Embed Size (px)

Citation preview

Financial Analyst Conference 2018

Olten, 26 March 2018

Agenda

1. Demanding environment 2. European business supports Swiss production 3. Financial results 4. Focus on core business 5. Outlook 6. Questions and answers

2 2 Alpiq Holding Ltd. Financial Analyst Conference 2018

3

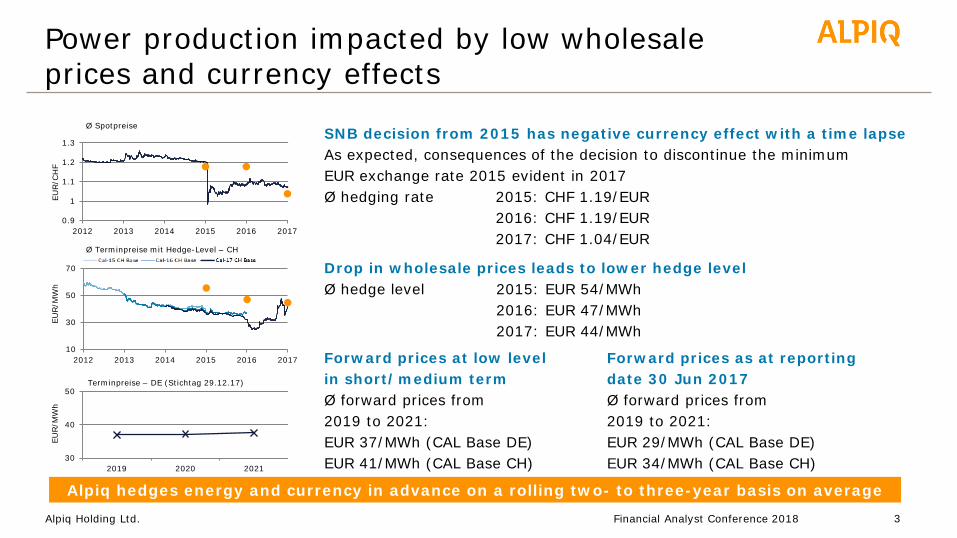

Power production impacted by low wholesale prices and currency effects

Alpiq Holding Ltd.

Alpiq hedges energy and currency in advance on a rolling two- to three-year basis on average

Forward prices at low level in short/medium term Ø forward prices from 2019 to 2021: EUR 37/MWh (CAL Base DE) EUR 41/MWh (CAL Base CH)

Drop in wholesale prices leads to lower hedge level Ø hedge level 2015: EUR 54/MWh 2016: EUR 47/MWh 2017: EUR 44/MWh

10

30

50

70

2012 2013 2014 2015 2016 2017

EUR/M

Wh

Ø Terminpreise mit Hedge-Level – CH

0.9

1

1.1

1.2

1.3

2012 2013 2014 2015 2016 2017

EUR/C

HF

Ø Spotpreise

30

40

50

2019 2020 2021

EUR/M

Wh

Terminpreise – DE (Stichtag 29.12.17)

Forward prices as at reporting date 30 Jun 2017 Ø forward prices from 2019 to 2021: EUR 29/MWh (CAL Base DE) EUR 34/MWh (CAL Base CH)

SNB decision from 2015 has negative currency effect with a time lapse As expected, consequences of the decision to discontinue the minimum EUR exchange rate 2015 evident in 2017 Ø hedging rate 2015: CHF 1.19/EUR 2016: CHF 1.19/EUR 2017: CHF 1.04/EUR

Financial Analyst Conference 2018

Asymmetry on the Swiss electricity market distorts competition

Alpiq Holding Ltd. 4

Power production operating at a loss in the partially liberated Swiss market

Taxes and duties Amortisation and financing Operation and maintenance

Decommissioning and waste disposal funds

1 ElCom (2017), median values 2 Swisselectric

Compensatory feed-in remuneration

Grid utilisation fee Duties

Energy price

3 Gösgen and Leibstadt nuclear power plants five-year average with long-term fund performance 4 Cal-17 Baseload CH (average from 1 Jan 2016 to 31 Dec 2016)

Hydropower production costs2

End customer price (household) in regulated Swiss market (including grid and compensatory feed-in remuneration)1

Wholesale price4

Energy price for end customers in regulated market1

Nuclear power production costs3

Nuclear power Hydropower Regulated end customer price

20.2 Rp/kWh

7.6 Rp/kWh

3.5 Rp/kWh

6.5 Rp/kWh 5.2 Rp/kWh

Financial Analyst Conference 2018

European business supports Swiss production

• Net debt reduced from CHF 0.9 billion to CHF 0.7 billion • Liquidity of CHF 1.4 billion at sound level

• International energy business generates more than 60% of earnings • Swiss business impacted by wholesale prices and currency effects

• Spin-off and sale of the industrial business creates added value and strengthens core business

• No more net debt thanks to sales proceeds of CHF 850 million

• Alpiq increases net revenue to CHF 7.2 billion • EBITDA before exceptional items of CHF 301 million

5 Alpiq Holding Ltd. 5

Financial Analyst Conference 2018

2017 Key Financial Figures

6 Alpiq Holding AG

Results of operations before exceptional items (EI) • Higher net revenue mainly attributable to trading and sales activities in Market France • As announced, EBITDA of CHF 301 million down on the previous year • Operating Cash Flow significantly improved, i.a. due to active capital management • Net debt reduction of CHF 142 million compared to the end of 2016

Net debt EBITDA Net revenue Net income Operating cash flow

+18%

7,173

82

6,078 301

395

1

-24%

>-100%

-33 9

115

>100%

329

94

-17%

714 856

CH

F m

illio

n

Financial Analyst Conference 2018

2016 FX effect

2017 2016 FX effect

2017 2016 FX effect

2017 2016 2017 31 Dec 2016 31 Dec 2017

Development of EBITDA Results from Swiss electricity production lowers results

7 Alpiq Holding AG

301300395

EBIT

DA 2

016

befo

re E

I

-24%

EBIT

DA 2

017

befo

re E

I

FX e

ffec

t

1

EBIT

DA 2

017

befo

re E

I an

d FX

effec

t

Variou

s

3

Cos

t re

duct

ion

and

effic

ienc

y im

prov

emen

t

9

Got

thar

d pr

ojec

t 20

16

-7

Trad

ing

&

Com

mer

ce

39

Inte

rnat

iona

l Th

erm

al P

rodu

ctio

n &

RES

9

Prod

uctio

n vo

lum

es

Port

folio

Sw

itzer

land

-16

KKL

dow

ntim

e

-11 Pr

ice

effe

ct

-44

FX H

edge

s -77

CH

F m

illio

n

Financial Analyst Conference 2018

EBITDA development by business division (I) Generation Switzerland burdened by external factors

8 Alpiq Holding AG

Generation Switzerland • Negative exchange rate effects caused by expiring hedges • Wholesale prices below production costs • Unscheduled extension of the maintenance work and an

imposed power reduction at the Leibstadt nuclear power plant

• Lower production volumes Results of partner power plants (consolidated in full and using the equity method) include O&M, amortisation and depreciation, taxes and fees as well as capital costs, either at the partner power plant or at Alpiq directly

1

EBIT

DA

2017

be

fore

EI

FX e

ffec

t 144

27

-118

Bus

ines

s de

velo

pmen

t

EBIT

DA

2016

be

fore

EI

-180 Res

ult

Gen

erat

ion

Sw

itzer

land

CH

F m

illio

n

Financial Analyst Conference 2018

Building Technology & Design • Significant increase in order intake and order backlog • Decrease in EBITDA attributable to the successful completion of the

Gotthard Base Tunnel project in the previous year • Positive contribution to earnings from acquisition of Lundy Projects Ltd.

EBITDA development by business division (II)

9 Alpiq Holding AG

Industrial Engineering • Contributions from Thermal Production and RES up on the previous year • Margins in energy and power plant technology down on the previous year • Increasing demand in the area of dismantling nuclear facilities

158 158

4 -4

EBIT

DA

2016

be

fore

EI

56

1

FX e

ffec

t

63

-8

Bus

ines

s de

velo

pmen

t

EBIT

DA

2017

be

fore

EI

CH

F m

illio

n CH

F m

illio

n

56

21

39

-4 Digital & Commerce • Successful use of price volatilities in Italy and Eastern Europe • Sales activities in Market France up on the previous year • Optimisation of power plant portfolio in CH and Spain below previous year • No contribution form AVAG after disposal in July 2016 C

HF

mill

ion

Financial Analyst Conference 2018

Increased contribution from thermal production and RES Stronger results from international production Negative exchange rate effects caused by expiring hedges, wholesale prices below production costs

Continuing operations Swiss production supported by European business

10 Alpiq Holding AG

CH

F m

illio

n

EBITDA before EI continuing operation

245

2017 2016

325

Therm. Production / RES Digital & Commerce Generation Switzerland

Financial Analyst Conference 2018

Discontinued operations EBITDA 2017 Bridge

11 Alpiq Holding AG

8574 11

EBITDA 2017 before EI incl. IAS 19

EBITDA 2017 before EI stand-alone true & fair view

Various Adjustments incl. IAS 19

Equivalent of EBIT Bridge incl. CHF 23 million depreciation and amortisation

CH

F m

illio

n

Financial Analyst Conference 2018

Development of financial result Financial result up to previous year

12

-91

-123

Fina

ncia

l res

ult

2017

be

fore

EI

FX e

ffec

t

9

Fina

nce

cost

s

20

Fina

nce

inco

me

3

Fina

ncia

l res

ult

2016

be

fore

EI

CH

F m

illio

n

Reduced interest burden due to lower financial debt

Alpiq Holding AG Financial Analyst Conference 2018

Development of net income

13

115

-42 -33

2322

-100

Net

inco

me

2017

be

fore

EI

FX e

ffec

t

9

Net

inco

me

2017

be

fore

EI

and

FX e

ffec

t

Inco

me

tax

expe

nse

-12

Fina

ncia

l res

ult

Sha

re o

f re

sults

of

part

ner

pow

er p

lant

s an

d ot

her

asso

ciat

es

Dep

reci

atio

n,

amor

tisat

ion

and

impa

irm

ent

4

Del

ta a

t EB

ITD

A

leve

l bef

ore

EI

-94

Net

inco

me

2016

be

fore

EI

CH

F m

illio

n

Current income tax expense: • higher tax expense on account

of higher earnings

Alpiq Holding AG

Deferred income tax expense: • one-off effect from tax rate reduction

in previous year • Fewer tax loss carryforwards

recognised • Higher deferred tax liabilities from

temporary measurement differences

Financial Analyst Conference 2018

Change in cash flow from operating activities 2017 compared to 2016

14 Alpiq Holding AG

CH

F m

illio

n

151

95

83

329

94

Cas

h flo

w f

rom

op

erat

ing

activ

ities

20

17

Bal

ance

she

et

man

agem

ent

Com

pens

atio

n fr

om

Swis

sgrid

in 2

017

Paym

ent

due

to

chan

ge in

met

hod

nucl

ear

fund

s 20

16

Dep

ress

ed

oper

atin

g pr

ofita

bilit

y (E

BIT

DA b

efor

e EI

) -94

Cas

h flo

w f

rom

op

erat

ing

activ

ities

20

16

Financial Analyst Conference 2018

Statement of cash flows

15

329 -291 -78

Rep

aym

ent

of

finan

cial

liab

ilitie

s

-38

Inte

rest

pai

d

49

Dis

trib

utio

n to

hy

brid

inve

stor

s/

Div

iden

d pa

id

1,403

Cur

renc

y tr

ansl

atio

n di

ffer

ence

s

Liqu

idity

as

at

31 D

ec 2

017

Proc

eeds

fro

m

disp

osal

s

52

Div

iden

ds f

rom

pa

rtne

r po

wer

pla

nts

and

inte

rest

rec

eive

d

41

CAPE

X

-185 Cas

h flo

w f

rom

op

erat

ing

activ

ities

Liqu

idity

as

at

1 Ja

n 20

17

1,524

CH

F m

illio

n

Alpiq Holding AG

• Purchase of Lundy Projects Ltd. • Capital increase Nant de Drance SA • Investments in fixed assets

Financial Analyst Conference 2018

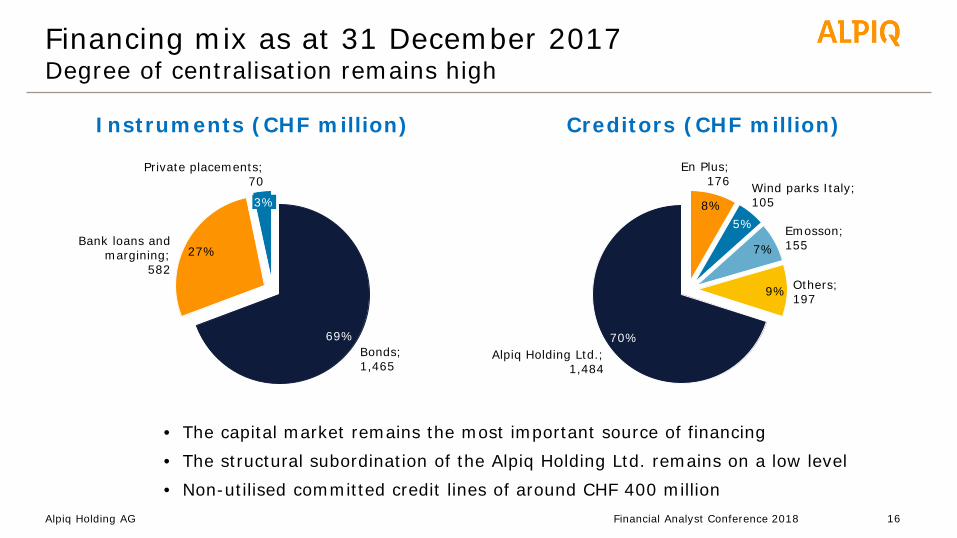

Financing mix as at 31 December 2017 Degree of centralisation remains high

16 Alpiq Holding AG

Creditors (CHF million) Instruments (CHF million)

• The capital market remains the most important source of financing • The structural subordination of the Alpiq Holding Ltd. remains on a low level • Non-utilised committed credit lines of around CHF 400 million

69% Bonds; 1,465

Private placements; 70

3%

Bank loans and margining;

582 27%

9%

70%

Others; 197

5%

Alpiq Holding Ltd.; 1,484

Wind parks Italy; 105

7% Emosson; 155

8%

En Plus; 176

Financial Analyst Conference 2018

Maturity profile as at 31 December 2017 Financial liabilities staggered over long term

17 Alpiq Holding AG

• Maturities are countered by a sound liquidity base of around CHF 1.4 billion • Maturity profile staggered over long term without significant spikes • Further systematic reduction of debt in the pipeline

358

2027ff 2026 2025

50

2024

336

2023 2022

224 390

2021

313

2020

105

2019

318

2018

338

31 Dec 17

1,403

Bonds Private placements Bank loans and margining Liquidity

Total: CHF 2,117 million

CH

F m

illio

n

Financial Analyst Conference 2018

Financial liabilities Debt situation improved significantly

18 Alpiq Holding AG

• Net debt further reduced by CHF 142 million to CHF 714 million • Net debt/EBITDA before exceptional items of 2.4

714856301395480609796997

2.42.22.7

3.2

2.6

4.0

3,989

2017 2016 2015

1,299

2014

1,939

2013

2,050

2012

Net debt/EBITDA before exceptional items EBITDA before exceptional items Net debt

CH

F m

illio

n

Financial Analyst Conference 2018

Development debt situation after closing of the transaction

19 Alpiq Holding AG

• Sales proceeds for InTec and Kraftanlagen Group of CHF 850 million • Net debt becomes Net liquidity of CHF 136 million

358

850

2027ff 2026 2025

50

2024

336

2023

224

2022

390

2021

313

2020

105

2019

318

2018

338

Liquidity

2,253

1,403

Gross debt

2,117

Bonds Private placements Bank loans and margining

CH

F m

illio

n

Financial Analyst Conference 2018

Balance Sheet remains stable Alpiq with sound liquidity and stable equity

20 Alpiq Holding AG

• Sound liquidity: CHF 1.4 billion

• Stable equity: CHF 4.0 billion

• Equity ratio at 38.9%

42%

38.9%

61%

39% 58%

7%

54%

39%

38.8%

12%

33%

55%

Non-current assets

Assets held for sale Total equity Equity ratio

Liabilities Current assets

2016 2017

10,008 10,197

Financial Analyst Conference 2018

Tax audit in Romania

• Assessment of Alpiq Energy SE, Prague, issued by Romanian tax authority ANAF in the amount of RON 793 million (CHF 199 million) for the period of 2010 to 2014

• Alpiq has contested on account of its reasoning and the extent of the amount assessed

• Alpiq currently deems it unlikely that this assessment will result in a negative outcome for the company

No liability (provision) of RON 793 million recognised; secured by a bank guarantee in the amount of CHF 202 million; disclosed under non-current term deposits

21 Alpiq Holding AG Financial Analyst Conference 2018

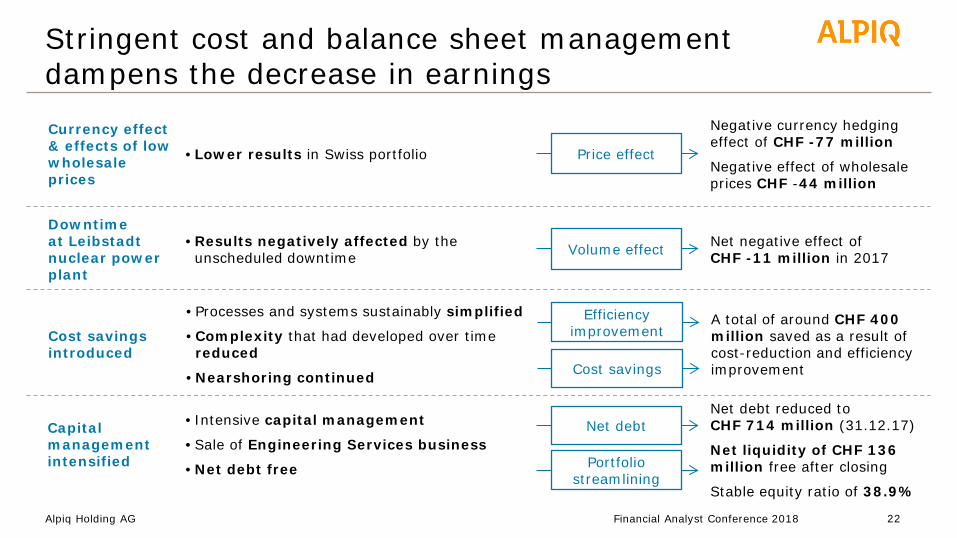

Stringent cost and balance sheet management dampens the decrease in earnings

22 Alpiq Holding AG

Cost savings introduced

• Processes and systems sustainably simplified

• Complexity that had developed over time reduced

• Nearshoring continued

Efficiency improvement

A total of around CHF 400 million saved as a result of cost-reduction and efficiency improvement Cost savings

• Lower results in Swiss portfolio

Currency effect & effects of low wholesale prices

Negative currency hedging effect of CHF -77 million

Negative effect of wholesale prices CHF -44 million

Price effect

Capital management intensified

• Intensive capital management

• Sale of Engineering Services business

• Net debt free

Net debt Net debt reduced to CHF 714 million (31.12.17)

Net liquidity of CHF 136 million free after closing

Stable equity ratio of 38.9%

Portfolio streamlining

• Results negatively affected by the unscheduled downtime

Downtime at Leibstadt nuclear power plant

Net negative effect of CHF -11 million in 2017 Volume effect

Financial Analyst Conference 2018

Alpiq splits off industrial business for CHF 850 million

23 Alpiq Holding Ltd.

Building Technology & Design InTec Group

Digital & Commerce

1,550 employees

Industrial Engineering Kraftanlagen Group

Generation Switzerland

7,650 employees, of which 4,420 are in Switzerland

Transaction creates significant added value for the Alpiq Group and strengthens its core business

New prospects with international industrial owner

International thermal power production New renewable energies

Financial Analyst Conference 2018

Customers Marketing

24 Alpiq Holding Ltd.

New renewable energies

Grid operators

Swiss production

Industry and commerce

International thermal production

Alpiq focuses on the core business

Production

International electricity trading

Origination and retail

Digital solutions

Digital & Commerce

Decentralised production by third parties

Prosumer

Asset optimisation

Utilities

Financial Analyst Conference 2018

2018 remains challenging

• Low wholesale prices continue to put Swiss production under pressure

• Slight relief for Swiss hydropower through market premium

• International energy business generates positive contributions to support Swiss production

25 Alpiq Holding Ltd. Financial Analyst Conference 2018

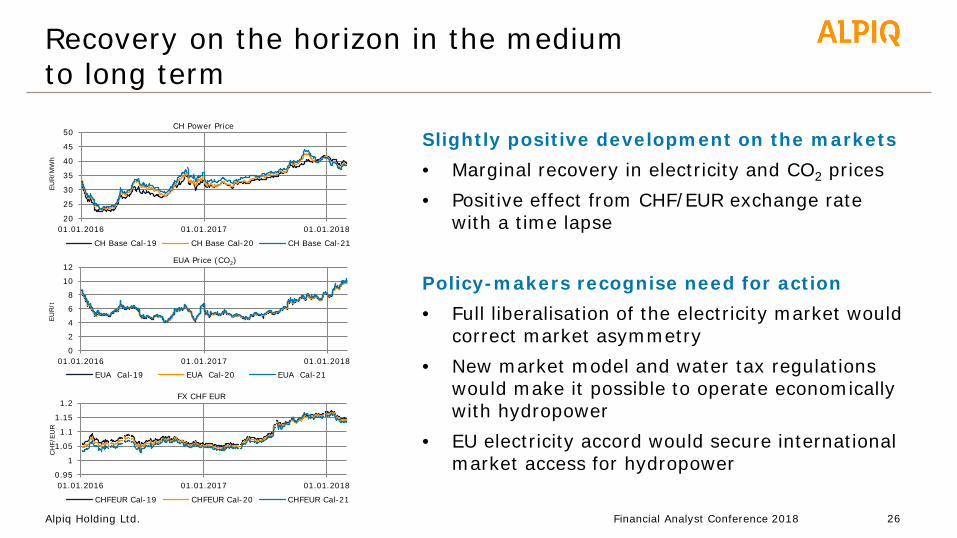

Recovery on the horizon in the medium to long term

26 Alpiq Holding Ltd.

Slightly positive development on the markets • Marginal recovery in electricity and CO2 prices • Positive effect from CHF/EUR exchange rate

with a time lapse

Policy-makers recognise need for action • Full liberalisation of the electricity market would

correct market asymmetry • New market model and water tax regulations

would make it possible to operate economically with hydropower

• EU electricity accord would secure international market access for hydropower

0

2

4

6

8

10

12

01.01.2016 01.01.2017 01.01.2018

EUR/t

EUA Price (CO2)

EUA Cal-19 EUA Cal-20 EUA Cal-21

0.95

1

1.05

1.1

1.15

1.2

01.01.2016 01.01.2017 01.01.2018

CH

F/EU

R

FX CHF EUR

CHFEUR Cal-19 CHFEUR Cal-20 CHFEUR Cal-21

20

25

30

35

40

45

50

01.01.2016 01.01.2017 01.01.2018

EUR/M

Wh

CH Power Price

CH Base Cal-19 CH Base Cal-20 CH Base Cal-21

Financial Analyst Conference 2018

Alpiq is fit for the future

27 Alpiq Holding Ltd.

• Successful divestment creates significant added value for the Group

• No more net debt thanks to sale proceeds of CHF 850 million

• Focus on core business: Generation Switzerland, Digital & Commerce, international thermal production, new renewable energies

• Positive developments on markets (electricity/CO2 prices) and regarding regulation (hydropower) in the medium/long term

• Opportunities in the areas of decarbonisation, decentralisation and digitalisation

Financial Analyst Conference 2018

You ask. We answer.

Organisation prior to closing

General Management CEO Jasmin Staiblin1

Generation Switzerland Michael Wider1

Digital & Commerce Markus Brokhof1

Industrial Engineering Reinhold Frank1

Building Technology & Design Peter Limacher1

Financial Services CFO Thomas Bucher1

Hydro Power Generation Christian Plüss

Nuclear Power Generation Michaël Plaschy

smart Energy West Michel Kolly

smart Energy East Peter Dworak

Nuclear Decommissioning Hans Genthner

Power & Heat Matthias Zwicky

Building Technologies Switzerland Peter Limacher

Building Technologies Europe Javier Romero

Accounting & Controlling Edgar Lehrmann

Taxes Eva Catillon

Legal & Compliance Peter Schib

Human Resources Daniel Huber

Digital Technologies & Innovation Hans Dahlberg

Operations Petter Torp

Industrial Plants Reinhold Frank

Renewable Energy Sources André Schnidrig

Treasury & Insurance Lukas Oetiker

M&A and Infrastructure Martin Schindler

Communications & Public Affairs Richard Rogers

Risk Management Walter Hollenstein

Transportation Thomas Rapp

Business Division

Business Unit

Functional Division

Functional Unit

1) Member of the Executive Board

General Management

Alpiq Holding Ltd. 29 Financial Analyst Conference 2018

Financial calendar 2018

16 May 2018 9th Annual General Meeting of Alpiq Holding Ltd. (Lausanne)

27 August 2018 Interim results 2018 (Olten)

Media Breakfast and Analyst Conference Call

30 Alpiq Holding Ltd. Financial Analyst Conference 2018

Disclaimer

This communication contains, among other things, forward-looking statements and information. Such statements include, but are not limited to, statements regarding management objectives, business profit trends, profit margins, costs, returns on equity, risk management or the competitive environment, all of which are inherently speculative in nature. Terms such as "anticipate," "assume," "aim," "goals," "projects," "intend," "plan," "believe," "try," "estimate," and variations of such terms, and similar expressions have the purpose of clarifying forward-looking statements. These statements are based on our current estimates and assumptions, and are therefore to some extent subject to risks and uncertainties. Therefore, Alpiq's actual results may differ materially from, and substantially contradict, forward-looking statements made expressly or implicitly. Factors contributing to or likely to cause such divergent outcomes include, but are not limited to, the general economic situation, competition with other companies, the effects and risks of new technologies, the Company's ongoing capital needs, financing costs, delays in integrating mergers or acquisitions, changes in operating expenses, currency fluctuations, changes in the regulatory environment on the domestic and foreign energy markets, oil price and margin fluctuations for Alpiq products, attracting and retaining qualified employees, political risks in countries where the Company operates, changes in applicable law, the realisation of synergies and other factors mentioned in this communication.

Should one or more of these risks, uncertainties or other factors materialise, or should any of the underlying assumptions or expectations prove incorrect, the results may differ materially from those stated. In light of these risks, uncertainties or other factors, the reader should not rely on such forward-looking statements. The Company does not assume any obligation beyond those arising out of law to update or revise such forward-looking statements, or to adapt them to future events or developments. The Company points out that past results are not meaningful in terms of future results. It should also be noted that interim results are not necessarily indicative of the year-end results.

This communication is neither an offer nor an invitation to sell or buy securities.

31 Alpiq Holding Ltd. Financial Analyst Conference 2018

Appendix

32 Alpiq Holding AG Financial Analyst Conference 2018

Development of net revenue

279

640

+18%

Net

rev

enue

201

7 be

fore

EI

7,173

FX e

ffec

t

82

Net

rev

enue

201

6 be

fore

EI

smar

t En

ergy

Wes

t (m

ainl

y M

arke

t Fr

ance

)

6,078

-39

Sal

e of

AVA

G

213

smar

t En

ergy

Eas

t

Net

pos

ition

s on

sp

ot e

xcha

nges

(v

olum

e im

pact

)

-9

Bui

ldin

g Te

chno

logy

&

Des

ign

Net

rev

enue

201

7 be

fore

EI

and

FX e

ffec

t

-17

Indu

strial

Eng

inee

ring

-54

Variou

s

7,091

CH

F m

illio

n

Alpiq Holding AG 33 Financial Analyst Conference 2018

Development of EBIT

34

11411539

204 -7

Got

thar

d pr

ojec

t 20

16

Variou

s

Prod

uctio

n vo

lum

es

Port

folio

Sw

itzer

land

3

-16 9

Trad

ing

&

Com

mer

ce

FX H

edge

s

Dep

reci

atio

n,

amor

tisat

ion

and

impa

irm

ent

EBIT

201

7 be

fore

EI

and

FX e

ffec

t

EBIT

201

7 be

fore

EI

-44

KKL

dow

ntim

e

6

Cos

t re

duct

ion

and

effic

ienc

y im

prov

emen

t

-1

EBIT

201

6 be

fore

EI

9

-77

FX e

ffec

t

-11

Pric

e ef

fect

Inte

rnat

iona

l Th

erm

al P

rodu

ctio

n &

RES

CH

F m

illio

n

Alpiq Holding AG Financial Analyst Conference 2018

Shareholder structure as at 31 December 2017

35

Free float

12%

WWZ

1% IBAarau

2% AIL 2%

Canton Solothurn 6%

EBL 7%

EBM 14%

EdF

25%

EOS Holding 31%

Number of shares outstanding: 27,874,649

Consortium of Swiss minority shareholders (KSM): 31.43 %

Alpiq Holding AG Financial Analyst Conference 2018