Embed Size (px)

Citation preview

SPONSORSHIP VALUATION

NSF SPONSORSHIP VALUATIONFEBRUARY 2016 | CALGARY & OTTAWAFACILITATION SESSIONS

2

Our GoalOBJECTIVES OF THE SESSION

•Sponsorship: to provide participants with knowledge and application competencies through an interactive leadership exercise

•Sponsorship valuation: to share the results of the initial stages in the NSF valuation process with participants

EXPECTATIONS FOR THE VALUATION PROJECT

Introduction

4

Overall Project GoalOUR COMMITMENT TO YOU (BY MAY 30)

•To provide you with a sponsorship valuation of your NSF and outline a strategy framework upon which you can base decisions about your sponsorship activities

TIMING

5

Expectations

Feb 19/23

Facilitation Sessions

Feb 29

Survey Closed

Mar 24

Report Completion

Apr

DigestReport

May

Webinar Review

6

TIMING

•Facilitation Sessions in Ottawa & Calgary

Expectations

Feb 19/23

Facilitation Sessions

Feb 29

Survey Closed

Mar 24

Report Completion

Apr

DigestReport

May

Webinar Review

7

TIMING

•Deadline for completion of survey responses by all NSFs that wish to receive a study

Expectations

Feb 19/23

Facilitation Sessions

Feb 29

Survey Closed

Mar 24

Report Completion

Apr

DigestReport

May

Webinar Review

8

TIMING

•Analysis of survey results, including benchmarking and secondary research

•Crafting reports for NSFs by cluster, and an overall report for the COC

Expectations

Feb 19/23

Facilitation Sessions

Feb 29

Survey Closed

Mar 24

Report Completion

Apr

DigestReport

May

Webinar Review

9

TIMING

•Draft reports shared

•NSFs to read, review and share their reports

•Opportunity for feedback

Expectations

Feb 19/23

Facilitation Sessions

Feb 29

Survey Closed

Mar 24

Report Completion

Apr

DigestReport

May

Webinar Review

10

TIMING

•Final presentation via a webinar (or webinars) to take you through the report and answer any questions/clarify the valuation

Expectations

Feb 19/23

Facilitation Sessions

Feb 29

Survey Closed

Mar 24

Report Completion

Apr

DigestReport

May

Webinar Review

BACKGROUND

Method

12

Project Outline•This project is an extensive benchmarking

process to support the strategy decisions of NSFs around sponsorship

•We will use a variety of data sources - primary and secondary - to cluster NSF’s and to provide each cluster and each NSF with an estimate of their sponsorship value based on ‘real data’ from comparable properties from all sponsorship industries

13

PHASES

Approach

1Establish

Objectives

2Situational

Analysis

3NSF

Analysis

4Benchmarking

Analysis

5Sponsorship

Strategy

14

PHASES

•Identify and fully understand the key outcomes and objectives of the COC and each participating NSF

Approach

1Establish

Objectives

2Situational

Analysis

3NSF

Analysis

4Benchmarking

Analysis

5Sponsorship

Strategy

15

PHASES

•Understand the internal and external environmental factors that impact sponsorship

Approach

1Establish

Objectives

2Situational

Analysis

3NSF

Analysis

4Benchmarking

Analysis

5Sponsorship

Strategy

16

PHASES

•Undertake primary and secondary research related to the participating NSFs to assess sponsorship reality by NSF cluster

Approach

1Establish

Objectives

2Situational

Analysis

3NSF

Analysis

4Benchmarking

Analysis

5Sponsorship

Strategy

17

PHASES

•Benchmark NSFs against other properties (NSFs, sport, and non-sport) to understand where they should be in terms of sponsorship revenue

Approach

1Establish

Objectives

2Situational

Analysis

3NSF

Analysis

4Benchmarking

Analysis

5Sponsorship

Strategy

18

PHASES

•Provide strategic direction and recommendations for participating NSFs in their pursuit of sponsorship

Approach

1Establish

Objectives

2Situational

Analysis

3NSF

Analysis

4Benchmarking

Analysis

5Sponsorship

Strategy

GENERAL

Sponsorship in Canada

Survey is open until April 15, 2016. Visit www.sponsorshiplandscape.ca to enter responses!

AnalysisTrends, Comparative

DesignPerspectives, Industry

OriginsIndustry Need, Share

ProcessOnline, Partners, Streamline

3,430 Respondents2006 to 2015#22.7% CEOs2006 to 2015

CSLS RESPONDENTS

21

0

100

200

300

400

500

600

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

65

117132

152

238218

294

145

167

247

3431334852

73

123

6561

86

2534457481

116142

67109

171

Re

spo

nd

en

ts (

#)

Sponsors Agencies Properties

2016 So Far: 92.7% EN, 7.3% FR55.2% For-Profit, 44.8% NFP

Sponsorship Industry

22

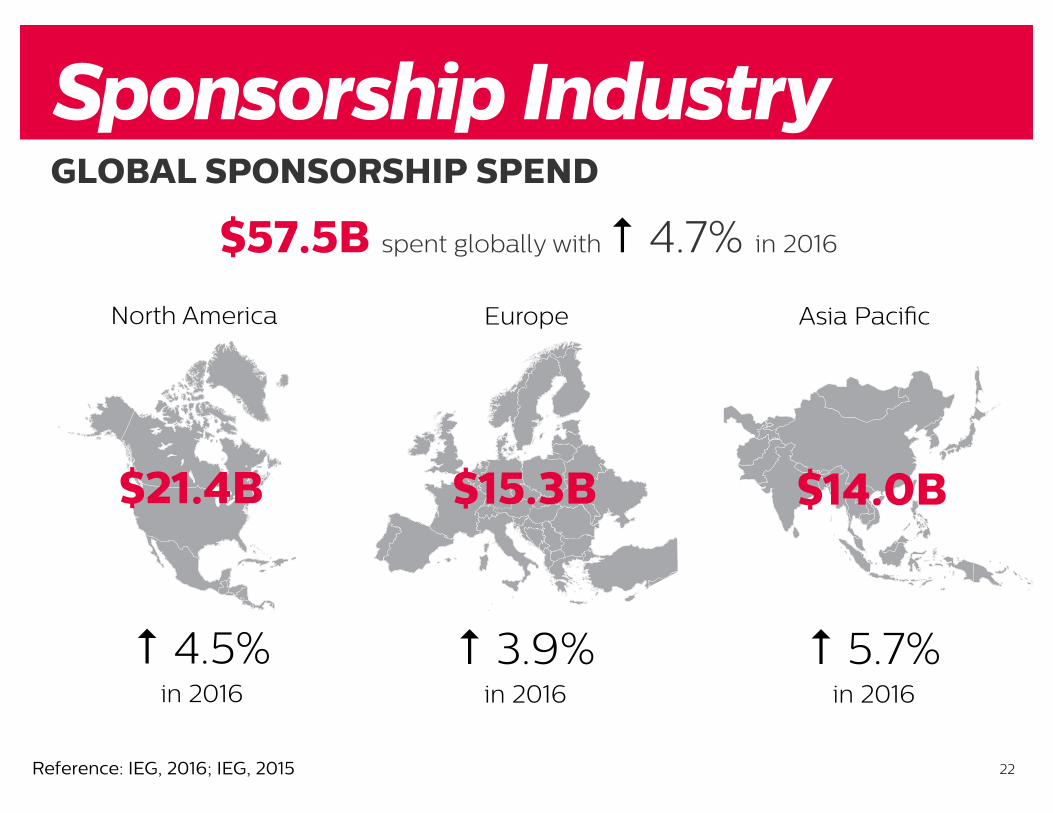

GLOBAL SPONSORSHIP SPEND

$57.5B spent globally with ↑ 4.7% in 2016

Sponsorship Industry

$21.4B

$15.3B $14.0B

↑ 4.5%in 2016

↑ 3.9%in 2016

↑ 5.7%in 2016

North America Europe Asia Pacific

Reference: IEG, 2016; IEG, 2015

23

SPONSORSHIP IN CANADA

Sponsorship Industry

$2.59B Industry Size (Rights

Fees + Activation)

$1.74B Sponsorship Spend

1 of 4 Marketing Dollars are Spent on Sponsorship

50% Industry Growth Since

2006

24

SPONSORSHIP IN CANADA

Sponsorship Industry

$0

$0.20

$0.40

$0.60

$0.80

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

0.43 0.46

0.710.76

0.620.57

0.75

0.62

0.41

0.49

Rig

hts

Fe

es:

Act

ivat

ion

Sp

en

d

Historical Activation Ratio

25

SPONSORSHIP IN CANADA

Sponsorship Industry

0%

2.0%

4.0%

6.0%

8.0%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

7.8%

4.5%

6.0%

4.1%

2.6% 2.3%2.7% 3.0%

1.1%

3.4%

Pe

rce

nt

of S

po

nso

rsh

ip S

pe

nd

Historical Spend on Sponsorship Evaluation

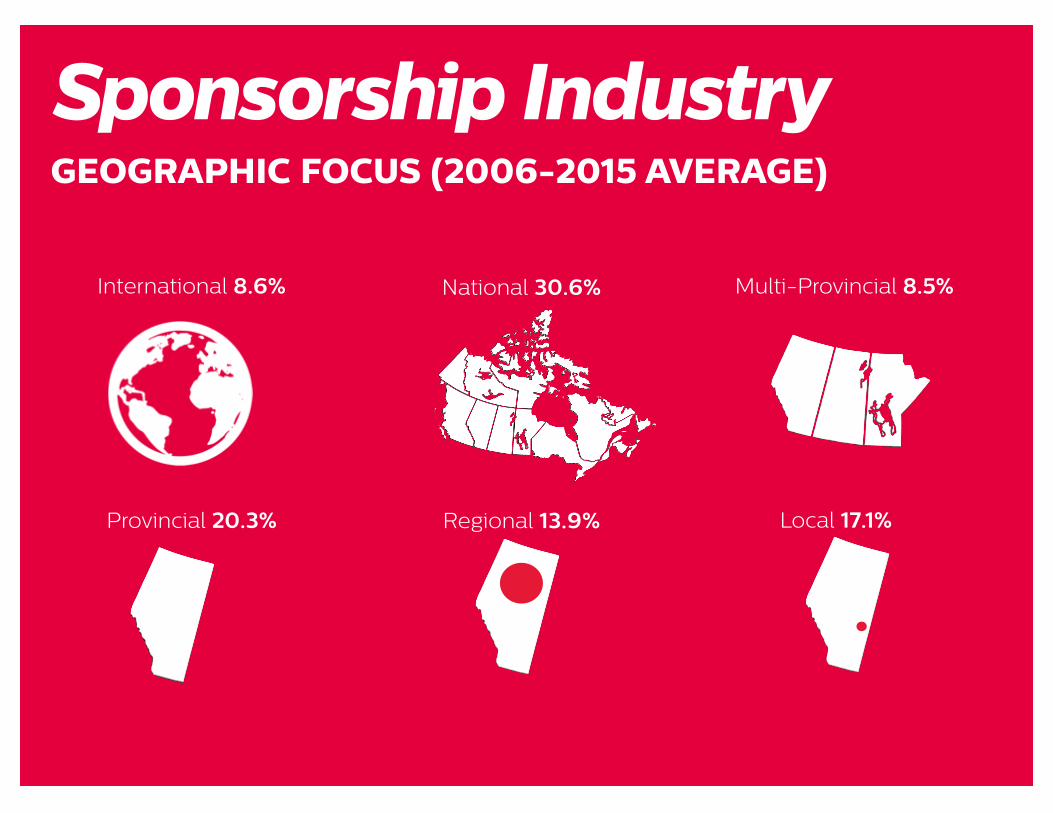

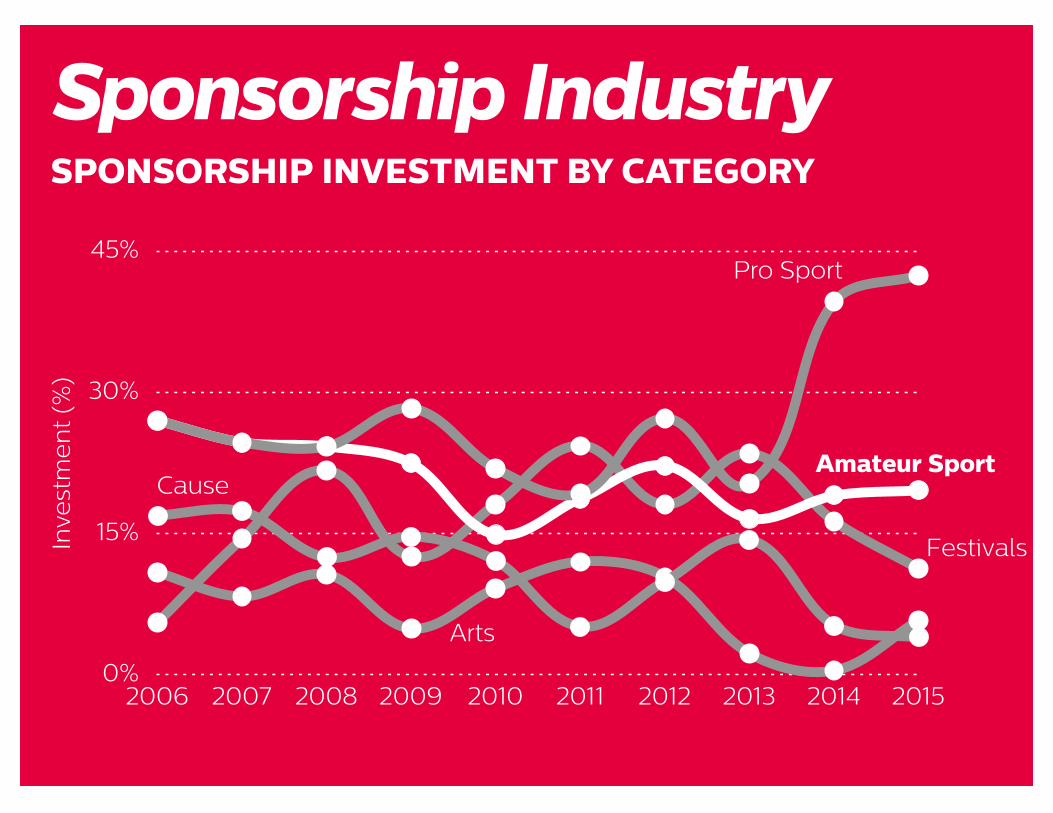

GEOGRAPHIC FOCUS (2006-2015 AVERAGE)

International 8.6% National 30.6% Multi-Provincial 8.5%

Provincial 20.3% Regional 13.9% Local 17.1%

Sponsorship Industry

0%

18%

35%

53%

70%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Inve

stm

en

t (%

)

Sponsorship IndustryCATEGORY OF LARGEST INVESTMENT

Pro Sport

Amateur Sport

EntertainmentFestivals

Avg

. Rig

hts

Fe

e (

$M)

$1.50

$1.20

$0.90

$0.60

$0.30

$0

Sponsorship Industry

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

$0.05$0.13

$1.20

$0.67$0.58

$1.26

$1.06

$0.72

$0.85

$1.34

LARGEST RIGHTS FEE ($M)

NSF-RELATED FINDINGS

Sponsorship in Canada

30

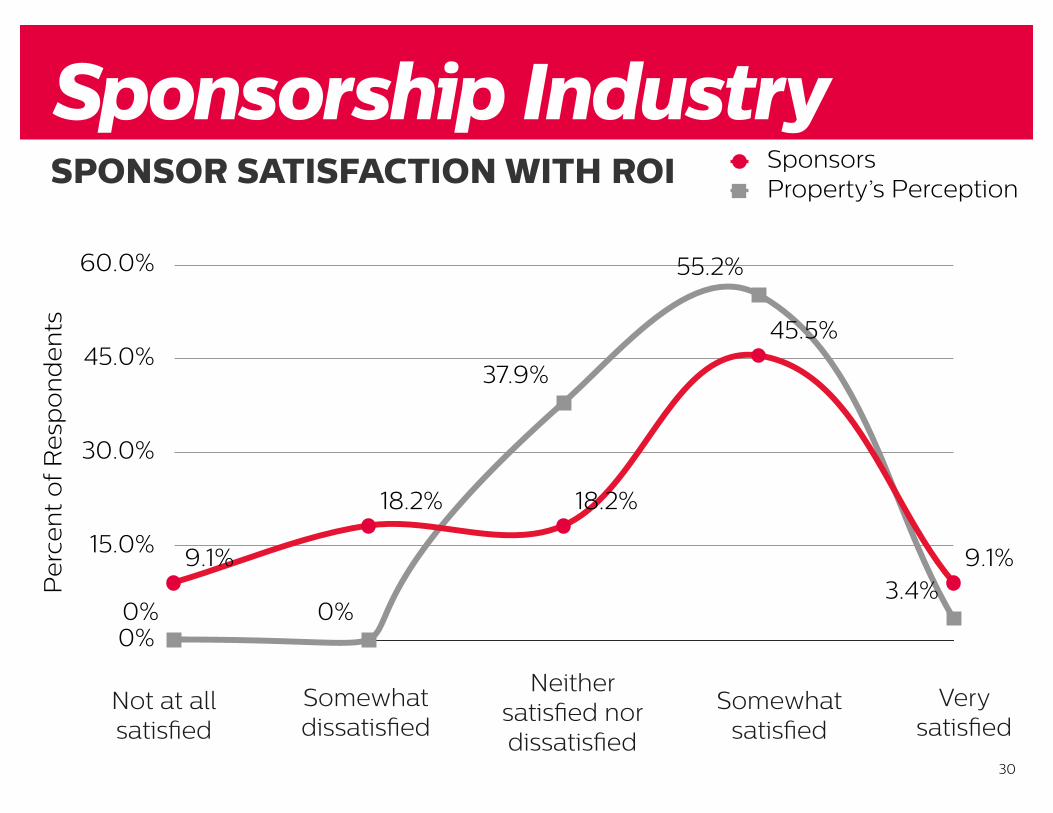

SPONSOR SATISFACTION WITH ROI

Sponsorship Industry

0%

15.0%

30.0%

45.0%

60.0%

0% 0%

37.9%

55.2%

3.4%9.1%

18.2% 18.2%

45.5%

9.1%

Pe

rce

nt

of R

esp

on

de

nts

SponsorsProperty’s Perception

Not at all satisfied

Somewhat dissatisfied

Neither satisfied nor dissatisfied

Somewhat satisfied

Very satisfied

31

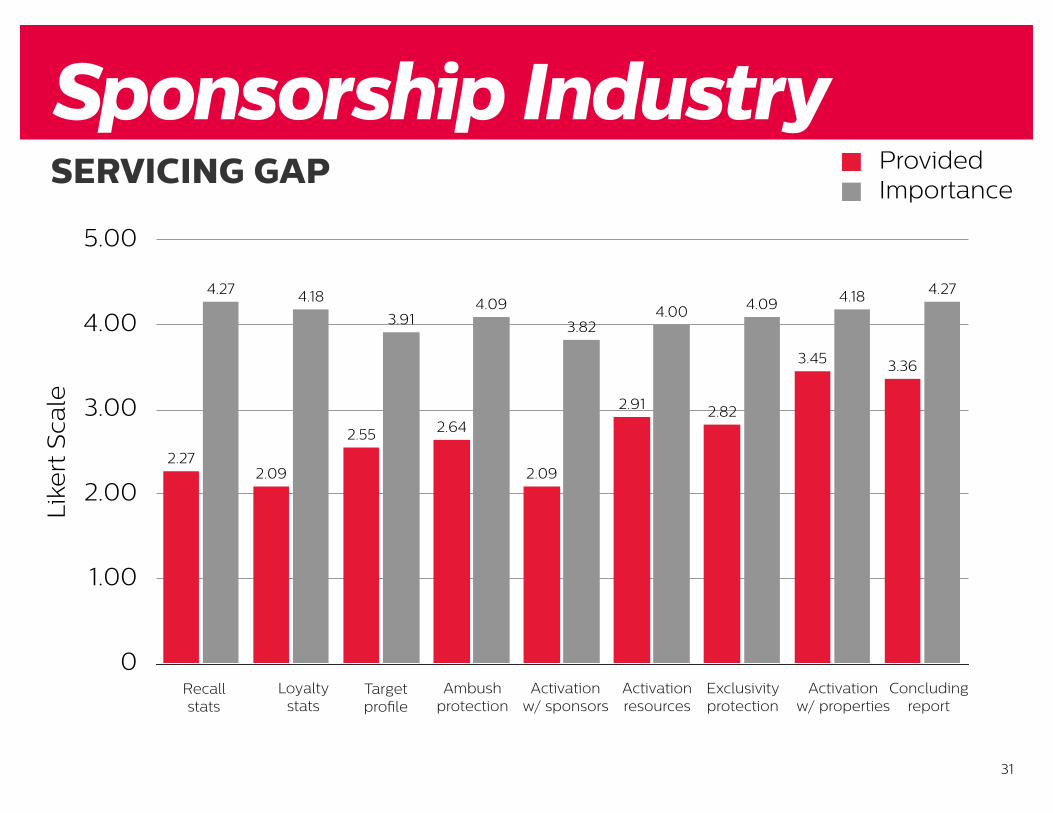

SERVICING GAP

Sponsorship Industry

Recallstats

0

1.00

2.00

3.00

4.00

5.00

4.274.184.094.003.82

4.093.91

4.184.27

3.363.45

2.822.91

2.09

2.642.55

2.092.27

Like

rt S

cale

ProvidedImportance

Loyalty stats

Target profile

Ambush protection

Activation w/ sponsors

Activation resources

Exclusivity protection

Activation w/ properties

Concluding report

Sponsorship IndustrySERVICING GAP (CONCLUDING REPORT)

0

1.00

2.00

3.00

4.00

5.00

2009 2010 2011 2012 2013 2014 2015

3.343.02 3.03 2.98

3.45 3.543.36

4.034.22

3.953.64

4.38 4.544.27

Se

rvic

es

Exp

ect

ed

/Pro

vid

ed

Expected

Provided

Sponsorship IndustrySERVICING GAP (ACTIVATION RESOURCES)

0

1.00

2.00

3.00

4.00

5.00

2009 2010 2011 2012 2013 2014 2015

3.032.84

2.592.82

3.13

2.08

2.91

4.00 3.904.09

4.33 4.17

4.77

4.00

Se

rvic

es

Exp

ect

ed

/Pro

vid

ed

Expected

Provided

0%

15%

30%

45%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Inve

stm

en

t (%

)

Sponsorship IndustrySPONSORSHIP INVESTMENT BY CATEGORY

Pro Sport

Amateur SportCause

Festivals

Arts

$0

$100

$200

$300

$400

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

$342$317

$295

$349

$298

$231

$322$338

$301$300

Am

ou

nt

($M

)

Sponsorship IndustryAMATEUR SPORT SPONSORSHIP

36

Sponsorship IndustryNSF SPONSORSHIP (Data Tidbits from 10 years of CSLS)

• 196 responses

• Average Sponsorship Revenue: $145,500

• No ability to test reliability of sample

• Average percentage of budget from sponsorship: 6.5%

• Average number of sponsors: 11.4

• Average size of sponsorship: $13,108 ($14,491 in 2015 dollars)

SOURCE OF PROPERTY REVENUE

Sponsorship Industry

$2015 34.5%

Retail Finance Services

2014 20.5%

2013 22.1%

2015 20.7%

2014 15.9%

2013 12.3%

2015 13.8%

2014 9.1%

2013 12.9%

• 10-year cash average is 69.6% and VIK average is 30.0%

CashVIK

38

Sponsorship IndustryCASH VS. VIK REVENUE

0%

20%

40%

60%

80%

100%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

24.2%22.1%23.6%30.8%33.6%32.3%34.8%33.0%39.0%30.0%

75.8%77.9%76.4%69.2%66.4%67.7%65.2%67.0%

61.0%

70.0%

Re

spo

nd

en

ts (

%)

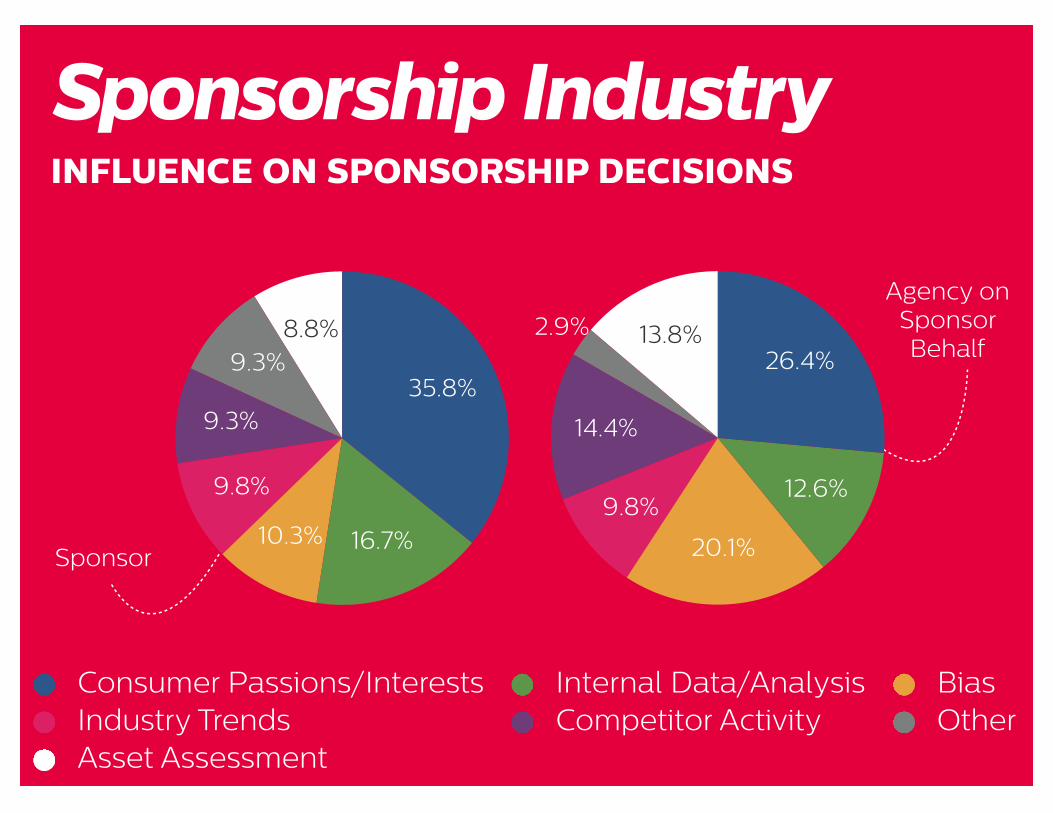

INFLUENCE ON SPONSORSHIP DECISIONS

Sponsorship Industry

8.8%9.3%

9.3%

9.8%

10.3% 16.7%

35.8%

Consumer Passions/Interests Internal Data/Analysis BiasIndustry Trends Competitor Activity OtherAsset Assessment

Sponsor

Agency on Sponsor Behalf13.8%2.9%

14.4%

9.8%

20.1%

12.6%

26.4%

ACTIVATION EXPANDS

Sponsorship Industry

0%

5%

10%

15%

20%

25%

6.0%6.3%

11.8%

15.4%

17.7%

21.7%

Act

ivat

ion

Sp

en

d (

%)

Branded content

Hosting/hospitality

Advertis-ing

Co-promotions

Socialmedia

PR

Activation Ratio (Property)

• 2015 4.10%• 2014 0.98%• 2013 0.29%

34.0% in 2014

17.0% in 2014

14.0% in 2014

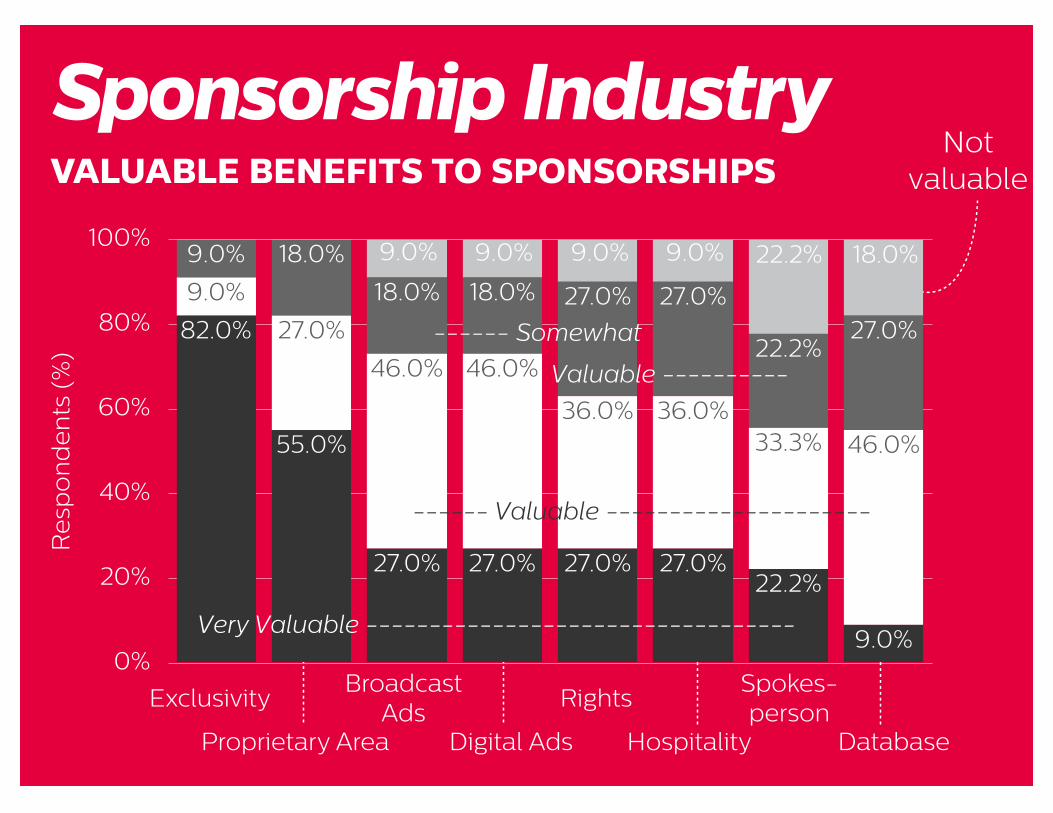

VALUABLE BENEFITS TO SPONSORSHIPS

Sponsorship Industry

ExclusivityBroadcast

AdsRights

Spokes-person

Digital AdsProprietary Area Hospitality Database

0%

20%

40%

60%

80%

100%

27.0%22.2%

27.0%27.0%18.0%18.0%

18.0%9.0%

46.0%33.3%36.0%36.0%

46.0%46.0%

27.0%

9.0%

9.0%

22.2%27.0%27.0%27.0%27.0%

55.0%

82.0%

Re

spo

nd

en

ts (

%)

9.0% 9.0% 9.0% 9.0% 18.0%22.2%

Not valuable

Very Valuable ----------------------------------

------ Valuable ---------------------

------ Somewhat

Valuable ----------

OPPORTUNITIES & THREATS TODAY

Sponsorship Industry

Opportunity Co-Sponsorship

• Having sponsors work together instead of competing for attention

• Increased integration of sponsor brands

Threat Talent Gap

• Lack of implementation, evaluation and activation knowledge

• Limited professional development opportunities• Succession planning

42

CONTENT & DIGITAL OPPORTUNITIES

Sponsorship Industry

The opportunity is well known, as is the decline of traditional mediums (e.g., cable TV). The integration across platforms, as well as enhanced digital activities are realities of sponsorship today. However, there are some very ambitious ideas expressed by industry leaders:

• “Technology opening new activation possibilities" • “Part ownership of properties by brands”• “Virtual reality to connect onsite and digital activations”• “Integrating apps with the sponsorship experience to enhance

consumer engagement thereby creating more effective sponsorships”

43

SHARED OPPORTUNITIES AND CHALLENGES

NSF Groupings

NOTE: Initial Results Only

45

METHOD

NSF Groupings

Primary Research

•Cluster Analysis - Survey Data

•CSLS Data Assessment

Secondary Research

•Case Studies

46

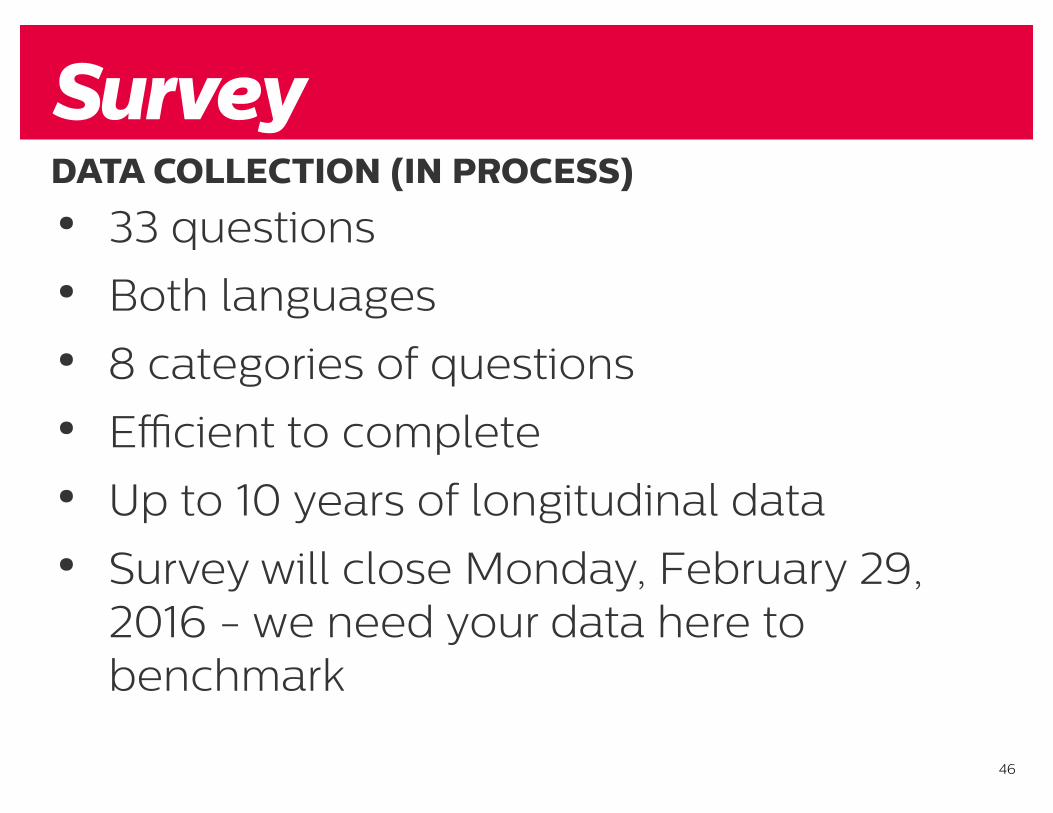

DATA COLLECTION (IN PROCESS)

• 33 questions

• Both languages

• 8 categories of questions

• Efficient to complete

• Up to 10 years of longitudinal data

• Survey will close Monday, February 29, 2016 - we need your data here to benchmark

Survey

47

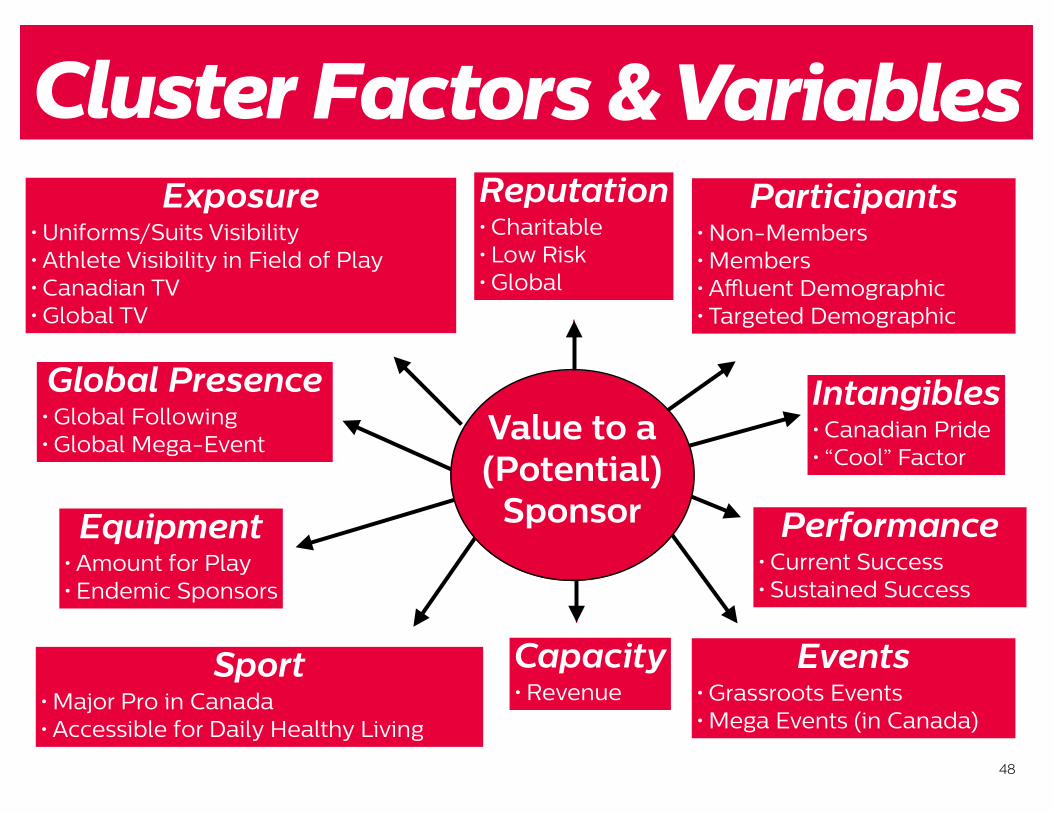

Cluster AnalysisFIRST DRAFT (PRE-SURVEY) OF CLUSTERS

•Consultation with COC: 48 NSF’s considered

•Each analyzed on 10 factors, including 24 variables

- Factors/Variables selected to represent ‘value to sponsors’

- All variables measured using a two (no/yes) or three level (low, medium, high) categorical scale, including a ‘0’ score (no)

- This analysis will be re-assessed following survey completion by NSF’s

48

Cluster Factors & VariablesExposure

• Uniforms/Suits Visibility• Athlete Visibility in Field of Play• Canadian TV• Global TV

Reputation• Charitable• Low Risk• Global

Intangibles• Canadian Pride• “Cool” Factor

Global Presence• Global Following• Global Mega-Event

Equipment• Amount for Play• Endemic Sponsors

Sport• Major Pro in Canada• Accessible for Daily Healthy Living

Events• Grassroots Events• Mega Events (in Canada)

Performance• Current Success• Sustained Success

Capacity• Revenue

Participants• Non-Members• Members• Affluent Demographic• Targeted Demographic

Value to a(Potential)

Sponsor

49

NSF Clusters

Mega ValueCanadian

Mega ValueGlobal

Performance& Participation

PRE-SURVEYPlease note that these are the initial pre-survey clusters and may change following the data analysis.

AttractiveAttributes

High Potential

Asset Build

50

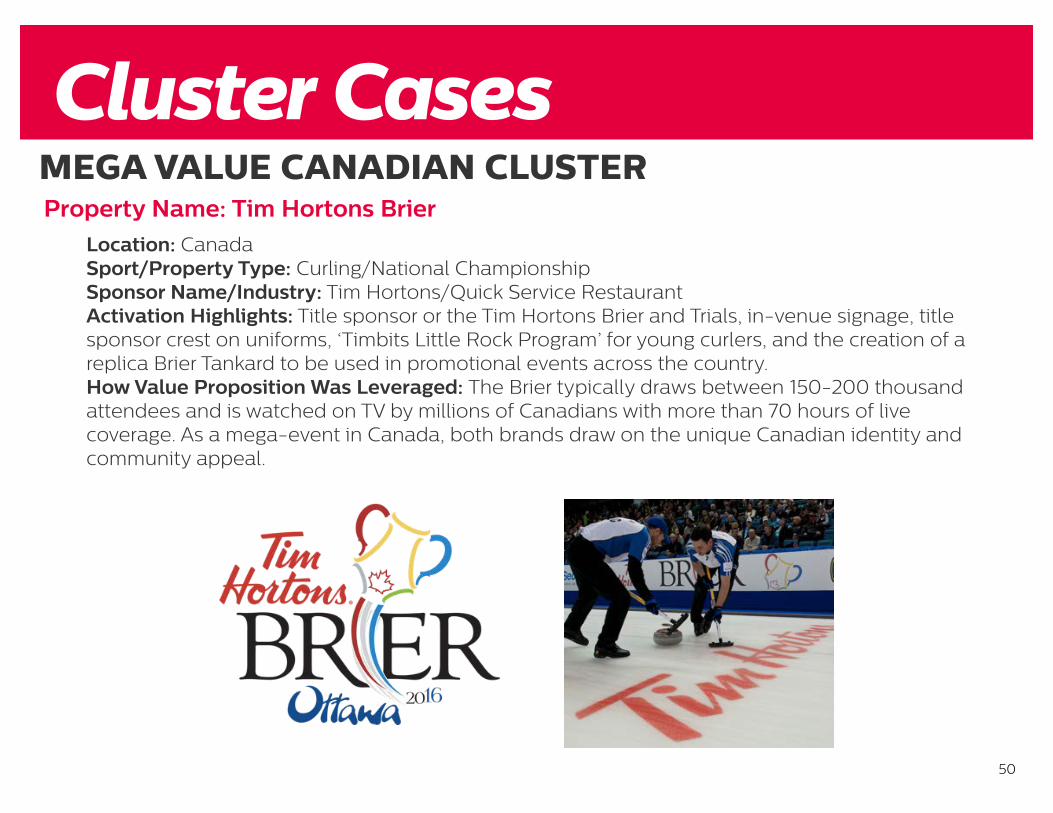

MEGA VALUE CANADIAN CLUSTERProperty Name: Tim Hortons Brier

Location: CanadaSport/Property Type: Curling/National Championship Sponsor Name/Industry: Tim Hortons/Quick Service RestaurantActivation Highlights: Title sponsor or the Tim Hortons Brier and Trials, in-venue signage, title sponsor crest on uniforms, ‘Timbits Little Rock Program’ for young curlers, and the creation of a replica Brier Tankard to be used in promotional events across the country.How Value Proposition Was Leveraged: The Brier typically draws between 150-200 thousand attendees and is watched on TV by millions of Canadians with more than 70 hours of live coverage. As a mega-event in Canada, both brands draw on the unique Canadian identity and community appeal.

Cluster Cases

51

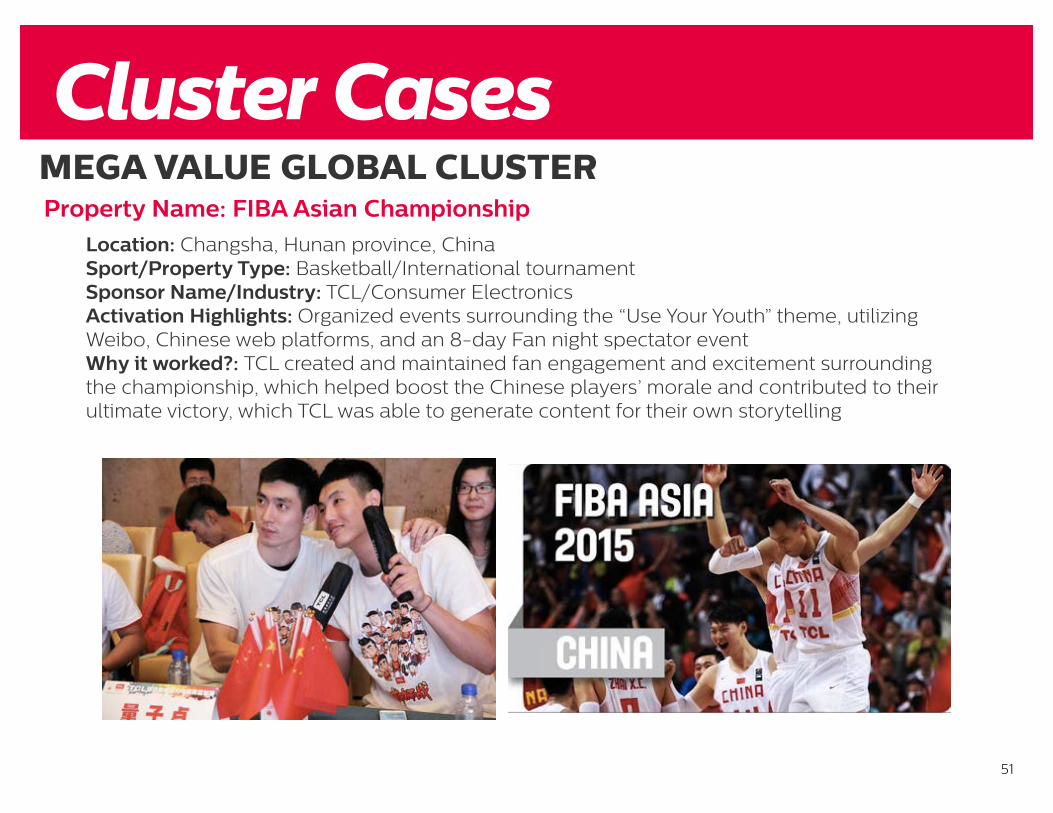

MEGA VALUE GLOBAL CLUSTERProperty Name: FIBA Asian Championship

Location: Changsha, Hunan province, ChinaSport/Property Type: Basketball/International tournamentSponsor Name/Industry: TCL/Consumer ElectronicsActivation Highlights: Organized events surrounding the “Use Your Youth” theme, utilizing Weibo, Chinese web platforms, and an 8-day Fan night spectator eventWhy it worked?: TCL created and maintained fan engagement and excitement surrounding the championship, which helped boost the Chinese players’ morale and contributed to their ultimate victory, which TCL was able to generate content for their own storytelling

Cluster Cases

52

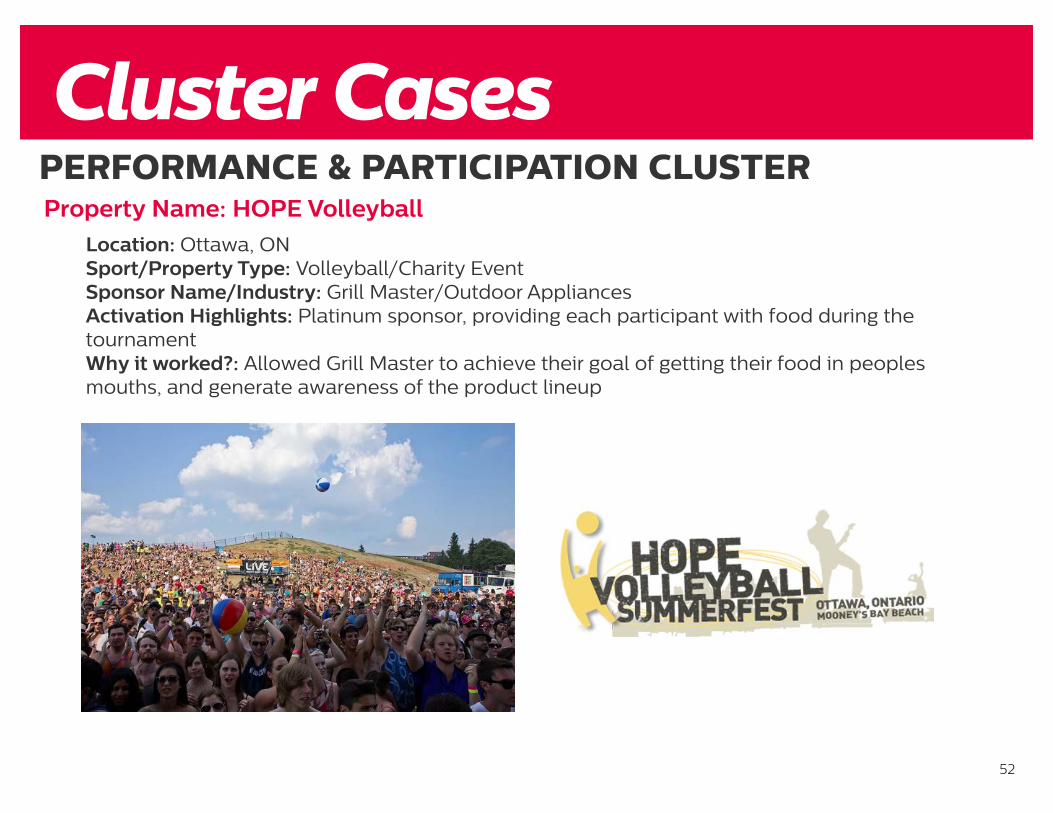

PERFORMANCE & PARTICIPATION CLUSTERProperty Name: HOPE Volleyball

Location: Ottawa, ONSport/Property Type: Volleyball/Charity EventSponsor Name/Industry: Grill Master/Outdoor AppliancesActivation Highlights: Platinum sponsor, providing each participant with food during the tournamentWhy it worked?: Allowed Grill Master to achieve their goal of getting their food in peoples mouths, and generate awareness of the product lineup

Cluster Cases

53

ATTRACTIVE ATTRIBUTES CLUSTER

Location: Mont-Tremblant, QCSport/Property Type: Triathlon/ Local eventSponsor Name/Industry: Subaru/AutomotiveActivation Highlights: Title sponsor with Subaru cars on-site as well as tent and banners set up for increased brand exposureWhy it worked?: Connected with the brands slogan for “Confidence in Motion” and the target demographic/profile of the Ironman participant and spectator

Property Name: Subaru Ironman

Cluster Cases

54

HIGH POTENTIAL CLUSTER

Location: Holmenkollen, Norway Sport/Property Type: Biathlon/National Grassroots ProgramSponsor Name/Industry: Statkraft/Renewable EnergyActivation Highlights: Financial support and talent development for youth biathlon participants Why it worked?: Positive association with finding the best talent to help further develop and access to the local communities to garner interest in future potential employees

Property Name: Statkraft Young Star

Cluster Cases

55

ASSET BUILD CLUSTER

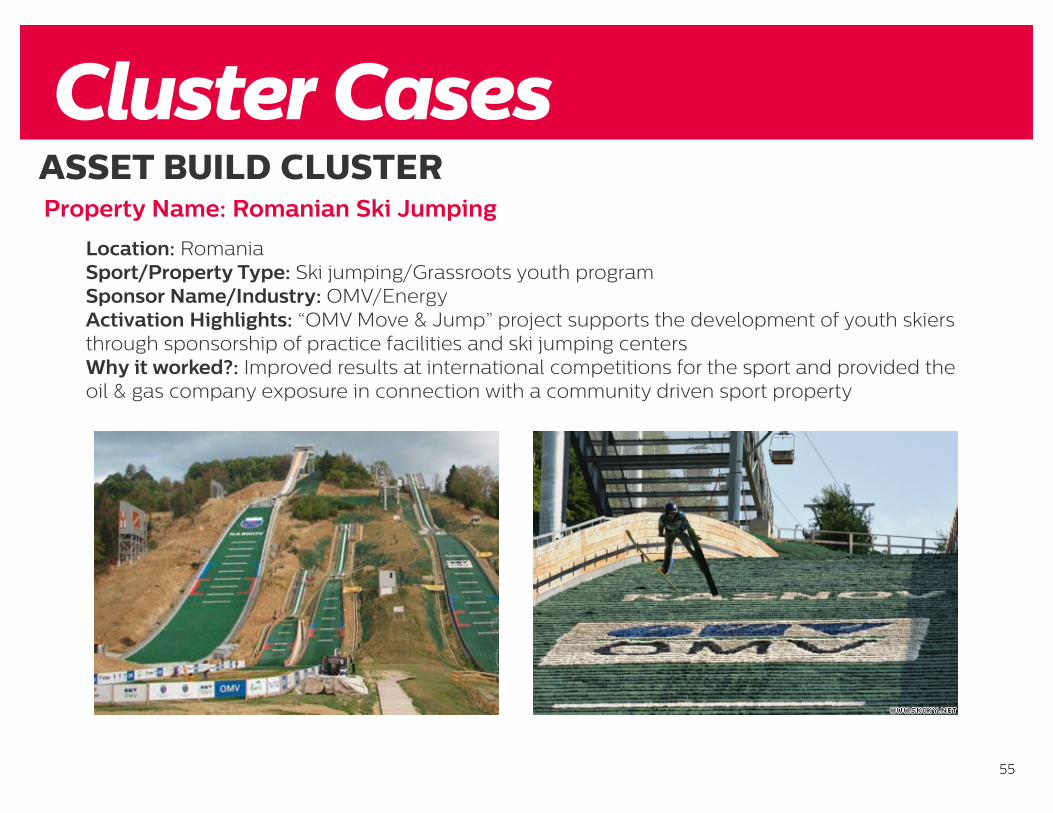

Location: RomaniaSport/Property Type: Ski jumping/Grassroots youth program Sponsor Name/Industry: OMV/EnergyActivation Highlights: “OMV Move & Jump” project supports the development of youth skiers through sponsorship of practice facilities and ski jumping centersWhy it worked?: Improved results at international competitions for the sport and provided the oil & gas company exposure in connection with a community driven sport property

Property Name: Romanian Ski Jumping

Cluster Cases

Most Valuable Property Study

57

MVP Study

A syndicated study designed to identify what drives the connection between sponsors and consumers/citizens

3

Value Partnership Love

Connection

SPONSOR CONSUMER PROPERTY

58

METHOD

•Focus Groups •Survey: 2012, 2014, 2015, 2016•2016 Survey

- 100 Properties- 2,500 Canadians surveyed

MVP Study

59

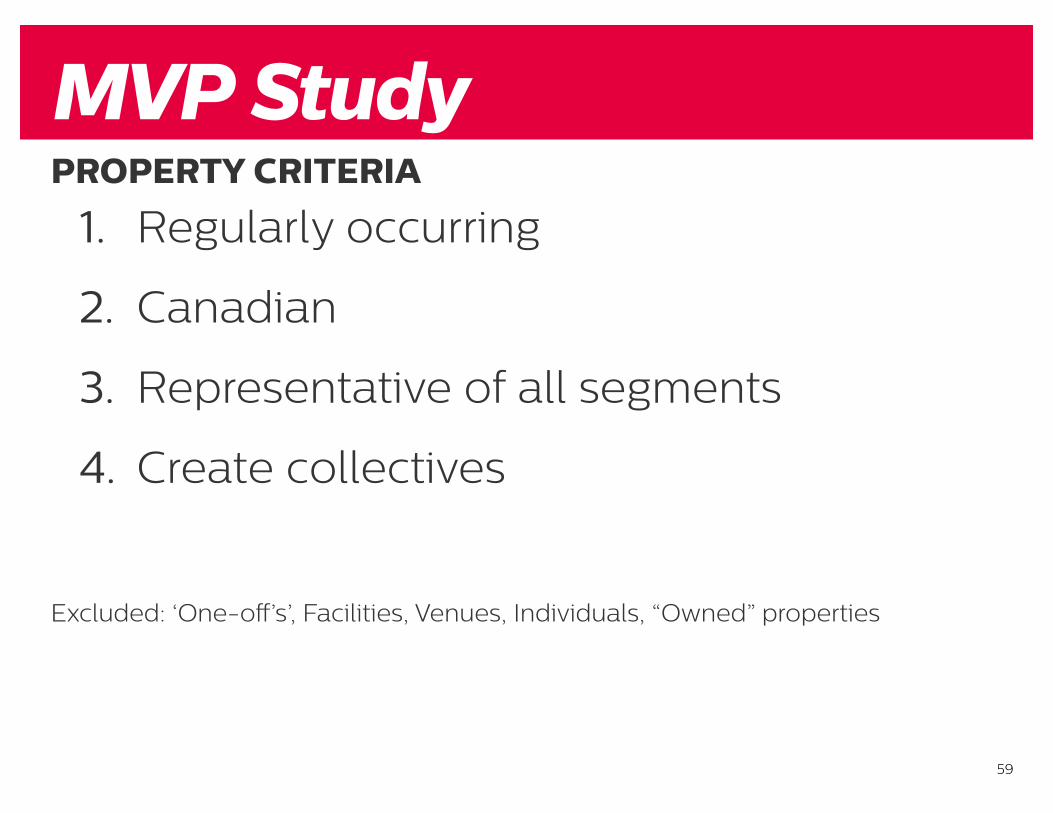

MVP StudyPROPERTY CRITERIA

1. Regularly occurring

2. Canadian

3. Representative of all segments

4. Create collectives

Excluded: ‘One-off’s’, Facilities, Venues, Individuals, “Owned” properties

60

MVP Study

69

Personal Involvement

67

Creating the Mom

ent

65

Impact on Cause

56

Sponsor Fit Herit

age

47

Respo

nsibl

e

44

Uniq

uene

ss

45

7 D

river

s of

Val

ue

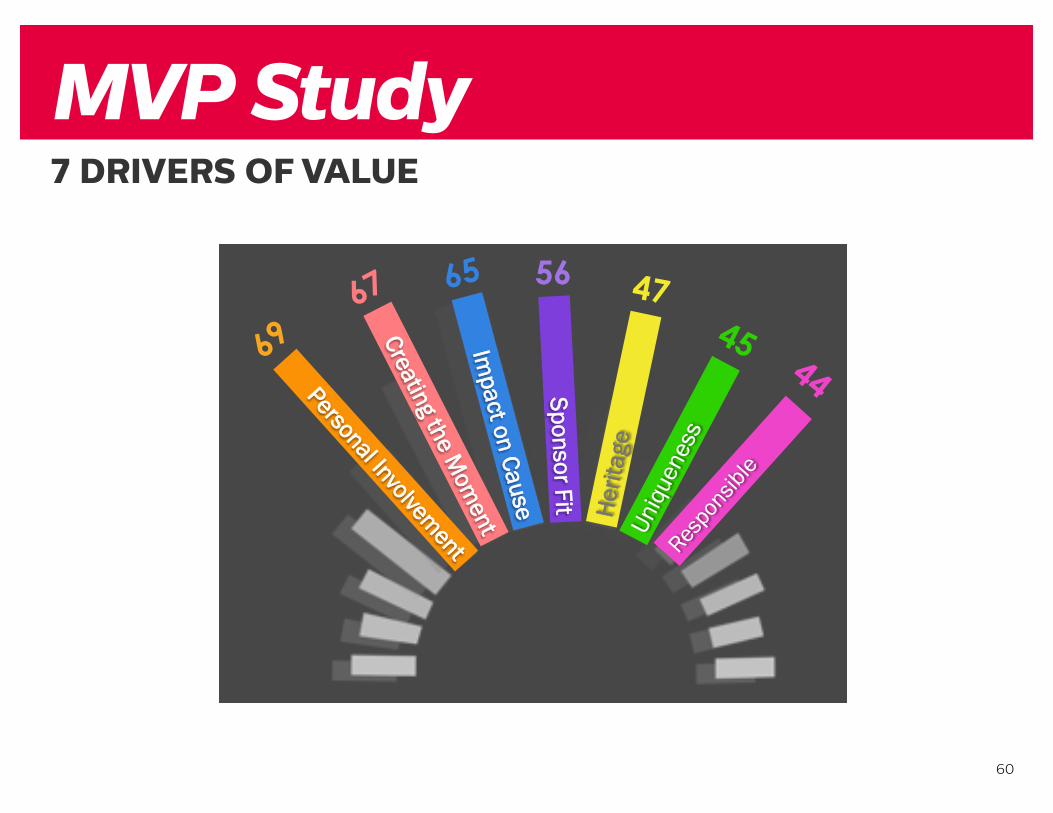

7 DRIVERS OF VALUE

PROPERTY CATEGORIES

61

MVP Study

28

EVENTS

ARTS

ENTERTAINMENT

HEALTH CAUSES

YOUTH CAUSES

AMATEUR SPORTS

PROFESSIONAL SPORTS

SOCIAL CAUSES

PAST MVPS BY CATEGORY

62

MVP Study

31

Past MVPs

Major Museum or Art Gallery

Winter Cultural Festivals

Nearest Theme Park /

Attraction

Major Museum or Art Gallery

Summer Cultural Festivals

Hockey Night in Canada

Major Performance

Arts or Theatre

Program in the nearest city

Arts Festivals in the Nearest

Major City

Hockey Night in Canada

Pro Sports Health Youth Social Entertainment Events Arts Amateur Sports

Favourite NHL Team

Canadian Olympic Team

National Hockey League

Canadian Paralympic

Team

Favourite NHL Team

Canadian Olympic Team

WWF Kids Help Phone

Canadian Cancer

Society/ Relay for Life

Salvation Army

United Nations Children’s

Fund Heart & Stroke

Salvation Army

Big Brothers and Sisters

Canadian Cancer

Society/ Relay for Life 20

12

2014

20

15

63

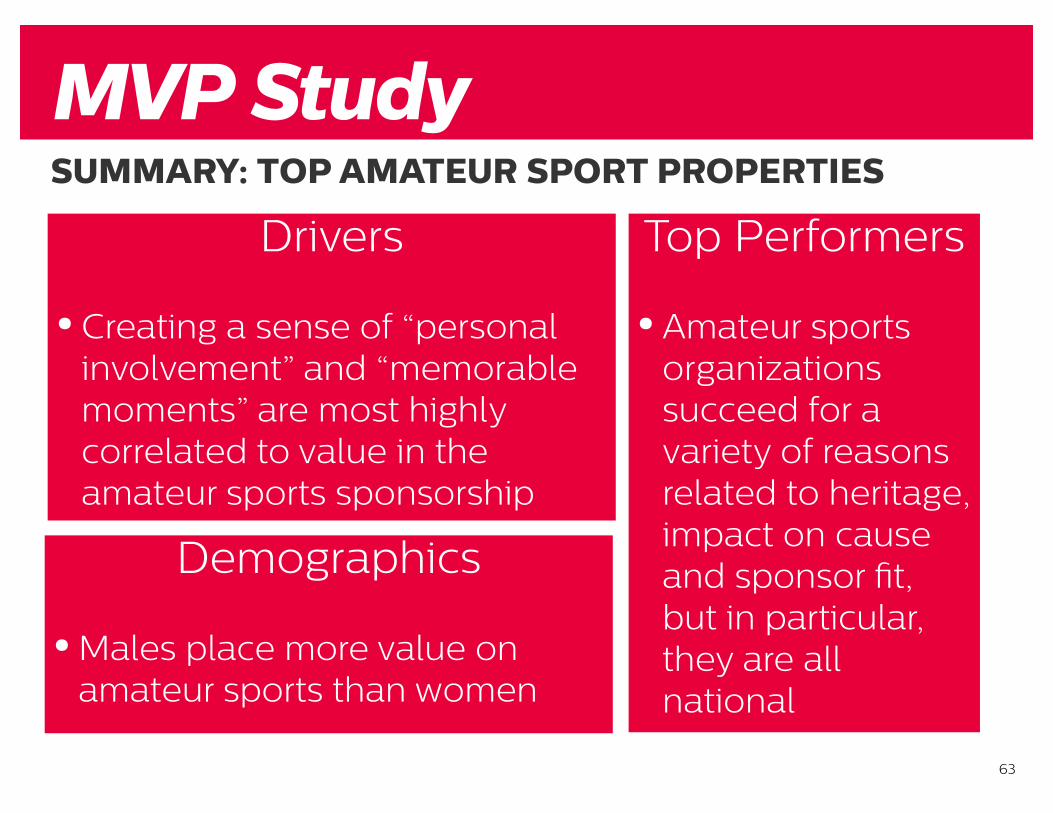

SUMMARY: TOP AMATEUR SPORT PROPERTIES

MVP Study

Drivers

•Creating a sense of “personal involvement” and “memorable moments” are most highly correlated to value in the amateur sports sponsorship

Top Performers

•Amateur sports organizations succeed for a variety of reasons related to heritage, impact on cause and sponsor fit, but in particular, they are all national

Demographics

•Males place more value on amateur sports than women

64

OVERALL KEY LEARNINGS

•Cause Champions: Sponsors are often rewarded when they are clear champions of the cause. The Sponsor - Property fit remains key

•Memories: Canadians connect through events that create collective, memorable moments

•Engagement: Getting the public personally involved. Mobilizing Canadians in communities across the country

•Building Community: If a property is attempting to make the world a better place or improve community life, it’s more likely to connect sponsors to the public

MVP Study

What Sponsors Want

5 PILLARS OFSPONSORSHIP

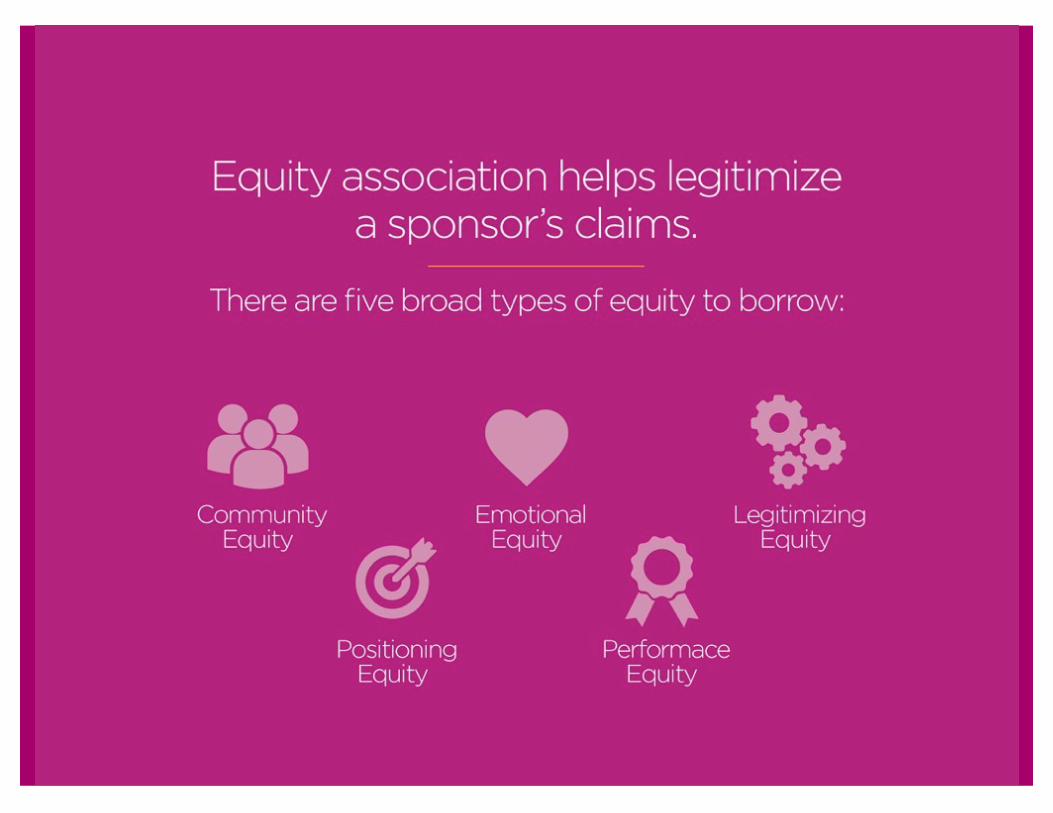

Borrowing Equity

Telling Stories

Engaging Stakeholders

Seeing Proof Getting Promoted

GETTING PROMOTED

Create a vision of working together

Help your sponsor do their job better

Help them write their internal recommendation

Develop planning tools to build your credibility

• Sponsorship Fulfillment Plan

• Quarterly Planning Sessions

• Online Partner Support

• Monthly Reports

• Validated ROI

Provide the support, reports, and plans to keep your partner

confident in the final result.

Elevate your role from selling your property to providing solutions.

5 PILLARS OFSPONSORSHIP

Borrowing Equity

Telling Stories

Engaging Stakeholders

Seeing Proof Getting Promoted

Sponsorship Fulfillment

84

COMPREHENSIVE APPROACH

Fulfillment Model

Sp

on

sors

hip

Fu

lfillm

ent

Servicing

Evaluation

Activation

85

PROPERTIES SHOULD INVEST IN SPONSORSHIP

Fulfillment Model

$

Sp

on

sors

hip

Rig

hts

Fee

Evaluation• % of individual sponsor

Servicing• % of individual sponsor

Activation• % of individual sponsor

DIRECT & INDIRECT (ACTIVATION) INVESTMENTS IN SPORTS SPONSORSHIPS

86

Activation 101DIRECT AND INDIRECT (ACTIVATION) INVESTMENTS

IN SPORTS SPONSORSHIP

A: DIRECT SPONSORSHIP INVESTMENT

B: INDIRECT (ACTIVATION) SPONSORSHIP INVESTMENT

Foster, O’Reilly & Davila, 2016

A. DIRECT SPONSORSHIP INVESTMENT

B. INDIRECT (ACTIVATION) SPONSORSHIP INVESTMENTS

87

•All the activities undertaken to enhance a sponsorship

•Types of Activation- Traditional (e.g., packaging, VIP’s,

hospitality)- Value-Adding (e.g., social media,

branded content, creative)

Activation Specifics

88

Activation SpecificsEXAMPLES•Advertising

•Event signage

•Public relations

•Banners

•Uniform logos

•Offsite events/promotions

•Vehicle signage

•PA announcements

•Logo placement

•Scoreboard promotions

•On-site activations

•Direct marketing

•Social media

•Mobile

•Digital promotions

•Blogs

•Websites

•Product sampling

•Hospitality

•VIP passes/entertainment

•Product demonstrations

•Point of Purchase (POP) displays

•Sales promotions

•Contests to drive in-store traffic

•Coupons

•Merchandising

•Sweepstakes

•Licensing

•Games/video games

•Player/athlete sponsorship

•Coach sponsorship

•League sponsorship

•Employee programs

•Staff rewards/hospitality

•Contests

• In-store displays

89

ALLOCATE RESOURCES FOR CONTRACT DELIVERY

•Set aside a small percentage of rights fees revenue

•Identify human resources•Build an Account Management Plan

- Contact control- Roles and responsibilities allocations- Critical path/workback schedule- Comprehensive schedule of fulfillment items - Inventory Tracking- Schedules- Reports

Servicing

90

BASED ON PUBLISHED MODEL

Evaluation1. Verify that sponsor wants an evaluation done.

2. Determine sponsor objective(s) by (i) reviewing contract, (ii) meeting contact at sponsor, and (iii) reviewing sponsor’s marketing plan.

3. Based on objectives, determine investment in evaluation, as well as metrics and methods to implement.

4. Measure before sponsorship begins to acquired benchmark(s).

5. Collect data and assess effectiveness.

6. Compare results to benchmark and objectives.

Build a body of evidence and case for renewal for your partner.

Assess if you are charging appropriate amount.

Determine if levels of activation are correct for both sponsor and property.

Assess if servicing and evaluation investments and activities by property are

sufficient.

From O’Reilly & Madill, 2011

91

If you have any questions, please let us know.

Contact InformationNORM O’REILLYPartner Consultant, T1Tel: (740) 517-7242 Email: [email protected]

ELISA BESELTConsultant, T1Tel: (416) 355-2688Email: [email protected]