Embed Size (px)

Citation preview

National and Texas Economic and Outlook

Dr. James P. GainesChief Economist

recenter.tamu.edu

THE CURRENT SITUATION

“The Future Just Ain’t What It Used to Be!”

Yogi Berra

National Economic Recovery still Going …

six years later!

Outlook still fairly bullish

3

Global• Europe, China, India, Russia and South America

all slowing or in recession

• Capital flight to U.S., especially U.S. government bond market, but also real estate, gold, other fixed assets

• Currency devaluations, officially or effectively, making dollar higher and our exports much lower

• Global energy market still unbalanced leading to sustained lower oil and gas prices 4

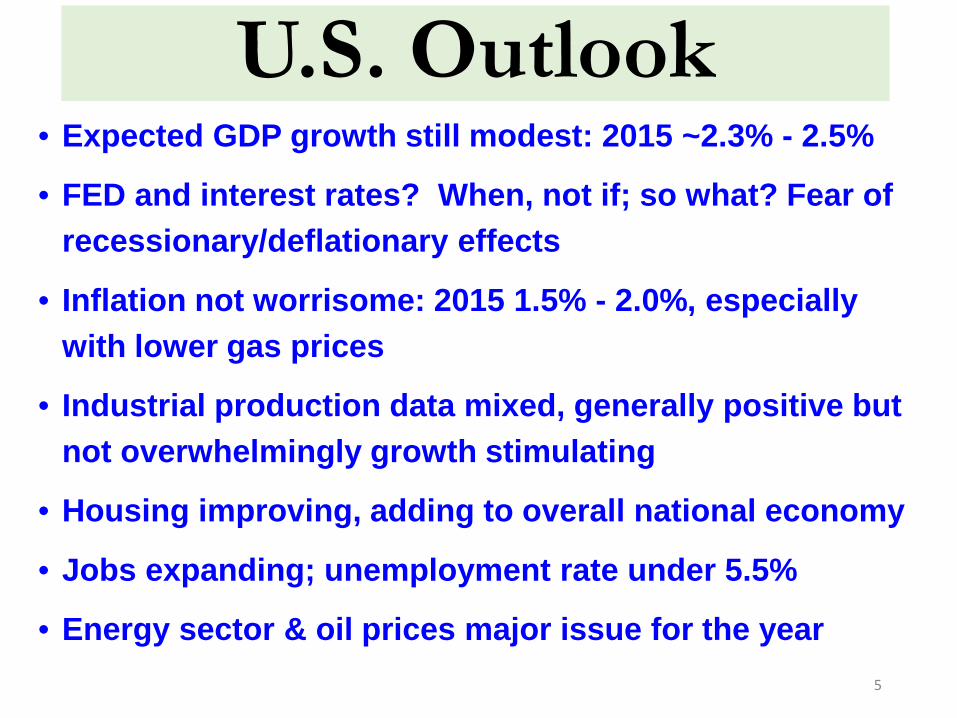

U.S. Outlook• Expected GDP growth still modest: 2015 ~2.3% - 2.5%

• FED and interest rates? When, not if; so what? Fear of recessionary/deflationary effects

• Inflation not worrisome: 2015 1.5% - 2.0%, especially with lower gas prices

• Industrial production data mixed, generally positive but not overwhelmingly growth stimulating

• Housing improving, adding to overall national economy

• Jobs expanding; unemployment rate under 5.5%

• Energy sector & oil prices major issue for the year5

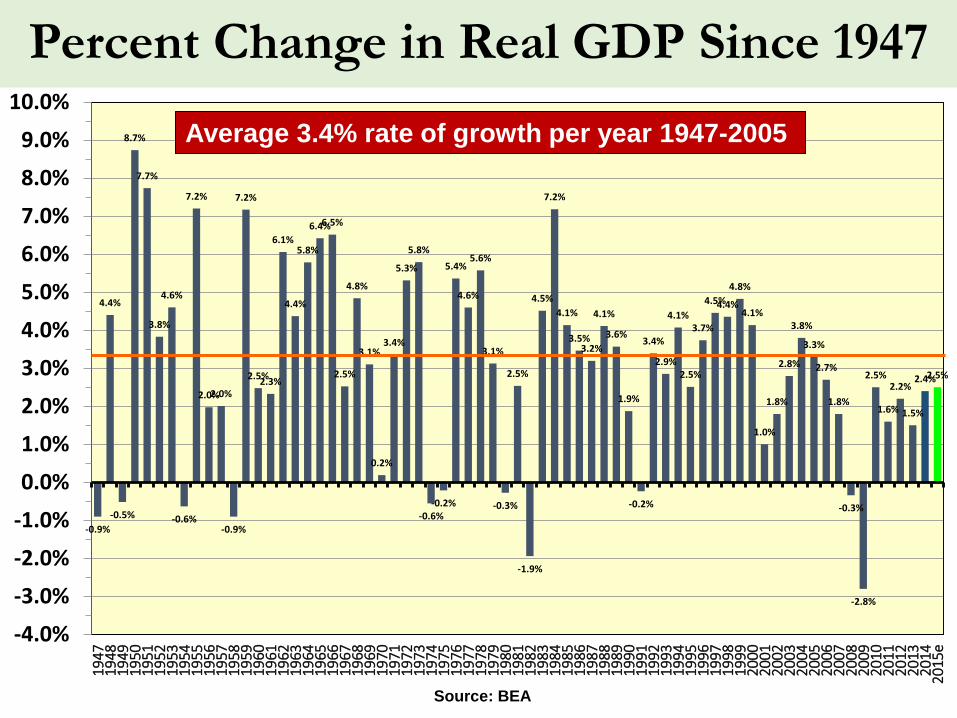

Percent Change in Real GDP Since 1947

-0.9%

4.4%

-0.5%

8.7%

7.7%

3.8%

4.6%

-0.6%

7.2%

2.0%2.0%

-0.9%

7.2%

2.5%2.3%

6.1%

4.4%

5.8%

6.4%6.5%

2.5%

4.8%

3.1%

0.2%

3.4%

5.3%

5.8%

-0.6%-0.2%

5.4%

4.6%

5.6%

3.1%

-0.3%

2.5%

-1.9%

4.5%

7.2%

4.1%

3.5%3.2%

4.1%

3.6%

1.9%

-0.2%

3.4%

2.9%

4.1%

2.5%

3.7%

4.5%4.4%

4.8%

4.1%

1.0%

1.8%

2.8%

3.8%

3.3%

2.7%

1.8%

-0.3%

-2.8%

2.5%

1.6%

2.2%

1.5%

2.4%2.5%

-4.0%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%19

4719

4819

4919

5019

5119

5219

5319

5419

5519

5619

5719

5819

5919

6019

6119

6219

6319

6419

6519

6619

6719

6819

6919

7019

7119

7219

7319

7419

7519

7619

7719

7819

7919

8019

8119

8219

8319

8419

8519

8619

8719

8819

8919

9019

9119

9219

9319

9419

9519

9619

9719

9819

9920

0020

0120

0220

0320

0420

0520

0620

0720

0820

0920

1020

1120

1220

1320

1420

15e

Source: BEA

Average 3.4% rate of growth per year 1947-2005

U.S. Jobs Finally Recovered

109,527108,427108,802

110,935

114,398

117,407119,836

122,951

126,157

129,240

132,019132,074130,628130,318

131,749134,005

136,398137,936137,170

131,233130,275

131,842134,104

136,393

139,042

90,000

100,000

110,000

120,000

130,000

140,000

150,000

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

Thou

sand

s of

Job

s

7Sources: BLS, Real Estate Center at Texas A&M University

2013 + 1.7%2014 +2.0%1999-2014 +7.6%!!

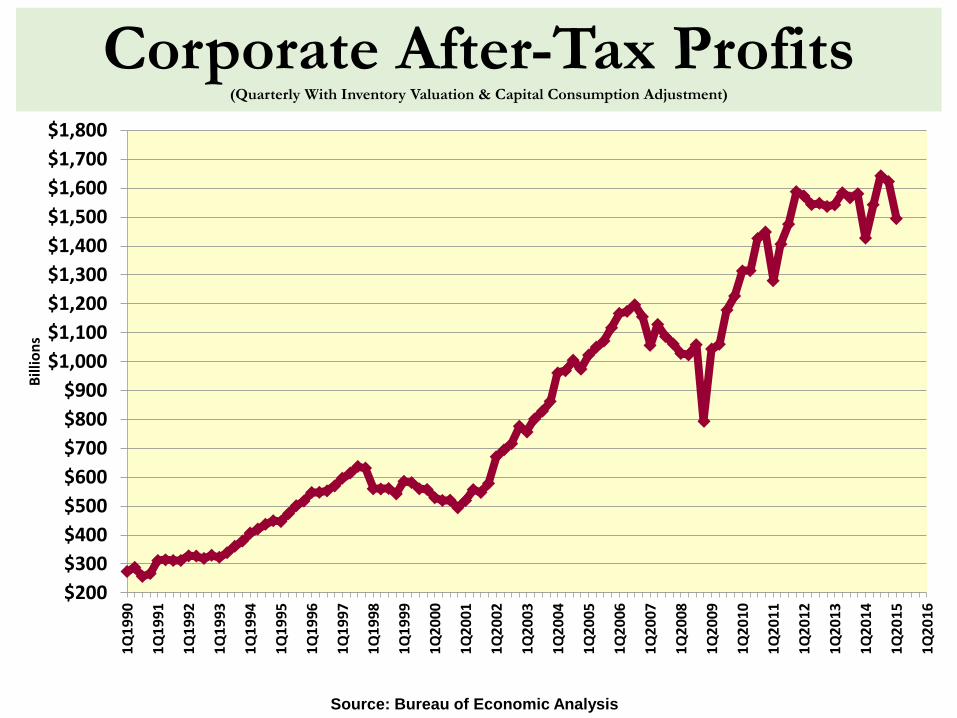

Corporate After-Tax Profits(Quarterly With Inventory Valuation & Capital Consumption Adjustment)

$200$300$400$500$600$700$800$900

$1,000$1,100$1,200$1,300$1,400$1,500$1,600$1,700$1,800

1Q19

90

1Q19

91

1Q19

92

1Q19

93

1Q19

94

1Q19

95

1Q19

96

1Q19

97

1Q19

98

1Q19

99

1Q20

00

1Q20

01

1Q20

02

1Q20

03

1Q20

04

1Q20

05

1Q20

06

1Q20

07

1Q20

08

1Q20

09

1Q20

10

1Q20

11

1Q20

12

1Q20

13

1Q20

14

1Q20

15

1Q20

16

Billi

ons

Source: Bureau of Economic Analysis

Inflation Remains Relatively Low

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%Ja

n-71

Jan-

72Ja

n-73

Jan-

74Ja

n-75

Jan-

76Ja

n-77

Jan-

78Ja

n-79

Jan-

80Ja

n-81

Jan-

82Ja

n-83

Jan-

84Ja

n-85

Jan-

86Ja

n-87

Jan-

88Ja

n-89

Jan-

90Ja

n-91

Jan-

92Ja

n-93

Jan-

94Ja

n-95

Jan-

96Ja

n-97

Jan-

98Ja

n-99

Jan-

00Ja

n-01

Jan-

02Ja

n-03

Jan-

04Ja

n-05

Jan-

06Ja

n-07

Jan-

08Ja

n-09

Jan-

10Ja

n-11

Jan-

12Ja

n-13

Jan-

14Ja

n-15

9Source: BLS, Y/Y % change in index

Consumer Price Index for All Urban Consumers: All Items

Source: The Conference Board (1985=100); Haver Analytics

Consumer Confidence Index

102030405060708090

100110120130140

Jan-

07

Jul-0

7

Jan-

08

Jul-0

8

Jan-

09

Jul-0

9

Jan-

10

Jul-1

0

Jan-

11

Jul-1

1

Jan-

12

Jul-1

2

Jan-

13

Jul-1

3

Jan-

14

Jul-1

4

Jan-

15

Jul-1

5

Jan-

16

Recession

10

U.S.

Expansion

Texas

Household Net Worth Has Rebounded Well

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

$80,000

$90,000

1Q19

801Q

1981

1Q19

821Q

1983

1Q19

841Q

1985

1Q19

861Q

1987

1Q19

881Q

1989

1Q19

901Q

1991

1Q19

921Q

1993

1Q19

941Q

1995

1Q19

961Q

1997

1Q19

981Q

1999

1Q20

001Q

2001

1Q20

021Q

2003

1Q20

041Q

2005

1Q20

061Q

2007

1Q20

081Q

2009

1Q20

101Q

2011

1Q20

121Q

2013

1Q20

14

Bill

ions

Source: Federal Reserve St. Louis

Source: Federal Reserve Board

Debt Service Payments as a Percent of Disposable Personal Income

Low

9.0

9.5

10.0

10.5

11.0

11.5

12.0

12.5

13.0

13.5

14.0

1Q19

801Q

1981

1Q19

821Q

1983

1Q19

841Q

1985

1Q19

861Q

1987

1Q19

881Q

1989

1Q19

901Q

1991

1Q19

921Q

1993

1Q19

941Q

1995

1Q19

961Q

1997

1Q19

981Q

1999

1Q20

001Q

2001

1Q20

021Q

2003

1Q20

041Q

2005

1Q20

061Q

2007

1Q20

081Q

2009

1Q20

101Q

2011

1Q20

121Q

2013

1Q20

141Q

2015

Perc

ent o

f Dis

posa

ble

Inco

me

12

Texas Has Been the “Bell weather” State for the Past Several Years, But

There Are Clouds on the Horizon

13

Texas Outlook

14

Energy, High tech and business services fueling job growth that is expected to stay relatively strong

Downside risks:o national (global) recession, even then Texas may

do better than most other states IF energy is strong

o Oil prices and energy sector Population expansion continues to fuel growth Local Growth Issues becoming more pressing,

causing greater strain on state and local infrastructure and resources

Source: The Conference Board (1985=100); Haver Analytics

Texas Leading Economic Index

80.0

90.0

100.0

110.0

120.0

130.0

140.0Ja

n-81

Jul-8

1Ja

n-82

Jul-8

2Ja

n-83

Jul-8

3Ja

n-84

Jul-8

4Ja

n-85

Jul-8

5Ja

n-86

Jul-8

6Ja

n-87

Jul-8

7Ja

n-88

Jul-8

8Ja

n-89

Jul-8

9Ja

n-90

Jul-9

0Ja

n-91

Jul-9

1Ja

n-92

Jul-9

2Ja

n-93

Jul-9

3Ja

n-94

Jul-9

4Ja

n-95

Jul-9

5Ja

n-96

Jul-9

6Ja

n-97

Jul-9

7Ja

n-98

Jul-9

8Ja

n-99

Jul-9

9Ja

n-00

Jul-0

0Ja

n-01

Jul-0

1Ja

n-02

Jul-0

2Ja

n-03

Jul-0

3Ja

n-04

Jul-0

4Ja

n-05

Jul-0

5Ja

n-06

Jul-0

6Ja

n-07

Jul-0

7Ja

n-08

Jul-0

8Ja

n-09

Jul-0

9Ja

n-10

Jul-1

0Ja

n-11

Jul-1

1Ja

n-12

Jul-1

2Ja

n-13

Jul-1

3Ja

n-14

Jul-1

4Ja

n-15

Jul-1

5

15

Texas Annual Jobs

7,098,9007,177,4007,272,9007,485,500

7,755,6008,027,300

8,260,200

8,610,9008,940,500

9,157,3009,428,9009,510,9009,412,7009,366,9009,494,100

9,737,50010,063,600

10,393,30010,607,300

10,305,60010,338,700

10,569,70010,880,300

11,206,90011,550,200

11,808,900

5,000,000

6,000,000

7,000,000

8,000,000

9,000,000

10,000,000

11,000,000

12,000,000

13,000,000

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

Jul-1

5

Sources: Texas Workforce Commission, Real Estate Center at Texas A&M University

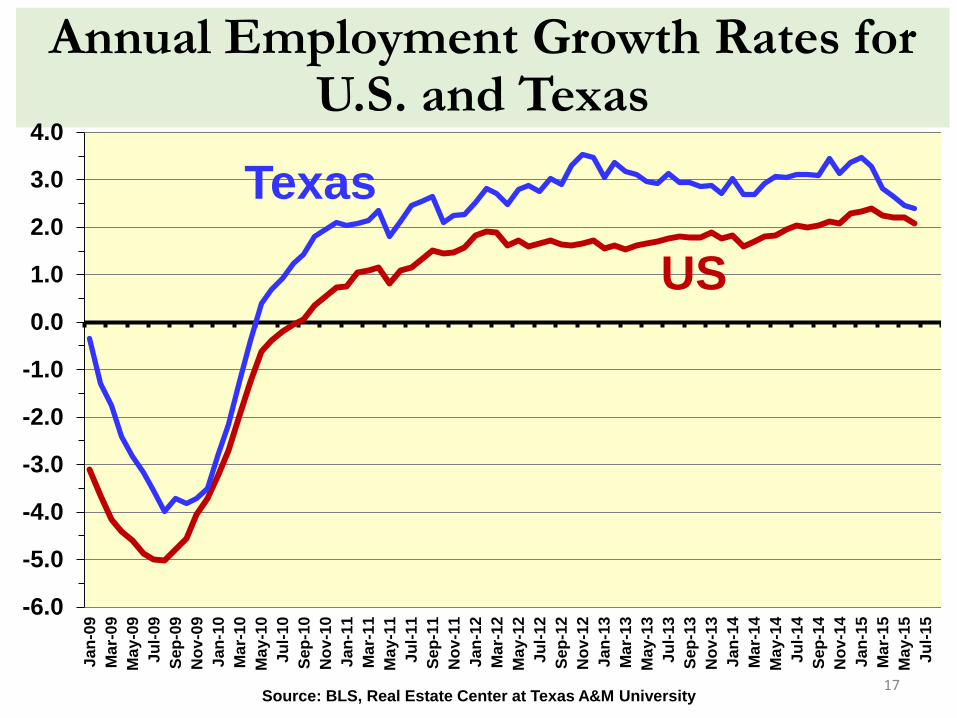

2013 +3.0%2014 +3.1%July 2015 +2.5% Y/Y, 284,000 jobs;+183,500 jobs since January

Annual Employment Growth Rates for U.S. and Texas

-6.0

-5.0

-4.0

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

Jan-

09M

ar-0

9M

ay-0

9Ju

l-09

Sep-

09N

ov-0

9Ja

n-10

Mar

-10

May

-10

Jul-1

0Se

p-10

Nov

-10

Jan-

11M

ar-1

1M

ay-1

1Ju

l-11

Sep-

11N

ov-1

1Ja

n-12

Mar

-12

May

-12

Jul-1

2Se

p-12

Nov

-12

Jan-

13M

ar-1

3M

ay-1

3Ju

l-13

Sep-

13N

ov-1

3Ja

n-14

Mar

-14

May

-14

Jul-1

4Se

p-14

Nov

-14

Jan-

15M

ar-1

5M

ay-1

5Ju

l-15

17Source: BLS, Real Estate Center at Texas A&M University

Texas

US

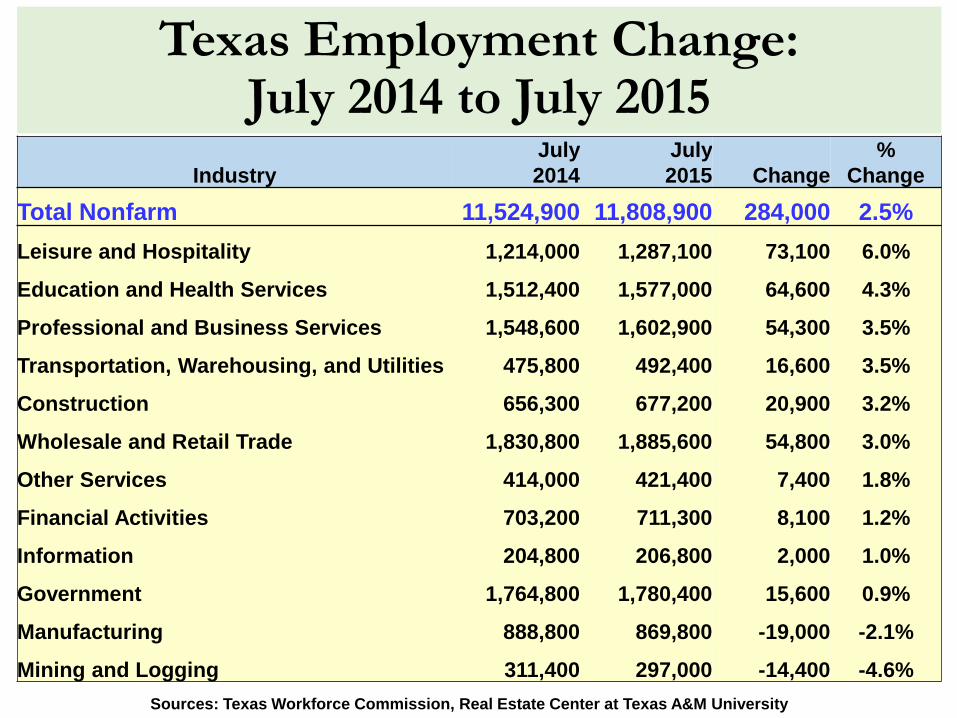

Texas Employment Change: July 2014 to July 2015

IndustryJuly 2014

July 2015 Change

% Change

Total Nonfarm 11,524,900 11,808,900 284,000 2.5%Leisure and Hospitality 1,214,000 1,287,100 73,100 6.0%

Education and Health Services 1,512,400 1,577,000 64,600 4.3%

Professional and Business Services 1,548,600 1,602,900 54,300 3.5%

Transportation, Warehousing, and Utilities 475,800 492,400 16,600 3.5%

Construction 656,300 677,200 20,900 3.2%

Wholesale and Retail Trade 1,830,800 1,885,600 54,800 3.0%

Other Services 414,000 421,400 7,400 1.8%

Financial Activities 703,200 711,300 8,100 1.2%

Information 204,800 206,800 2,000 1.0%

Government 1,764,800 1,780,400 15,600 0.9%

Manufacturing 888,800 869,800 -19,000 -2.1%

Mining and Logging 311,400 297,000 -14,400 -4.6%Sources: Texas Workforce Commission, Real Estate Center at Texas A&M University

Energy Summary• Oil Prices may not have bottomed yet:

• Global oil production increased

• Global oil demand not rapidly increasing even with rapidly-falling prices

• Significant cut back in upstream capital spending on E&P, i.e., fewer wells drilled, but production increases

• Cuts in energy employment probably not over

• Hedges run out this Fall for 2015; futures prices converging to current price

• Growing number of “DUCs” bode ill for future production shortages, e.g., if 4,000 @ 300bls/day = 1.2 million bls/day

• Increased geo-political-military volatility among oil producing nations that need (require) $95-$100+ oil price

19

Active Texas Rig Count & Price of WTI

20Source: Baker Hughes; EIA; Haver Analytics

WTI $/bl (right)

$10$20$30$40$50$60$70$80$90$100$110$120$130$140$150$160

0

100

200

300

400

500

600

700

800

900

1,000

1,100

1/7/

2000

3/31

/200

06/

23/2

000

9/15

/200

012

/8/2

000

3/2/

2001

5/25

/200

18/

17/2

001

11/9

/200

12/

1/20

024/

26/2

002

7/19

/200

210

/11/

2002

1/3/

2003

3/28

/200

36/

20/2

003

9/12

/200

312

/5/2

003

2/27

/200

45/

21/2

004

8/13

/200

411

/5/2

004

1/28

/200

54/

22/2

005

7/15

/200

510

/7/2

005

12/3

0/20

053/

24/2

006

6/16

/200

69/

8/20

0612

/1/2

006

2/23

/200

75/

18/2

007

8/10

/200

711

/2/2

007

1/25

/200

84/

18/2

008

7/11

/200

810

/3/2

008

12/2

6/20

083/

20/2

009

6/12

/200

99/

4/20

0911

/25/

2009

2/19

/201

05/

14/2

010

8/6/

2010

10/2

9/20

101/

21/2

011

4/15

/201

17/

8/20

119/

30/2

011

12/2

2/20

113/

16/2

012

6/8/

2012

8/31

/201

211

/21/

2012

2/15

/201

35/

10/2

013

8/2/

2013

10/2

5/20

131/

17/2

014

4/11

/201

47/

3/20

149/

26/2

014

12/1

9/20

143/

13/2

015

6/5/

2015

Rigs (left)

WTI $/bl (right)

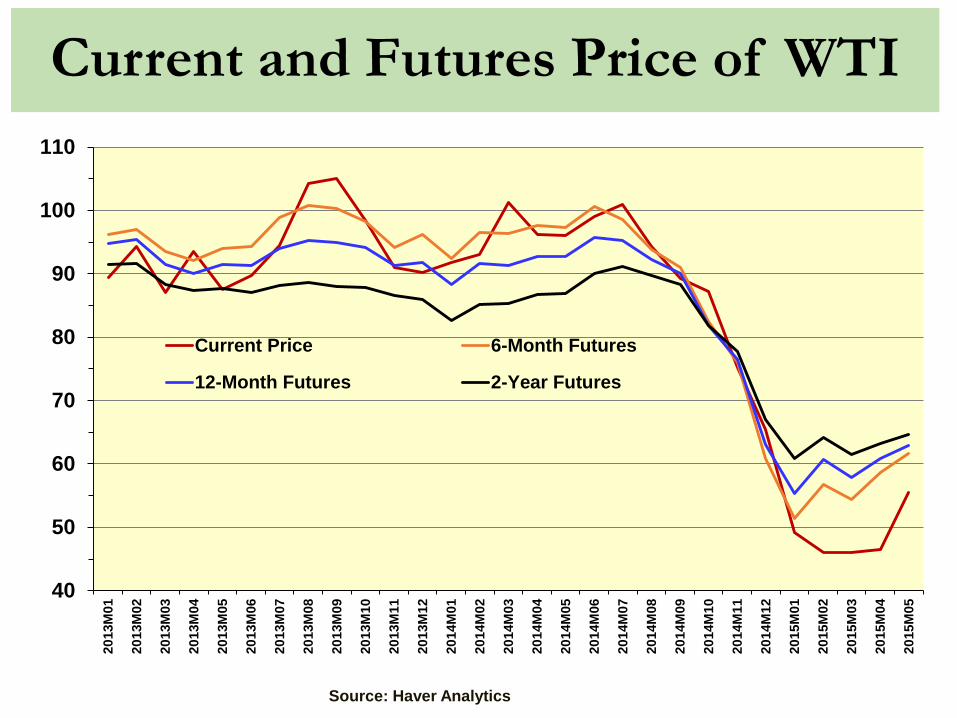

Current and Futures Price of WTI

40

50

60

70

80

90

100

110

2013

M01

2013

M02

2013

M03

2013

M04

2013

M05

2013

M06

2013

M07

2013

M08

2013

M09

2013

M10

2013

M11

2013

M12

2014

M01

2014

M02

2014

M03

2014

M04

2014

M05

2014

M06

2014

M07

2014

M08

2014

M09

2014

M10

2014

M11

2014

M12

2015

M01

2015

M02

2015

M03

2015

M04

2015

M05

Current Price 6-Month Futures

12-Month Futures 2-Year Futures

Source: Haver Analytics

Macro Housing Issues• Demographics: growing, shifting• Affordability: workforce priced out of

ownership• Capital: more equity• Infrastructure: transportation, education,

utilities• Development: Design, Density, Resources and

Processes• Regulatory: lending; environmental; land use

• Federal• State• Local Growth Controls/Initiatives

23

62.0

63.0

64.0

65.0

66.0

67.0

68.0

69.0

70.02Q

1971

2Q19

722Q

1973

2Q19

742Q

1975

2Q19

762Q

1977

2Q19

782Q

1979

2Q19

802Q

1981

2Q19

822Q

1983

2Q19

842Q

1985

2Q19

862Q

1987

2Q19

882Q

1989

2Q19

902Q

1991

2Q19

922Q

1993

2Q19

942Q

1995

2Q19

962Q

1997

2Q19

982Q

1999

2Q20

002Q

2001

2Q20

022Q

2003

2Q20

042Q

2005

2Q20

062Q

2007

2Q20

082Q

2009

2Q20

102Q

2011

2Q20

122Q

2013

2Q20

14

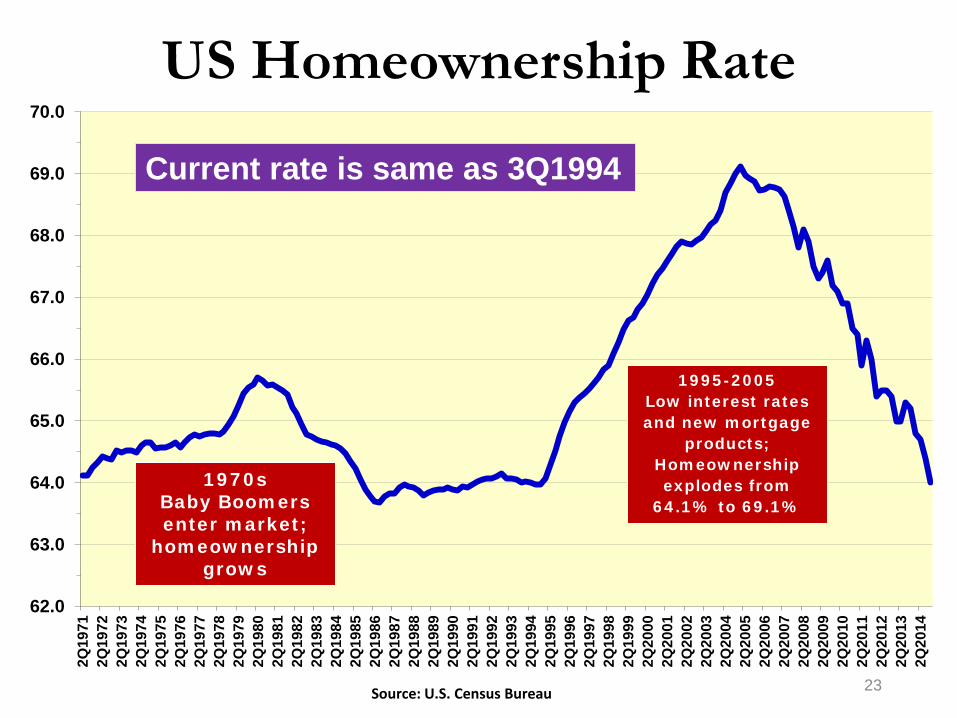

US Homeownership Rate

Source: U.S. Census Bureau

1970sBaby Boomers enter market;

homeownership grows

1995-2005Low interest rates and new mortgage

products; Homeownership explodes from

64.1% to 69.1%

(Percent)

Current rate is same as 3Q1994

Major Demographic Trends & Changing Housing Preferences

Aging population• Generational changes• Lifestyle & life cycle: Gen Y vs. Boomers

Increasing racial/ethnic diversity & cultural shifts

Economic Shift: income & wealth gap • Educated and less well educated• Age• Race & Ethnicity

Urban Concentration - urban areas24

Average Age of Major Life Events

25Source: U.S. Department of Labor, U.S. Department of Commerce and Wells Fargo Securities, LLC

First Marriage, Males: 28.6 YearsFirst Marriage, Females: 26.6 YearsFirst Child: 26.0 Years

~26

~23.5

~23

28.6

26.626.0

Projected Population Change, Texas Counties, 2010-2050

26Source: Texas State Data Center 2012 Population Projections . 2000-2010 Migration Scenario

-6,200 - 0

1 - 2,000

2,001 - 10,000

10,001 - 100,000

100,001 - 1,000,000

1,000,001 -3,480,000

Texas Population 1910-2050

3,896,542

11,196,730

25,145,56127,695,284

37,155,084

54,369,297

0

10,000,000

20,000,000

30,000,000

40,000,000

50,000,000

60,000,000

1910 1920 1930 1940 1950 1960 1970 1980 1990 2000 2010 2015 2020 2025 2030 2035 2040 2045 2050

27

From 1970 to 2010 (40 years), Texas added 13.9 million people –an average rate of 349,000 per year

From 2010 to 2050 (40 years), Texas will add another 30 million people – an average rate of about 750,000 per year

Sources: U.S. Census Bureau, Texas State Demographer 2014 Projections (2000-2010 Scenario)

Overall Growth and Change in State Population 2010-2050

Texas D-FW Houston Austin San Antonio

Population Population% of

State Total Population

% of State Total Population

% of State Total Population

% of State Total

2010 25,145,561 6,426,214 25.3% 5,920,416 23.5% 1,716,289 6.8% 2,142,508 8.5%

2020 30,541,978 7,920,671 25.8% 7,413,214 24.3% 2,306,857 7.6% 2,635,183 8.6%

2030 37,155,084 9,970,678 26.8% 9,278,789 25.0% 3,035,547 8.2% 3,182,644 8.6%

2040 44,955,896 12,728,992 28.4% 11,519,566 25.6% 3,960,317 8.9% 3,735,981 8.3%

2050 54,369,297 16,367,293 30.4% 14,221,267 26.1% 5,176,940 9.7% 4,013,515 7.7%Number Increase 29,223,736 9,941,079 34.6% 8,300,851 28.2% 3,460,651 12.0% 2,151,724 7.0%Percent Increase 116.2% 154.7% 140.2% 201.6% 100.4%

28Sources: U. S. Census; Texas State Demographer 2014 Projections (2000-2010 Scenario)

82% of total increase will go to the Major MSAs

Biggest Obstacles to Homeownership

All adults 18-34 year-olds only

Saving enough for a down payment 55% 58%

Not having a stable job 36% 43%

Having a poor credit history 35% 33%

Qualifying for a mortgage 32% 29%

Unable to pay off existing debt 26% 30%

Rising home prices 22% 23%

Rising mortgage rates 15% 18%

Limited inventory 5% 5%

Among renters who wish to buy a home right now. Respondents could choose multiple options. Survey conducted November 2013. Trulia Trends, December 2013.

Gen Y Housing OutlookGen Y

• Emerging Adults• Plugged in• Social• Educated• Outspoken• More liberal• Multicultural• High performance• High expectations• Marry later – buy later• Fewer children, later

30

Gen Y Housing• Seen the housing collapse• Currently 51% rent• 80+% eventually want to buy• First-time buyers mostly with

financial constraints to buying• Jobs and student debt = less

savings for down payment• First-time buyers <30% vs.

historic 40%• “Gen Rent”

Sources: M. Leanne Lachman and Deborah L. Brett, “Generation Y: America's New Housing Wave,” Urban Land, February 2011, FNMA National Housing Survey; Pew Research Group; Real Estate Center at Texas A&M University

Number of HHs by Age Group

8,000

8,500

9,000

9,500

10,000

10,500

11,000

11,50019

95

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

Thou

sand

s

30-34 25-29

Source: US Census HVS/Haver Analytics; Real Estate Center at Texas A&M University

Number of HHs: Head of HH 35-44

20,000

20,500

21,000

21,500

22,000

22,500

23,000

23,500

24,000

24,50019

95

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

Thou

sand

s

Source: US Census HVS/Haver Analytics; Real Estate Center at Texas A&M University

Household Formations and SF Starts

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Thou

sand

s

HH Formations^ SF Starts*

^ March-to-March Change CPS *NAHB projected 2015Source: US Census Bureau; NAHB; Real Estate Center at Texas A&M University

New SF Home Starts

1,012970964

779844

899

811813

1,151

1,309

1,132

888892

1,162

1,4511,433

1,194

852

705663

1,0671,0841,072

1,1791,146

1,081

1,003

895840

1,030

1,126

1,198

1,076

1,1611,134

1,2711,303

1,2311,273

1,359

1,499

1,610

1,716

1,465

1,046

622

445471431

535

618648

726

935

200300400500600700800900

1,0001,1001,2001,3001,4001,5001,6001,7001,800

1963

1964

1965

1966

1967

1968

1969

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

*2015 & 2016 NAHB projections Apr 2015Source: US Census Bureau; NAHB; Real Estate Center at Texas A&M University

1963-2002 average per year (1.06 million)

(000s SAAR)

Texas Household Formations and SF Starts

0

50,000

100,000

150,000

200,000

250,000

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

HH Formations SF Starts

Source: Federal Reserve Bank St. Louis; US Census Bureau; NAHB; Real Estate Center at Texas A&M University

Number of Texas Households Added Annually

209,633

196,204

139,779131,160

117,262112,024

32,833

52,105

105,718

44,952

116,063

137,000

108,00098,000

162,000

142,000139,000140,000145,886

134,468

93,985

79,27868,150

156,086

187,242

131,293134,634

178,227

105,689

210,726

111,706120,589

139,894

171,438

0

50,000

100,000

150,000

200,000

250,00019

8119

8219

8319

8419

8519

8619

8719

8819

8919

9019

9119

9219

9319

9419

9519

9619

9719

9819

9920

0020

0120

0220

0320

0420

0520

0620

0720

0820

0920

1020

1120

1220

1320

14

36Sources: U.S. Census Bureau; Real Estate Center at Texas A&M

Average number of households added annually = 126,500

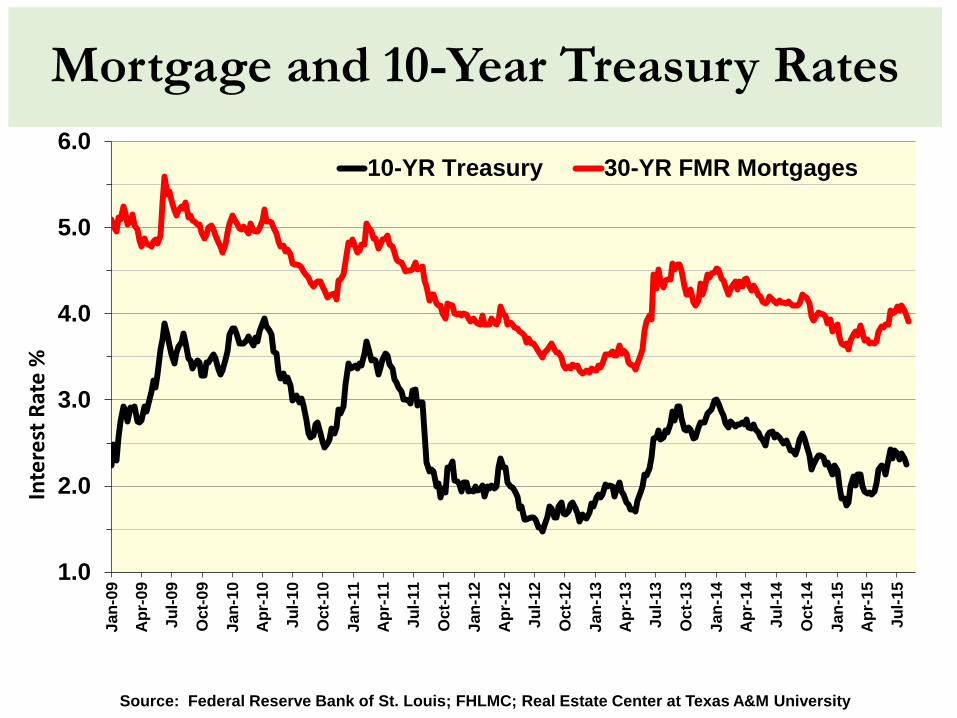

Mortgage and 10-Year Treasury Rates

1.0

2.0

3.0

4.0

5.0

6.0Ja

n-09

Apr

-09

Jul-0

9

Oct

-09

Jan-

10

Apr

-10

Jul-1

0

Oct

-10

Jan-

11

Apr

-11

Jul-1

1

Oct

-11

Jan-

12

Apr

-12

Jul-1

2

Oct

-12

Jan-

13

Apr

-13

Jul-1

3

Oct

-13

Jan-

14

Apr

-14

Jul-1

4

Oct

-14

Jan-

15

Apr

-15

Jul-1

5

Inte

rest

Rat

e %

10-YR Treasury 30-YR FMR Mortgages

Source: Federal Reserve Bank of St. Louis; FHLMC; Real Estate Center at Texas A&M University

38

0

200

400

600

800

1,000

1,200

1,400

1,600

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000Ja

n-00

Jul-0

0Ja

n-01

Jul-0

1Ja

n-02

Jul-0

2Ja

n-03

Jul-0

3Ja

n-04

Jul-0

4Ja

n-05

Jul-0

5Ja

n-06

Jul-0

6Ja

n-07

Jul-0

7Ja

n-08

Jul-0

8Ja

n-09

Jul-0

9Ja

n-10

Jul-1

0Ja

n-11

Jul-1

1Ja

n-12

Jul-1

2Ja

n-13

Jul-1

3Ja

n-14

Jul-1

4Ja

n-15

Jul-1

5

Sources: US Census Bureau , NAR, SAAR

New and Existing SF Home Sales U.S.

Existing SF Home Sales(left axis)

New Home Sales(right axis)

New Home Sales 000sExisting Home Sales 000s

Source: Real Estate Center at Texas A&M University

Annual Texas Home Sales

109,755

90,79881,105

69,279

86,28791,340

89,40582,86787,218

92,37089,848

100,04799,619107,107

116,604122,134121,823

138,123146,395

170,638

184,056188,738

196,401201,528

216,147

241,020

266,842

292,805

275,584

232,381

213,334203,637205,786

238,060

276,361284,479

151,904

50,000

70,000

90,000

110,000

130,000

150,000

170,000

190,000

210,000

230,000

250,000

270,000

290,000

310,00019

7919

8019

8119

8219

8319

8419

8519

8619

8719

8819

8919

9019

9119

9219

9319

9419

9519

9619

9719

9819

9920

0020

0120

0220

0320

0420

0520

0620

0720

0820

0920

1020

1120

1220

1320

141H

2015

39

2014 up 5%Second best year ever!

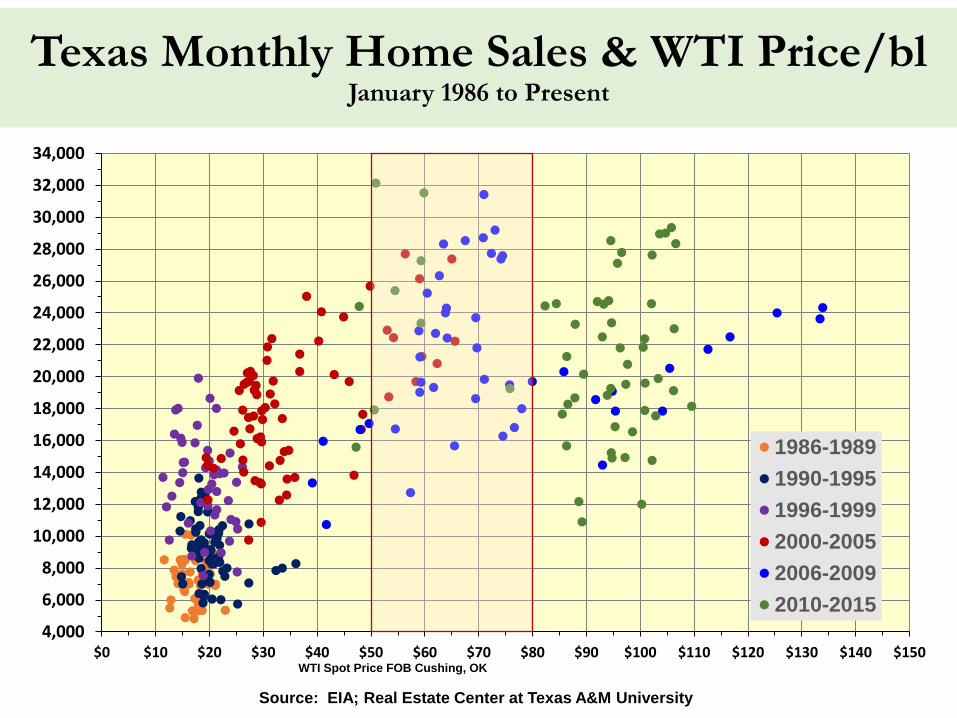

Texas Monthly Home Sales & WTI Price/blJanuary 1986 to Present

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

22,000

24,000

26,000

28,000

30,000

32,000

34,000

$0 $10 $20 $30 $40 $50 $60 $70 $80 $90 $100 $110 $120 $130 $140 $150

1986-19891990-19951996-19992000-20052006-20092010-2015

Source: EIA; Real Estate Center at Texas A&M University

WTI Spot Price FOB Cushing, OK

Texas Median Home Prices

68,50068,10071,200

75,20078,20080,00081,60086,400

90,60096,200

100,900

112,100119,400

124,500127,700130,100

136,800143,100

147,300146,900145,800147,600148,800

158,000

172,300

183,700

194,000

$50,000$60,000$70,000$80,000$90,000

$100,000$110,000$120,000$130,000$140,000$150,000$160,000$170,000$180,000$190,000$200,000$210,000

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

1H20

15

Source: Real Estate Center at Texas A&M University 41

Texas Median Price & WTI Price/bl. Monthly January 1990 to Current

$50,000

$70,000

$90,000

$110,000

$130,000

$150,000

$170,000

$190,000

$210,000

$230,000

$0 $10 $20 $30 $40 $50 $60 $70 $80 $90 $100 $110 $120 $130 $140 $150

90-9495-9900-0405-0910-1415-19

Source: Avg. Monthly WTI Spot Price FOB Cushing, OK; Real Estate Center at Texas A&M University

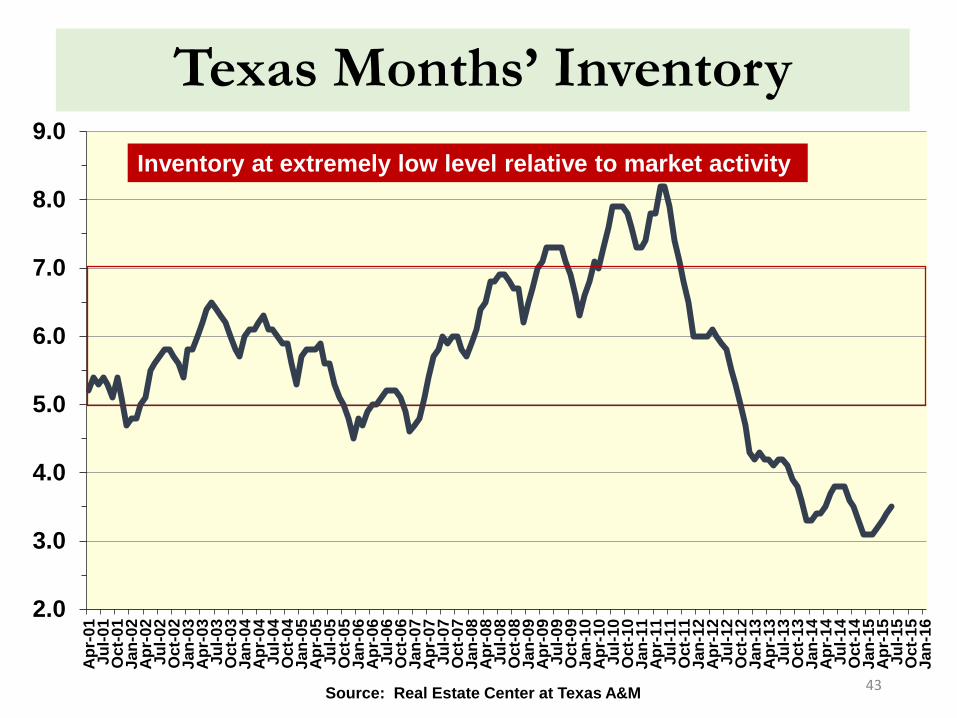

Texas Months’ Inventory

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

Apr

-01

Jul-0

1O

ct-0

1Ja

n-02

Apr

-02

Jul-0

2O

ct-0

2Ja

n-03

Apr

-03

Jul-0

3O

ct-0

3Ja

n-04

Apr

-04

Jul-0

4O

ct-0

4Ja

n-05

Apr

-05

Jul-0

5O

ct-0

5Ja

n-06

Apr

-06

Jul-0

6O

ct-0

6Ja

n-07

Apr

-07

Jul-0

7O

ct-0

7Ja

n-08

Apr

-08

Jul-0

8O

ct-0

8Ja

n-09

Apr

-09

Jul-0

9O

ct-0

9Ja

n-10

Apr

-10

Jul-1

0O

ct-1

0Ja

n-11

Apr

-11

Jul-1

1O

ct-1

1Ja

n-12

Apr

-12

Jul-1

2O

ct-1

2Ja

n-13

Apr

-13

Jul-1

3O

ct-1

3Ja

n-14

Apr

-14

Jul-1

4O

ct-1

4Ja

n-15

Apr

-15

Jul-1

5O

ct-1

5Ja

n-16

43Source: Real Estate Center at Texas A&M

Inventory at extremely low level relative to market activity

Texas SF Building Permits

67,87066,161

78,714

103,252

84,565

67,96459,143

43,97535,90836,65838,233

46,209

59,543

69,96470,45270,421

83,13282,228

99,912101,928108,782111,915

122,913

137,493

151,384

166,203163,032

120,366

81,107

68,23068,170

67,254

81,926

93,478

103,045

53,139

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,00019

8019

8119

8219

8319

8419

8519

8619

8719

8819

8919

9019

9119

9219

9319

9419

9519

9619

9719

9819

9920

0020

0120

0220

0320

0420

0520

0620

0720

0820

0920

1020

1120

1220

1320

141H

2…

Source: US Census Bureau, Real Estate Center at Texas A&M

2014 +10%

1990-2014 average 94,693/year

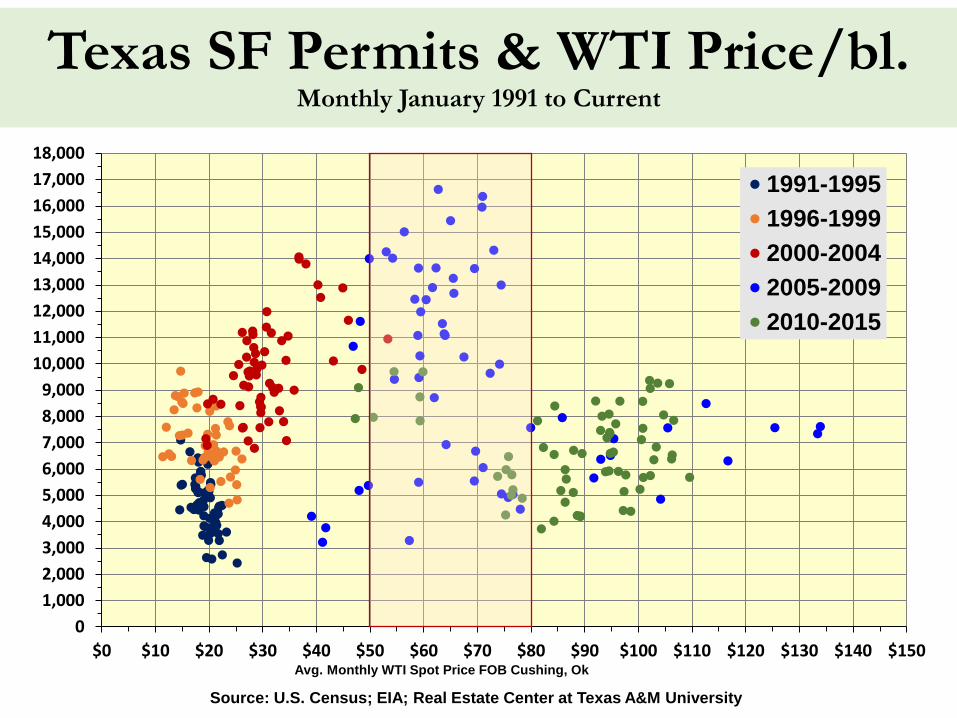

Texas SF Permits & WTI Price/bl. Monthly January 1991 to Current

01,0002,0003,0004,0005,0006,0007,0008,0009,000

10,00011,00012,00013,00014,00015,00016,00017,00018,000

$0 $10 $20 $30 $40 $50 $60 $70 $80 $90 $100 $110 $120 $130 $140 $150

1991-19951996-19992000-20042005-20092010-2015

Source: U.S. Census; EIA; Real Estate Center at Texas A&M University

Avg. Monthly WTI Spot Price FOB Cushing, Ok

Real Estate:Location, Location, Location!

National and Texas Economic and Outlook

Dr. James P. GainesChief Economist

recenter.tamu.edu