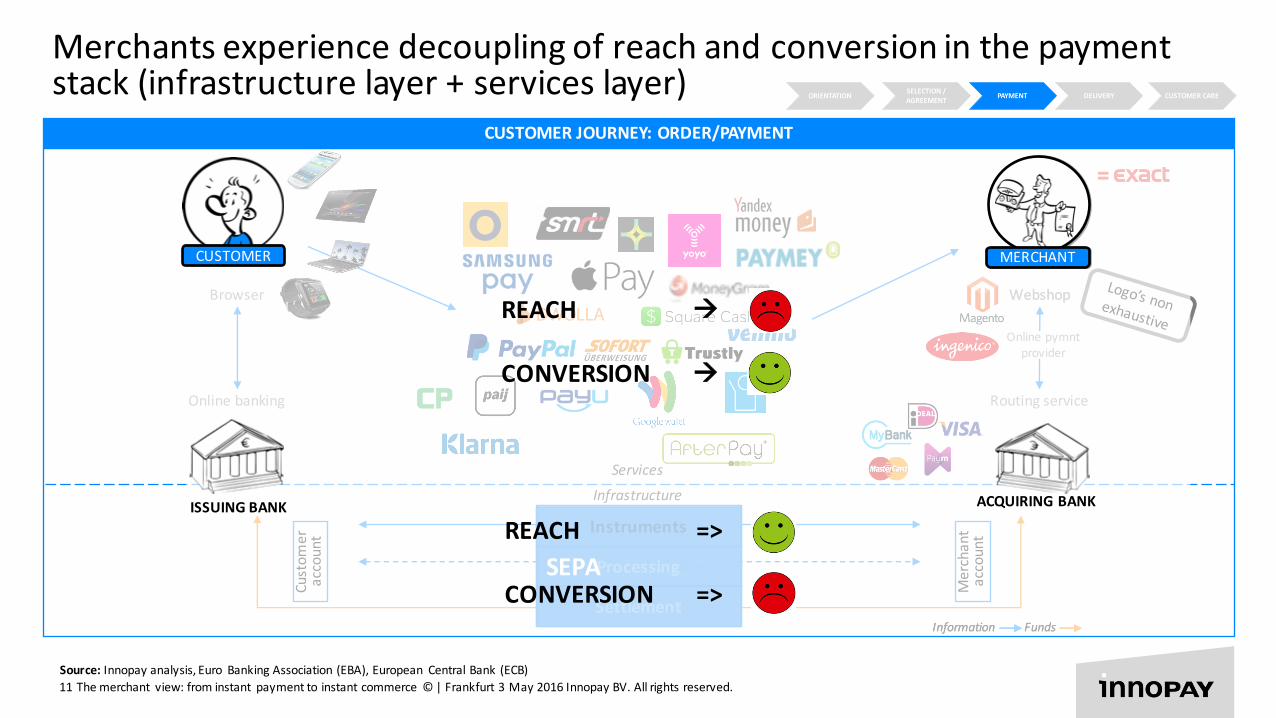

CUSTOMERJOURNEY:ORDER/PAYMENT

Webshop

Information FundsInformation Funds

SCT,SDD,Cards

ACH,Visanet,Banknet

RealTimeGrossSettlement

Instruments

Processing

Settlement

SEPA

Custom

er

account

Merchant

account

MERCHANT

Browser

Onlinebanking

Webshop

Routingservice

Onlinepymntprovider

Source:Innopayanalysis,Euro BankingAssociation(EBA),European CentralBank(ECB)

ISSUINGBANK ACQUIRINGBANK

SELECTION/AGREEMENT PAYMENT DELIVERY CUSTOMERCAREORIENTATION

CUSTOMER MERCHANT

ServicesInfrastructure

REACH à

CONVERSION à

REACH =>

CONVERSION =>

Merchantsexperiencedecouplingofreachandconversioninthepaymentstack(infrastructurelayer+serviceslayer)

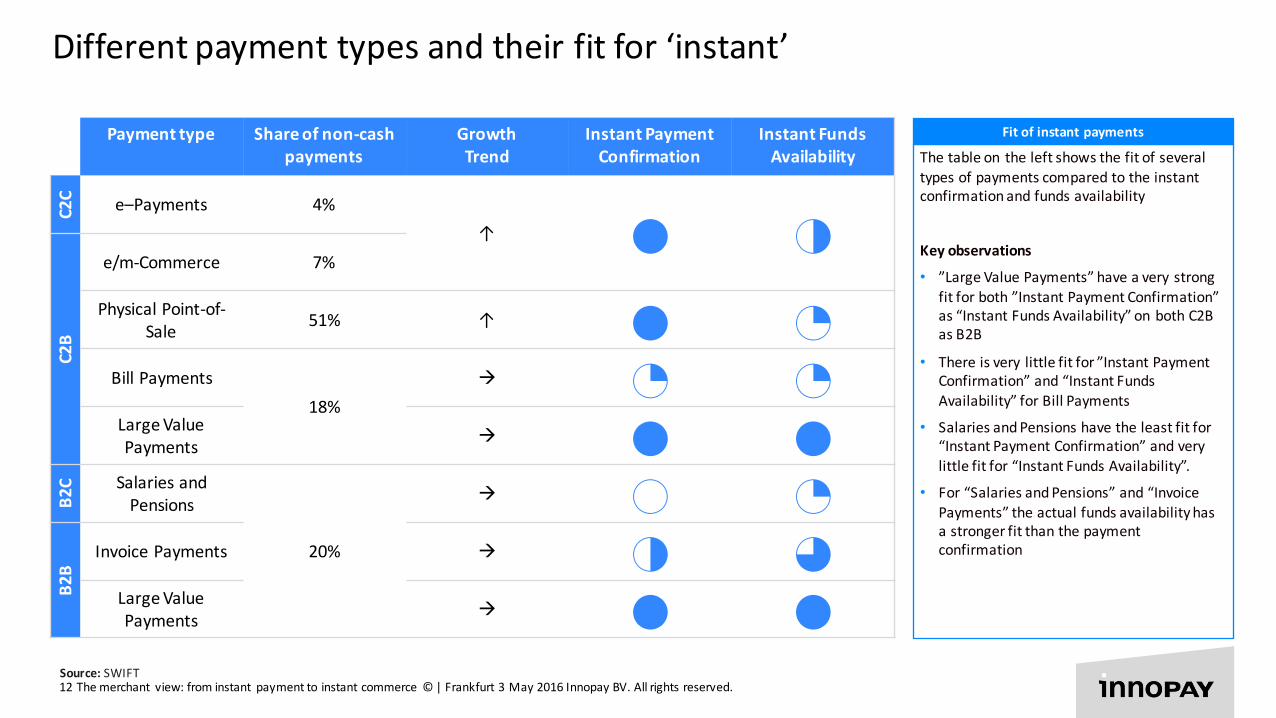

12 Themerchant view:frominstant paymenttoinstantcommerce©|Frankfurt3May2016InnopayBV.Allrightsreserved.Source:SWIFT

Differentpaymenttypesandtheirfitfor‘instant’

Paymenttype Shareofnon-cashpayments

GrowthTrend

Instant PaymentConfirmation

Instant FundsAvailability

C2C e–Payments 4%

↑ 4 2

C2B

e/m-Commerce 7%

PhysicalPoint-of-Sale 51% ↑ 4 1

BillPayments18%

à 1 1LargeValuePayments à 4 4

B2C Salariesand

Pensions

20%

à 0 1

B2B

InvoicePayments à 2 3LargeValuePayments à 4 4

Fitofinstantpayments

Thetableon theleftshowsthefitofseveraltypesofpaymentscomparedtotheinstantconfirmationandfundsavailability

Keyobservations

• ”LargeValuePayments”haveavery strongfitforboth”InstantPaymentConfirmation”as“InstantFundsAvailability”onbothC2BasB2B

• Thereisvery littlefitfor”InstantPaymentConfirmation”and“InstantFundsAvailability”forBillPayments

• SalariesandPensionshavetheleastfitfor“InstantPaymentConfirmation”andverylittlefitfor“InstantFundsAvailability”.

• For“SalariesandPensions”and“InvoicePayments”theactualfundsavailabilityhasastrongerfitthanthepaymentconfirmation

13 Themerchant view:frominstant paymenttoinstantcommerce©|Frankfurt3May2016InnopayBV.Allrightsreserved.

Webshop

Information FundsInformation Funds

SCT,SDD,Cards

ACH,Visanet,Banknet

RealTimeGrossSettlement

Instruments

Processing

Settlement

SEPA

ServicesInfrastructure

Custom

er

account

Merchant

account

ISSUINGBANK ACQUIRINGBANK

Browser

Onlinebanking

Webshop

Routingservice

Onlinepymntprovider

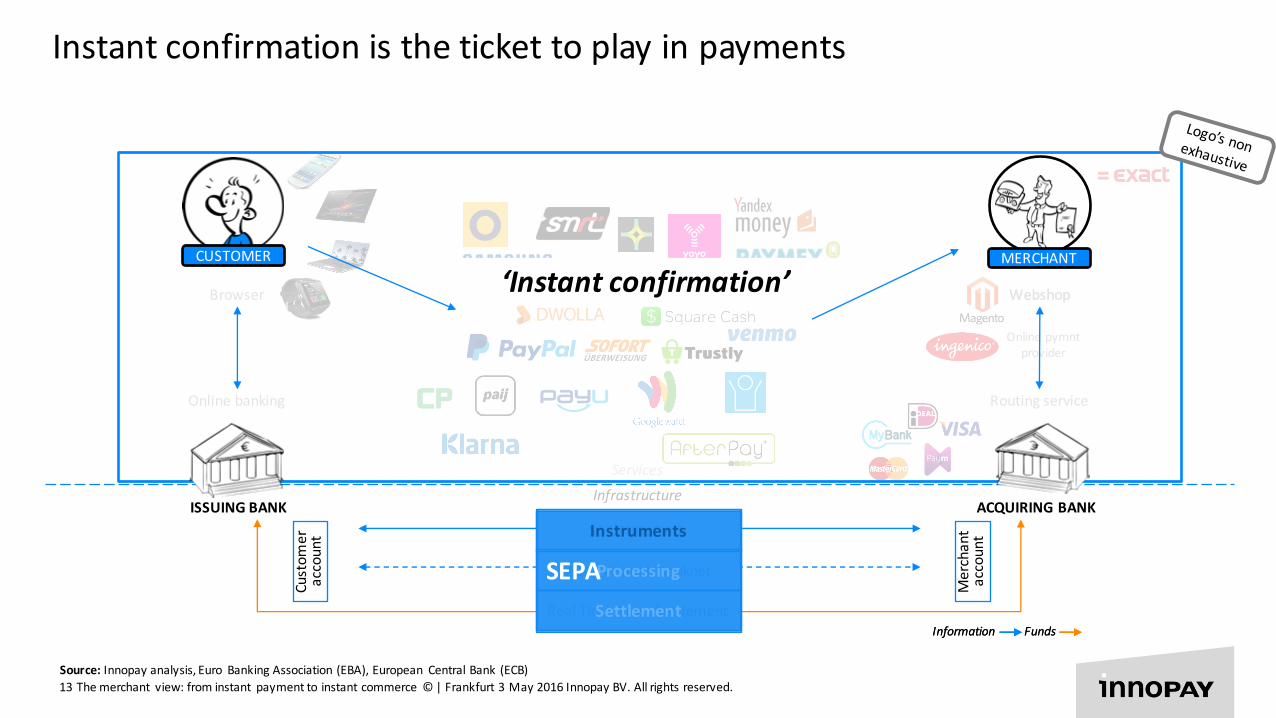

Source:Innopayanalysis,Euro BankingAssociation(EBA),European CentralBank(ECB)

‘Instantconfirmation’CUSTOMER MERCHANT

Instantconfirmationisthetickettoplayinpayments

14 Themerchant view:frominstant paymenttoinstantcommerce©|Frankfurt3May2016InnopayBV.Allrightsreserved.

Instantpaymentsintheworldofmerchantstoday

• Valuechaininthecustomerjourney• Providerspersegment• Roleofreal-time

• Interoperabillity intheserviceslayer• Conclusion3.Fulfillingmerchantneeds

• Infrastructure• Instantpaymentsolutions• Suitabilityofinstantpayments

2.Instantpaymentsoftoday

1.Themerchantperspective

15 Themerchant view:frominstant paymenttoinstantcommerce©|Frankfurt3May2016InnopayBV.Allrightsreserved.

Apaymentcanmeanmanythingswithonethingincommon…

16 Themerchant view:frominstant paymenttoinstantcommerce©|Frankfurt3May2016InnopayBV.Allrightsreserved.Source:Innopayanalysis,Euro BankingAssociation(EBA),European CentralBank(ECB)

InformationFunds

InformationFunds

SCT,SDD,Cards

ACH,Visanet,Banknet

RealTimeGrossSettlement

Instruments

Processing

Settlement

SEPA/Instantclearing&settlement

Custom

er

account

Merchant

account

ISSUINGBANK ACQUIRINGBANK

CUSTOMER MERCHANT

Browser

Onlinebanking

Webshop

Routingservice

Onlinepymntprovider

Instantpaymentsdeliversinstantconfirmationaboutthepaymenttoboththecustomerandmerchantand transfersthefundsinstantly

Information

‘Instantfundstransfer’

‘Instantconfirmation’

ServicesInfrastructure

‘InstantPayments’

17 Themerchant view:frominstant paymenttoinstantcommerce©|Frankfurt3May2016InnopayBV.Allrightsreserved.Source:Innopayanalysis,Euro BankingAssociation(EBA),European CentralBank(ECB)

InformationFunds

InformationFunds

SCT,SDD,Cards

ACH,Visanet,Banknet

RealTimeGrossSettlement

Instruments

Processing

Settlement

SEPA/Instantclearing&settlement

ServicesInfrastructure

Closed system/wallet

Custom

er

account

Merchant

account

ISSUINGBANK ACQUIRINGBANK

CUSTOMER MERCHANT

Browser

Onlinebanking

Webshop

Routingservice

Onlinepymntprovider

ThirdPartyDirect

‘Onus’transaction

InstantPayment

Variousinstantpaymentinfrastructure&servicesolutionsfacilitatean”instantpayment”

Information

Layeredinfrastructure&service

Makedirectpaymentstootherusersofthesamewalletservice

AThirdPartyDirectservicehasaccountsat(all)banksandcanthereforemakeinstanttransfers

Thepayerandmerchanthaveanaccountatthesamebank

Clearingandsettlementbetweenbanksareinstantly

18 Themerchant view:frominstant paymenttoinstantcommerce©|Frankfurt3May2016InnopayBV.Allrightsreserved.Source:Innopayanalysis,Euro BankingAssociation(EBA),European CentralBank(ECB)

InformationFunds

InformationFunds

SCT,SDD,Cards

ACH,Visanet,Banknet

RealTimeGrossSettlement

Instruments

Processing

Settlement

SEPA/Instantclearing&settlement

ServicesInfrastructure

Closed system/wallet

Custom

er

account

Merchant

account

ISSUINGBANK ACQUIRINGBANK

CUSTOMER MERCHANT

Browser

Onlinebanking

Webshop

Routingservice

Onlinepymntprovider

ThirdPartyDirect

‘Onus’transaction

InstantPayment

ExistingfragmentationofmobileP2Psolutionsisachallengewithover50(local)solutionsfrom22countries

Information

Layeredinfrastructure&service

Makedirectpaymentstootherusersofthesamewalletservice

AThirdPartyDirectservicehasaccountsat(all)banksandcanthereforemakeinstanttransfers

Thepayerandmerchanthaveanaccountatthesamebank

Clearingandsettlementbetweenbanksareinstantly

19 Themerchant view:frominstant paymenttoinstantcommerce©|Frankfurt3May2016InnopayBV.Allrightsreserved.Source:FIS,EuropeanPaymentCouncil (EPC)

Manyversionsof‘instantpayments’intheinfrastructurelayer

20 Themerchant view:frominstant paymenttoinstantcommerce©|Frankfurt3May2016InnopayBV.Allrightsreserved.Source:European PaymentsCouncil (EPC),Innopayanalysis

‘Instantpayments’donotpositionclearlyyettowardsotherpaymentoptions

Expectations Debit card Creditcard Banktransfer Directdebit Instantpayments

Payer&

Payee

24/7/365 accessible 4 4 4 4 4

Easytouse 4 4 3 3 4Confidence inthe

reliabilityofsolution 4 4 4 4 4Reachability ofthe

solution 4 4 4 2 4Interoperability of

solution 4 4 4 4 4

Payer Easytopaywith 4 4 4 4 4

Instantcertaintyofpayment 4 4 4 2 4

Payee

Availabilityoffunds Delay Delay MaxD+1 Max D+1 4

Fitofinstantpayments

PayerandPayeeexpectationsforaninstantpaymentsolutioncomparedtootherpaymentsolutions

Thepayeristheconsumer,howeverthiscanalsobeaconsumingbusiness.ThePayeeisthemerchant

Strikingfeatures

• Besidesafewtherearehighexpectationscomparableexpectationsfrombothperspectives

• ”Directdebit”hasthelowestexpectationsespeciallyon the“Reachabilityofthesolution”andthe“Instantcertaintyofthepayment”

• “Instantpayments”hasthehighestexpectationsonallpoint

21 Themerchant view:frominstant paymenttoinstantcommerce©|Frankfurt3May2016InnopayBV.Allrightsreserved.

Whatdoesinstantpaymentmeantomerchants?

• Valuechaininthecustomerjourney• Providerspersegment• Roleofreal-time

• Interoperabillity intheserviceslayer• Conclusion3.Fulfillingmerchantneeds

• Infrastructure• Instantpaymentsolutions• Suitabilityofinstantpayments

2.Instantpaymentsoftoday

1.Themerchantperspective

22 Themerchant view:frominstant paymenttoinstantcommerce©|Frankfurt3May2016InnopayBV.Allrightsreserved.Source:Innopayanalysis,Euro BankingAssociation(EBA),European CentralBank(ECB)

Webshop

SCT,SDD,Cards

ACH,Visanet,Banknet

RealTimeGrossSettlement

Instruments

Processing

Settlement

CUSTOMER

ISSUINGBANK

ServicesInfrastructure

MERCHANT

ACQUIRINGBANK

SELECTION/AGREEMENT PAYMENT DELIVERY CUSTOMERCAREORIENTATIONBrowser

Onlinebanking

Webshop

Routingservice

Onlinepymntprovider

Merchant

account

Custom

er

account

Instantclearing&settlement

1.‘Instantpayments’mustconnectwiththeinstantcommerceprocess

FundsFundsInformation

MinimizemigrationmerchanteffortthroughAPIIntegrationinexistingchannels:PSP,plugin’sandotherFintech players

23 Themerchant view:frominstant paymenttoinstantcommerce©|Frankfurt3May2016InnopayBV.Allrightsreserved.Source:Innopayanalysis,Euro BankingAssociation(EBA),European CentralBank(ECB)

Webshop

Information Funds

SCT,SDD,Cards

ACH,Visanet,Banknet

RealTimeGrossSettlement

Instruments

Processing

Settlement

Instantclearing&settlement

ServicesInfrastructure

Custom

er

account

Merchant

account

Browser

Onlinebanking

Webshop

Routingservice

Onlinepymntprovider

ISSUINGBANK

CUSTOMER MERCHANT

ACQUIRINGBANK

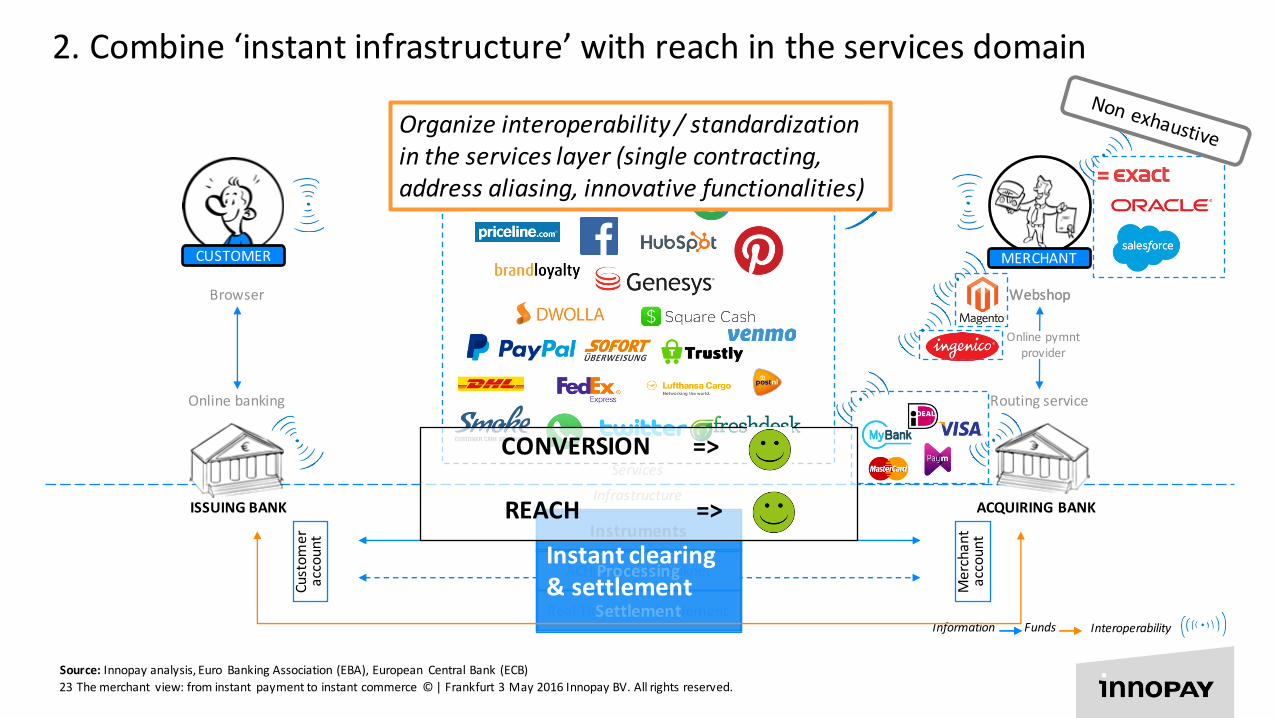

2.Combine‘instantinfrastructure’withreachintheservicesdomain

CONVERSION =>

REACH =>

Interoperability

Organizeinteroperability/standardizationintheserviceslayer(singlecontracting,addressaliasing,innovativefunctionalities)

24 Themerchant view:frominstant paymenttoinstantcommerce©|Frankfurt3May2016InnopayBV.Allrightsreserved.

Onemorething:inspirationfromIndia

Mobiles

E-wallets

Web

Pointofsale(POS)

Thirdpartyapps

Persontoperson(p2p)payments

PayingmerchantsPayingbillers Business toBusiness

(B2B)Payments

NPCI– UniversalElectronicPayments

UnifiedPaymentInterface(UPI)

PrescheduledRecurringPayments

UsingmobileasaprimarydeviceforallpaymentsUnifiedPaymentsInterface

TheIndianproject“UnifiedPayments Interface”isanexcellentexampleofthecombinationofboth‘reach’intheinfrastructureand‘conversion’throughinnovativefunctionalitiesviathemobilechannel

Formoreseehere

tomorrow’stransactionstoday

ThankyouForyourattention

Douwe Lycklamafounder/partner

[email protected]+31655711150

www.innopay.com

Open Forum on Pan-European Instant Payments, 3rd May 2016

Discussion and exchange of views on non-scheme issues

Open Forum on Pan-European Instant Payments, 3rd May 2016

Closing remarks

Hansjörg Nymphius

Advisor to the Board

Euro Banking Association

Open Forum on Pan-European Instant Payments, 3rd May 2016

• When: Tuesday, 7th June 2016, from 8:00 to 9:45

CET (meeting precedes the opening of EBAday)

• Where: Milano Congressi (MiCo) Conference

Centre, Milan

• Possible topics:

– Potential adoption of instant payments as

services become available

– Expected use cases in the P2P and B2B area

– Consultation phase on SCTinst: where do we

stand?

Next meeting

Open Forum on Pan-European Instant Payments, 3rd May 2016

For any comments or questions, please contact us at