Embed Size (px)

Citation preview

978–0–19–956578–8 00-ADB-2-Main-drv African Development Bank2 (Typeset by SPi, Chennai) 13 of 233 July 29, 2009 15:25

2

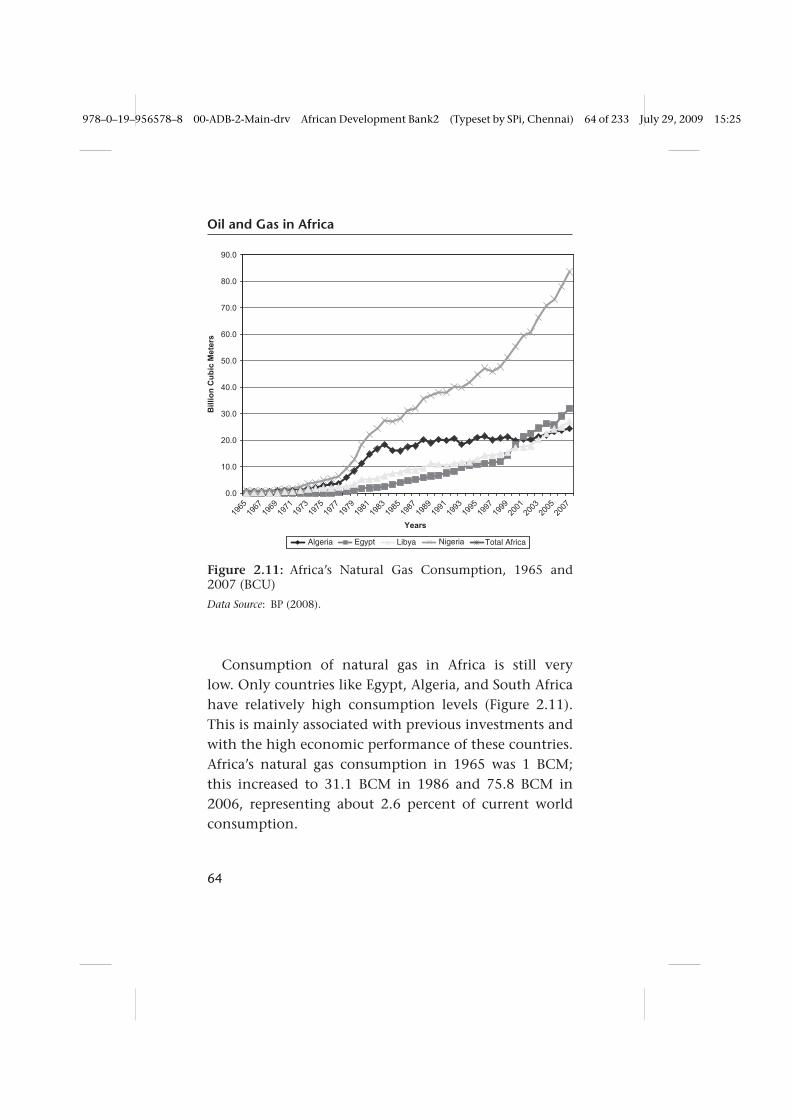

Oil and Gas in Africa

Africa has historically been referred to as a continentwith rich natural resources but with high levels ofpoverty. Indeed, Africa is considered to be well-endowedwith minerals, including fossil fuels, although the exacteconomic potential of these resources is not known.New discoveries of oil and gas in Africa—in locationsnever before thought to hold such resources in signifi-cant amounts—prove that the continent is still “virgin”in many aspects regarding exploration and exploitationof oil and gas resources.

2.1 The International Perspective

This chapter briefly reviews major developments inthe oil and gas sector in the context of developmentsin global energy markets over the last 40 years. The

13

978–0–19–956578–8 00-ADB-2-Main-drv African Development Bank2 (Typeset by SPi, Chennai) 14 of 233 July 29, 2009 15:25

Oil and Gas in Africa

discussion focuses on the dynamics of oil and gas mar-kets over the last ten years, during which Africa has beenplaying an increasingly important role.

2.1.1 Evolution of World Energy Markets

The evolution of world energy markets in the post-1970period has been dramatic and its impact on the worldeconomy and on politics profound. This is illustratedby the worldwide economic ripple effects caused bythe volatility and occasional spectacular spikes in theprices of dominant global energy resources such as oiland gas. Another major trend with significant impacthas been the fundamental changes in the structure,conduct, and performance of the oil and gas sector—including considerable improvements in oil and gastechnology, unprecedented consolidation among multi-national oil companies, increasing global price trans-parency implicit in oil trade, new market fundamentals,and environmental considerations. The transition froma seller’s market environment (in the early 1970s), firstcontrolled and managed by multinational oil compa-nies and subsequently by major net oil-exporting coun-tries (OPEC), to a buyer’s market illustrates the pro-found changes that occurred in the oil industry duringthe period spanning the 1970s to the late 1990s. Theseissues are further explored in the following section,which focuses on oil prices and on post-1990 events inparticular.

14

978–0–19–956578–8 00-ADB-2-Main-drv African Development Bank2 (Typeset by SPi, Chennai) 15 of 233 July 29, 2009 15:25

Oil and Gas in Africa

0

20

40

60

80

100

120

140

160

1989

M1

1989

M8

1990

M3

1990

M10

1991

M5

1991

M12

1992

M7

1993

M2

1993

M9

1994

M4

1994

M11

1995

M6

1996

M1

1996

M8

1997

M3

1997

M10

1998

M5

1998

M12

1999

M7

2000

M2

2000

M9

2001

M4

2001

M11

2002

M6

2003

M1

2003

M8

2004

M3

2004

M10

2005

M5

2005

M12

2006

M7

2007

M2

2007

M9

2008

M4

2008

M11

Months/Years

US

$

Figure 2.1: Crude Oil Spot Price between 1989 and 2008

Source: Authors, from IMF Commodity Prices Database, January 2009.

2.1.2 Trends in Prices of Crude Oil and Petroleum Products

Crude oil prices exhibit wide swings in times ofshortage or excess supply. The crude oil price cycle(Figure 2.1) may extend over several years, even decades,responding to changes in overall geopolitical develop-ments and to demand and supply trends. Understandingand distinguishing among the factors affecting short-and long-term behavior has been the subject of muchdiscussion since the 1970s. The stylized facts aboutglobal energy have been widely documented; however,the scope of this publication does not allow furtherelaboration on the debate. This report briefly exam-ines the recent dynamics in the industry, as highlightedby price changes and industry structure, conduct, and

15

978–0–19–956578–8 00-ADB-2-Main-drv African Development Bank2 (Typeset by SPi, Chennai) 16 of 233 July 29, 2009 15:25

Oil and Gas in Africa

performance. It also draws some emerging lessons fromthese developments.

The dramatic rise in crude oil prices in 1973–74marked a new era in the industry. The rise in oil priceswas triggered in part by the supply shortage associ-ated with the oil embargo imposed on some major oil-consuming countries—as a result of the Middle Eastcrisis—and the transfer of oil property rights from multi-national oil companies to oil-producing countries. It isworth noting that oil price increases in 1973–74 and1979–80 signaled the end of the era of inexpensiveenergy in general. The nominal price of oil, which wasbelow $2 per barrel in 1970, rose to over $40 in 1981, tojust over $147 in July 2008 and to about $42 per barrelin February 2009. Indeed, since the beginning of thisdecade, and over the past two years in particular, worldoil and gas prices have risen to new historic heights. Pre-dictably, the prices of petroleum products have also sky-rocketed, triggered partly by the development in crudeoil prices.

The prices of natural gas imports, which averaged lessthan $2 per thousand cubic feet in the 1990s, jumpedto $4 in 2001, and doubled to an annual average of $8in 2005. Overall, large increases in gas prices in the pastdecade ushered in a new era with considerably higherenergy prices. However, because natural gas does nothave the same political profile as crude oil, its mar-ket development has been less contentious. Natural gasprices, like oil prices, have also experienced volatilitysince 1990. For example, the price of U.S. natural gas

16

978–0–19–956578–8 00-ADB-2-Main-drv African Development Bank2 (Typeset by SPi, Chennai) 17 of 233 July 29, 2009 15:25

Oil and Gas in Africa

imports fell by about 37 percent in September 2008, froma peak of $11.99 in October 2005.

2.1.3 Market Dynamics: Emerging Trends

The behavior of crude oil prices can be viewed fromtwo broad perspectives: prior to 1973 and post 1973.During the first period, prices exhibited long-term sta-bility. The multinational oil companies in control of theindustry at that time managed market supply of crudeto avoid substantial excess supply that could destabilizethe market. The playing field has changed significantlysince the 1970s. A series of events were fundamental tothe radical changes in market structure. First, oil propertyrights were transferred from multinational oil compa-nies to OPEC oil-producing countries. Second, the oilprice increases of the 1970s, coupled with extremelyhigh taxes on oil in the major OECD consuming coun-tries, helped trigger demand and supply responses thateventually produced the first major market slump in the1980s. However, increasingly in recent years, the supplyresponse to increased demand has been weak, inducinghigher price volatility.

In recent years, several factors have led to the currentstate of the oil market, which is characterized by volatileand high prices for crude oil and petroleum products.These factors include:

� Rise in demand in emerging economies, especially inChina and India;

17

978–0–19–956578–8 00-ADB-2-Main-drv African Development Bank2 (Typeset by SPi, Chennai) 18 of 233 July 29, 2009 15:25

Oil and Gas in Africa

� Decline in the spare capacity of major producingcountries and the peaking of production in severalimportant oil-producing areas (such as the North Seaand North America);

� Decline in global investment in the industry;� Lack of expansion in refinery capacity;� Supply bottlenecks and uncertainties associated with

domestic problems (for example, in Nigeria), andinternational politics (Iran, Iraq, Venezuela, andRussia) that impact supply;

� Supply uncertainties associated with extremeweather events (such as hurricanes);

� Lack of a dominant actor in the market to manageexcess supply and demand; and

� Commoditization of world oil (for example, throughNYMEX).

In the longer term, there will primarily be three marketdrivers: demand from emerging countries (China andIndia in particular); production from OPEC countries;and inventory movement in major consuming countries(especially the United States). Increasingly, environmen-tal policy considerations may also shape the future of themarket. Policies aimed at reducing carbon emissions inthe quest to mitigate global warming are likely to impactthe future use of oil.

Meanwhile, price movements—reflecting marketconditions—as well as pure speculation will continueto have a significant impact on the global economy.

18

978–0–19–956578–8 00-ADB-2-Main-drv African Development Bank2 (Typeset by SPi, Chennai) 19 of 233 July 29, 2009 15:25

Oil and Gas in Africa

Sustained energy price shocks, as witnessed in recentyears, constitute a major constraint on economicgrowth. Since oil and gas are likely to remain thedominant energy fuels, recent developments in thesemarkets have far-reaching implications for achievinguniversal, affordable, commercial energy access in netoil-importing developing countries. Undoubtedly, forthe more than two billion poor people living in Africa,Asia and Latin America, the current oil and gas marketdynamics are likely to make universal and affordableaccess to commercial energy more difficult to achieve.The impact of rising oil prices for Africa is furtheranalyzed in Chapter 4.

2.1.4 Supply and Demand Outlook

Any analysis of the outlook of oil and gas supply anddemand is fraught with difficulties. Assumptions have tobe made about growth in demand, commodity prices,reserve base, potential new discoveries, technology evo-lution, and world politics. The problem is that data onproduction and demand from the recent past, as wellas predictions in the short to medium term, are ofteninaccurate. These inaccuracies stem from the way thedata is compiled using OPEC production estimates aswell as commercial figures from other countries aroundthe world. These figures are sometimes slanted for polit-ical or economic reasons. The uncertainty increases forpredictions of future production demand. In the nearterm, companies are constantly revising their production

19

978–0–19–956578–8 00-ADB-2-Main-drv African Development Bank2 (Typeset by SPi, Chennai) 20 of 233 July 29, 2009 15:25

Oil and Gas in Africa

targets downwards, and in the longer term, publishedsupply and demand estimates show a large margin oferror. Recent analysis by ExxonMobil, for instance, indi-cates that, over the next 10 years, oil and gas demand willincrease by about 2 percent a year, while current fieldsin production will deplete at an average of 3 percentto 5 percent per year. A similar situation exists for gasproduction, demand, and supply, although the availablereserves figures are even less certain than those for oil.A significant amount of gas is still in the “possible”category.

2.1.5 Global Energy Resource Profile: Oil andGas in Perspective

World proven crude oil reserves1 at the end of 2006were estimated at 1,208.2 billion barrels.2 Global oilreserves are unequally distributed as the data on regional

1 Conventional crude oil reserves include all crude oil that it is tech-nically possible to produce from reservoirs through a well bore, usingprimary, secondary, improved, enhanced, or tertiary methods. This doesnot include liquids extracted from mined solids or gases. Oil reserves areclassified as proven, probable, and possible. Proven reserves are generallyintended to have at least 90% or 95% certainty of containing the amountspecified. Probable reserves have an intended probability of 50%, and pos-sible reserves an intended probability of 5% or 10%. Current technologyis capable of extracting about 40% of the oil from most wells. In severalmajor producing countries, the majority of reserves claims have not beensubject to outside audit or examination. Unconventional sources, such asheavy crude oil, tar sands, and oil shale, are not counted as part of oilreserves. For further elaboration on reserve categories and terminology,also see Whateley and Harvey (1994).

2 The analysis in this chapter is based mainly on data from BP StatisticalReview of World Energy (2006 and 2007 volumes).

20

978–0–19–956578–8 00-ADB-2-Main-drv African Development Bank2 (Typeset by SPi, Chennai) 21 of 233 July 29, 2009 15:25

Oil and Gas in Africa

composition of proven reserves in Table 2.1 demon-strates. The Middle East region is the dominant region,accounting for 61.5 percent of estimated world provenoil reserves. Europe and Eurasia come in a distant second,with 12.0 percent; while Africa ranks a close third, with9.7 percent of global reserves. The geographical distribu-tion has remained relatively unchanged in the past threedecades. The OECD region, which includes the major oil-and gas-consuming countries in the world, accounts forless than 6.6 percent of global reserves. In contrast, OPECholds 75.7 percent of global reserves.

From a longer-term perspective, world oil reserves grewat an annual rate of 1.7 percent between 1980 and 2006.Reserves growth in Africa was double the global rate, at3.2 percent; while OPEC reserves grew 1.5 percent.

The upward trend in proven reserves is attributableto two main factors: rising oil prices and technologi-cal progress. It is widely recognized that the upwardtrend in demand and crude oil prices have provideda very attractive environment for exploration and fora subsequent increase in proven and probable oil andgas reserves. Technological progress has boosted averagerecovery rates and also enabled economically attractiveproduction from what was previously regarded as mar-ginal and infra-marginal oil fields.

The lopsided distribution of oil wealth has generatedconcerns about global access, oil geopolitics, and energysecurity. In fact, the concentration of proved reservesin a few countries has been a contentious factor in theevolving state of global energy markets in past decades.

21

978–0–19–956578–8 00-ADB-2-Main-drv African Development Bank2 (Typeset by SPi, Chennai) 22 of 233 July 29, 2009 15:25

Oil and Gas in Africa

Tab

le2.

1:Pr

oved

Cru

deO

ilRe

serv

esby

Regi

on,1

980

to20

06(B

illio

nBa

rrel

s)

Reg

ion

1980

1985

1990

2000

2005

2006

%o

fto

tal

in20

06

Afr

ica

53.3

57.0

58.7

93.4

114.

311

7.2

9.7

Nor

thA

mer

ica

92.5

101.

596

.375

.660

.759

.95.

0So

uth

and

Cen

tral

Am

eric

a26

.762

.971

.697

.910

3.2

103.

58.

6Eu

rop

e&

Eura

sia

98.4

78.6

80.3

114.

114

5.2

144.

412

.0M

iddl

eEa

st36

2.4

431.

365

7.7

691.

074

2.7

742.

761

.5A

sia

Paci

fic33

.839

.136

.342

.640

.540

.53.

4W

orl

d66

7.1

770.

41,

000.

91 ,

114.

71,

209.

51,

208.

210

0of

whi

chO

ECD

109.

211

8.6

115.

110

0.0

81.9

79.8

6.6

OPE

C43

4.6

535.

876

5.9

840.

591

4.5

914.

675

.7N

on-O

PEC

150.

517

2.0

171.

718

0.8

176.

417

4.5

14.4

Dat

aSo

urce

:BP

Stat

istic

alRe

view

ofW

orld

Ener

gy20

07(B

P,20

07).

22

978–0–19–956578–8 00-ADB-2-Main-drv African Development Bank2 (Typeset by SPi, Chennai) 23 of 233 July 29, 2009 15:25

Oil and Gas in Africa

World proven gas reserves in January 2007 were esti-mated to be 181.46 trillion cubic meters. However,although the distribution of global gas resources isunequal, similar to that of crude oil, its regional imbal-ance is less pronounced. Of the world’s proved reserves,the Middle East region ranks first with a 40.5 percentshare (Table 2.2); Europe, including gas reserves in Russiaand the former Soviet Republics, follows closely with35.3 percent; while Africa ranks fourth, with 7.8 percent.

2.1.6 Trends and Patterns of Global Energy Productionand Consumption

To understand recent energy market developments, it isnecessary to examine the long-term trends and patternsof world primary energy supply and demand. The analy-sis is based only on commercial and conventional energysources due to lack of data.

Table 2.3 shows that world primary energy supply rosefrom 288 quadrillion BTU (British Thermal Units) in1980 to 443 quadrillion BTU in 2004. Primary energysupply almost doubled in Africa. Table 2.4 presents thegeographical distribution of primary energy production.It is evident that oil and gas remain the dominant sourceof energy worldwide.

The regional composition of global energy consump-tion reveals a wide disparity in global access to reliableand adequate commercial energy. Although Africa (Sub-Saharan Africa and North Africa) accounts for about15 percent of the world’s population, it consumes only

23

978–0–19–956578–8 00-ADB-2-Main-drv African Development Bank2 (Typeset by SPi, Chennai) 24 of 233 July 29, 2009 15:25

Oil and Gas in Africa

Tab

le2.

2:Re

gion

alD

istr

ibut

ion

ofN

atur

alG

asRe

serv

es,1

980

to20

06(T

rillio

nm

3)

Reg

ion

1980

1990

1995

2000

2005

2006

%sh

are

of

tota

lin

2006

Afr

ica

5.99

8.55

9.93

12.4

714

.08

14.1

87.

8N

orth

Am

eric

a9.

899.

498.

477.

497.

837.

984.

4So

uth

and

Cen

tral

Am

eric

a2.

785.

255.

966.

986.

856.

883.

8Eu

rop

e&

Eura

sia

36.0

059

.84

63.1

661

.74

64.3

064

.13

35.3

Mid

dle

East

24.6

937

.99

45.3

759

.81

72.4

973

.47

40.5

Asi

aPa

cific

4.47

9.88

10.5

412

.28

14.6

614

.82

8.2

Wo

rld

83.3

013

1.00

143.

4216

0.76

180 .

2018

1.46

100.

0

Dat

aSo

urce

:BP

Stat

istic

alRe

view

ofW

orld

Ener

gy20

07(B

P,20

07).

24

978–0–19–956578–8 00-ADB-2-Main-drv African Development Bank2 (Typeset by SPi, Chennai) 25 of 233 July 29, 2009 15:25

Oil and Gas in Africa

Tab

le2.

3:W

orld

Prim

ary

Ener

gyPr

oduc

tion

inQ

uadr

illio

nBT

U,1

980–

2004

Year

Afr

ica

No

rth

Am

eric

aS.

&C

.A

mer

ica

Euro

pe

Eura

sia

Mid

dle

East

Asi

a&

Oce

ania

Wo

rld

Tota

l

1980

17.3

9583

.276

12.0

8340

.216

56.4

6342

.265

35.8

6128

7.55

919

9021

.610

91.9

0316

.749

46.9

0772

.111

40.9

9559

.389

349.

663

2000

27.8

4498

.754

26.0

4250

.821

55.6

8957

.480

80.4

9939

7.12

920

0128

.098

99.4

6825

.990

51.4

1257

.705

56.1

5585

.467

404.

295

2002

28.0

0410

0.01

925

.318

51.2

0059

.463

54.2

5187

.867

406.

121

2003

30.1

0598

.523

25.7

3850

.672

63.2

0957

.612

95.8

5542

1.71

420

0432

.043

99.3

1027

.169

50.6

1066

.714

62.0

7810

5.17

744

3.10

0

Dat

aSo

urce

:U.S

.Dep

artm

ent

ofEn

ergy

(200

6a).

25

978–0–19–956578–8 00-ADB-2-Main-drv African Development Bank2 (Typeset by SPi, Chennai) 26 of 233 July 29, 2009 15:25

Oil and Gas in Africa

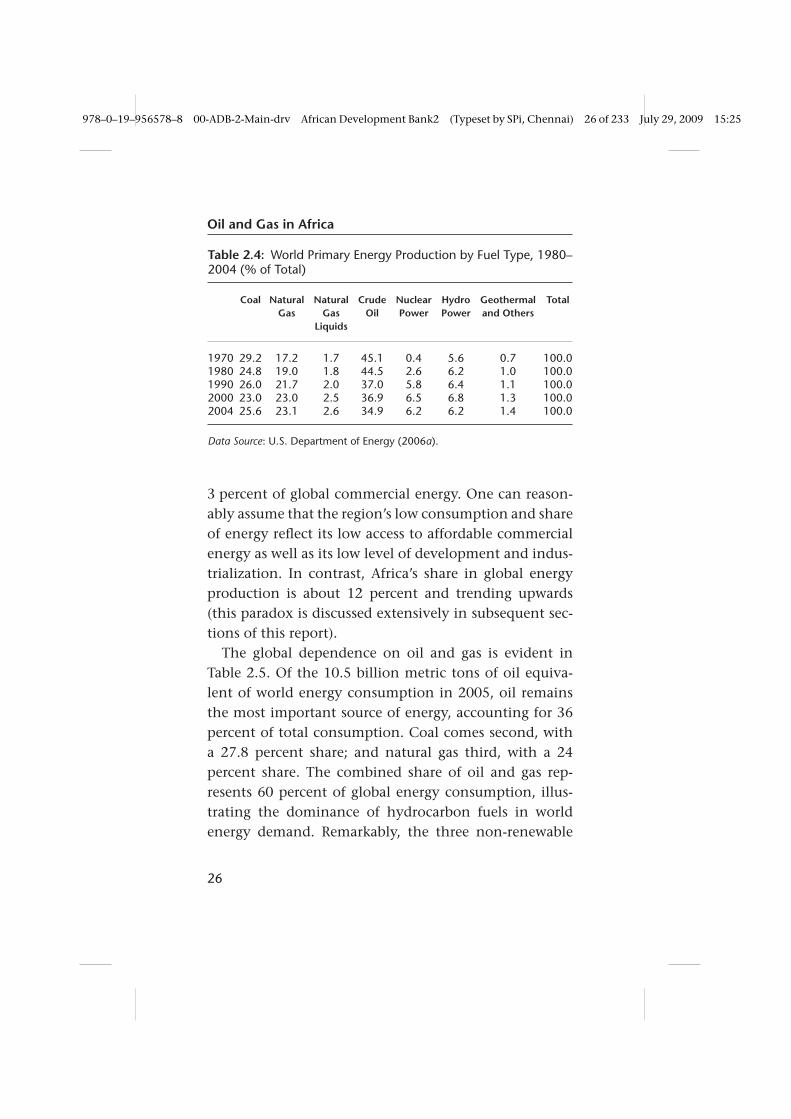

Table 2.4: World Primary Energy Production by Fuel Type, 1980–2004 (% of Total)

Coal NaturalGas

NaturalGas

Liquids

CrudeOil

NuclearPower

HydroPower

Geothermaland Others

Total

1970 29.2 17.2 1.7 45.1 0.4 5.6 0.7 100.01980 24.8 19.0 1.8 44.5 2.6 6.2 1.0 100.01990 26.0 21.7 2.0 37.0 5.8 6.4 1.1 100.02000 23.0 23.0 2.5 36.9 6.5 6.8 1.3 100.02004 25.6 23.1 2.6 34.9 6.2 6.2 1.4 100.0

Data Source: U.S. Department of Energy (2006a).

3 percent of global commercial energy. One can reason-ably assume that the region’s low consumption and shareof energy reflect its low access to affordable commercialenergy as well as its low level of development and indus-trialization. In contrast, Africa’s share in global energyproduction is about 12 percent and trending upwards(this paradox is discussed extensively in subsequent sec-tions of this report).

The global dependence on oil and gas is evident inTable 2.5. Of the 10.5 billion metric tons of oil equiva-lent of world energy consumption in 2005, oil remainsthe most important source of energy, accounting for 36percent of total consumption. Coal comes second, witha 27.8 percent share; and natural gas third, with a 24percent share. The combined share of oil and gas rep-resents 60 percent of global energy consumption, illus-trating the dominance of hydrocarbon fuels in worldenergy demand. Remarkably, the three non-renewable

26

978–0–19–956578–8 00-ADB-2-Main-drv African Development Bank2 (Typeset by SPi, Chennai) 27 of 233 July 29, 2009 15:25

Oil and Gas in Africa

Table 2.5: Global Dependence on Oil and Gas, 2005 (%)

Oil NaturalGas

Coal NuclearEnergy

HydroElectric

Total

Africa 40.9 20.3 31.7 0.9 6.3 100.0North America 40.4 24.9 21.9 7.5 5.3 100.0South and Central

America44.5 22.3 4.2 0.7 28.3 100.0

Europe and Eurasia 32.3 33.8 18.0 9.6 6.3 100.0Middle East 53.2 44.3 1.8 − 0.8 100.0Africa 40.9 20.3 31.7 0.9 6.3 100.0Asia 32.6 10.7 48.1 3.7 4.9 100.0World 36.4 23.5 27.8 6.0 6.3 100.0United States 40.4 24.4 24.6 8.0 2.6 100.0EU 25 40.8 24.7 17.4 12.9 4.1 100.0OECD 41.0 23.0 21.1 9.6 5.4 100.0

Data Source: BP Statistical Review of World Energy (BP, 2006).

fossil fuels—oil, natural gas, and coal—constitute almost90 percent of commercial energy consumed worldwide.

2.2 Oil and Gas and the Global Economy

The interrelationship between oil and gas and the eco-nomic status and development of countries remains adominant and persistent theme. A key factor is the factthat the world economy runs largely on hydrocarbons.The issue of unequal global access to commercial energyand the gains of global economic prosperity have alsofrequently been highlighted in international discourse.

Energy has traditionally played an important role inthe economy of any nation because it is an indispensable

27

978–0–19–956578–8 00-ADB-2-Main-drv African Development Bank2 (Typeset by SPi, Chennai) 28 of 233 July 29, 2009 15:25

Oil and Gas in Africa

input for economic growth and development. Two-thirds of global energy requirements are met from oiland gas supplies. Conventional wisdom holds that thereis a strong correlation between energy consumption percapita and the level of economic and social progress. Thisstill holds true despite globalization, increasing growth—in Asia, for example—and energy market developmentsin recent decades.

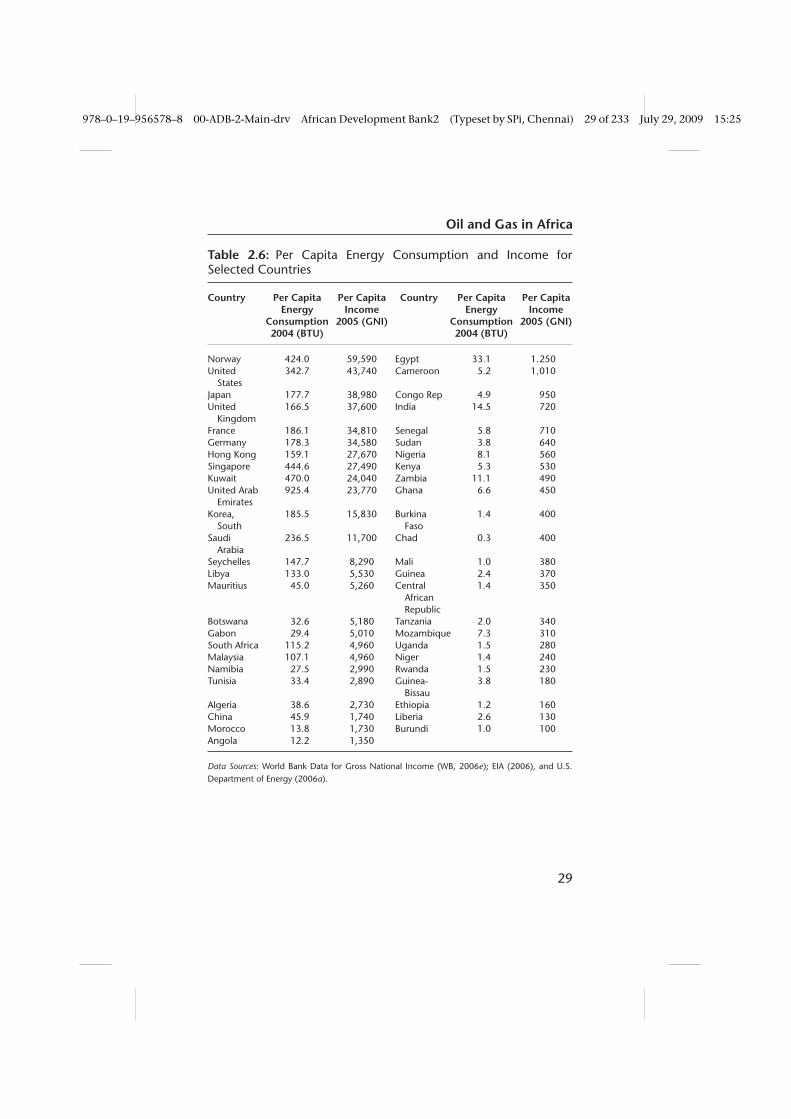

Since economic and social development depend, inlarge part, on an adequate supply of energy at affordableprices, changes in energy prices are bound to affect eco-nomic growth and development. However, the resilienceof developed and developing countries to the shocksproduced by these changes varies as a function of thedifferent economic strengths of these countries. Afford-able access to adequate and reliable energy supply wasa central factor in the achievement of the large produc-tivity gains that guaranteed sustained economic growthand led to a significant leap in material prosperity andwidespread improvement in human well-being in thelast century. The data in Table 2.6 supports the hypothe-sis that there is a strong correlation between energy (andoil) consumption per capita and the level of economicand social progress. The data clearly shows that countrieswith higher per capita income also consume more energyper head.

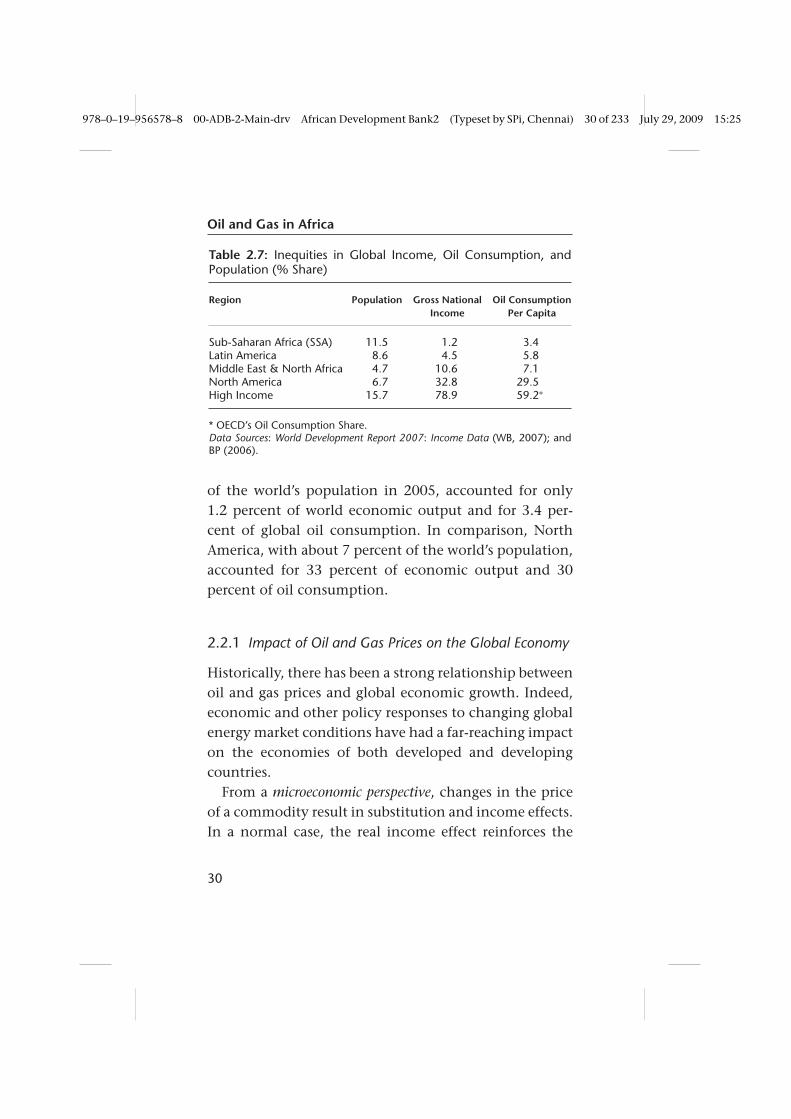

Table 2.7 further reveals the wide disparities in globalaccess to reliable and adequate commercial energy as wellas in the sharing of the fruits of global economic pros-perity. Sub-Saharan Africa (SSA), with almost 12 percent

28

978–0–19–956578–8 00-ADB-2-Main-drv African Development Bank2 (Typeset by SPi, Chennai) 29 of 233 July 29, 2009 15:25

Oil and Gas in Africa

Table 2.6: Per Capita Energy Consumption and Income forSelected Countries

Country Per Capita Per Capita Country Per Capita Per CapitaEnergy Income Energy Income

Consumption 2005 (GNI) Consumption 2005 (GNI)2004 (BTU) 2004 (BTU)

Norway 424.0 59,590 Egypt 33.1 1,250United

States342.7 43,740 Cameroon 5.2 1,010

Japan 177.7 38,980 Congo Rep 4.9 950United

Kingdom166.5 37,600 India 14.5 720

France 186.1 34,810 Senegal 5.8 710Germany 178.3 34,580 Sudan 3.8 640Hong Kong 159.1 27,670 Nigeria 8.1 560Singapore 444.6 27,490 Kenya 5.3 530Kuwait 470.0 24,040 Zambia 11.1 490United Arab

Emirates925.4 23,770 Ghana 6.6 450

Korea,South

185.5 15,830 BurkinaFaso

1.4 400

SaudiArabia

236.5 11,700 Chad 0.3 400

Seychelles 147.7 8,290 Mali 1.0 380Libya 133.0 5,530 Guinea 2.4 370Mauritius 45.0 5,260 Central

AfricanRepublic

1.4 350

Botswana 32.6 5,180 Tanzania 2.0 340Gabon 29.4 5,010 Mozambique 7.3 310South Africa 115.2 4,960 Uganda 1.5 280Malaysia 107.1 4,960 Niger 1.4 240Namibia 27.5 2,990 Rwanda 1.5 230Tunisia 33.4 2,890 Guinea-

Bissau3.8 180

Algeria 38.6 2,730 Ethiopia 1.2 160China 45.9 1,740 Liberia 2.6 130Morocco 13.8 1,730 Burundi 1.0 100Angola 12.2 1,350

Data Sources: World Bank Data for Gross National Income (WB, 2006e); EIA (2006), and U.S.Department of Energy (2006a).

29

978–0–19–956578–8 00-ADB-2-Main-drv African Development Bank2 (Typeset by SPi, Chennai) 30 of 233 July 29, 2009 15:25

Oil and Gas in Africa

Table 2.7: Inequities in Global Income, Oil Consumption, andPopulation (% Share)

Region Population Gross NationalIncome

Oil ConsumptionPer Capita

Sub-Saharan Africa (SSA) 11.5 1.2 3.4Latin America 8.6 4.5 5.8Middle East & North Africa 4.7 10.6 7.1North America 6.7 32.8 29.5High Income 15.7 78.9 59.2∗

* OECD’s Oil Consumption Share.Data Sources: World Development Report 2007: Income Data (WB, 2007); andBP (2006).

of the world’s population in 2005, accounted for only1.2 percent of world economic output and for 3.4 per-cent of global oil consumption. In comparison, NorthAmerica, with about 7 percent of the world’s population,accounted for 33 percent of economic output and 30percent of oil consumption.

2.2.1 Impact of Oil and Gas Prices on the Global Economy

Historically, there has been a strong relationship betweenoil and gas prices and global economic growth. Indeed,economic and other policy responses to changing globalenergy market conditions have had a far-reaching impacton the economies of both developed and developingcountries.

From a microeconomic perspective, changes in the priceof a commodity result in substitution and income effects.In a normal case, the real income effect reinforces the

30

978–0–19–956578–8 00-ADB-2-Main-drv African Development Bank2 (Typeset by SPi, Chennai) 31 of 233 July 29, 2009 15:25

Oil and Gas in Africa

pure substitution effect and yields a negative relation-ship between the amount purchased and the price of theproduct. Higher prices lead to reduced consumption, allother things being equal.

Analysis of the macroeconomic effects of higher oilprices has been a recurrent theme since the first majoroil price shock of the 1970s. Historical evidence showsthat oil price increases and volatility have had a sig-nificant impact on global, regional, and national eco-nomic performance and outlook. Conventional wisdom,backed by empirical analysis, suggests that increases inoil prices tend to exert strong inflationary pressures,reduce output, slow down economic growth, and exac-erbate unemployment in net oil-importing countries.Thus, the rising costs of oil imports caused by both theexchange rate depreciation and the rising dollar price ofoil are bound to have profound ripple effects throughoutnational economies.

Broadly speaking, higher oil prices can impact aggre-gate economic activity directly or indirectly. The mainchannels through which oil prices impact macroeco-nomic aggregates are well understood (IMF, 2000, 2005).These channels include the following:

1. Terms of trade effects: These result in the trans-fer of income from oil-importing countries to oil-producing countries at the global level and from oilconsumers to oil producers at the domestic level. Atthe global level, the net gain to oil-exporting coun-tries is offset by the net loss to net oil-importing

31

978–0–19–956578–8 00-ADB-2-Main-drv African Development Bank2 (Typeset by SPi, Chennai) 32 of 233 July 29, 2009 15:25

Oil and Gas in Africa

countries. The bigger the oil price increase, thelarger the potential macroeconomic effects are likelyto be at the national, regional, and global levels.

2. Input price: This channel works through productionand investment via increasing cost of productionin the economy. The size of this impact of higheroil prices on the economy depends on oil intensityof aggregate output. Adding price volatility to theprice shock, the consequences are high cost of pro-duction, deterrence of irreversible investment, andultimate reduction in aggregate economic activity,or, at best, slowdown in rate of economic growth.

3. Exchange rate pass-through: The invoicing currencyfor the oil trade has traditionally been the U.S. dol-lar. Oil-importing countries are adversely affected bychanges in the value of the U.S. dollar vis-à-vis othercurrencies. The exchange rate pass-through effectexacerbates the input shock effect of oil prices in netoil-importing developing countries. The magnitudeof the pass-through depends on government policyand the state of energy market liberalization. Thesize of the pass-through also depends on the struc-ture of the domestic oil market. A more competitivemarket structure would minimize the pass-throughrelative to monopolistic or oligopolistic cartel-likecontrol of the market.

4. Oil price pass-through to inflation: Oil priceincreases work as a shock to the aggregateprice level, exacerbating inflationary pressure that

32

978–0–19–956578–8 00-ADB-2-Main-drv African Development Bank2 (Typeset by SPi, Chennai) 33 of 233 July 29, 2009 15:25

Oil and Gas in Africa

decreases money balances with its macroeconomicconsequences. There could be partial or total pass-through from higher oil prices to core inflationdepending on the monetary policy stance.

5. Balance of payments impact through higher oilimport costs: This will be more severe if there are nocountervailing and compensating changes in exportrevenues through higher volume of exports andthrough terms of trade gains.

The magnitude of the macroeconomic impact of higheroil prices has been the subject of considerable debate inthe literature (Mork, 1989; Hamilton, 1996; and Lee, Niand Ratti, 1995). Two basic methodological approacheshave been adopted in quantifying the macroeconomicimpact of higher oil prices. The macro-econometricapproach is the most widely used methodology. Fromthis approach, substantial empirical evidence shows thatboth developed and developing countries have been ableto cope increasingly better with the challenges associatedwith oil price increases with each successive decade sincethe first major price increase in the 1970s (IMF, 2000).Nevertheless, economic performance would have beenmore robust if oil prices had not risen so sharply.3

3 Two major defects of the conventional macro-econometric approachare worth noting. The first is its inability to capture the non-linearand asymmetric relationship between oil price changes and output andemployment. Oil price volatility, as evident in the time series behavior ofoil prices, further complicates the problem of estimating the magnitudeof the macroeconomic impact of higher oil prices. The second defect ofthe macro-econometric approach is its inability to capture properly thedistributional effects of higher oil prices. Although this may not be an

33

978–0–19–956578–8 00-ADB-2-Main-drv African Development Bank2 (Typeset by SPi, Chennai) 34 of 233 July 29, 2009 15:25

Oil and Gas in Africa

Finally, an important issue is the role of economicpolicy—at both the micro and macro levels—in miti-gating the potential adverse economic impact of higheroil prices. Two questions come to mind: What can andshould be done to mitigate or even neutralize the impactof higher oil prices? In other words, what is the optimalpolicy mix that would help economies cope with thehigh economic and social costs of the external shocksthat accompany oil and gas market price changes? Itis in this context that an African Petroleum Fund wasproposed to assist African countries to deal with oil priceshocks.

2.2.2 Importance of Petroleum Products

The analysis in this section focuses on the magnitudeand importance of petroleum products for society andfor fueling the world economy. There are strong linksbetween the oil industry and other sectors of the domes-tic economy.

2.2.2.1 PETROLEUM PRODUCTS SUPPLY CHAIN

The energy supply cycle can be divided into upstreamand downstream elements: the upstream comprisesexploration and production activities; while the down-stream includes refining and retail activities. In basicterms, the cycle consists of acquisition of crude oil,

important issue in developed countries, the same cannot be said of low-income countries, where a majority of the people lives on less than $1 aday.

34

978–0–19–956578–8 00-ADB-2-Main-drv African Development Bank2 (Typeset by SPi, Chennai) 35 of 233 July 29, 2009 15:25

Oil and Gas in Africa

transportation to the refinery, refining, transportation tostorage, management of inventories, and selling of finalproducts. Specifically, the complex downstream industryconsists of

� Refining: Crude oil ships and refinery terminals

– Refinery storage and local terminal rack– Refinery products

� Wholesale: Shipping activities

– Marine terminals– Local and international markets

� Retail: Bulk terminal, retail/wholesale, and industrialand home usage.

2.2.2.2 IMPORTANT REFINED PRODUCTS

Refineries turn crude oil into liquefied products, aliphaticchemicals, asphalt paving mixtures, aviation fuels, ben-zene, butylenes, resid/fuel oil/bunker, cumene, cyclicaromatic hydrocarbons, diesel fuels, ethylene, gasoline,heating oils, hydraulic fluids, jet fuels, kerosene, lubri-cating oils and greases, naphtha, naphthenic acids,paraffin waxes, petrochemicals, petroleum coke, petro-leum jelly, petroleum lubricating oils, propane gases,propylene, solvents, styrene, tar, toluene, and xylene(EIA, 2008).

Petroleum products, especially motor gasoline, diesel,and jet fuel, provide virtually all the energy consumed inthe transportation sector. Transportation is the greatestsingle use of petroleum, accounting for over 67 percentof all U.S. petroleum consumed in 2005. The industrial

35

978–0–19–956578–8 00-ADB-2-Main-drv African Development Bank2 (Typeset by SPi, Chennai) 36 of 233 July 29, 2009 15:25

Oil and Gas in Africa

sector is the second largest petroleum-consuming sectorand accounts for about 24 percent of all petroleum con-sumption in the U.S. The residential/commercial andelectric utility sectors account for the remaining 9 per-cent of petroleum consumption (EIA, 2008).

Distillate fuel oil includes diesel oil, heating oils, andindustrial oils. It is used to power diesel engines in buses,trucks, trains, automobiles, and other machinery. It isalso used to heat residential and commercial buildingsand to fire industrial and electric utility boilers.

Liquefied petroleum gases (LPGs) rank third in usageamong petroleum products, behind motor gasoline anddistillate fuel oil. LPGs are used as inputs (feedstock) forpetrochemical production processes. This is their majornon-fuel use. LPGs are also used as fuel for domesticheating and cooking, farming operations, and as analternative to gasoline for use in internal combustionengines. Most jet fuel is a kerosene-based fuel used pri-marily in commercial airlines. Naphtha jet fuel meetsthe specifications required for certain military aircraft.Kerosene-type jet fuel is sometimes blended into heat-ing oil and diesel fuel during periods of extreme coldweather. Although this sector uses relatively little petro-leum, compared with the transportation and industrialsectors, the electric utility sector depends on petroleumfor about 3 percent of its total energy requirements.Residual fuel oil is also used as bunker fuel (fuel forships), industrial boiler fuel, and heating fuel in somecommercial buildings. Kerosene is used for residentialand commercial space heating. It is also used in water

36

978–0–19–956578–8 00-ADB-2-Main-drv African Development Bank2 (Typeset by SPi, Chennai) 37 of 233 July 29, 2009 15:25

Oil and Gas in Africa

heaters, as a cooking fuel, and in lamps. Petroleum cokecan be used as a relatively low-ash solid fuel for powerplants and industrial use (marketable coke) if its sulfurcontent is low enough, or used in non-fuel applications(catalyst coke), such as in refinery operations (Nage-ria, 2005).

Non-fuel use of petroleum is small, compared with fueluse, but it is nevertheless very important from a com-mercial and economic point of view. Non-fuel uses forpetroleum include various specialized products for use inthe textile, metallurgical, electrical, and other industries.A partial list of non-fuel uses for petroleum includes(Nageria, 2005):

� Solvents such as those used in paints, lacquers, andprinting inks;

� Lubricating oils and greases for automobile enginesand other machinery;

� Petroleum (or paraffin) wax used in candy, packag-ing, candles, matches, and polishes;

� Petrolatum (petroleum jelly) in medical products andtoiletries;

� Asphalt used to pave roads and airfields, to surfacecanals and reservoirs, and to make roofing materialsand floor coverings;

� Petroleum coke used as a raw material for manycarbon and graphite products, including furnaceelectrodes and liners, and the anodes used in theproduction of aluminum; and

37

978–0–19–956578–8 00-ADB-2-Main-drv African Development Bank2 (Typeset by SPi, Chennai) 38 of 233 July 29, 2009 15:25

Oil and Gas in Africa

� Petroleum feedstock used as chemical feedstockderived from petroleum, mainly for the manufac-ture of chemicals, synthetic rubber, and a variety ofplastics.

Petroleum has been used as feedstock in the produc-tion of petrochemicals since the 1920s. Petrochemicalfeedstocks also include products recovered from naturalgas and refinery gases (ethane, propane, and butane).Petrochemical feedstocks are converted to basic chemi-cal building blocks and intermediates, such as ethylene,propylene, normal and iso-butylenes, butadiene, andaromatics such as benzene, toluene, and xylene, whichare in turn used to produce plastics, synthetic rubber,synthetic fibers, drugs, and detergents.

2.2.2.3 INDIRECT IMPORTANCE OFPETROLEUM PRODUCTS

Petroleum products are very important for governments,essentially because they are a source of revenue throughtax contributions. Furthermore, both downstream andupstream industries and associated services employ a sig-nificant number of people. The oil industry has socialresponsibilities with local communities where it helps inbuilding access, schools, and hospitals. These aspects arefurther analyzed in Chapters 3 and 4.

2.2.3 Natural Gas and Biofuels

The use of petroleum products has been the subject ofpublic outcry because of their environmental impact.

38

978–0–19–956578–8 00-ADB-2-Main-drv African Development Bank2 (Typeset by SPi, Chennai) 39 of 233 July 29, 2009 15:25

Oil and Gas in Africa

There is also growing concern about the viability of oil-based fuels and products—leading to initiatives to findand develop alternative energy sources.

At present, alternative energy sources—to the oil-basedfuels and products—are quite limited and have untilrecently consisted of gasoline blends, ethanol, methanol,and liquefied gas. Most of these products still rely onexpensive technology, which makes them less compet-itive when compared to oil products. The alternativeenergies are still held back by the extremely large capitalinstallation costs, which reduces its popularity in today’sworld economy. However, both natural gas and biofuelsin various forms have gained considerable attention andmomentum in recent years.

2.2.3.1 NATURAL GAS

Natural gas can be used in a number of ways: in house-holds, in industry, and for power generation. It can alsobe used in the transport sector, in the form of compressednatural gas (CNG), as a substitute for gasoline and diesel.There has been a steady shift towards natural gas as aclean (that is, cleaner than oil and coal) and relativelycheap source of power in recent years. However, byvirtue of being a gas, natural gas is more costly to trans-port and store than liquid or solid fuels. Consequently,natural gas transportation is more complex and costlybecause it requires special vehicles or special pipelines.To address this problem, economies of scale must be pur-sued, especially in laying down extensive pipelines and

39

978–0–19–956578–8 00-ADB-2-Main-drv African Development Bank2 (Typeset by SPi, Chennai) 40 of 233 July 29, 2009 15:25

Oil and Gas in Africa

distribution systems. A pipeline network is economicallyviable especially if there are large consumers (such aspower plants and large industrial operations). The factorsneeded for sustainable conversion to CNG include theexistence of a gas distribution pipeline for other naturalgas users, close proximity to the supply, and inter-fueltaxation policy.

Biofuels are derived from biological (for example, agri-cultural) sources (Chow, 2007):

i. Cereals, grains, sugar crops and other starches canbe fermented to produce ethanol, which can beused pure or as a blending component (as ethanolor after being converted to Ethyl Tertiary ButylEther, ETBE;4

ii. Cellulosic materials, including grasses, trees andvarious waste products from crops, wood process-ing facilities, and municipal solid waste, can alsobe converted to alcohols or diesel type fuels;

iii. Oil-seed crops (such as rapeseed, soybean, and sun-flower) can be converted into methyl esters, whichcan be blended with conventional diesel or burntas pure biodiesel;

4 ETBE is an oxygenated fuel that can be blended with gasoline to makeit burn more cleanly and thus improve overall air quality. ETBE is producedby mixing ethanol and isobutylene and reacting them with heat over acatalyst. The promise of ETBE is that it eliminates many of the historicalimpediments to the greater use of ethanol, such as increased volatility ofgasoline and incompatibility with gasoline pipelines. This would allowETBE to be used at the refinery level and be economically transportedto areas that previously had not been able to utilize ethanol (Governors’Ethanol Coalition, 2007).

40

978–0–19–956578–8 00-ADB-2-Main-drv African Development Bank2 (Typeset by SPi, Chennai) 41 of 233 July 29, 2009 15:25

Oil and Gas in Africa

iv. Organic waste material can be converted intoenergy forms, which can be used as automotivefuel: waste oil (such as cooking oil) into biodiesel;animal manure and organic household wastes intobiogas (such as methane); and agricultural andforestry waste products into ethanol.

Countries such as Argentina, Brazil, Canada, Colombia,India, Malaysia, Mozambique, the Philippines, Thailand,and the United States of America have been promotingand boosting the production and use of biofuels (bio-diesel from soy bean palm and jatropha; ethanol fromsugar cane and others) and LNG as a coping mechanismfor high oil prices. Most of these countries have adoptedtargets for increasing the contribution of biofuels to theirtransport fuel supplies. In terms of production costs,ethanol from sugar cane has historically been the lowest-cost biofuel. However, recent surges in world sugar priceshave altered the relative economics of biofuels, with bio-diesel from palm oil emerging as potentially more viableunder certain market conditions (Chow, 2007).

2.3 Africa’s Oil Reserves and Production

2.3.1 Reserves

Reserves are defined as the known and estimated quan-tity in units of oil or gas that can be produced. Thecertainty to which we know the quantities defines thecategory of reserves. As outlined in Section 2.1, there

41

978–0–19–956578–8 00-ADB-2-Main-drv African Development Bank2 (Typeset by SPi, Chennai) 42 of 233 July 29, 2009 15:25

Oil and Gas in Africa

are proven, probable, and possible reserves. It shouldthus be noted that a reserve estimate is dynamic andcan change depending on the current technology level,economic conditions (for instance, the price of selling oilversus the costs of extracting it), location, and associatedenvironmental issues.

The most common notion of “proved reserves”—declared quantities known to a high level of confidencein terms of primarily geological data—is used in thisreport. However, it is worth noting that even with thispresumably physical and measurable estimation, dataon oil and gas resources from geological resources maybe inaccurate for a number of reasons, including: weakgovernment capacity to monitor oil companies (whichmay not wish to have an accurate data disclosure); geo-political interests of governments (who may not wanta full disclosure either); or lack of geological surveydata.

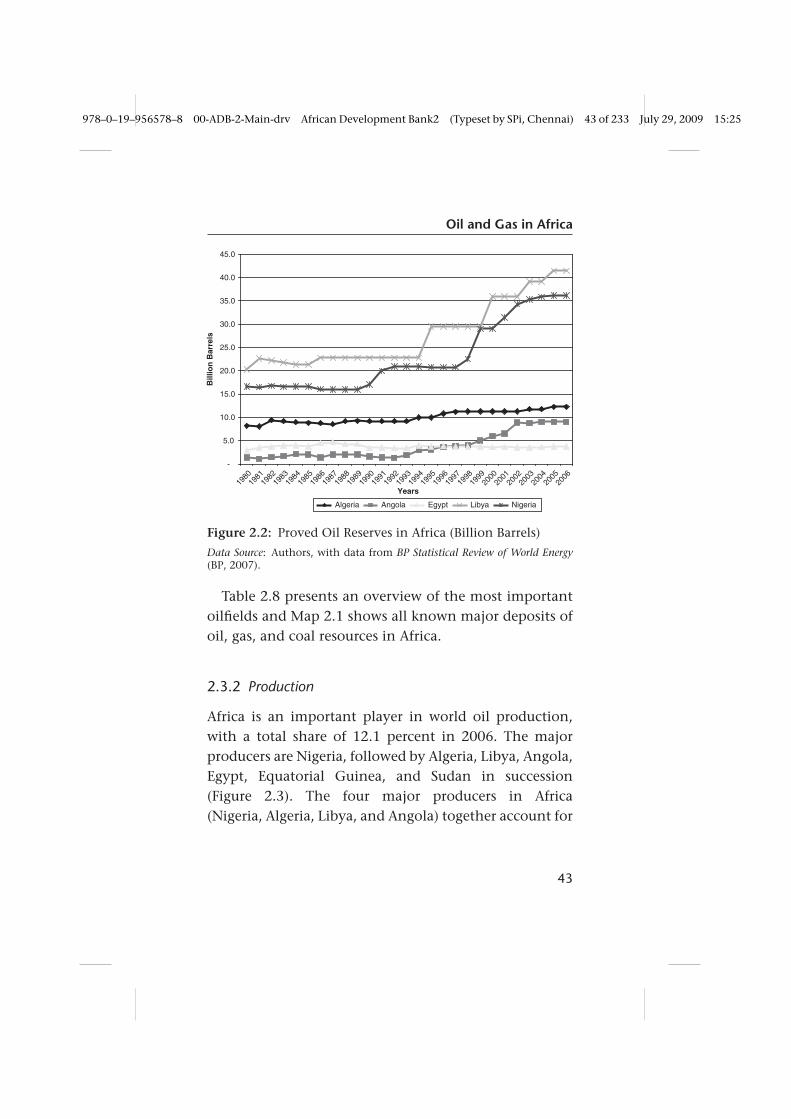

Figure 2.2 presents an overview of proved oil reservesin Africa. The majority of African oil reserves (and pro-duction) is located in Libya, Nigeria, Algeria, Angola,and Sudan, which together account for more than 90percent of the continent’s reserves. There is growingknowledge about Africa’s proved oil reserves, which rosefrom 53.3 billion barrels in 1980 to 117.2 billion barrelsin 2006, a share of 9.7 percent of total world reserves. Thelargest reserves are in Libya and Nigeria, which accountfor 3.4 and 3.0 percent, respectively, of world reserves(BP, 2007).

42

978–0–19–956578–8 00-ADB-2-Main-drv African Development Bank2 (Typeset by SPi, Chennai) 43 of 233 July 29, 2009 15:25

Oil and Gas in Africa

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

Years

Bill

ion

Bar

rels

Algeria Angola Egypt Libya Nigeria

Figure 2.2: Proved Oil Reserves in Africa (Billion Barrels)

Data Source: Authors, with data from BP Statistical Review of World Energy(BP, 2007).

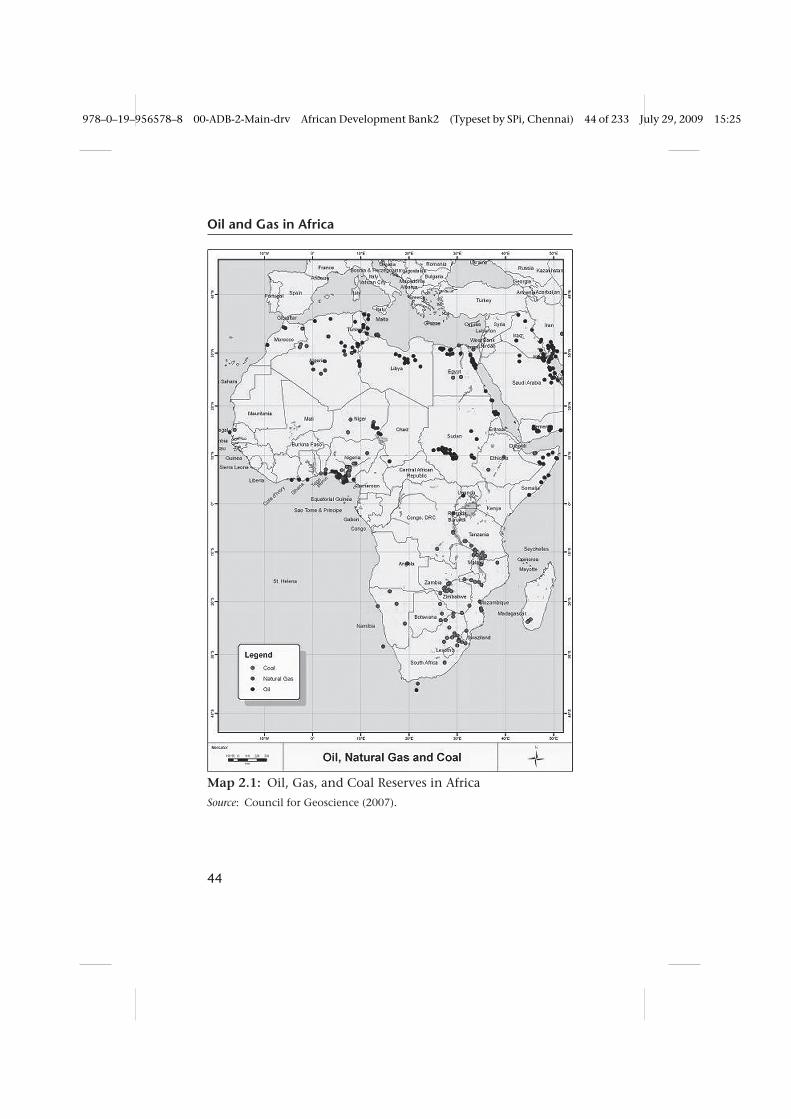

Table 2.8 presents an overview of the most importantoilfields and Map 2.1 shows all known major deposits ofoil, gas, and coal resources in Africa.

2.3.2 Production

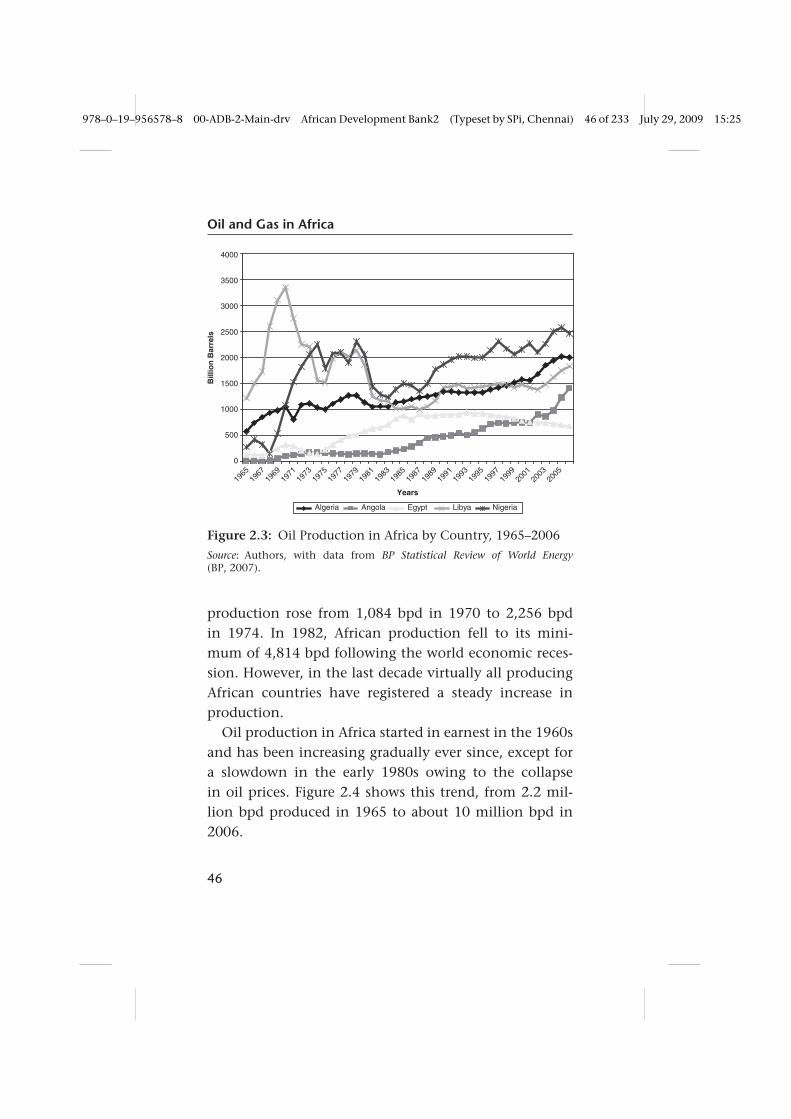

Africa is an important player in world oil production,with a total share of 12.1 percent in 2006. The majorproducers are Nigeria, followed by Algeria, Libya, Angola,Egypt, Equatorial Guinea, and Sudan in succession(Figure 2.3). The four major producers in Africa(Nigeria, Algeria, Libya, and Angola) together account for

43

978–0–19–956578–8 00-ADB-2-Main-drv African Development Bank2 (Typeset by SPi, Chennai) 44 of 233 July 29, 2009 15:25

Oil and Gas in Africa

Map 2.1: Oil, Gas, and Coal Reserves in Africa

Source: Council for Geoscience (2007).

44

978–0–19–956578–8 00-ADB-2-Main-drv African Development Bank2 (Typeset by SPi, Chennai) 45 of 233 July 29, 2009 15:25

Oil and Gas in Africa

Table 2.8: Major African Oil Fields, 2007

State Deposit Name Size of Resource(Barrels)

Status

Algeria Hassi MessaoudNorth & South

>300 million Continuouslyproducing

Algeria Rhourde El Baguel;Hassi BerkineSouth; ZarzanTine;and Edj’leh

All 4 resources:160–300 million

Continuouslyproducing (all)

Angola 29 offshore andonshore blocks

Several resources>160 millionwithin blocks

Some producing

Chad Doba 160–300 million Deposit neverexploited

Egypt El Morgan; and JulyOilfield

160–300 million Continuouslyproducing

Gabon Emeraude; Loango >300 millionLibya Zelten 160–300 million Derelict mineLibya Waha; Amal; Serir;

Gialo; and DahraAll resources:

160–300 millionContinuously

producing (all)Morocco Meskalia 160–300 million Continuously

producingNigeria Usan; Ukot; Aparo;

Agabami; andBonga Sw

All resources: 160million

Continuouslyproducing (all)

Nigeria Jones Creek 160–300 million Continuouslyproducing

Tunisia El Borma 160–300 million Continuouslyproducing

Data Source: Council for Geoscience and Mintek (2007).

77 percent of the continent’s production and contribute9.2 percent to world oil production.

Figure 2.3 illustrates the trend of oil productionin Africa. It is worth noting that Libyan productiondropped sharply from 3,300 barrels per day (bpd) in1970 to 1,514 bpd in 1975. At the same time, Nigerian

45

978–0–19–956578–8 00-ADB-2-Main-drv African Development Bank2 (Typeset by SPi, Chennai) 46 of 233 July 29, 2009 15:25

Oil and Gas in Africa

0

500

1000

1500

2000

2500

3000

3500

4000

1965

1967

1969

1971

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

Years

Bill

ion

Bar

rels

Algeria Angola Egypt Libya Nigeria

Figure 2.3: Oil Production in Africa by Country, 1965–2006

Source: Authors, with data from BP Statistical Review of World Energy(BP, 2007).

production rose from 1,084 bpd in 1970 to 2,256 bpdin 1974. In 1982, African production fell to its mini-mum of 4,814 bpd following the world economic reces-sion. However, in the last decade virtually all producingAfrican countries have registered a steady increase inproduction.

Oil production in Africa started in earnest in the 1960sand has been increasing gradually ever since, except fora slowdown in the early 1980s owing to the collapsein oil prices. Figure 2.4 shows this trend, from 2.2 mil-lion bpd produced in 1965 to about 10 million bpd in2006.

46

978–0–19–956578–8 00-ADB-2-Main-drv African Development Bank2 (Typeset by SPi, Chennai) 47 of 233 July 29, 2009 15:25

Oil and Gas in Africa

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

1100019

65

1967

1969

1971

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

Th

ou

san

d b

arre

ls d

aily

Figure 2.4: Africa’s Average Oil Production per Year (DailyProduction, bpd)

Data Source: BP Statistical Review of World Energy (BP, 2007).

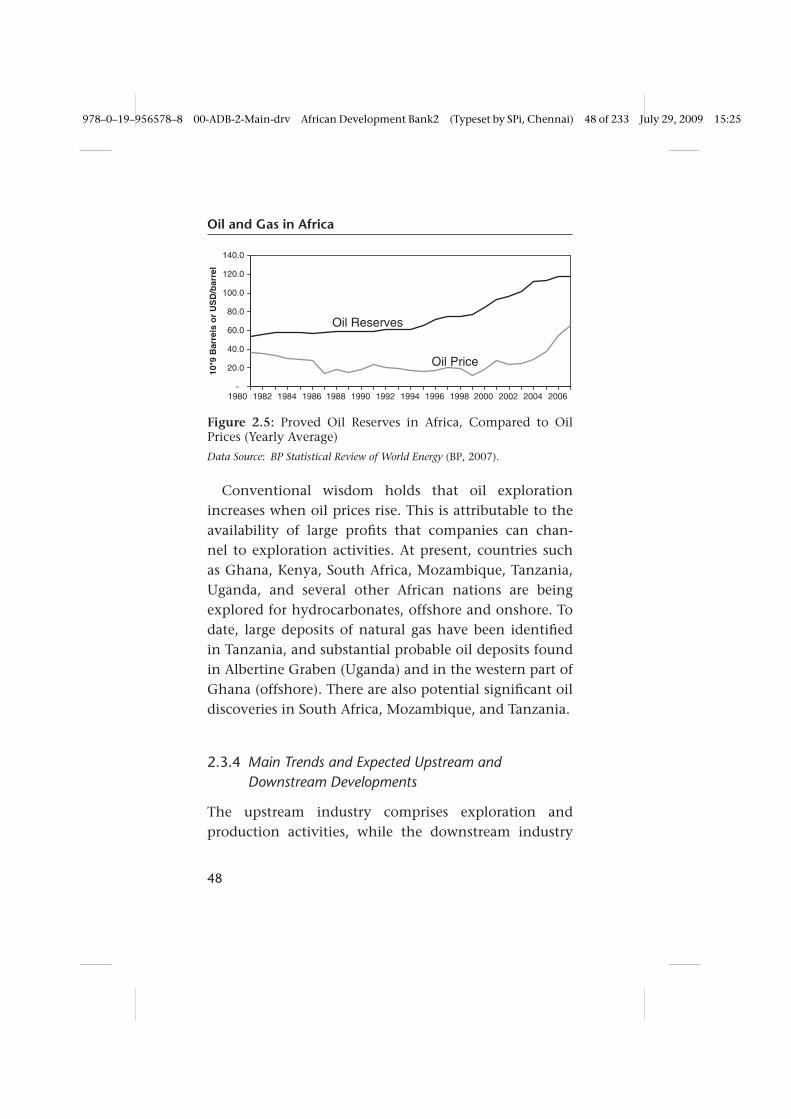

2.3.3 Exploration and Planned Production

Oil exploration activities are generally led by oil com-panies. It is rare for governments to directly lead theseactivities, although nationalized or state-run oil compa-nies are often involved. Oil exploration efforts in Africahave been boosted significantly in recent years, as illus-trated by the rate at which proved reserves are growingover time. Figure 2.5 presents an overview of cumulativeknown reserves in Africa and illustrates the close corre-lation with the gradual rise in oil prices over the last 10years. It is worth noting, however, that exploration, aswell as estimates of reserves, increased gradually even inthe 1980s, when oil prices were declining—most likelyillustrating that exploration in Africa was underpinnedby geopolitical and oil supply security motives (mostlyfrom Western nations, in the early phase, but, increas-ingly, with emerging countries such as China).

47

978–0–19–956578–8 00-ADB-2-Main-drv African Development Bank2 (Typeset by SPi, Chennai) 48 of 233 July 29, 2009 15:25

Oil and Gas in Africa

-

20.0

40.0

60.0

80.0

100.0

120.0

140.0

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006

10*9

Bar

rels

or

US

D/b

arre

l

Oil Price

Oil Reserves

Figure 2.5: Proved Oil Reserves in Africa, Compared to OilPrices (Yearly Average)

Data Source: BP Statistical Review of World Energy (BP, 2007).

Conventional wisdom holds that oil explorationincreases when oil prices rise. This is attributable to theavailability of large profits that companies can chan-nel to exploration activities. At present, countries suchas Ghana, Kenya, South Africa, Mozambique, Tanzania,Uganda, and several other African nations are beingexplored for hydrocarbonates, offshore and onshore. Todate, large deposits of natural gas have been identifiedin Tanzania, and substantial probable oil deposits foundin Albertine Graben (Uganda) and in the western part ofGhana (offshore). There are also potential significant oildiscoveries in South Africa, Mozambique, and Tanzania.

2.3.4 Main Trends and Expected Upstream andDownstream Developments

The upstream industry comprises exploration andproduction activities, while the downstream industry

48

978–0–19–956578–8 00-ADB-2-Main-drv African Development Bank2 (Typeset by SPi, Chennai) 49 of 233 July 29, 2009 15:25

Oil and Gas in Africa

0

500

1000

1500

2000

2500

3000

3500

1965

1967

1969

1971

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

10*3

Bar

rels

dai

ly

Total Refinery Capacity

Total Consumption

Figure 2.6: Total Oil Consumption and Refinery Capacity inAfrica

Data Source: BP Statistical Review of World Energy (BP, 2006).

includes refining and retail activities. Oil refineries con-vert crude oil into fuel products, lubricating oils, bitu-men, chemical feedstocks and other oil products (seeSection 2.2).

The first African refineries were built in Algiers(CFP/Total) and Durban (Socony/Mobil) in 1954. In the50 years up to 2004, a total of 48 refineries were built inAfrica. However, the majority of them were establishedin the 1970s and 1980s. The only new refineries builtin the last 10 years were Khartoum (Sudan) in 2001 andMIDOR (Egypt) in 2002. Africa’s historic refinery capacityis presented in Figure 3.5. The continent’s total activedistillation capacity is about 3 million bpd (15 millionmt/yr), an average of 79,000 bpd per refinery (Figure 2.6).

The major refining centers in Africa are located inSouth Africa (4 refineries and 3 synthetic fuel plants),Nigeria (3 refineries), Egypt (9 refineries), and Algeria(4 refineries) (Figure 2.7). The largest single refinery is

49

978–0–19–956578–8 00-ADB-2-Main-drv African Development Bank2 (Typeset by SPi, Chennai) 50 of 233 July 29, 2009 15:25

Oil and Gas in Africa

Figure 2.7: Refining Centers in Sub-Saharan Africa

Source: African Energy (2008).

the Skikda refinery in Algeria (300 million bpd), whereasthe smallest operating refinery is the Solimar refinery inMadagascar, with a capacity of 14 million bpd (AfricanEnergy, 2008).

Many African refineries have been forced to closebecause of low worldwide refining margins, small localmarkets, high operating costs (due to small size), andpoor yields. Following the World Bank/IMF insistenceon market liberalization in the early 1980s, many ofthe remaining refineries have faced significant chal-lenges. Although installed capacity in Africa is higherthan present consumption (Figure 2.6), the continent

50

978–0–19–956578–8 00-ADB-2-Main-drv African Development Bank2 (Typeset by SPi, Chennai) 51 of 233 July 29, 2009 15:25

Oil and Gas in Africa

still faces high shortages in refined products that arebalanced by imports. As a consequence of such short-ages and of the need to maximize economic profit byplacing the refinery close to the source, several initiativesand plans are underway to install new refineries in suchcountries as Nigeria, Sudan, Uganda, and Mozambique,as outlined in Boxes 2.1 to 2.4.

Box 2.1: THE EXAMPLE OF NIGERIA’S REFINERY INDUSTRY

There are considerable investment opportunities in Nigeria’s down-stream oil and gas sector. The government’s focus is on deregulatingthe sector by licensing private refineries, eliminating government subsi-dies to the downstream sector, and privatizing existing ones. Throughsuch strategic action, domestic capacity is expected to at least meetdemand. The four existing refineries have significantly and consistentlyproduced below capacity, owing to a host of factors, including poormanagement and maintenance.

The deregulation of the downstream oil and gas sector (PetroleumRefining & Marketing) has been in focus for a number of years. Indeed,scarcity of petroleum products and gradual deregulation of petroleumproduct prices have generated heated controversies in Nigeria. Thegovernment is determined to nurture private-sector participation andengage local companies in the oil and gas sector—hence the licensingof private refineries and deregulation of petroleum product prices—toimprove local capacity. In the coming years, consolidation is expectedin the oil refining and marketing sector, with new entrants. There aresignificant investment opportunities and a need for both local andinternational funding.

Sahara Petroleum Exploration, a subsidiary of Global EnvironmentalEnergy, has been contracted to build a 70,000 bpd oil refinery at Eket,Akwa Ibom state, Nigeria.

This is an approximately $4 billion project that represents cash flowat today’s market rate of approximately $1.5 billion per annum. Suchplans to increase Nigeria’s refining capacity will also provide consider-able cost savings to operators (such as Sahara Petroleum) by refiningoil products close to source. At present, the country has four mainrefineries with a nameplate capacity of 438,750 bpd.

Data Sources: Market Research (2008) and Onlinenigeria.com (2005).

51

978–0–19–956578–8 00-ADB-2-Main-drv African Development Bank2 (Typeset by SPi, Chennai) 52 of 233 July 29, 2009 15:25

Oil and Gas in Africa

Box 2.2: TULLOW OIL REFINERY PLAN IN UGANDA

Tullow Oil is currently working to find out the quantity and qualityof oil that has been discovered in the Albertine Graben in Ugandabefore a decision is made to build a multi-billion dollar refinery or not.The Uganda government and Tullow Oil have agreed to build a minirefinery in an early production scheme that will enable installation ofa 100 MW heavy fuel oil thermal power plant. The mini refinery (witha capacity of about 5,000 barrels of oil per day) will cost Tullow someUS$200 million.

Data Source: Kisambira (2007).

Box 2.3: SUDAN TO DOUBLE ITS OIL-REFINING CAPACITY

Sudan is planning to double its oil refining capacity, with a short,three-year investment plan, to handle increased production, havingreached an agreement to end its 21-year civil war. A new 100,000bpd refinery will be built in Port Sudan, on the Red Sea coast, andthe capacity of two existing refineries will be increased. Talks havebeen held with India’s Oil & Natural Gas, China’s Sinopec, Malaysia’sPetronas, and an unidentified Turkish company to build the newrefinery. Boosting refinery capacity is especially timely since Sudanexpects crude oil production to increase significantly in the comingyears.

Data Source: Chmaytelli (2005).

Box 2.4: NEW MOZAMBIQUE OIL REFINERY APPROVED

The Mozambican Council of Ministers has approved the constructionof an oil refinery, valued at more than $1.3 billion, in the northernprovince of Nampula. Dubbed the ‘Ayr Logistics Limited—Nacala’,the project is spearheaded by a privately owned American company,Ayr Logistics, in partnership with one Mozambican and three SouthAfrican investors. The project is expected to create about 450 jobs andgenerate extra tax revenue for the Mozambican government. With aninstalled capacity of about 100,000 bbl/d, most of the product will beexported to Malawi, Zimbabwe, and Zambia. The project also includesthe construction of several infrastructures that will support the main

52

978–0–19–956578–8 00-ADB-2-Main-drv African Development Bank2 (Typeset by SPi, Chennai) 53 of 233 July 29, 2009 15:25

Oil and Gas in Africa

activity of the project, which will be implemented over an area of838 ha and will be situated in the district of the Nacala port, whichis also home to Mozambique’s deepest and busiest port.

Data Source: Engineering News (2007).

Despite the plans and visions illustrated in the boxes, thefact remains that very little new global refining capacityhas been added in the last three years, including in 2007.Nevertheless, significant refinery capacity additions arestill planned, although a major concern is that construc-tion costs are rising with inflationary prices. Other non-economic reasons—important in Africa, as elsewhere—for the slow growth in refining capacity (worldwide) areenvironmental and local concerns, more stringent envi-ronmental laws, and effective community organizing,which have made it very difficult to build new refineries.Some analysts consider refinery capacity a significantfactor of high oil prices. It thus makes sense to increaserefinery capacity in Africa as a way to reduce the costs ofrefined oil products. However, this needs to be done inan environment-friendly manner.

2.4 Oil Trade in Africa

The oil market can be divided into two parts: withinAfrica and between Africa and the rest of the world.The major trends are clear: There is significant oil tradewithin West Africa and North Africa, whereas there isvery little oil trade between African producers and the

53

978–0–19–956578–8 00-ADB-2-Main-drv African Development Bank2 (Typeset by SPi, Chennai) 54 of 233 July 29, 2009 15:25

Oil and Gas in Africa

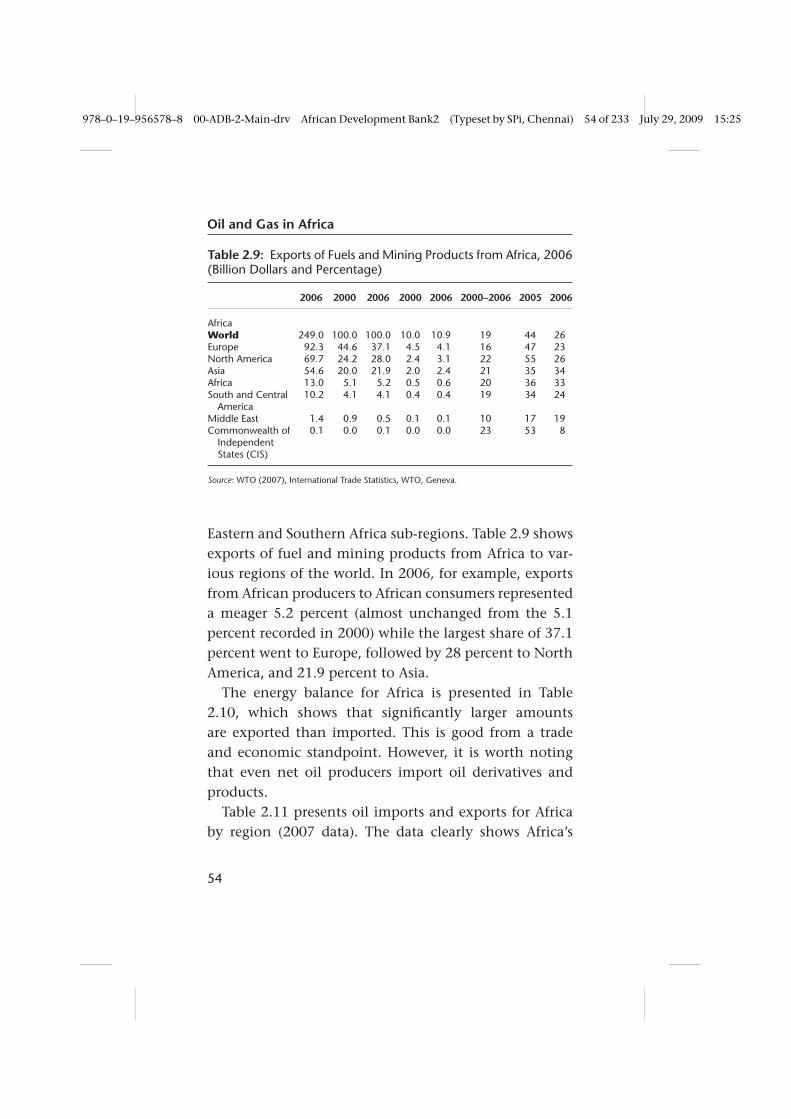

Table 2.9: Exports of Fuels and Mining Products from Africa, 2006(Billion Dollars and Percentage)

2006 2000 2006 2000 2006 2000–2006 2005 2006

AfricaWorld 249.0 100.0 100.0 10.0 10.9 19 44 26Europe 92.3 44.6 37.1 4.5 4.1 16 47 23North America 69.7 24.2 28.0 2.4 3.1 22 55 26Asia 54.6 20.0 21.9 2.0 2.4 21 35 34Africa 13.0 5.1 5.2 0.5 0.6 20 36 33South and Central

America10.2 4.1 4.1 0.4 0.4 19 34 24

Middle East 1.4 0.9 0.5 0.1 0.1 10 17 19Commonwealth of

IndependentStates (CIS)

0.1 0.0 0.1 0.0 0.0 23 53 8

Source: WTO (2007), International Trade Statistics, WTO, Geneva.

Eastern and Southern Africa sub-regions. Table 2.9 showsexports of fuel and mining products from Africa to var-ious regions of the world. In 2006, for example, exportsfrom African producers to African consumers representeda meager 5.2 percent (almost unchanged from the 5.1percent recorded in 2000) while the largest share of 37.1percent went to Europe, followed by 28 percent to NorthAmerica, and 21.9 percent to Asia.

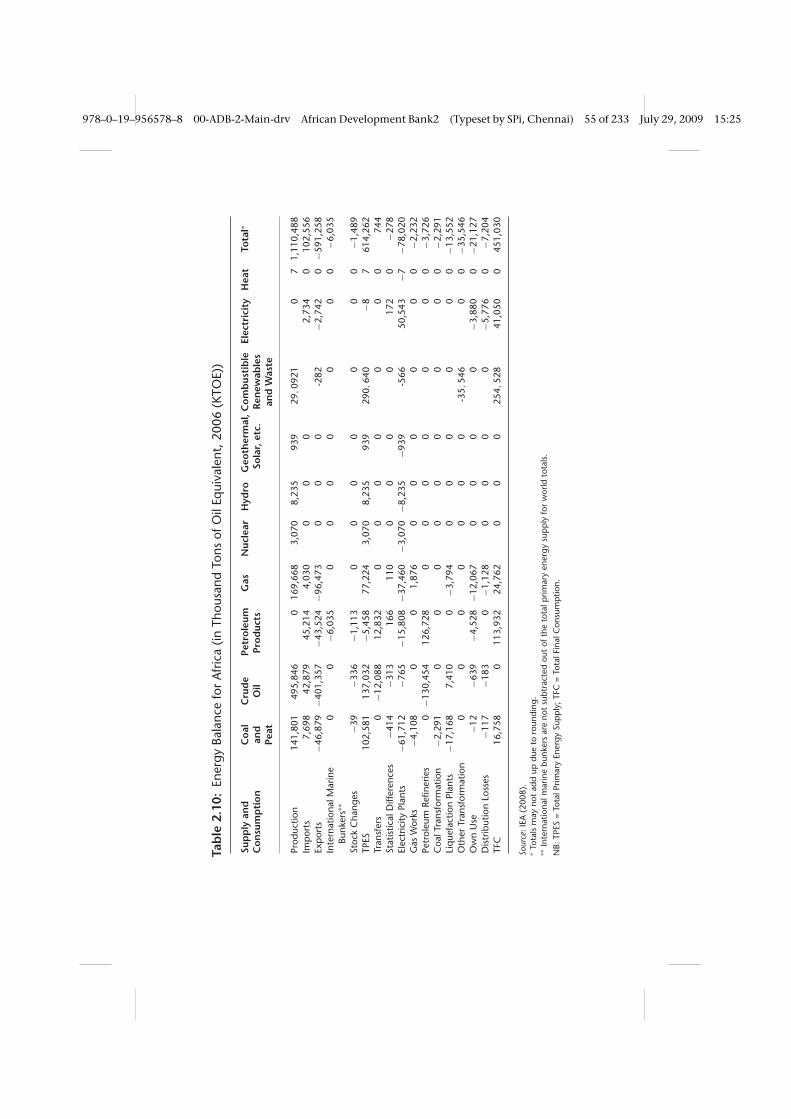

The energy balance for Africa is presented in Table2.10, which shows that significantly larger amountsare exported than imported. This is good from a tradeand economic standpoint. However, it is worth notingthat even net oil producers import oil derivatives andproducts.

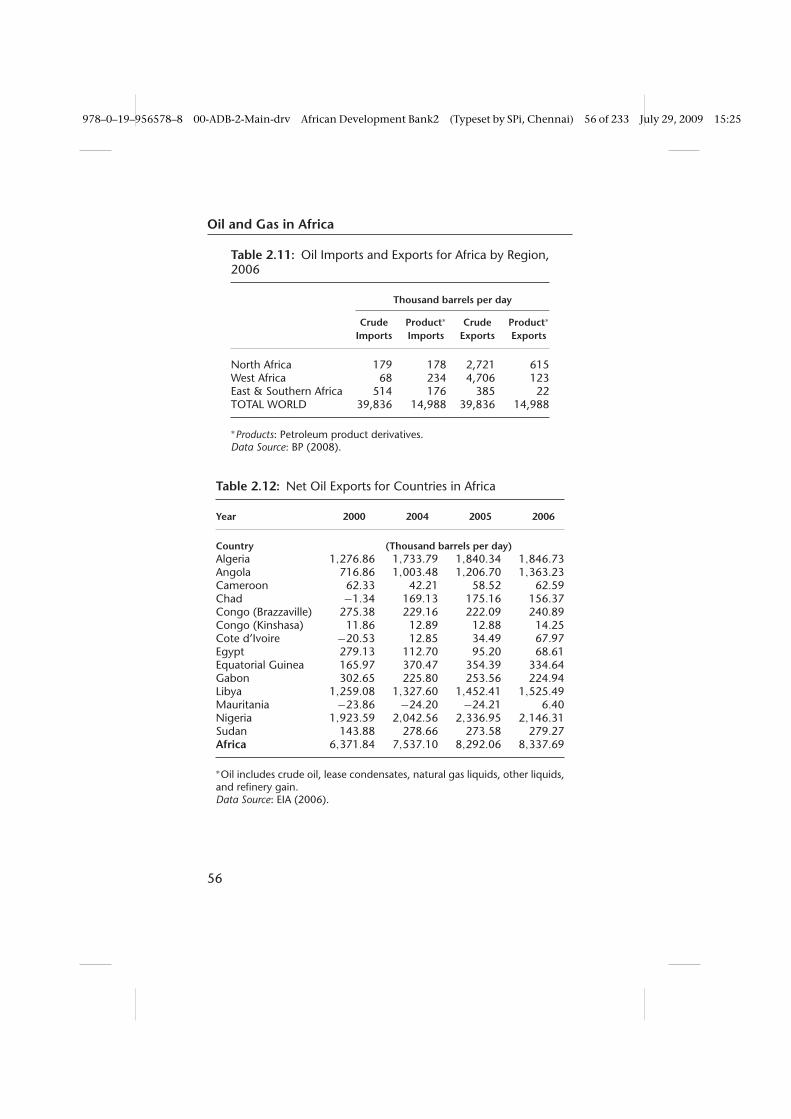

Table 2.11 presents oil imports and exports for Africaby region (2007 data). The data clearly shows Africa’s

54

978–0–19–956578–8 00-ADB-2-Main-drv African Development Bank2 (Typeset by SPi, Chennai) 55 of 233 July 29, 2009 15:25

Tab

le2.

10:

Ener

gyBa

lanc

efo

rA

fric

a(in

Thou

sand

Tons

ofO

ilEq

uiva

lent

,200

6(K

TOE)

)

Sup

ply

and

Co

nsu

mp

tio

nC

oal

and

Peat

Cru

de

Oil

Petr

ole

umPr

od

ucts

Gas

Nuc

lear

Hyd

roG

eoth

erm

al,

Sola

r,et

c.C

om

bus

tib

leR

enew

able

san

dW

aste

Elec

tric

ity

Hea

tTo

tal∗

Prod

uctio

n14

1,80

149

5,84

60

169,

668

3,07

08,

235

939

29,09

210

71,

110,

488

Imp

orts

7,69

842

,879

45,2

144,

030

00

02,

734

010

2,55

6Ex

por

ts−4

6,87

9−4

01,3

57−4

3,52

4−9

6,47

30

00

-282

−2,7

420

−591

,258

Inte

rnat

iona

lMar

ine

Bunk

ers∗

∗0

0−6

,035

00

00

00

0−6

,035

Stoc

kC

hang

es−3

9−3

36−1

,113

00

00

00

0−1

,489

TPES

102,

581

137,

032

−5,4

5877

,224

3,07

08,

235

939

290,

640

−87

614,

262

Tran

sfer

s0

−12,

088

12,8

320

00

00

00

744

Stat

istic

alD

iffer

ence

s−4

14−3

1316

611

00

00

017

20

−278

Elec

tric

ityPl

ants

−61,

712

−765

−15,

808

−37,

460

−3,0

70−8

,235

−939

-566

50,5

43−7

−78,

020

Gas

Wor

ks−4

,108

00

1,87

60

00

00

0−2

,232

Petr

oleu

mRe

finer

ies

0−1

30,4

5412

6,72

80

00

00

00

−3,7

26C

oalT

rans

form

atio

n−2

,291

00

00

00

00

0−2

,291

Liq

uefa

ctio

nPl

ants

−17,

168

7,41

00

−3,7

940

00

00

0−1

3,55

2O

ther

Tran

sfor

mat

ion

00

00

00

0-3

5,54

60

0−3

5,54

6O

wn

Use

−12

−639

−4,5

28−1

2,06

70

00

0−3

,880

0−2

1,12

7D

istr

ibut

ion

Loss

es−1

17−1

830

−1,1

280

00

0−5

,776

0−7

,204

TFC

16,7

580

113,

932

24,7

620

00

254,

528

41,0

500

451,

030

Sour

ce:I

EA(2

008)

.∗

Tota

lsm

ayno

tad

dup

due

toro

undi

ng.

∗∗In

tern

atio

nalm

arin

ebu

nker

sar

eno

tsu

btra

cted

out

ofth

eto

talp

rimar

yen

ergy

sup

ply

for

wor

ldto

tals

.N

B:TP

ES=

Tota

lPrim

ary

Ener

gySu

pp

ly;T

FC=

Tota

lFin

alC

onsu

mp

tion.

978–0–19–956578–8 00-ADB-2-Main-drv African Development Bank2 (Typeset by SPi, Chennai) 56 of 233 July 29, 2009 15:25

Oil and Gas in Africa

Table 2.11: Oil Imports and Exports for Africa by Region,2006

Thousand barrels per day

Crude Product∗ Crude Product∗

Imports Imports Exports Exports

North Africa 179 178 2,721 615West Africa 68 234 4,706 123East & Southern Africa 514 176 385 22TOTAL WORLD 39,836 14,988 39,836 14,988

∗Products: Petroleum product derivatives.Data Source: BP (2008).

Table 2.12: Net Oil Exports for Countries in Africa

Year 2000 2004 2005 2006

Country (Thousand barrels per day)Algeria 1,276.86 1,733.79 1,840.34 1,846.73Angola 716.86 1,003.48 1,206.70 1,363.23Cameroon 62.33 42.21 58.52 62.59Chad −1.34 169.13 175.16 156.37Congo (Brazzaville) 275.38 229.16 222.09 240.89Congo (Kinshasa) 11.86 12.89 12.88 14.25Cote d’Ivoire −20.53 12.85 34.49 67.97Egypt 279.13 112.70 95.20 68.61Equatorial Guinea 165.97 370.47 354.39 334.64Gabon 302.65 225.80 253.56 224.94Libya 1,259.08 1,327.60 1,452.41 1,525.49Mauritania −23.86 −24.20 −24.21 6.40Nigeria 1,923.59 2,042.56 2,336.95 2,146.31Sudan 143.88 278.66 273.58 279.27Africa 6,371.84 7,537.10 8,292.06 8,337.69

∗Oil includes crude oil, lease condensates, natural gas liquids, other liquids,and refinery gain.Data Source: EIA (2006).

56

978–0–19–956578–8 00-ADB-2-Main-drv African Development Bank2 (Typeset by SPi, Chennai) 57 of 233 July 29, 2009 15:25

Oil and Gas in Africa

limited significance with respect to imports as well asto derived products, but its very significant contributionto basic world crude oil exports. Table 2.12 presentsexport data from 2000 to 2006 for the 14 African netoil-producing countries.

It should be noted that only two of the 14 net oil-exporting African countries are landlocked (Chad andMauritania). Marketing (exporting) crude oil from alandlocked country is an added challenge for an investor.The case of Chad (Box 2.5) illustrates an effort to solvethis problem.

Box 2.5: CHAD–CAMEROON PIPELINE

Chad has a long history of civil war and exhibits many conditionsassociated with post-conflict zones. To overcome its geographic dis-advantage of being landlocked, Chad needed a pipeline to exploitits over one billion barrels in proven oil reserves. In 1999, conditionsinside Chad were so bad that no one in the private oil sector waswilling to invest in a pipeline unless the World Bank was involved.In the first project of its kind, the World Bank agreed to provideinvestment coupled with institutional oversight and transparency (U.S.Department of Energy, 2007b). The World Bank and a consortium ofoil companies, led by ExxonMobil, ChevronTexaco, and Petronas, setup a pipeline project in Chad.

Construction of the $3.5 billion Chad–Cameroon Petroleum Devel-opment and Pipeline Project began in 2000 and was completed in2004. To increase transparency, Chad was required to adopt thePetroleum Revenues Management Law, which stipulated that Chad’s12.5 percent of the oil revenues would be deposited into a Citibankescrow account monitored by an independent “college” before theChadian government received it. Another 10 percent was deposited ina “future generations” fund to provide Chad with revenues after theexhaustion of the oil reserves (Zissis, 2007). However, in December2005, Chad’s National Assembly abolished the future generations fundand diverted money away from poverty-mitigation efforts to armspurchase. The World Bank responded by suspending $124 million inloans.

(cont.)

57

978–0–19–956578–8 00-ADB-2-Main-drv African Development Bank2 (Typeset by SPi, Chennai) 58 of 233 July 29, 2009 15:25

Oil and Gas in Africa

Box 2.5: (Continued)

In July 2006, the two sides reached a compromise, which specified thatthe Chadian government would commit 70 percent of revenues todevelopment programs and 30 percent to government expenditures(Thibodeaux, 2007). Some have called the Chad experiment a primafacie failure; others maintain that after only a few years it is still tooearly to judge.

2.5 Africa’s Consumption of Oil

Figure 2.8 shows the growing pattern of oil product typeconsumption in Africa. Consumption of oil derivates inAfrica has grown steadily, with total consumption in2006 close to 3 million barrels per day. However, thisonly represents about 3 percent of world consumption.

0

500

1000

1500

2000

2500

3000

1965 1968 1971 1974 1977 1980 1983 1986 1989 1992 1995 1998 2001 2004

10*3

Bar

rels

dai

ly

Light distillates Fuel oilMiddle distillatesOthers Total Africa

Figure 2.8: Africa’s Oil Consumption by Product Type (barrelsper day)

Data Source: BP (2008).

58

978–0–19–956578–8 00-ADB-2-Main-drv African Development Bank2 (Typeset by SPi, Chennai) 59 of 233 July 29, 2009 15:25

Oil and Gas in Africa

Table 2.13: World and Africa Total Proved Natural Gas Reserves,1986–2006

At end 1986 At end 1996 At end 2005 At end 2006(trillion cubic

meters)(trillion cubic

meters)(trillion cubic

meters)(trillion cubic

meters)

Algeria 3.26 3.70 4.50 4.50Egypt 0.29 0.85 1.90 1.94Libya 0.73 1.31 1.32 1.32Nigeria 2.40 3.48 5.15 5.21Other Africa 0.72 0.83 1.21 1.21Total Africa 7.40 10.17 14.08 14.18TOTAL WORLD 107.67 147.89 180.20 181.46

Data Source: BP (2007).

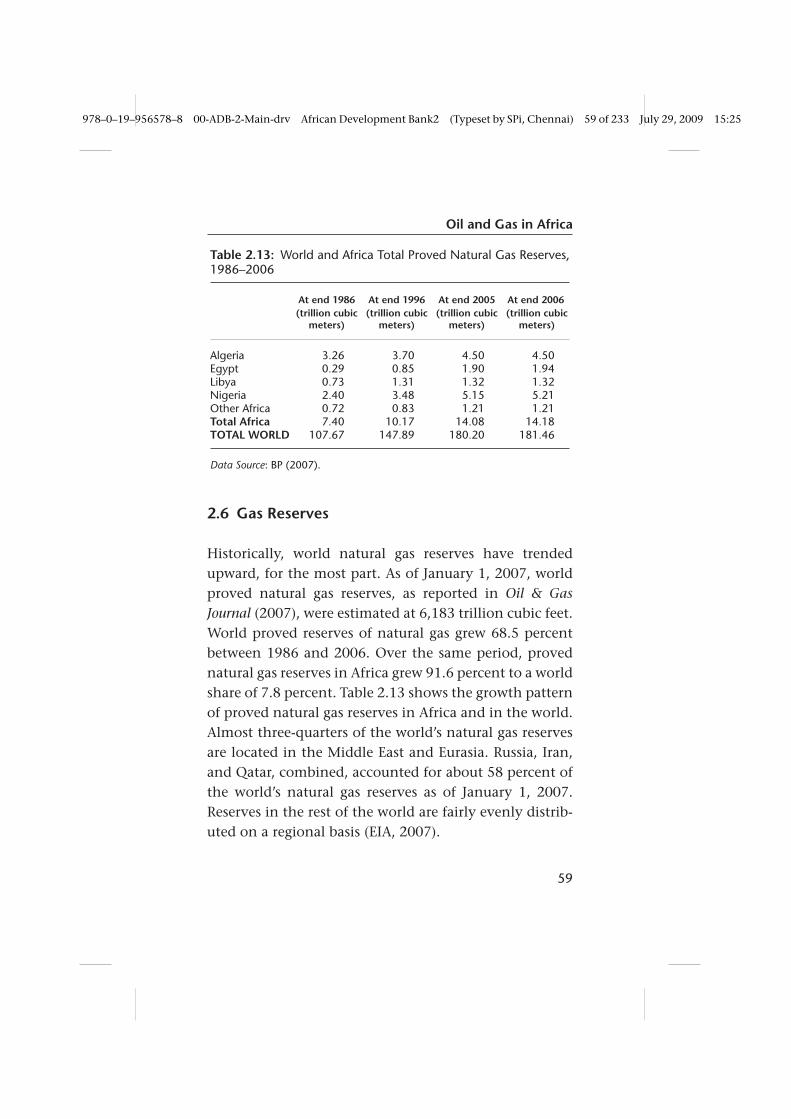

2.6 Gas Reserves

Historically, world natural gas reserves have trendedupward, for the most part. As of January 1, 2007, worldproved natural gas reserves, as reported in Oil & GasJournal (2007), were estimated at 6,183 trillion cubic feet.World proved reserves of natural gas grew 68.5 percentbetween 1986 and 2006. Over the same period, provednatural gas reserves in Africa grew 91.6 percent to a worldshare of 7.8 percent. Table 2.13 shows the growth patternof proved natural gas reserves in Africa and in the world.Almost three-quarters of the world’s natural gas reservesare located in the Middle East and Eurasia. Russia, Iran,and Qatar, combined, accounted for about 58 percent ofthe world’s natural gas reserves as of January 1, 2007.Reserves in the rest of the world are fairly evenly distrib-uted on a regional basis (EIA, 2007).

59

978–0–19–956578–8 00-ADB-2-Main-drv African Development Bank2 (Typeset by SPi, Chennai) 60 of 233 July 29, 2009 15:25

Oil and Gas in Africa

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

Years

Tri

llio

n C

ub

ic M

eter

s

Algeria Egypt Libya Nigeria Total Africa

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2007

2006

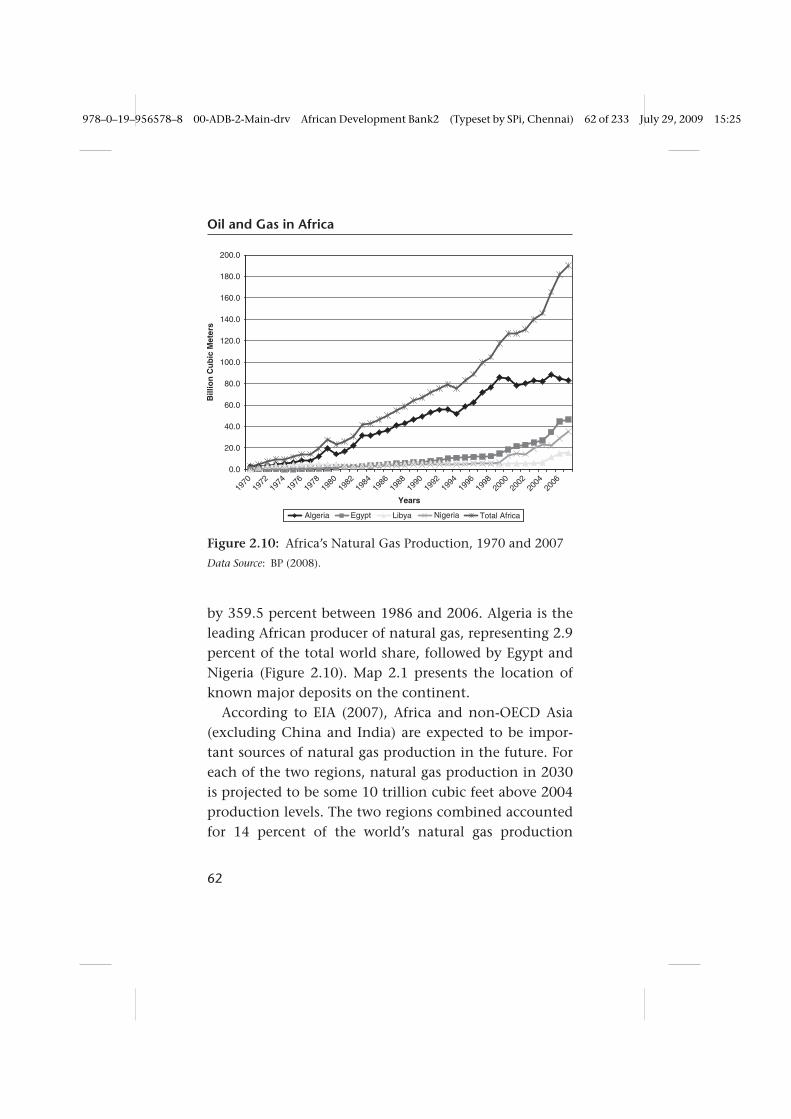

Figure 2.9: Africa’s Proved Natural Gas Reserves, 1980 and2007

Data Source: BP (2008).

Despite the high rates of increase in natural gasconsumption, particularly over the past decade, mostregional reserves-to-production ratios are substantial.Worldwide, the reserves-to-production ratio is estimatedat 65 years. Central and South America have a reserves-to-production ratio of about 52 years; Russia, 80 years;and Africa, 88 years. The reserves-to-production ratio ofthe Middle East exceeds 100 years (EIA, 2007).

Proved natural gas reserves in Africa are concen-trated mainly in four countries—Algeria, Egypt, Libya,and Nigeria—which possess 91.5 percent of provedreserves. Figure 2.9 presents the distribution pattern of

60

978–0–19–956578–8 00-ADB-2-Main-drv African Development Bank2 (Typeset by SPi, Chennai) 61 of 233 July 29, 2009 15:25

Oil and Gas in Africa

proved natural gas reserves per country in Africa. Theundeveloped natural gas reserves in Nigeria, in particu-lar, are a target of the international giants in the sector(Box 2.6).

Box 2.6: NIGERIA NATURAL GAS AT STAKE

Nigeria exports about 18 million tons of liquefied natural gas eachyear through Nigeria Liquefied Natural Gas, jointly owned by the stateenergy company, Shell, Total, and Agip. Nigeria has the seventh-largestproven gas reserves in the world, but it has not developed its gasindustry to anywhere near full potential.