Embed Size (px)

Citation preview

Mutual Fund ScreenerFor the quarter ended Mar-17

ICRA Online LtdA Group ICRA company

Mutual Fund Screener – What’s Inside

01

Industry

QAAUM

02

Inflow Outflow

Analysis

03

Sector

Update

05

Industry

Insights

06

SEBI Investor

Survey 2015

04

Category

Performance

07

Regulatory

Update

INDUSTRY QAAUM

Section I

Industry QAAUM hits another high, Rs. 136,244 cr

added in Q4FY17

Industry QAAUM grew for the 14th consecutive period in Q4FY17

The 8.05% Q-o-Q growth in QAAUM was driven by strong participation by retail investors, robust inflow in

equity schemes through SIP, and mark to market gains

Growth in QAAUM for the Quarter Ended Mar-17

AMCs Range

Top 5 6% to 12%

Next 10 4% to 18%

Rest -20% to 37%Source: AMFI; ICRA Online Research. AMC list based on Mar-17 QAAUM

ICRA Online Limited 41AMFI

AUM of the mutual fund industry has increased five

times in the last decade1 and is expected to touch the

magical figure of Rs. 20 trillion in CY17

Mar-17,

1,829,583 Dec-16,

1,693,339

Mar-16,

1,353,443

0

500,000

1,000,000

1,500,000

2,000,000

Mar-17 Dec-16 Mar-16

QA

AU

M (

n R

s. C

rore

)

Mutual Fund Industry (QAAUM)

Source: AMFI, ICRA Online Research; QAAUM – Quarterly Average

Assets Under Management

Q-o-Q

8%

Y-o-Y

35.2%

Top 10 AMCs account for ~81% of QAAUM

ICRA Online Limited 5

0%

3%

6%

9%

12%

15%

0

50,000

100,000

150,000

200,000

250,000

ICICI

Prudential

Mutual Fund

HDFC

Mutual Fund

Reliance

Mutual Fund

Birla Sun Life

Mutual Fund

SBI Mutual

Fund

UTI Mutual

Fund

Kotak

Mahindra

Mutual Fund

Franklin

Templeton

Mutual Fund

DSP

BlackRock

Mutual Fund

IDFC Mutual

Fund

Q-o

-Q G

row

th (

In %

)

AU

M (

in R

s. C

rore

)

Top Ten AMCs

Mar-17 Dec-16 Q-o-Q

Source: AMFI, ICRA Online Research

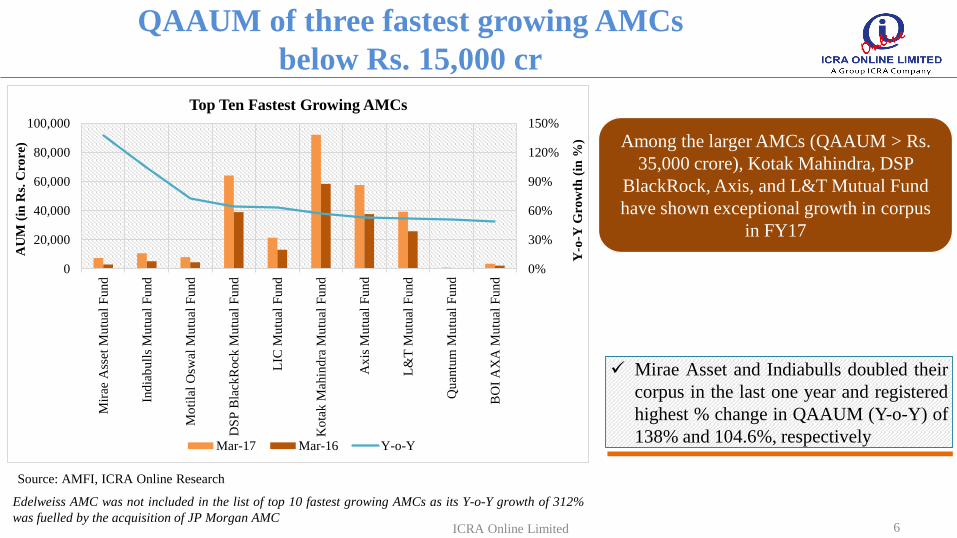

QAAUM of three fastest growing AMCs

below Rs. 15,000 cr

Edelweiss AMC was not included in the list of top 10 fastest growing AMCs as its Y-o-Y growth of 312%

was fuelled by the acquisition of JP Morgan AMC

Mirae Asset and Indiabulls doubled their

corpus in the last one year and registered

highest % change in QAAUM (Y-o-Y) of

138% and 104.6%, respectively

Among the larger AMCs (QAAUM > Rs.

35,000 crore), Kotak Mahindra, DSP

BlackRock, Axis, and L&T Mutual Fund

have shown exceptional growth in corpus

in FY17

ICRA Online Limited 6

0%

30%

60%

90%

120%

150%

0

20,000

40,000

60,000

80,000

100,000

Mir

ae A

sset

Mu

tual

Fun

d

Ind

iab

ull

s M

utu

al F

und

Mo

tila

l O

swal

Mu

tual

Fu

nd

DS

P B

lack

Rock

Mu

tual

Fun

d

LIC

Mu

tual

Fu

nd

Ko

tak

Mah

ind

ra M

utu

al F

un

d

Ax

is M

utu

al F

un

d

L&

T M

utu

al F

un

d

Qu

antu

m M

utu

al F

und

BO

I A

XA

Mutu

al F

un

d

Y-o

-Y G

row

th (

in %

)

AU

M (

in R

s. C

rore

)

Top Ten Fastest Growing AMCs

Mar-17 Mar-16 Y-o-Y

Source: AMFI, ICRA Online Research

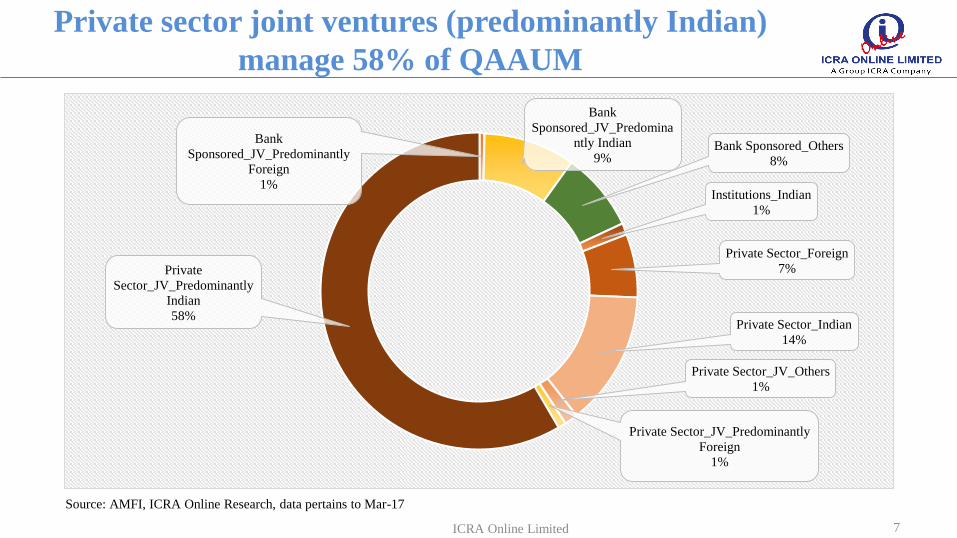

Private sector joint ventures (predominantly Indian)

manage 58% of QAAUM

ICRA Online Limited 7

Bank

Sponsored_JV_Predominantly

Foreign

1%

Bank

Sponsored_JV_Predomina

ntly Indian

9%Bank Sponsored_Others

8%

Institutions_Indian

1%

Private Sector_Foreign

7%

Private Sector_Indian

14%

Private Sector_JV_Others

1%

Private Sector_JV_Predominantly

Foreign

1%

Private

Sector_JV_Predominantly

Indian

58%

Source: AMFI, ICRA Online Research, data pertains to Mar-17

INFLOW OUTFLOW ANALYSIS

Section II

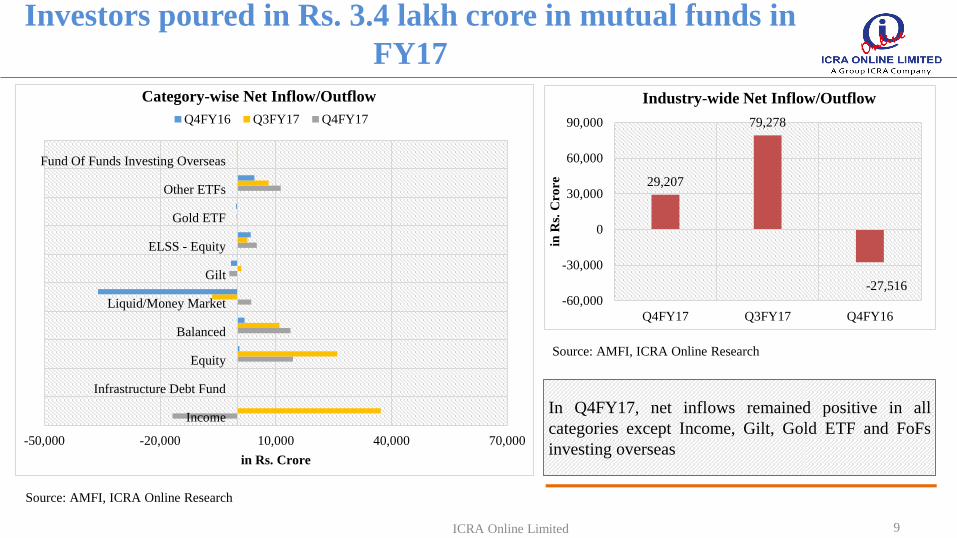

Investors poured in Rs. 3.4 lakh crore in mutual funds in

FY17

In Q4FY17, net inflows remained positive in all

categories except Income, Gilt, Gold ETF and FoFs

investing overseas

ICRA Online Limited 9

29,207

79,278

-27,516-60,000

-30,000

0

30,000

60,000

90,000

Q4FY17 Q3FY17 Q4FY16

in R

s. C

rore

Industry-wide Net Inflow/Outflow

Source: AMFI, ICRA Online Research

-50,000 -20,000 10,000 40,000 70,000

Income

Infrastructure Debt Fund

Equity

Balanced

Liquid/Money Market

Gilt

ELSS - Equity

Gold ETF

Other ETFs

Fund Of Funds Investing Overseas

in Rs. Crore

Category-wise Net Inflow/Outflow

Q4FY16 Q3FY17 Q4FY17

Source: AMFI, ICRA Online Research

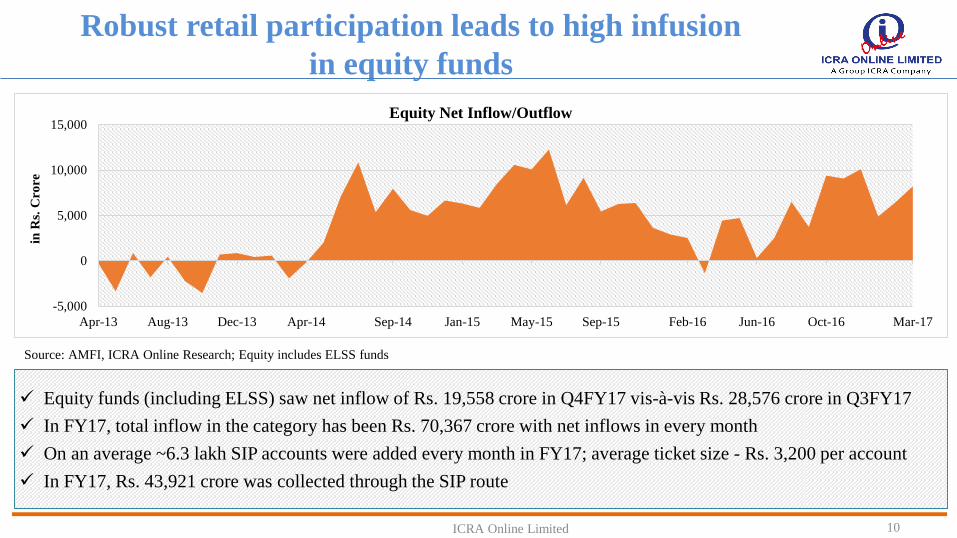

Robust retail participation leads to high infusion

in equity funds

Equity funds (including ELSS) saw net inflow of Rs. 19,558 crore in Q4FY17 vis-à-vis Rs. 28,576 crore in Q3FY17

In FY17, total inflow in the category has been Rs. 70,367 crore with net inflows in every month

On an average ~6.3 lakh SIP accounts were added every month in FY17; average ticket size - Rs. 3,200 per account

In FY17, Rs. 43,921 crore was collected through the SIP route

ICRA Online Limited 10

-5,000

0

5,000

10,000

15,000

Apr-13 Aug-13 Dec-13 Apr-14 Sep-14 Jan-15 May-15 Sep-15 Feb-16 Jun-16 Oct-16 Mar-17

in R

s. C

rore

Equity Net Inflow/Outflow

Source: AMFI, ICRA Online Research; Equity includes ELSS funds

SECTOR UPDATE

Section III

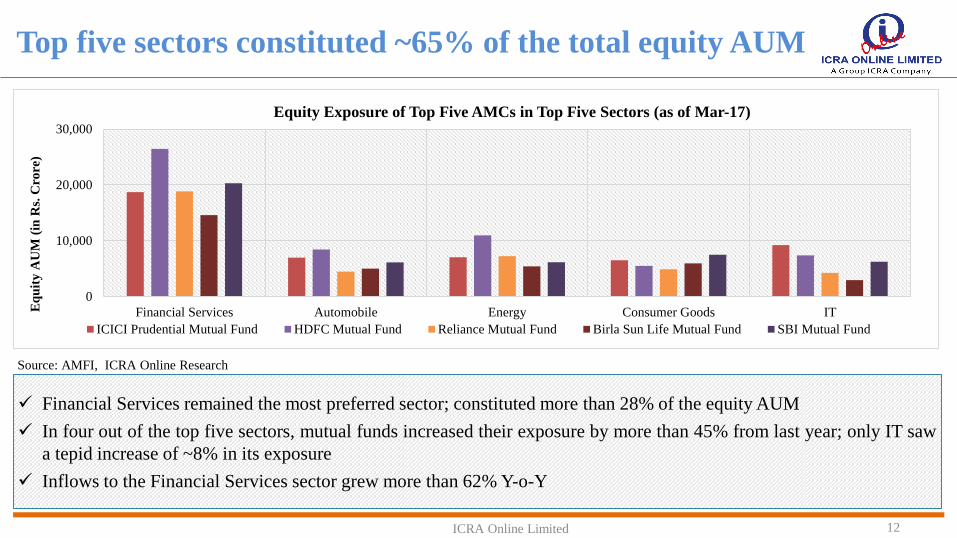

Top five sectors constituted ~65% of the total equity AUM

ICRA Online Limited 12

Source: AMFI, ICRA Online Research

Financial Services remained the most preferred sector; constituted more than 28% of the equity AUM

In four out of the top five sectors, mutual funds increased their exposure by more than 45% from last year; only IT saw

a tepid increase of ~8% in its exposure

Inflows to the Financial Services sector grew more than 62% Y-o-Y

0

10,000

20,000

30,000

Financial Services Automobile Energy Consumer Goods ITEq

uit

y A

UM

(in

Rs.

Cro

re)

Equity Exposure of Top Five AMCs in Top Five Sectors (as of Mar-17)

ICICI Prudential Mutual Fund HDFC Mutual Fund Reliance Mutual Fund Birla Sun Life Mutual Fund SBI Mutual Fund

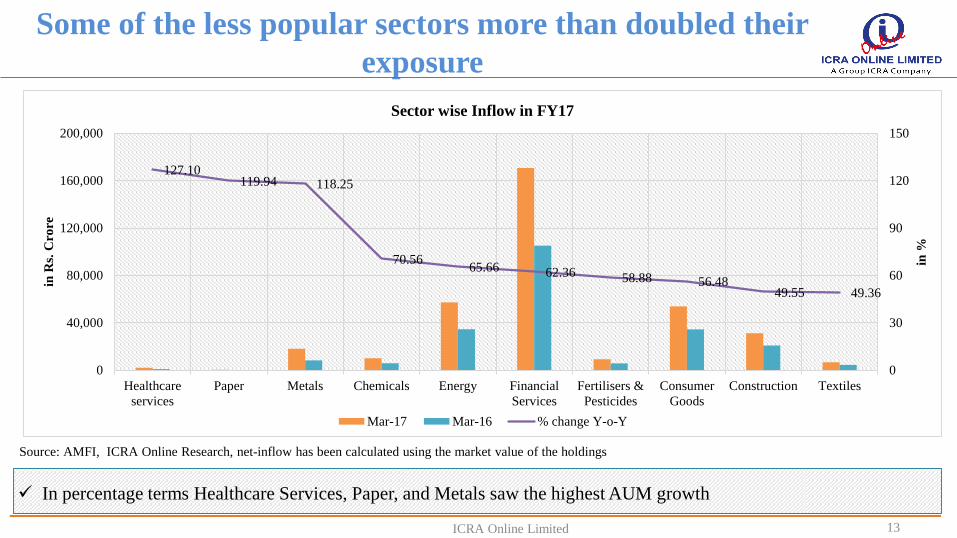

Some of the less popular sectors more than doubled their

exposure

ICRA Online Limited 13

Source: AMFI, ICRA Online Research, net-inflow has been calculated using the market value of the holdings

In percentage terms Healthcare Services, Paper, and Metals saw the highest AUM growth

127.10119.94 118.25

70.5665.66 62.36 58.88 56.48

49.55 49.36

0

30

60

90

120

150

0

40,000

80,000

120,000

160,000

200,000

Healthcare

services

Paper Metals Chemicals Energy Financial

Services

Fertilisers &

Pesticides

Consumer

Goods

Construction Textiles

in %

in R

s. C

rore

Sector wise Inflow in FY17

Mar-17 Mar-16 % change Y-o-Y

CATEGORY PERFORMANCE

Section IV

All Equity-Oriented categories posted positive returns

Key drivers:

Benchmark indices, Sensex and Nifty, surpassed the 29,000 and 9,000 marks, respectively

Outcome of state assembly elections held in five states

Government moving closer towards launching the long-awaited GST

ICRA Online Limited 15

26

.99

20

.81

17

.47

12

.64

13

.76

10

.65

11

.82

26

.01

19

.97

15

.63

12

.52

25

.44

19

.71

17

.23

12

.17

20

.62

12

.18

12

.52

8.7

1

0.00

10.00

20.00

30.00

1 Year 3 Year 5 Year 10 Year

Ret

urn

s (i

n %

)

Performance* of Equity-Oriented Mutual Fund Categories

Diversified Funds Global Funds Sector Funds ELSS Index Funds

Source: ICRA Online Research; Data as of Mar-17

*Compound Annualized returns

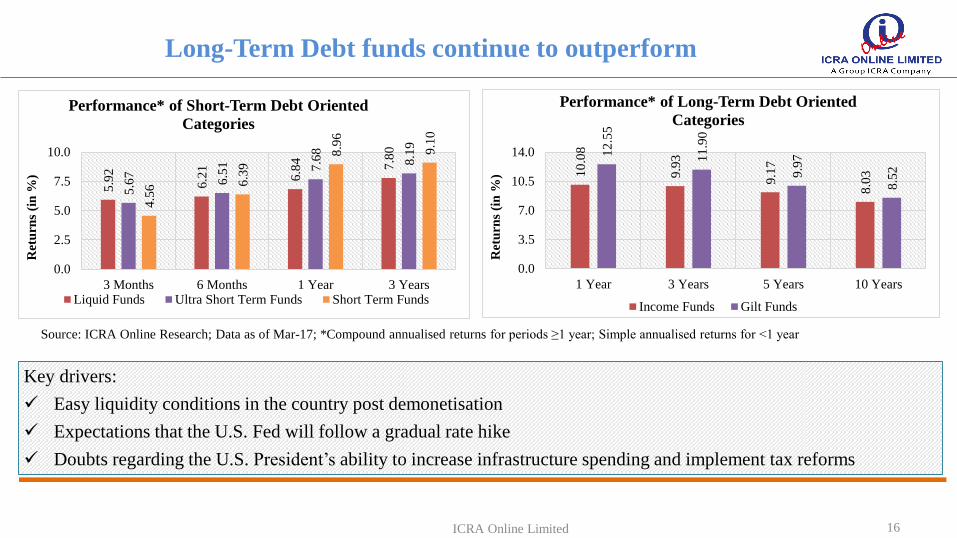

Long-Term Debt funds continue to outperform

Key drivers:

Easy liquidity conditions in the country post demonetisation

Expectations that the U.S. Fed will follow a gradual rate hike

Doubts regarding the U.S. President’s ability to increase infrastructure spending and implement tax reforms

ICRA Online Limited 16

5.9

2

6.2

1

6.8

4 7.8

0

5.6

7

6.5

1 7.6

8

8.1

9

4.5

6 6.3

9

8.9

6

9.1

0

0.0

2.5

5.0

7.5

10.0

3 Months 6 Months 1 Year 3 Years

Ret

urn

s (i

n %

)

Performance* of Short-Term Debt Oriented

Categories

Liquid Funds Ultra Short Term Funds Short Term Funds

Source: ICRA Online Research; Data as of Mar-17; *Compound annualised returns for periods ≥1 year; Simple annualised returns for <1 year

10

.08

9.9

3

9.1

7

8.0

3

12

.55

11

.90

9.9

7

8.5

2

0.0

3.5

7.0

10.5

14.0

1 Year 3 Years 5 Years 10 Years

Ret

urn

s (i

n %

)

Performance* of Long-Term Debt Oriented

Categories

Income Funds Gilt Funds

INDUSTRY INSIGHTS

Section V

Mar-17 witnesses highest monthly folio addition in FY17

As per SEBI data,10.1 lakh folios were added in Mar-17; total folio count reached 5.54 crore, 1.9% higher than Feb-17

The ELSS category drove the increase; 3.2 lakh folios were added in the month

The folio count for the Liquid category more than doubled in FY17, suggesting retail investors are looking at this route

for surplus cash deposit

ICRA Online Limited 18

0 100 200 300 400

Liquid/ Money Market

Gilt

Income

ELSS

Equity

Balanced

GOLD ETF

Other ETFs

Fund of funds investing overseas

Category-wise Folio Count (in Lakhs)

Mar-16 Feb-17 Mar-17

Source: AMFI, ICRA Online Research

48

0.7

48

4.5

48

9.2

49

2.4

49

8.0 50

5.6

51

2.9 52

0.5 52

8.2 53

7.8

54

3.9 55

4.0

470

500

530

560

Ap

r-1

6

May

-16

Jun

-16

Jul-

16

Au

g-1

6

Sep

-16

Oct

-16

No

v-1

6

Dec

-16

Jan

-17

Feb

-17

Mar

-17

Fo

lio

(in

La

kh

s)

Folio Growth in FY17

Source: SEBI, ICRA Online Research

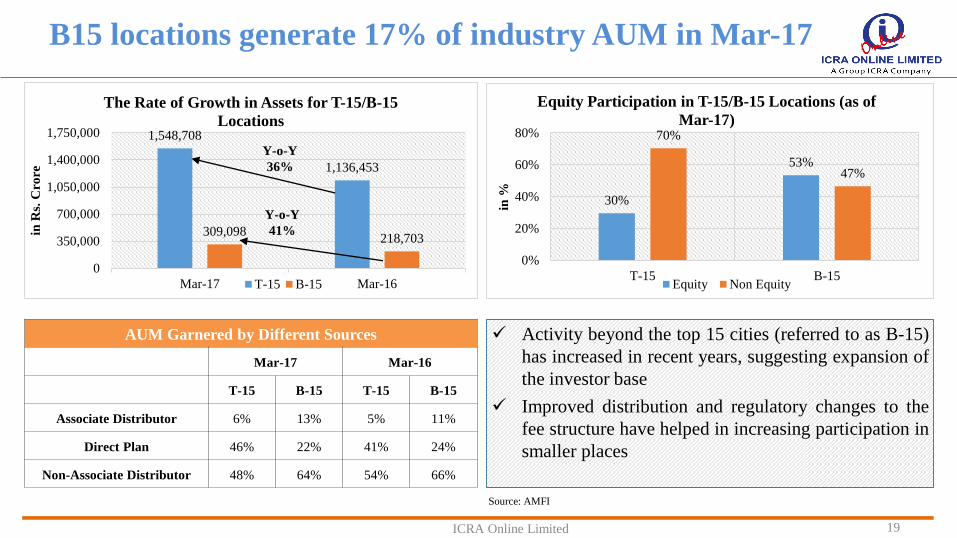

B15 locations generate 17% of industry AUM in Mar-17

Activity beyond the top 15 cities (referred to as B-15)

has increased in recent years, suggesting expansion of

the investor base

Improved distribution and regulatory changes to the

fee structure have helped in increasing participation in

smaller places

ICRA Online Limited 19

Source: AMFI

1,548,708

1,136,453

309,098218,703

0

350,000

700,000

1,050,000

1,400,000

1,750,000

Mar-17 Mar-16

in R

s. C

rore

The Rate of Growth in Assets for T-15/B-15

Locations

T-15 B-15

30%

53%

70%

47%

0%

20%

40%

60%

80%

T-15 B-15

in %

Equity Participation in T-15/B-15 Locations (as of

Mar-17)

Equity Non Equity

AUM Garnered by Different Sources

Mar-17 Mar-16

T-15 B-15 T-15 B-15

Associate Distributor 6% 13% 5% 11%

Direct Plan 46% 22% 41% 24%

Non-Associate Distributor 48% 64% 54% 66%

Y-o-Y

41%

Y-o-Y

36%

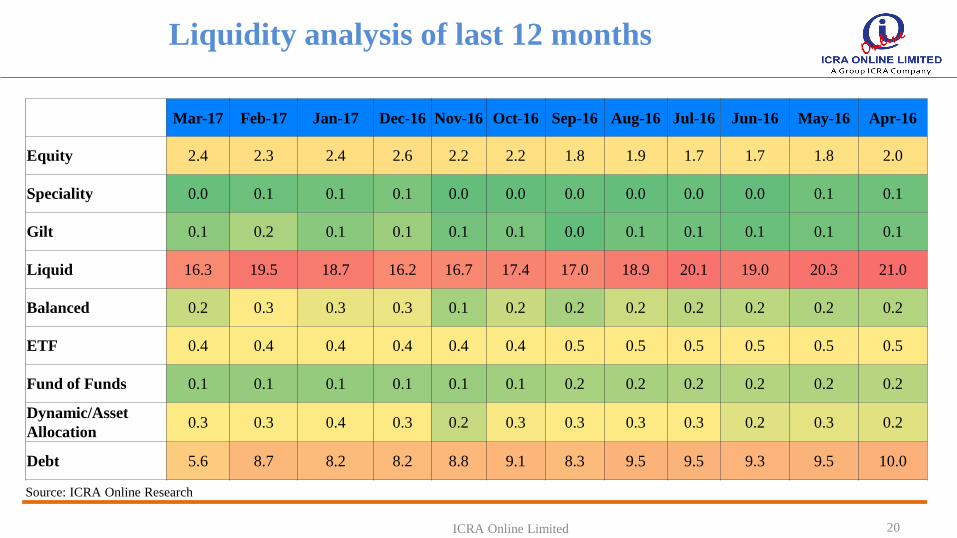

Liquidity analysis of last 12 months

ICRA Online Limited 20

Source: ICRA Online Research

Mar-17 Feb-17 Jan-17 Dec-16 Nov-16 Oct-16 Sep-16 Aug-16 Jul-16 Jun-16 May-16 Apr-16

Equity 2.4 2.3 2.4 2.6 2.2 2.2 1.8 1.9 1.7 1.7 1.8 2.0

Speciality 0.0 0.1 0.1 0.1 0.0 0.0 0.0 0.0 0.0 0.0 0.1 0.1

Gilt 0.1 0.2 0.1 0.1 0.1 0.1 0.0 0.1 0.1 0.1 0.1 0.1

Liquid 16.3 19.5 18.7 16.2 16.7 17.4 17.0 18.9 20.1 19.0 20.3 21.0

Balanced 0.2 0.3 0.3 0.3 0.1 0.2 0.2 0.2 0.2 0.2 0.2 0.2

ETF 0.4 0.4 0.4 0.4 0.4 0.4 0.5 0.5 0.5 0.5 0.5 0.5

Fund of Funds 0.1 0.1 0.1 0.1 0.1 0.1 0.2 0.2 0.2 0.2 0.2 0.2

Dynamic/Asset

Allocation0.3 0.3 0.4 0.3 0.2 0.3 0.3 0.3 0.3 0.2 0.3 0.2

Debt 5.6 8.7 8.2 8.2 8.8 9.1 8.3 9.5 9.5 9.3 9.5 10.0

Instrument allocation pattern in debt segment

Source: ICRA Online Research

ICRA Online Limited 21

2.1

56.2

17.2

6.34.9

7.9

0.4 0.3

4.62.1

49.9

20.9

6.28.8

7.5

0.41.8 2.42.1

45.0

22.3

1.8

16.6

9.5

0.1 0.52.2

0

15

30

45

60

Equity Bond/Debentures GILT Money Market CD CP Cash Current Assets Others

in %

Mar-17 Dec-16 Mar-16

Average maturity increased post demonetisation on

rate-cut expectations; eased as RBI maintained status-quo

ICRA Online Limited 22

Source: ICRA Online Research

0

4

8

12

16

Mar-16 Apr-16 May-16 Jun-16 Jul-16 Aug-16 Sep-16 Oct-16 Nov-16 Dec-16 Jan-17 Feb-17 Mar-17

in y

rs

Average Maturity Trends in Income, GILT Long-Term & GILT Short-Term Funds

Average Maturity_Income Funds Average Maturity_GILT LT Average Maturity_GILT ST

FY17 saw mutual funds match FII inflows

ICRA Online Limited 23

Source: ICRA Online Research

140,033

79,723

110,540

-14,171

52,977

-22,678 -20,925

40,281

65,04154,912

-50,000

0

50,000

100,000

150,000

FY13 FY14 FY15 FY16 FY17

in R

s. C

rore

FPI/FII & Mutual Fund Investment Trends in Equity Markets

FPI/FII MF

Large Caps command the largest share of assets

ICRA Online Limited 24

Source: ICRA Online Research

0%

20%

40%

60%

80%

100%

Apr-16 May-16 Jun-16 Jul-16 Aug-16 Sep-16 Oct-16 Nov-16 Dec-16 Jan-17 Feb-17 Mar-17

in %

Investment Across Market Caps*

Large Cap Mid Cap Small Cap Debt & Others

*On the basis of MFI market cap classification, only equity diversified funds were considered for analysis

SEBI INVESTOR SURVEY (SIS) 2015

Section VI

SEBI conducted its fourth investor survey

ICRA Online Limited 26Source: ICRA Online Research

SEBI Investor Survey 2015 (SIS 2015) is the fourth in a series of periodic

studies conducted/sponsored by SEBI to quantify actions and perceptions of

retail investors

The survey aims to collect information on socio-economic parameters, savings

and investment behavior, reasons for non-investment in securities market and

relation of risks with investment behavior

This iteration of the study has the largest breadth and depth, covering more

than 200,000 households in the listings exercise and more than 50,000

households in the final survey across cities and villages in all states and Union

Territories (except Lakshadweep)

Total number of respondents were 50,453, of which 36,756 were urban

respondents and 13,697 were rural respondents

Bank deposits remain the most preferred investment and

savings vehicle among urban respondents

ICRA Online Limited 27Source: ICRA Online Research

Household Awareness of Investment Instruments

Mutual Funds Equities DebenturesEquity/Currency

Derivatives

Commodity

Futures

Awareness 28.4% 26.3% 13.1% 10.4% 9.5%

Investor

Awareness84.6% 79.4% 48.2% 33.6% 29.2%

Non-Investor

Awareness18.7% 17.1% 7.0% 2.4% 6.1%

95.0%

61.7%

30.3%

30.1%

16.5%

9.7%

8.1%

8.1%

4.3%

3.5%

1.4%

1.0%

0% 20% 40% 60% 80% 100%

Bank Deposits

Life Insurance

Precious Metals

Post Office Saving Schemes

Real Estate

Mutual Funds/SIPs

Equity/Stocks/Shares

Pension Schemes

Company Deposits

Debentures/Bonds

Derivatives (Equity/Currency)

Commodities Futures

Investment and Savings Vehicles Used by Survey

Respondents

N1 = 36,756 (all urban respondents); Respondents could check multiple options

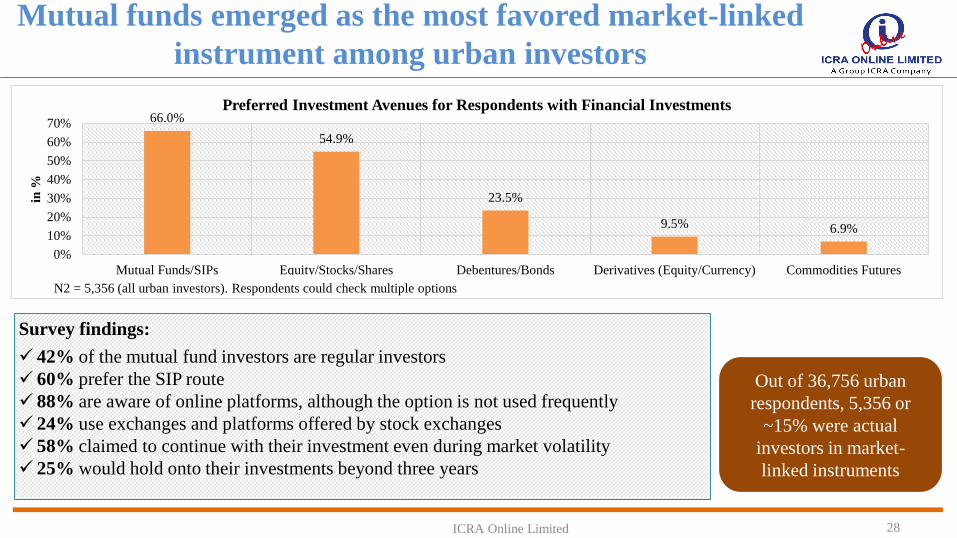

Mutual funds emerged as the most favored market-linked

instrument among urban investors

ICRA Online Limited 28

Out of 36,756 urban

respondents, 5,356 or

~15% were actual

investors in market-

linked instruments

66.0%

54.9%

23.5%

9.5% 6.9%

0%

10%

20%

30%

40%

50%

60%

70%

Mutual Funds/SIPs Equity/Stocks/Shares Debentures/Bonds Derivatives (Equity/Currency) Commodities Futures

in %

Preferred Investment Avenues for Respondents with Financial Investments

N2 = 5,356 (all urban investors). Respondents could check multiple options

Survey findings:

42% of the mutual fund investors are regular investors

60% prefer the SIP route

88% are aware of online platforms, although the option is not used frequently

24% use exchanges and platforms offered by stock exchanges

58% claimed to continue with their investment even during market volatility

25% would hold onto their investments beyond three years

Risk aversion and inadequate returns keep urban

investors away from mutual funds

ICRA Online Limited 29

Not sure about

safety of

investments

33%

Inadequate returns

26%

Inadequate

information

14%

Lack of expertise

13%

Investment not

very liquid

8%

others

6%

Why Do Households not Invest in Mutual Funds?

N2 = 5,356 (all urban investors). Respondents could check multiple options

Sustained and widespread mutual fund

information dissemination in India has

ensured that information availability is no

longer a concern

Potential investors are not aware of the

superior risk adjusted returns of mutual

funds and seem to consider savings and

investment instruments independently

instead of calculating their optimal weights

in a diversified portfolio

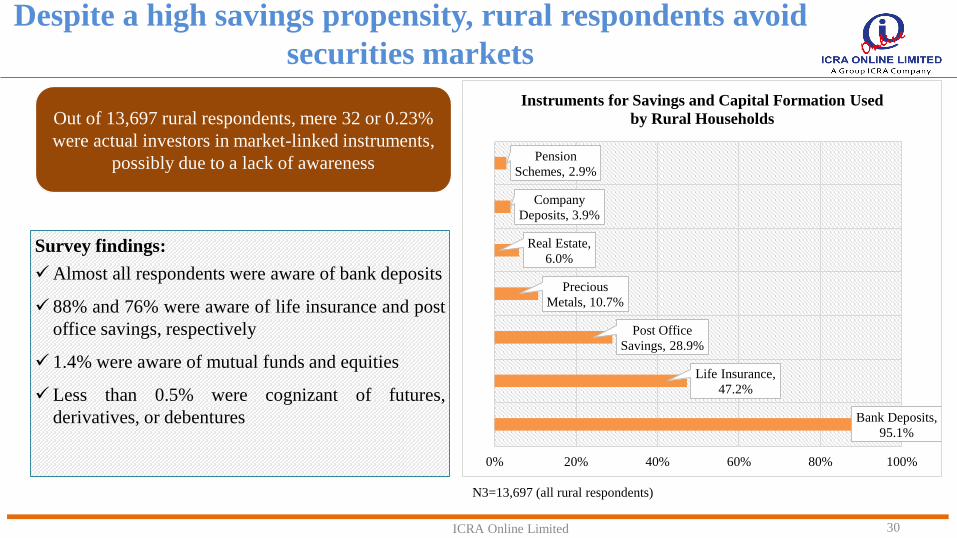

Despite a high savings propensity, rural respondents avoid

securities markets

ICRA Online Limited 30

Bank Deposits,

95.1%

Life Insurance,

47.2%

Post Office

Savings, 28.9%

Precious

Metals, 10.7%

Real Estate,

6.0%

Company

Deposits, 3.9%

Pension

Schemes, 2.9%

0% 20% 40% 60% 80% 100%

Instruments for Savings and Capital Formation Used

by Rural Households

N3=13,697 (all rural respondents)

Out of 13,697 rural respondents, mere 32 or 0.23%

were actual investors in market-linked instruments,

possibly due to a lack of awareness

Survey findings:

Almost all respondents were aware of bank deposits

88% and 76% were aware of life insurance and post

office savings, respectively

1.4% were aware of mutual funds and equities

Less than 0.5% were cognizant of futures,

derivatives, or debentures

REGULATORY UPDATE

Section VII

Regulator remains pro-active during the quarter

SEBI allows mutual funds to

invest in REITs and InvITs

SEBI reviews advertisement

guidelines of mutual funds

SEBI has allowed mutual funds to invest in Real Estate

Investment Trusts (REITs) and Infrastructure Investment Trusts

(InvITs) to make these investment tools more attractive for

investors. As per the norm, no mutual fund under all its schemes

shall own more than 10% of units issued by a single issuer of

REIT and InvIT

Regarding advertisement of the mutual fund scheme

performance, SEBI has instructed asset management companies

to advertise their returns in terms of Compounded Annualized

Growth Rate (CAGR) for the past one year, three years, five

years, and since inception. However, where the scheme has been

in existence for less than one year, past performance shall not be

provided. A point-to-point returns chart on a standard investment

of Rs. 10,000 must be given to help investors understand the

scheme better

ICRA Online Limited 32

Source: Media Reports

Disclaimer:

All information contained in this document has been obtained by ICRA Online Limited from sources believed by it to be accurate and reliable. Although reasonable

care has been taken to ensure that the information herein is true, such information is provided ‘as is’ without any warranty of any kind, and ICRA Online Limited or

its affiliates or group companies and its respective directors, officers, or employees in particular, makes no representation or warranty, express or implied, as to the

accuracy, suitability, reliability, timelines or completeness of any such information. All information contained herein must be construed solely as statements of

opinion, and ICRA Online Limited, or its affiliates or group companies and its respective directors, officers, or employees shall not be liable for any losses or injury,

liability or damage of any kind incurred from and arising out of any use of this document or its contents in any manner, whatsoever. Opinions expressed in this

document are not the opinions of our holding company, ICRA Limited (ICRA), and should not be construed as any indication of credit rating or grading of ICRA for

any instruments that have been issued or are to be issued by any entity.

Contact Information

Saugat Acharya

+91 98209 74940

Atul Sharma

+91 96191 12544

Eshna Basu

+91 98318 27490