Embed Size (px)

Citation preview

SBA Opportunities for Credit Unions

SBA Opportunities for Credit Unions

Kathryn Baxter, Moderator Vanessa Lowe, Host

Guest Speakers: • Scott Bossom, SBA • J. Christopher Webb, SBA • Rippy Madan, NCUA

Office of Small Credit Union Initiatives

February 15, 2017

SBA Opportunities for Credit Unions 2

Adjust computer volume as needed. Drag bottom right corner to resize slide view. Allow pop-ups. Click “Ask a Question” on the left corner of the console

window. Please complete post-webinar survey. In three weeks, a closed captioned archive will be at:

https://www.ncua.gov/services/Pages/small-credit-union-learning-center/services/videos-webinars.aspx

Administrative Announcements

SBA Opportunities for Credit Unions 3

NCUA Disclaimer

This webinar is offered for informational

and educational purposes only. NCUA does not endorse any particular credit union or vendor, or their employees,

products, or services.

3

SBA Opportunities for Credit Unions 4

What You’ll Hear Today

SBAOne – SBA’s Lender Platform

SBA’s Microloan Program

NCUA MBL Rule, Effective January 1, 2017

Q&A – Send questions at any time

SBA Opportunities for Credit Unions 5

Vanessa Lowe

Voices on the Webinar

Economic Development Specialist NCUA Office of Small Credit Union Initiatives

SBA Opportunities for Credit Unions 6

Lender Relations Specialist

Voices on the Webinar

Scott Bossom

SBA Opportunities for Credit Unions 7

Microloan Division SBA Office of Economic Opportunity

Voices on the Webinar

J. Christopher Webb

SBA Opportunities for Credit Unions 8

NCUA Region II Lending Specialist

Voices on the Webinar

Rippy Madan

SBA Opportunities for Credit Unions 9

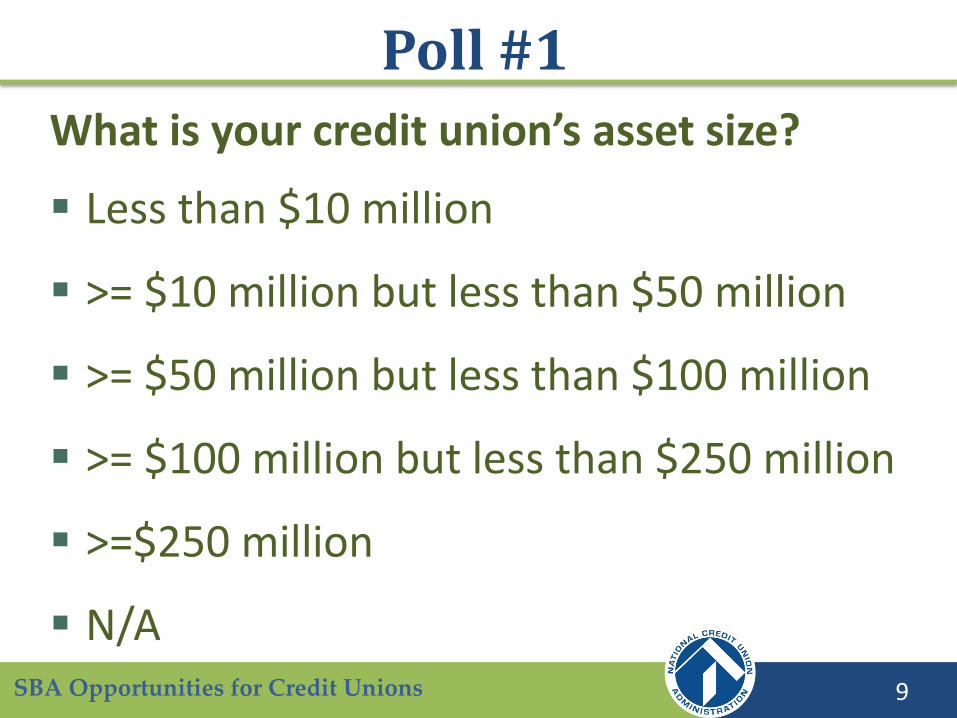

What is your credit union’s asset size?

Less than $10 million

>= $10 million but less than $50 million

>= $50 million but less than $100 million

>= $100 million but less than $250 million

>=$250 million

N/A

Poll #1

SBA Opportunities for Credit Unions 10

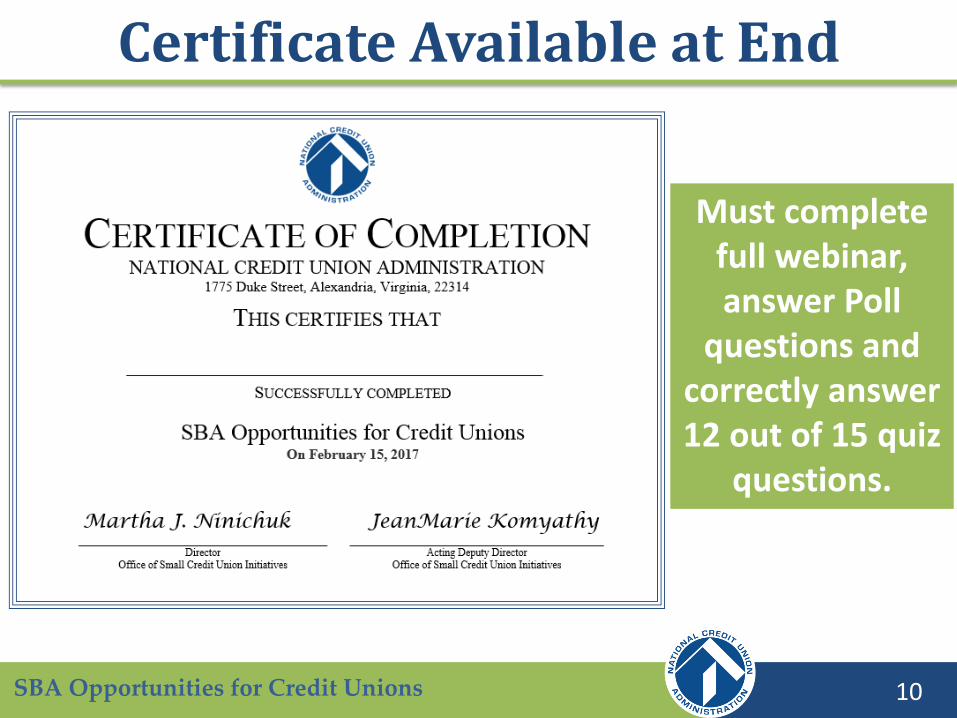

Certificate Available at End

Must complete full webinar, answer Poll

questions and correctly answer 12 out of 15 quiz

questions.

SBA Opportunities for Credit Unions 11

Portland District Office U.S. Small Business Administration

SBA 7(a) Lending Program Overview

SBA Opportunities for Credit Unions 12

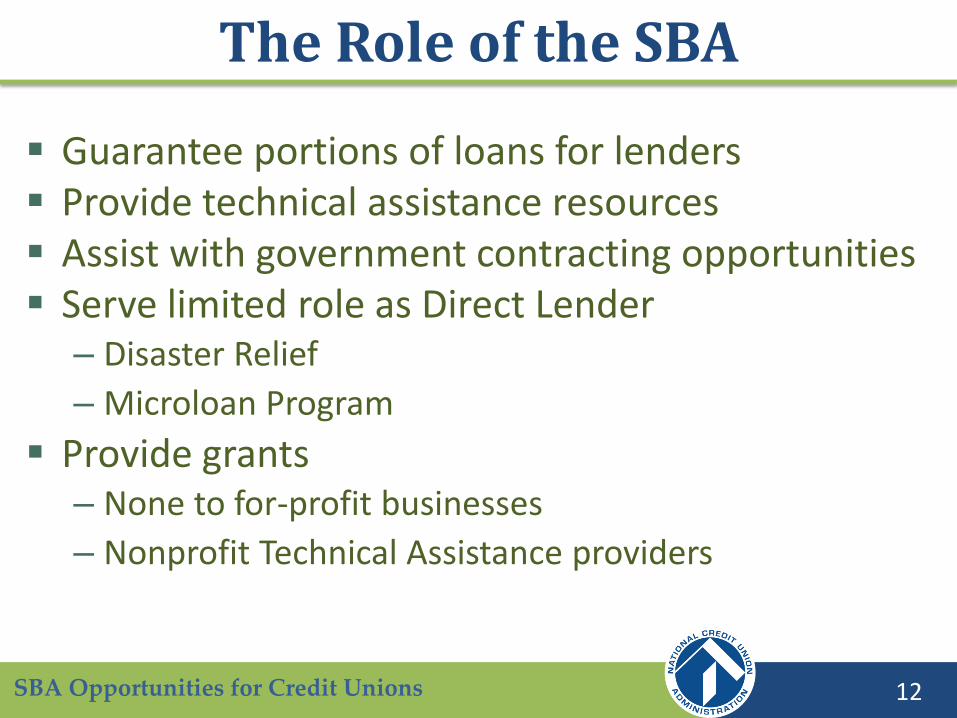

The Role of the SBA

Guarantee portions of loans for lenders Provide technical assistance resources Assist with government contracting opportunities Serve limited role as Direct Lender

– Disaster Relief

– Microloan Program

Provide grants – None to for-profit businesses

– Nonprofit Technical Assistance providers

SBA Opportunities for Credit Unions

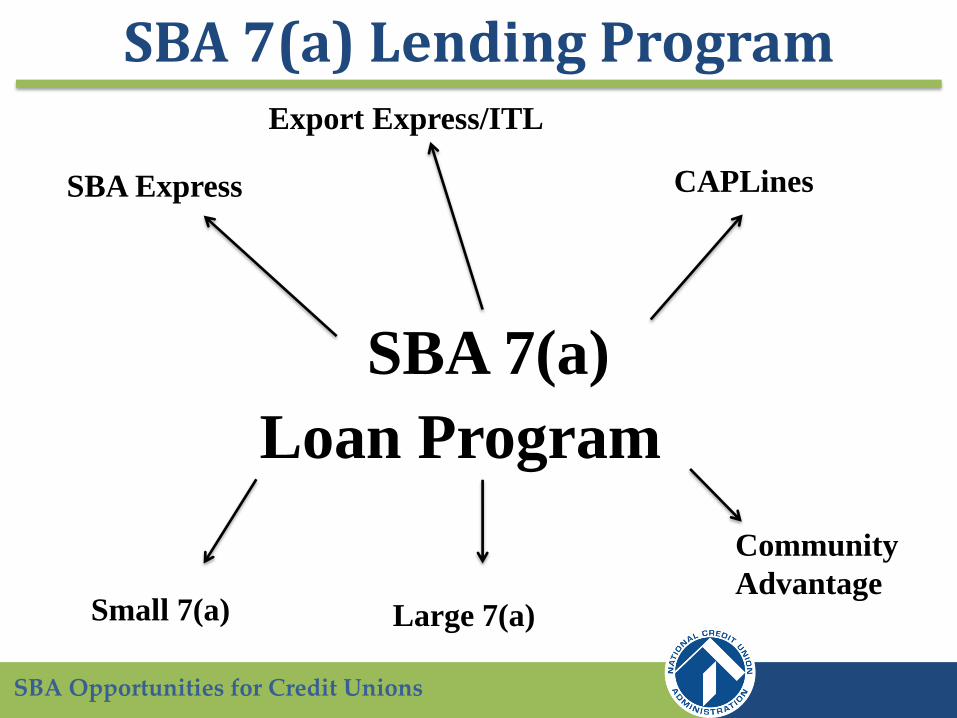

SBA 7(a)

Loan Program

SBA Express CAPLines

Small 7(a)

Community

Advantage

Export Express/ITL

Large 7(a)

SBA 7(a) Lending Program

SBA Opportunities for Credit Unions 14

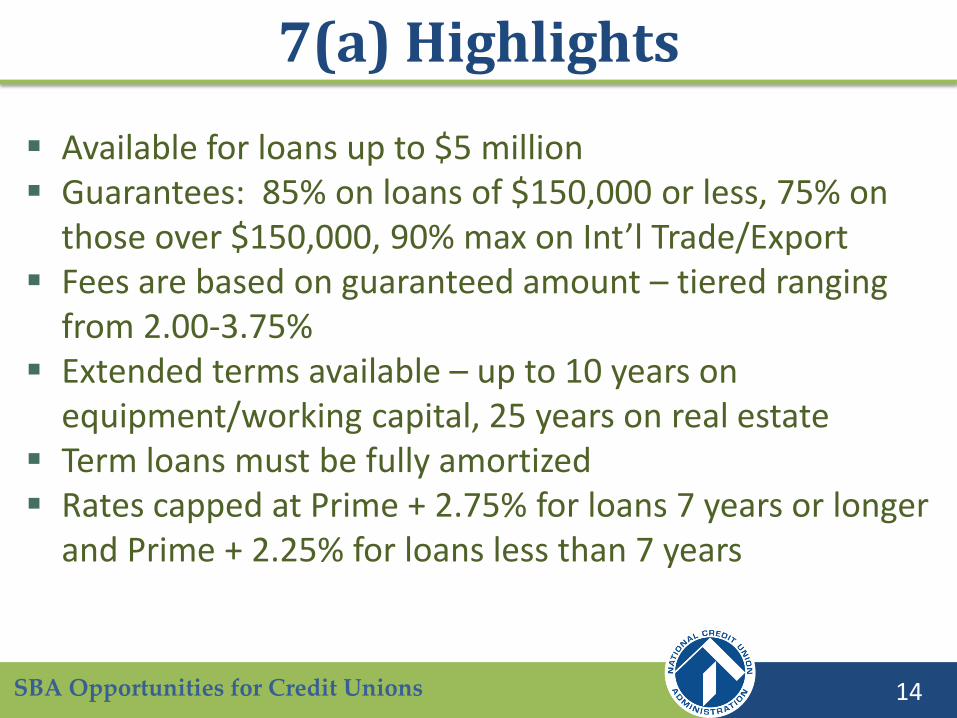

7(a) Highlights

Available for loans up to $5 million Guarantees: 85% on loans of $150,000 or less, 75% on

those over $150,000, 90% max on Int’l Trade/Export Fees are based on guaranteed amount – tiered ranging

from 2.00-3.75% Extended terms available – up to 10 years on

equipment/working capital, 25 years on real estate Term loans must be fully amortized Rates capped at Prime + 2.75% for loans 7 years or longer

and Prime + 2.25% for loans less than 7 years

SBA Opportunities for Credit Unions 15

Underwriting an SBA 7(a) Loan

It’s really no different than what you currently do.

SBA instructs lenders to analyze a credit the same way it would a non-SBA deal.

Our guaranty allows a lender to mitigate aspects of the deal that fall in the fringes of your credit policy (i.e., collateral shortfalls).

SBA Opportunities for Credit Unions 16

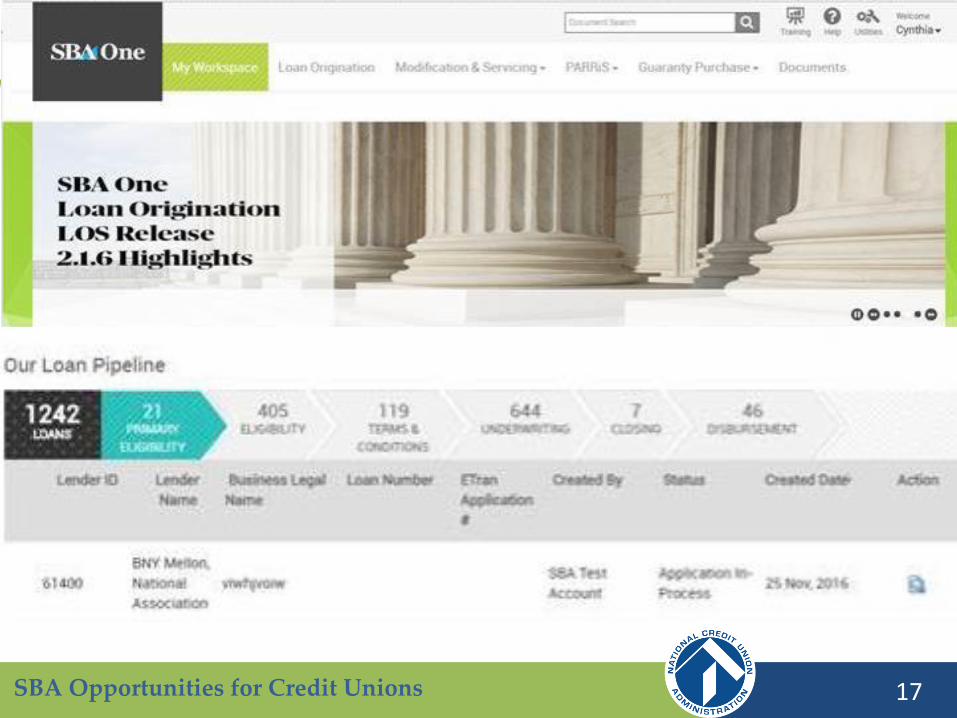

SBAOne Lender Platform

In use since February 2016 Will ultimately be a “Cradle to Grave” system…

– Processing Servicing Purchasing system

Currently only processing is available Non-Delegated lenders are mandated to use SBAOne Delegated still process PLP/Express loans through Etran Creates significant efficiencies overall and is much more

user friendly On-Demand Training Portal housed within the SBAOne

system

SBA Opportunities for Credit Unions 17

SBAOne Lender Platform

SBA Opportunities for Credit Unions 18

SBAOne Lender Platform

SBA Opportunities for Credit Unions 19

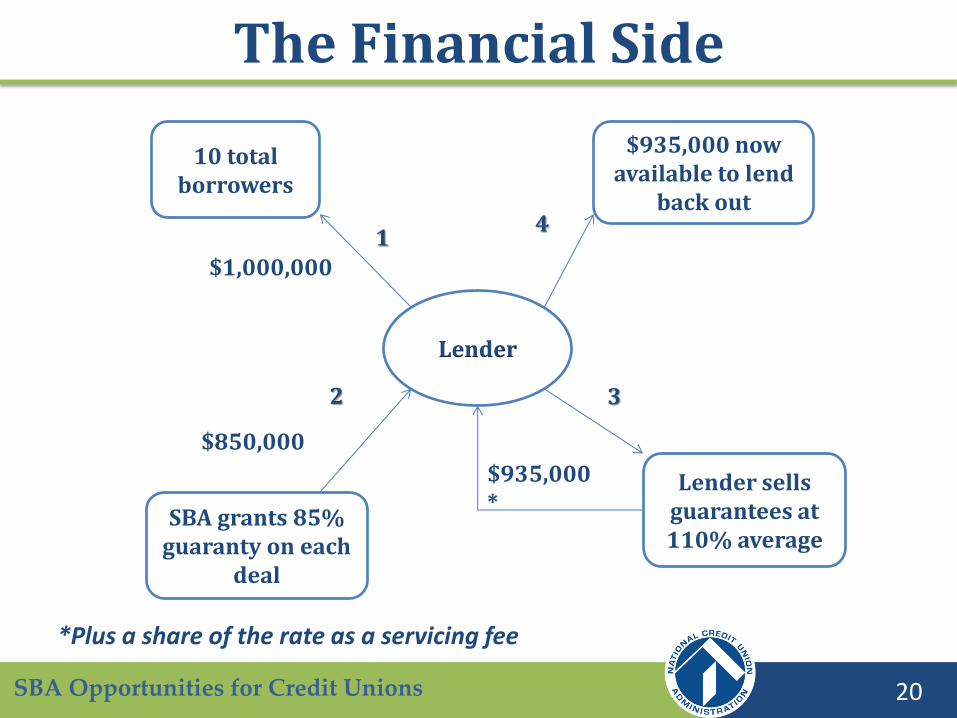

The Financial Side

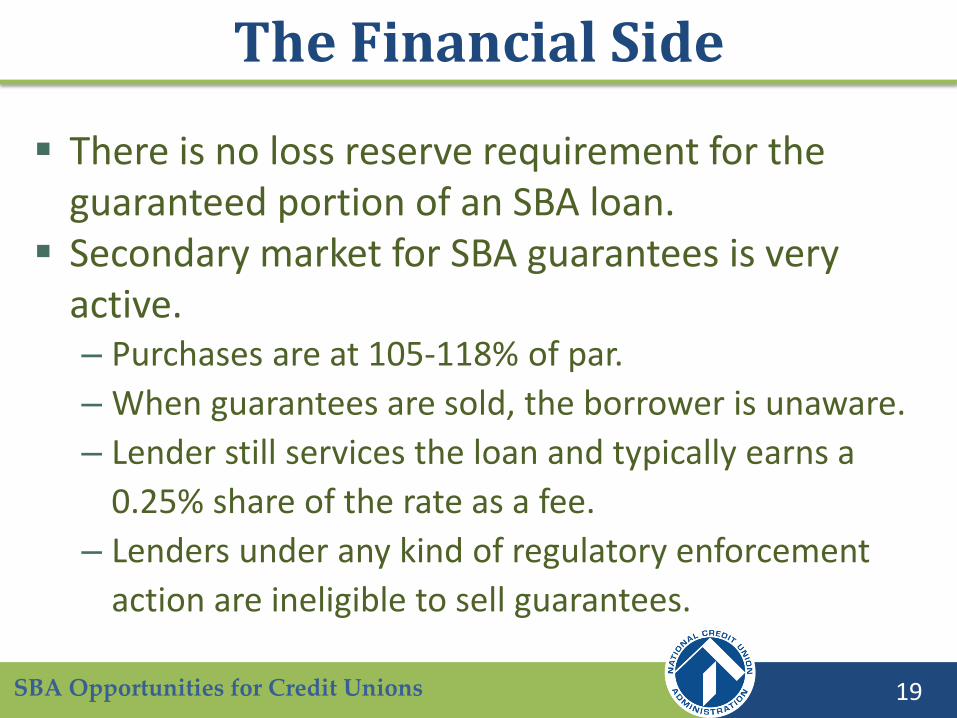

There is no loss reserve requirement for the guaranteed portion of an SBA loan.

Secondary market for SBA guarantees is very active. – Purchases are at 105-118% of par.

– When guarantees are sold, the borrower is unaware.

– Lender still services the loan and typically earns a

0.25% share of the rate as a fee.

– Lenders under any kind of regulatory enforcement

action are ineligible to sell guarantees.

SBA Opportunities for Credit Unions 20

The Financial Side

Lender

Lender sells guarantees at 110% average

$935,000*

10 total borrowers

$1,000,000

SBA grants 85% guaranty on each

deal

$850,000

$935,000 now available to lend

back out

1

2 3

4

*Plus a share of the rate as a servicing fee

SBA Opportunities for Credit Unions 21

Poll #2

Does your credit union offer business loans?

No

Yes, and we have had SBA guarantees

Yes, but we haven’t had SBA guarantees

Unsure

N/A (for participants not affiliated with a credit union)

SBA Opportunities for Credit Unions

U. S. Small Business Administration www.SBA.gov

Office of Economic Opportunity Microloan Program

SBA Opportunities for Credit Unions 23

Office of Economic Opportunity Programs

Microloan Program – How it works

Highlights / Statistics – FY2010 - FY2016

Microloan Program – Application Process

Resources / Contacts

What I’ll Cover

SBA Opportunities for Credit Unions 24

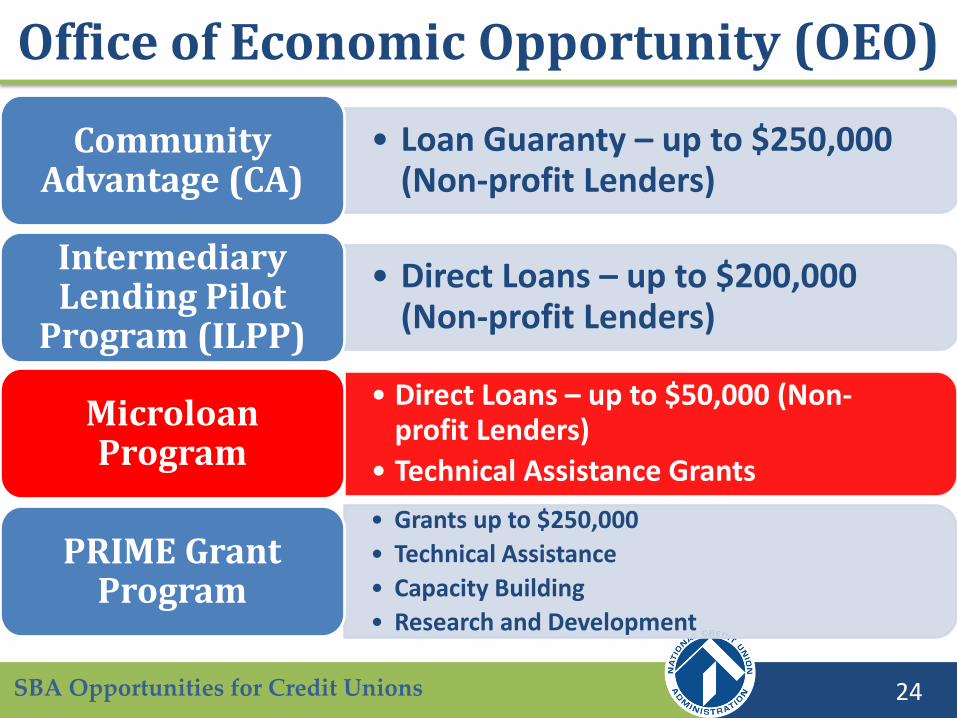

• Loan Guaranty – up to $250,000 (Non-profit Lenders)

Community Advantage (CA)

• Direct Loans – up to $200,000 (Non-profit Lenders)

Intermediary Lending Pilot

Program (ILPP)

• Direct Loans – up to $50,000 (Non-profit Lenders)

• Technical Assistance Grants

Microloan Program

• Grants up to $250,000

• Technical Assistance

• Capacity Building

• Research and Development

PRIME Grant Program

Office of Economic Opportunity (OEO)

SBA Opportunities for Credit Unions 25

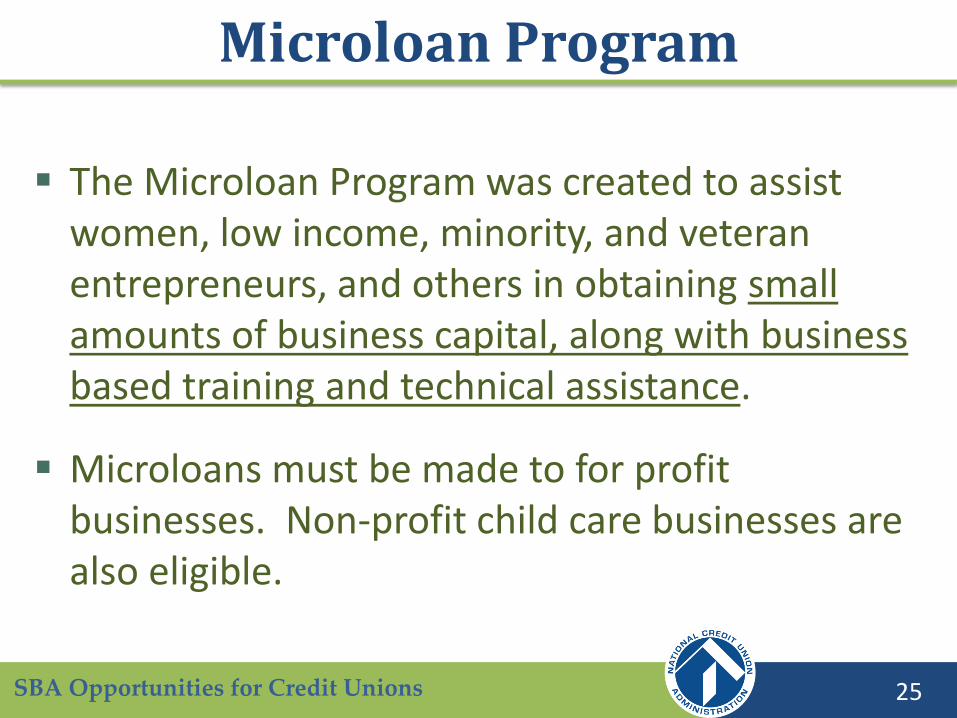

The Microloan Program was created to assist women, low income, minority, and veteran entrepreneurs, and others in obtaining small amounts of business capital, along with business based training and technical assistance.

Microloans must be made to for profit businesses. Non-profit child care businesses are also eligible.

Microloan Program

SBA Opportunities for Credit Unions 26

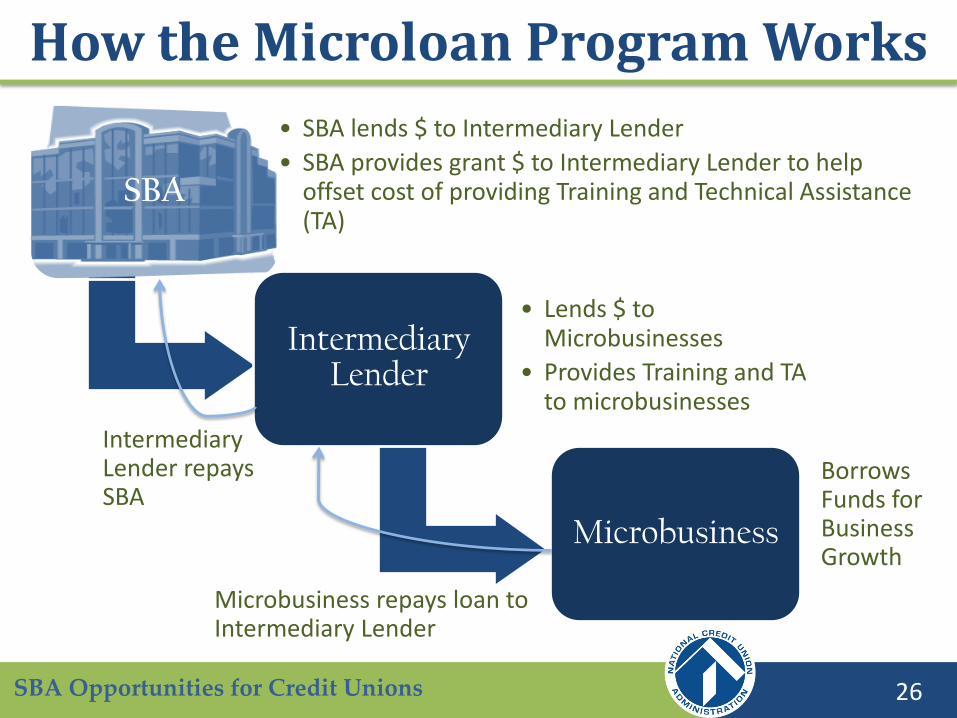

SBA

• SBA lends $ to Intermediary Lender

• SBA provides grant $ to Intermediary Lender to help offset cost of providing Training and Technical Assistance (TA)

Intermediary Lender

• Lends $ to Microbusinesses

• Provides Training and TA to microbusinesses

Microbusiness

How the Microloan Program Works

Borrows Funds for Business Growth

Intermediary Lender repays SBA

Microbusiness repays loan to Intermediary Lender

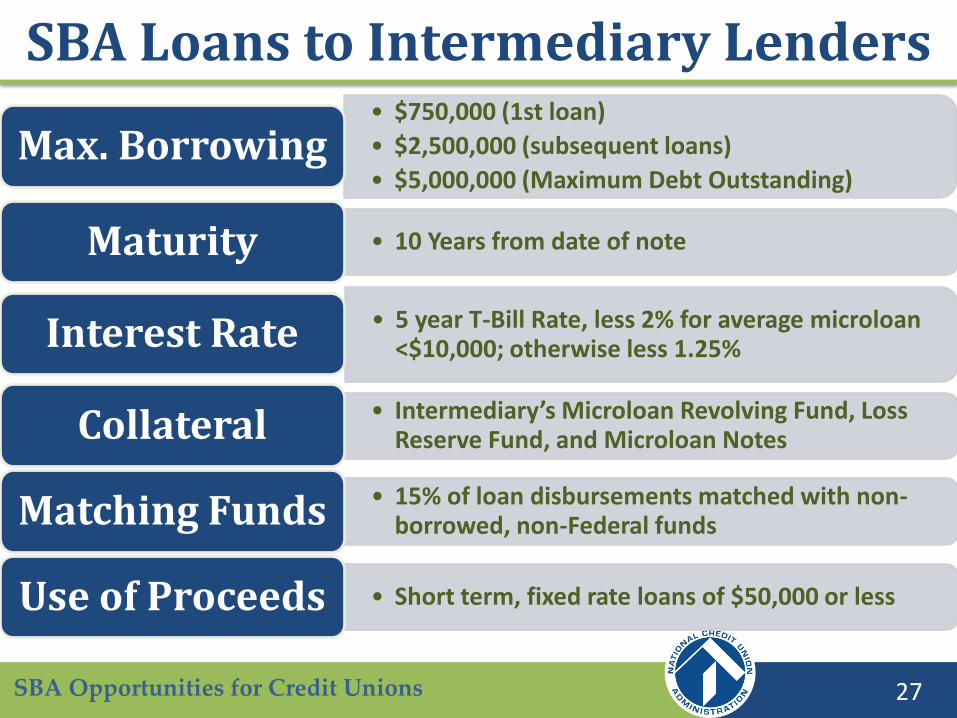

SBA Opportunities for Credit Unions 27

• $750,000 (1st loan)

• $2,500,000 (subsequent loans)

• $5,000,000 (Maximum Debt Outstanding) Max. Borrowing

• 10 Years from date of note Maturity

• 5 year T-Bill Rate, less 2% for average microloan <$10,000; otherwise less 1.25% Interest Rate

• Intermediary’s Microloan Revolving Fund, Loss Reserve Fund, and Microloan Notes Collateral

• 15% of loan disbursements matched with non-borrowed, non-Federal funds Matching Funds

• Short term, fixed rate loans of $50,000 or less Use of Proceeds

SBA Loans to Intermediary Lenders

SBA Opportunities for Credit Unions 28

Loans from Intermediary to Microbusiness

• Up to $50,000 Loan Amount

• Up to 6 years (72 months) Maturity

• Fixed rate, up to: Cost of Funds + 8.50% (if <=$10,000)

• Cost of Funds + 7.75% (if loan >$10,000) Interest Rate

• Loans for supplies, furniture, fixtures, materials, equipment, or working capital

Use of Proceeds

• Required at Intermediary’s discretion – flexibility in structuring loan

Collateral

• Decisions made by Intermediary, not SBA

• Intermediary’s policies and procedures Underwriting/Servicing

SBA Opportunities for Credit Unions 29

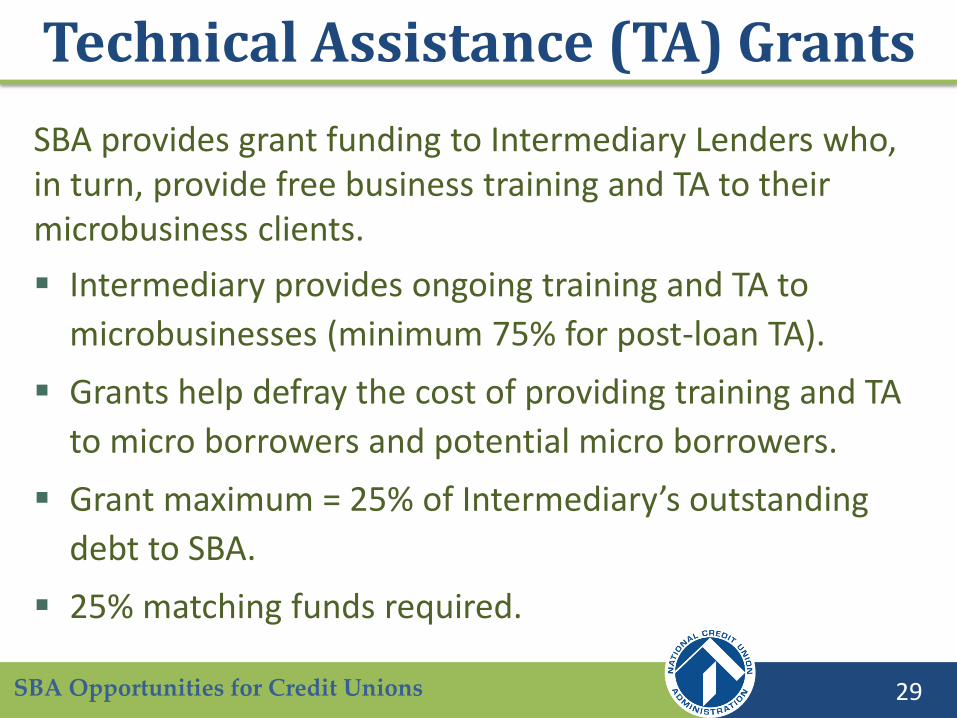

Technical Assistance (TA) Grants

SBA provides grant funding to Intermediary Lenders who, in turn, provide free business training and TA to their microbusiness clients.

Intermediary provides ongoing training and TA to

microbusinesses (minimum 75% for post-loan TA).

Grants help defray the cost of providing training and TA

to micro borrowers and potential micro borrowers.

Grant maximum = 25% of Intermediary’s outstanding

debt to SBA.

25% matching funds required.

SBA Opportunities for Credit Unions 30

Microloan Program Highlights

• 150 (approximately) Active Intermediary

Lenders

(Current)

• $537,294,000 (as of 12/31/16) SBA Loans Disbursed to

Micro-Lenders (Historical)

• 64,857 Loans Closed

• $797 Million Funded to Micro Businesses

• $12,290 (Average Microloan Size)

Microloans Closed (Historical)

• Created – 94,593

• Retained – 138,841

Jobs Created/Retained

(Historical)

SBA Opportunities for Credit Unions 31

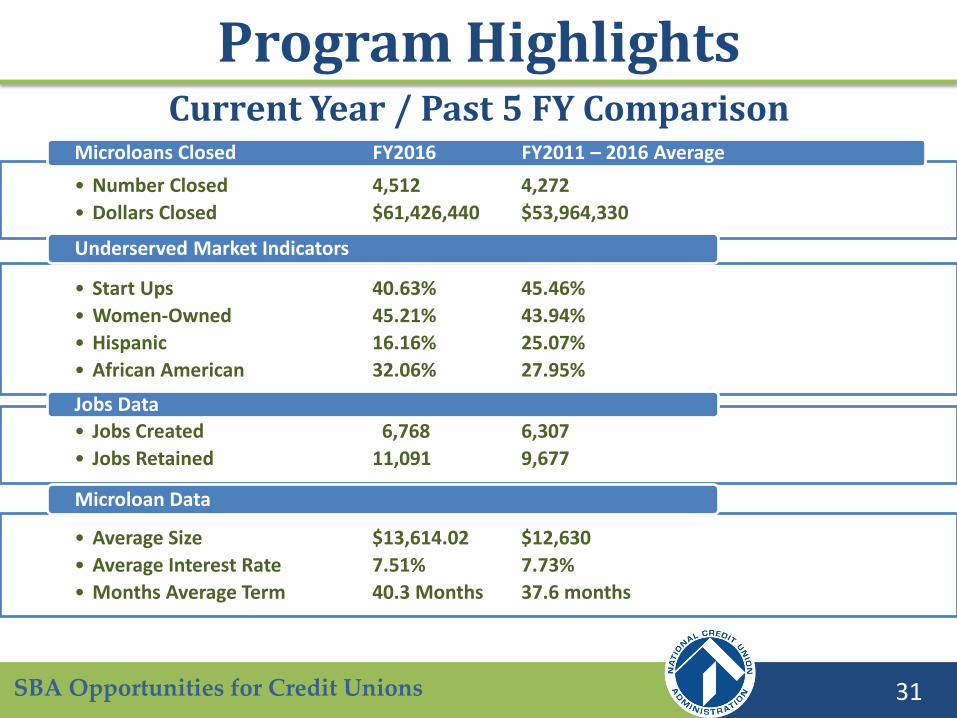

Program Highlights

• Number Closed 4,512 4,272

• Dollars Closed $61,426,440 $53,964,330

Microloans Closed FY2016 FY2011 – 2016 Average

• Start Ups 40.63% 45.46%

• Women-Owned 45.21% 43.94%

• Hispanic 16.16% 25.07%

• African American 32.06% 27.95%

Underserved Market Indicators

• Jobs Created 6,768 6,307

• Jobs Retained 11,091 9,677

Jobs Data

• Average Size $13,614.02 $12,630

• Average Interest Rate 7.51% 7.73%

• Months Average Term 40.3 Months 37.6 months

Microloan Data

Current Year / Past 5 FY Comparison

SBA Opportunities for Credit Unions 32

Microloan Program Application Eligibility

– Non-Profit

– At least 1 Year Direct Lending and Loan Servicing

Experience

– At least 1 Year In-house Technical Assistance Experience

Qualifications

– Personnel – Relevant Micro-lending Experience

– Lending – Experience

– Training / TA Experience

– Financial Strength / Stability

SBA Opportunities for Credit Unions 33

Application Components 1. Cover sheet.xls

2. SBA 1081.pdf

3. Lending History Chart.xls

4. Cost of Lending Calculation.xls

5. Item 10 Chart.xls

6. Cert. of Contracts sba1711.pdf

7. Disclosure of Lobbying Activities sflllin.pdf

8. Debarment sba1623.pdf

9. Resolution of the Board of Directors sba160.pdf

10. Security Agreement SBA1059.pdf

11. 1Microloan SOP 52 00 (FINAL).pdf

Microloan Program Application

SBA Opportunities for Credit Unions 34

Microloan Program Application

Where do I get the application zip file? From the Local SBA District Office

https://www.sba.gov/tools/local-assistance/districtoffices

Where do I deliver the completed application? To the Local SBA District Office

What happens next? District Office reviews for completeness / delivers to HQ HQ reviews for eligibility and qualification / makes

decision

SBA Opportunities for Credit Unions 35

Application Rules

Read the Microloan Program SOP. Clearly describe current lending and TA

programs. Follow the directions / Cover Sheet carefully. Only deliver a complete application. Use the Lending History and TA History

templates.

SBA Opportunities for Credit Unions 36

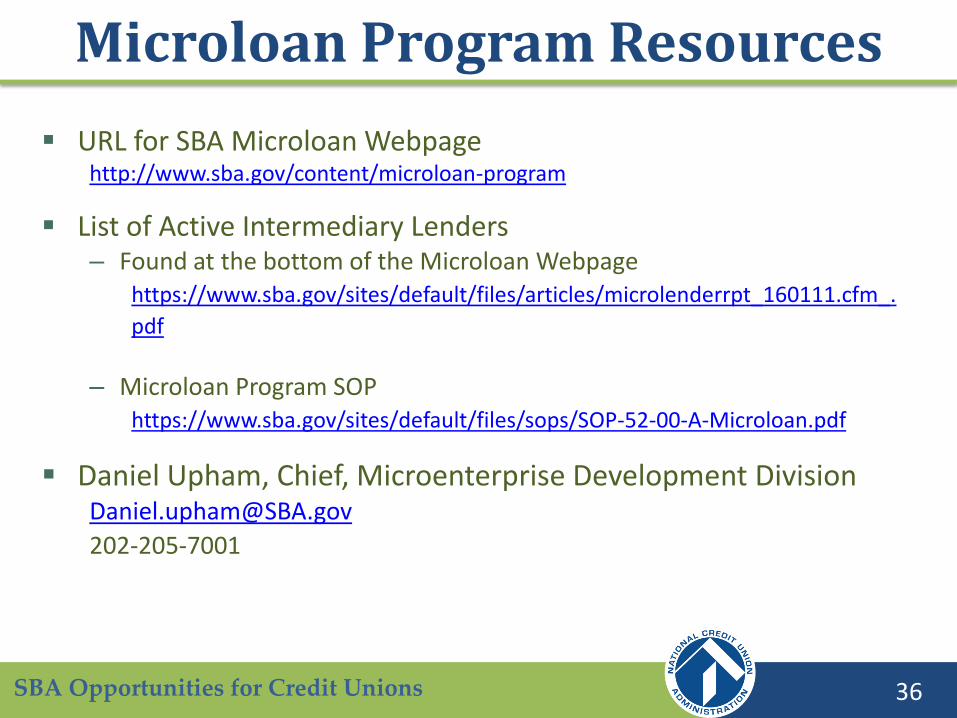

Microloan Program Resources

URL for SBA Microloan Webpage http://www.sba.gov/content/microloan-program

List of Active Intermediary Lenders

– Found at the bottom of the Microloan Webpage https://www.sba.gov/sites/default/files/articles/microlenderrpt_160111.cfm_.

– Microloan Program SOP https://www.sba.gov/sites/default/files/sops/SOP-52-00-A-Microloan.pdf

Daniel Upham, Chief, Microenterprise Development Division

202-205-7001

SBA Opportunities for Credit Unions 37

Questions and Point of Contact

James (Chris) Webb Deputy Chief

[email protected] Phone 202-619-0628

SBA Opportunities for Credit Unions 38

Poll #3

How does your credit union support microenterprises? (check all that apply)

We offer entrepreneurship training.

We refer members to a training partner.

We make loans via the SBA microloan program.

We make loans via another partner.

None of the above.

SBA Opportunities for Credit Unions

Final Rule: Part 723 Member Business Loans

Prescriptive vs. Principles-Based Rule Changes

SBA Opportunities for Credit Unions

Goals of Modernizing Part 723

40

1. Replace overly prescriptive requirements with principles-based standards.

2. Clarify and expand risk management requirements needed to safely conduct commercial lending activities.

3. Improve the expertise and policy provisions of the regulation.

SBA Opportunities for Credit Unions

Goals of Modernizing Part 723

41

4. Change supervisory focus to sound commercial risk management practices from compliance with prescriptive regulatory requirements.

5. Eliminate NCUA involvement in day-to-day operations of CUs by eliminating need for waivers.

6. Distinguish between commercial loans and the statutory definition of MBLs.

7. Incorporate statutory limit for aggregate MBLs pursuant to Section 107A of the FCU Act.

SBA Opportunities for Credit Unions

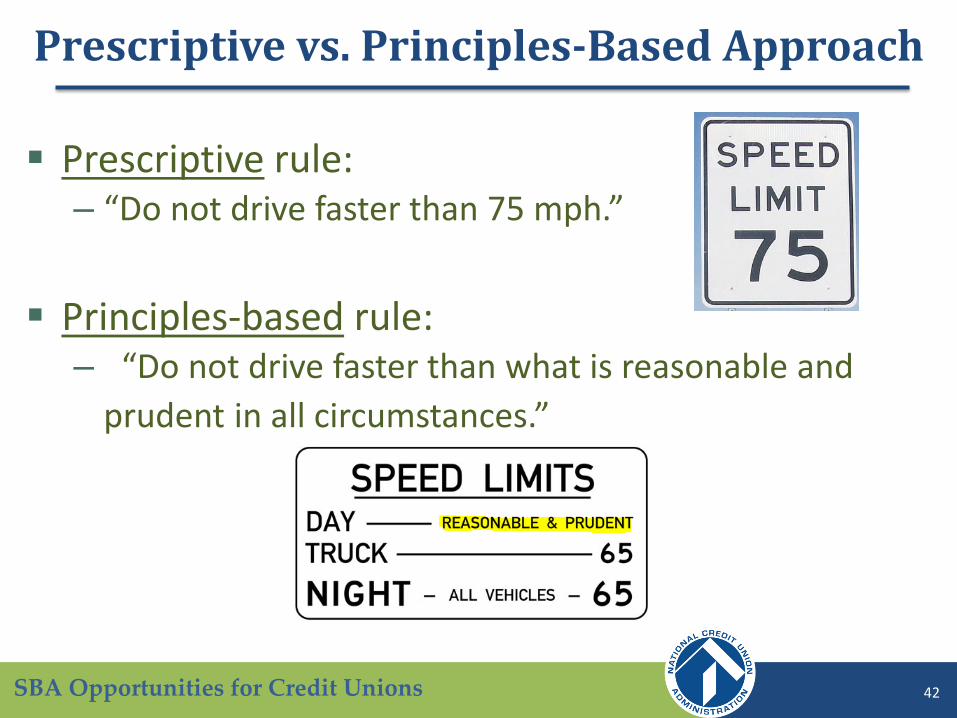

Prescriptive vs. Principles-Based Approach

42

Prescriptive rule: – “Do not drive faster than 75 mph.”

Principles-based rule:

– “Do not drive faster than what is reasonable and

prudent in all circumstances.”

SBA Opportunities for Credit Unions

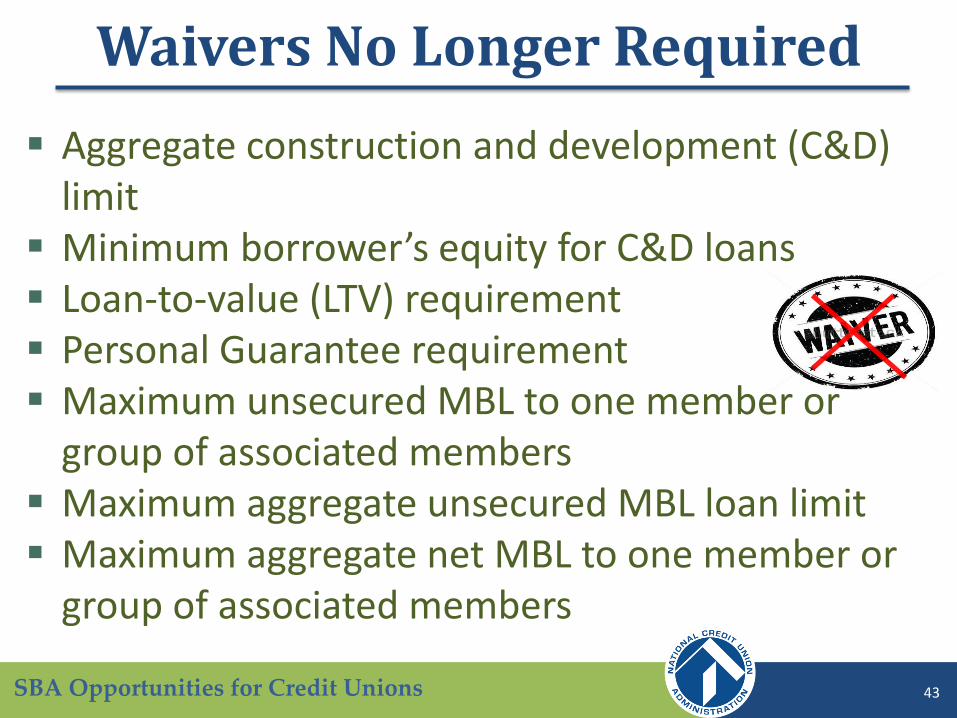

Waivers No Longer Required

43

Aggregate construction and development (C&D) limit

Minimum borrower’s equity for C&D loans Loan-to-value (LTV) requirement Personal Guarantee requirement Maximum unsecured MBL to one member or

group of associated members Maximum aggregate unsecured MBL loan limit Maximum aggregate net MBL to one member or

group of associated members

SBA Opportunities for Credit Unions

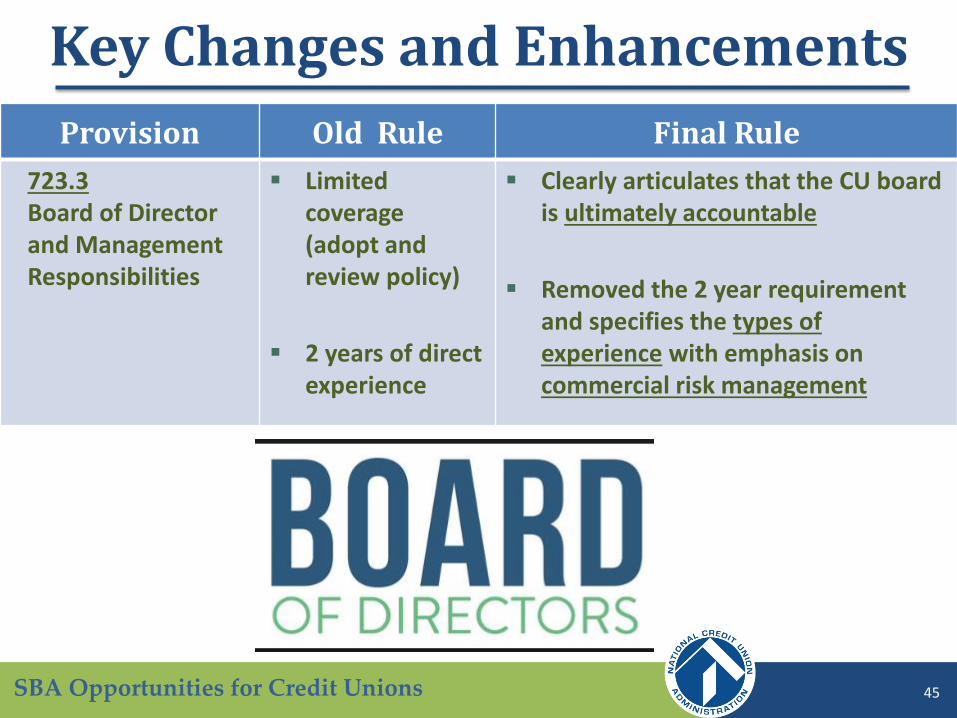

Key Changes and Enhancements

44

Provision Old Rule Final Rule

723.1(b)(1) Exemption from the Board / Management Responsibilities (723.3) and Loan Policy Requirements (723.4)

N/A Smaller credit unions (Total Assets <$250 million) with limited commercial loan exposures and that infrequently originate and sell commercial loan participations are exempt from the commercial loan policy and board/management requirements.

SBA Opportunities for Credit Unions 45

Provision Old Rule Final Rule

723.3 Board of Director and Management Responsibilities

Limited coverage (adopt and review policy)

2 years of direct experience

Clearly articulates that the CU board is ultimately accountable

Removed the 2 year requirement and specifies the types of experience with emphasis on commercial risk management

Key Changes and Enhancements

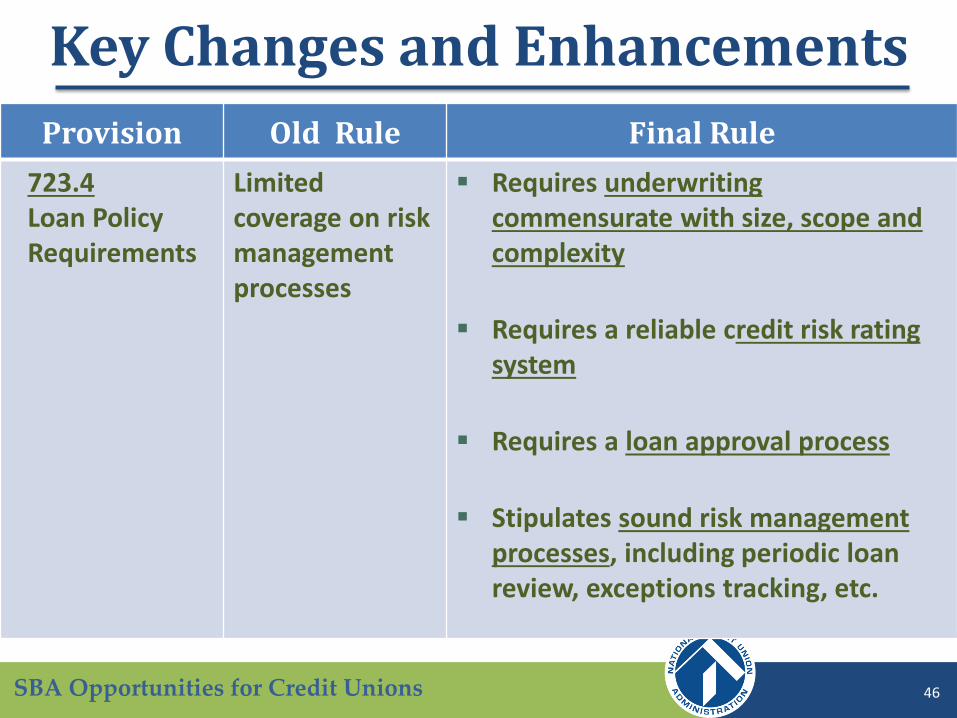

SBA Opportunities for Credit Unions 46

Provision Old Rule Final Rule

723.4 Loan Policy Requirements

Limited coverage on risk management processes

Requires underwriting commensurate with size, scope and complexity

Requires a reliable credit risk rating system

Requires a loan approval process

Stipulates sound risk management processes, including periodic loan review, exceptions tracking, etc.

Key Changes and Enhancements

SBA Opportunities for Credit Unions 47

Provision Old Rule Final Rule

723.4(c) Loans to a Single Borrower or a Group of Associated Borrowers

The greater of $100,000 or 15% of net worth

Maintains the 15% limit with added flexibility to go up to 25% if the amount above the 15% is secured by “readily marketable collateral”

Modifies the definition of “associated borrower” to narrow its scope (parallel change made to Loan Participation rule)

Key Changes and Enhancements

SBA Opportunities for Credit Unions 48

Provision Old Rule Final Rule

723.4(c) Unsecured MBLs

Lesser of $100,000 or 2.5% of CU Net Worth to one member (Well Capitalized CUs only)

10% of CU Net Worth

Removed the limits

Requires credit unions to set internal policy limits

Key Changes and Enhancements

SBA Opportunities for Credit Unions 49

Provision Old Rule Final Rule

723.5(a) LTV

80% Removed the 80% limit

Requires sufficient collateral commensurate with the level of risk

Excludes junior debt from other lenders in calculating the LTV ratio

Key Changes and Enhancements

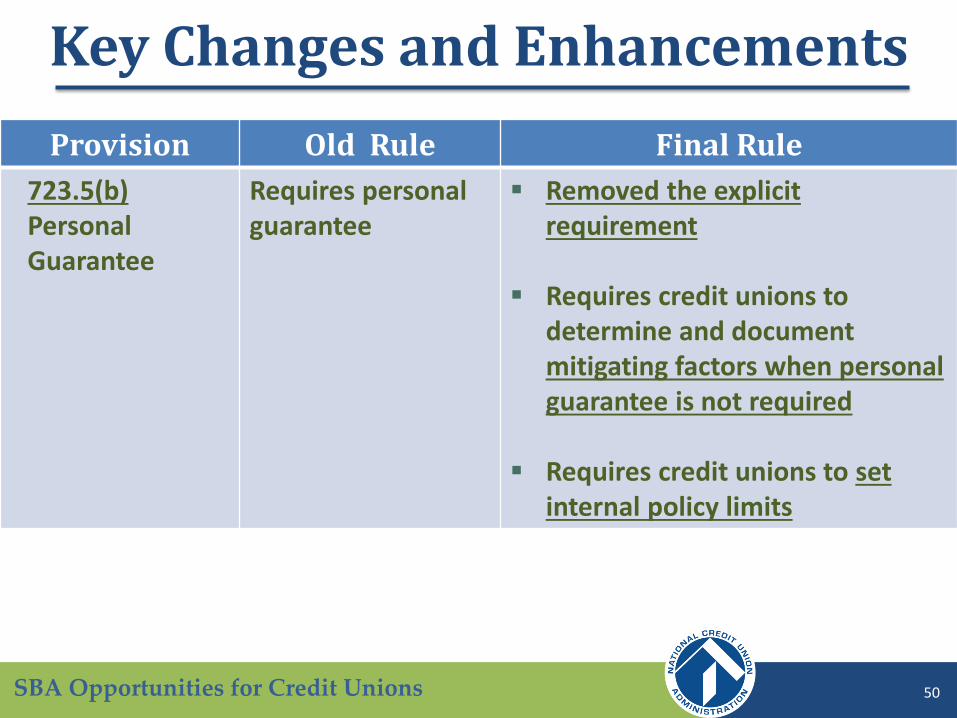

SBA Opportunities for Credit Unions 50

Provision Old Rule Final Rule

723.5(b) Personal Guarantee

Requires personal guarantee

Removed the explicit requirement

Requires credit unions to determine and document mitigating factors when personal guarantee is not required

Requires credit unions to set internal policy limits

Key Changes and Enhancements

SBA Opportunities for Credit Unions 51

Provision Old Rule Final Rule

723.6 Construction and Development Loans

25% equity interest

15% of net worth

Removed the limits

Clearly defines collateral valuation method

Requires CUs to value collateral appropriately and ensure risk sharing

Requires CUs to set internal policy limit

Stipulates loan administration requirements

Key Changes and Enhancements

SBA Opportunities for Credit Unions 52

Provision Old Rule Final Rule

723.8 Non-member business loan participations

Included in the MBL cap unless waiver is granted

Removed non-member business loans from the calculation against the MBL cap

No longer requires waivers

Key Changes and Enhancements

SBA Opportunities for Credit Unions 53

Provision Old Rule Final Rule

723.10 State Rule

Seven states have parallel state rules (CT, IL, MD, OR, TX, WA, WI)

Grandfathers the 7 existing state rules

Preserves the option for a state to develop state rule that complies with FCU Act and is at least as stringent as Part 723

Key Changes and Enhancements

SBA Opportunities for Credit Unions 54

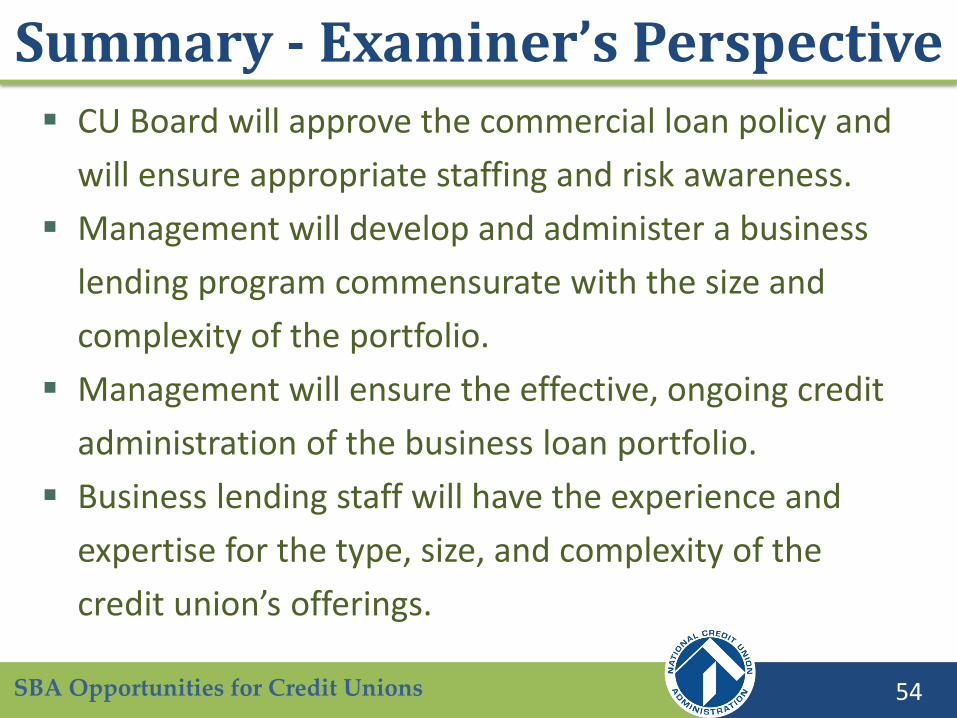

Summary - Examiner’s Perspective CU Board will approve the commercial loan policy and

will ensure appropriate staffing and risk awareness.

Management will develop and administer a business

lending program commensurate with the size and

complexity of the portfolio.

Management will ensure the effective, ongoing credit

administration of the business loan portfolio.

Business lending staff will have the experience and

expertise for the type, size, and complexity of the

credit union’s offerings.

SBA Opportunities for Credit Unions

NCUA References

55

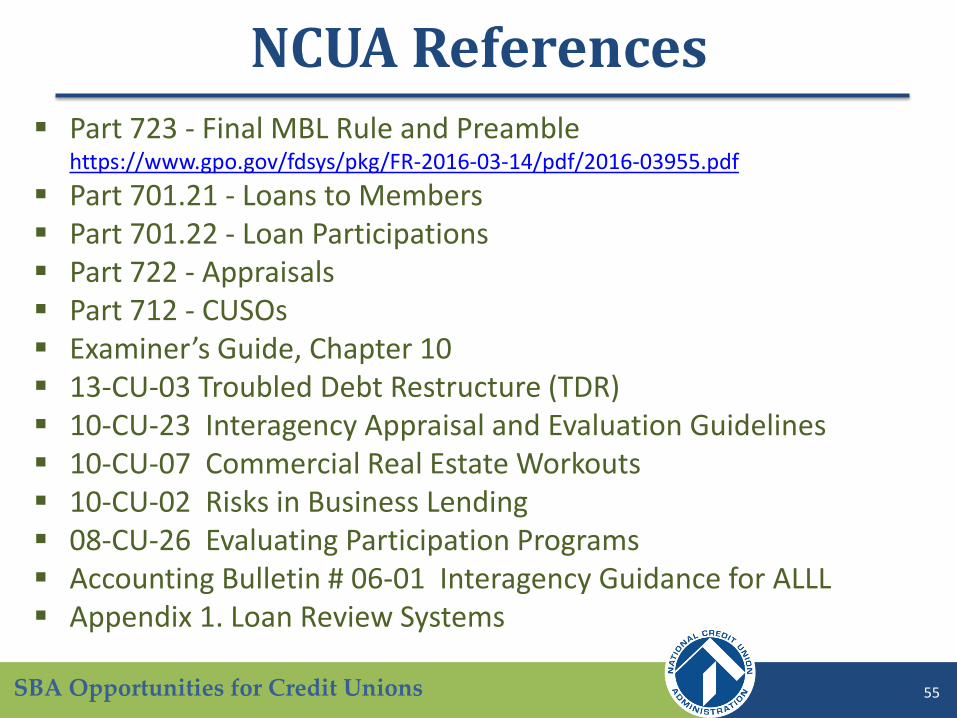

Part 723 - Final MBL Rule and Preamble https://www.gpo.gov/fdsys/pkg/FR-2016-03-14/pdf/2016-03955.pdf

Part 701.21 - Loans to Members Part 701.22 - Loan Participations Part 722 - Appraisals Part 712 - CUSOs Examiner’s Guide, Chapter 10 13-CU-03 Troubled Debt Restructure (TDR) 10-CU-23 Interagency Appraisal and Evaluation Guidelines 10-CU-07 Commercial Real Estate Workouts 10-CU-02 Risks in Business Lending 08-CU-26 Evaluating Participation Programs Accounting Bulletin # 06-01 Interagency Guidance for ALLL Appendix 1. Loan Review Systems

SBA Opportunities for Credit Unions 56

Poll #4

Which MBL rule change is most helpful?

Moving from prescriptive requirements to principles-based standards

Clarifying and expanding guidance on commercial lending risk management practices

Eliminating the need for NCUA waivers

Differentiating commercial loans from the MBL statutory definition

N/A

SBA Opportunities for Credit Unions 57

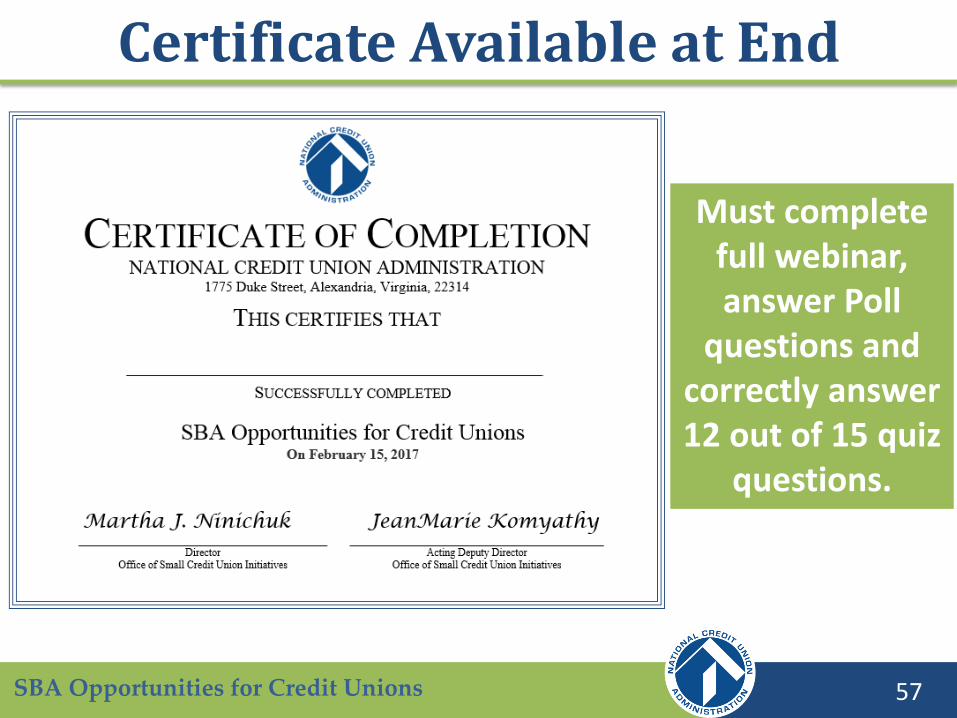

Certificate Available at End

Must complete full webinar, answer Poll

questions and correctly answer 12 out of 15 quiz

questions.

SBA Opportunities for Credit Unions 58

CDFI Certification - More Than One Way to Get There: The June 23, 2016 joint-agency webinar explained the two methods a credit union may use for becoming a CDFI.

CDFI Fund Certification: This video explains the benefits of CDFI certification and guidance from the CDFI Fund for credit unions using the traditional application.

Announcement for the Community Development Financial Institution (CDFI) Initiative

We encourage credit unions to explore the benefits of becoming a CDFI-certified credit union.

SBA Opportunities for Credit Unions

Q & A Session

You may submit a question at any time in the “Ask A Question” box, which you should see on

the left side of the console window.

59

SBA Opportunities for Credit Unions 60

NCUA Contact Page

Office of Small Credit Union Initiatives

[email protected] Phone: 703-518-6610

FAX: 703-518-6619

![LWK 0-11 B4 - Startseite - [WSA Berlin] · ugm tca tem sba acm smm smm acm aam aam sba agm agm cbm qrm sbm sba sbm tma sba psm tma tca tma tcm sba pda sba sbm sbm sba tcm ara tmm](https://img.dokumen.tips/doc/110x75/5e04232e2810341c1c798ad3/lwk-0-11-b4-startseite-wsa-berlin-ugm-tca-tem-sba-acm-smm-smm-acm-aam-aam.jpg)