Embed Size (px)

Citation preview

JOHN MCCALLUM

N O N C O N T R I B U T O R Y P E N S I O N S

F O R L E S S D E V E L O P E D C O U N T R I E S :

R E H A B I L I T A T I N G A N O L D I D E A

ABSTRACT. Less developed countries are facing choices in policies for retirement income support that bear similarities to the choices made in more developed countries 50 to 100 years ago. About 100 years ago, Australia and New Zealand developed a noncontributory pension system which continues to the present day. This system delivers basic, economic well-being at relatively low cost. Within less developed countries, values and goals for retirement income support vary widely. These axe explored in the history of the development of the Australian and New Zealand systems. This paper also examines the impact of these unique systems on several indicators of well-being. Poverty is well controlled in this system but adequate income replacement is dependent upon private, individual saving. Because of efficiency and effectiveness, this unique noncontributory system is argued to provide an important, if old, idea for less developed countries.

Key Words: aging and development, pensions, retirement income, noncontributory versus contributory welfare

INTRODUCTION

Schemes providing income security for the elderly are of three general types: basic flat rate schemes which derive money from general taxation and pay it to those in need; social insurance schemes which derive money from contributions of working people and employers and pay out according to contributions; and mixes o f basic and insurance scheme types (OECD 1988). The income support systems in Austral ia and New Zealand are o f the first type. They are unique (OECD 1988), except for the Icelandic system, in being noncontributory and the only public support for a majori ty of the aged namely, about 75 percent of Austral ians and 90 percent of New Zealanders.

This public involvement in organizing retirement income support is directed towards the goal o f relieving poverty rather than maintaining preretirement earnings levels after retirement. The latter objective is the responsibil i ty of the aging person and their family, and it is achieved mainly through private savings in ' superannuat ion ' and private housing. The public noncontributory pension is also targeted on the needy by means tests. Thus there is a strong incentive for private saving for those who desire more than a basic min imum income. Because the system delivers economic well-being in an egalitarian way at a relat ively low cost to the public sector, this paper argues that the Austral ian and New Zealand experience provides important ideas for less developed countries.

Less developed countries are now facing choices in policies for retirement income support that bear similarities to the choices made in more developed countries 50 to 100 years ago. It is important, therefore, for pol icy makers in less

Journal of Cross-Cultural Gerontology 5: 255-275, 1990. © 1990 Kluwer Academic Publishers. Printed in the Netherlands.

256 JOHN MCCALLUM

developed countries to understand the policy decisions made in these countries at a much earlier stage in their economic development. Australia and New Zealand, for example, are now approaching 100 years of history of public retirement income support. Their noncontributory, flat rate income support schemes have continued to exist despite serious consideration of contributory, eamings related schemes at numerous points in history. Just why Australia and New Zealand have followed a system of noncontributory pensions as the major part of retirement income support is the main topic considered in this paper.

Why are noncontributory pensions an important option for less developed countries today? One key premise of Bismarckian Social Security and the earlier English Poor Law of 1601 was that the needs of the elderly should not go beyond the capacity of the family to respond. The problem for a less developed country is to find a way of providing that income to families without constrain- ing other development choices. Intemational Labour Office standards and the example of most developed countries would recommend contributory systems, but a majority of citizens in less developed countries are unable to contribute to them. Because the necessity of depending on children for support in old age is a known factor in preferences for children (Bulatao 1979; Nugent and Gillaspy 1983), there are even stronger incentives to provide basic income support in less developed countries which typically have high birth rates. The strategy for development in such countries is, in part, dependent on providing a stable expectation of adequate income in old age.

The Philippines, for example, has the longest history of contributory pensions in the Asia-Pacific region (McCallum 1989a), but the schemes still only cover around eight percent of the population (Domingo 1989). The problem is that most poorer people cannot contribute or cannot be forced to contribute to schemes for retirement. I f people are to voluntarily reduce birthrates in countries such as the Philippines, more extensive provision of retirement income is necessary. Similarly, in China universal coverage of the rural population with the minimal five guarantees of food, clothing, medical care, housing and burial (McCallum 1989a) would seem to be a precondition for population control and further economic development. The minimal support of the 'five guarantees', which are means tested through the 'three no 's ' (no family, no work, and no income), are an in kind noncontributory system which potentially should be extended to provide basic support to all before contributory pensions are improved for a minority. This idea of extending a basic provision, the heart of the Australian and New Zealand model, is a practical alternative to the much more widely practiced but inequitable contributory retirement income support.

On the matter of cross-cultural policy interchanges Binstock (1986:338) has commented:

The prime challenge in drawing 'implications for policy' through cross-cultural learning would seem to be the need to maintain a keen awareness of one's own culture even as one makes observations from other cultures.

REHABILITATING NONCONTRIBUTORY PENSIONS 257

By definition, 'cul ture ' is the f ramework of beliefs, symbols and values in terms of which a particular social group defines itself. The truth is, however, that most of us are unaware of our own culture when offering advice to others. W e are most often aware of culture as an exception or as resistance to our own. Within different cultures, values and goals of retirement income support vary con- siderably. Two directions are pursued here to highlight the cultural background for these systems. Firstly the values underlying the Austral ian and New Zealand systems are observed by exploring in detail the process o f historical develop- ment of the system. Secondly this detailed historical analysis o f noncontributory pension systems reveals the developmental nature of retirement income support systems. That is to say, their current forms in developed countries are not necessarily representative of the earlier forms in place when these countries were not fully developed. These two directions embodied in history are dis- cussed here, firstly by describing the development of the major components of income and savings for old age and, secondly, by examining the impact on well- being that is generated by these resources.

INCOME AND SAVINGS

Definition of Income

A somewhat ancient definition of income from the Medical Journal of 1802, Vol. VIII: 129 reminds us of the historical and cultural specificity of definitions

of income:

Income, in its usual acceptation, is a loose and vague term; it applies equally to gross receipts and to net produce: But when legislature had limited it to be synonimous [sic] with profits and gains, it became as clear and precise as any other word.

In less developed countries, receipts and produce are still meaningfully related to income, and monetary profits and gains are the minor part o f economic resources. To deal with this in Indonesia, for example, excellent work has been done developing global measures of economic well-being comprised of non- monetary assets or conditions of l iving (Sigit 1988).

The definition of income is further dependent upon social context and purpose of definition. The provision of age pensions on the basis of ' need ' in Austral ia rather than through the mechanism of social insurance puts an added importance on how income is defined. The Austral ian Social Security Act [1947:s.3(1)] provided, for its purposes, a comprehensive definition o f income:

In this Act, unless the contrary intention appears . . . . ' income' in relation to a person means personal earnings, moneys, valuable consideration or profits, whether of a capital nature or not, earned, derived or received by that person for the person's own use or benefit by any means from any source whatsoever, within or outside Australia and includes a periodical payment or benefit by way of gift or allowance...

258 JOHN MCCALLUM

This is clearly a bureaucratic definition of income. It has caused most conflict in dealing with income derived from or accumulated in assets and capital. Thus the meaning of income in old age has been constructed by particular debates over these issues in Australia. In contrast, New Zealand has avoided this debate by removing means tests after age 65 from 1940, as will be discussed. But both countries have parallel experiences of the system discussed here and will, therefore, be treated together. The definitions of income in less developed countries will not match these, so the noncontributory systems will have to be reconsidered in different contexts.

The Age Pension

In 1898 in New Zealand and 1908 in Australia, older people became eligible for flat rate benefits from age 65 subject to need, moral character, citizenship and residency qualifications. From that time, the benefits have been paid from general revenue rather than financed by a social insurance contributory system. It is worthy of note that the argument against compulsory contributions was pioneered in Parliamentary Debates in New Zealand in terms that are relevant to less developed countries. In 1897, responding to a proposal for German Bismarckian-type social insurance, New Zealand Prime Minister Richard Seddon argued:

It would be impossible in a young country tike this to give effect to such a scheme as that in Germany, our conditions being so different. First, the work of our artisan class is intermittent. Then, our artisans and people would not for a moment agree or submit to a policeman coming and demanding contributions; that would at once meet with opposition and such a scheme would fail. (New Zealand, 1897:56)

In Australia, the New South Wales Old Age Pension Act closely followed the New Zealand legislation, and this soon became the national scheme for the Australian Commonwealth. Because they were early starters in the age welfare stakes, Australia and New Zealand were able to deal with the aged poor without succumbing to pressure to provide a universal provision to attract taxpayers generally into the scheme. They have remained resolute in this despite flirtation with alternatives throughout the 20th century.

In spite of the early rejection of the contributory approach to financing pensions for reasons of liberty, cost and effectiveness, the possibility of social insurance remained at the forefront of income security debates until the 1950s (Dixon 1978/9). The most serious attempts were made in Australia by the Lyons/Page governments in their National Health and Pensions Insurance Bill of 1938 which was discontinued at the onset of the Second World War because of vigorous criticism. The Chifley government subsequently established a wartime National Welfare Fund. A.W. Fadden, the conservative leader of the Australian Country Party and a long-time supporter of the social insurance principle, criticized the scheme as:

REHABILITATING NONCONTRIBUTORY PENSIONS 259

...economically unscientific . . . . actuarially unsound, and politically unjust .... Even if [the contributor] paid his social service contributions regularly every year, he would still not be eligible for a pension [because of the means test]. (Australia 1945:153)

When post-war conservative Australian Prime Minister Menzies subsequently promised to provide a social insurance blueprint for the election in 1952, he was soon forced to break his promise because of dissatisfaction within the electorate and concern with high inflation. He publicly renounced social insurance in the 1954 election, ending the commitment of conservative parties to the idea. The Labor Party had traditionally opposed the idea of social insurance on equity grounds as expressed by Seddon. Thus, somewhat against the odds, a flat rate, means tested system financed out of general revenue was begun and has continued in Australia right through this century.

In order to finance the universalisation of benefits for those aged more than 65 years, in 1939 New Zealand imposed a Social Security tax of 7.5 percent on all income as an accounting device. As Ashton and St. John (1988:22) point out, '...although this was paid into a separate fund it was not intended that the social security system should be regarded as a contributory insurance system...'. The Social Security Fund was abolished in 1964 and the tax was absorbed into general tax scales in 1969. This accounting device reappeared in the 1989 New Zealand budget at the same historical rate of 7.5 percent. In practice, the scheme remains financed out of general revenue rather than by specific contributions.

In Australia there was a further consideration of the idea of a universal earnings related National Superannuation Scheme to replace the age pension under the Labor government in the early part of the 1970s (Hancock Committee of Inquiry 1977). A change to conservative govemment, however, ensured that this proposal was presented to an unsympathetic government. The return of a Labor government in the 1980s brought with it a promise to implement the National Superannuation proposals of the early 1970s. This was not fulfilled, except to encourage the Australian Council of Trade Unions to pursue a proposal to develop more extensive private occupational superannuation (McCallum and Shaver 1986). This support continued in the 1989 Australian Budget with a new proposal for the development of occupational superannua- tion.

In 1972 the New Zealand Royal Commission on Social Security specifically rejected an earnings related scheme, again reiterating the purpose of the noncontributory mechanism:

...The community's first responsibility for income maintenance is to give benefits which will enable its dependent sections to reach an adequate standard of living. This can best be done by a system of selective flat-rate benefits and allowances. Adopting an earnings related benefit system would not help those sections of the community to whom it owes In'st responsibility .... (New Zealand 1972:181)

Despite this, in 1974 the New Zealand Labour Party passed the contributory scheme with the 1974 New Zealand Superannuation Act, which required four percent contributions each from employers and employees. There were concerns

260 JOHN MCCALLUM

about this scheme generally: in particular, the size of the fund to be accumulated and the 40-year lag before full benefits were paid. Before the scheme actually began, it was abolished by the incoming National Party government in 1976 and replaced by the more generous flat rate, noncontributory National Superannua- tion Scheme. The noncontributory principle has proved robust through different political and economic periods in Australia and New Zealand.

Means Testing

Means testing is a critical component of the efficiency of noncontributory schemes. In Hung Kong, for example, the Old Age Allowance is not means tested for persons over 70 years but the result is that scarce resources are given to many who do not need them and the basic pension remains too little to live on for those who are needy. Consequently, as this pension eligibility age is lowered to 65 years, means tests have been introduced in a limited way for persons aged 65 to 69 years. A more general means test would target scarce resources more effectively on those who need them.

In Australia, since the introduction of the age pension in 1909, there have been assessments of assets and incomes above 'free areas', i.e. the amount of income or assets one can have before the age pension is reduced. Beyond the free area there was a one-for-one reduction of the pension for income received, and more recently a one-for-two, less stringent test. In Australia the private home was excluded from consideration as an asset from 1909 and remains so to the present day. In New Zealand private homes became exempt from the means test in 1925. This special treatment of the ownership of private homes as a basic right has been stoutly defended and the politics of means testing has been one of the major sources of public conflict in Australian government policy (McCallum 1984; Shaver 1984). The lesson is that means tests need to be applied early in the development of such pension systems and retained on rational economic grounds in the face of special pleading and political pressures.

The New Zealand attitude to means testing has generally been more liberal than that of Australia, but at some cost to the economy (McCallum 1989a). From 1940, means tests were applied only between ages 60 and 64; however, the New Zealand system broke step with Australia in 1976. A simple, generous, 80 percent of the after-tax average wage was provided to couples and 48 percent to single people at age 60 years, subject only to ten years' residency in the country. This is paid out of general revenue and adjusted annually with increases in average wages. From October 1988 a tax surcharge of 20 cents in the dollar was imposed on other income received above minimum rates. This effectively acts as a means test; however, only ten percent of people 60 years and over lose all their National Superannuation through the surcharge and, in the year to March 1987, 77 percent received the full payment (Ashton and St John 1988).

The important point to note is that the general revenue funded, flat rate retirement income schemes in Australia and New Zealand have not continued into the 1990s simply because of inertia. The contributory, earnings related

REHABILITATING NONCONTRIBUTORY PENSIONS 261

alternatives have been seriously considered and rejected at a number of points in their 80-year history. The key factors in favour of retention have been the relatively low cost to the public and efficiency in dealing with the target of poverty in old age without making the situation of poor families worse by compulsory contributions. The other major component of retirement income, private or occupational superannuation, is relatively less important in New Zealand than in Australia, where it has been promoted to supplement the minimum means tested age pension. It is the responsibility of private savers and their employers to contribute to this eamings related, nongovemment retirement income system.

Occupational Superannuation

The term 'occupational superannuation' is used here to refer to what some readers may know as 'occupational pensions' or 'private pensions' because of the need to clearly distinguish these from Australian 'age pensions'. This is a system of private saving for retirement which has a longer history than that of public involvement in income support. The provision of retirement benefits through contributions by employers and employees in Australia dates from 1842 with a scheme in the Bank of Australasia. This was very early in modem Australian history, as the first white settlement was established in 1788, only 54 years before. Like their European models, Australian occupational superannua- tion schemes began in banks, Life Offices, government departments and public utilities such as the Australian Gas Light Company (McCallum 1990). They were very much the preserve of the male, highly educated or well-born company worker. These schemes became the top tier in the new system after the old age pension was introduced in 1909. Private saving was necessary to ensure replacement of earnings in retirement above the basic minimum income provided by the new age pension. The Australian noncontributory pension became coupled with strong incentives for saving encouraged by tax conces- sions.

In New Zealand schemes were primarily developed for public employees, who were all covered after 1910. No specific tax measures were applied; however, in 1915 personal contributions to funds were tax deductible within specified limits. Income derived from superannuation funds became exempt from tax in 1916. Employer contributions became tax deductible in 1921, subject to government approval of the scheme. No penalties were incurred for refunds prior to retirement. This coverage was challenged by the reforms of the 1940s but grew rapidly again in the 1960s. In 1988 only five percent of households with head 60 years and over received benefits as regular payment. Others may have received lump sums at retirement. The virtue of private saving for retirement is thus rewarded by tax breaks or 'fiscal welfare'. This policy has not been without political difficulties in Australia.

In Australia income taxation was imposed in 1915, but income contributed by employers to superannuation schemes for employees was exempted, and there

262 JOHN MCCALLUM

was a concessional deduction of AS100 for individual contributions. This unlimited deduction of employer contributions was clearly open to abuse, but there was little public interest in such matters until after World War II. Minor limitations were imposed on employer contributions in 1944, while in 1952 income of self-employed persons was allowed the same exemptions. Conse- quently, the early development of schemes was virtually devoid of government control or interest.

In response to growing concerns in Australia, the Ligertwood Committee was set up in 1959, and two years later it reported widespread abuse of superannua- tion concessions. Constraints on funds, such as holding a proportion of Public Sector bonds, subsequently were imposed as conditions for approval for concessions. More control was achieved in 1964-5 when the discretions for approval of tax exempt status of funds were vested in the Commissioner for Taxation. Even this development, however, demonstrated the lack of policy interest of the Commonwealth government beyond regulating abuses of tax concessions.

In the context of National Superannuation considerations, occupational superannuation schemes were critically reviewed by the Australian Hancock Committee of Inquiry (1977). The problems identified with the system were multiple:

- poor coverage of the work force, namely just over one-third; - poor performance of investments of funds; - lack of portability of entitlements; - lack of vesting standards for contributions; - use of funds for internal investments and defense against takeovers; - failure to preserve accumulated funds for use in retirement because of lack

of portability and general payment of entitlements as lump sums; - and elements of discrimination, e.g. against women relative to men. While the committee recommended as a solution a contributory system such

as the short-lived New Zealand insurance scheme, nothing came of this because of a change in government and the arrival of the oil price shock recession. The problems have been progressively addressed during the 1980s.

The contribution of private pensions to retirement income is significant, but so is the tax concession to such saving. The Australian Treasury estimates that the total value of tax concessions for occupational superannuation in tax year 1984-5 was A$22,610 million, which was between 35 and 40 percent of total superannuation contributions for that year. Other authors recognize the taxation of benefits and reduce that figure, and still others increase it to take into account unfunded schemes and interest costs associated with tax deferral.

All tax concessions were removed in New Zealand in December 1987 and those in Australia were modified in May 1988. These concessions are inevitably enjoyed by higher income earners rather than lower income earners. Only 3.1 percent of Australian employees earning under A$120 per week were covered by superannuation schemes, compared to 71.7 percent of those earning A$520 per week or more, which indicates a strong earnings related pattern in this

REHABILITATING NONCONTRIBUTORY PENSIONS 263

scheme. As the Australian Council of Trade Unions evaluated the situation:

...There is great inequity in the current availability of, and participation in, occupa- tional superannuation. This implies not only great inequalities in terms of the living standards of retirees, but also in terms of the way in which the community's tax burden is shared. (Weaven 1986:110)

This inequity is reduced by the means tested, flat rate age pension and by the high rates of private home ownership in Australia and New Zealand.

Home Owne~h~

The nearly complete dependence of the Australian and New Zealand elderly on the flat rate age pension may not have survived as an acceptable system without the background of high rates of home ownership. In Australia nearly 80 percent of heads of households aged 65 or more in private dwellings own their own homes or are in low rent public housing, and nearly another ten percent are provided with rent free accommodation (Table I). Finally ten percent are in non- private dwellings. Of these, around six percent are in residential care, a rate exceeded only by the United States and Denmark (Rossiter 1985). Compared to Britain and the US, Australia and New Zealand have higher rates of persons over age 65 who are outfight owners or mortgagees and lower rates of private tenants. Britain, however, has by far the highest rates of government housing (Kendig 1984). Consequently, some assumptions about ownership of other resources underlie minimum support schemes.

The needs of Australia's elderly are also met by a complex set of local government and community provisions, collectively called 'fringe benefits', that are not available in New Zealand. The community provides a whole range of discounts on goods and services to holders of Pensioner Health Benefit cards. These range from substantial rate rebates (taxes on land and housing), free or subsidised local and long distance travel, cheap animal licences, cheap rates at hairdressers and retail shops such as butchers and fishmongers, and so on. Babbage (1984) estimates that these add five to ten percent to the value of the Australian age pension as a proportion of average weekly earnings. The value has considerable variability because of the availability of different provisions in geographical regions and because older consumers have different tastes.

Earnings from Work

In Australia and New Zealand the labor force participation rate of men aged 65 and over is around nine percent and of women about two percent. As can be seen in Table H, these rates have declined markedly during the 1970s in more developed countries, particularly for men aged 60-64 years. There has been a lively debate about the declines in male rates of workforce participation in Australia. Stficker and Sheehan (1981:132) proposed that declines were 'hidden

264 JOHN MCCALLUM

TABLE I Housing tenure of income units a in private dwellings

by age of head, Australia 1982 (percentages)

Housing tenure All heads Heads aged 65+ (%) (%)

Owner 30.8 68.2 Purchaser 33.5 5.1 Tenant of:

housing authority 4.7 6.0 private landlord 19.1 5.6 someone in dwelling 3.5 3.9 other b 2.9 2.3

Rent free 5.6 8.9

Number ('000) 5738.2 c 1044.4

a Income units are defined as either i) couples with children, ii) couples with no dependent children, iii) single parents with dependent children, or iv) single people. Income unit heads are either the individual or the male parmer of a married or de facto couple. b Tenants paying rent to relatives not in the dwelling or to employers who rent properties on a non-commercial basis are coded as "other". ¢ This excludes income units who were the non-dependent children of the household head, for which the survey did not gather data. Source: Australian Bureau of Statistics (1985).

unemployment ' , defined as " . . . the number of persons not now in the labour [sic] force who would be in the labour [sic] force if the conditions characteristic of full employment had continued. . ." . Merri lees (1983:263) proposed an alterna- tive explanation to this state of the labor market argument, namely " . . . the increased financial attractiveness of social security benef i ts . . . " and " . . . the voluntary character of much of the recent exodus. . ." . Unfortunately the voluntary/involuntary distinction is a complex one and the factors behind labor force participation rate declines are multiple. Less developed countries are unlikely to have the resources to sustain similarly low rates of participation o f older workers.

The major change in pensions eligibil i ty came from a temporary upsurge in the numbers of Wor ld War II veterans reaching retirement ages who were eligible for pensions five years earlier than other older Australians. Hughes (1984) identified another factor to be added to declining labor market conditions and improved pensions, namely improved wealth accumulation in the post World War II years, which lead to a voluntary preference for early retirement. The Bureau of Labour Market Research in Austral ia (1983) and Merrilees (1986) showed all three factors at work: improved pensions, worsening un- employment and improved wealth. Similar factors would be expected to operate with the process o f economic development in developed countries.

The question remains whether there are large numbers of older Australians

REHABILITATING NONCONTRIBUTORY PENSIONS 265

TABLE II Labour force participation rates (percentages) of older men

Aged 55-59 years Aged 60--64 years

1970 1981 1970 1981

Australia ~ 88.4 81.3 75.6 53.1 New Zealand ~ 92.1 88.9 69.2 46.7

Austria b 88.4 85.7 47.7 29.8 Belgium 82.3 70.5 63.8 34.1 France 82.5 79.8 65.2 42.4 Germany 89.2 81.9 74.7 44.5 Great Britain a 95.3 91.1 86.6 72.0 Netherlands a 86.9 71.1 73.9 48.4 Sweden 90.8 87.8 79.5 68.2 U.S.A. 89.5 81.3 75.0 58.7

a 1971 instead of 1970. b 50--59 years instead of 55-59 years. Source: Casey (1986), Australian Censures of Population and Housing, and Ashton and St John (1988).

who really want to work but are prevented from doing so. Special surveys o f persons not in the labor force in Austral ia show a low rate of three to four percent o f men and one to two percent of women aged 60 and over who want to work but are currently not in the work force. In contrast, surveys show a consistent 40 percent of Australians aged 60 years and over who would have preferred to work longer than they did (McCallum 1989b). Why is it that around a third of Australians (removing those who were ill) would have l iked to have worked longer than they did while only a few percent actually wish to work at any one time? The most compell ing reason is that effective marginal tax rates (the combinat ion of tax and means tests) can be as much as 70 cents in the dollar, and provide severe disincentives to earning income (Bureau of Labour Market Research 1983). The desire to work longer therefore does not convert into an actuality of wanting to work, because the realities o f the situation intrude on older persons ' calculations. It is a relevant observation for less developed countries seeking to restructure their work forces that this can be used as a mechanism for l imiting employment options of older workers.

Whi le the age pension provides a min imum satisfactory standard of l iving for older Australians, it provides disincentives for them to supplement that income through work. A similar situation exists in New Zealand, where a more generous pension becomes available to all at age 60. This structure of disincentives could be reversed by policies cutting rates of pension, extending eligibil i ty ages and making means tests more stringent.

266 JOHN MCCALLUM

Wealth

The existing studies of wealth in Australia are limited by the scarcity of reliable data and by deficiencies of technique (Piggott 1984). Ashton and St. John (1988) report that even less information is available for New Zealand. Studies contain limited information about the elderly, mostly in the context of life cycle pattems of wealth holdings. Podder (1978), for example, reports that the best predictors of wealth were high status occupation and older age of household heads. Similarly, Piggott (1984) and Nevile and Warren (1984) also show the over- representation of older persons in top wealth groups.

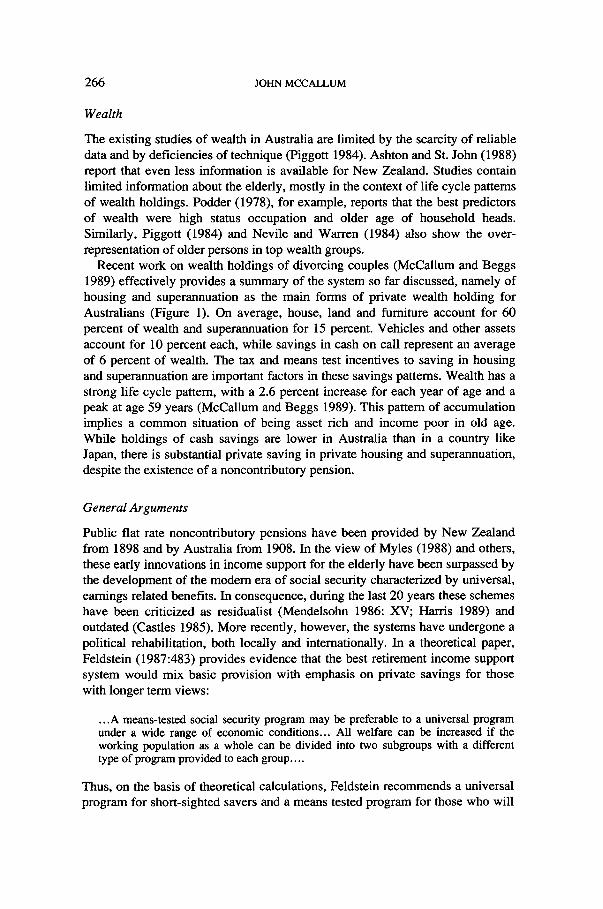

Recent work on wealth holdings of divorcing couples (McCallum and Beggs 1989) effectively provides a summary of the system so far discussed, namely of housing and superannuation as the main forms of private wealth holding for Australians (Figure 1). On average, house, land and furniture account for 60 percent of wealth and superannuation for 15 percent. Vehicles and other assets account for 10 percent each, while savings in cash on call represent an average of 6 percent of wealth. The tax and means test incentives to saving in housing and superannuation are important factors in these savings patterns. Wealth has a strong life cycle pattern, with a 2.6 percent increase for each year of age and a peak at age 59 years (McCallum and Beggs 1989). This pattern of accumulation implies a common situation of being asset rich and income poor in old age. While holdings of cash savings are lower in Australia than in a country like Japan, there is substantial private saving in private housing and superannuation, despite the existence of a noncontributory pension.

General Arguments

Public flat rate noncontributory pensions have been provided by New Zealand from 1898 and by Australia from 1908. In the view of Myles (1988) and others, these early innovations in income support for the elderly have been surpassed by the development of the modem era of social security characterized by universal, earnings related benefits. In consequence, during the last 20 years these schemes have been criticized as residualist (Mendelsohn 1986: XV; Harris 1989) and outdated (Castles 1985). More recently, however, the systems have undergone a political rehabilitation, both locally and internationally. In a theoretical paper, Feldstein (1987:483) provides evidence that the best retirement income support system would mix basic provision with emphasis on private savings for those with longer term views:

...A means-tested social security program may be preferable to a universal program under a wide range of economic conditions... All welfare can be increased if the working population as a whole can be divided into two subgroups with a different type of program provided to each group ....

Thus, on the basis of theoretical calculations, Feldstein recommends a universal program for short-sighted savers and a means tested program for those who will

R E H A B I L I T A T I N G N O N C O N T R I B U T O R Y P E N S I O N S 267

70"

60 ¸

50 ¸

=~40 o

2 3 0 . D.

20

1 0

0 24

. .- Superannuation

• - Other assets

- - Vehicles

--, Cash holdings

- - Businesses

, j , "

- ~ . . ~ . . ~ . . ~ . ~ , w -=1¢: . . . . ~ . ~ ~ . . . . ~ "

- - ' . ; : . . . . . . t

I ', ~ ~ ', I I I I I I I I I t ~ ) : ~ ~ : : 2 8 3 2 3 6 4 0 4 4 4 8 5 2 5 6 6 0 6 4 6 8

A g e in y e a r s

Fig. 1. Proportions of net wealth of Australians by age and type of wealth. Source: McCallum and Beggs (1989).

voluntarily save. Through a more political calculus, Australian and New Zealand governments have independently reached the same conclusion.

In Australia, McAllister, Ingles and Tune (1981) and Gruen (1989) have defended the effectiveness of the system in dealing with need, and praise its economic sustainability. The OECD (1988) points out the ability of flat rate schemes to reduce poverty and prevent cost problems resulting from population aging, maturation of systems and variable economic performance. In Australia the Social Security Review produced a substantial investigation of the retirement income system (Foster 1988) and the 1988 New Zealand Royal Commission on Social Policy (New Zealand 1988) was similarly comprehensive in its considera- tion of retirement income. So, after extensive research and discussion, the 1989 budgets in both Australia and New Zealand have substantially retained these 'archaic' systems. More critical questions, therefore, need to be asked about the earnings related contributory schemes found in most developed countries.

268 JOHN MCCALLUM

THE IMPACT ON WELL-BEING

Definition

Well-being in old age is multifaceted, including levels of satisfied 'needs' and general goals and values of the society. As even the most cursory observation of different cultures demonstrates, 'needs' are socially determined and differ markedly in their expression across cultures. Bradshaw (1972) discusses four different senses of 'social need', namely normative need, or need as defined by authorities, experts and opinion leaders; felt need, or need as experienced by the population concerned and measured by social surveys; expressed need, or felt need turned into action in the form of demand for service; and comparative need, which is inferred from an analysis of demographic characteristics and levels of service provision. Bradshaw also points out that one form of need does not necessarily imply another, with the exception of expressed need deriving from felt need.

The needs of the elderly are both complex and culturally specific. Different sub-groups of the population will express different needs for service provision that will not necessarily be matched by normative need statements made by authorities. In consequence, there are difficult ethical and practical questions about setting priorities for different sections of the population, such as geographi- cal communities, ethnic or racial groups, income groups and age groups. Net contributions of age groups to government also vary across the life cycle because of different age cohort sizes. Intergenerational equity therefore becomes a major issue. The general values embodied in the system encompass all these complexities.

Two important values underlying the Australian retirement income system are poverty alleviation and income maintenance (Podger 1983). In Australia the age pension is thought to deal with poverty alleviation and occupational superannua- tion with income maintenance. These values emerged from Australian welfare and minimum wage legislation of the early part of this century. Minimum wages were established in 1907 and based on an assessment of the needs of a male worker, spouse and two children. When a female basic wage rate was es- tablished in 1912, it was set at 60 percent of the male rate because children were assumed to be dependent on the male bread winner. Minimum pension rates were fixed relative to these and to trial and error figures derived from the experience of rates in New Zealand and the Australian states. There was no gender difference set in pension rates because of the assumed absence of children. This has proved to be an important feature of the system for women who, because of less time in the workforce, get less out of contributory schemes than do men.

The generosity of the basic rate is the first indicator of the well-being generated by the pension. By the simple mechanism of raising the basic rate, the resources available to the poorest elderly can be increased. The 1989 Australian budget proposed to raise the single pension by about a percentage point to 25

REHABILITATING NONCONTRIBUTORY PENSIONS 269

percent of average weekly earnings. The 1989 New Zealand budget alternatively proposed to reduce benefits for couples from about 80 percent of average weekly wages to a range of 65 to 72.5 percent after tax, of which the single rate would be half. This reduction could be achieved politically because the New Zealand actual rate was about double that of Australia. Comparisons of economic well-being cannot be confined merely to the generosity of the pension. The system also can be evaluated against its stated general goals.

Poverty

One critical indicator of well-being is the number of households below a minimum level of income. It used to be a consistent finding of research in Australia that old age was an important risk factor for poverty by the standard of equivalence scales such as those developed by Henderson (See Manning 1982; Whiteford 1983). The Australian Poverty Inquiry of 1975, for example, using data collected in 1972-3, found that about a quarter of households headed by aged Australians fell below the poverty line, compared to ten percent of all adult income units. After housing costs were taken into account, however, fewer than ten percent of elderly households fell below the poverty line because of their high rates of outright home ownership. Using data collected in 1981-2, Brad- bury, Rossiter and Vipond (1986) found that age was no longer a major factor in predicting poverty after taking housing costs into account. They warn against over-optimism, however, because the group within 120 percent of the poverty line is dominated by elderly households. Further research by Gallagher (1985) indicates that major causes of poverty include unemployment and being out of the work force because of single parenthood. Those elderly households below poverty lines are most likely to be the small numbers of private renters now targeted by supplementary rental assistance in Australia.

The OECD (1988) shows a 92 percent reduction in its poverty measure for Australian elderly as a result of age pension transfer payments. It is further argued that increases in the rate of pensions can quickly lift the majority of age pensioners to regions just above the official poverty lines. Poverty is less of an issue in New Zealand with its higher fiat rate of pension. Snively (1988) shows that households with two persons receiving National Superannuation have an average adjusted yearly income of NZ$21,756, which is below the national average of NZ$24,423 but above both two-adult households with children and single parent households. This confirms the picture of the overall effectiveness of the flat rate age pension in alleviating poverty among the aged.

Income Replacement

Australian private sector retirees have actual replacement ratios (income relative to preretirement earnings) in the range 17 to 40 percent; in comparison, those with the highest incomes have the best replacement ratios (Table III). Using Australian data, Borowski, Schulz and Whiteford (1987) argue that a replace-

270 JOHN MCCALLUM

TABLE III Income replacement provided by Australian retirement benefits 1981

Pre-retirement Average Income Percentage salary ($) retirement replacement of

benefits ($) rate (%) retirees

1-13,499 19,897 16.6 38.6 13,500-19,999 50,875 30.4 35.1 20,000-27,499 100,276 42.2 14.7 27,500-39,999 134,275 40.1 7.7 40,000 and over 177,446 39.4 3.9

Total 57,503 37.3 100

Source: Donald (1984:46).

ment ratio of around 70 percent is required to maintain a preretirement lifestyle. Those with higher incomes need to add more to the age pension base than those with lower incomes. For example, the single age pension is about half the Australian minimum wage: 35 percent of a c leaner 's preretirement earnings but only 20 percent of a t rucker 's earnings. Arguments for replacement ratios in excess of those currently achieved are beginning to get some public airing.

I f the statements of normative need were correlated with expressed need, we would expect to find high levels of expressed dissatisfaction with retirement income adequacy. In fact, only four percent of respondents 60 years and over to a national survey claimed to have inadequate income. These rates were higher - around 25 percent - for some Southem European migrant groups (McCallum and Mackiewicz 1986:118). Furthermore, in a series of search conferences run throughout the state of New South Wales (Will iams 1984) at a t ime when debates about means testing of assets had a high profile, there was a surprisingly low level of expressed dissatisfaction with retirement income arrangements. Issues about transport, medical and health matters, housing and accommodation, loneliness, quality of life and so on are typically regarded as more important problem areas for older people than income and finances.

As in eamings related systems, the winners are those with better education and, consequently, higher paid jobs. As in Feldste in 's (1987) ideal model, these people depend only on private savings for retirement income; however, some income differences are flattened out at the bottom and middle of the income distribution. As the Brookings Institution study of the Australian Welfare system (Caves and Krause 1984:362) observed, in comparison to the US insurance-type system:

...the Australian system is probably more generous to the aged workers who have had low earnings than is the US system. In contrast the Australian system gives far less to those at the middle-income levels than do US and other social insurance systems. The average US social security recipient receives more, and those who had above average earnings receive much more than they would receive from age pensions in Australia...

REHABILITATING NONCONTRIBUTORY PENSIONS 271

First generation migrants from southern European countries such as Greece and Italy also tend to receive less income than would be expected given their education (McCallum 1990); however, the gender gap is virtually removed by the fiat rate benefit and means tests. This latter feature of the performance of this system has ensured the support of the women's movement for the age pension system. The gains are most evident in New Zealand, where regardless of her work history, a woman will receive in her own right 40 percent of average earnings from age 60 for the rest of her life. Both in dealing with poverty, which is perennial, and in answering newly voiced demands of women that they be treated as individuals, the fiat rate pensions have proven themselves effective and efficient as a public sector policy instrument.

CONCLUSION

The flat rate, noncontributory means tested pensions in Australia and New Zealand effectively deal with poverty and basic needs but constrain retirement income to a moderate level. This system is supplemented by high rates of home ownership and, in Australia, by occupational superannuation. The system consequently offers protection for the poor as well as incentives for the rich to save for their old age. The Australian and New Zealand flat rate, targeted noncontributory pensions are simple and effective in dealing with poverty in old age. Such schemes do not suffer problems of scheme maturation occurring along with population aging. On the negative side they do not of themselves maintain standards of living into retirement; however, they can be supported by private pensions, health insurance and housing policies to produce satisfactory support in old age.

The relative stability of the flat rate systems through different stages of development with different coverage of the population of older people is another positive feature of the flat rate system. The problems of the insurance type system in a less developed country are well demonstrated by the case of the Philippines. Despite the existence of such funds since the 1930s, only 8 percent of the elderly population is covered. A Chinese noncontributory, in kind system like the five guarantees would be a much more effective system of providing for the rural elderly who constitute a majority of the population. Even within the small group covered by the pension schemes the tensions with the welfare imperative to provide flat rate, minimum income are clear. In both the govern- ment workers and private schemes the minimum pension was increased to P400 (US$19.20) in 1989. About 37 percent of government retirees received the minimum as did a third of private sector retirees (Domingo 1989). The necessity of providing an adequate minimum pension constrains the capacity to pay true earnings related pensions. There is currently pressure to increase the minimum to P500 which will change the profile of payouts to be more like a flat rate scheme. The question posed by the noncontributory model outlined here is: Would not a less developed country be better off by concentrating its public monies on those most in need by providing noncontributory, means tested

272 JOHN MCCALLUM

pensions either in money or in kind from general revenue? The experience of Australia and New Zealand supports a positive answer to this question.

One concern has been the expected impact on private savings when the existence of noncontributory public pensions becomes part of families' secure expectations. As Feldstein's (1987) model shows, the effect of the means test is to push people with higher expectations of retirement income into private savings. Thus we find that after houses, holdings of superannuation assets are the second major form of personal wealth held by Australians. The current incentives in contributory schemes like those in the Philippines are to encourage contributors and employees to engage in minimum compliance to achieve the basic payout. The incentive of the dual system of Feldstein would be to save to provide for consumption above some minimum survival standard e.g. the Chinese five guarantees. The existence of that secure minimum provides an incentive to reduce family size since children are no longer so critical to survival in old age. So effective income support can be part of a successful development strategy to reduce high birth rates (Nugent and Gillaspy 1983).

Despite its minority representation among schemes around the world (OECD 1988), the noncontributory retirement income scheme offers a useful set of strategies for dealing with income support in old age. It was produced by historical forces that may match those in some less developed countries in the present day. In particular, it solves the problem of contributions in poor countries and efficiently targets basic needs through use of means tests. The coverage of a population can be tailored to resources available in a country by weakening or strengthening these means tests, and over time, a more comprehen- sive coverage can be built up from a basic provision as a country develops. This is an old idea, but one with a respectable history in Australia and New Zealand and worthy of consideration by less developed countries.

ACKNOWLEDGEMENTS

Peggy Koopman-Boyden assisted with the collection of historical material for New Zealand. Mary Jo Cosover Martin and Stefanie Pearce provided comments on the text and Elizabeth Freeman prepared the tables and figure.

REFERENCES

Ashton, T. and S. St. John 1988 Superannuation in New Zealand: Averting the Crisis. Wellington: Victoria University Institute of Policy Studies.

Australia 1945 Commonwealth Parliamentary Debates. Volume 184(6). Canberra: Australian Government Printer.

Australian Bureau of Statistics 1985 Australian Income and Housing Survey 1981-2. [machine readable data file] Canberra: Social Science Data Archives.

Babbage, S. 1984 The Range, Cost and Value of Fringe Benefits. Canberra: Social Welfare Policy Secretariat.

Binstock, R.H. 1986 Drawing Cross-Cultural Implications for Policy. Some Caveats. Journal of Cross-Cultural Gerontology 1:331-338.

REHABILITATING NONCONTRIBUTORY PENSIONS 273

Borowski, A., J.H. Schulz, and P. Whiteford 1987 Providing Adequate Retirement Income: What Role Occupational Superannuation? Australian Journal on Ageing 6(1):3-13.

Bradbury, B, C. Rossiter, and J. Vipond 1986 Poverty Before and After Paying for Housing. Sydney: Social Welfare Research Centre Reports and Proceedings No. 56.

Bradshaw, J. 1972 The Concept of Social Need. New Society 19(496):640--643. Bulatao, R.A. 1979 On the Nature of the Transition Value of Children. Honolulu: Papers

of the East-West Population Institute. Bureau of Labour Market Research 1983 Retired, Unemployed or at Risk: Changes in the

Australian Labour Market for Older Workers, Research Report No. 4. Canberra: Australian Government Publishing Service.

Casey, B. 1986 Recent Trends in Retirement Income Policy and Practice in Europe and USA. In The Finance of Old Age. R. Mendelsohn, ed. Canberra: Centre for Research on Federal Financial Relations.

Castles, F.G. 1985 The Working Class and Welfare. Sydney: Alien and Unwin. Caves, R.E. and L.B. Krause, eds. 1984 The Australian Economy: A View from the

North. Sydney: Allen and Unwin. Dixon, J. 1978/9 The Evolution of Australia's Social Security System, 1890-1972: The

Social Insurance Debate. Social Security Quarterly, Summer 5(2): 1-10. Domingo, L. 1989 Work, Retirement and Income Security: A View from the Philippines.

Paper prepared for the XIV International Congress of Gerontology, Acapulco, Mexico.

Donald, O. 1984 Government Support of Retirement Incomes in Australia. Canberra: Department of Social Security.

Feldstein, M.S. 1987 Should Social Security Benefits Be Means Tested? Journal of Political Economy 95(3):468--484.

Foster, C. 1988 Towards a National Retirement Incomes Policy. Canberra: Social Security Review Issues Paper No. 6.

Gallagher, P. 1985 Targeting Welfare Expenditures on the Poor. Presented at NSW Council of Social Service, 'Welfare Services for the Most Needy' Public Meeting, Sydney, 25 June.

Gruen, F.H. 1989 Australia's Welfare State: Rearguard or Avant Garde? Canberra: Centre for Economic Policy Research Paper No. 212, Australian National University.

(Hancock) National Superannuation Committee of Inquiry 1977 Occupational Superan- nuation in Australia. Final Report of the National Superannuation Committee of Inquiry: Part Two. Canberra: Australian Government Publishing Service.

Harris, P. 1989 Child Poverty, Inequality and Social Justice. Melbourne: Brotherhood of St. Laurence.

Hughes, B. 1984 Labour Force Participation: What Are the Issues? In Labour Force Participation in Australia: The Proceedings of a Conference. A.J. Kaspura, ed. Bureau of Labour Market Research Monograph Series No. 1. Canberra: Australian Govern- ment Publishing Service.

Kendig, H.L. 1984 Housing Tenure and Generational Equity. Ageing and Society 4(4):249-272.

Manning, I. 1982 The Henderson Poverty Line in Review. Social Security Journal June: 1-13.

McAllister, C., D. Ingles, and D. Tune 1981 General Revenue Financing of Social Security: The Australian Minimum Income Support System. Social Security Journal (December): 24-38.

McCallum, J. 1984 The Assets Test and the Needy. Australian Journal of Social Issues 19(3): 218-233.

McCallum, J. 1989a Legislation and the Elderly in Asia and the Pacific. In ESCAP, Issues in the Integration of the Ageing in Development. Bangkok: The United Nations.

274 JOHN MCCALLUM

McCallum, J. 1989b Technology and Social Change in the Ageing Lifecourse. In Ageing and Technology. R.B. Lefroy and R.W. Warne, eds. Parkville: Australian Association of Gerontology.

McCallum, J. 1990 Winners and Losers in the Australian Retirement Income System. In Grey Policy: Australian Policies for an Ageing Society. H.L. Kendig and J. McCal- lum. Sydney: Allen and Unwin.

McCallum, J. and J. Beggs 1989 New Pieces of the Wealth Puzzle. Australian Society July: 39---40.

McCallum, J. and G. Mackiewicz 1986 Work, Retirement and Income. In Australian Institute of Multicultural Affairs. Community and Institutional Care for Aged Migrants in Australia. Melbourne: Australian Institute of Multicultural Affairs.

McCallum, J. and S. Shaver 1986 Industry Superannuation: A Great Leap Forward? Social Welfare Impact 16(6): 2-8.

Mendelsohn, R., ed. 1986 Finance of Old Age. Canberra: Centre for Research on Federal Financial Relations.

Merrilees, W.J. 1983 Pension Benefits and the Decline in Elderly Male Labour Force Participation. Economic Record 29(166):260-270.

Merrilees, W.J. 1986 Economic Determinants of Retirement. In The Finance of Old Age. R. Mendelsohn, ed. Canberra: Centre for Research on Federal Financial Relations, pp. 203-221.

Myles, J. 1988 Postwar Capitalism and the Extension of Social Security into a Retirement Wage. In The Politics of Social Policy in the United States. M. Weir, A.S. Orloff and T. Skocpol, eds. Princeton, New Jersey: Princeton University Press.

Nevile, J.W. and N.A. Warren 1984 How Much Do We Know About Wealth Distribution in Australia? The Australian Economic Review 4th Quarterly:23-33.

New Zealand 1897 New Zealand Parliamentary Debates, 18 November. New Zealand 1972 Royal Commission on Social Security. Wellington: Government

Printer. New Zealand 1988 Royal Commission on Social Policy. Wellington: Government

Printer. Nugent, J.B. and R.T. Gillaspy 1983 Old Age Pensions and Fertility in Rural Areas of

Less Developed Countries: Some Evidence from Mexico. Economic Development and Change 31:809-829.

OECD 1988 Reforming Public Pensions. Paris: Social Policy Studies No. 5, OECD. Piggott, J 1984 The Distribution of Wealth in Australia: A Survey. Economic Record

September:252-265. Podder, N. 1978 The Economic Circumstances of the Poor. Australian Government

Commission of the Inquiry into Poverty Research Report. Canberra: Australian Government Publishing Service.

Podger, A. 1983 Choices in Retirement Income Policies. Social Security Journal (June): 15-22.

Rossiter, C. 1985 The Housing Circumstances of Australia's Elderly Population: Gender and Income Issues. Paper presented at the Sociological Association of Australia and New Zealand Conference, Brisbane.

Shaver, S. 1984 The Assets Test and the Politics of Means Testing. Australian Journal of Social Issues 19(4):300-306.

Sigit, H. 1988 A Socio-Economic Profile of the Elderly in Indonesia. Jakarta: Biro Pusat Statistik.

Snively, S. 1988 The Government Budget and Social Policy. Paper prepared for the New Zealand Royal Commission on Social Policy.

Stricker, P. and P. Sheehan 1981 Hidden Unemployment: The Australian Experience. Melbourne: Institute of Applied Economic and Social Research, University of Melbourne.

Weaven, G. 1986 Superannuation: The Great Leap Forward. In The Finance of Old Age.

REHABILITATING NONCONTRIBUTORY PENSIONS 275

R. Mendelsohn, ed. Canberra: The Centre for Research on Federal Finance Relations, pp. 107-120.

Whiteford, P. 1983 A Family's Needs: Equivalence Scales, Poverty and Social Security. Research Paper No. 27, Canberra: Department of Social Security.

Williams, P. 1984 Consulting the Aged: A Search Conference Approach. Australian Journal of Adult Education 24(3):29-39.

National Centre for Epidemiology and Population Health The Australian National University Canberra, Australia