Embed Size (px)

Citation preview

Assessment Practices and Procedures Office 1

Office

Last Document Review Date: September 29, 2014

TABLE OF CONTENTS

Executive Summary .............................................................................. 2

Compliance Checklist ............................................................................ 3

Processing Office Properties ................................................................... 4

General ............................................................................................ 4

Practices and Procedures .................................................................... 5

Appendix A: Frequently Asked Questions ............................................... 13

General FAQs .................................................................................. 13

BOMA Rentable Area FAQs – Link to BOMA ......................................... 14

Appendix B: Occupancy Descriptions ..................................................... 23

Foreword ........................................................................................ 23

Assessment Practices and Procedures Office 2

EXECUTIVE SUMMARY

The following properties, identified by actual use, are within scope:

o 203 – Stores and/or Offices with Apartments

o 204 – Store(s) and Offices o 208 – Office Building (Primary Use)

Office properties often hold non-office components, such as apartment, retail, or parking that have to be valued

separately from the office property itself.

Assessment Practices and Procedures Office 3

COMPLIANCE CHECKLIST

The following is a list of items that must be completed in order to be considered compliant with this document:

1. Where they are determined to be the highest and best use

(HBU), office properties as defined in this document are to be be valued using a capitalized NOI except:

a. A cost or DCA approach may be used in rural/remote

areas only when information to support an income valuation is not available.

b. A cost approach may be used for properties determined

not to be at HBU.

2. Offices will be Class 6 – business and other except for any component determined to be used for other non-office

purposes.

3. Improvements will be based on an improvement residual unless the property is an air space parcel or designated

heritage building, where a land residual will be used.

4. Office properties with additional components will use a

separate model for each significant non-office use (De

Minimus rule applies).

5. Market support must accompany any adjustments to the

base rate or model for market influencing characteristics (attributes) at the model level. For example, adjustments to

income, expense, vacancy, land, quality, view, etc., that

varies from the base rate or model for the competitive market set.

6. Do not record individual expense amounts.

7. Do not record an occupancy for each office tenant. Instead, summarize all tenants within the same occupancy into one

spreadsheet entry.

Assessment Practices and Procedures Office 4

PROCESSING OFFICE PROPERTIES

General

1. Valuation method(s):

a. Capitalized NOI – primary method.

b. Cost or DCA methods in rural and remote (unincorporated) areas only when information to

support an income valuation is not available.

c. Units of measure are dollar per square foot of gross leasable area or GLA for multi-tenant and single tenant

office properties.

d. GLA will be based on reported space and be consistently determined for all properties linked to a model.

CAUTION: Some office owners do not include vacant space

and as such, their reported information may be understated.

e. A building residual approach will be used to determine

the improvement value.

TIP

Inability to obtain information in a local market should not be the

deciding factor in selecting the cost or DCA methods. Market information for competitive properties in similar communities

within the region should first be investigated.

EXCEPTIONS:

o The cost method will be used for properties for which

the current use is not the HBU. o The land residual method will be used for value

apportionment in the case of air-space parcels and designated heritage buildings.

o Regions will develop a DCA value as a backup only when the market trades on this basis. A business case,

approved by the Executive will be required for GIM backup models.

Assessment Practices and Procedures Office 5

Practices and Procedures

1. Attach the necessary documents to the viewers as needed,

refer to Attachments (valueBC).

2. When completing the mandatory fields in the IncomeDCA Model viewer/Keypane, keep the following in mind:

Office properties with one or more non-office

component(s) will be valued through application of a

separate model and income record for each significant non-office use within the building.

The De Minimus rule will be applied to determine whether space devoted to non-office use is significant enough to

require creation of one or more additional income records (drawing rates from another model).

CAUTION: Be careful when applying the De Minimus rule, for example when a large office has a small area of storage

or limited parking, this area is included in order to reflect what is on the rent roll.

o Model Creation: a model should be designed to encompass the largest number of relatively similar

properties, within the geographically broadest possible

competitive market set. valueBC provides considerable flexibility to account for the diversity of buildings within

a specific model (e.g., income quality, size or suite mix, variable adjustments).

▪ The starting point for development of office models will be occupancy and region.

o Method: select CAP Direct Capitalization o Model Type: select OFF – Office

o Primary Model Use: select applicable occupancy (1800, 1801, 1802, 1803).

o Model Description: The model description will be based on the following naming convention, in the following

order:

▪ Occupancy Short Description

▪ Geographic Area that model applies – Region, Jur or

NBHD or smaller area (if necessary) ▪ Physical Attributes that further define model (if

necessary) ▪ Sub-Markets included (if any)

Assessment Practices and Procedures Office 6

- The Model Description will apply to space with

similar office rental amenities in mixed-use properties.

- Examples: Offices with Elevator – North Fraser Region

Office Blg C Class – Victoria – Pre 1960 Office Blg C Class – Vancouver CBD – 1 Sub-

Market Indus Flex Warehse – Vancouver Isl Region –

Small Towns and Rural Strata Res Low Rise – Downtown Poco to Pitt

River Rd Strata Res High Rise – Vancouver Nr Joyce St

Sky Train

o Additional information documenting the Model should be

placed in:

- Income-DCA Model viewer/Notes tab/Category: 08 – General.

TIP

While it is not strictly necessary to identify the occupancy and

geographic application of the model in the model name, addition of this information improves clarity when multiple models are

open at the same time.

3. When completing the mandatory fields in the Income DCA Model viewer/Occupancies and Adjustments tab, keep the

following in mind:

Enter a spreadsheet row for each required combination of

Quality and Unit of Measure by Unit of Measure order (e.g., Q1 GLA, Q2 GLA, Q3 GLA, etc.).

Size adjustment curve, general vacancy, non-variable adjustment, all model attribute adjustments, CAP rates

and adjustments, and effective age adjustments must have market support.

o On the Occupancy spreadsheet:

▪ Occupancy: select appropriate occupancy – refer to

occupancy definitions in Appendix B:

- 1800 Class D Office

- 1801 Class C Office - 1802 Class B Office

Assessment Practices and Procedures Office 7

- 1803 Class A Office

▪ Quality: select appropriate.

- Establish quality classes based on the properties

within the geographic competitive set. - Determine an average quality property from this

competitive set. - Determine the range of qualities required to

encompass the competitive set, (sub markets may be required if there is a rate differential

between areas for similar qualities of property. - The variance between qualities for additional

occupancy entries (new rows) should be significant, representing a differential of at least

five percent in net operating income. - In many cases, only two to three qualities may be

necessary to encompass a specific rental office

competitive set.

▪ Economic Rate: enter economic rate associated with

occupancy and quality.

- The economic rate for an occupancy, unit of

measure, and quality will be recorded to the nearest 25 cents per annualized period (annual).

- The economic rate will be determined from analysis of net lease information for the specific

competitive market set. The lease type will be based on the amount of expenses being passed

through and the industry standard associated with the competitive market set.

- Record the basis for economic rates (e.g. type of net lease) in the Income DCA Model viewer/Notes

tab.

- The economic rate for an occupancy and quality may be adjusted at the model and incomeDCA

record level to reflect non-typical obligations of the building owner or tenants within the

competitive market set.

▪ Unit of Measure: select GLA.

▪ Annualization: select An – Annual ▪ Size Adjustment Curve: select Size Adjustment

Curve if associated with the office model. ▪ Size curve, if used, must have market support.

Assessment Practices and Procedures Office 8

o On the General Vacancy/Occupancy field, enter general

vacancy as percentage of potential gross income directly (do not use detailed Vacancy).

▪ A vacancy entry in the occupancy spreadsheet will override the general vacancy field entry – use

general vacancy only.

o The General Expense field is a non-editable field that

shows the amount totals from the Expense and Adjustment tab.

o On the Non-Variable Adjustments spreadsheet:

- Record a non-variable adjustment only if the

feature is not captured in the economic rate for a specific occupancy and quality.

▪ Adjustment Type: select Rev or Vac (Revenue or Vacancy).

- Do not select Expense Adjustment Type at the

model level. If an expense adjustment is required for anomalies in the competitive set, apply the

adjustment at the income record level. Ensure you are not adjusting for a landlord’s poor or

superior management (value to owner). - Vacancy adjustments will be expressed as percent

of potential gross rental income.

▪ Attribute: select appropriate.

- Ensure that attribute is not included in economic rate for the specific model occupancy and quality

to avoid double adjusting.

▪ Value: enter appropriate value, e.g., “Y” for presence

or “N” for absence of most attributes, (other attributes, such as basement, require "Finished" or

"Unfinished", etc.)

▪ Dollar Value/Percent: enter dollar/percent amount adjustment to economic rate.

- Use dollar adjustments to apply lump-sum adjustments only for market attributes (expressed

in dollars) which are relatively stable over several years. It will still be necessary to review dollar

adjustments on an annual basis along with associated economic-market rates. Examples of

Assessment Practices and Procedures Office 9

dollar adjustments to economic rates may be

“heat not included” or “parking”. - Use percent adjustments to apply relationship

adjustments only for market attributes which are potentially unstable over the long-term (actual

dollar amounts will fluctuate). Examples of percent adjustments may be location or view.

Percentage adjustments will not likely require review as frequently as dollar adjustments.

- Dollar and percent adjustments will be applied consistently for all ICI models in a region on a

property specific basis. See Appendix A.

o On the Variable Adjustments spreadsheet:

- Extreme caution should be applied when adding variable adjustments.

▪ Adjustment Type: select Revenue, Vacancy or

Expense.

- Vacancy and expense adjustments will be

expressed as a percent.

▪ Attribute: select appropriate

- A sub-market attribute should only be selected for a significant number of properties in the

competitive set, which share a similar range of non-typical rents or vacancies (e.g., greater than

10). Otherwise, adjustments for anomalous situations should be made at the income record or

property specific level.

▪ To – From Values: enter From/To Values associated

with attribute (e.g., total GLA of building, ceiling height, number of floors, etc.).

- When applying these adjustments consider the

impact on other model variables such as expenses, vacancy, and OCR.

▪ Basic Range $/% Adj per unit: enter dollar amount or percent adjustment.

▪ Add Range $/% Adj per unit Cumulative: enter dollar amount or percent amount for ramp-up of

adjustment (e.g., on basis of building floor level).

Assessment Practices and Procedures Office 10

o On the CAP/GIM tab:

- A CAP adjustment for a variety of attributes should be made at the incomeDCA model level,

See CAP/GIM User Guide.

NOTE

Make sure to add a model-level CAP/GIM attribute to all qualities. A corresponding attribute must be added to the

IncomeDCA Valuation viewer to reflect the model-level adjustment on the income record.

- Surplus or excess land can also be valued through one or more additional land component (refer to

Highest and Best Use – Interim Use).

▪ Quality: select appropriate quality

- Range of qualities selected should be consistent with range of occupancy qualities recorded in

model.

▪ From Eff Year to Eff Year: CAUTION: use only in exceptional circumstances due to potential for double

adjustment (e.g., effective age already accounted for in quality of economic rate, CAP, and other

adjustments). ▪ CAP/GIM tab: enter CAP rate for each quality

required.

- CAP rates should be rounded to nearest 0.25%.

4. When completing the mandatory fields in the Income DCA Model viewer/Expenses tab, keep the following in mind:

o Expense: select overall expense category.

▪ No new expense items will be added to available expense categories.

▪ The total of all expenses will sum directly to the Income and Vacancy tab\General Expenses field.

o Rate: enter percentage of effective gross income.

5. When completing the mandatory fields in the Income DCA

Valuation viewer/Keypane, keep the following in mind:

Create one or more additional income records for mixed-

use properties where it is necessary to draw rates from a non-office model (e.g., retail tenancies on first floor,

apartments, parking, etc.).

Assessment Practices and Procedures Office 11

o Model Name: enter Model Name (e.g. OFF 150) if

known or query Income-DCA Model viewer to identify appropriate model based on Model Type, Area, Jur, and

Neighbourhood. o Model Type: select OFF – Office.

o Primary Model Use: select office. o Building Name: enter if applicable.

o CAP/GIM Adjustment: enter percent adjustment (plus or minus) only for building size, FSR or site coverage

differences relative to the typical property for a specific occupancy and quality (competitive set).

▪ If there are multiple income records contributing to the value of the property, a Folio CAP/GIM

adjustment may be required. Use the Property viewer/Commercial Building tab to enter the

predominant income record and an overall CAP

adjustment (only if required) in the CAP/GIM Adjustment field.

▪ Adjustments must have market support.

6. When completing the mandatory fields in the Income DCA

Valuation viewer/Valuation tab, keep the following in mind:

Do not record an occupancy for each office tenant. All tenants within the same occupancy will be summarized

into one spreadsheet entry.

o On the Occupancy spreadsheet:

▪ Tenant Description: enter Office

▪ Occupancy: select occupancy associated with appropriate model.

- Add occupancies entries (new rows) for multiple floors when:

A building is not uniform in rentable floor area for each floor

Economic rates vary significant with numbered storeys

Some floors are not built-out A floor adjustment (variable) is required to

account for impact of floor height on economic rates.

▪ Quality: select quality that will apply to all space associated with the selected office occupancy and

unit of measure.

Assessment Practices and Procedures Office 12

▪ Unit of Measure: GLA Gross Leasable Area.

▪ Num Units: GLA units expressed as square feet.

o On the Attributes/Adjustments spreadsheet:

▪ Attribute: select attribute(s) from model or apply a manual adjustment.

- Do not enter manual attribute adjustments if the adjustment is already present in the model – this

will result in a double adjustment. - Adjustments for the present value of capital cost

to cure items should be made in the Commercial Building viewer/IncomeDCA Summary tab/Non

Assessable spreadsheet (cost to cure capital, TI build-out required). Key reason for deduction in

Notes tab.

▪ Value: enter value consistent with attribute selected

from model (e.g., ceiling height, GLA size, sub-

market number, etc.) ▪ Rate Adj $/%: enter dollar/percent value only if a

manual adjustment is recorded.

- If a value is entered for a model adjustment, the

total adjustment applied will be equal to model adjustment plus the amount entered in the Value

field.

▪ Vac/Exp Adj %: enter percent only if anomalous

situation with property.

o On the Distribution spreadsheet:

▪ Property Class: select property class 6. ▪ Exempt Tax Code: select 00 – fully taxable.

▪ Exempt Percent: key “100%” (e.g., 100 percent of value associated with income record).

Assessment Practices and Procedures Office 13

APPENDIX A: FREQUENTLY ASKED QUESTIONS

General FAQs

BOMA Rentable Area FAQs

General FAQs

Question

How should reported area be treated for recording GLA units of measure in valueBC?

1. Answer

First, determine the standard for space measurement in the competitive market set. For example, in some suburban or

rural markets, most owners and property managers may report rentable area equivalent to NLA (essentially space

occupied by the tenant, exclusive of common areas).

Second, review each property linked to a model to ensure that the standard for space measurement has been applied –

this may require an adjustment to rentable area recorded for some properties. For example, if most buildings are reported

on an NLA basis but several are reported on a GLA or other basis, it will be necessary to convert the non-NLA buildings to

the NLA standard. This is a critical step since the economic rates applied to properties linked to the model will have been

determined on the basis of the space standard for the model,

in this example – NLA.

The rentable area for assessment purposes for all office properties will be recorded as GLA units of measure in

valueBC.

Question

How should buildings, which are leased on a single tenant basis, be valued and recorded in valueBC?

2. Answer

While property owners or managers of single tenant buildings

may quote rentable areas on the basis of gross building area (GBA), the property will be valued as a conventional multi-

tenanted property based on the space standard that applies

Assessment Practices and Procedures Office 14

to the applicable office model (e.g., GLA). This approach is

necessary since BC Assessment (BCA) is not valuing the landlord or tenant’s interest but the sum of all interests.

Economic rates, vacancy, expenses, etc. will be applied to the building in the same fashion as all other properties in the

model.

It will be necessary to apply an efficiency factor to the GBA reported space to determine the rentable area for assessment

purpose.

BOMA Rentable Area FAQs – Link to BOMA

Question

Is atrium space measured by the standard?

3. Answer

Atrium space above the main lobby floor does not constitute

rentable area. It is empty space and is treated, in effect, as a major vertical penetration. The base of the atrium, however

(i.e., the finished floor) is measured.

Question

How are enclosing walls defined in conjunction with major

vertical penetrations? What about the floor of the stair tower or the elevator pits of the elevator shaft?

4. Answer

The term enclosing walls refers to those walls required by

building code, and not to the architectural or decorative treatments of those walls. The floor of a stair tower and the

pits of the elevator shaft, when found inside the enclosing walls, are part of the major vertical penetration. However, if

an area is not within the enclosing walls (such as a storage room under the stair tower), the area is part of the rentable

area.

NOTE

If the elevator starts at the parking level, the floor area of the

elevator is not included.

Assessment Practices and Procedures Office 15

Question

Are areas outside the fire resistance enclosure of a major vertical penetration considered part of that penetration? For

example, plumbing chases behind restrooms?

5. Answer

No. Walls enclosing the major vertical penetration, which are required by building codes, are part of the penetration.

Additional walls outside these enclosing walls are not considered part of the penetration and are not deducted from

rentable area.

Question

Are areas of refuge (mainly a feature of Canadian buildings) deducted as major vertical penetrations?

6. Answer

If the area of refuge is not isolated from the stairwell, then it

is part of the major vertical penetration and is deducted as

such. If the area of refuge is isolated from the stairwell with its own set of doors, then it is part of floor rentable area and

is distributed to each office area through the application of the R/U ratio.

Question

Can a mechanical room serving tenants on an aboveground

floor be part of building common area?

7. Answer

Yes, if it is not already part of a floor common area.

Question

On an aboveground floor, can a corridor that is ordinarily floor common area be assessed to a particular tenant if it provides

the only access to their space? Similarly, can a portion of a ground floor lobby that is ordinarily part of building common

area be assessed to a particular tenant if it provides the only

access to their space?

8. Answer

Corridors by their nature typically provide the only access to an office or store, even when the corridor is required primarily

for fire egress. Page 16 of the standard states that:

Assessment Practices and Procedures Office 16

"where alcoves, recessed entrances or similar deviation

from the corridor line are present Usable Area shall be computed as if the deviation were not present."

You should first determine whether the suite entrance could

be positioned to incorporate the area in question without obstructing other occupants, fire egress, or other building

services, before deciding that the area belongs to the usable area of an office or store. Remember that no area can be

accounted for more than once. If an area belongs to the usable area of an office or store, it must be excluded from

floor common area, building common area, or the usable area

of any other office or store.

Question

Is storage space part of building common area in a multi-tenant building? Is storage space usable area if it is for the

express use of a given tenant?

9. Answer

Areas that are used for storage, whether above or below grade, are measured just like an office (or store in the cases

of street frontage), because these spaces could house tenants’ personnel, furniture, files or supplies. If the space is

a common storage area available for use by all tenants at no additional charge, than it would be calculated under building

common area. If it is for the express use of a given tenant, the storage space would have both a usable and rentable

measurement.

Question

Is a courtyard included in building common area if it is

enclosed by four sides but not a roof?

10. Answer

Fully enclosed refers to an enclosed space where environmental conditions are maintained by a heating,

ventilating and air conditioning system. Therefore, there must be a roof in order for the courtyard to be fully enclosed.

Question

The standard states that “building common areas are

considered to be part of floor usable area”. Can this possibly mean that the building common areas on a ground-level floor

are to be measured twice?

Assessment Practices and Procedures Office 17

11. Answer

No, the standard does not allow the same space to be measured twice.

The intent of the standard is for building common area to be

part of the floor usable area. Building common area needs to take part of the floor common area allocation on the floor(s)

on which the building common area is located. Building common area, just like store area and office area, benefits

from the circulation corridors and other floor common area. This allocation is necessary in order to fairly distribute the

floor common area to the users. If the allocation were not made, occupants on floors with building common area would

receive an unfair higher allocation of floor common area.

Question

Are the exercise club and restaurant part of building common

area if they serve the entire building?

12. Answer

No; these areas represent rent-paying tenants; so while they do provide a service to the entire building (indeed to any

paying customer); they are store area rather than building common area. However, if these areas were a building

amenity that all tenants could use as part of their lease, then they would be considered building common area instead.

Question

In an office complex, would mechanical areas located in one

building, but which serve others as well, be considered building common area? What about underground corridors

that link one building with another?

13. Answer

Although the standard does not deal specifically with building

complexes, it would be a reasonable adaptation to consider the entire project as one building and to allocate the common

corridors and building mechanical area as allowed through building common area.

Question

On a single tenant floor, are the elevator lobby and restrooms

considered usable areas?

Assessment Practices and Procedures Office 18

14. Answer

The BOMA standard defines usable area as space that tenants can actually occupy and use and may allocate to house

personnel and furniture. Thus, if an elevator lobby is under the tenant’s control and could be put to use (as a reception

area, for instance), it is usable area. However, if the tenant cannot use that space because of fire code or other

restrictions, it is not usable area. Restrooms are not considered usable area under the standard, although they are

part of rentable area.

Question

If a private stairway is built between two floors occupied by one tenant, is that stairway part of rentable area? Is it part of

the usable area?

15. Answer

Yes and yes. The standard states specifically that “vertical

penetrations built for the private use of a tenant occupying office areas on more than one floor” are counted as rentable.

The stairway would also be part of the usable area of the tenant.

Question

If a tenant expands its rentable area, does the floor R/U ratio

and building R/U ratio change as a result – meaning that each tenant’s rentable area would change?

16. Answer

Tenant expansion and new tenant activity may indeed affect

the floor R/U ratio and/or building R/U ratio. If tenant expansion or new tenant activity occurs in part or all of an

existing store area or office area, the ratios remain unchanged. However, if tenant expansion or new tenant

activity incorporates what had been floor common area or

building common area into the newly created store or office area, or creates additional floor common area or building

common area from what was previously store or office area then one or both ratios will be affected.

The floor R/U ratio will change if floor common area is

increased or decreased (e.g., by changing the configuration of floor circulation corridors or enlarging a restroom). The

building R/U ratio will change if building common area is increased or decreased (e.g., by leasing an exercise room) or

Assessment Practices and Procedures Office 19

if the floor R/U ratio is adjusted on a floor containing building

common area.

Changes to the floor R/U ratio and building R/U ratio will affect the rentable area of all the offices or stores located on

that floor or in the building. For purposes of stability, adjustments to existing leases based on changes to rentable

area are typically not made, although the new ratios are used in future lease transactions.

Question

Is parking ever counted as rentable area?

17. Answer

No, the standard excludes parking space.

Question

Are major vertical penetrations included in store area?

18. Answer

No. Major vertical penetrations are excluded when calculating

store area. Rentable area itself excludes major vertical penetrations – and, since store area is less than or equal to

floor rentable area on the floor where the store is located, store area likewise will exclude major vertical penetrations.

Question

If a store area is on a corner, is the measurement taken to

the building line on both sides? Does it matter whether entrances to the space are located on both sides?

19. Answer

Store area requires a street frontage and a ground level. It is

possible for a square building to meet these conditions on every one of its sides. In that situation and on that level, the

dominant portion would be the building line on each side.

However, the sides do not have to be at the same level. A building can have street frontage and ground level on one

side (e.g., Floor 1) and street frontage and ground level on another side (e.g., on Floor 3). Each of those two floors would

be considered store area, and the dominant portion would be the building line. Having a separate street entrance for the

space is not a requirement in determining street frontage for a store area.

Assessment Practices and Procedures Office 20

Question

How is building line defined where the ground floor building face is set back further than the upper floors from the street

frontage?

20. Answer

The standard is intended to measure space that is fully enclosed. Therefore the building line, as used in the standard

to determine store area, is the outside face of the column line (or the exterior building surface if columns are not present) of

the ground floor on the street frontage exposure. Deviations to the building line, including projections or recesses, are

ignored unless they are part of the permanent building exterior of the ground floor.

Question

Should ground floor spaces that have separate entrances and

have no access to ground floor lobbies still receive a gross-up

for those areas?

21. Answer

Yes, all tenant spaces within a building should be treated equally. Therefore, tenant spaces with separate entrances

and no access to ground floor lobbies are treated in the same manner as tenants who do have access to the ground floor

lobby.

Question

Regarding dominant portion … where a wall meets a column a bite appears to be taken out of the column as the

measurement line shifts. If the column is not square, how are the dimensions of the bite determined?

22. Answer

Columns are not considered in the standard. Therefore, where

a column interrupts the dominant portion, the dominant

portion that exists on each side of the column continues through one-half of the horizontal distance of the column.

Where a column interrupts a dominant portion that is the same on both sides, the dominant portion continues through

the column as if the column did not exist. Where a column interrupts a dominant portion that is different on each side,

the dominant portion on one side continues for one-half the horizontal distance and then either steps in or out to meet the

dominant portion from the other side.

Assessment Practices and Procedures Office 21

Question

Is the measurement taken to the centre line of partitions between adjoining tenant spaces and to the centre line of

partitions between tenant spaces and building common areas?

23. Answer

Yes, the measurement is taken to the centre line of partitions

between adjoining office area(s) or store area(s), building common area(s) and the building common area being

measured. Building common area is measured just like office or store area in determining usable area.

Question

Are mezzanines measured by the standard?

24. Answer

All floor space in a building is measured, including

mezzanines. The purpose of the standard is to measure the

actual square feet contained in the building. The usefulness of a particular space is not addressed by the standard, and is

better left for lease negotiations between landlord and tenant. Varying lease rates are common in the market using such

criteria as location on the floor, proximity to the elevator lobby, windows, views, heights in the building, and the

usefulness of a particular space.

Question

Does the standard measure space in belowground floors?

25. Answer

Yes, except for those areas specifically excluded by the standard, such as parking areas.

Question

Is gross building area an appropriate way to measure a single

occupant building?

26. Answer

The standard is a systematic method for measuring office

buildings, and should be used in its entirety for each building. Its purpose is to provide a common and agreed-upon basis

for comparing lease rates, building efficiencies, operating costs and other relevant data. For example, gross building

area is used within the industry primarily to determine

Assessment Practices and Procedures Office 22

construction costs or building value. Usable area is often used

to determine cleaning costs and space efficiencies.

Single occupant buildings will often need to be compared to multi-occupant buildings and, in these cases, building

rentable area is the recommended measurement to use. Gross building area would be an appropriate method in

determining lease rate only if the parties agree. Each part of the standard has its own use and needs to be applied

regardless of the number of occupants.

Question

Does the standard provide for the measurement of warehouse or industrial space? Does it cover a shopping centre or strip

mall?

27. Answer

No, the standard is intended to apply specifically to the

measurement of office buildings. A method for measuring store area in office buildings is contained in the standard. No

provision is currently made for measuring any other types of buildings.

Question

Does BOMA certify space measurement firms or instruments?

28. Answer

Neither BOMA nor the American National Standards Institute

(ANSI) certifies, approves, or endorses any space measurement firm or measurement device.

Question

Is it appropriate to treat Corporation Capital Tax (CCT) as an

expense when calculating the net operating income to the real estate?

29. Answer

The CCT is a tax on the corporation, not on the real estate owned by the corporation. CCT varies widely depending on

the corporation, its investments and its financing structure. Because the CCT is unique to the corporation, it would not be

appropriate to treat it as an expense in calculating the net operating income to the real estate.

Assessment Practices and Procedures Office 23

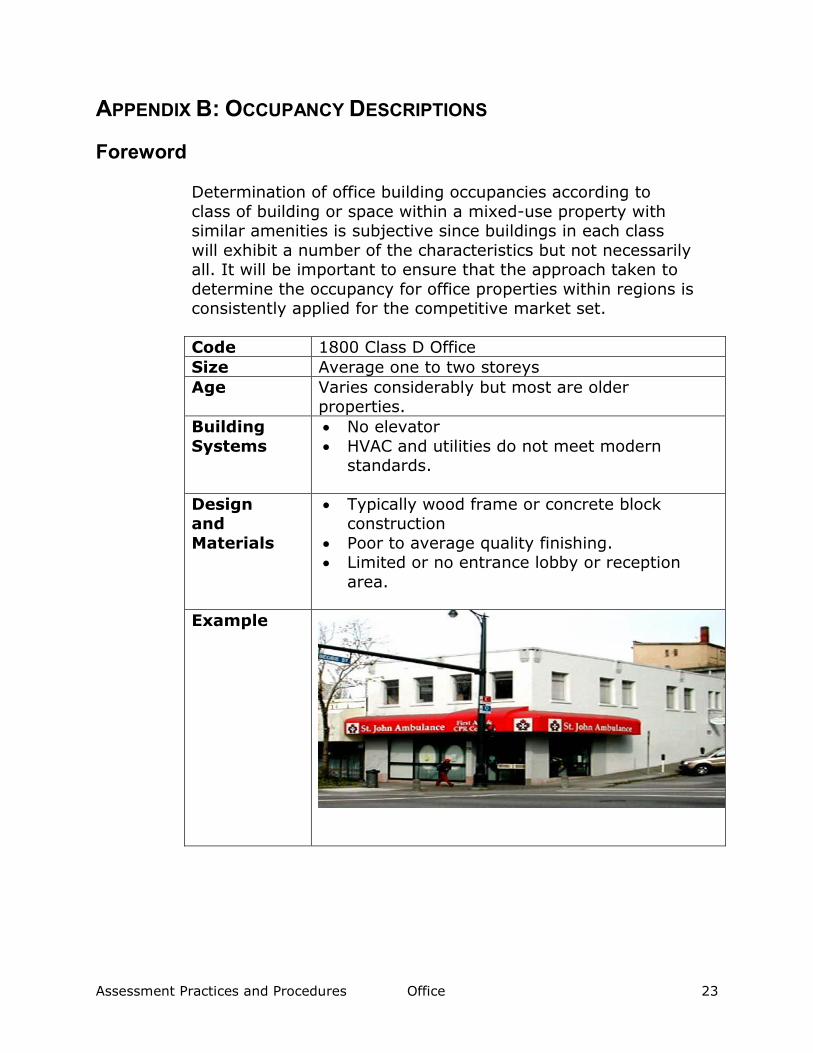

APPENDIX B: OCCUPANCY DESCRIPTIONS

Foreword

Determination of office building occupancies according to

class of building or space within a mixed-use property with similar amenities is subjective since buildings in each class

will exhibit a number of the characteristics but not necessarily all. It will be important to ensure that the approach taken to

determine the occupancy for office properties within regions is consistently applied for the competitive market set.

Code 1800 Class D Office

Size Average one to two storeys

Age Varies considerably but most are older properties.

Building

Systems

No elevator

HVAC and utilities do not meet modern standards.

Design and

Materials

Typically wood frame or concrete block construction

Poor to average quality finishing. Limited or no entrance lobby or reception

area.

Example

Assessment Practices and Procedures Office 24

Assessment Practices and Procedures Office 25

Code 1801 Class C Office

Size Varies from 1 to 10 storeys. Rentable area of most buildings varies from 10,000 square feet

to 100,000 square feet.

Age Varies, but typically older buildings in urban centres

Building Systems

Elevator access, HVAC

Design

and Materials

Good quality design, common foyer area,

tenant improvements are functional and are not often upgraded in older buildings

Example

Assessment Practices and Procedures Office 26

Code 1802 Class B Office

Size Average 15 floors, 110,000 square feet

Age Average age 1965

Building

Systems

Mechanical, HVAC and utilities meet current

tenant requirements

Design

and Materials

High quality design; more use of brick and

concrete and less glass Tenant improvements are mid to high

quality and are updated regularly.

Assessment Practices and Procedures Office 27

Example

Code 1803 Class A Office

Size Average 25 floors, 275,000 square feet

Age Average age 1981

Building

Systems

Mechanical, HVAC and utilities meet current

and anticipated future tenant requirements

Assessment Practices and Procedures Office 28

(e.g. telecomm infrastructure)

Design and

Materials

High quality design and materials; extensive use of glass

Tenant improvements are high quality and updated regularly.

Older buildings remain competitive with newer product

Example

Assessment Practices and Procedures Office 29