Embed Size (px)

Citation preview

OIL PRICES AND THE WORLD ECONOMY

Ray Barrell and Olga PomerantzNIESR

November 2004

Introduction

• Oil price increases and inflation were associated in the 1970’s and 1980’s– What factors affect oil prices– What makes oil prices ‘cause’ inflation– How do higher oil prices affect the level

of output

• Why is the world different

What affects output and inflation

• The oil intensity of production • Nominal inertia in wages and prices• The monetary policy response• The speed of recycling oil revenues into

demand• Patterns of trade have an important

influence

What should modellers and forecasters look at

• Temporary and permanent shocks differ– Expectations influence the impact of shocks– The effects on long term interest rates differ

• The use of oil revenues influences outcomes– Oil shocks redistribute income flows– The effects on trade in goods and services

determine the pattern of effects – So include oil producers and trade in services

The Role of OPEC

• OPEC is a lead producer, but it only sets a floor to prices– A positive output gap in the OECD puts

upward pressure on prices • Real oil prices display dollar inertia

because OPEC sets dollar prices– The real oil price is influenced by movements

in the dollar real exchange rate– Recent price increases have been much less

marked in euros

Oil Intensity

• The amount of oil per unit of GDP has been falling since 1975– In Europe oil intensity has fallen by one third since

1982– In the US oil intensity has fallen by as much

• Oil intensity is now 60 per cent higher in the US than in the major Euro Area countries

• The first round effect on output and prices must be higher in the US

Oil Intensity of Output(barrels of oil per unit of real output at 1994 PPPs)

0.400

0.500

0.600

0.700

0.800

0.900

1.000

1.100

1.200

1.300

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

France Germany UK US

Oil as per cent of total energy supply

10

15

20

25

30

35

40

45

50

55

60

1982 1984 1986 1988 1990 1992 1994 1996 1998 2000

OECD North America Europe Pacific

non-OECD China Other Asia Latin America

Oil Prices and Trade

• Oil prices affect the terms of trade– Higher dependence on oil imports raises the

impact on GDP• The impact on saving and investment is greater• Tax revenues and solvency are affected

• Patterns of OPEC (Russian, Norwegian) imports affect the pattern of trade impacts– The US has 22% of world GDP but only 11

percent of major oil exporters imports

World Tade in Oilimport share less export share

-0.4

-0.3

-0.2

-0.1

0

0.1

0.2

0.3

Euro A

rea

Other E

U countries

US

Other N

. Am

erica

JP Other A

sia

LA OP

EC

DE

Russia

Norw

ay

Transition countries

All other

US22%

Japan7%

Euro Area17%UK

3%

Asia excl. Japan24%

Other27%

US11%

Japan7%

Euro Area26%

UK6%

Asia excl. Japan18%

Other32%

Share of World GDP

(at PPPs), 2000

Share of Oil Producers’Imports, 2000

The role of the labour market

• An increase in the oil price reduces equilibrium income for each level of output

• Real wages need to fall – Bargaining institutions may resist and induce a recession– The central bank may allow inflation to reduce output costs – There may be asymmetries between upward and downward

shocks • Labour market institutions are now more flexible than

in the 1970s because of reforms• Bargainers realise that real wages must change• Hunt and Laxton NIER 2002 discuss these issues

Oil Prices and NiGEM

• The model is an estimated new Keynesian description of the world economy– Almost all OECD countries are covered– OPEC, and other regions are included– Trade and financial markets cover the world– Each country has a demand and supply

structure with a government sector– Financial, exchange rate and labour markets

have forward looking expectations

Monetary Policy Rules

• All countries must have monetary policy • We have an ECB strategy with a nominal

aggregate and inflation as targets

• We also have a Taylor Rule (TR) whose coefficients can change

• They have different implications for prices as TR treats inflation misses as a bygone

*)loglog()*)log()(log( 21 jtjtttttt PPYPYPr ++ ∆−∆+−= γγ

021 *)loglog(*)log(log γγγ +∆−∆+−= ++ jtjtttt PPYYr

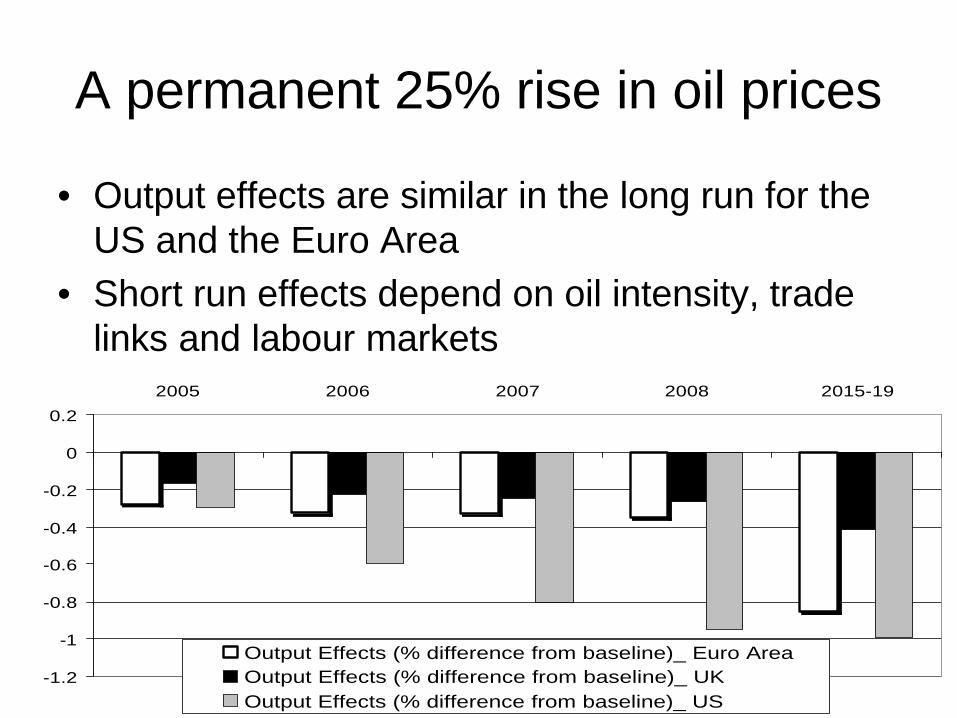

A permanent 25% rise in oil prices

• Output effects are similar in the long run for the US and the Euro Area

• Short run effects depend on oil intensity, trade links and labour markets

-1.2

-1

-0.8

-0.6

-0.4

-0.2

0

0.2

2005 2006 2007 2008 2015-19

Output Effects (% difference from baseline)_ Euro AreaOutput Effects (% difference from baseline)_ UK Output Effects (% difference from baseline)_ US

Impacts on Output of a 25% permanent rise in oil prices

-1

-0.9

-0.8

-0.7

-0.6

-0.5

-0.4

-0.3

-0.2

-0.1

0

France Germany Japan UK US

2005 2006 2007 2008

% difference from baseline

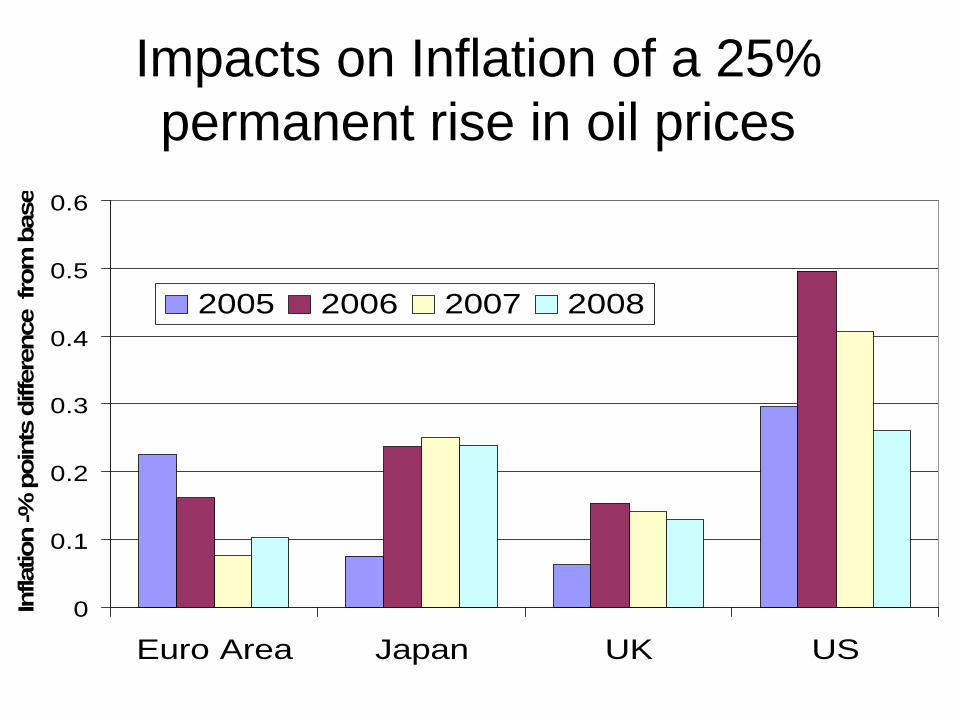

Impacts on Inflation of a 25% permanent rise in oil prices

0

0.1

0.2

0.3

0.4

0.5

0.6

Euro Area Japan UK US

Infla

tion -%

poin

ts d

iffer

ence

fro

m b

ase

2005 2006 2007 2008

Long term effects of a 25% permanent rise in real oil prices

• Higher oil prices change the terms of trade for the OECD as a whole

• The saving investment balance has to change

• Real interest rates have to rise, and output will be lower in the long run

• The rise in long term real interest rates will affect output now

The impact of a 25% permanent real oil price increase on long rates

0

0.05

0.1

0.15

0.2

0.25

0.3

Euro Area longrate

Euro Area longreal rate

US Long Rate US long real ratePer

cent

age

poin

ts d

iffe

renc

e fr

om b

ase

2005 2006 2007

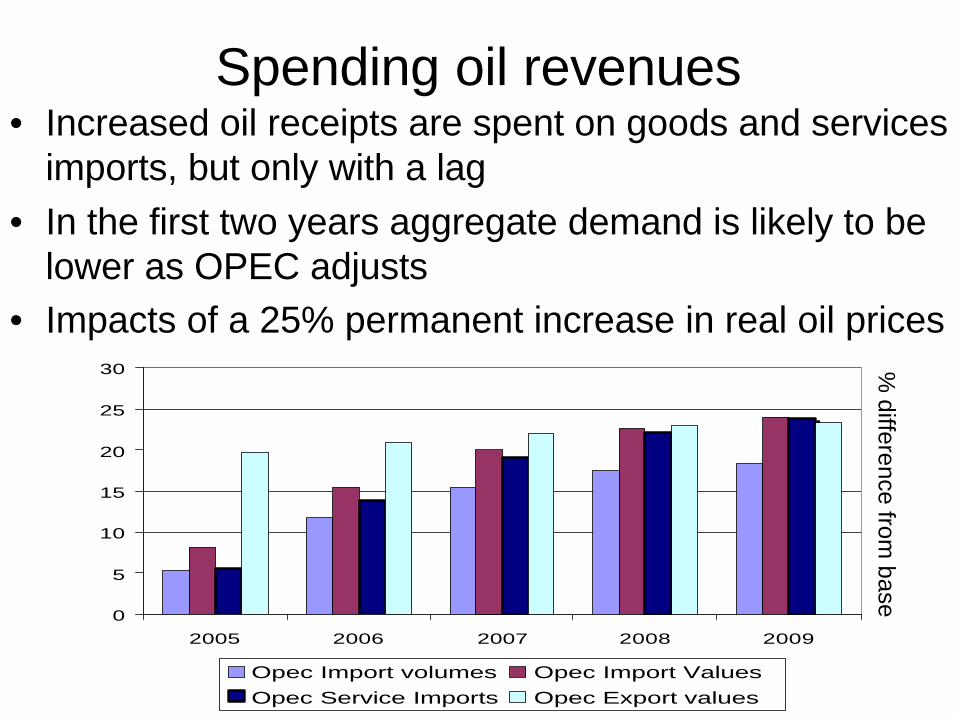

Spending oil revenues• Increased oil receipts are spent on goods and services

imports, but only with a lag• In the first two years aggregate demand is likely to be

lower as OPEC adjusts• Impacts of a 25% permanent increase in real oil prices

0

5

10

15

20

25

30

2005 2006 2007 2008 2009

Opec Import volumes Opec Import ValuesOpec Service Imports Opec Export values

% difference from

base

Slower spending of oil receipts

• Until 1985 OPEC recycled money into goods at half the speed they now spend at so we cut the speed of reaction to half its level

• Output effects of an oil price shock increase, especially in inertial Europe

-1.2

-1

-0.8

-0.6

-0.4

-0.2

0

2005 2006 2007 2008 2009

Euro Area Base Euro Area Slow US Base US Slow

Output %difference from base

Impact of slower spending of oil revenues of trade

0

5

10

15

20

25

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

% d

iffer

ence

from

bas

elin

e

Opec imports - fast Opec imports - slow

-2.5

-2

-1.5

-1

-0.5

0 2005

2007

2009

2011

2013

2015

2017

2019

% d

iffe

ence

fro

m b

asel

ine

World trade - fast world trade - slow

The role of monetary policy

• Short run effects on output also depend on policy – a looser monetary stance can half the impact on output

• Inflation effects depend on wage price flexibility and the policy rule– A looser monetary stance must mean a

greater price impact– More real wage inflexibility raises the costs of

keeping price effects small

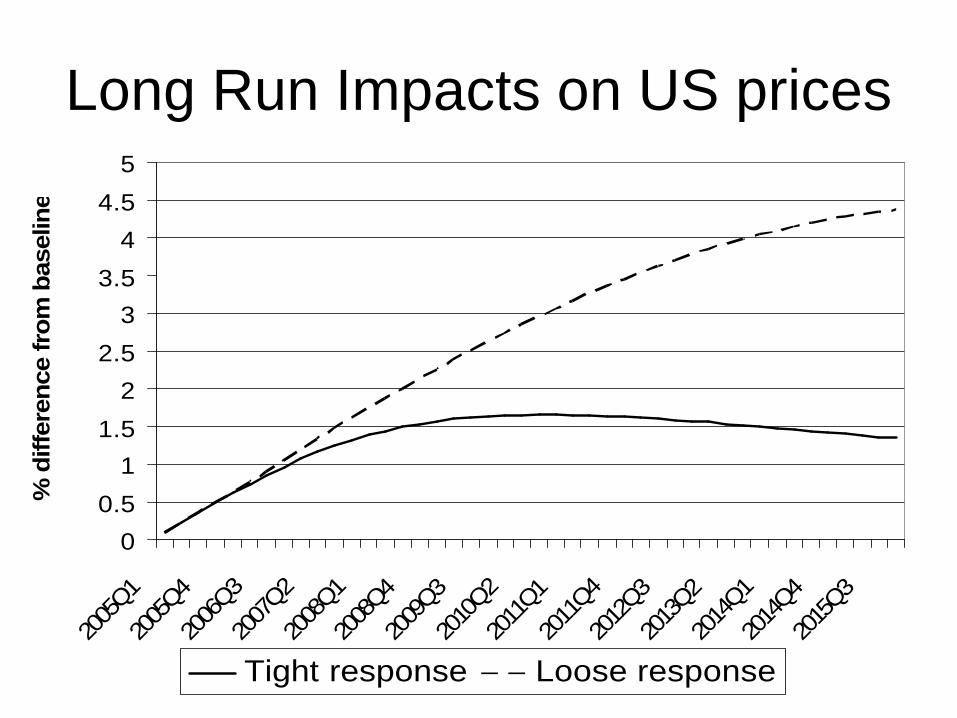

Changing Policy in the US• We compare our default with a looser response and

output effects are smaller in the short run • Inflation effects are larger after the first year and the

price level is noticeably higher in the long run than in the default Looser Monetary Policy in the US

Ratio of loose to tight

0.00

0.50

1.00

1.50

2.00

2.50

2004 2005 2006

Effects of Loosening policy (loose/tight) Inflation Effects of Loosening policy (loose/tight) Output

Long Run Impacts on US prices

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

5

2005

Q1

2005

Q4

2006

Q3

2007

Q2

2008

Q1

2008

Q4

2009

Q3

2010

Q2

2011

Q1

2011

Q4

2012

Q3

2013

Q2

2014

Q1

2014

Q4

2015

Q3

% d

iffer

ence

fro

m b

asel

ine

Tight response Loose response

Are temporary shocks different• We compare a permanent shock to a 2 year

shock under the same rules• Temporary shocks have less output effects

because real interest rates do not rise• Inflation effects can be larger as a result

-1.2

-1.0

-0.8

-0.6

-0.4

-0.2

0.0

0.2

0.4Inflation Output Inflation Output Inflation Output

Euro Area UK US

2004 2005

% difference temporaryand permanent shocks

Conclusions

• Higher oil prices lead to higher prices– Output should fall in the short and long run– Real interest rates should rise

• Wage price spirals worsen problems • Oil intensity is important for output effects• Inflation depends on the central bank

– Output effects can be reduced in the short run

• The speed of re-spending revenues on goods and services affects the impacts on output

SourcesMuch of the argument is contained in

Barrell and Pomerantz ‘Oil Prices and the World Economy’ NIESR Discussion Paper July 2004.

available at www.niesr.ac.ukAl Eyd et al ‘The world economy’ in National Institute Economic Review July and October

Information available at www.niesr.ac.uk

Contact Ray Barrell (rbarrell), Ian Hurst (aihurst) or Olga Pomerantz (opomerantz) @niesr.ac.ukfor details