Embed Size (px)

Citation preview

Oil Markets and the Global Economy

Christof Rühl, Global Head of Research

Abu Dhabi

February 2016

1

Outline

The economy: an age of stagnation and low returns?

Oil price recap

Why are lower oil prices not boosting economic growth?

Where next for oil markets?

2

“Secular Stagnation“ ?

3

Source: The Economist

0%

1%

1%

2%

2%

3%

US Germany Japan

1985-1994 1995-2004 2005-2014

Real interest rates and total factor productivity (TFP)

Yield

Real return on 10-year

Government bonds Average annual growth

TFP in Advanced Economies

4

Source: OECD Source: Haver

-3%

0%

3%

6%

9%

1983 '87 '91 '95 '99 '03 '07 '11 2015

US Germany Japan

Where is…

Oil price decline

5

20

30

40

50

60

70

80

90

100

110

120

Jan-14 Jul-14 Jan-15 Jul-15 Jan-16

Dated Brent

US dollars per barrel

Source: Bloomberg

July 2014

20

30

40

50

60

70

80

90

100

110

120

Jan-14 Jul-14 Jan-15 Jul-15 Jan-16

Dated Brent

Where is the “shot in the arm”?

Revisions to GDP growth projections 2015

GDP growth

Source: IMF

6

Oil price decline

US dollars per barrel

Source: Bloomberg

July 2014

0%

1%

2%

3%

4%

5%

6%

World US Advancedeconomies

Emergingeconomies

Jul-14 Jan-15 Jul-15 Oct-15

3

4

5

6

7

8

9

China Emerging World

Apr-13 Oct-15

Long term growth projections in emerging markets

Revisions to 5-year GDP growth forecast

Percent

Source: IMF WEO

-1.0pp

-2.2pp

-0.5pp

20

25

30

35

40

45

50

55

1990 1993 1996 1999 2002 2005 2008 2011 2014

China

Emerging excl. China

Source: BP Statistical Review

Share of global oil demand

Percent

7

Outline

The economy: an age of stagnation and low returns?

Oil price recap

Why are lower oil prices not boosting economic growth?

Where next for oil markets?

8

20

30

40

50

60

70

80

90

100

110

120

Jan-14 Jul-14 Jan-15 Jul-15 Jan-16

Dated Brent

Oil price vs. other commodities

US dollars per barrel

Daily oil price

Source: Bloomberg

High price band of

2011-2014 period

Low price band

post 2015

0

100

200

300

400

500

600

700

0

20

40

60

80

100

120

140

Jan-00 Jan-03 Jan-06 Jan-09 Jan-12 Jan-15

Dated Brent (lhs)

Industrial metals (rhs)

Oil and industrial metals prices

US Dollars per barrel

9

Source: Bloomberg

Index

Oil supply disruptions and US production growth

Cumulative change since 4Q10, Mb/d

-4

-3

-2

-1

0

1

2

3

4

5

1Q11 3Q11 1Q12 3Q12 1Q13 3Q13 1Q14 3Q14 1Q15 3Q15

Libya Iran Other US Net

3Q15

Source: Includes data from BP Statistical Review of World

Energy and BP Energy Outlook 10

Oil supply disruptions and US production growth

Cumulative change since 4Q10, Mb/d

-4

-3

-2

-1

0

1

2

3

4

5

1Q11 3Q11 1Q12 3Q12 1Q13 3Q13 1Q14 3Q14 1Q15

Libya Iran Other US Net

3Q15

Source: Includes data from BP Statistical Review of World

Energy and BP Energy Outlook 11

Oil supply disruptions and US production growth

Source: Includes data from BP Statistical Review of World

Energy and BP Energy Outlook

Cumulative change since 4Q10, Mb/d

12

-4

-3

-2

-1

0

1

2

3

4

5

1Q11 3Q11 1Q12 3Q12 1Q13 3Q13 1Q14 3Q14 1Q15

Libya Iran Other US Net

3Q15

TO CUT PRODUCTION?

YES

OIL PRICE HIGHER

U.S. SHALE PRODUCTION

HIGHER

OPEC LOSES MARKET SHARE

OPEC REVENUES

DECLINE

NO

OIL PRICE LOWER

U.S. SHALE PRODUCTION

LOWER

OPEC GAINS MARKET SHARE

OPEC REVENUES

DECLINE

OPEC’s dilemma

13

Outline

The economy: an age of stagnation and low returns?

Oil price recap

Why are lower oil prices not boosting economic growth?

Where next for oil markets?

14

(1) US Dollar is appreciating

Source: Bloomberg

Real trade weighted US Dollar index…

• Relatively strong US growth and

productivity gains

• The end of QE in the US

… rises for good reasons

19% real appreciation since July

2014 (26% since July 2011):

Index, Jan 1990 = 100

85

90

95

100

105

110

115

120

125

Jan-90 Jan-95 Jan-00 Jan-05 Jan-10 Jan-15

15

(2) Households are deleveraging...

Household debt as a share of GDP

Change in household

debt since peak:

- 4 percentage points

- 19 percentage points

40

50

60

70

80

90

100

1Q 99 1Q 01 1Q 03 1Q 05 1Q 07 1Q 09 1Q 11 1Q 13 1Q 15

US

Euro area

1Q 2008 = 97.9%

4Q 2009 = 64.6%

16

… while government debt hampers demand management

% of GDP

19

20

21

22

23

24

25

26

1990 1995 2000 2005 2010 2015

Investment in Advanced

Economies

% of GDP

60

70

80

90

100

110

2001 2003 2005 2007 2009 2011 2013 2015

Government debt in Advanced

Economies

17

Source: Haver Source: Haver

(3) Major importers are becoming producers

30%

40%

50%

60%

70%

80%

90%

1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

US Brazil

Share of local consumption produced ‘at home’

Decline in imports

since 1994:

- 150 Kb/d

- 1,940 Kb/d

18

Source: BP Statistical Review of World Energy

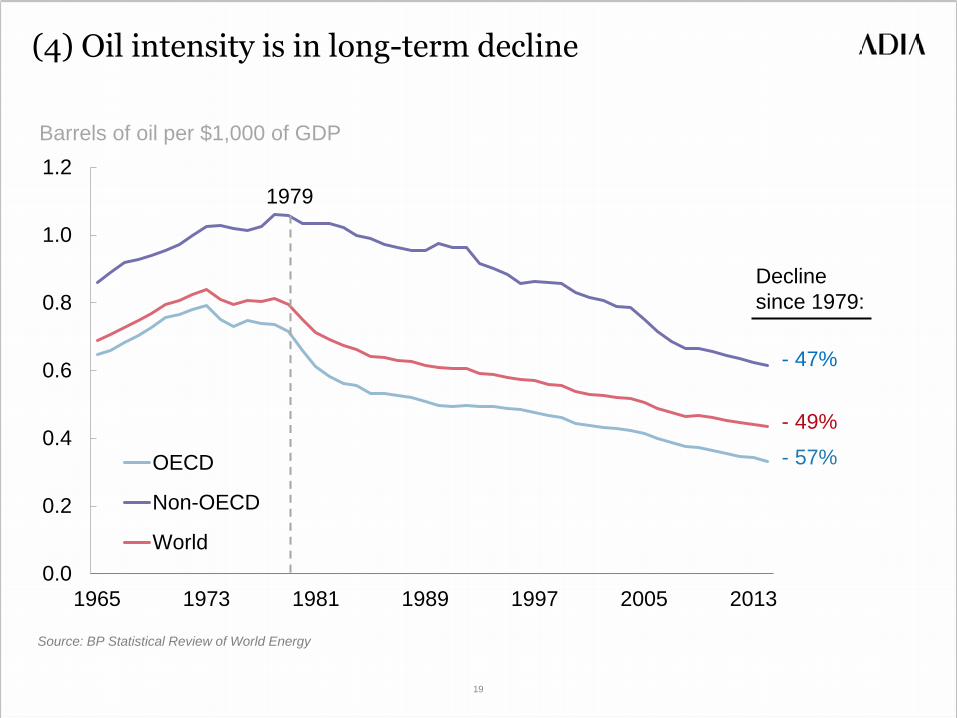

(4) Oil intensity is in long-term decline

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1965 1973 1981 1989 1997 2005 2013

OECD

Non-OECD

World

Barrels of oil per $1,000 of GDP

- 47%

- 49%

- 57%

Decline

since 1979:

1979

Source: BP Statistical Review of World Energy

19

Outline

The economy: an age of stagnation and low returns?

Oil market recap

Why are lower oil prices not boosting economic growth?

Where next for oil markets?

20

-8

-6

-4

-2

0

2

4

6

8

10

12

14

20

30

40

50

60

70

80

90

100

110

120

130

Jan-14 Jun-14 Nov-14 Apr-15 Sep-15

12M – Dated Brent (rhs)

Dated Brent

0

20

40

60

80

100

120

140

Jan-00 Jan-03 Jan-06 Jan-09 Jan-12 Jan-15

Dated Brent

Weekly oil price

$/bbl $/bbl $/bbl

Contango

Backwardation

Daily oil price and term structure

Crude prices and term structure

21

Source: Bloomberg Source: Bloomberg

(1) OECD inventories are at historic highs…

22

2,500

2,600

2,700

2,800

2,900

3,000

3,100

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2010-14 Inventory range 2015 2014

Million barrels of crude oil and oil products

Source: EIA

… and so is the US strategic petroleum reserve

23

0

2

4

6

8

10

12

14

16

0

20

40

60

80

100

120

140

160

Jan-00 Jan-02 Jan-04 Jan-06 Jan-08 Jan-10 Jan-12 Jan-14

Strategic reserve

Net imports of crude and products (rhs)

Million barrels of oil per day Forward imports cover in days

(2) US shale oil production finally declining…

-5%

0%

5%

10%

15%

20%

25%

30%

Jan-11 Sep-11 May-12 Jan-13 Sep-13 May-14 Jan-15 Sep-15

US on-shore oil production (excl. Alaska)

YoY growth

US on-shore production

declined by more than 0.6

Mb/d since peaking at 7.7

Mb/d in March 2015

22% was the average

US onshore production

growth in the 2012 to

end-2014 period

24

… driving overall production lower

6.0

6.4

6.8

7.2

7.6

8.0

8.4

8.8

9.2

9.6

10.0

Jan-14 Apr-14 Jul-14 Oct-14 Jan-15 Apr-15 Jul-15 Oct-15

Total US crude production

Lower-48 production

Million barrels per day (Mb/d)

25

Source: EIA

-0.4

-0.3

-0.2

-0.1

0.0

0.1

0.2

0.3

0.4

Average 2011-14 2015

Europe US

(3) Above-average demand growth driven by the OECD

European and US demand growth

Million barrels per day (Mb/d)

Source: EIA

OECD and Non-OECD demand growth

-0.5

0.0

0.5

1.0

1.5

2.0

Average 2011-14 2015

OECD Non-OECD World

Million barrels per day (Mb/d)

Source: EIA

1.27 Mb/d 1.36 Mb/d

26

0.0

0.1

0.2

0.3

0.4

0.5

Average 2011-14 2015

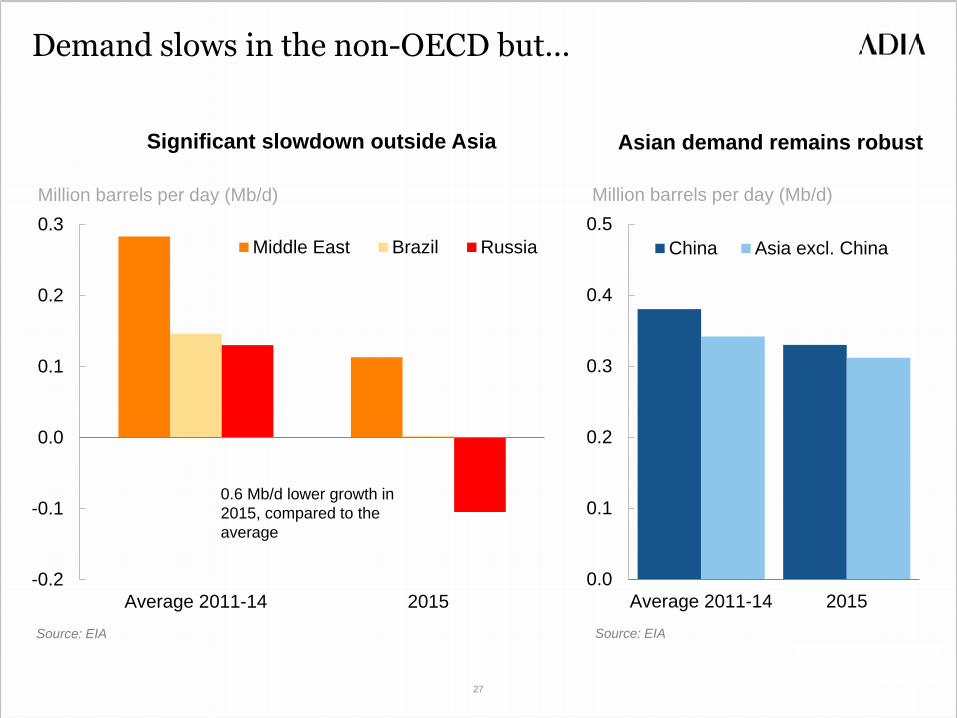

China Asia excl. China

Demand slows in the non-OECD but…

Asian demand remains robust

Million barrels per day (Mb/d)

Source: EIA

Significant slowdown outside Asia

-0.2

-0.1

0.0

0.1

0.2

0.3

Average 2011-14 2015

Middle East Brazil Russia

Million barrels per day (Mb/d)

Source: EIA

0.6 Mb/d lower growth in

2015, compared to the

average

27

… China worries overblown

-30%

-20%

-10%

0%

10%

20%

30%

40%

Jan-11 Jul-11 Jan-12 Jul-12 Jan-13 Jul-13 Jan-14 Jul-14 Jan-15 Jul-15

Gasoline Diesel

YoY growth

2015

28

Source: JODI

500

550

600

650

700

750

Jan-12 Dec-12 Nov-13 Oct-14 Sep-15

Source: Bloomberg

0

200

400

600

800

1,000

1,200

Jan-14 Jul-14 Jan-15 Jul-15 Jan-16

(4) Saudi Arabia: FOREX reserves and forward rate

Saudi Arabian FOREX reserves

Million US dollars

Saudi Riyal 12-month forward premium

Basis points (above spot rate)

Source: Bloomberg

$129bn

decline

since

August

2014

29

Selected oil market shares

6%

7%

8%

9%

10%

11%

12%

Jan-12 Oct-12 Jul-13 Apr-14 Jan-15 Oct-15

Russia

Saudi Arabia

US crude oil

Market share

30%

31%

32%

33%

34%

35%

36%

Jan-12 Oct-12 Jul-13 Apr-14 Jan-15 Oct-15

OPEC

Market share

Country market shares OPEC market share

OPEC meeting OPEC meeting

30

Source: EIA Source: EIA

US and Saudi Arabia: oil market shares

6%

7%

8%

9%

10%

11%

12%

Jan-11 Aug-11 Mar-12 Oct-12 May-13 Dec-13 Jul-14 Feb-15 Sep-15

Saudi Arabia market share (crude only) US market share (crude only)

Market share

Saudi Arabian share

essentially flat

US market share

increased from

6.1% to 10.2%

at the peak

31

Source: EIA

2.8%

3.2%

3.6%

4.0%

4.4%

4.8%

Jan-11 Dec-11 Nov-12 Oct-13 Sep-14 Aug-15

Iran Iraq

Oil market shares of key OPEC producers

Market share

9.5%

9.9%

10.3%

10.7%

11.1%

11.5%

Jan-11 Dec-11 Nov-12 Oct-13 Sep-14 Aug-15

Saudi Arabia

Market share

Iran & Iraq Saudi Arabia

32

Source: EIA Source: EIA

Conclusion

The economy: Multiple and volatile adjustments, but still locally driven

Relationship between oil and global growth has weakened

Oil markets are searching for a new equilibrium, accommodating OPEC

as well as unconventional growth

Expect volatility with an upward drift in prices for 2016-17

33