Embed Size (px)

Citation preview

Money

Monetary Economics

Mark Huggett1

1Georgetown

April 17, 2018

Money

A longstanding problem is to formally incorporatemoney into an economic model framework. This isnot so easily done because modern currencies closelyresemble fiat money (i.e. unbacked and intrinsicallyworthless objects that function as money).Thus, a theory for why modern currencies arevalued is not similar to a theory for why Corn Flakeshave value: Corn Flakes enter the utility functionwhile (fiat) money does not.

Money

Methodology

Economists are strong believers that in most areasof economics it is useful to construct modeleconomies (agents with preferences, firms withtechnologies and some rules of exchange) to figureout how policies work within model economies.Model economies are our laboratories. In discussingmonetary economics we will construct formal modelsto only a limited extent due to the difficulties ofbuilding tractable monetary economies.

Money

Jevons (1875): Objects Serving as Money

1. Gold, silver, copper, salt, oxen, sea shells

2. Certificates to gold or tobacco.

3. Modern paper money (e.g. US dollars)

The objects in point 1-2 are termed commoditymonies. They would have value even if they did nothave a special role as a media of exchange. Theobject in point 3 is arguably a fiat money (unbackedand intrinsically worthless).

Money

Jevons: Functions of Money

1. Media of exchange

2. Medium of account

3. Store of value

4. Standard of deferred payment

US dollars serve all four functions currently

Money

Jevons: Properties of Objects Relevant for Use as Media ofExchange

1. Portable

2. Divisible

3. Recognizable

4. Durable

Governments have worked hard to make media ofexchange effectively more divisible or recognizable.

Money

Jevons: Media of Exchange

Jevons view was that a good media of exchangewould have these properties. In his view, gold wasideal as it was (or could be made) very portable,divisible, recognizable and durable.

Arguably US dollars also display these four keyproperties to a large degree. Of course, one couldargue that certificates to some underlyingcommodities could also be made to display thesefour properties (e.g. plywood standard).

Money

Jevons: Media of Exchange

To economists, the defining property of a money isthat it is used as a media of exchange. An objectcould be described as being a media of exchange ifit is on one side of many exchanges.

US dollars are currently on one side of manyexchanges.

Money

Jevons: Media of Exchange

Economists think that media of exchange arisebecause of “frictions” in (decentralized) exchange.Example frictions:

1. Electronic means for settling payment may notbe possible (no credit or debit cards) in someexchanges.

2. The so called double coincidence of wantsproblem.

3. Not all goods are equally portable, divisible,recognizable, durable.

Money

John Law (1705)

“He who had more Goods than he had use for,would choose to barter them for Silver, though hehad no use for it; Because, Silver was certain in itsQuality”.

An Interpretation: Credit arrangements may notbe possible, double coincidence of wants may nothold and, thus, trading a recognizable object mayhelp make trade possible.

Money

Three Basic Questions about Money

1. Are there potential welfare gains to replacinga commodity money with a fiat money?

2. Is there an arbitrage opportunity betweenT-bills and dollar bills given that one paysinterest and the other does not?

3. Is money simpy a creation of the State?

Answers: 1. Yes, 2. Yes and 3. No. These areargued in the slides that follow.

Money

Welfare Gains?

Centuries ago gold, silver or copper coins circulatedas media of exchange. If it were possible to replacethese circulating media of exchange with worthlesspaper money or worthless tokens that serve as mediaof exchange, then the gold, silver and copper coinscould be used for other purposes. For example,these coins could be converted into gold watches orsilverware. These objects enter the utility function.

Money

Welfare Gains?

While economists accept this argument in principle,economists are also skeptical that these welfaregains are being achieved. The fiat money era is ahigh inflation era with many countries experiencinghyperinflations. Thus, there is still the issue thathumans have to be able to manage a fiat money.

Ecuador and Panama employ the US dollar. Youcan speculate on why this is so.

Money

Arbitrage between Tbills and Dollars?

There is a straightforward scheme that, at least inprinciple, can make large amounts of money off thefact that T-bills pay interest but US dollars do not.

1. Print the Huggett Dollar - the H$

2. Exchange the H$ for US $ one for one.

3. Use US $ to buy T-bills and to back each H$.

4. Enjoy life in Aruba using the interest payments.

Money

Money Only a Creation of the State?

Radford (1945) “The Economic Organization of aPOW Camp” is a wonderful article describingeconomic life in WWII POW camps. He argues thatmedia of exchange (specifically cigarettes) ariseendogenously, without any governmental decree, tosolve problems in decentralized exchange.

Upshot: Money is not just a creation of the State.In practice States monopolize the management ofmoney for various reasons.

Money

Price Level: Theory and Some Empirics

David Hume, John Stuart Mill and others arecredited with developing a theory of the price level.This theory is now called the Quantity Theory ofmoney.

They probably were aware of the Price Revolution -the rise in prices starting after 1500.

Money

Price Level: England and UK Data

‐0.50

0.00

0.50

1.00

1.50

2.00

2.50

1200 1300 1400 1500 1600 1700 1800 1900 2000

Log CP

I

Year

British Consumer Prices: Log CPI

CPI‐Bank of England CPI‐Clark

Money

Price Level: British Data

‐0.50

0.00

0.50

1.00

1.50

2.00

2.50

1660 1710 1760 1810 1860 1910 1960 2010

Log CP

I

Year

Log British CPI: 1661‐2015

Log British CPI

Money

Price Level: England and UK Data

There are several notable things in the price seriesdata:

1. After several centuries of stable prices, the pricelevel increased from the early 1500s to the early1600s. This is called the Price Revolution.

2. The period after WWII was both the start of thefiat money era and a era of historically highinflation rates.

Money

Quantity Theory

The Quantity Theory is an identity and oneassumption:

1. MV = PY

2. V is constant

M and V are money and velocityP and Y are the price level and output

Money

Quantity Theory: Implications

Simple manipulations of the quantity theoryequation imply:

1. P is proportional to MY since P = MV

Y

2. ∆MM

.= ∆P

P + ∆YY

Both equations offer simple tests of the theory bymeans of a scatter plot.

Money

Highly Averaged Cross-County DataChart 1

Money Growth and Inflation:A High, Positive CorrelationAverage Annual Rates of Growth in M2 and in Consumer PricesDuring 1960–90 in 110 Countries

Source: International Monetary Fund

0

20

40

60

80

100

0

20

40

60

80

100

0 20 40 60 80 100

%Inflation

Money Growth%

45°

0

Source: McCandless and Weber (1995)

Money

US Time Series (Yearly) Data: Using M1 Measure

0.05

0.1

0.15

0.2

/P

Figure1: ∆P/P vs. ∆M/M‐∆Y/Y

‐0.15

‐0.1

‐0.05

0

‐0.15 ‐0.1 ‐0.05 0 0.05 0.1 0.15 0.2

∆P/

∆M/M‐∆Y/Y

45 degree line

Money

Quantity Theory: Measuring Velocity Using M1

1. V = PYM

2. measure numerator with nominal GDP and thedenominator with a specific monetary aggregate

These choices imply that P is the GDP deflator.

M1 is a monetary aggregate equal to notes andcoins in circulation and demand deposits. Demanddeposits are checking accounts in banks.

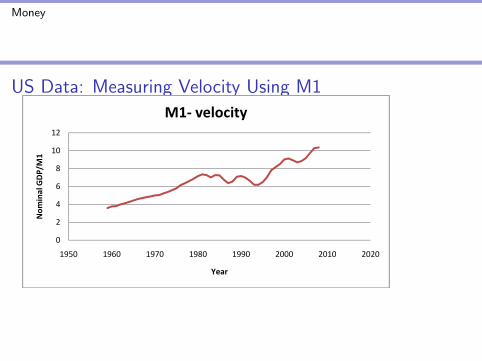

Money

US Data: Measuring Velocity Using M1

8

10

12

GDP/M1

M1‐ velocity

0

2

4

6

1950 1960 1970 1980 1990 2000 2010 2020

Nom

inal G

Year

Money

US Data: Explaining Velocity Based on M1

What explains the upward trend in velocity?

1. There have been many new transactions technologies over thelast 70 years.

2. Checks replace cash in some transactions

3. ATMs economize on costly trips to traditionalbrick-and-mortar banks

4. Credit cards replace cash in many transactions

5. As with many technological changes, there is slow difusion inadoption. Urban hipsters adopt early but eventually manyGrandmas and Grandpas adopt.

Money

Quantity Theory: A Foundation

We will offer a theoretical foundation for thequantity theory. Theorists present assumptionson the objectives of agents and some rules onhow they interact and then derive implications ofthe purely theoretical model.

We will now do so using some hand waving.Eventually, the result will be a 1980’s era“cash-in-advance model” of money.

Money

Quantity Theory: A Foundation

1. Many students are put into a room. Students are stuck inthe room forever.

2. Each is given M = 100 tokens on the first day. Each isgiven Y = 10 candy bars each day. Students likecandy bars but do not like tokens.

3. Catch: each student must put all Y candy bars intotheir own vending machine each day.

4. Rules: each student sets the token price of their candybars. only tokens enter the machine and buy candybars. anyone can put tokens into any vending machine.

Money

Quantity Theory: A Foundation

Clarifications:

1. After a student spends the initial M tokens, the only wayto consume candy bars in future periods is by emptyingtokens from their personal vending maching and usingthem.

2. Students set the price of their candy bars at the beginningof each day. They put candy into their machine in themorning.

3. They visit vending machines at mid day. They emptyvending machines of tokens at the end of each day.

4. Any candy remaining in the machine at the end of the dayis rotten and is tossed out.

Money

Quantity Theory: A Foundation

Given the objectives of agents (they like candy each day andare never satiated) and the rules of exchange, the keyquestions are stated below:

1. How will each student set the token price of their candybar?

2. How much candy will each student consume?

Experiments 1-3 illustrate how prices and consumption changewhen we change the money supply or the rules of exchange.

Money

Experiment 1: Mt = 100 and Y = 10

Answers:

1. Each student will set the price to P = MY

= 10010

= 10.

2. Each student will consume 10 candy bars each day.

Note: The answer is the price predicted by the quantity theorywith a velocity of 1.The answer seems plausible as no student benefits fromsetting a different price when all the other students are settingP = 10. The price above has the feature that all the money isspent once per day to buy up all the candy bars.

Money

Experiment 2: Mt = 2t−1100 Y = 10

If the money supply is doubled at each date by giving equalamounts of extra tokens to all students, then what is the priceprediction and the candy bar consumption prediction?

1. Each student will set the price toPt = Mt

Yt= 2t−1100

10= 2t−1 × 10 for t = 1, 2, ...., where Mt

is the money supply per person at time t.

2. Each student will consume 10 candy bars each day.

Note: The answer is the price predicted by the quantity theorywith a velocity of 1.

Money

Experiment 3: Mt = 100 Y = 10 and empty machinetwice/day

If money can be taken out of the machine twice per day, thenwhat is the price prediction and the candy bar consumptionprediction?

1. Each student will set the price to Pt = 2Mt

Yt= 2100

10= 20

for t = 1, 2, ...., where Mt and Yt are the money supplyand the candy supply per person at time t.

2. Each student will consume 10 candy bars each day.

Note: The answer is the price predicted by the quantity theorywith a velocity of 2 so that Pt = MtVt

Yt= 100×2

10.

Money

Quantity Theory: Vending Machine Economy

Is Money A Veil?

Money is largely a veil in the vending-machine economy. Thereis a long line of thought that views money as somewhatunimportant and as hiding the real workings of the economy.At the most extreme, some view money as neutral. Whenmoney is neutral, changes in money or in the mechanism bywhich money works do not affect real quantities (e.g. GDP,real interest rates and real wage rates) but do affect nominalquantities.

Money

Real and Nominal Interest Rates

The gross nominal interest rate measures thenumber of units of money one receives next periodfor giving up 1 unit of money now.

The gross real interest rate measures the number ofbaskets of goods one receives next period for givingup 1 basket of goods now.

Money

Real and Nominal Interest Rates

How to figure out the gross real interest rate, if welive in a nominal world?

1. Start with 1 basket of time t goods.2. Covert basket into pt dollars - use CPI.3. Convert pt into pt(1 + it+1) dollars tomorrow byloaning pt dollars to a bank.4. Convert dollars into pt(1+it+1)

pt+1baskets of time

t+ 1 goods!

Money

Real and Nominal Interest Rates

Summarizing:

(1 + rt+1) =ptpt+1× (1 + it+1)

(1 + it+1) = (1 + rt+1)(1 + πt+1)

The Fisher equation holds (i.e. gross nominalinterest rate equals the product of the gross realinterest rate and one plus the inflation rate), wherewe define 1 + πt+1 ≡ pt+1

pt.

Money

Real and Nominal Interest Rates

What is the real and the nomimal interest rate inthe vending machine economy?

Economy 1: Agents receive Y = 10 candy barsevery period. Agents start out with M = 100 unitsof money per person.

Agents are allowed to make risk-free loans of tokensfrom one day to the next. How should they set thenominal interest rate?

Money

Real and Nominal Interest Rates

To answer this question we need to know somethingabout preferences :

Assume: Preferences for candy consumption aregiven by the utility function

U(c1, c2, ...) =∞∑t=1

βt−1 log(ct)

When 0 < β < 1 then an agent gets more utilityfrom 10 candy bars consumed today versus 10candy bars consumed tomorrow.

Money

Real and Nominal Interest Rates

If (c1, c2, ...) = (10, 10, ...), then MRS(ct, ct+1) =?

U(c1, c2, ...) =∞∑t=1

βt−1 log(ct)

MRS(ct, ct+1) =UtUt+1

=

βt−1

ctβt

ct+1

=1

β

ct+1

ct

MRS(10, 10) =1

β

10

10=

1

β> 1

Money

Real and Nominal Interest Rates

Assume: (c1, c2, ...) = (10, 10, ...) andU(c1, c2, ...) =

∑∞t=1 β

t−1 log(ct)

Claim: If there were no money (just candy bars), then ct = 10and gross real interest rate 1 + rt+1 = 1/β > 1.

1 + rt+1 = MRS(ct, ct+1) =1

β

ct+1

ct=

1

β

10

10=

1

β

At any other real interest rate ALL agents would want to saveor ALL agents would want to lend. This is impossible. Loanmarkets work by having two parties on opposite sides of eachtransaction!

Money

Real and Nominal Interest Rates: Economy 1

Economy 1: Agents receive Y = 10 candy barsevery period. Agents start out with M = 100 unitsof money per person. Constant money.

Conjecture: constant prices, consumption andinterest rates

Pt = Mt

Yt= 100/10 = 10

ct = 10(1 + it+1) = (1 + rt+1)(1 + πt+1) = 1

β × 1 = 1β

Money

Real and Nominal Interest Rates: Economy 1

Given the price conjecture Pt = 10 each period, noother nominal interest makes sense.

At any larger nominal interest rate other than(1 + it+1) = 1

β ALL agents would want to lend somemoney. At any smaller rate ALL agents would wantto borrow. This is impossible.

At (1 + it+1) = 1β ALL agents neither want to

borrow nor to lend.

Money

Real and Nominal Interest Rates: Economy 2

Economy 2: Agents receive Y = 10 candy barsevery period. Agents start out with M = 100 unitsof money per person and money suppy doublesevery period.

Conjecture:

Pt = Mt

Yt= 2t−1100/10 = 2t−110

ct = 10(1 + it+1) = (1 + rt+1)(1 + πt+1) = 1

β × 2 = 2β

Money

Real and Nominal Interest Rates: Economy 2

Economy 2

1. ct = 10 the same as in Economy 1.

2. Pt = 2t−110 prices double every period.

3. nominal interest rate (1 + it+1) = 2/β

4. real interest rate is the SAME in Economy 1 and 2.

Real interest rates are the same because preferences for candybars and candy bar endowments pin down real interest rates.

Money is a veil: it does not impact consumption or realinterest rates but it does impact prices and nominal interestrates.

Money

Real and Nominal Interest Rates

Conclusion:

In the vending machine economy, the quantitytheory holds. The Fisher equation holds. Thenominal interest rate is pinned down by the agent’smarginal rate of substitution across periods and bythe inflation rate. Higher inflation rates passthrough into higher nominal interest rates withoutimpacting the real interest rate, which is determinedby preferences and endowments of candy bars.

Money

Tradition Question: Optimal Quantity of Money

How is the quantity of fiat money optimally managed tomaximize welfare?

1. All agents are identical in preferences and endowments. InEconomy 1 and Economy 2 the money supply differs butconsumption is exactly the same. Constant money,growing money or shrinking money are equivalent whenwelfare is measured by the agent’s common utility level.

2. There is no unique optimal quantity in this economy. Thisis because money does not serve an important role invending machine economies. A deeper model wheremoney helps solve a “friction” in the exchange process isneeded to produce a more trustworthy answer.