Embed Size (px)

Citation preview

MODEL GST LAWDecoding The Regulation…

Khandhar Mehta & Shah 1

122nd Constitution Amendment Bill, 2014 was approved in Lok

Sabha on 06-05-2015

Select Committee of Rajya Sabha submitted its

report on 22-07-2015

Rajya Sabha passed the bill unanimously on

03-08-2016

Lok Sabha has passed the bill on 08-08-2016 for the amendments suggested

by Rajya Sabha

More than half of the State Assemblies have

ratified the Bill and have received Presidential

Assent on 08-09-2016

GST Council is set up comprising Union and State Finance Ministers and will meet frequently to decide

on GST rates / slabs/ exemptions etc.

Parliament would take up GST Bill in the Budget

session along with CGST and IGST bill likely to

commence on 23-01-2017

31 State Assemblies (29 States + 2 UT) will pass SGST bill during

February and March 2017

GST TO GO LIVE BY 1st April 2017

GST – The Road Ahead

GST Council meeting Progress

Meeting No.

Date of Meeting Matters Decided / to be decided

1 22nd / 23rd September, 2016 1. Threshold Limit finalized at Rs. 20 Lacs and Rs. 10 Lacs for North EasternStates + Sikkim. It was also decided to subsume all the cesses into GST

2. On issue of compensation, it was suggested to take an average of revenuegrowth for three out of last five years excluding two outliers withsuggestion of fixing base year as 2015-16.

3. Control Jurisdictiona) Services: Central Authorities for initial 3 yearsb) Goods : Based on turnover

i)Turnover up to Rs. 1.5 Crores : Statesii) Turnover over Rs. 1.5 Crores : States + Centre

2 30th September, 2016 1. Many states gave incentive for setting up industry and exempted exciseduty. It was decided to grant cash refund will be given to all such entitiesin GST Regime.

2. The Council also agreed on five subordinate legislations i.e. draft rules andformats released on 26th and 27th September viz. (1) Registration (2)Invoice (3) Return (4) Payments & (5) Refund

3 17th, 18th / 19th October, 2016 Council was to decide upon rate slabs and exemption; however meeting was concluded without arriving at consensus on rate structure

4 3rd November, 2016 5% / 12% / 18% and 28% + Cess approved by the GST Council

5 2nd / 3rd December, 2016 No consensus among the States & Centre; Council receives few suggestions oncritical issue of cross empowerment

6 11 / 12th December, 2016 To be discussed on approval of drafts and cross empowerment

CONTENTS

BASICS OF GST

LEVY IN GST REGIME

TIME AND PLACE OF SUPPLY

GST VALUATION RULES

INPUT TAX CREDIT (ITC)

TAX ADMINISTRATION

TRANSITIONAL PROVISIONS

4

BASICS OF GST

5

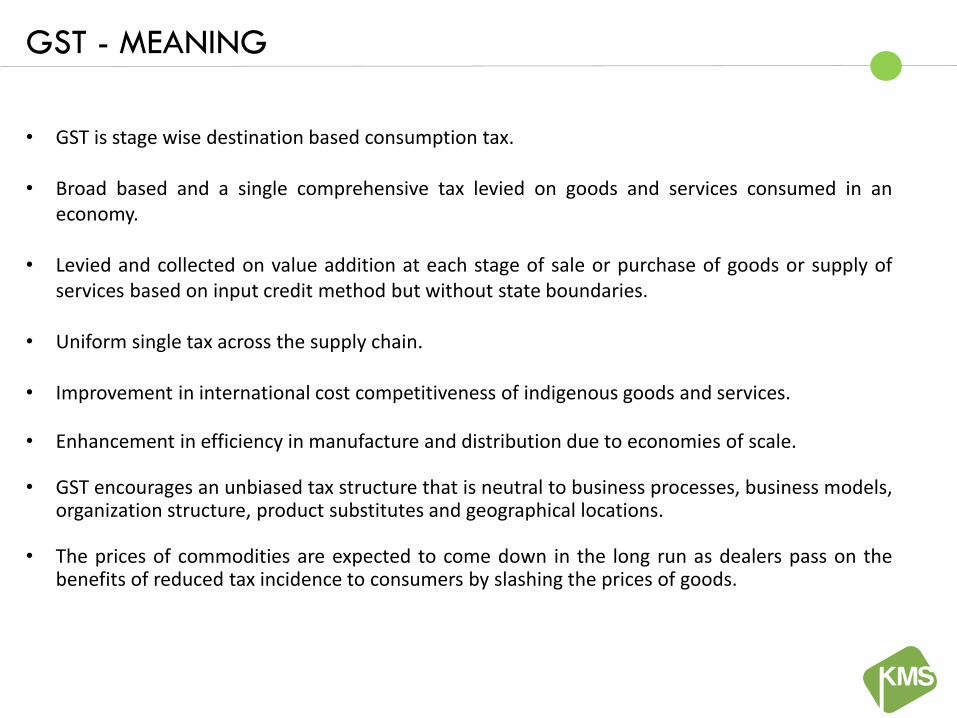

GST - MEANING

• GST is stage wise destination based consumption tax.

• Broad based and a single comprehensive tax levied on goods and services consumed in aneconomy.

• Levied and collected on value addition at each stage of sale or purchase of goods or supply ofservices based on input credit method but without state boundaries.

• Uniform single tax across the supply chain.

• Improvement in international cost competitiveness of indigenous goods and services.

• Enhancement in efficiency in manufacture and distribution due to economies of scale.

• GST encourages an unbiased tax structure that is neutral to business processes, business models,organization structure, product substitutes and geographical locations.

• The prices of commodities are expected to come down in the long run as dealers pass on thebenefits of reduced tax incidence to consumers by slashing the prices of goods.

6

Intra-state Supply of Goods and Services

•Central GST

•State GST

Inter-state Supply of Goods and Services

• IGST

•1% Additional Tax on Supply of Goods

Imports

•Basic Customs Duty

• IGST (in place of CVD and SAD)

Exports

•Zero Rated

Excise Duty – Manufacturing of GoodsVAT / CST – Sale of GoodsService Tax – Provision of Services

DUAL GST : BASIC PROPOSED STRUCTURE

7

8

Summary…

Sr. No. Situation Supply Tax

1 Location of Supplier and Place of Supply in same State

Intra State CGST & SGST

2 Location of Supplier and Place of Supply in different States

Inter State IGST

3 Import of Goods or Services from outside India

Inter State IGST

4 Location of Supplier in India and Place of Supply outside India

Exports Zero Rated

PROBABLE RATE STRUCTURE IN GST

SGST (+) CGSTTotal Rate %

Goods and Services

Exempted Basic Education, Healthcare, Agriculture related, Public Transport etc.

Zero RatedEssential items including food grains, 50% of items under Consumer PriceIndex (CPI), Export of Goods and Services

5% Gold and Silver ornaments, precious and semi-precious stones

12% Rate for Basic Commodities

18% Standard Goods and Services

28% Items currently taxable with 30-31% like partial luxury items

28% + Cess Luxury & De-merit goods (Like Luxury Cars, Tobacco, Cigarettes)

Will be brought in GST at a later Stage

Petroleum and Petroleum products

Out of GST Alcoholic Liquor for Human Consumption

9

CHALLENGES

Multiple levies & Compliances at

State and Centre Levels

Overlapping of tax in various transactions

Complex Laws on movement of

Goods –

Form C,F…

Cascading of Taxes

Ineligibility of ITC for SPs & CENVAT

for Traders

Disputes of Classification, Valuation &

Credit Eligibility

CHALLENGES IN CURRENT INDIRECT TAX STRUCTURE

10

CENTRAL LEVIES

Excise Duty

@ 12.50%

Service Tax

@ 15%

CVD @ 12.50% / SAD @ 4%

Central Sales Tax @ 2%

GST

Customs Duty

Customs Duty

State VAT

@ 5% - 15%

Entry/ Purchase Tax

Octroi / LBT

Luxury / Entertainment Tax

@ 5% - 25%

GST

STATE LEVIES

11

12

TAXES NOT SUBSUMED IN GST

TAXES TO REMAIN IN GST

Property Tax &Stamp Duty

ElectricityDuty

Professional Tax

Excise Duty on Alcohol for

Human Consumption

CustomsDuty

Excise Duty on PetroleumProducts

Entitlement/Obligations - Present Laws and GST

13

Particulars VAT Excise Service Tax

GST

Allowance of Input Tax Credit (ITC) of pre-registration period No Yes Yes No

Allowance of Input Tax Credit when supplier does not discharge his liability

*No Yes Yes No

Allowance of ITC of tax paid on inter-state transactions No NA NA Yes

Refund of ITC to exporters Yes Yes Yes Yes

Refund of accumulated ITC due to inverted rate structure Yes No No Yes

Option of Revised Return Yes Yes Yes No

Rectification of Filed Returns No No No Yes

Matching of Invoices and Recovering tax from purchasers in case of mismatch

*Yes No No Yes

Reverse Charge Mechanism (RCM) for Goods No No NA Yes

Reverse Charge Mechanism (RCM) for Services NA NA Yes Yes

Partial Reverse Charge Mechanism (RCM) for services NA NA Yes No

* In some states such as Gujarat and Maharashtra

Entitlement/Obligations - Present laws and GST

14

Particulars VAT Excise Service Tax

GST

Tax on Advance Receipts No No Yes Yes

Power to reject transaction value declared in invoice* No No No No

Centralised Registration No No Yes No

Inclusion of free supplies in the taxable value No Yes Yes Yes

Inclusion of incidental expenses in the taxable value Yes Yes Yes Yes

Tax on Distribution of free samples No Yes NA No

MRP based valuation No Yes No No

Specific valuation in case of Related Party Transactions* No Yes No No

Post supply Discounts / Incentives not known at the time of supply to be included in transaction value

No Yes No Yes

* The same provision was there in earlier MGL. But, the same has not incorporated in Revised MGL.

FORMATION

• Provide common PAN-based registration

• Enable returns filing and paymentsprocessing for all States on a sharedplatform

• Ensure integration of the common GSTPortal with the existing tax administrationsystems of the Central / State Governmentsand other stake holders

• Build efficient and convenient interfaceswith tax payers to increase tax compliance

• Carry out research, study best practices andprovide training to the stakeholders

• Special Purpose Vehicle (GSTN-SPV) has beenset up to create enabling environment forsmooth introduction of GST

• GSTN-SPV will provide IT infrastructure andservices to various stakeholders including theCentre and the States

• Strategic control over GSTN-SPV has beenensured with the Government due tosensitivity of role of GSTN-SPV and theinformation which would be available with it

• GSTN-SPV has been incorporated as a not-for-profit, non-Government, private limitedcompany with 49% equity held by theGovernment and 51% equity held by the non-Government institutions

GST NETWORK – GSTN SPV

ROLES & RESPONSIBILITY

15

STAKEHOLDERS OF GSTN

GSTN

State Tax Authorities

Central Tax Authorities

SME Taxpayers

Corporate Taxpayers

Facilitation Agencies

Banks

GSTN

Registration

Returns

GST Payment

Refunds

Audits

Appeals

STAKEHOLDERS WORKFLOW

16

LEVY IN GST REGIME

17

MEANING AND SCOPE OF SUPPLY

Supply includes

18

For consideration & for business

• Sale

• Barter

• Transfer

• Exchange

• License

• Rental

• Lease

• Disposal

For consideration whether or not for business

• Importation of service for Consideration

Supply without consideration (Schedule-I)

• Permanent transfer/disposal of business assets only where ITC has been availed

• Supply b/w related persons and distinct person as specified

• Supply of goods by agent to principal and vice-versa

• Importation of service from related person or any of his other establishment o/s India in course or furtherance of business

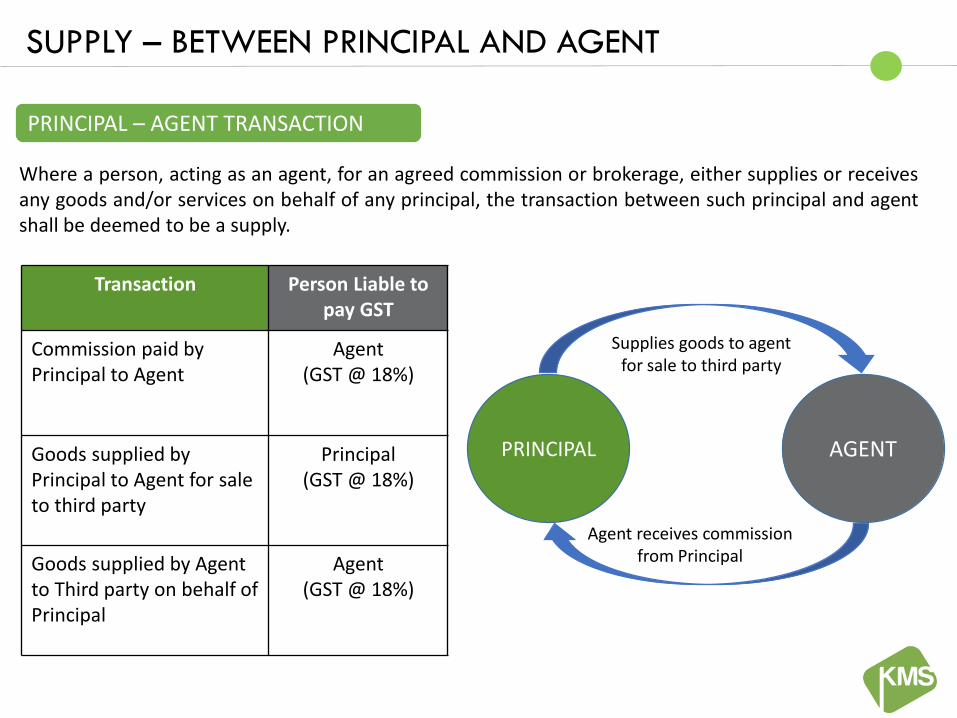

SUPPLY – BETWEEN PRINCIPAL AND AGENT

Where a person, acting as an agent, for an agreed commission or brokerage, either supplies or receivesany goods and/or services on behalf of any principal, the transaction between such principal and agentshall be deemed to be a supply.

PRINCIPAL – AGENT TRANSACTION

PRINCIPAL AGENT

Supplies goods to agent for sale to third party

Agent receives commission from Principal

Transaction Person Liable to pay GST

Commission paid by Principal to Agent

Agent (GST @ 18%)

Goods supplied by Principal to Agent for sale to third party

Principal(GST @ 18%)

Goods supplied by Agent to Third party on behalf of Principal

Agent(GST @ 18%)

GIST OF SCHEDULE – II – GOODS VS. SERVICE

20

Service

• Transfer of goods without transfer in title thereof

• Transfer of business assets for private use with or without consideration

• Lease, tenancy, license to occupy land

• Lease or letting out of commercial or residential building

• Treatment or process which is applied to another person’s goods

• Declared list of service viz. Works Contract Service, Construction Services, IT Services, Restaurant and Outdoor Catering Service

Goods

•Transfer in title in goods

•Supply of goods by unincorporated association of body to their members for consideration

•Transfer of business assets except transfer made for the private use with or without consideration

GST SUPPLY CHAIN – LAY OUT

Supplier

DistributorOverseas Supplier

Customer

Distributor

Factory

Gujarat Maharashtra

Outside India

Import

Overseas CustomerExport (Zero Rated)

Purchase

CGST + SGST

Trfin

Gu

jarat

No

Tax

Sale

CG

ST + SGST

Transfer

IGST

Sale

IGST

Sale

CGST + SGST

Warehouse

Warehouse

BCD - Cost

IGST - Credit

India

21

TIME & PLACE OF SUPPLY OF GOODS

& SERVICES

22

TIME OF SUPPLY OF GOODS

23

Earliest of :

• Date of issue of invoice or last date of invoice required to issue

- Invoice shall issue on date of removal of goods or date on which goods made available to recipient

• Date on which supplier receives payment

Normal/

Continuous Supply

Earliest of :

• Date of receipt of goods

• Date of payment - earlier of entered in books or debited in bank

• Date immediately following thirty days from the date of issue of invoice by the supplier

• Any other case – date of entry in books of recipient

Reverse charge

• Incase of supply of vouchers, supply shall be

• date of issue of voucher, if supply is identifiable at that point or

• the date of redemption of voucher, in all other cases

• If time of supply is not determinable

• in a case where a periodical return has to be filed, be the date on which such return is to be filed, or

• in any other case, be the date on which the CGST/SGST is paid

Other cases

TIME OF SUPPLY OF SERVICES

24

Earliest of :

• Date of issue of invoice or last date of invoice required to issue

- Invoice shall issue before or after the provision of service but within period prescribed

• Date on which supplier receives payment

Normal/

Continuous Supply

Earliest of :

• Date of payment - earlier of entered in books or debited in bank

• Date immediately following Sixty days from the date of issue of invoice by the supplier

• Any other case – date of entry in books of recipient

Reverse charge

• Incase of supply of vouchers, supply shall be

• date of issue of voucher, if supply is identifiable at that point or

• the date of redemption of voucher, in all other cases

• If time of supply is not determinable

• in a case where a periodical return has to be filed, be the date on which such return is to be filed, or

• in any other case, be the date on which the CGST/SGST is paid

Other cases

PLACE OF SUPPLY OF GOODS (OTHER THAN IMPORT & EXPORT)

25

• Place where movement of goods terminate

Movement of goods

• Location of such Third person

Supply on direction of Third

person

• Location of goods at time of delivery to recipient

Supply without movement

• Location at which goods are taken on board

Supply on Board Conveyance

• As per law of Parliament based on Council’s suggestion

Others

PLACE OF SUPPLY OF GOODS FOR IMPORT & EXPORT

26

Import of goods in India –

Location of ImporterExport of goods o/s India –

Location of Exporter

PLACE OF SUPPLY OF SERVICES

Particulars Place of supply

General Provision Supply to Registered Person - Location of such person Supply to any other person - Location of recipient of services

where the address is on record; and in other cases locationof supplier of service

Immovable property Location of such property, and if the same is o/s India then,Location of recipient

Restaurant, personal grooming, fitness etc.

Location where the services are performed

Training service Where supplied to a registered person, location of suchperson

Any other person, location where services are performed

Admission to a cultural, sporting event etc.

Location where event is actually held

Organization of a cultural, sporting event etc.

Supply to Registered Person - Location of such person Supply to any other person - Location where event is held If event is held o/s India – Location of recipient

Goods Transportation Service including mail & courier

Supply to Registered Person - Location of such person Supply to any other person - Location where goods are

handed over for their transportation27

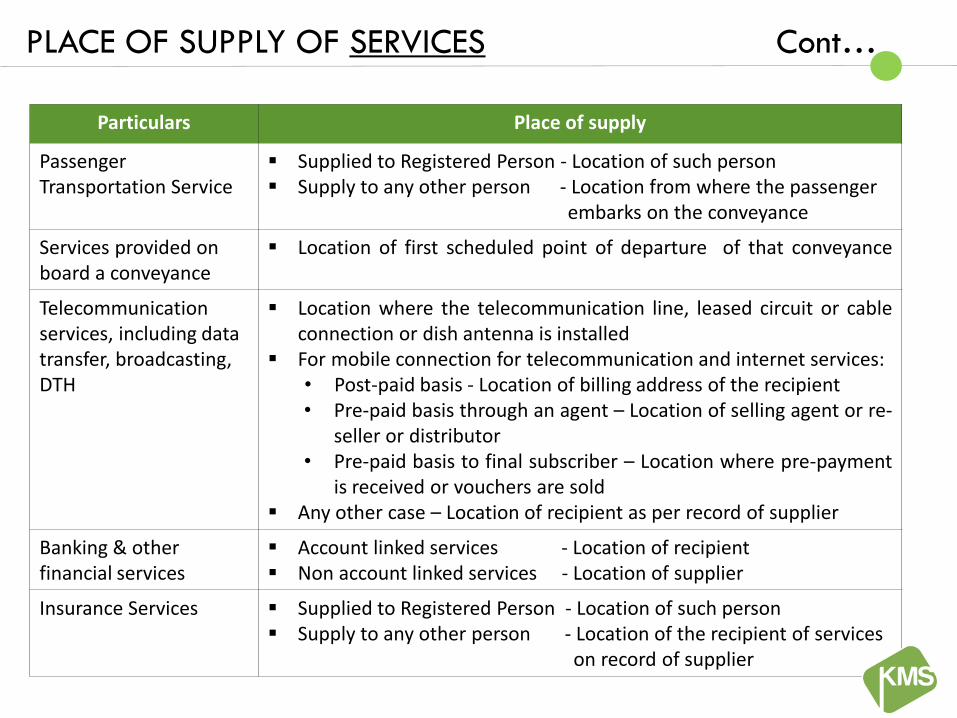

PLACE OF SUPPLY OF SERVICES Cont…

Particulars Place of supply

Passenger Transportation Service

Supplied to Registered Person - Location of such person Supply to any other person - Location from where the passenger

embarks on the conveyance

Services provided on board a conveyance

Location of first scheduled point of departure of that conveyance

Telecommunication services, including data transfer, broadcasting, DTH

Location where the telecommunication line, leased circuit or cableconnection or dish antenna is installed

For mobile connection for telecommunication and internet services:• Post-paid basis - Location of billing address of the recipient• Pre-paid basis through an agent – Location of selling agent or re-

seller or distributor• Pre-paid basis to final subscriber – Location where pre-payment

is received or vouchers are sold Any other case – Location of recipient as per record of supplier

Banking & other financial services

Account linked services - Location of recipient Non account linked services - Location of supplier

Insurance Services Supplied to Registered Person - Location of such person Supply to any other person - Location of the recipient of services

on record of supplier28

VALUATION RULES

29

VALUATION OF SUPPLY

Value of supply

30

Transaction Value, subject to • Unrelated Parties• Price is sole consideration

Transaction Value

• Shall Include

• Taxes and duties other than GST

• Amount paid by recipient instead of supplier and not included in price

• Incidental costs/ expenses (such as commission, packing, royalties etc.)

• Interest or late fee or penalty for delayed payment of any consideration

• Subsidies directly linked to the price except for Central / State Government subsidies

• Shall not Include

• Any discount allowed before or at the time of supply as recorded in invoice

• Post Supply Discount provided

• Discount is as per agreement entered into / before supply

• Discount is specifically linked to relevant invoices

• Input Tax Credit is reversed by recipient as is attributable to the discount

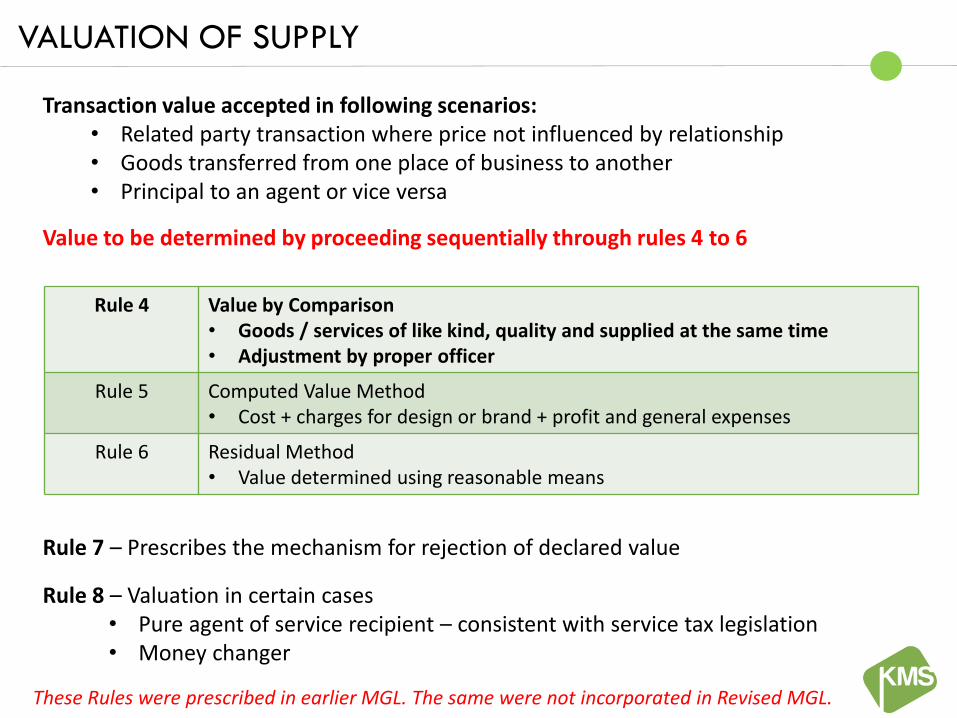

Transaction value accepted in following scenarios: • Related party transaction where price not influenced by relationship • Goods transferred from one place of business to another• Principal to an agent or vice versa

Value to be determined by proceeding sequentially through rules 4 to 6

Rule 7 – Prescribes the mechanism for rejection of declared value

Rule 8 – Valuation in certain cases • Pure agent of service recipient – consistent with service tax legislation • Money changer

VALUATION OF SUPPLY

Rule 4 Value by Comparison • Goods / services of like kind, quality and supplied at the same time • Adjustment by proper officer

Rule 5 Computed Value Method • Cost + charges for design or brand + profit and general expenses

Rule 6 Residual Method• Value determined using reasonable means

These Rules were prescribed in earlier MGL. The same were not incorporated in Revised MGL.

INPUT TAX CREDIT (ITC)

32

CASCADING OF TAX - PRESENT TAX STRUCTURE

33

Input CENVAT(Service Tax + Excise Duty)

Input Tax Credit of VAT

Input CST – Always a COST

(Service Tax + Excise Duty) Liability

VAT Liability

CST Liability

Credit available

Credit not available

Cascading Impact – Burden of Tax on Tax

Non – availability of VAT credit against Service Tax / Excise liability and vice-versa

Non – availability of CST credit against any liability

34

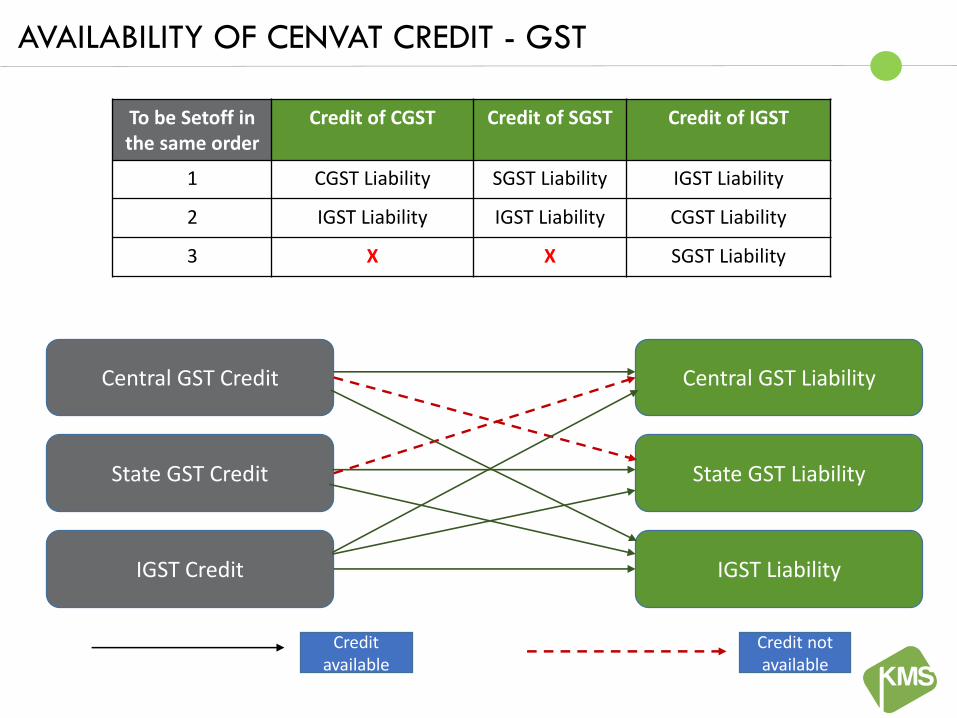

Central GST Credit

State GST Credit

IGST Credit

Central GST Liability

State GST Liability

IGST Liability

Credit available

Credit not available

AVAILABILITY OF CENVAT CREDIT - GST

To be Setoff in the same order

Credit of CGST Credit of SGST Credit of IGST

1 CGST Liability SGST Liability IGST Liability

2 IGST Liability IGST Liability CGST Liability

3 X X SGST Liability

AVAILABILITY OF CENVAT CREDIT - GST

CreditLiability

Gujarat SGST

GujaratCGST

Gujarat IGST

MaharashtraSGST

Maharashtra CGST

Maharashtra IGST

Gujarat SGST a X a X X X

Gujarat CGST X a a X X X

Gujarat IGST a a a X X X

Maharashtra SGST X X X a X a

Maharashtra CGST X X X X a a

Maharashtra IGST X X X a a a

INPUT TAX CREDIT

Credit in respect of any invoice or debit note pertaining to a financial year cannot betaken after

• Filing of return for the month of September following the end of financial yearto which such invoice or debit note pertains, or;

• Filing of the relevant annual return, whichever is earlier

Credit not admissible on such tax component of the cost of capital goods, for whichdepreciation has been claimed under the Income Tax Act, 1961 .

In case of supply of capital goods on which input tax credit has been taken, paymentis required to be made

• for an amount equal to input tax credit reduced by percentage as may bespecified, or;

• tax on the transaction value of such capital goods, whichever is higher

Time limit

Capital Goods

36

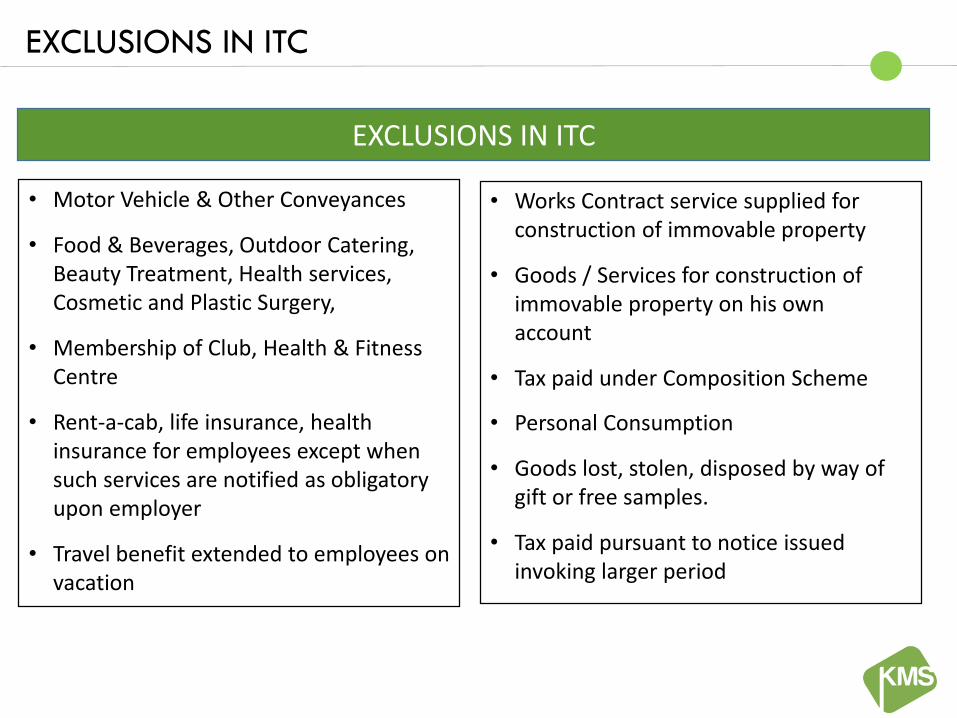

EXCLUSIONS IN ITC

EXCLUSIONS IN ITC

• Motor Vehicle & Other Conveyances

• Food & Beverages, Outdoor Catering, Beauty Treatment, Health services, Cosmetic and Plastic Surgery,

• Membership of Club, Health & Fitness Centre

• Rent-a-cab, life insurance, health insurance for employees except when such services are notified as obligatory upon employer

• Travel benefit extended to employees on vacation

• Works Contract service supplied for construction of immovable property

• Goods / Services for construction of immovable property on his own account

• Tax paid under Composition Scheme

• Personal Consumption

• Goods lost, stolen, disposed by way of gift or free samples.

• Tax paid pursuant to notice issued invoking larger period

ITC IN RESPECT OF STOCK

Entitlement of Credit of input tax in respect of input held in stock and Inputs contained in Semi Finished or Finished Goods

Person Eligible Point in Time

Person who has applied for registration within 30 days from the date he become liable and has been granted certificate of registration

On the day immediately preceding the date from which he becomes liable to pay tax

Person who has taken Voluntary Registration u/s. 23(3) of GST Act

On the day Immediately preceding the date of registration

Registered Taxable person ceases to pay tax u/s. 9 i.e. Composition Levy

On the day immediately preceding the date from which he becomes liable to pay tax u/s. 8

38

SWITCH OVER PROVISIONS

Registered Taxable person availing benefits of Input

Tax Credit (ITC)

Switches over as a taxable person paying tax u/s. 9 i.e. Composition levy

Goods / Services supplied by him become exempt absolutely u/s. 11

1. He shall pay an amount equal to the credit of input tax in respect ofinputs held in stock and inputs contained in semi finished or finishedgoods held in stock and on capital goods reduced by such prescribedpercentage points immediately preceding the date of such switchover or date of exemption.

2. Balance of Input tax credit, if any, lying in electronic credit ledgershall be lapsed.

39

REVERSAL OF ITC

ITC on Goods / Services

• Partly used for Business• Partly used for other

purpose

• Partly used for taxable supply

• Partly used for Exempt supply

ITC attributable to business purposes

will be eligible

ITC attributable to taxable supply will be eligible

Taxable supply shall include zero rated supply

40

GST ELECTRONIC CREDIT ALLOWED ON SUPPLY TRANSACTIONS

41

GSTN

Dealer A

Dealer BSupply along with Invoice

Cash Flow

Credit Flow

TAX ADMINISTRATION

42

REGISTRATION, PAYMENT & REFUND

State wise, Business vertical wise and Voluntary Registration options are available.

Concept of ISD continue.

Single threshold limit for goods and services. i.e. Rs. 20 Lakhs for normal category andRs. 10 Lakhs for Special category States & States specified under Article 279A(4)(g) of TheConstitution

Certain persons required to take compulsory registration. Such as Inter state supplier, Casualdealer, Person required to pay tax under RCM, Person paying TDS, Person acting agent, ISD,e-Commerce operator, Other persons to be notified by Government.

Registration

Payment

Single threshold limit for goods and services. i.e. Rs. 20 Lakhs for normal category andRs. 10 Lakhs for Northern Eastern State including Sikkim.

Three modes of payment of tax under GST regime are proposed i.e. through internet banking /credit or debit card, Over the Counter payment (upto Rs. 10,000 per challan) and paymentsthrough NEFT/RTGS.

The input tax credit as self-assessed in the return of a taxable person shall be credited to hiselectronic credit ledger to be maintained in the manner as may be prescribed.

43

REGISTRATION, PAYMENT & REFUND

Refund claim is required to be filed within 2 years from relevant date.

Refund order to be passed within 90 days from the date of receipt of application.

80% refund can be released provisionally and balance 20% after verification.

For refund application < Rs. 5 Lakhs only declaration & proof for incidence of tax is required.

Refund

44

Refund claim available in case of

ExportAccumulated credit due to inverted duty

structureDeemed Export

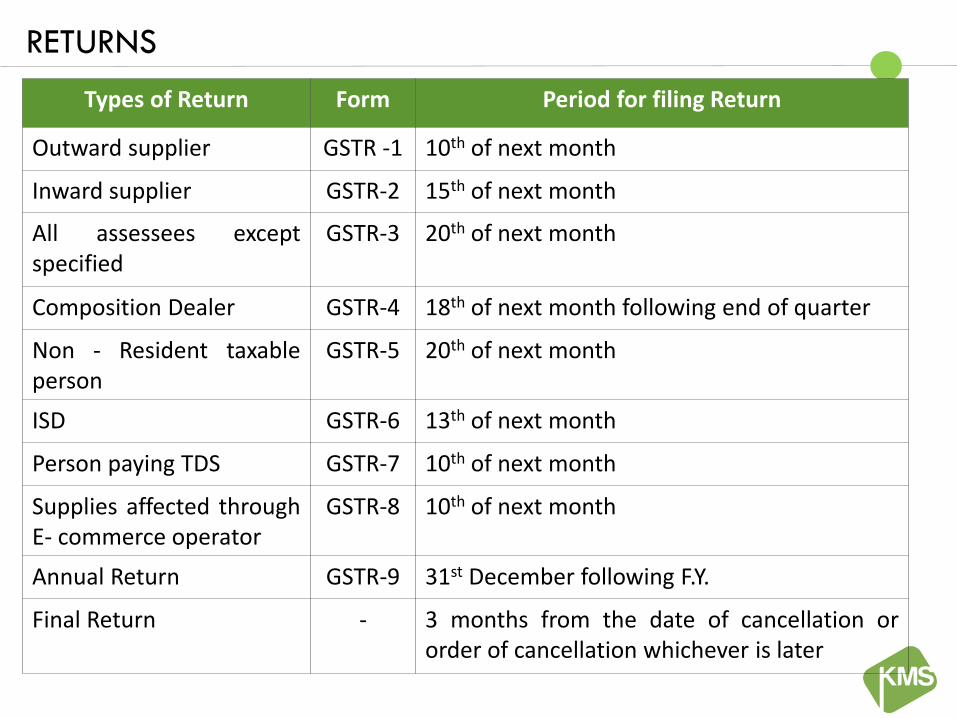

RETURNS

45

Types of Return Form Period for filing Return

Outward supplier GSTR -1 10th of next month

Inward supplier GSTR-2 15th of next month

All assessees exceptspecified

GSTR-3 20th of next month

Composition Dealer GSTR-4 18th of next month following end of quarter

Non - Resident taxableperson

GSTR-5 20th of next month

ISD GSTR-6 13th of next month

Person paying TDS GSTR-7 10th of next month

Supplies affected throughE- commerce operator

GSTR-8 10th of next month

Annual Return GSTR-9 31st December following F.Y.

Final Return - 3 months from the date of cancellation ororder of cancellation whichever is later

46

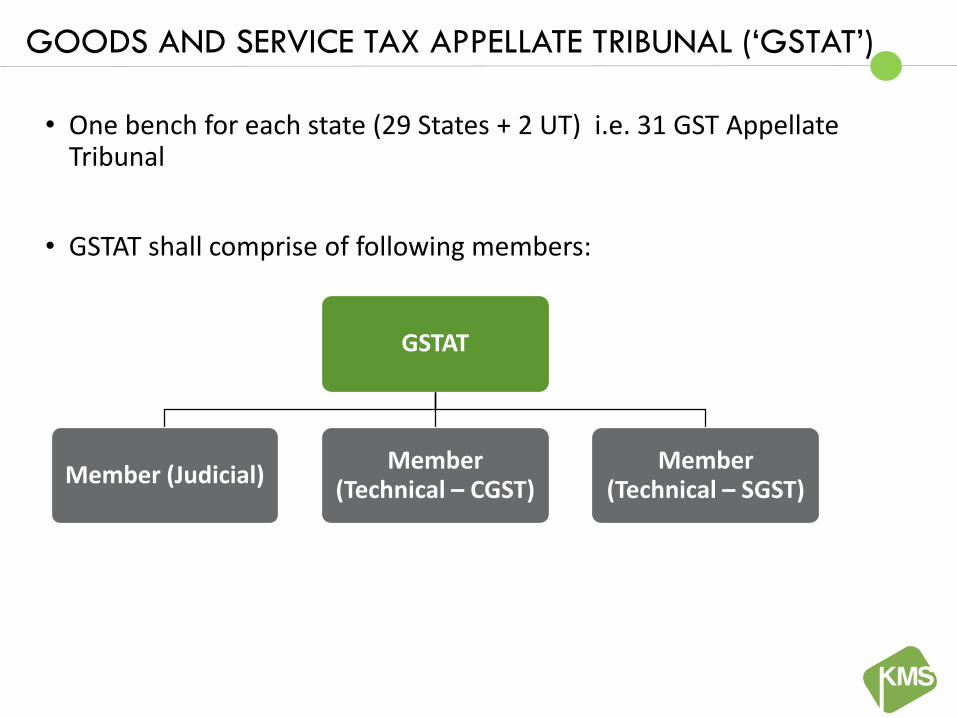

GOODS AND SERVICE TAX APPELLATE TRIBUNAL (‘GSTAT’)

• One bench for each state (29 States + 2 UT) i.e. 31 GST Appellate Tribunal

• GSTAT shall comprise of following members:

GSTAT

Member (Judicial)Member

(Technical – CGST)Member

(Technical – SGST)

TRANSITIONAL PROVISIONS

47

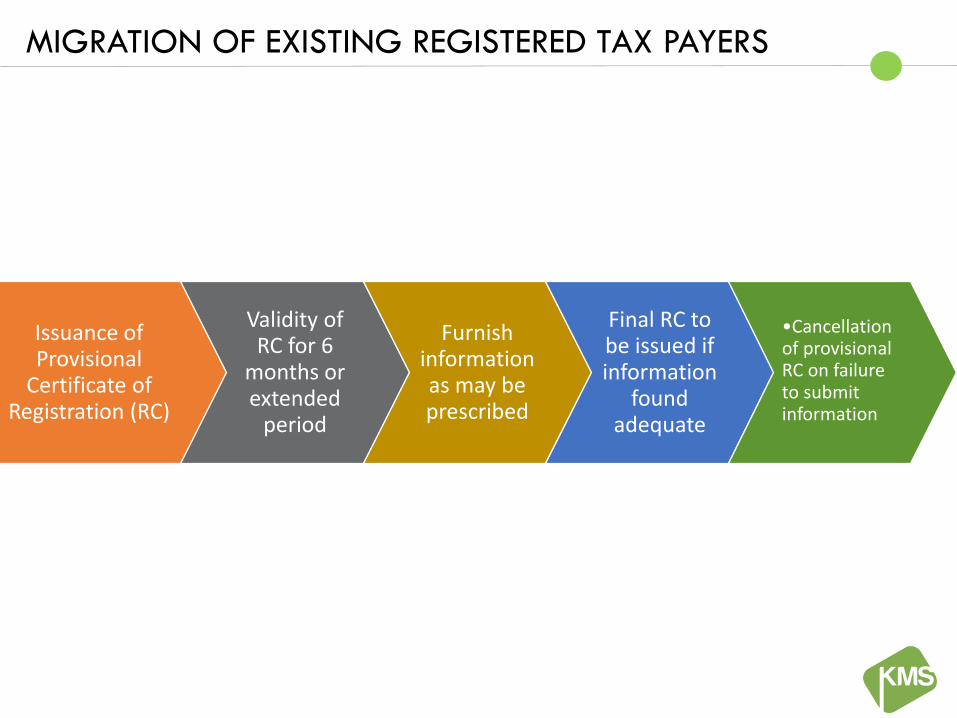

MIGRATION OF EXISTING REGISTERED TAX PAYERS

Issuance of Provisional

Certificate of Registration (RC)

Validity of RC for 6

months or extended

period

Furnish information as may be prescribed

Final RC to be issued if information

found adequate

•Cancellation of provisional RC on failure to submit information

48

STATE WISE ENROLMENT SCHEDULE

Government has started phase wise GST enrolment process of existing taxpayers for onlyexisting VAT registered taxpayers.

49

States / Union Territories Start Date End Date

Puducherry, Sikkim 08/11/2016 23/11/2016

Maharashtra*, Goa, Daman and Diu, Dadra Nagar Haveli, Chhattisgarh 14/11/2016 29/11/2016

Gujarat* 15/11/2016 30/11/2016

Odisha, Jharkhand, Bihar, West Bengal, Madhya Pradesh, Assam, Tripura,

Meghalaya, Nagaland, Arunachal Pradesh, Manipur, Mizoram

30/11/2016 15/12/2016

Uttar Pradesh, Jammu and Kashmir, Delhi, Chandigarh, Haryana, Punjab,

Uttarakhand, Himachal Pradesh, Rajasthan

16/12/2016 31/12/2016

Kerala, Tamil Nadu, Karnataka, Telangana, Andhra Pradesh 01/01/2017 15/01/2017

Service Tax / Excise Registrants not registered under State VAT Act 01/01/2017 31/01/2017

Delta All Registrants (All Groups) 01/02/2017 20/03/2017

The window will be open till 31/01/2017 for those who miss the chance.

* Extended upto 07.12.2016

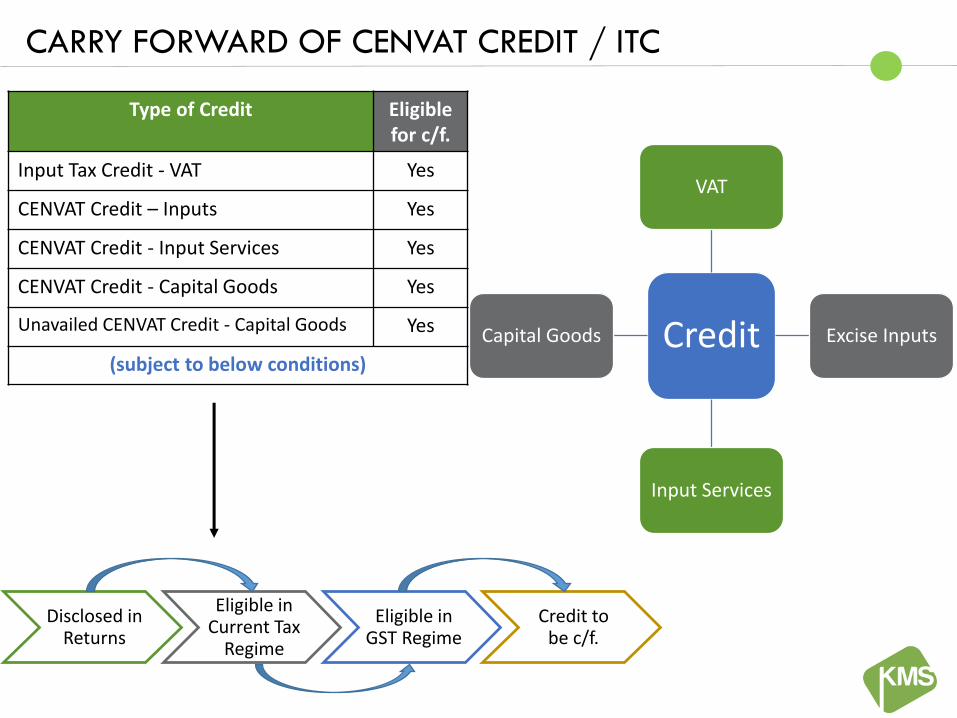

CARRY FORWARD OF CENVAT CREDIT / ITC

•Amount of eligible CENVAT credit, VAT and Entry Tax# carried forward as per earlier law in return filed for the period ending immediately prior to appointed day

•Such credit shall also be eligible under GST Regime

Amount of CENVAT Credit / ITC to be allowed to registered taxable

person

• Un-availed CENVAT credit not carried forward in return filed for the period ending immediately prior to appointed day under earlier law

• Such credit shall also be eligible under GST Regime

Amount of un-availed* CENVATcredit of Capital goods to be allowed to registered taxable

person under GST

50

# Under VAT / Entry Tax, return shall be filed within 90 days of the appointed date

*Un-availed amount of CENVAT credit in respect of Capital goods = Aggregate amount of CENVAT Credit (-) Credit already availed in respect of capital goods in earlier return

CARRY FORWARD OF CENVAT CREDIT / ITC

Credit

VAT

Excise Inputs

Input Services

Capital Goods

Disclosed in Returns

Eligible in Current Tax

Regime

Eligible in GST Regime

Credit to be c/f.

Type of Credit Eligiblefor c/f.

Input Tax Credit - VAT Yes

CENVAT Credit – Inputs Yes

CENVAT Credit - Input Services Yes

CENVAT Credit - Capital Goods Yes

Unavailed CENVAT Credit - Capital Goods Yes

(subject to below conditions)

ELIGIBILITY OF CENVAT CREDIT / ITC FOR INPUTS IN STOCK

Category of Persons

Registered taxable personunder GST who :

• Was not liable to registerunder earlier law

• Is engaged inmanufacturing of exemptgoods or provision ofexempted service underearlier law

• Is engaged inmanufacturing of exemptedas well as taxable goods orproviding taxable as well asnon-taxable service

• Has availed benefit ofcomposition scheme underearlier law

• Was providing WorksContract Service by availingabatement benefit

• Is first stage dealer or asecond stage dealer orregistered Importer

Taxes in respect of:

• inputs held in stock onappointed date

• inputs contained in semi-finished or finished goodsheld in stock on appointeddate

Intended to be used formaking taxable supplies

Not availed CENVAT creditunder earlier law due to abovementioned situations

The said taxable person passeson the benefit of such creditby way of reduced prices tothe recipient

Not paying tax undercomposition scheme in GSTregime

Eligible CENVAT credit underGST regime also

Possession of invoice issuedwhich is not earlier thantwelve months immediatelypreceding appointed day

The suppliers of services is noteligible for any abatementunder GST regime

Eligible Duties & Taxes Conditions

52

ELIGIBLE DUTIES AND TAXES TO BE CARRIED FORWARD

Service Tax

Excise Duty

Additional Excise Duty on Textile

and Textile Articles

Additional Excise Duty on Goods of

Special Importance

COUNTER-VAILING

DUTY (CVD)

National Calamity

Contingent Duty

Whether Krishi Kalyan Cess (KKC) to be carried forward in GST regime ? 53

SPECIAL ADDITONAL DUTY (SAD)

Tax paid on Goods / Capital Goods lying with Agent (only SGST)

Sr.

No.

Tax paid on goods lying with agents on the appointed day to be allowed as credit to agent

GOODS CAPITAL GOODS

1 The agent is a registered taxable person under GST

2 Both the principal and the agent declare the details of stock of Goods / Capital Goods lying with

such agent on the date immediately preceding the appointed day

3 The invoices for such Goods / Capital Goods had been issued not earlier than twelve months

immediately preceding the appointed day

4 The principal has either reversed or not

availed of the input tax credit in respect of

such goods.

The principal has either not availed the input tax

credit in respect of such capital goods or, having

availed such credit, has reversed the said credit,

to the extent availed by him.

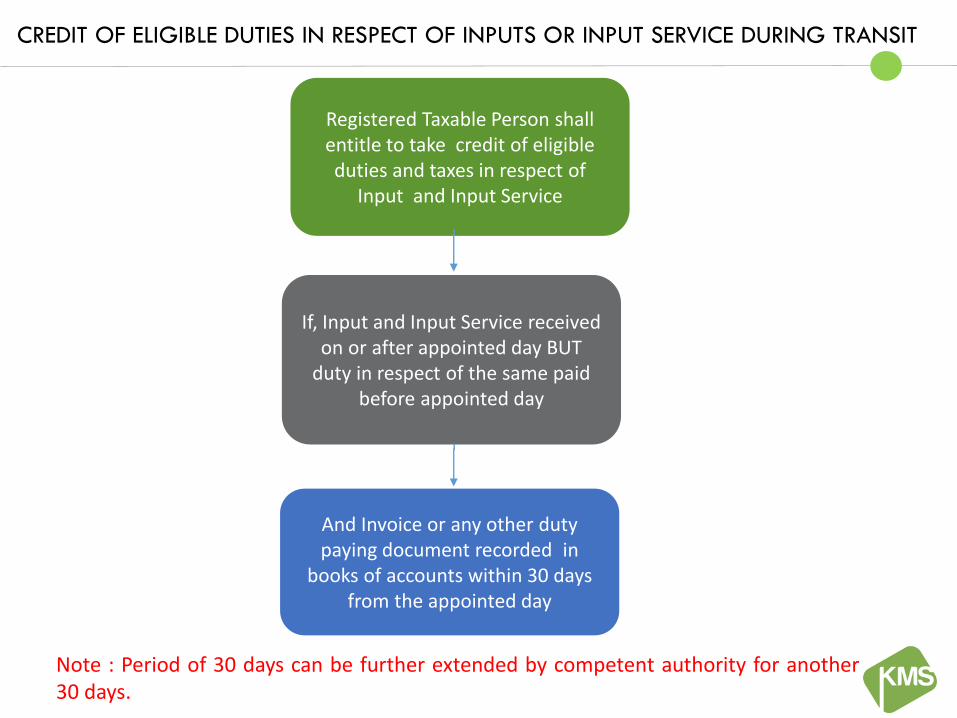

CREDIT OF ELIGIBLE DUTIES IN RESPECT OF INPUTS OR INPUT SERVICE DURING TRANSIT

Registered Taxable Person shall entitle to take credit of eligible duties and taxes in respect of

Input and Input Service

If, Input and Input Service received on or after appointed day BUT

duty in respect of the same paid before appointed day

And Invoice or any other duty paying document recorded in

books of accounts within 30 days from the appointed day

55Note : Period of 30 days can be further extended by competent authority for another30 days.

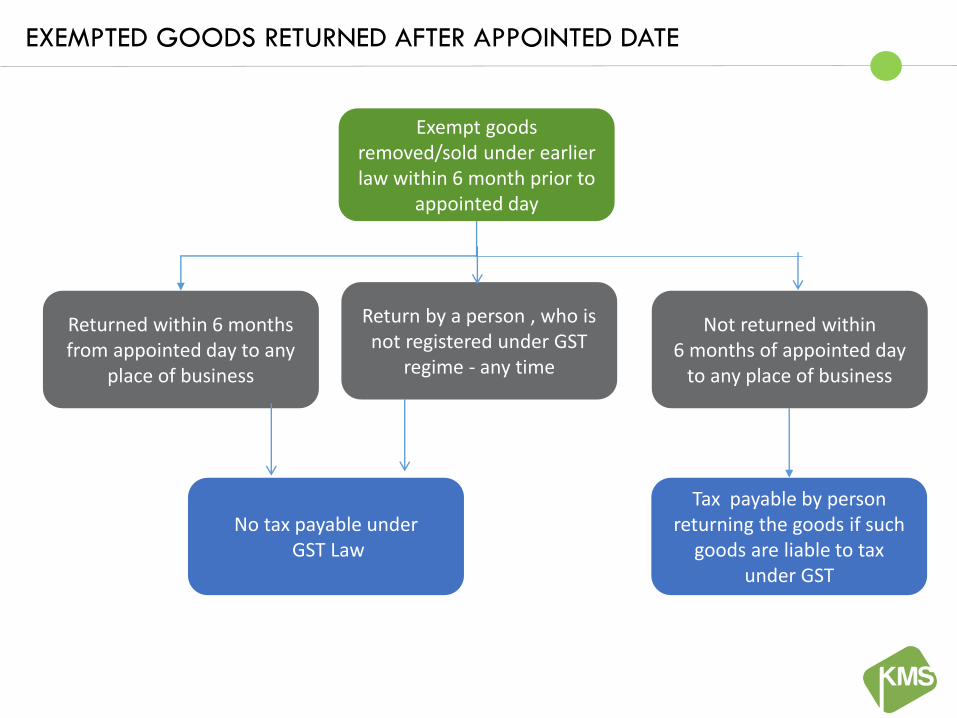

EXEMPTED GOODS RETURNED AFTER APPOINTED DATE

Exempt goods removed/sold under earlier law within 6 month prior to

appointed day

Returned within 6 months from appointed day to any

place of business

Not returned within 6 months of appointed day

to any place of business

No tax payable underGST Law

Tax payable by person returning the goods if such

goods are liable to tax under GST

56

Return by a person , who is not registered under GST

regime - any time

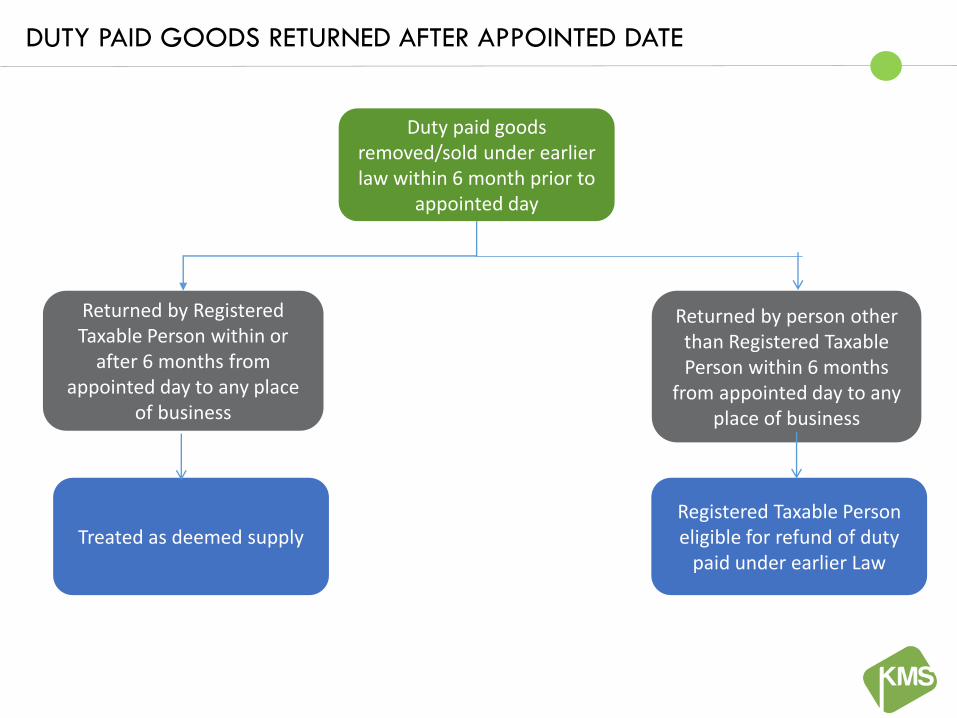

DUTY PAID GOODS RETURNED AFTER APPOINTED DATE

Duty paid goods removed/sold under earlier law within 6 month prior to

appointed day

Returned by Registered Taxable Person within or

after 6 months from appointed day to any place

of business

Returned by person other than Registered Taxable Person within 6 months

from appointed day to any place of business

Treated as deemed supplyRegistered Taxable Person eligible for refund of duty

paid under earlier Law

57

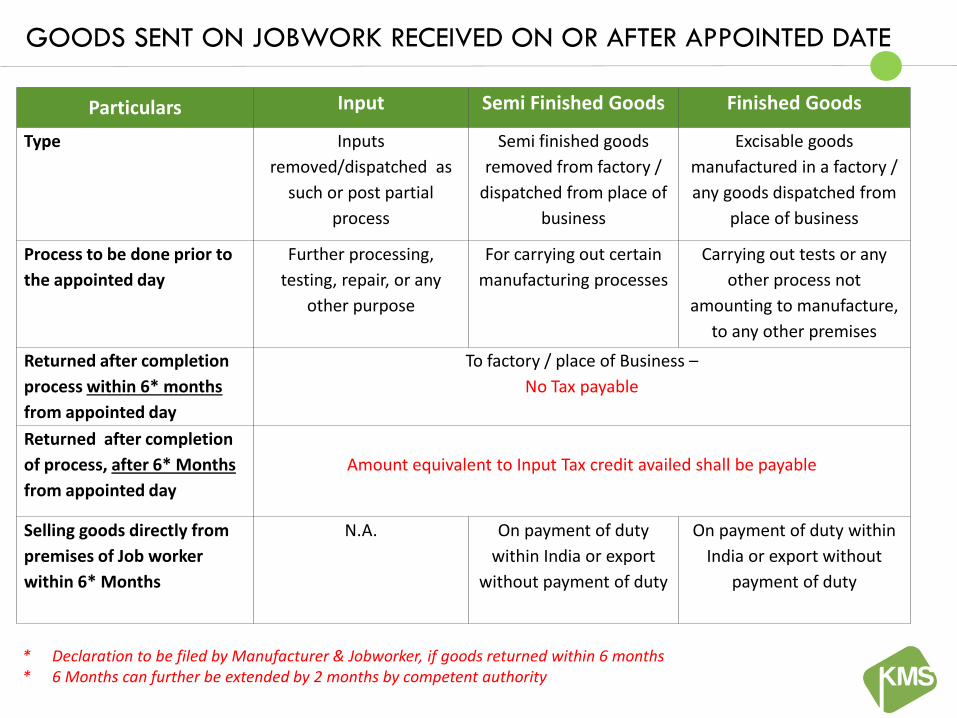

GOODS SENT ON JOBWORK RECEIVED ON OR AFTER APPOINTED DATE

Particulars Input Semi Finished Goods Finished Goods

Type Inputs

removed/dispatched as

such or post partial

process

Semi finished goods

removed from factory /

dispatched from place of

business

Excisable goods

manufactured in a factory /

any goods dispatched from

place of business

Process to be done prior to

the appointed day

Further processing,

testing, repair, or any

other purpose

For carrying out certain

manufacturing processes

Carrying out tests or any

other process not

amounting to manufacture,

to any other premises

Returned after completion

process within 6* months

from appointed day

To factory / place of Business –

No Tax payable

Returned after completion

of process, after 6* Months

from appointed day

Amount equivalent to Input Tax credit availed shall be payable

Selling goods directly from

premises of Job worker

within 6* Months

N.A. On payment of duty

within India or export

without payment of duty

On payment of duty within

India or export without

payment of duty

* Declaration to be filed by Manufacturer & Jobworker, if goods returned within 6 months* 6 Months can further be extended by 2 months by competent authority

PRICE REVISION IN EXISTING CONTRACT UNDER GST

A supplementary invoice ordebit note is required to beissued within 30 days of PriceRevision.

Tax is required to be paid to theextent revision under GSTregime.

A supplementary invoice orcredit note is required to beissued within 30 days of pricerevision

Tax liability to be reduced to theextent of revision under GSTregime.

UPWARD REVISION

DOWNWARDREVISION

BRANCH TRANSFER AND GOODS SENT ON APPROVAL BASIS

Treatment of Branch Transfers :

Treatment under SGST Amount of input tax credit reversed prior to the

appointed day shall not be admissible as credit of

input tax under this Act

Goods sent on Approval Basis :

Goods returned within 6*

months from appointed day

No tax payable

Goods returned post 6*

months from appointed day

Tax shall be payable by:

Person returning goods

Person who has sent goods on approval basis

60

* 6 Months can further be extended to 2 months by competent authority

IMPORT / INTERSTATE SUPPLY ON OR AFTER APPOINTED DATE

Transaction Liability of Tax payment under GST regime

Supply made on or after appointed date Liable to Tax

Transaction initiated on or beforeappointed date on which full tax hasbeen paid in earlier law

Not liable to Tax

Transaction initiated on or beforeappointed date on which partial tax hasbeen paid in earlier law

Liable to pay Tax to the extent of balance amount

Note: A transaction shall be deemed to have been initiated before the appointed day ifeither the invoice relating to such supply or payment, either in full or in part, has beenreceived or made before the appointed day.

61

VENDOR MANAGEMENT

62

WHAT IS VENDOR MANAGEMENT?

Vendor Management is ongoing management of third-party providers of product or service

• The goal of VM is to ensure the organization continuously obtains the best value from external

providers of products and services while controlling exposure to vendor-related risk.

Governance & Process

Select Vendors

Manage Vendor

Contracts

Manage Vendor Risk

Manage Vendor

Performance

Vendor Appraisal Reporting

Vendor Mgt.

Lifecycle

WHY IT IS IMPORTANT ?

Because we must measure, manage, and scrutinize the vendors we rely on to deliver value

Co-ordination

• Manage 500 to 5,000 vendors

• Continuous monitoring and follow-up with vendors

• Managerial Decision for continuous defaults by vendors

.Scarcity of Resources

• Increase in manpower to carry out co-ordination task with vendors

• Increase in Payroll Cost

Risk

• Hit on Cash Flow due to delay in availability of ITC

• Credit Risk due to non-payment of Tax / non-filing of Return by vendors

• Increase in Working Capital Requirement

Service Providers

Contractors

Joint

VenturesAgencies

Law Firms

KEY TAKEAWAYS

Assess / Monitor effectiveness of vendor post vendor selection stage (though

procedural but one of the important aspect of GST)

Fix financial terms with vendors based on GST Score Card Rating.

Familiarize with the latest regulatory guidance including procedural aspect

Include vendor risk management as a function within the vendor management

program

Ensure Vendor Compliance

Vendor Selection

Vendor Management

Vendor Reporting

66

GST IMPACT ON BUSINESS VERTICALS

Suppliers

• ITC Credit

Marketing

• Pricing Strategies

• Effect on demand

IT Systems & Human Resource

• Employee education

• System design

• Change Master Record

Supply Chain & Logistics

• Transaction Framework

• Warehousing

• Costing Analysis

Legal & Finance

• Cash Flow Impact

• Drafting Agreement

• Impact on existing contract

Customers

• Financing Model

• Offer Structure

GST RECONCILIATION

Particulars Amount (INR)

Amount (INR)

Sales as per financials statement 110.00

Add: Advances for goods recd. during the year (incl. GST) 25.00

GST on advances refunded 1.00

Branch Transfer Supply 20.00

Packing Charges (not forming part of sales) 5.50 51.50

Less: Advances refunded, if any (incl. GST) 5.00

GST on advances received 4.50

Export of Goods including deemed exports 15.00

Exempted Supply of Goods 5.00 29.50

Value of Supply liable for GST 132.00

GST Payable @ 18%Less: Input Tax Credit

23.7520.50

Net GST Payable 3.25

GST RECONCILIATION STATEMENT

(Rs. in Crores)

APPROACH TO GST

69

Mapping ‘As-Is’ Scenario

Impact Assessment

Implementation Go Live

Approach to GST Implementation

Mapping of ‘As-is’Business model

Tax implications onthe existing BusinessModel

Working out impact of Dual GST on ‘As-Is’ model

Transition of tax credits

Evaluation of options to optimize GST impact

Finalization of changes required

Adjust business structure / transactions

Assist for changes in ERP systems / processes

Review contractual arrangements with suppliers/ customers

Train Accounts, Finance and Taxation Team

Review of documentation

Review of Central and State GST Returns

Tax adjustments

Handholding Support

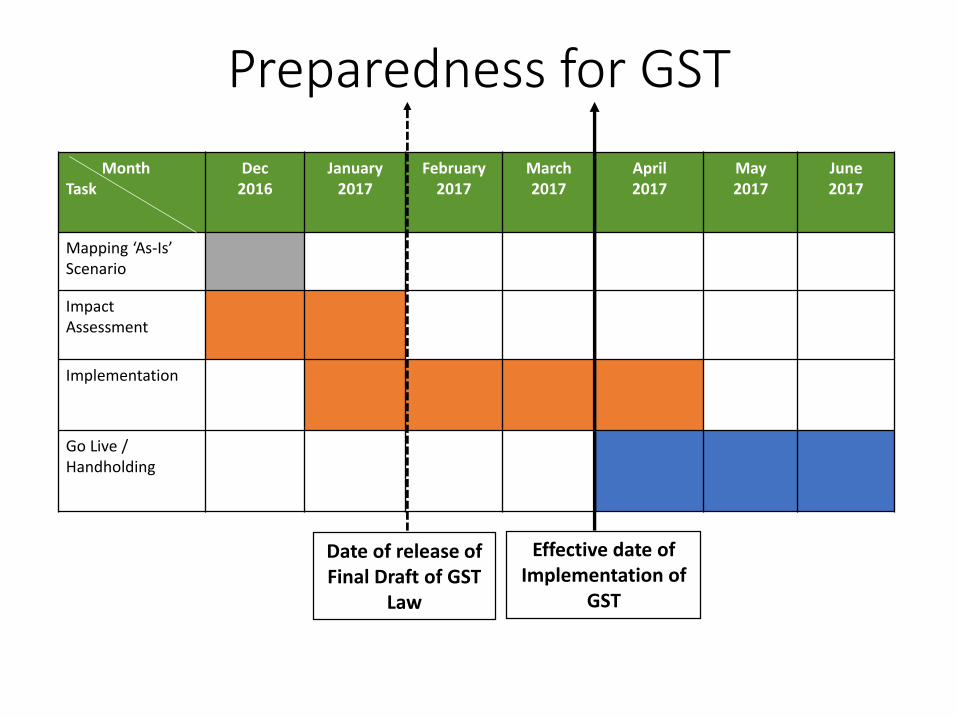

Preparedness for GST

MonthTask

Dec2016

January 2017

February 2017

March 2017

April 2017

May 2017

June 2017

Mapping ‘As-Is’ Scenario

Impact Assessment

Implementation

Go Live / Handholding

Date of release of Final Draft of GST

Law

Effective date of Implementation of

GST

SECTOR SPECIFIC IMPACT

72

Manufacturing Sector

Pharma Sector

Automobile Sector

Media and Entertainment Sector

Hospitality Sector

IT & ITES Sector

Turnkey Projects / EPC Sector

Real Estate Sector

Education Sector

Banking and Financial Sector

Logistics Sector

E-Commerce

KMS GST Tool

73

GST TOOL is a calculator for computing impact of proposed GST Model Law on Indirect Taxes levied onGoods and Services. It also gives a comparative result on taxes under current Indirect Tax regime andpost implementation of GST on ‘AS IS’ basis.

GST Impact Analyzer – Sensitivity Analyzer

Following Steps are required to be followed to achieve decisive analysis of GST :

• Download the Standard Input Data Template (SIDT) and provide the data in the format of thetemplate

• Upload the data of SIDT on GST Tool

• Tool will compute the comparable impact on Indirect Taxes under Existing Regime and GST Regime

• Reporting Option will allow the user to obtain the report of impact analysis conducted by tool inrequired and customized formats

KMS GST Tool

74

Thank YouCA. Amish Khandhar

Khandhar Mehta & Shah

3rd Floor, Devpath Complex,

Off C G Road, Bh. Lal Bunglow,

Ahmedabad – 380006

Gujarat – India

Phone : +91 79 66315450/51/52/53

Email : [email protected]

URL : www.kmsindia.in