Embed Size (px)

Citation preview

MSc in AUDIT & MANAGEMENT CONTROL

2012-2013

Page 1

MSc in AUDIT & MANAGEMENT CONTROL

2012-2013

Page 2

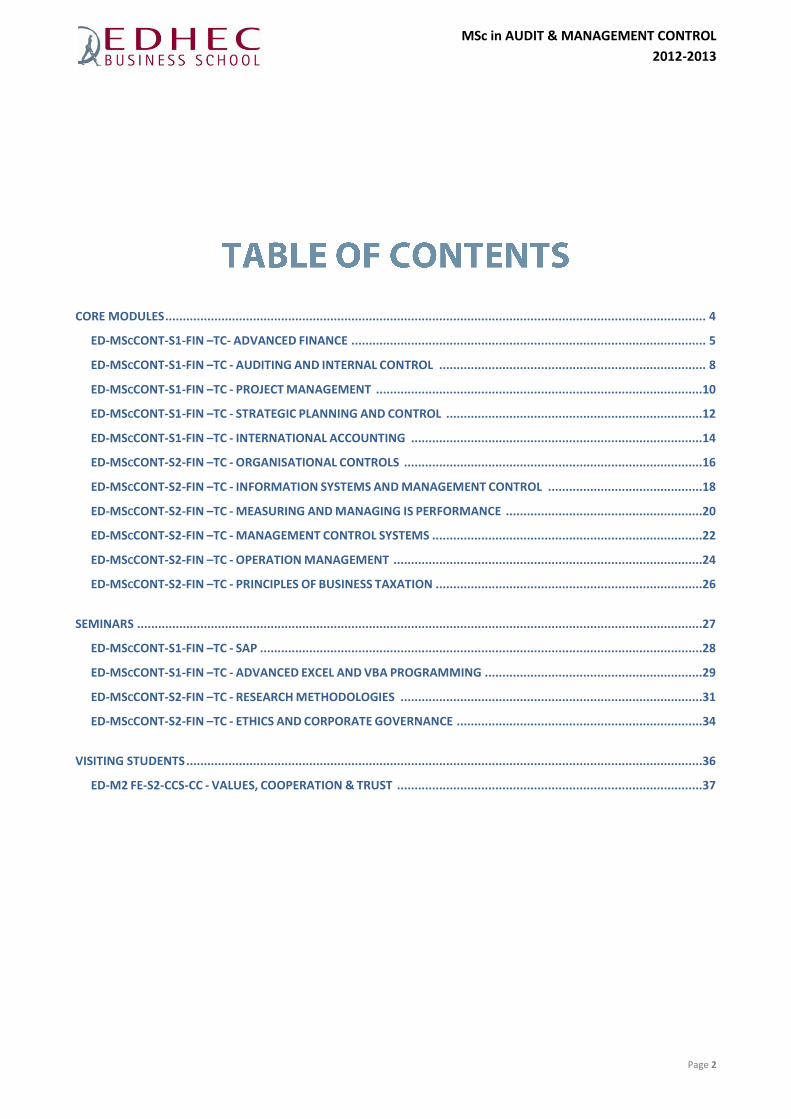

CORE MODULES .......................................................................................................................................................... 4

ED-MSCCONT-S1-FIN –TC- ADVANCED FINANCE ..................................................................................................... 5

ED-MSCCONT-S1-FIN –TC - AUDITING AND INTERNAL CONTROL ............................................................................ 8

ED-MSCCONT-S1-FIN –TC - PROJECT MANAGEMENT .............................................................................................10

ED-MSCCONT-S1-FIN –TC - STRATEGIC PLANNING AND CONTROL .........................................................................12

ED-MSCCONT-S1-FIN –TC - INTERNATIONAL ACCOUNTING ...................................................................................14

ED-MSCCONT-S2-FIN –TC - ORGANISATIONAL CONTROLS .....................................................................................16

ED-MSCCONT-S2-FIN –TC - INFORMATION SYSTEMS AND MANAGEMENT CONTROL ............................................18

ED-MSCCONT-S2-FIN –TC - MEASURING AND MANAGING IS PERFORMANCE ........................................................20

ED-MSCCONT-S2-FIN –TC - MANAGEMENT CONTROL SYSTEMS .............................................................................22

ED-MSCCONT-S2-FIN –TC - OPERATION MANAGEMENT ........................................................................................24

ED-MSCCONT-S2-FIN –TC - PRINCIPLES OF BUSINESS TAXATION ............................................................................26

SEMINARS .................................................................................................................................................................27

ED-MSCCONT-S1-FIN –TC - SAP ..............................................................................................................................28

ED-MSCCONT-S1-FIN –TC - ADVANCED EXCEL AND VBA PROGRAMMING ..............................................................29

ED-MSCCONT-S2-FIN –TC - RESEARCH METHODOLOGIES ......................................................................................31

ED-MSCCONT-S2-FIN –TC - ETHICS AND CORPORATE GOVERNANCE ......................................................................34

VISITING STUDENTS ...................................................................................................................................................36

ED-M2 FE-S2-CCS-CC - VALUES, COOPERATION & TRUST .......................................................................................37

MSc in AUDIT & MANAGEMENT CONTROL

2012-2013

Page 3

Accounting and management control are undergoing change as swiftly and as profoundly as finance. Organisational and strategic issues linked to business models are new topics in accounting that must be addressed and companies are making radical changes to their accounting and performance steering systems. It also develops additional skills such as communication, strategy, project management and human capital management. The programme has been designed in partnership with our Corporate Programme Sponsor, PwC, involved in sharing its expertise and know-how with students. It responds to today's needs for financial controllers capable of managing reporting procedures and implementing innovative financial and management accounting solutions.

CODE COURSE HOURS EDHEC INCOMING INCOMING

DD ECTS

ED-MScCONT-S1-FIN -TC Advanced EXCEL and VBA Programming 15 x x x 1,5

ED-MScCONT-S1-FIN -TC SAP 15 x x x 1,5

ED-MScCONT-S1-FIN -TC Advanced Finance 30 x x x 4

ED-MScCONT-S1-FIN -TC Auditing and Internal Control 30 x x x 4

ED-MScCONT-S1-FIN -TC Project Management 30 x x x 4

ED-MScCONT-S1-FIN -TC Strategic planning and Control 30 x x x 4

ED-MScCONT-S1-FIN -TC International Accounting 30 x x x 4

ED-MScCONT-S1-FIN -MT Master Thesis 50 x x 5

ED-MScCONT-S1-FIN -TC TI&CD 20 x x 2

SEMESTRE 1 250 30

ED-MScCONT-S2-FIN -TC Research Methodologies 15 x x x 1,5

ED-MScCONT-S2-FIN -TC Ethics and Corporate Governance 15 x x x 1,5

ED-MScCONT-S2-FIN -TC Organisational Controls 30 x x x 4

ED-MScCONT-S2-FIN -TC Information Systems and Management Control 30 x x x 4

ED-MScCONT-S2-FIN -TC Measuring and Managing IS performance 30 x x x 4

ED-MScCONT-S2-FIN -TC Management control Systems 30 x x x 4

ED-MScCONT-S2-FIN -TC Operation Management 15 x x x 2

ED-MScCONT-S2-FIN -TC Principles of business Taxation 15 x x x 2

ED-MScCONT-S2-FIN -MT Master Thesis 50 x x 5

ED-MScCONT-S2-FIN -TC TI&CD 20 x x 2

ED-MScCONT-S2-FIN -IWE Internhip / Work Experience (only for IC) 480 15

SEMESTRE 2 250 30

MSc in AUDIT & MANAGEMENT CONTROL

2012-2013

Page 4

MSc in AUDIT & MANAGEMENT CONTROL

2012-2013

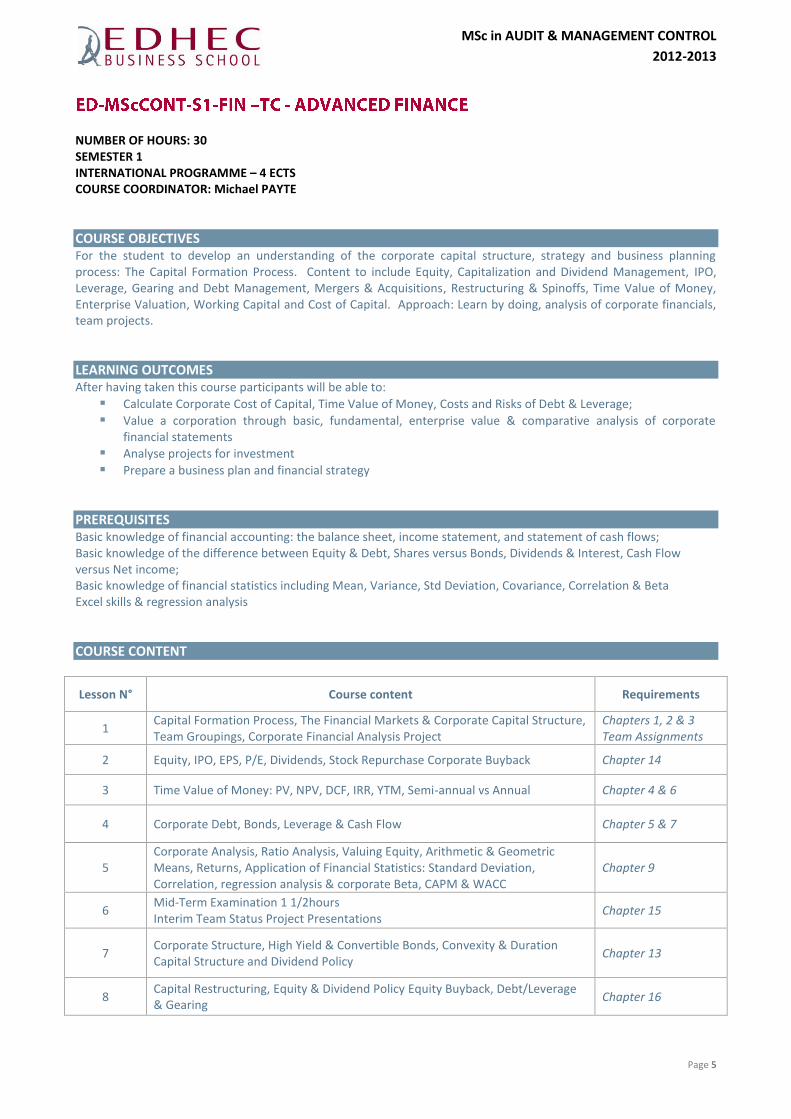

Page 5

NUMBER OF HOURS: 30 SEMESTER 1 INTERNATIONAL PROGRAMME – 4 ECTS COURSE COORDINATOR: Michael PAYTE

COURSE OBJECTIVES For the student to develop an understanding of the corporate capital structure, strategy and business planning process: The Capital Formation Process. Content to include Equity, Capitalization and Dividend Management, IPO, Leverage, Gearing and Debt Management, Mergers & Acquisitions, Restructuring & Spinoffs, Time Value of Money, Enterprise Valuation, Working Capital and Cost of Capital. Approach: Learn by doing, analysis of corporate financials, team projects.

LEARNING OUTCOMES After having taken this course participants will be able to:

Calculate Corporate Cost of Capital, Time Value of Money, Costs and Risks of Debt & Leverage;

Value a corporation through basic, fundamental, enterprise value & comparative analysis of corporate financial statements

Analyse projects for investment

Prepare a business plan and financial strategy

PREREQUISITES Basic knowledge of financial accounting: the balance sheet, income statement, and statement of cash flows; Basic knowledge of the difference between Equity & Debt, Shares versus Bonds, Dividends & Interest, Cash Flow versus Net income; Basic knowledge of financial statistics including Mean, Variance, Std Deviation, Covariance, Correlation & Beta Excel skills & regression analysis

COURSE CONTENT

Lesson N° Course content Requirements

1 Capital Formation Process, The Financial Markets & Corporate Capital Structure, Team Groupings, Corporate Financial Analysis Project

Chapters 1, 2 & 3 Team Assignments

2 Equity, IPO, EPS, P/E, Dividends, Stock Repurchase Corporate Buyback Chapter 14

3 Time Value of Money: PV, NPV, DCF, IRR, YTM, Semi-annual vs Annual Chapter 4 & 6

4 Corporate Debt, Bonds, Leverage & Cash Flow Chapter 5 & 7

5 Corporate Analysis, Ratio Analysis, Valuing Equity, Arithmetic & Geometric Means, Returns, Application of Financial Statistics: Standard Deviation, Correlation, regression analysis & corporate Beta, CAPM & WACC

Chapter 9

6 Mid-Term Examination 1 1/2hours Interim Team Status Project Presentations

Chapter 15

7 Corporate Structure, High Yield & Convertible Bonds, Convexity & Duration Capital Structure and Dividend Policy

Chapter 13

8 Capital Restructuring, Equity & Dividend Policy Equity Buyback, Debt/Leverage & Gearing

Chapter 16

MSc in AUDIT & MANAGEMENT CONTROL

2012-2013

Page 6

9 Foreign Currency, Derivatives & Interest Rate Risk Management Chapters 17 & 18

10 Team/Case Presentations Corporate Analysis

Final Examination

December, Final Exam Date to be announced

Dividend Policy - Process and Effect of Information for Dividend Management - Impact on Share Values & Taxes

Management of Stock Value - Stock Repurchase/Buybacks: Process, Effect, Political Implications - Operational Strategy - Restructuring - Spinoffs/IPOs of Subsidiaries

Mergers & Acquisitions - Debt Funding & Creditors

Management of Debt & Creditors - Objective & Methods of Repayment, Deleveraging, Debt Reduction, Reduction of Gearing

Divestitures & Liquidation in terms of Underperforming Subsidiaries

Structures of Financing - Common Stock, Preferred, Mezzanine, Hybrid/Convertibles, Subordination and Asset Backed

Valuing the enterprise and Cost of Capital - Modigliani-Miller Proposition I - Capital Asset Pricing Model - Weighted Average Cost of Capital

TEACHING & LEARNING METHODS The course will be conducted on a highly interactive basis with strong student participation expected and required, team projects essential portion of course, periodic & continuous evaluations with emphasis on financial analytical and decision making skills

ASSESSMENT METHODS Evaluation will consist of student participation, continuous evaluation/mid-term exam, team/case analysis and presentations and the final examination. 10% Student Participation 25% Continuous Evaluation, individual assignments and mid-term exam 30% Team/Case Assignments, Corporate Analysis/Report & Investment Banking Game 35% Final Exam

RECOMMENDED READING Required Text: Modern Financial Management: Ross, Westerfield, Jaffe, Jordan, McGraw-Hill International Edition; Required: Financial Calculator (non-programmable), capable of computing PV, NPV, DCF, IRR, YTM Suggested model Casio FC100/200. HP 12C, etc. Cell or Smart Phones, etc are NOT ACCEPTABLE/Not Permitted for use in examinations. No Cell Phones to be visible during classes. Other Source Texts:

Corporate Finance: Brealey, Myers, Allen, McGraw-Hill International Edition

Capital Markets Institutions & Instruments: Fabozzi & Modigliani, Pearson International Edition

Foundations of Financial Markets & Institutions: Fabozzi, Modigliani, Jones, Pearson International Edition

Financial Markets & Institutions: Saunders, Cornett, McGraw-Hill International Edition

MSc in AUDIT & MANAGEMENT CONTROL

2012-2013

Page 7

Financial & Managerial Accounting, The Basis for Business Decisions: Williams, Haka, Bettner, Carcello, McGraw-Hill International Edition

Other Source Material:

Financial Times: Daily Reading Required

Wall Street Journal

Bloomberg

Reuters

Yahoo.finance.com

MSN Money, moneycentral.msn.com

Google Finance, www.finance.google.com

Corporate Financial Reports/Annual Reports and websites

MSc in AUDIT & MANAGEMENT CONTROL

2012-2013

Page 8

NUMBER OF HOURS: 30 SEMESTER 1 INTERNATIONAL PROGRAMME – 4 ECTS COURSE COORDINATOR: Charlotte CYCMAN

COURSE OBJECTIVES The course aims to develop an understanding of the general nature of an audit, the objectives of an independent audit of the financial statements, the audit planning and methodologies, audit risks and types of audit tests.

LEARNING OUTCOMES After having taken this course participants will be able to:

Understand the general nature and objective of an audit

Identify main risks for an activity/entity

Determine the audit strategy / types of audit tests to be performed

PREREQUISITES None.

COURSE CONTENT

1. General Framework of the audit - Audit objective - Types of Audit - Audit Standards - Legal Environment - Independence

2. Understand the Entity, Risk Assessment and Materiality

- Understand Client’s business and Industry - Types of risks - Materiality

3. Internal Control and Control Risk

- Internal Control Objectives - COSO Components of Internal Control - Assess Control Risks (including Internal Controls Specific to Information Technology)

4. Audit Planning and Tests of Controls

- Tests of Controls and Audit Evidence - Design Audit Program - Application to Financial Cycles

5. Audit Completion

- Audit documentation - Issue Audit Report

TEACHING & LEARNING METHODS This course includes lectures and case studies. Each student will be expected to participate actively in class.

MSc in AUDIT & MANAGEMENT CONTROL

2012-2013

Page 9

ASSESSMENT METHODS 30% Coursework 70 % Final examination

RECOMMENDED READING Auditing and Assurance Services – an Integrated Approach - Randal J.Elder & Mark S. Beasley & Alvin A.Arens

/ Pearson

Principles of Auditing – An Introduction to International Standards on Auditing - R. Hayes, R. Dassen, A.Schilder & P.Wallage / FT Prentice Hall (Pearson)

DSCG Preparation:

DSCG 4 – Comptabilité et audit - Manuels et applications - Robert Obert & Marie-Pierre Mairesse/Dunod

DSCG 5 - Management des systèmes d'information - Manuels et applications - Michelle Gillet & Patrick Gillet/Dunod

DSCG 5 - Management des systèmes d'information – Cas pratiques - Michelle Gillet & Patrick Gillet/Dunod CIMA Preparation :

CIMA Official Learning System Financial Operations - Jo Watkins -CIMA Publishing

CIMA Official Exam Practice Kit Financial Operations - Jo Watkins - CIMA Publishing

CIMA Official Learning System Financial Management - Luisa Robertson - CIMA Publishing

CIMA Official Exam Practice Kit Financial Management - Jo Watkins - CIMA Publishing

CIMA Official Learning System Financial Strategy - By John Ogilvie - CIMA Publishing

MSc in AUDIT & MANAGEMENT CONTROL

2012-2013

Page 10

NUMBER OF HOURS: 30 SEMESTER 1 INTERNATIONAL PROGRAMME – 4 ECTS COURSE COORDINATOR: Romain HENNION DE THYSES

COURSE OBJECTIVES This course proposes a process-based approach for project management providing an easily tailored and scaleable method for the management of all types of projects. The method is the de-facto standard for project management and is practiced worldwide. It is a structured approach to project management and provides a method for managing projects within a clearly defined framework. Divided into manageable stages, the method enables an efficient control of resources. Being a structured method which is widely recognized and understood, the course provides a common language for all participants in the project. This course is based on a case study. The participants propose daily presentations and a final structured project the last day.

LEARNING OUTCOMES Upon successful completion of this course, students will be able to:

How to start, control and close projects

Prepare information for inclusion in a Project Initiation Document

Understand techniques for the management of product development, quality control & change control

Prepare project plans using product based planning techniques and undertake risk analysis and management for the project

How to manage quality

How to manage risk

How to deliver projects on time, within budget and to the specified business case

To tailor the project management methods to different project environments. Candidates need to show that they understand the principles and terminology of the method.

PREREQUISITES Students motivated by consulting challenges, team work, international contexts, and worldwide opportunities.

COURSE CONTENT DDAAYY OONNEE:: Introduction, Background, Objectives, Benefits, Scope, Structure

DDAAYY TTWWOO:: Project organization: Organizational structure, Roles and responsibilities, the project board, the project manager, Team management Planning: Components, Types of plan, Planning techniques, Product based planning, the steps in planning

DDAAYY TTHHRREEEE Project control: Work package authorization, Stage assessment, Establishing project, Stage tolerance Handling exception situations: Project issues, Project reporting

DDAAYY FFOOUURR Risk management: Types of business and project risk, Risk analysis and management, The risk log Quality : Ensuring qualityQuality planning, Product descriptions, Quality control and quality review, Change control and Configuration Management, Change control steps, Authority levels, Analyzing the impact Configuration management Day five

MSc in AUDIT & MANAGEMENT CONTROL

2012-2013

Page 11

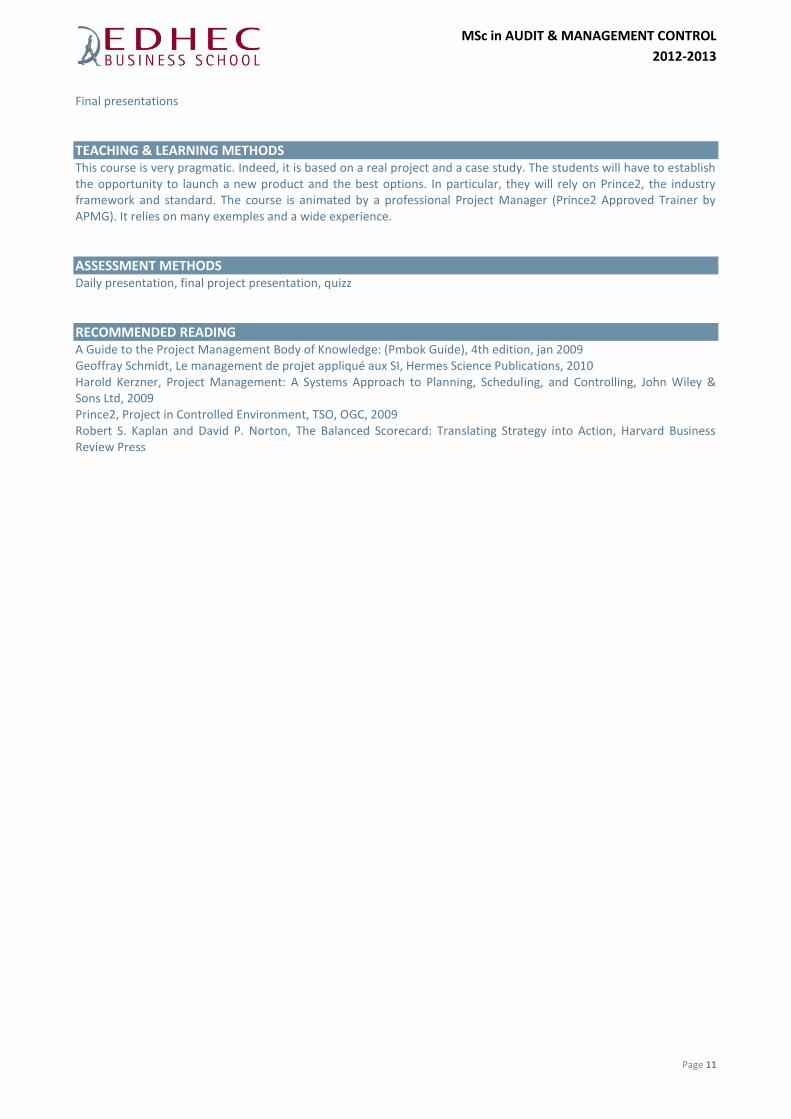

Final presentations

TEACHING & LEARNING METHODS This course is very pragmatic. Indeed, it is based on a real project and a case study. The students will have to establish the opportunity to launch a new product and the best options. In particular, they will rely on Prince2, the industry framework and standard. The course is animated by a professional Project Manager (Prince2 Approved Trainer by APMG). It relies on many exemples and a wide experience.

ASSESSMENT METHODS Daily presentation, final project presentation, quizz

RECOMMENDED READING A Guide to the Project Management Body of Knowledge: (Pmbok Guide), 4th edition, jan 2009 Geoffray Schmidt, Le management de projet appliqué aux SI, Hermes Science Publications, 2010 Harold Kerzner, Project Management: A Systems Approach to Planning, Scheduling, and Controlling, John Wiley & Sons Ltd, 2009 Prince2, Project in Controlled Environment, TSO, OGC, 2009 Robert S. Kaplan and David P. Norton, The Balanced Scorecard: Translating Strategy into Action, Harvard Business Review Press

MSc in AUDIT & MANAGEMENT CONTROL

2012-2013

Page 12

NUMBER OF HOURS: 30 SEMESTER 1 INTERNATIONAL PROGRAMME – 4 ECTS COURSE COORDINATOR: Georges IATRIDIS

COURSE OBJECTIVES & LEARNING OUTCOMES This course is about cost and management accounting. Cost accounting is concerned with information on the acquisition and consumption of resources. Whereas the central focus of management accounting is on the management of organizational performance. Then, with the measurement and reporting of financial and other types of information, cost accounting provides a useful input into management accounting. Our concern is to encompass both management accounting and cost accounting, stressing particularly the management decision making process. Management control systems (as budgets, balanced scorecard) provide information that is intended to be useful to managers in performing their jobs. This course offers an introduction to these managerial decision making tools. The course has two main objectives:

1. To provide an introduction to the field of cost and management accounting 2. To explain how a management control system has to be elaborated in function of the managerial context / of

contingent criteria.

PREREQUISITES Accounting & Management Control level 1 – Cost Accounting

COURSE CONTENT

Lesson N°

Course content

1 The accountant’s role in the organisation

2 An introduction to cost terms and purposes

3 Cost-volume-profit relationships

4 Relevant information for decision making, Part A

5 Relevant information for decision making, Part B

6 Budgetary control systems

7 Transfer Pricing

8 Control Systems and Performance Measurement

9 Balanced Scorecard

10 Total Quality Management /Revision

TEACHING & LEARNING METHODS This course includes lectures, readings assignments and exercises, quizzes and case studies. An individual written final assignment will be due after the last session. Each student will be expected to participate actively in class discussions and will be graded accordingly.

ASSESSMENT METHODS The assessment of the course comprises of a final exam (60%) and a coursework (40%).

MSc in AUDIT & MANAGEMENT CONTROL

2012-2013

Page 13

RECOMMENDED READING We will use the following book: Bhimani A., Horngren C.T., Datar S.M., Foster G., 2008, Management and Cost Accounting, 4

th ed, Prentice hall, ISBN 978-0-273- 71149-0.

Other Reading:

Cadez S., Guilding C., 2008, An exploratory investigation of an integrated contingency model of strategic management accounting, Accounting, Organizations and Society, 33, 836–863

Ittner C.D., Larcker D.F., 1997, QUALITY STRATEGY, STRATEGIC CONTROL SYSTEMS, AND ORGANIZATIONAL PERFORMANCE, Accounting, Organizations and .Society. 22 (4), 293-314.

Kaplan R.S., Norton D.P., 1996, Using the Balanced Scorecard as a Strategic Management System, HARVARD BUSINESS REVIEW, February, 75-85.

Kaplan R.S., Norton D.P., 2000, Having Trouble with Your Strategy? Then Map It, HARVARD BUSINESS REVIEW, September-October 167-176.

Otley D., 1999, Performance management: a framework for management control systems research, Management Accounting Research, 10, 363-382

MSc in AUDIT & MANAGEMENT CONTROL

2012-2013

Page 14

NUMBER OF HOURS: 30 SEMESTER 1 INTERNATIONAL PROGRAMME – 4 ECTS COURSE COORDINATOR: PWC

COURSE OBJECTIVES International Financial Reporting Standards (IFRS) have been adopted for the first time in 2005 in many countries around the world including, for listed companies initially, in the EU. The main objective of the International Accounting Standards Board (IASB) was to put in place a stable platform of International accounting rules. The IASB and the Financial Accounting Standards Board (FASB) in the US have been committed to working toward converging the two frameworks. Despite convergence initiatives, there are still many differences between these two standards. In this context, it is very important to understand main characteristics and differences of the international accounting principles (US Gaap and IAS/IFRS) with a specific focus on IFRS framework.

LEARNING OUTCOMES Upon successful completion of this course, students will be able:

to know differences between accounting policies of international companies (local Gaap, IFRS, US Gaap …),

to better understand the IASB framework and issues arising from the implementation of IFRS rules,

to gain knowledge about IFRS international accounting and financial norms implementation,

to present Financial statements standards under IFRS (Balance Sheet, Profit & Loss, cash flow statements, notes and other financial reporting)

to show how it is possible to measure financial performance of a company under IFRS (including financial analysis and financial reporting tools)

to define some specific items under IFRS such as Non current assets, Equity, Liabilities

to present some specific norms related to Financial Instruments, revenue recognition, Intangible and tangible assets, provisions, pensions, first time application …

to highlight main current Developments under IFRS framework and main differences between IFRS and US Gaap

PREREQUISITES None.

COURSE CONTENT 1-Introduction and main accounting reminders 2-IASC/IASB Framework (history, organization, elaboration process) 3-international accounting frameworks (standardization, Local, US and IFRS/IAS Gaap) 4-Framework for the preparation and the presentation of IFRS Financial statements

4.1-IFRS main principles 4.2-Presentation of financial statements

4.2.1 Key consolidation rules 4.2.2 IAS1 requirements on the presentation of financial statements

Statements of financial position (Balance sheet)

Statement of comprehensive income

Statement of changes in equity

Statement of cash-flows

5-Focus on specific IFRS items

MSc in AUDIT & MANAGEMENT CONTROL

2012-2013

Page 15

5.1-Revenue recognition (IAS 18) 5.2-Tangible and Intangible Assets (IAS 16, IAS 17, IAS 23, IAS 36 and IAS38) (1h) 5.3-Financial Assets and liabilities

Definition and Measurement

Disclosure of financial instruments 5.4-Provisions 5.5-Other assets and liabilities

6. New developments in IFRS framework Business Combination (IFRS 3R)

TEACHING & LEARNING METHODS This course is taught by professionals from PricewaterhouseCoopers Audit. It includes theoretical description of the international accounting standards, as well as case studies and small quiz. After Day 3, a specific analysis of one IFRS/IAS norm will be prepared by each group of two students. This analysis will be presented to the other teams on day 4. Each student will be expected to participate actively in class.

ASSESSMENT METHODS 40 % Course participation 60 % Final examination

RECOMMENDED READING Basic knowledge : Comparative International Accounting 10/E. Christopher Nobers and Robert B Parker. Financial Times Press Financial Accounting and reporting. My accounting Labpack. 13/E. Barry Elliott and Jamie Elliott. Financial Times Press Le Petit IFRS 2010. Robert Obert ; Editions Dunod DSCG 4 Comptabilité et Audit Manuel et applications : Robert Obert et Marie-Pierre Mairesse. Editions Dunod S’initier aux IFRS . Alain Frydlender, Julien Pagezy. Editions de la performance Further knowledge : Pratique des normes IFRS. Robert Obert. Editions Dunod. Comptabilité Générale. Système Français et norms IFRS. Jacques Richard et Christine Colette. Editions Dunod

.

MSc in AUDIT & MANAGEMENT CONTROL

2012-2013

Page 16

NUMBER OF HOURS: 30 SEMESTER 2 INTERNATIONAL PROGRAMME – 4 ECTS COURSE COORDINATOR: Louis-David BENYAYER

COURSE OBJECTIVES Control is a central function in organizations and goes usually further than common control department assignments. This course provides a clarification on control in organization:

why controlling?

what is control?

who exerts control? As a transversal function, control is closely related to other functions: strategy, structure, human resources, information systems… In this course, the relations between control and strategy on the one hand and between control and performance on the other hand will be specifically discussed.

How does the strategy influence the control system? How controlling the implementation of a specific strategy?

What are the different kinds of performances pursued? Are the controls similar?

LEARNING OUTCOMES Upon successful completion of this course, students will be able to design a comprehensive organizational control system

Strategy definition and implementation

performance measures

organization / structure

rewards and incentives

PREREQUISITES Accounting & Management Control level1 – Cost Accounting

COURSE CONTENT Introduction

What is control?

Why is control needed in organizations?

Organizational controls definition Strategic control

Basic strategy concepts

Links between strategy and control system

Strategic planning process

Johnson & Johnson Case study

New trends in strategy and impact on control systems

Other control system drivers Performance measurement

Financial performance indicators

Operations related performance indicators

CSR

MSc in AUDIT & MANAGEMENT CONTROL

2012-2013

Page 17

Who exerts control

Management control : its role and place in organization

Audit : internal vs external, legal & contracts

Internal control

Audit vs internal control vs management control Management control

Types of management control

Rewards and incentives

TEACHING & LEARNING METHODS This course includes lectures, readings assignments and exercises, quizzes and case studies. A collective written assignment will be due. Each student will be expected to participate actively in class discussions and will be graded accordingly.

ASSESSMENT METHODS 40 % Continuous assessment and participation 60 % Final examination:

RECOMMENDED READING Management Accounting Performance Evaluation - CIMA publishing

DSCG3 – Management et controle de Gestion - P. Fabre, S. Sépari, G. Solle, H. Charrier

Management control systems : performance measurement, evaluation and incentives, 2/E – Pearson – FT – K. Merchant, W. Vand der stede

Management and cost accounting (4th edition) – A. Bhimani, C. Hornger, S. Datar, G. Foster

MSc in AUDIT & MANAGEMENT CONTROL

2012-2013

Page 18

NUMBER OF HOURS: 30 SEMESTER 2 INTERNATIONAL PROGRAMME – 4 ECTS COURSE COORDINATOR: Jean-Louis TOMAS

COURSE OBJECTIVES This course examines the basic framework for integrated management information systems named Enterprise Resources Planning (ERP). The emphasis is on information systems governance for operations support including the impact of information and communication technology on management control system.

LEARNING OUTCOMES After having taken this course participants will be able to:

Understand how to govern and align the Information Systems and the strategy of the Company

Organize and control the deployment of an ERP Project: processes, people, organizations

Drive the changes when transforming the Company

PREREQUISITES Understanding of the key Business Processes of the Enterprise

High level awareness of the role and mission of an IS Department

Accounting knowledge

COURSE CONTENT

Lesson N° Course content

1 Environment of the ERP’s

2 Management of Changes

3 Demonstrations: Oracle, SAP, Sage, Crunch

4 Selection of an ERP

5 Business Case 1 – What are the Roadblocks to Avoid ?

6 Implementation Lifecycle of an ERP

7 ERP Operations & Management Control

8 Business Case 2 – The Key Focus in Deploying & Operating an ERP

9 Information Exchange

10 Final Quiz

TEACHING & LEARNING METHODS This course includes lectures, readings assignments and exercises, quizzes and Business Cases studies. An individual written final quiz will be due after the last session. Each student will be expected to participate actively in class discussions and will be graded accordingly.

ASSESSMENT METHODS

MSc in AUDIT & MANAGEMENT CONTROL

2012-2013

Page 19

40 % Business Cases and participation 60 % Final examination

RECOMMENDED READING ERP & changes management: alignment, selection and deployment – 2011, JL.Tomas - Dunod

Fundamentals of Information Systems - George Reynolds & Ralph Stair - Course Technology Inc

DSCG preparation :

DSCG 5 - Management des systèmes d'information – Manuels, applications, cas pratiques - Michelle Gillet & Patrick Gillet - Dunod

CIMA Preparation:

CIMA Official Learning System Organizational Management and Information Systems - Bob Perry - CIMA Publishing

CIMA Official Exam Practice Kit Organisational Management and Information Systems - Darren Sparkes - CIMA Publishing

Basic knowledge:

IT Performance Management - Peter Wiggers, Maritha de Boer-De-Wit, Henk Kok - Butterworth-Heinemann Ltd

Champy J., Reengineering du Management, Dunod, Paris, 1995

IT Performance Management - Peter Wiggers, Maritha de Boer-De-Wit, Henk Kok - Butterworth-Heinemann Ltd

Management Accounting Performance Evaluation - CIMA publishing

DSCG3 – Management et controle de Gestion - P. Fabre, S. Sépari, G. Solle, H. Charrier

Creating The Accountable Organization : A Practical Guide To Improve Performance Execution – Paperback 2007 - Mark Samuel

Open Erp for Retail and Industrial Management - Open Object Press, 2009 - Pinckaers F., Gardiner G.

The Politics of Information Management - New American Library – 1995 - Strassmann P.

.

MSc in AUDIT & MANAGEMENT CONTROL

2012-2013

Page 20

NUMBER OF HOURS: 30 SEMESTER 2 INTERNATIONAL PROGRAMME – 4 ECTS COURSE COORDINATOR: Christophe TALLON / Christophe BIANCO

COURSE OBJECTIVES Technological advances in information handling pose major challenges for the business enterprise. The course focuses on the importance and characteristics of information for organisations and the use of cost/benefit analysis to assess its value. The course will also address how aligning information systems with business strategy.

LEARNING OUTCOMES After having taken this course participants will be able to:

Understand and use IS performance vocabulary and calculation methodologies

Understand and follow-up the strategy of an IT department

Challenge added-value of an IT solution and global performance of an IT department

Make decision about an IT performance increase solution (such as outsourcing, off-shoring, cloud computing…)

Master IS security main concepts

PREREQUISITES Accounting & Management Control level1 – Cost Accounting

COURSE CONTENT

Lesson N°

Course content

1 Position and mission of IS in the firm (2h)

2 Resources of an IT department : typology and specific accounting rules (2h)

3 IT solutions costing : Activity-Based Costing applied to IS & Total Cost of Ownership (4h)

4 IT Planning : Budgeting approaches applied to IS (4h)

5 IS performance measures : Service Level Agreement, IT Projects evaluation, IT Balanced Scorecard (4h)

6 Improving IS performance : IT Benchmarking, ITIL, IT Outsourcing/Off-shoring, IT Cost killing (4h)

7 What is IT Security (3h)

8 Risk Management and Mitigation in IT Security (4h)

9 IT Security and Compliance(3h)

TEACHING & LEARNING METHODS This course includes lectures and case studies. An individual written final assignment will be due after the last session. Each student will be expected to participate actively in class.

MSc in AUDIT & MANAGEMENT CONTROL

2012-2013

Page 21

ASSESSMENT METHODS 100 % Final examination

RECOMMENDED READING Basic knowledge : Fundamentals of Information Systems, George Reynolds & Ralph Stair, Course Technology Inc Further knowledge : IT Performance Management, Peter Wiggers, Maritha de Boer-De-Wit, Henk Kok, Butterworth-Heinemann Ltd Comment réduire vos coûts informatiques, Olivier Brongniart, Démos Foundations of IT Service Management: The Unofficial ITIL v3 Foundations Course in a Book, Brady Orand, Createspace ITIL pour un service optimal, Christian Dumont, Eyrolles

DSCG preparation : DSCG 5 - Management des systèmes d'information - Manuels et applications, Michelle Gillet & Patrick Gillet, Dunod DSCG 5 - Management des systèmes d'information – Cas pratiques, Michelle Gillet & Patrick Gillet, Dunod CIMA preparation : CIMA Official Learning System Organisational Management and Information Systems, Bob Perry, CIMA Publishing CIMA Official Exam Practice Kit Organisational Management and Information Systems, Darren Sparkes, CIMA Publishing

MSc in AUDIT & MANAGEMENT CONTROL

2012-2013

Page 22

NUMBER OF HOURS: 30 SEMESTER 2 INTERNATIONAL PROGRAMME – 4 ECTS COURSE COORDINATOR: Olivier HERRBACH / Dipankar GHOSH

COURSE OBJECTIVES Management control systems (MCS) are tools to aid management for steering an organization toward its strategic objectives and competitive advantage by gathering and using information to evaluate the performance of different organizational resources, and by guiding the behavior of managers and other employees. Thus, the treatment of the MCS subject is broad. The primary objectives of our sessions will be on the process and structure of efficient MCS designed to achieve results control, which involves motivating employees to produce organizational outcomes. This type of management control, which has a decidedly behavioral focus, requires performance measures and evaluations and the provision of incentives, dominates in importance in a vast majority of organizations. Because management control is a core function of management, all managers must be aware of the fundamental tenets of MCS. The contexts in which MCS operate and the outcomes they produce are complex and multidimensional. Hence, simple problems and exercises cannot capture the essence of the issues managers face in designing and using MCS. Students must develop the critical thinking processes that will guide them successfully through decision tasks with multiple embedded issues and large amounts of unstructured information. They must learn to develop problem finding skills and problem solving skills, and they must learn to defend their ideas. Case analyses, discussions, and presentations provide the best method available for simulating these tasks in a classroom. The case method is generally recognized to be the best method for teaching topics in MCS. The course materials are prepared accordingly. A special focus will be made on human resources planning and control. Indeed, the importance given to HR management is growing as contemporary organizations rely more and more on the skills and attitudes of their workforce. The objective of the class is to highlight the implications of these trends for management controllers. This will involve tackling both the quantitative and qualitative dimensions of personnel management.

LEARNING OUTCOMES After having taken this course participants will be able to:

Understand how to evaluate the performance of different organizational resources, and the process and structure of efficient management control systems designed to achieve the desired organizational results (i.e., results control)

Understand the role of performance measures and evaluations and the provision of incentives in motivating employees to produce organizational results

Analyze personnel costs

Understand and measure the contribution of HR to organizational performance

PREREQUISITES None

COURSE CONTENT

Introduction/overview

Basics of designing MCS, including evaluating the performance of organizational resources

Incentive Compensation Schemes

The Use of Performance Measures

Financial Results Control and Uncontrollable Factors

Corporate Governance

Variations in Control Needs – Effect of Environment Uncertainty, Strategy and Multinationality

MSc in AUDIT & MANAGEMENT CONTROL

2012-2013

Page 23

HR Performance Management (principles of HR strategy, HR performance indicators)

Monitoring Organizational Learning and Change (principles of skills management, analyzing and conducting change)

HR Planning (headcount analysis, the HR planning process)

Personnel Cost Planning (analysis of payroll variations, building a personnel budget)

TEACHING & LEARNING METHODS This course includes lectures, problem solving, exercises and extensive case discussions. Each student will be expected to participate actively in class discussions and will be graded accordingly. Write-ups to specific questions from various cases, exercises, and/or problems are required for the course. The write-ups maybe individual or group assignments and will be turned in at the session when the case or problem is scheduled to be discussed. The ground rules for the write-ups are: maximum of 5 pages (typewritten) and any exhibits must be explained within the 5 pages; what you choose to write about is almost as important as what you say.

ASSESSMENT METHODS Case and/or problem write-up (individual or group) Case and/or problem discussion (individual or group) Class participation Final Examination Individual report

COURSE MATERIALS Materials put together for various topics Selected published articles Case studies, problems or exercises

RECOMMENDEND READINGS M. Huselid, B. Becker, D. Ulrich, The HR Scorecard, Harvard Business School Press. W. Cascio, J. Boudreau, Investing in People, FT Press.

MSc in AUDIT & MANAGEMENT CONTROL

2012-2013

Page 24

NUMBER OF HOURS: 15 SEMESTER 2 INTERNATIONAL PROGRAMME – 2 ECTS COURSE COORDINATOR: Franck GSEGNER

COURSE OBJECTIVES The course focuses on the relationships between operations and cost control management in an industry perspective. The course will also address how improving global performance in design, planning, inventory management through supply chain and manufacturing with the implementation of total quality management approach (continuous improvement, lean manufacturing, business process management) and cost control management.

LEARNING OUTCOMES After having taken this course participants will be able to:

Identify value and the core competencies of an organization

Utilize a robust business process management methodology to identify, document and manage core business process in manufacturing as well as financial areas

Use industrial management control basis combined with total quality management approach

PREREQUISITES Accounting & Management Control level1 – Cost Accounting

COURSE CONTENT

Lesson N°

Course content

1

1-Overview of functional areas of operations management in industry:

core business and support processes relationship

business process mapping and main measurement

business process management methodology

2

2-Supply Chain and Inventory Management as key drivers in a global performance sustained by Total Quality Management approach:

lean manufacturing, VA/VE, product cycle life value

productivity

vendor management inventory

forecasting process

3

3- Operations Management and Controlling:

costing system overview (material, labor, overhead cost, routing, bill of material)

cost reduction tracking (carry over, implemented, pending projects)

4

4-Appreciation of the role of quality and statistical quality control in operations management:

statistical process control

six sigma

5 5-Cost of Quality: Cost of Conformance, cost of non conformance

TEACHING & LEARNING METHODS This course includes lectures and case studies. The final notation will be based on your attendance, your individual participation during the class, your involvement in the teamwork during the workshop for the accomplishment of business cases and assignment. Each student will be expected to participate actively in class. Assignments have to be delivered on time.

MSc in AUDIT & MANAGEMENT CONTROL

2012-2013

Page 25

ASSESSMENT METHODS 50 % Continuous assessment and participation 50 % Final examination

RECOMMENDED READING DSCG preparation : DSCG 3 - Management et contrôle de gestion - Manuels et applications - Pascal Fabre / Dunod CIMA Preparation : CIMA Learning System Enterprise Operations - Bob Perry / CIMA Publishing

MSc in AUDIT & MANAGEMENT CONTROL

2012-2013

Page 26

NUMBER OF HOURS: 15 SEMESTER 2 INTERNATIONAL PROGRAMME – 2 ECTS COURSE COORDINATOR:

COURSE OBJECTIVES In an open and competitive world operations are international. Tax is a permanent issue to deal with as it is fully part of the economic performance of companies with international activities and groups composed of domestic and foreign entities. Individuals also live abroad, receive foreign source income and own foreign assets.

LEARNING OUTCOMES After having taken this course participants will be able to:

Understand tax treaty provisions

Understand business taxation rules (domestic / international)

Understand group taxation rules (domestic / international)

Understand personal taxation rules (domestic / international)

PREREQUISITES None.

COURSE CONTENT Tax picture and stakes

Personal taxation

Business taxation

VAT rules

Group taxation

Tax avoidance and tax evasion

TEACHING & LEARNING METHODS The course will be conducted on a highly interactive basis with strong student participation expected and required.

ASSESSMENT METHODS 40% Practical cases (1 hour - individual written test). 60% A final examination (1.5 hour).

RECOMMENDED READING OECD Model tax treaties.

MSc in AUDIT & MANAGEMENT CONTROL

2012-2013

Page 27

MSc in AUDIT & MANAGEMENT CONTROL

2012-2013

Page 28

NUMBER OF HOURS: 15 SEMESTER 1 INTERNATIONAL PROGRAMME – 1.5 ECTS COURSE COORDINATOR: Olivier Maghe

COURSE CONTENT FIRST DAY: 1 - A quick story of SAP.

2 - Building blocks of an SAP landscape: ERP, BI, CRM, EPM, sustainability...

3 - Basic principles of SAP ERP: Customizing, Structures, Master Data, Transactions, Reports, Workflows

4 - Focus on the accounting and controlling modules

5 - Integrated Scenario: Make to order scenario. A customer orders and customizes a motorbike. This event triggers

the production, delivery and invoicing processes. These events trigger automatic postings in accounting, product cost

controlling, and profitability analysis. Drill down from the profitability report to the corresponding sales order,

production order...

6 - Working with SAP as a controller or as an auditor.

Becoming an SAP consultant.

Working on an SAP project.

SECOND DAY:

- Scenario with two streams of purchase (on one hand, overhead on cost center then purchase an item on stock

trading).

- Run reports financial and management control to try to find the original stream (eg. from a report by cost center).

- Stream of reselling the product to a customer trading and profitability analysis.

MSc in AUDIT & MANAGEMENT CONTROL

2012-2013

Page 29

NUMBER OF HOURS: 15 SEMESTER 1 INTERNATIONAL PROGRAMME – 1.5 ECTS COURSE COORDINATOR: Pierre TELLER

COURSE OBJECTIVES The course is designed to give the students knowledge of how to use spreadsheets to solve problems and how to program in Visual Basic for Applications (VBA) for management control.

LEARNING OUTCOMES After having taken this course participants will be able to:

Record macros in a MS Excel environment

Edit macros in the macro-editor

Add user defined functions to Excel

Use VBA and userforms to create real applications

PREREQUISITES Basic knowledge about spreadsheets (references, simple formulas (maths, statistics, text , etc.), financial formulas)

COURSE CONTENT 15 hours on three days, at the beginning of fall semester. Part1: the basics 1. Introduction

What is computer programming

What is VBA

Security issues 2. The macro recorder

Using the macro recorder

Assigning a macro to a control

Shortcomings of the macro recorder 3. The macro editor

Subroutines

Data Types

Arrays 4. A closer look to VBA elements

VBA Objects

Adding new functions

Looping

Flow control In-class Exercises: 1. Macro recording 2. The classic “Hello World” 3. The InputBox 4. Call remote subroutines 5. Create a new function and use it in Excel 6. Create, fill and browse arrays 7. Create, rename, and browse worksheets 8. Using the different looping structures 9. Using conditional structures

MSc in AUDIT & MANAGEMENT CONTROL

2012-2013

Page 30

PART 2: ADVANCED FEATURES

User forms

R1C1 style

Creating Chart

Creating pivot tables

TEACHING & LEARNING METHODS The courses will take place in computer rooms. There will be a lecture to explain the different notions to the students, but every notion will be supported by one or several exercises to make in class.

ASSESSMENT METHODS 1. Continuous assessment (in-class exercises): 50% 2. Take-home assignment (after the end of the last class): 50%

RECOMMENDED READING VBA and Macros: Microsoft Excel 2010, Bill Jelen and Tracy Syrstad Mr Excel library - QUE Publishing ISBN-13: 978-0-7897-4314-5 ISBN-10: 0-7897-4314-0

.

MSc in AUDIT & MANAGEMENT CONTROL

2012-2013

Page 31

NUMBER OF HOURS: 15 SEMESTER 1 & 2 INTERNATIONAL PROGRAMME – 1.5 ECTS COURSE COORDINATOR: Paul KLUMPES – [email protected]

COURSE OBJECTIVES & LEARNING OUTCOMES The aim of this course is to discuss the various methods of undertaking empirical research in accounting and the presentation of the analysis. The course starts by defining accounting research and the different steps involved in setting up the various research questions. The course then presents the historical developments in research in Accounting and develops qualitative and quantitative research methods, including event studies and cross-sectional analysis of stock returns. The course includes a discussion of upcoming effects of major institutional changes on capital markets and firms’ behaviour as well as training in data collection from various sources and in project writing and presentation skills. The course puts significant emphasis on the interactions between the development of the research questions and the testing of such questions, and is run over two semesters to give opportunities for students to develop full blown research proposals. The course will make it possible for participants to:

familiarize with the ways of generating ideas for research

understand the recent developments in research in accounting

Present a set of techniques that allows for a concise review of the literature via a research proposal and a structured thesis

Appreciate the use of statistical techniques in testing research questions in accounting

Develop analytical skills to evaluate the impact of major regulatory changes on complex accounting choices and cost of capital estimation

Understand the relationships with the supervisor and what is usually expected to a high standard dissertation in accounting

PREREQUISITES None.

COURSE CONTENT On completing the course the participants will

Know how to undertake empirical research in Accounting and be able to prepare and present a good project research proposal

Understand how to set up and test some topic reseach questions

Gain an appreciation of applications, techniques and concepts in accounting

Contrast various approaches to test hypotheses and link relevant theories in accounting to practice

SESSIONS

FIRST SEMESTER 1- Research processes in accounting 2 General principles of writing up ‘good’ research proposals 3 Reviewing the literature

SECOND SEMESTER 1 Use of databases and techniques in accounting 2 Examples of empirical research in accounting

SYLLABUS

MSc in AUDIT & MANAGEMENT CONTROL

2012-2013

Page 32

FIRST SEMESTER Research processes in Accounting Research concerns obtaining information relevant to answering some research questions which will lead to the generation of new ideas. The research involves identifying and solving an unresolved issue of prior or existing research and needs to be incremental to that research literature. It usually involves first identifying the research question to be answered, followed by a deep and critical appreciation of the relevant literature, stating a series of logically related propositions or research hypotheses to be tested, selecting a sample, collecting data, defining and developing the methodology to be used for testing, discussion and analysis of results and finally drawing some conclusions. A recently produced paper on cost of capital by Barth et al. (2009) will be sued to illustrate this typicdal research process. We will also discuss the relationship of the student to the supervisor. General principles of writing up ‘good’ project research proposals This session discusses the role of motivation, the literature review and basics of data presentation, as well as the importance of interpretation, developing testable hypotheses and various qualifications in obtaining empirical results and their interpretation. In this session, techniques for developing abstracts, introductions, conclusions and reference lists are also discussed. This leads to the discussion of what constitutes a ‘good’ project research proposal with examples of good and poor practices.

Literature review This session provides general information about developing a literature review. This will cover the basics of commencing a detailed and thorough investigation of relevant papers, together with ways in which to develop succinct and critical appraisals of that literature. The process is shown to be a recursive one and is interrelated with the development of the research question and hypotheses.

SECOND SEMESTER

Sample selection, data collection and using external sources in research This session focuses on discussing the various resources available to collect and analyse financial and accounting data. The data may be extracted from various publicly available sources. The session allows the students to understand how the data can be effectively summarised and collated, documented and analysed in order to test the hypthoses.

Examples of empirical research in accounting: developing alternative approaches to estimating cost of capital This session provides a critical review of Barth et al. (2009) and Da et al. (2009) and are compared to the published paper of Daske (2006) as examples of contemporary empirical research in accounting that estimates the cost of capital. The article is compared and contrasted with existing prior published research on this topic and is appraised in terms of what unresolved issues are or are not addressed.

TEACHING & LEARNING METHODS The course will comprise a total of 15 hours split roughly into 5 sessions of 3 hours each. The first three sessions will be held in semester 1 and emphasize the skills needed to identify, scope and refine literature reviews and research questions into the development of hypotheses or qualitative research ideas that are incremental to and develop the existing literature. The second part of the course emphasizes technical skills in garnering research tools, databases and other sources to test the propositions and develop a fully implementable research plan.

ASSESSMENT METHODS The course is assessed by reference to (a) a mark for active participation, courteous behaviour and attendance (10%), (b) a team based mark for a presentation on a prior-nominated potential area of interest (auditing, financial reporting, tax, management accounting) at the 18 January class (10%); (c) team-based (max 3 per team) brief literature review, 2000 words of current literature related to (b) on www.ssrn.com of interest (10%) to be submitted at the start of the presentation, which contains a research question, statement of motivation, cites at least 5 authoritative published prior papers; states a hypothesis and proposes a research method, data, sample and results analysis approach and research outcome and results; (d) the writing up of the project’s research proposal, worth 70%, due on 28 February 2012. The presentation and brief literature review is due to be presented on 8 february class. Failure to attend or submit by the start of class will result in zero marks for parts (b) And/or (c).You be required to define clearly your

MSc in AUDIT & MANAGEMENT CONTROL

2012-2013

Page 33

research questions, discuss the rationale for such questions and the expected results, and present the methodology and the data sources you intend to use. The grades awarded will be based on the accuracy and depth of analysis, the way the proposal is written and presented, and the way you show your work so that your reasoning is followed by the marker. To get more than 14/20 you need to have an excellent research question, issues raised in classes covered, and an original and critical analysis to motivate your research question is undertaken. Between 12/20 and 14/20; research question is good and issues raised in class covered, and some original thoughts are provided; between 10/20 and 12/20; the research question seems reasonable, various issues raised are covered superficially, but no original thoughts are provided; less than 10/20; inadequate research proposal.

RECOMMENDED READING The course is based on a number of original research papers, two of which are attached, and some general references will be suggested.

MSc in AUDIT & MANAGEMENT CONTROL

2012-2013

Page 34

NUMBER OF HOURS: 15 SEMESTER 2 INTERNATIONAL PROGRAMME – 1.5 ECTS COURSE COORDINATOR: Luc Van LIEDEKERKE

COURSE OBJECTIVES basic insight in the meaning and importance of values and norms in the functioning of financial markets

capability to analyze cases in financial ethics in an autonomous manner

developing an attitude of a responsible actor in financial markets

LEARNING OUTCOMES After having taken this course participants will be able to:

PREREQUISITES A sound background in the architecture of financial markets

COURSE CONTENT

Lesson N°

Course content

1

fundamentals of business ethics basic elements of stakeholder theory functioning of values and norms in economic markets impact of economic systems on value formation

2 the normative balance between the firm and primary stakeholders: consumers, suppliers, employees, shareholders

3 Ethics in financial markets; real function of the financial system; normative background for financial regulation (role of Mifid etc)

4 ethics in financial services: contractual justice; how to manage the trust contract between buyers and sellers

5 Interaction between the financial firm as organization and the attitude of employees of financial firms e.g . the Barings disaster, Jerome Kerviel topics in financial ethics: insider trading, SRI, islamic banking

TEACHING & LEARNING METHODS Lectures with stress on interactive dialogue. Case studies are used throughout the course in order to strengthen the dialogue. Students are requested to read the cases before the course takes place. They discuss the cases in group during college time and the discussion is then brought into the group.

ASSESSMENT METHODS 1 article or case is presented to the students, they get 24 hours to read the article and answer a number of questions. The answer is a short essay containing a response to the question from around 3 to 4 pages. The essays are collected through the blackboard drop box.

MSc in AUDIT & MANAGEMENT CONTROL

2012-2013

Page 35

COURSE MATERIALS Required readings: Harvard business school’s cases A number of documents and PowerPoint presentation used during college. This is made available to the students via blackboard. These documents mainly act as support for the student in the building up of reliable college notes Cases Standard cases coming from Harvard business school Martha Stewart and insider trading The near collapse of Solomon Brothers The analyst dilemma Accountancy fraud at worldcom Smaller cases picked directly from financial newspaper of that moment with examples of where financial deals can go wrong, e.g. this year the Goldman Sachs case

MSc in AUDIT & MANAGEMENT CONTROL

2012-2013

Page 36

MSc in AUDIT & MANAGEMENT CONTROL

2012-2013

Page 37

NUMBER OF HOURS: 30 (5 sessions of 3 hours each) SEMESTER 1 INTERNATIONAL PROGRAMME– 7 ECTS COURSE COORDINATOR: Anne WITTE

COURSE OBJECTIVES A study of global demographics and economic history leads to an exploration of social and cultural values and how they drive migratory patterns, population profiles, women’s issues and technological and media literacy. The aim of the course is to consider the world’s cultures in terms of the social factors that impact economies and determine consumption and behaviour. These include public and private exchanges with particular consideration of the distribution of food, health, pollution, energy, education and social policy. An historical evaluation of how different value systems function economically and the contexts which allow for a successful combination of economic policy and growth allows for gaining perspective on social and cultural change in recent times and how values prompt prosperity, the use of technology and drive interpersonal change. This is an interdisciplinary course drawing from economic history, sociology, political science and cultural studies.

LEARNING OUTCOMES After having taken this course participants will be able to:

Identify the moral, historical and cultural factors impacting economies over history

discuss the major theoreticians on political economy

associate the work of public and private institutions (education, courts, sports, religion) with economic outcomes

recognize and anticipate how cultural, social and ethical priorities built within societies have enduring impact on economic behavior and the organization of trade

PREREQUISITES Three years of general business courses or Bac + 3 Business Administration

COURSE CONTENT

An Introduction to social and cultural perspectives on the economy

Types of Capital (Social Capital Theories & Bourdieu)

Cultural Factors: Hofstede, Trompenaar, Hall

The view of political economy: Landes, Weber, Sen,

The World Values Surveys (Inglehart & al.)

Trust and Cooperation (Fukuyama)

TEACHING & LEARNING METHODS Lectures, student study cohorts, Socratic dialogue, reading.

ASSESSMENT METHODS Participation 25% & Reading Presentation 25%