Embed Size (px)

Citation preview

1

Mobilising resources for war in eighteenth century Netherlands. TheDutch financial revolution in comparative perspective1

Marjolein ’t HartUniversity of Amsterdam, [email protected]

Paper for the IEHA Congress in Helsinki (21-25 August 2006)Session 69 "Mobilising Money and Resources for War", 25 August 2006

The outstanding development of the seventeenth century Dutch Republic is a well-knownestablished fact. Recent historiography has stressed the powers and the relative efficiency ofthe decentralised Netherlands.2 Above all, the power of public credit allowed the Dutch tomaintain a big-power status in wars. The ease with which massive loans could be contracted,at relatively low rates of interest, had been labelled a ‘financial revolution’.3 Thanks to thispublic credit system troops were paid relatively on time, giving the United Provinces asignificant leverage over most of its competitors on the continent. The flow of funds alsoallowed for victories at sea, and the navy secured the Dutch international trade routes fordecades to come.

However, whereas the system of public credit of the seventeenth century has beenstudied in detail, little is known to what degree the system was actually continued in theeighteenth century. Historians have stressed the difficulties of the Dutch to maintain its big-power status, in particular after the War of Spanish Succession.4 Yet similar difficulties werealso encountered by all other belligerents. Actually, the 1720 burst of the Bubbles in Paris(John Law’s system) and London (South Sea Company) disrupted their respective systems ofpublic credit more as compared to Amsterdam.5

1 I am extremely grateful to Oscar Gelderblom and Joost Jonker (Utrecht University) for allowing me to use theirdata on the Rotterdam obligations. I also thank Richard Bakx (National Archives, The Hague) for approving myconsulting of a damaged book of the Holland obligations-accounts. This paper also profited from the commentsby several participants at the Second Low Countries Conference, April 20-21 Antwerp 2006, where I presentedsome of the data. Furthermore, Larry Neal, Ann Carlos, Kirsten Wandschneider, Oscar Gelderblom, Joost Jonkerand Wantje Fritschy allowed me to read their work prior to publication, which proved an enormous stimulus inwriting this paper.2 Griet Vermeesch, Oorlog, steden en staatsvorming. De grenssteden Gorinchem en Doesburg tijdens degeboorte-eeuw van de Republiek (1570-1680) (Amsterdam 2006); Wantje Fritschy, ‘The efficiency of taxation inHolland’, in: Oscar Gelderbom (ed.), The political economy of the Low Countries (Aldershot 2007,forthcoming); Jan Glete, War and the state in early modern Europe. Spain, the Dutch Republic and Sweden asfiscal-military states, 1500-1660 (London and New York 2002); Nickolas C. Kyriazis, ‘A naval revolution andinstitutional change: the case of the United Provinces’, European Journal of Law and Economics 19 (2005) 41-68.3 The term has been coined by P.G.M. Dickson, The financial revolution in England. A study in the developmentof public credit 1688-1756 (Londen etc. 1967).4 Johan Aalbers, ‘Holland’s financial problems (1713-33) and the wars against Louis XIV’, in: A.C. Duke andC.A. Tamse (eds.), Britain and the Netherlands Vol. VI (The Hague 1977) 79-93; Jan de Vries and Ad van derWoude, The first modern economy. Succes, failure, and perseverance of the Dutch economy, 1500-1815(Cambridge 1997) 118.5 Eric S. Schubert, ‘Innovations, debts, and bubbles: international integration of financial markets in WesternEurope, 1688-1720’, Journal of Economic History 48 (1988) 299-306; Ron Harris, ‘The Bubble Act: its passageand its effect on business organization’, The Journal of Economic History 54 (1994) 610-627, 610.

2

This paper addresses the central question to what degree the merits of the earlierfinancial revolution in the Netherlands were continued in the eighteenth century. Was the wayto raise loans for warfare still an efficient system, as it had been in the previous century? Andto what degree had the British financial revolution of the eighteenth century become superiorto the Dutch? Detailed information as to the kind, number and size of the bonds are comparedto data provided by Dickson’s study on England and to data concerning the Dutch GoldenAge. Yet first an overview of the concept and scope of the financial revolution follows.

The financial revolutions in England and in Holland

I start with the English financial revolution as this was the model that inspired a generation ofhistorians. The arrival of William of Orange in 1688 was followed by a series of structuralinnovations in the English state’s finances. With the Declaration of Rights in 1689 Parliamentstrengthened its position as the real focus for the major interests in the country. Crown’srevenues were henceforth revenues of the nation. As a result, government loans also were‘uplifted’ from being loans to the king to loans to the Nation and a true National Debtemerged. Peter Dickson has described meticulously the development from (predominantly)short-term loans in the 1690s to regular long-term arrangements in public finance by themiddle of the eighteenth century. New institutions like the Bank of England (1694) wereestablished; in the decades to come this Bank proved of tremendous importance as anintermediary between government and potential investors in the state’s debt. The number ofpublic creditors rose spectacularly and the stock market itself received a major boost as thenumerous new government bonds were traded freely. Dickson’s analysis showed that thefinancial revolution had a relatively slow start, but from the 1740s onwards, the British stateproved most successful in mobilising massive and cheap loans for war.6 In the long run, thefinancial-revolution techniques were copied by other states again and became a hallmark ofthe nineteenth century nation-states.7

Dickson’s model on eighteenth century England underwent an adaptation by JamesTracy. He asserted that the English financial revolution had been inspired by earlier Dutchinstitutional settings: in fact, the financial revolution had occurred there in the sixteenthcentury. Tracy focussed on three aspects, that had also been following each other in time.First, in 1515 the provincial Estates of Holland (actually the six major cities) acceptedcommon and mutual responsibility for the service of interest payments on the renten (as thelong-term loans were called). Second, in the 1540s the Estates started to levy efficientprovincial taxes to be able to serve the renten. Third, in the 1550s all forced loans were doneaway with and a voluntary, free market emerged. As a result, the province of Holland becamean efficient entity to mobilise funds for the long and expensive Habsburg wars.8

Tracy’s interpretation of the financial revolution bears some different emphases fromDickson’s. The first aspect of Tracy (‘Estates/ provincial responsibility’) is more or lesscomparable to the Declaration of Rights in Dickson’s England. The second aspect (‘efficienttaxation’) received hardly any attention by Dickson itself but was actually a prerequisite for

6 Dickson, The financial revolution, 243-245.7 Charles P. Kindleberger, World economic primacy: 1500 to 1900 (New York and Oxford 1996) 96; RichardSylla, ‘Financial systems and economic modernization’, The Journal of Economic History 62 (2002) 277-292; p.281: the financial revolutions of the Dutch Republic, of England, and of the United States preceded theirrespective periods of economic growth. On the integration of the international financial markets and the gradualexpanding role of London at the expense of Amsterdam, Larry Neal, The rise of financial capitalism.International capital markets in the Age of Reason (Cambridge 1990).8 James D. Tracy, A financial revolution in the Habsburg Netherlands: renten and renteniers in the County ofHolland, 1515-1565 (Berkeley 1985).

3

the whole financial revolution, allowing for a funded debt system.9 Voluntary loans and freetrade in government bonds corresponded again with Dickson’s emphasis on the impact of thefinancial revolution on the stock market, yet in contrast to Dickson Tracy hardly studied theactual impact on the stock market itself.

Following Tracy, other historians joined in the debate, like John Munro who pointedto the earlier medieval roots of the financial revolution.10 In analysing the resources for theHolland government in the first decades of the Revolt, Wantje Fritschy argued that a ‘taxrevolution’ had been much more important than a financial revolution with long-term loans.In her view, only after 1600 the domestic capital market started to play a role, whereas bycomparison the rise in tax revenues had been spectacular.11 Oscar Gelderblom and JoostJonker found that in the early seventeenth century the major boost to the Dutch stock marketwas caused by the bonds of the East India Company. Not government bonds, but the companybonds ‘completed’ the financial revolution.12 Marjolein ’t Hart showed in her thesis that thetradition of the previous financial revolution in Holland as described by Tracy was oftremendous importance for the Dutch Republic in the 1620s-1650s. Thanks to the enormoustrust by the investing public (interest payments on Holland bonds had only been suspendedduring the most distressing period in the 1570s) the Dutch state could rest upon massive andcheap loans which allowed the United Provinces to assume big-power-status in a relativelyshort time-span.13

Leaving all possible interpretations and amendments to the concept aside for themoment, the example of Holland’s enormous borrowing power was indeed astounding inseventeenth century Europe. Dutch public credit was maintained by an institutional webwhich included an efficient tax system (based on excises), voluntary public loans (managedby a set of tax receivers through which funds of potential investors were mobilised) and amature stock market (supported by the Bank of Amsterdam). Thanks to the high security indebt servicing (unequalled in early modern Europe) interest rates were low, declining from8.33 and 6.25 per cent in the beginning of the seventeenth to 4 and 3 per cent in the secondhalf of the seventeenth century.

And indeed, the example of Dutch public loans impressed contemporaries in Englandand schemes were drafted to copy the system. The obvious advantages of the Bank ofAmsterdam led to several proposals to introduce a Bank for England too, yet that had to waitto the 1690s.14 One of the earliest crucial innovations were the excises of 1643, that had

9 Funded debt: a certain portion of the state revenues are reserved for the future payment of the interest on theloans. Taxation was excellently described by John Brewer, who linked up with Dickson in his The sinews ofpower. War, money and the English state, 1688-1783 (London etc. 1989); see also Patrick O’Brien and Philip A.Hunt, 'England 1485-1815' in R. Bonney (ed.), The Rise of the Fiscal State in Europe (Oxford 1999), 53-100 andPatrick O’Brien. Fiscal and financial preconditions for the rise of British naval hegemony, 1485-1815 (EHWorking Paper, 91/01 2005).10 John Munro, ‘The medieval origins of the financial revolution: usury, rentes, and negotiablity’, TheInternational History Review, 25:3 (September 2003), 505-62.11 Wantje Fritschy, ‘A financial revolution reconsidered. Public finance in Holland during the Dutch Revolt,1658-1648’, Economic History Review 56 (2003) 57-89.12 Oscar Gelderblom and Joost Jonker, ‘Completing a financial revolution. The finance of the Dutch East Indiatrade and the rise of the Amsterdam capital market’, Journal of Economic History, 64(2004), 641-672. For acritique on Gelderblom and Jonker, see Wantje Fritschy, ‘Holland’s public debt and Amsterdam’s capital market1585-1609’, paper presented to the VI Seminario Internacional de Historia. Banca, crédito y capital: lamonarquía y los antiguos Países Bajos, 1505-1700 (December 12-15, 2005), Madrid [forthcoming in: Carlos deAmberes (ed.)].13 Marjolein C. ’t Hart, The making of a bourgeois state. War, politics and finance during the Dutch Revolt(Manchester 1993), 161-165.14 Henry Roseveare, The financial revolution 1660-1760 (London and New York 1991) 10-11.

4

proved such a powerful fund for the Holland interest payments.15 Next, in the 1660s SirGeorge Downing introduced a funded debt system that was successful until the Stop of theExchequer in 1672.16 In certain respects the English state finances improved in the decadesbefore 1688,17 yet by and all public credit remained haphazard and uncertain and interest ratesremained high (8 per cent was not uncommon, compared to 4 per cent in the Netherlands).18

The number of investors was restricted and quite a number of the most important creditorswent bankrupt due to recurrent failures to service the debts.

Although the novelties of the 1690s drew inspiration from the Dutch example,19 theEnglish reforms went significantly further (or rather ‘in another direction’) in a number ofrespects. Some of them will be dealt again with below in more detail, but it is handy to pointto a couple of differences that jump to the forefront. Above all, the Bank of England of 1694was different from the Amsterdam Bank of Exchange of 1609.20 The Amsterdam Bank was amunicipal bank and its revenues supported the local burgomasters (likewise, there were localbanks in Delft, Rotterdam and Middelburg). It was not a credit institution: its main task was tohandle the deposits of major traders and to take care of the major bills of exchange.21

Accounts among traders were settled at the Bank through a giro system without the need ofcash transfers. Loans were only supplied to the municipal government and to the East IndiaCompany. Since 1683, with the issue of recepissen notes (recepis= proof of a coin deposit)the Bank did support the trading community with the creation of numerous bills, that could betraded freely on the market, which raised the actual money supply.

The Amsterdam Bank thus served primarily the interests of the local tradingcommunity, only secondarily the local government, and only indirectly the central orprovincial government. The burgomasters had established the Bank because they feared theuncontrolled activity of the numerous cashiers in the town.22 Since 1609, all major bills ofexchange had to be discounted through the Bank. Also, the Bank took care of the a securedtransaction system by regulating the money of account (bank guilder) through the agio withcurrent money (mainly guilders too). For the local trading community, these advantages wereimmense indeed.

The Bank of England (initially called Bank of London) was first and foremost aninstrument to raise funds for the government as a joint-stock company. The establishment of

15 Marjolein ’t Hart, ‘The Devil of the Dutch? Holland’s impact on the financial revolution in England, 1643-1694’, Parliaments, Estates, Representations 11 (1989) 39-52, 43. The excises (duties upon consumer goods)became a firm foundation for the later financial revolution.16 Roseveare, The financial revolution, 78.17 Ibidem, 3. As to the relative maturity of the London stock market prior to the 1690s: Ann M. Carlos, JenniferKey and Jill. L. Dupree, ‘Learning and the creation of stock-market institutions: evidence from the RoyalAfrican and Hudson’s Bay Companies’, 1670-1700’, The Journal of Economic History 58 (1998) 318-344, 333.As to the solutions in navy finance prior to the 1690s, J.S. Wheeler,’Navy finance, 1649-1660’, The HistoricalJournal 39(1996) 457-466, 461.18 See also Gregory Clark, ‘The political foundations of modern economic growth: England, 1540-1800’,Journal of Interdisciplinary History 26 (1996) 563-588, 567.19 Cf. Eric Schubert, ‘Innovations, debts’, 300: ‘…the administration of William III imported Dutch techniquesof finance’.20 Peter Dickson assumed that the Bank of England was a copy of the Bank of Amsterdam, yet he noticed as tothe English bank: ‘ …[the Bank of England, MtH] quickly showed that in the quality of its management it couldchallenge comparison with the Bank of Amsterdam, hitherto the cynosure of European eyes’. Dickson, Thefinancial revolution, 58. I would pose this more strongly: The Bank of England was superior to the Bank ofAmsterdam as an instrument for securing public credit.21 Credit was provided by another municipal bank, the Amsterdam Bank van Lening, since 1614. L. Jansen,Geschiedenis van de Stads Bank van Lening te Amsterdam 1614-1964 (Amsterdam 1964).22 Peter Spufford, ‘Access to credit and capital in the commercial centres of Europe’, in: Karel Davids and JanLucassen (eds.), A miracle mirrored. The Dutch Republic in European perspective (Cambridge 1995) 303-337,322.

5

the Bank of England led directly to an increased activity on the stock market; theestablishment of the Bank of Amsterdam had no such effects at all. The Bank of England alsodiscounted bills, yet as it was controlled by the central government, the bank was in a positionto assume later nation-wide tasks such as issuing paper notes and managing new governmentloans. By being able to expand the money supply by using a fractional reserve system, theBank could act with a high degree of elasticity during times of crises (by comparison: theBank of Amsterdam had no elasticity at all). By the later eighteenth century, the Bank ofEngland came to act as a lender of last resort. At the same time, the London mayors imposedless restrictions upon the financial community, leaving more elbow-room for private bankinghouses and the stock market. Meanwhile the Bank of Amsterdam remained strongly geared tothe interests of the trading community, yet could not serve the individual banks that got intodistress during financial crises such as in 1763 and 1773.

Secondly, the English revenue-raising machine continued to use joint-stock companiesto mobilise funds for war. The English East India Company and the South Sea Company wereused to finance the war efforts of the state. Again, these numerous new bonds had animmediate impact on the stock market. In the Netherlands, neither the East India Companynor the West India Company were used to finance the Dutch Republic or its wars in Europe.The capital raised was used primarily for the colonial ventures themselves (which did involvewarfare in the Indies, of course). Their bonds thus had no close relationship to the system ofpublic credit, the investors did not become state creditors, the Dutch colonial capital remained‘private’ capital.23

Finally, the whole English financial revolution was set in a much more centralisedpolity. London housed c. one-tenth of the population and a disproportionate amount of thetaxable wealth of the country. Even though the London stock market remained of immenseimportance, the government could draw upon nation-wide resources too (in particular nation-wide tax revenues to support the debt service that went mainly to the London creditors). TheHolland financial revolution had been based upon the strong financial tradition of the townsthat had managed large-scale loans through annuities for at least a century before Habsburgrule. Although in the sixteenth century that tradition had been uplifted to encompass thewhole province (drawing upon provincial taxes to service the predominantly urban-basedloans), the Dutch financial revolution remained restricted to the provincial level.24Yet Hollandwas just one of the seven sovereign provinces that met together in the States General of theUnited Provinces. Most financial policies were strictly provincial oriented. There was no waythat tax revenues from other provinces could be used to service the creditors in –mainly- theHolland towns. The decentralised setting may have constituted an advantage during the earlystages of the Revolt, as the networks and the mutual trust between the local/regional war-establishments and the local/regional fund-raising institutions were strong, yet this certainlyproved a disadvantage on the long run.

However, these aspects are only part of the explanation. It is of interest to establish towhat degree the eighteenth century ‘financial revolution’ of Holland was still the same as inthe previous century. Seventeenth century Dutch public funds had been characterised by alarge number of creditors; small-scale contracts dominated. Did the managers of the stateloans (the tax receivers in the towns) still open their doors to the small-scale investors and to

23 Moreover, the number of East India Stock was and remained restricted: in 1612 some 830 stock-holders werenoted: Femme Gaastra, Geschiedenis van de VOC (Zutphen 2002) 34. This calls into question whether theserelatively few bonds (compared to English colonial stock 830 is an absolute non-figure, see Dickson, Thefinancial revolution, 249 ff.) could perform the task to ‘fulfill’ a financial revolution. See also Gelderblom andJonker, ‘Completing a financial revolution’.24 Thus actually Holland; to a certain degree Zeeland and Utrecht enjoyed similar advantages due to a similarsecure tax base, but it was Holland’s credit that supported the Republic.

6

those with only moderate funds? Were creditors still dispersed over all Holland towns or wasa considerable concentration noticeable? And is it possible to discern an aristocratisationamong the investors in state funds? With a concentration of the loans in place and person, thatmay well have implied an improved efficiency for the state (i.e. economies of scale). Acomparison with the English eighteenth century loans will reveal to what degree the Dutchcould still count upon advantages in the financial revolution. Yet first it is instrumental toprovide some detailed information as to the seventeenth century loans.

The public loans of Holland and the Union since the Dutch Revolt of the 1570s

In the seventeenth century, the Dutch Republic relied above all upon the credit of theProvince of Holland, next upon the credit of the Receiver General of the Union (theGenerality, representing the United Seven Provinces) in The Hague, and only third upon thecredit of the other provinces and of the five admiralties. In this analysis I will focus on thepublic loans of Holland and the Generality only; they were by far the most important.Holland’s credit consisted in turn of funds from the regional tax officers.25 In this study I willlook in particular at the loans of the Receiver General of Holland (based, like his colleaguethe Receiver General of the Union, in The Hague) and of the Receivers General of theAmsterdam and Rotterdam tax districts (based respectively in Amsterdam and Rotterdam). Toavoid confusion, I will not speak about Receivers General but about the Union Receiver, theHolland Receiver, the Amsterdam Receiver and the Rotterdam Receiver; likewise I will usethe terms Union loans, Holland loans, Amsterdam loans and Rotterdam loans when dealingwith their respective loans. The terminology is not wholly accurate yet handy for the purposeof this paper.

The most prominent instrument to raise funds in the seventeenth century had been theannuity, rente, which had been the main tool in the medieval tradition of urban public debtsfor centuries. Interest payments were provided by the yield from the numerous excise duties(funded debt). In return for the provision of a capital sum, the investor received an annual (orbi-annual) compensation which stood at 5 per cent or 4 per cent (the prevailing rates duringmost of the seventeenth century) for the perpetual annuities (losrente). With the losrente, thepayments halted when the capital sum was returned to the investor (hence the term “los” from“aflossing”, redemption) – yet most annuities were repaid only on the (very) long term andsome were even never repaid. Therefore, the perpetual annuities were typical instruments forthe Dutch long-term debt.

Alongside the perpetual annuities life annuities were issued. These lasted only as longas the nominee in the loan contract lived: the ‘life’ or lijf in Dutch, hence the term lijfrenten.In contrast to the perpetual annuities, the capital of the life annuities was never repaid; withthe death of the nominee, interest payments halted and the capital fell to the public authorities.As the capital was never returned, the interest rates upon life annuities was twice (orsomewhat less than twice) as high as the rate upon the perpetual annuities. Some buyers oflife annuities were the nominees themselves (lasting generally shorter), yet most creditorschose a child as a nominee (generally their own children, or nieces and nephews, thus lasting

25 Their numbers varied between eight and ten in the Southern Quarter of Holland, including the tax receivers atThe Hague (for Holland), Amsterdam, Rotterdam, Dordrecht, Delft, Haarlem, Leiden, Gouda, Brill andGorinchem. The Northern Quarter of Holland (with Alkmaar, Hoorn , Enkhuizen, Edam, Monnikendam, andPurmerend) supplied separately loans too. By far, the Holland (The Hague) and the Amsterdam receiversmanaged the largest funds. Rotterdam is taken as an example for the smaller Holland offices; in the eighteenthcentury Rotterdam grew into one of the larger receiving offices.

7

generally longer).26 By and all, the life annuities constituted a typical instrument for themedium and the long-term, with the advantage that on the very long term the capital burdendecreased and even disappeared. The disadvantage was that on the short term they were quiteexpensive in debt-service.27

The typical short-term loans of Holland had been the obligations. In the sixteenthcentury, their predominant term would have been lening (literary loan) or penningen opinterest (monies against interest). These terms were still used in the seventeenth andeighteenth centuries, yet the individual bonds were known by the term obligatie (literary acommitment/promise to repay the capital sum with interest). In the first decades of theRepublic, obligations lasted between one and twelve months, yet by the 1610s the usual termhad settled at six months. Interest rates assumed the same as for perpetual annuities; howevercontrary to the latter, obligations had not been rooted in the strong tradition of urban publicdebts; neither were they funded automatically by excise taxes. In the first decades, thereceiver stood bail for the repayment with his own credit, for which he received a commissionof 1 per cent. Soon, the revenues of the province were to stand bail, and the receiver’scommission was reduced to a 0.5 per cent. After 1600, the obligations changed in character: atfirst they had been treated as short-term bonds and represented a typical floating debt. Yet bythe 1620s, most obligations were renewed every six months, rendering them in practiceinstruments for the medium and long term as well.

All these bonds, annuities and obligations alike, received their interest paymentsregularly, once or twice a year. They all could be traded on the market.28 Throughout theseventeenth century contemporaries noted that Holland bonds made a good price there: thestrength of Holland’s credit was underscored by the fact that sixteenth-century annuitiesregularly made prices at 112 and 113 per cent.29 The transfers were recorded by the notariesand in the ledgers of the receivers, new annuity owners were noted upon receiving theinstalment. Increasingly, financial intermediaries dealt with this kind of business. Lifeannuities –with their relatively high interest rates- were typically investments for securing the(near) future of beloved ones; hence, they generally remained within the family. They werealso most cumbersome to handle: at each instalment a proof had to be handed over that thenominee was still alive. By far, the easiest to transfer were the obligations made payable tobearer. Yet how often obligations changed hands is uncertain, as the remaining accounts bookyield only fragmented information. Moreover, as obligations could be changed for readymoney at the receiver’s offices without any problem twice a year, most owners probably didnot even bother to try to sell them on the free market.30

Characteristics of loans: annuities

26 Variations existed: life annuities on two or three lives/nominees, at lower rates of interest, payments haltingafter the longest living nominee had died, and tontine loans in which a group investors provided a large sum,interest payments were divided over the investors, the sums increasing when the other investors died. Contrary towhat Dickson assumes (p. 53), the tontine was not an instrument often used in the Netherlands. For France,though, this became a favourite instrument in the eighteenth century.27 Schemes as proposed by the famous statesman Johan de Witt, Waardije, to vary the interest rates acccording tothe age of the nominee, were not put into regular practice.28 Dickson, The financial revolution, referring to Hamilton’s work .29 Weveringh, Handleiding geschiedenis staatsschulden, I, 4; Jan de Vries, The economy of Europe in an age ofcrises (Cambridge 1976), 227; William Temple, Observations (aanv & check). See also Oscar Gelderblom andJoost Jonker, ‘Probing a virtual market. Interst rates and trade in government bonds in the Dutch republic’,paper, Utrecht University.30 Short bills (three months) however became increasingly popular during 1700-1720; see Schubert,‘Innovations, debts’, 302. Probably by then the six months term had become probably rather cumbersome for anincreasing group of traders.

8

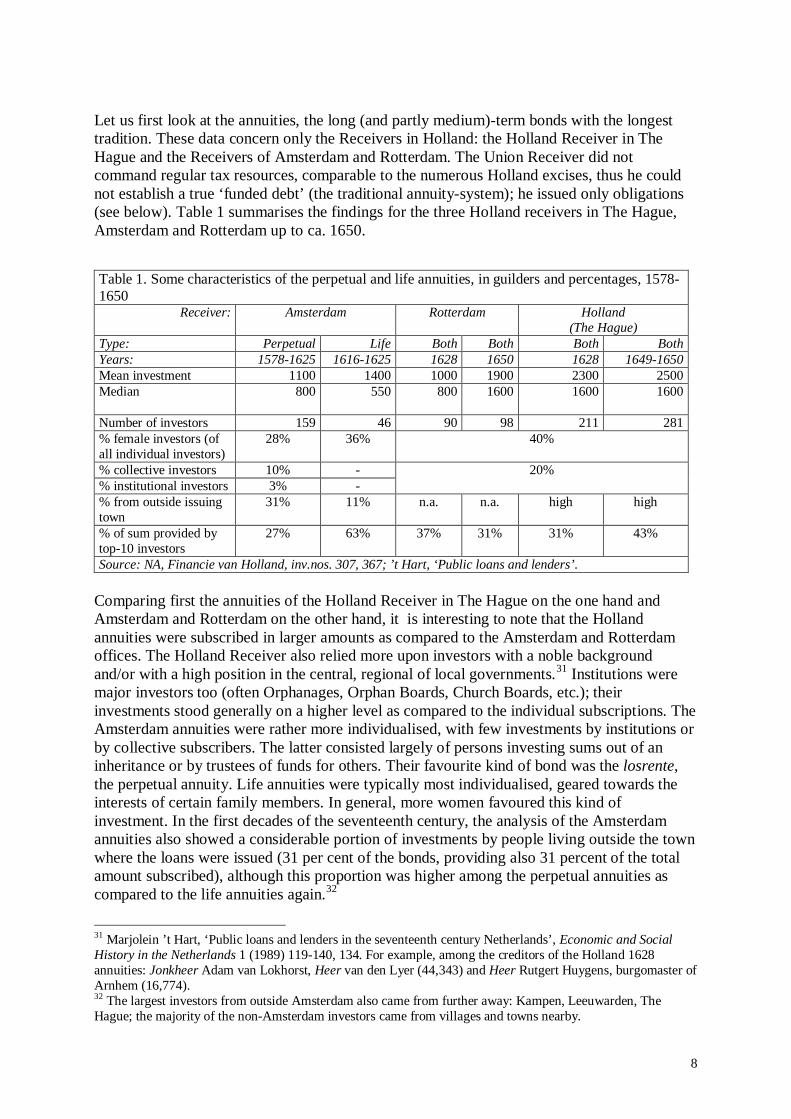

Let us first look at the annuities, the long (and partly medium)-term bonds with the longesttradition. These data concern only the Receivers in Holland: the Holland Receiver in TheHague and the Receivers of Amsterdam and Rotterdam. The Union Receiver did notcommand regular tax resources, comparable to the numerous Holland excises, thus he couldnot establish a true ‘funded debt’ (the traditional annuity-system); he issued only obligations(see below). Table 1 summarises the findings for the three Holland receivers in The Hague,Amsterdam and Rotterdam up to ca. 1650.

Table 1. Some characteristics of the perpetual and life annuities, in guilders and percentages, 1578-1650

Receiver: Amsterdam Rotterdam Holland(The Hague)

Type: Perpetual Life Both Both Both BothYears: 1578-1625 1616-1625 1628 1650 1628 1649-1650Mean investment 1100 1400 1000 1900 2300 2500Median 800 550 800 1600 1600 1600

Number of investors 159 46 90 98 211 281% female investors (ofall individual investors)

28% 36% 40%

% collective investors 10% -% institutional investors 3% -

20%

% from outside issuingtown

31% 11% n.a. n.a. high high

% of sum provided bytop-10 investors

27% 63% 37% 31% 31% 43%

Source: NA, Financie van Holland, inv.nos. 307, 367; ’t Hart, ‘Public loans and lenders’.

Comparing first the annuities of the Holland Receiver in The Hague on the one hand andAmsterdam and Rotterdam on the other hand, it is interesting to note that the Hollandannuities were subscribed in larger amounts as compared to the Amsterdam and Rotterdamoffices. The Holland Receiver also relied more upon investors with a noble backgroundand/or with a high position in the central, regional of local governments.31 Institutions weremajor investors too (often Orphanages, Orphan Boards, Church Boards, etc.); theirinvestments stood generally on a higher level as compared to the individual subscriptions. TheAmsterdam annuities were rather more individualised, with few investments by institutions orby collective subscribers. The latter consisted largely of persons investing sums out of aninheritance or by trustees of funds for others. Their favourite kind of bond was the losrente,the perpetual annuity. Life annuities were typically most individualised, geared towards theinterests of certain family members. In general, more women favoured this kind ofinvestment. In the first decades of the seventeenth century, the analysis of the Amsterdamannuities also showed a considerable portion of investments by people living outside the townwhere the loans were issued (31 per cent of the bonds, providing also 31 percent of the totalamount subscribed), although this proportion was higher among the perpetual annuities ascompared to the life annuities again.32

31 Marjolein ’t Hart, ‘Public loans and lenders in the seventeenth century Netherlands’, Economic and SocialHistory in the Netherlands 1 (1989) 119-140, 134. For example, among the creditors of the Holland 1628annuities: Jonkheer Adam van Lokhorst, Heer van den Lyer (44,343) and Heer Rutgert Huygens, burgomaster ofArnhem (16,774).32 The largest investors from outside Amsterdam also came from further away: Kampen, Leeuwarden, TheHague; the majority of the non-Amsterdam investors came from villages and towns nearby.

9

Over time, the sums subscribed showed a minor increase at the The Hague office, yetin Rotterdam the increase was quite substantial. This may well point to some increasedefficiency of the loan-raising machine during the first half of the seventeenth century.Looking also at the figures noting the concentration of the amounts subscribed by the top-teninvestors of each Receiver, also some increase was noted, but this time the advantage wasmore obvious for the The Hague office whereas Rotterdam showed only a minor rise.Remarkable was the high concentration of the sums provided by the top-ten investors in life-annuities at Amsterdam. This showed the particular popularity of these bonds among the veryrich.33 Although the capital of these bonds was never reimbursed, the life annuities sufferedgenerally less from conversions (i.e., when the rate of interest was reduced).

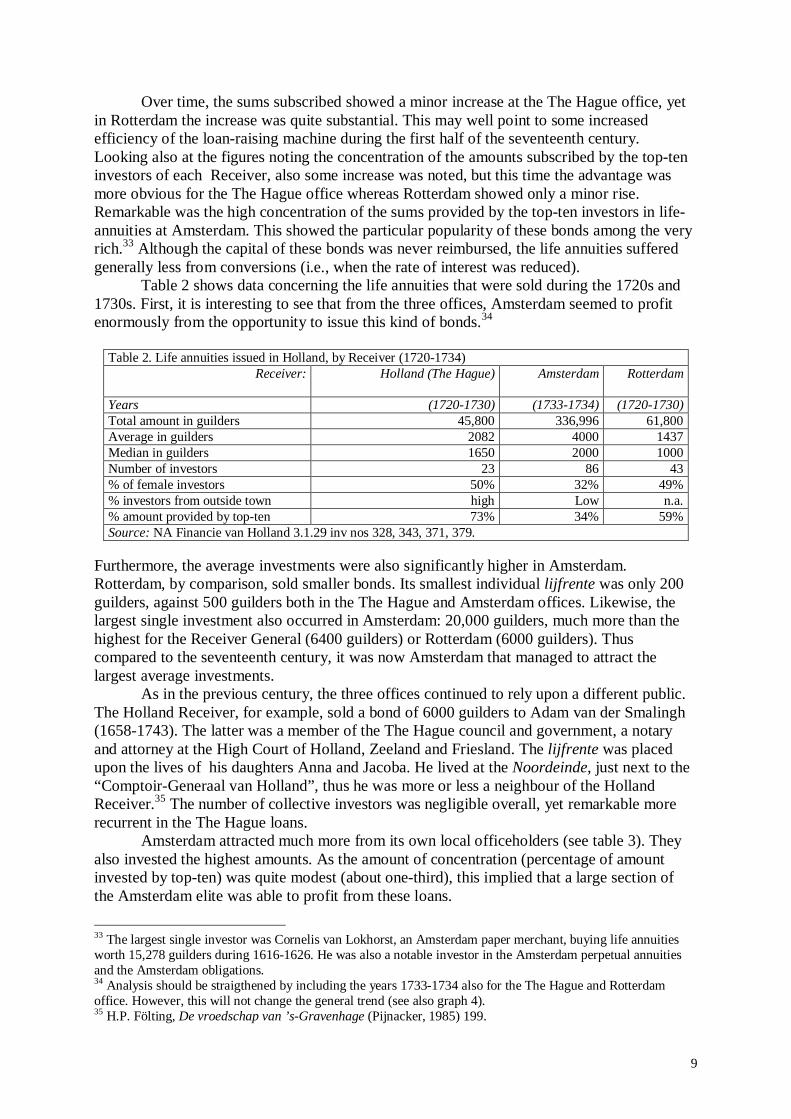

Table 2 shows data concerning the life annuities that were sold during the 1720s and1730s. First, it is interesting to see that from the three offices, Amsterdam seemed to profitenormously from the opportunity to issue this kind of bonds.34

Table 2. Life annuities issued in Holland, by Receiver (1720-1734)Receiver: Holland (The Hague) Amsterdam Rotterdam

Years (1720-1730) (1733-1734) (1720-1730)Total amount in guilders 45,800 336,996 61,800Average in guilders 2082 4000 1437Median in guilders 1650 2000 1000Number of investors 23 86 43% of female investors 50% 32% 49%% investors from outside town high Low n.a.% amount provided by top-ten 73% 34% 59%Source: NA Financie van Holland 3.1.29 inv nos 328, 343, 371, 379.

Furthermore, the average investments were also significantly higher in Amsterdam.Rotterdam, by comparison, sold smaller bonds. Its smallest individual lijfrente was only 200guilders, against 500 guilders both in the The Hague and Amsterdam offices. Likewise, thelargest single investment also occurred in Amsterdam: 20,000 guilders, much more than thehighest for the Receiver General (6400 guilders) or Rotterdam (6000 guilders). Thuscompared to the seventeenth century, it was now Amsterdam that managed to attract thelargest average investments.

As in the previous century, the three offices continued to rely upon a different public.The Holland Receiver, for example, sold a bond of 6000 guilders to Adam van der Smalingh(1658-1743). The latter was a member of the The Hague council and government, a notaryand attorney at the High Court of Holland, Zeeland and Friesland. The lijfrente was placedupon the lives of his daughters Anna and Jacoba. He lived at the Noordeinde, just next to the“Comptoir-Generaal van Holland”, thus he was more or less a neighbour of the HollandReceiver.35 The number of collective investors was negligible overall, yet remarkable morerecurrent in the The Hague loans.

Amsterdam attracted much more from its own local officeholders (see table 3). Theyalso invested the highest amounts. As the amount of concentration (percentage of amountinvested by top-ten) was quite modest (about one-third), this implied that a large section ofthe Amsterdam elite was able to profit from these loans.

33 The largest single investor was Cornelis van Lokhorst, an Amsterdam paper merchant, buying life annuitiesworth 15,278 guilders during 1616-1626. He was also a notable investor in the Amsterdam perpetual annuitiesand the Amsterdam obligations.34 Analysis should be straigthened by including the years 1733-1734 also for the The Hague and Rotterdamoffice. However, this will not change the general trend (see also graph 4).35 H.P. Fölting, De vroedschap van ’s-Gravenhage (Pijnacker, 1985) 199.

10

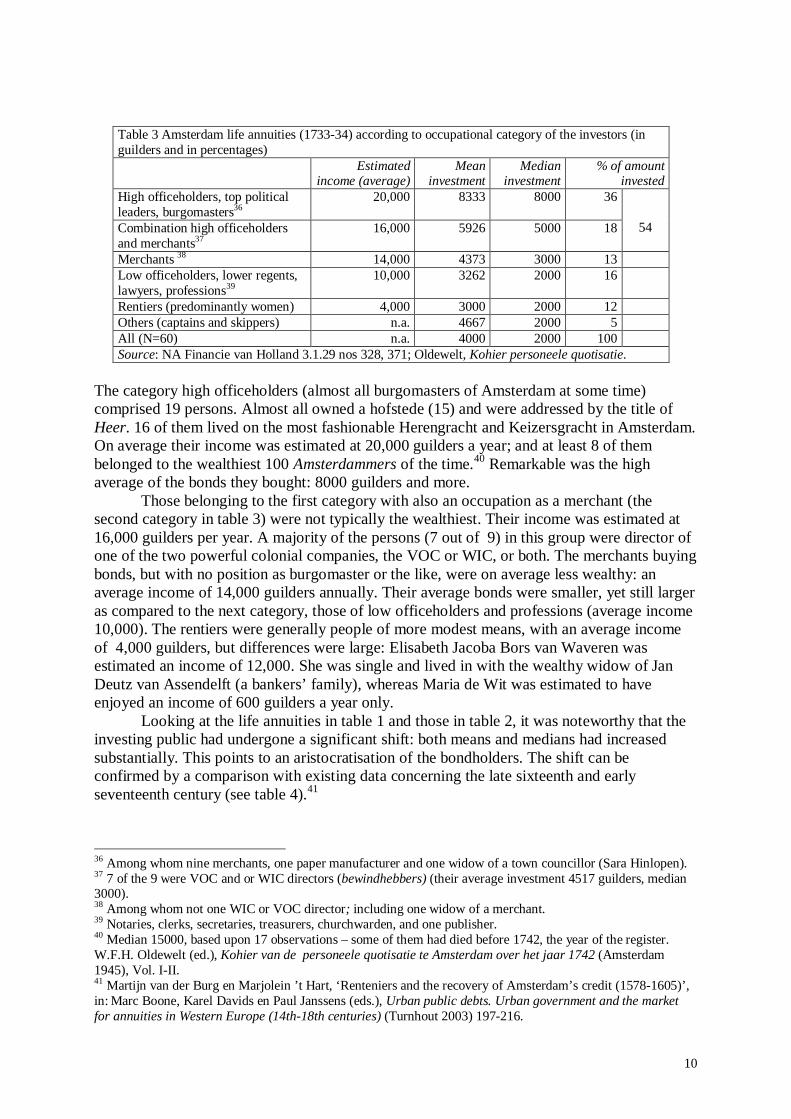

Table 3 Amsterdam life annuities (1733-34) according to occupational category of the investors (inguilders and in percentages)

Estimatedincome (average)

Meaninvestment

Medianinvestment

% of amountinvested

High officeholders, top politicalleaders, burgomasters36

20,000 8333 8000 36

Combination high officeholdersand merchants37

16,000 5926 5000 18 54

Merchants 38 14,000 4373 3000 13Low officeholders, lower regents,lawyers, professions39

10,000 3262 2000 16

Rentiers (predominantly women) 4,000 3000 2000 12Others (captains and skippers) n.a. 4667 2000 5All (N=60) n.a. 4000 2000 100Source: NA Financie van Holland 3.1.29 nos 328, 371; Oldewelt, Kohier personeele quotisatie.

The category high officeholders (almost all burgomasters of Amsterdam at some time)comprised 19 persons. Almost all owned a hofstede (15) and were addressed by the title ofHeer. 16 of them lived on the most fashionable Herengracht and Keizersgracht in Amsterdam.On average their income was estimated at 20,000 guilders a year; and at least 8 of thembelonged to the wealthiest 100 Amsterdammers of the time.40 Remarkable was the highaverage of the bonds they bought: 8000 guilders and more.

Those belonging to the first category with also an occupation as a merchant (thesecond category in table 3) were not typically the wealthiest. Their income was estimated at16,000 guilders per year. A majority of the persons (7 out of 9) in this group were director ofone of the two powerful colonial companies, the VOC or WIC, or both. The merchants buyingbonds, but with no position as burgomaster or the like, were on average less wealthy: anaverage income of 14,000 guilders annually. Their average bonds were smaller, yet still largeras compared to the next category, those of low officeholders and professions (average income10,000). The rentiers were generally people of more modest means, with an average incomeof 4,000 guilders, but differences were large: Elisabeth Jacoba Bors van Waveren wasestimated an income of 12,000. She was single and lived in with the wealthy widow of JanDeutz van Assendelft (a bankers’ family), whereas Maria de Wit was estimated to haveenjoyed an income of 600 guilders a year only.

Looking at the life annuities in table 1 and those in table 2, it was noteworthy that theinvesting public had undergone a significant shift: both means and medians had increasedsubstantially. This points to an aristocratisation of the bondholders. The shift can beconfirmed by a comparison with existing data concerning the late sixteenth and earlyseventeenth century (see table 4).41

36 Among whom nine merchants, one paper manufacturer and one widow of a town councillor (Sara Hinlopen).37 7 of the 9 were VOC and or WIC directors (bewindhebbers) (their average investment 4517 guilders, median3000).38 Among whom not one WIC or VOC director; including one widow of a merchant.39 Notaries, clerks, secretaries, treasurers, churchwarden, and one publisher.40 Median 15000, based upon 17 observations – some of them had died before 1742, the year of the register.W.F.H. Oldewelt (ed.), Kohier van de personeele quotisatie te Amsterdam over het jaar 1742 (Amsterdam1945), Vol. I-II.41 Martijn van der Burg en Marjolein ’t Hart, ‘Renteniers and the recovery of Amsterdam’s credit (1578-1605)’,in: Marc Boone, Karel Davids en Paul Janssens (eds.), Urban public debts. Urban government and the marketfor annuities in Western Europe (14th-18th centuries) (Turnhout 2003) 197-216.

11

Table 4. Investors in life annuities at Amsterdam, in percentages of total of whom occupation is known(1584-1604 and 1733-1734)

1584-1604 1733-1734Artisans, industrial entrepreneurs 2142 1943 244 045

High officeholders, top political leaders, burgomasters 546 15Combination merchants/high officeholders 13

2115

3447

Professions, lower offices (lawyers) 748 649 23 21Merchants with no high office 50 50 20 20Rentiers 0 0 20 20Others (captains, skippers) 4 4 5 5Total excl unknown 100 100 100 100N= 206 206 60 60Sources: see table 3; and Martijn van der Burg and Marjolein ’t Hart, ‘Renteniers’.

The comparison revealed a clear development: much more than in the previous centuries,investors in life annuities had become a more close and restricted group. The category of‘merchants’ had been driven back and the high officeholders had become the dominant group.Their possible side interests in trade or handicrafts were negligible, apart from the position inone of the colonial companies. In our 1733-1734 annuities, no artisans were traced at all.50 Byand all, the merchant influence in these bonds had diminished, and the group of rentiers hadbecome a new category.

At the same time, the tax receiver did not close his doors for those with moderatefunds. Someone with only 100 guilders could still buy a lijfrente. Yet the opportunities toinvest in these highly desired bonds had decreased for those that did not belong to the rulingelite. Life annuities thus served in particular the interests of the local political officeholders bythe early eighteenth century. This is consistent with the findings of Julia Adams: the policy ofthe Dutch patriciate household-heads was geared predominantly towards the furthering oftheir family-interests.51 These bonds enabled the investors to take care of their beloved onesfor the future. This had not been different in the seventeenth century, yet the degree of eliteparticipation had increased considerably, at the expense of the people with more moderatemeans.

Even more as compared with the life annuities, the perpetual annuities had underwent asignificant shift since the first half of the seventeenth century, as can be seen in table 5. Aconsiderable concentration had occurred.

42 Of whom 5 who also belonged to the category of high officeholders43 Excluding 5 who belonged to the category of high officeholders44 One paper-manufacturer who also belonged both to the category of high officeholders and merchants.45 Excluding the paper-manufacturer who also belonged both to the category of high officeholders andmerchants.46 Excluding the 5 high-officeholders who also belonged to the categories of artisans/entrepreneurs and 2 highofficeholders belonging to the group of professions.47 Including the paper-manufacturer who also belonged both to the category of high officeholders and merchantsand the two high-office-holders among the professions.48 Including 2 who also belonged to the group of high officeholders.49 Excluding 2 who also belonged to the group of high officeholders.50 They might have been among the 8 male investors about whom no further details are known as yet.51 Julia Adams, The familial state. Ruling families and merchant capitalism in early modern Europe (Ithaca andLondon 2005) 138.

12

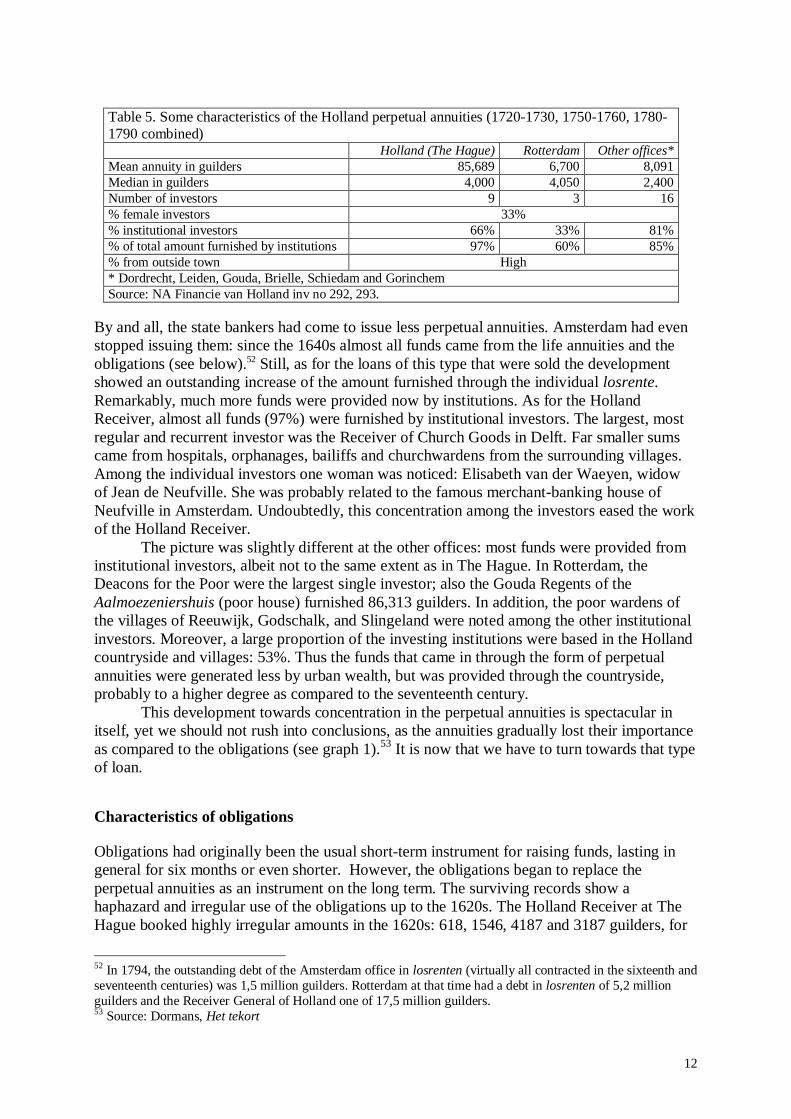

Table 5. Some characteristics of the Holland perpetual annuities (1720-1730, 1750-1760, 1780-1790 combined)

Holland (The Hague) Rotterdam Other offices*Mean annuity in guilders 85,689 6,700 8,091Median in guilders 4,000 4,050 2,400Number of investors 9 3 16% female investors 33%% institutional investors 66% 33% 81%% of total amount furnished by institutions 97% 60% 85%% from outside town High* Dordrecht, Leiden, Gouda, Brielle, Schiedam and GorinchemSource: NA Financie van Holland inv no 292, 293.

By and all, the state bankers had come to issue less perpetual annuities. Amsterdam had evenstopped issuing them: since the 1640s almost all funds came from the life annuities and theobligations (see below).52 Still, as for the loans of this type that were sold the developmentshowed an outstanding increase of the amount furnished through the individual losrente.Remarkably, much more funds were provided now by institutions. As for the HollandReceiver, almost all funds (97%) were furnished by institutional investors. The largest, mostregular and recurrent investor was the Receiver of Church Goods in Delft. Far smaller sumscame from hospitals, orphanages, bailiffs and churchwardens from the surrounding villages.Among the individual investors one woman was noticed: Elisabeth van der Waeyen, widowof Jean de Neufville. She was probably related to the famous merchant-banking house ofNeufville in Amsterdam. Undoubtedly, this concentration among the investors eased the workof the Holland Receiver.

The picture was slightly different at the other offices: most funds were provided frominstitutional investors, albeit not to the same extent as in The Hague. In Rotterdam, theDeacons for the Poor were the largest single investor; also the Gouda Regents of theAalmoezeniershuis (poor house) furnished 86,313 guilders. In addition, the poor wardens ofthe villages of Reeuwijk, Godschalk, and Slingeland were noted among the other institutionalinvestors. Moreover, a large proportion of the investing institutions were based in the Hollandcountryside and villages: 53%. Thus the funds that came in through the form of perpetualannuities were generated less by urban wealth, but was provided through the countryside,probably to a higher degree as compared to the seventeenth century.

This development towards concentration in the perpetual annuities is spectacular initself, yet we should not rush into conclusions, as the annuities gradually lost their importanceas compared to the obligations (see graph 1).53 It is now that we have to turn towards that typeof loan.

Characteristics of obligations

Obligations had originally been the usual short-term instrument for raising funds, lasting ingeneral for six months or even shorter. However, the obligations began to replace theperpetual annuities as an instrument on the long term. The surviving records show ahaphazard and irregular use of the obligations up to the 1620s. The Holland Receiver at TheHague booked highly irregular amounts in the 1620s: 618, 1546, 4187 and 3187 guilders, for

52 In 1794, the outstanding debt of the Amsterdam office in losrenten (virtually all contracted in the sixteenth andseventeenth centuries) was 1,5 million guilders. Rotterdam at that time had a debt in losrenten of 5,2 millionguilders and the Receiver General of Holland one of 17,5 million guilders.53 Source: Dormans, Het tekort

13

example. The number of people willing and ready to invest in these funds seemed to havebeen rather restricted. The 1616-1617 obligations of the Amsterdam Receiver were providedby four (or three) persons only: Mr Jasper van Vosbergen for 40,000 guilders; BartholomeusPanhuijsen for 70,000 guilders; the same but now as a trustee for Jan Hesse, 30,000 guilders;and finally Juffrouw Catharina Malapert, widow of Jan Vueren, for 60,000 guilders. Neitherof these persons had an obvious connection to Amsterdam.54 Rather, they seemed to havebelonged to the circle of investors of the Holland and Union Receivers in the Hague.

Above all, the obligations in the first decades of the Dutch Revolt had been thefavourite loan instruments of the Union Receiver and the Holland Receiver (and also at theDelft tax office, close to The Hague). The The Hague Receivers were both confronted withfrequent and urgent demands for payments to troops and admiralties; expenses that could notalways wait until the Estates of Holland had reached an agreement and until the authoritieshad issued a regular ordinance to raise annuities for so and so much funds to be divided overthe separate tax offices in such and so proportions to be services by such and so funds. Thefunds that were necessary to pay the interests on the The Hague obligations were to arrivefrom the tax receivers in the Holland towns (for the Holland Receiver) and from theprovincial receivers (for the Union Receiver), yet as no specific revenue item was assigned itwas not a funded debt in the strict sense. But Holland Receivers in the towns increasingly soldobligations too, for which the revenues of that particular tax office was to stand bail. Allobligations were only sold after order by the Holland government. The Receiver could onlyissue new obligations upon his own account to replace former ones that were redeemed.

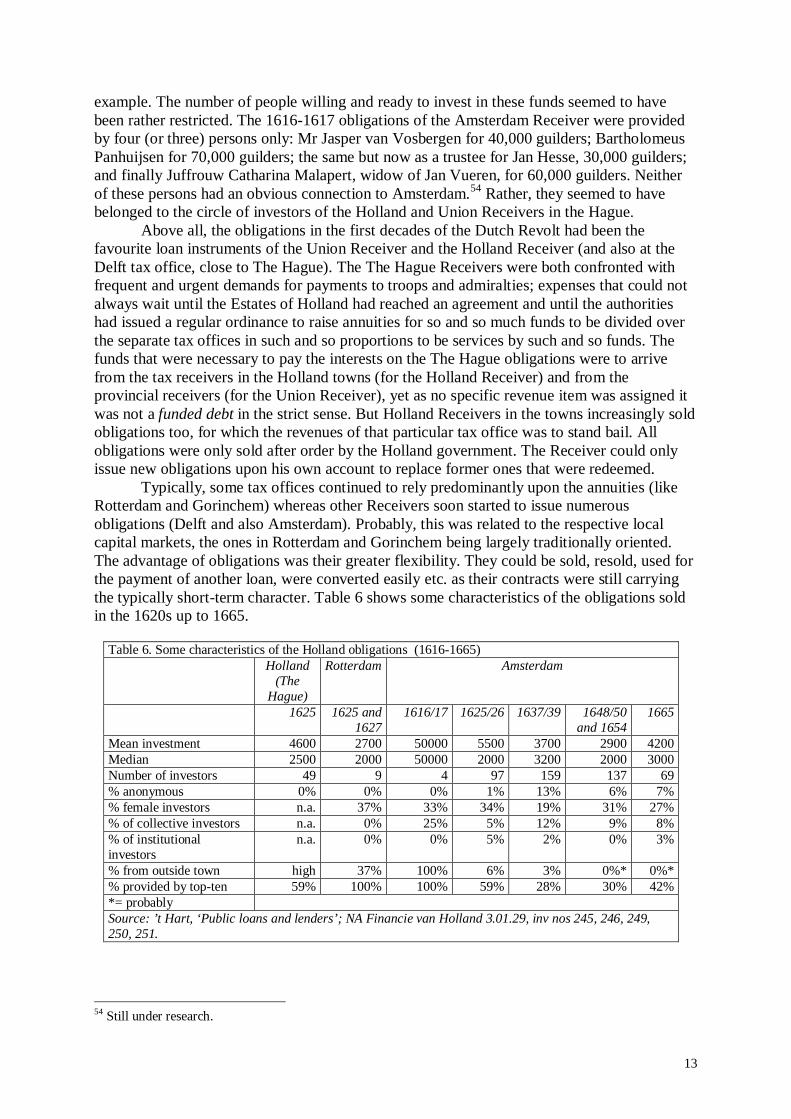

Typically, some tax offices continued to rely predominantly upon the annuities (likeRotterdam and Gorinchem) whereas other Receivers soon started to issue numerousobligations (Delft and also Amsterdam). Probably, this was related to the respective localcapital markets, the ones in Rotterdam and Gorinchem being largely traditionally oriented.The advantage of obligations was their greater flexibility. They could be sold, resold, used forthe payment of another loan, were converted easily etc. as their contracts were still carryingthe typically short-term character. Table 6 shows some characteristics of the obligations soldin the 1620s up to 1665.

Table 6. Some characteristics of the Holland obligations (1616-1665)Holland

(TheHague)

Rotterdam Amsterdam

1625 1625 and1627

1616/17 1625/26 1637/39 1648/50and 1654

1665

Mean investment 4600 2700 50000 5500 3700 2900 4200Median 2500 2000 50000 2000 3200 2000 3000Number of investors 49 9 4 97 159 137 69% anonymous 0% 0% 0% 1% 13% 6% 7%% female investors n.a. 37% 33% 34% 19% 31% 27%% of collective investors n.a. 0% 25% 5% 12% 9% 8%% of institutionalinvestors

n.a. 0% 0% 5% 2% 0% 3%

% from outside town high 37% 100% 6% 3% 0%* 0%*% provided by top-ten 59% 100% 100% 59% 28% 30% 42%*= probablySource: ’t Hart, ‘Public loans and lenders’; NA Financie van Holland 3.01.29, inv nos 245, 246, 249,250, 251.

54 Still under research.

14

The concentration of the sums provided by the top-ten investors was quite high in the 1620s:varying from some 60 to 100 per cent. The series for Amsterdam showed that after a probablyslow start in the 1610s and the early 1620s the market for obligations had grown more mature.The records for 1625/26 still pointed to a couple of wealthy individual investors withconnections to the The Hague governmental institutions, yet this time the link withAmsterdam was more clearly established. Thus, among the top ten investors, we did findNicolaas (70,000 guilders) and Adriaan (52,000 guilders) Pau – the latter had been pensionary(high secretary) for Amsterdam and was to become later the pensionary for Holland. Heowned a hofstede in Heemstede and was also one of the directors of the powerful VOC, theEast India Company. Others among the top-ten were Cornelis van Lokhorst (34,000 guilders,an Amsterdam paper merchant) and the Amsterdam cloth merchant Jacob Hendrik Servaes(13,000). Cornelis van Lokhorst was also the largest investor (56,937 guilders) among theobligation-buyers of the Holland receiver. Two major Amsterdam institutions boughtobligations: the hospital (gasthuis) with 38,000 and the Regents of the Leper House (12,800).Our only anonymous investor was also among the top ten with 36,000 guilders. Yet besidethese massive sums some smaller investors were noted too, the smallest sum being 200guilders provided by a widow. At the same time, the concentration (funds provided by thetop-ten) diminished to some 30 per cent, but then it seemed to rise again up to some 42 %.

It is a pity we cannot dispose of data concerning the obligations sold by theAmsterdam office after 1665 (apart from the 1790s, see below). It is difficult to concludeanything about the possible development of this major instrument for raising war fundsbetween 1665 and the 1780s. However, for Rotterdam data exist on the obligations soldbetween 1672 and 1692. If we would look at table 7, the Rotterdam obligations seemed tohave turned into a more mature instrument, probably related to a more mature market too.

Table 7. Some characteristics of the Rotterdam obligations (1625-1627, 1672 and 1690/92)Year(s) 1625 and 1627 1672 1690-1692Mean investment 2700 788 1600Median 2000 480 1000Number of investors 9 760 155% anonymous 0% 12% 48%% female investors 37% 27% 46%% collective investors 0% 13% 11%% institutional investors 0% 0,5% 5%% from outside Rotterdam ?% provided by top-ten 100% 13% 23%Source: see table 6; excel-file of Gelderblom and Jonker, Utrecht University.

Comparing the later issues to the first and sparse bonds sold in the 1620s in Rotterdam, thenumber of investors in these bonds had increased tremendously. 1672 was also a year ofimmense war threats. In the 1670s-1690s, the lowest amount was 200 guilders, yet adifference was that in 1672 this was a regularly recurrent amount and in 1690/92 only oneinvestor with this amount was noted: a women with the name Jannetge Willems. Anotherdifference between 1672 and 1690/92 was the amount of the individual bonds. In 1672numerous bonds were noted in all sorts of amounts, such as 706 or 207 or 1071; several bondswere not even in full guilders but specified of how many additional stuivers and penningen.This was quite different from the The Hague offices (in particular after 1626) and Amsterdam,whose officers dealt with the more regular and recurrent amounts. The Rotterdam bonds in1690/92 were often more uniformly worded as 500, 1000, 1500 and 2000.55

55 Bonds sold in irregular amounts (other than 500, 1000, 1200, 2000 and so) made lower prices on the freemarket in the 1760s and 1770s, see analysis Maandelijksche Nederlandsche Mercurius (see below).

15

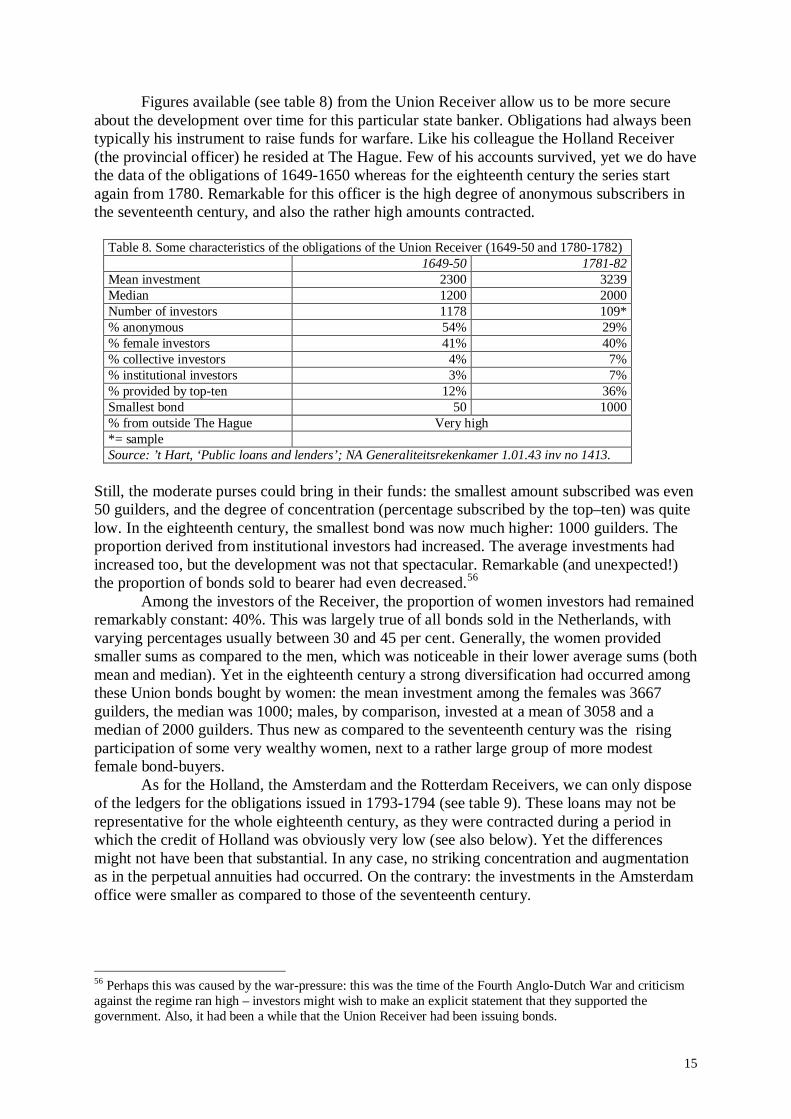

Figures available (see table 8) from the Union Receiver allow us to be more secureabout the development over time for this particular state banker. Obligations had always beentypically his instrument to raise funds for warfare. Like his colleague the Holland Receiver(the provincial officer) he resided at The Hague. Few of his accounts survived, yet we do havethe data of the obligations of 1649-1650 whereas for the eighteenth century the series startagain from 1780. Remarkable for this officer is the high degree of anonymous subscribers inthe seventeenth century, and also the rather high amounts contracted.

Table 8. Some characteristics of the obligations of the Union Receiver (1649-50 and 1780-1782)1649-50 1781-82

Mean investment 2300 3239Median 1200 2000Number of investors 1178 109*% anonymous 54% 29%% female investors 41% 40%% collective investors 4% 7%% institutional investors 3% 7%% provided by top-ten 12% 36%Smallest bond 50 1000% from outside The Hague Very high*= sampleSource: ’t Hart, ‘Public loans and lenders’; NA Generaliteitsrekenkamer 1.01.43 inv no 1413.

Still, the moderate purses could bring in their funds: the smallest amount subscribed was even50 guilders, and the degree of concentration (percentage subscribed by the top–ten) was quitelow. In the eighteenth century, the smallest bond was now much higher: 1000 guilders. Theproportion derived from institutional investors had increased. The average investments hadincreased too, but the development was not that spectacular. Remarkable (and unexpected!)the proportion of bonds sold to bearer had even decreased.56

Among the investors of the Receiver, the proportion of women investors had remainedremarkably constant: 40%. This was largely true of all bonds sold in the Netherlands, withvarying percentages usually between 30 and 45 per cent. Generally, the women providedsmaller sums as compared to the men, which was noticeable in their lower average sums (bothmean and median). Yet in the eighteenth century a strong diversification had occurred amongthese Union bonds bought by women: the mean investment among the females was 3667guilders, the median was 1000; males, by comparison, invested at a mean of 3058 and amedian of 2000 guilders. Thus new as compared to the seventeenth century was the risingparticipation of some very wealthy women, next to a rather large group of more modestfemale bond-buyers.

As for the Holland, the Amsterdam and the Rotterdam Receivers, we can only disposeof the ledgers for the obligations issued in 1793-1794 (see table 9). These loans may not berepresentative for the whole eighteenth century, as they were contracted during a period inwhich the credit of Holland was obviously very low (see also below). Yet the differencesmight not have been that substantial. In any case, no striking concentration and augmentationas in the perpetual annuities had occurred. On the contrary: the investments in the Amsterdamoffice were smaller as compared to those of the seventeenth century.

56 Perhaps this was caused by the war-pressure: this was the time of the Fourth Anglo-Dutch War and criticismagainst the regime ran high – investors might wish to make an explicit statement that they supported thegovernment. Also, it had been a while that the Union Receiver had been issuing bonds.

16

Table 9. Some characteristics of the obligations, by receiver (Union 1781-1782 and Holland,Amsterdam and Rotterdam 1793-1794)

Union (TheHague)

Holland ( TheHague)

Amsterdam Rotterdam

1781-82 1793-1794Mean in guilders 3239 1306 2244 1950Median in guilders 2000 1000 1000 1000Number of investors 109* 63 111 41% female investors 40% 40% 34% 32%% of known investors: collective 7% 5% 18% 7%% of known investors: institutions 7% 13% 3.5% 17%% of all bonds sold anonymous 29% 93% 79% 88%% of the total amount by top-ten 36% 50% 42% 69%Lowest amount supplied by a non-anonymous buyer

1000 100 100 100

Source: NA Financie van Holland 3.01.29 inv no 274, 275; NA Generaliteitsrekenkamer 1.01.43 invno 1413. *=sample

By and all, the number of bonds held by institutions and by collective investors (inheritances,trustees) had increased. In the seventeenth century, these investors had favoured the perpetualannuities; with the decline of the latter, their attention had shifted towards the obligations.Furthermore, the proportion of bonds sold to bearer (anonymous) had increased significantlyfor the Holland bonds (not for the Union bonds, though). This points to a greater flexibility ofthe eighteenth century Holland obligations. These figures suggest that many Holland bond-buyers regarded their investment as a temporary one.

In Amsterdam a similar development as with the Union loans was noticeable: thefemale bond-buyers had grown into a more diversified group too. The mean for womeninvestors was 2337 (median 1000), for men 2007 (median 1000). The public debt system hadthus become more dependent upon a relatively small group of wealthy women. Compared tothe seventeenth century this was a significant reversal of the trend – by and all, femaleinvestors had then supplied less funds (on average, mean and median) seen against the fundsprovided by male bond-buyers. However, this trend was not noticed among the investors ofthe Holland (The Hague) loans, nor at Rotterdam: there, the male investors continued to buylarger bonds as compared to the females.

To a significant degree the standard amount of obligation had become 1000 guilders inthe later eighteenth century, although they could be as small as 100 guilders in the Amsterdamoffice (and also in the Holland The Hague office and in Rotterdam). Yet few investors boughtan obligation of 100 guilders on its own. Most 100-bonds were sold in combination withhigher amounts: for example, an investor could supply 2600 guilders, this was divided over1000+1000+500+100. The reason was that a 1000-obligation made a better relative price onthe market as compared to a 600- or 1600- or 2600- obligation (see below). By and all, thepredominance of the 1000-bonds meant a greater efficiency for the administration of the taxreceivers – thus an improvement as compared to the seventeenth century. Yet this greaterefficiency was noticeable above all at the office of the Union Receiver, less so among theHolland Receivers. The increased efficiency of the Union Receiver counted less as this statebanker declined in importance as compared to the Holland state bankers (see graph 2).57 Thedebt at Union level had risen up to the beginning of the eighteenth century but declined

57 Source: E.H.M. Dormans, Het tekort. Staatsschuld in de tijd der Republiek (Amsterdam 1991) 65-66, 80, 110-111, 139-140, 156, 165. The figures for Holland for 1630 and 1650 are including the Northern Quarter, the laterdata excluding the Northern Quarter.

17

thereafter. Meanwhile, the Holland debt remained much more massive, and even increasedagain later in the eighteenth century.

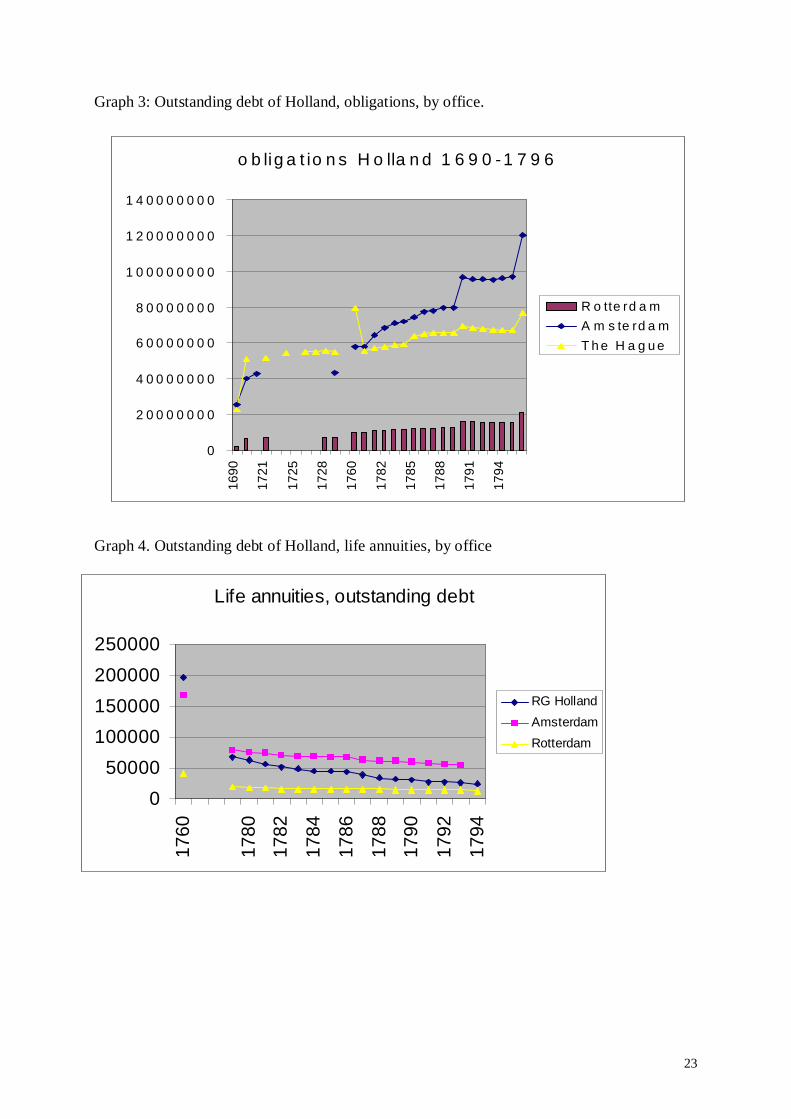

Concentration in Amsterdam bonds

Yet concentration of funds did occur at another level: within the Holland bonds. Graph 3shows that among the obligations, Amsterdam came to dominate the field. For much of theseventeenth century the Holland Receiver at The Hague had been the most important statebanker, yet by the later eighteenth century, Amsterdam took the prime position. Among theHolland state bankers, Rotterdam was the only other office that increased next to Amsterdam;all other Holland offices declined in this regard.58 Also, as for the life annuities, it was clearthat Amsterdam also had issued the largest portion of these highly popular items (see graph4).59 More than in other towns, the Amsterdam elite was thus able to invest in these ratherexpensive sort of bonds.

The growing dependency upon Amsterdam was not such a problem as long as thecredit of the Union and of Holland stood high, which was still a fact up to the 1770s.Throughout the eighteenth century, Dutch public credit had maintained a strong position.Holland and Union bonds were usually sold above par on the free market and it was neverparticularly difficult to get the new loans subscribed.60 The public even complained about therestricted opportunities to invest in state bonds.

Yet in the 1780s Holland’s credit declined, which was shown in the prices an ordinary1000-guilder Holland/Amsterdam obligation made on the public market.61 After the demise ofthe Fourth Anglo-Dutch War (1780-1784) a political movement (Patriot uprising) arose thatstood highly critical to the oligarchic rule.62 Order was restored only in 1787 with support oftroops of the Prussian in-laws of Stadholder William V of Orange. This invasion had adisastrous effect upon public credit, and above all in Amsterdam. Some of the most powerfulAmsterdam banking houses (like Stadnitski) were unwilling to support the Orangistgovernment.63 They demanded the full amnesty and free return of a couple of Patriot rebelleaders before they were willing to come to the rescue of the Dutch state.64

The political factor was not the only problem. The decision-structure of the provincewas still heavily dependent upon the towns.65 In the Holland Estates, no less than eighteen

58 In the eighteenth century, other types of loans were issued, such as lottery loans, twenty-years annuities, thirty-years annuities, yet their distribution over the offices was comparable to the one of the obligations.59 I still have to find out why and how Amsterdam could grab the largest portion of life-annuities.60 Maandelijksche Nederlandsche Mercurius 1760s-1770s noting the prices of the 1000 Amsterdam, Holland andUnion obligations sold at public auctions in Amsterdam. Bonds smaller or other than a 1000-quantity (or 2000 or3000) were obviously less popular.61 Jan Luiten van Zanden and Arthur van Riel, The strictures of inheritance. The Dutch economy in thenineteenth century (Princeton 2004) 39.62 Simon Schama, Patriots and liberators. Revolution in the Netherlands 1780-1813 (Oxford 1977).63 See also J.M.F. Fritschy, De patriotten en de financiën van de Republiek. Hollands krediet en de smallemarges voor een nieuw beleid (1795-1801) The Hague 1988) 197, 291; James Riley, International governmentfinance and the Amsterdam capital market (Cambridge 1980) 56.64 A.J. van der Meulen, Studies over het ministerie van Van de Spiegel (Leiden 1905) 337. At the same time,subscription to the bonds of the Union Receiver (The Hague) showed a strong representation from Orangistcircles. Perhaps that was the reason also that the Union bonds were less sold to bearer (see table 8): the investorswere proud to be known as supporters of the regime. Members of the Orange family, next to militarycommanders, for example, were major creditors of the Union Receiver in the 1780s.65 In this respect I am of the opinion that local particularism was still very strong in the Dutch Republic –although the funds raised for war purposes were provincial the control of the towns over these resources was stillsubstantial. See also J.L. Price, Holland and the Dutch Republic in the seventeenth century. The politics ofparticularism (Oxford 1994) and the critique on the particularist concept by Wantje Fritschy, ‘Three centuries of

18

individual towns (and the nobility) had to agree before a loan could be issued. In 1788, newloans were urgently needed. As the traditional voluntary arrangements had not yieldedsufficient funds, a forced loan was proposed. But Gorinchem (one of the smaller towns)refused to agree. This problem could be solved, as usual, through ‘persuasie’. Yet a far moreserious problem was the opposition by Amsterdam. This mighty town only wished to agreeunder the condition that a significant part of the loan was used to support the Dutch East IndiaCompany, the VOC, that was heavily indebted. The central authorities though had otherpriorities: the payment of the troops and the support for the admiralties. In the end, there wasno other way than to comply to Amsterdam – from the 57 million guilders that came in (partlythanks to the positive influence of the banking house Van der Hope), 21 million guilders wasgranted to the VOC as a subsidy.66

Amsterdam’s political leadership had become increasingly entangled with that of theVOC. The directors of that company had always been strongly represented in Amsterdam’sruling elite. That was not such a problem for the Union as a whole in the seventeenth century,as long as the colonial enterprise expanded and yielded enormous riches that could be taxedand invested again in public debts.67 In fact, the numerous networks in trade and power thatexisted then allowed for a relatively efficient way to organise (colonial) warfare. Yet the sameclose-knit networks proved a strong stumbling-block for an efficient allocation of the fundswhen the VOC lost ground in the international competition in the later eighteenth century.Next to the obvious entwining of interests, the Amsterdam economy was quite dependentupon the VOC too. The threat uttered by the VOC-leadership that they had to close theirworkshops and wharves alone raised the motivation to demand state loans to support thecompany. In fact, this multinational managed to dictate much of Amsterdam’s politicaldecisions (and hence the Union’s policies). Thus the growing dependency of public credit onthe Amsterdam market turned out not an efficient asset for the Dutch Republic as a whole.

Of course, other policies were possible to support Holland’s loans in the difficult timesof the 1780s. One of the obvious possibilities was the levy of a duty upon the bonds that hadbeen sold by foreign governments in the Netherlands. In fact, the Holland and Union annuitiesand obligations yielded a nominal 4 per cent, yet after taxes only 2.5 per cent remained.68 Thebonds sold by France, Sweden, Denmark, Russia, Mecklenburg, Poland, Austria and theUnited States yielded at least 4 per cent and often higher interest rates. Dormans hascalculated that Dutch investors received annually about 27 million guilders from theseinvestments. 69 Moreover, they were not subject to the same heavy taxes. An imposition of atax upon these bonds would easily have improved Holland’s credit. Yet again, like with new

urban and provincial public debt’, in: Marc Boone, Karel Davids and Paul Janssens (eds), Urban public debts,75-92, on p. 91-92.66 Van der Meulen, Studies, 351-352. It was no solution; the VOC remained dependent upon subsidies time andagain, they could not get out of their debts any more. The proposal to put the VOC under legal restraint(curatele) – not such a strange proposal in view of the enormous difficulties of the VOC- was of coursehaughtily rejected by the Amsterdam authorities. Ibidem 355. Meanwhile, the VOC had the opportunity to issueloans upon its own, by taking their own vast assets as a surety – yet that policy was refused as not desirable. It isquestionable whether that could have saved the VOC at all, see also Femme Gaastra, Geschiedenis van de VOC166-170, 173.67 Femme Gaastra, Bewind en beleid bij de VOC. Financiële en commerciële politiek van de bewindhebbers,1672-1702 (Zutphen 1989) 255-258; Julia Adams, ‘Trading states, trading places: the role of patrimonialism inearly modern Dutch development’, Comparative Studies in Society and History 36 (1994) 319-355; Marjolein ’tHart, ‘Networks of trade and power. The raising of war funds and the East India Company Directors inseventeenth-century Amsterdam’, forthcoming (2006).68 R. Liesker en W. Fritschy, Gewestelijke financiën van de Republiek der Verenigde Nederlanden. Holland1572-1795 (The Hague) 371, 382.69 Dormans, Het tekort, 127; Ibidem, 179: a tax that would have reduced these incomes to a comparabe 2,5 percent would have yielded the Dutch state a fine 12 million guilders annually which could have serviced a hugeloan, even at the higher rate of 5 per cent.

19

loans, new taxes also had to be agreed upon in the Estates of Holland before they could beimplemented – and again, Amsterdam refused to agree, thus this was a dead-end street also.

Concluding: Dutch advantages over the English in the eighteenth century?

It is time to turn again to England. In several respects, both the Dutch and the Englishfinancial revolutions shared important characteristics. Both were able to draw upon massiveloans in order to find the means for the ever increasing war-costs in the eighteenth century.Both were able to do so without a structural damage to public credit. The trust of the investingpublic in government bonds was extremely large. Both systems were supported by anenormous number of domestic creditors. 70 Both could serve the interest-payments out of anefficient tax-system.71 And both had stock markets that supported the system of public creditagain by stimulating the free trade in government bonds.

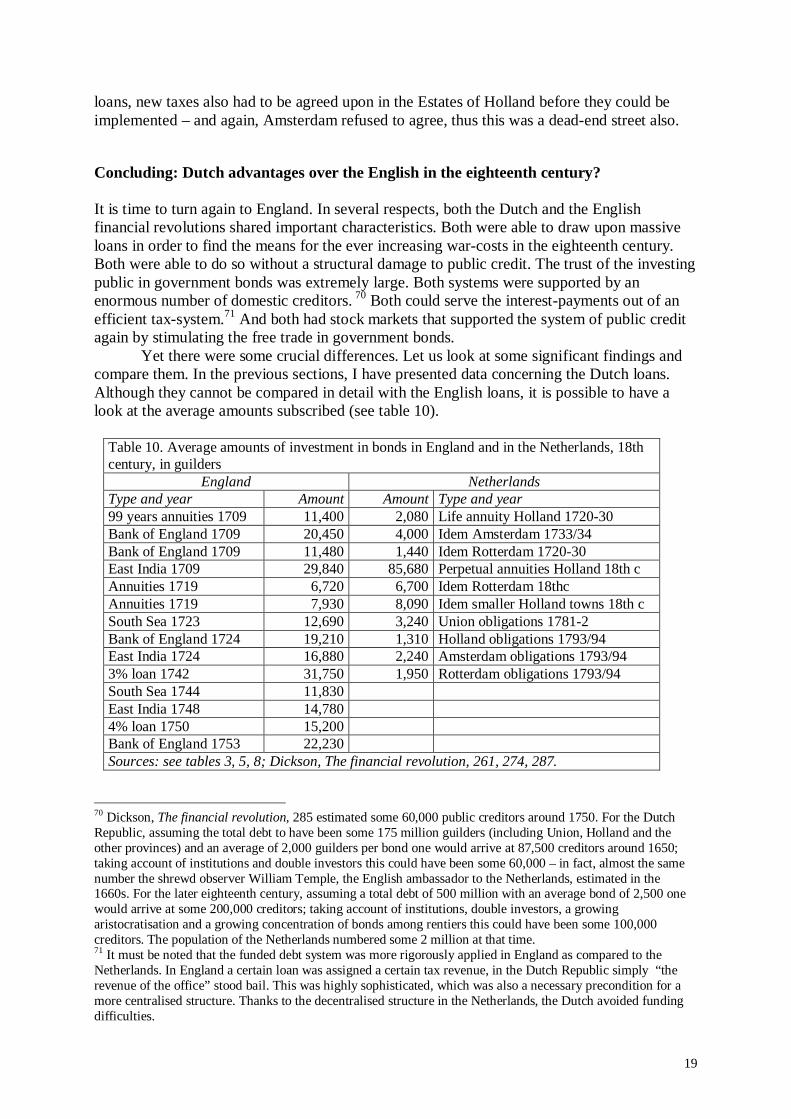

Yet there were some crucial differences. Let us look at some significant findings andcompare them. In the previous sections, I have presented data concerning the Dutch loans.Although they cannot be compared in detail with the English loans, it is possible to have alook at the average amounts subscribed (see table 10).

Table 10. Average amounts of investment in bonds in England and in the Netherlands, 18thcentury, in guilders

England NetherlandsType and year Amount Amount Type and year99 years annuities 1709 11,400 2,080 Life annuity Holland 1720-30Bank of England 1709 20,450 4,000 Idem Amsterdam 1733/34Bank of England 1709 11,480 1,440 Idem Rotterdam 1720-30East India 1709 29,840 85,680 Perpetual annuities Holland 18th cAnnuities 1719 6,720 6,700 Idem Rotterdam 18thcAnnuities 1719 7,930 8,090 Idem smaller Holland towns 18th cSouth Sea 1723 12,690 3,240 Union obligations 1781-2Bank of England 1724 19,210 1,310 Holland obligations 1793/94East India 1724 16,880 2,240 Amsterdam obligations 1793/943% loan 1742 31,750 1,950 Rotterdam obligations 1793/94South Sea 1744 11,830East India 1748 14,7804% loan 1750 15,200Bank of England 1753 22,230Sources: see tables 3, 5, 8; Dickson, The financial revolution, 261, 274, 287.

70 Dickson, The financial revolution, 285 estimated some 60,000 public creditors around 1750. For the DutchRepublic, assuming the total debt to have been some 175 million guilders (including Union, Holland and theother provinces) and an average of 2,000 guilders per bond one would arrive at 87,500 creditors around 1650;taking account of institutions and double investors this could have been some 60,000 – in fact, almost the samenumber the shrewd observer William Temple, the English ambassador to the Netherlands, estimated in the1660s. For the later eighteenth century, assuming a total debt of 500 million with an average bond of 2,500 onewould arrive at some 200,000 creditors; taking account of institutions, double investors, a growingaristocratisation and a growing concentration of bonds among rentiers this could have been some 100,000creditors. The population of the Netherlands numbered some 2 million at that time.71 It must be noted that the funded debt system was more rigorously applied in England as compared to theNetherlands. In England a certain loan was assigned a certain tax revenue, in the Dutch Republic simply “therevenue of the office” stood bail. This was highly sophisticated, which was also a necessary precondition for amore centralised structure. Thanks to the decentralised structure in the Netherlands, the Dutch avoided fundingdifficulties.

20

This comparison was revealing: virtually all loan types in England drew upon significantlarger amounts as compared to the Dutch Republic. The only larger Dutch loans were theperpetual annuities issued by the Holland Receiver, yet I had noted that these loans were quiterare. Moreover, those loans were hardly subscribed on the “open market”, as 97 per cent wasprovided by institutions. The English system was thus more efficient in raising sizeable warfunds. Moreover, the English state relied more upon financial consortia and upon financialintermediaries to get the loans subscribed, which improved the speed of getting the funds in.72

The role of the Bank of England and of the colonial companies must be mentioned in thisregard again. Whereas in England the colonial companies served the interests of the state atwar, the previous section has shown that in Holland they had grown into milestones aroundthe Republic’s neck.73

Typically, the English financial revolution rested upon the wealthier groups in societyas compared to the Netherlands (perhaps one could say: in the Netherlands the financialrevolution rested upon those with a higher political office, at least in the eighteenth century).The lowest English bond had been 10 pounds (=100 guilders), in the lottery loans of the1690s, yet with most of the stock emissions the smallest denomination was always 100pounds (=1000 guilders). At the same time, the number of collective subscriptions wassomewhat higher in England: varying between 9 and 18 per cent, depending upon the type ofloan.74 Corresponding to the higher average amounts in England the proportion of femaleinvestors was somewhat lower as compared to the Netherlands too – indeed, also in Englandthe investments by women were smaller as compared to those of the male creditors.75

Nevertheless, women creditors constituted a considerable minority in the English financialrevolution, usually varying between 17 and 32 per cent. Probably, this was consistent with atypical persistent motivation to invest in government bonds: they were highly secure, both inEngland and in Dutch Republic, and thus served the creditors’ strategies to reduce risks anduncertainties in the future.

Another crucial difference was the degree of foreign investors. Dutch public credit wasowned virtually totally by domestic investors only. To a high degree the town receivers weresupported by their own townsmen also. The English system profited much more frominvestors from abroad, above all from the Netherlands. Dickson assumed that around 15 percent of the English public debt was in hands of Dutch investors.76 That portion has beendebated by other historians; nevertheless, whatever the exact size, thanks to the continuousflow of funds from the Netherlands the British managed to weather the storms caused by thesoaring expenses during the Seven Years’ War: it held down interest rates on the long-termdebt.77 In that respect the English financial revolution had the advantage that when it was wellon its way, the stock market was already much more mature; when the Dutch financialrevolution started, the stock market was still in its infancy.78 The Dutch public creditcontinued on the line which had been quite profitable in the seventeenth century, yet which

72 Dickson, The financial revolution, 217, 220.73 Julia Adams, ‘Principals and agents, colonialists and company men: the decay of control in the Dutch EastIndies’, American Sociological Review 61 (1996) 12-28.74 Dickson, The financial revolution, 287.75 See for the proportion of women investors in England Ibidem, 268, 281, 287.76 Ibidem, 304 ff.77 Larry Neal, ‘Interpreting power and profit in economic history: a case study of the Seven Years War’, TheJournal of Economic History 37 (1977) 20-35, 35.78 See also Ann Carlos, Larry Neal, Kirsten Wandschneider, ‘The origins of national debt: the financing and re-financing of the War of the Spanish Succession’, paper EHA annual meeting, Toronto 14-16 september 2005.Another difference that should be taken into account was that the predominant bonds in England were long-term,thus prone to be traded on the market, whereas the predominant bond in the Netherlands was the obligation,which could be changed for ready money every six months. Thus in this way again the English bonds stimulatedactivity of the stock market too, which was less the case for the Netherlands.

21

failed to grasp the opportunities of the expanding international financial markets.79 Imaginethe difference a tradition of foreign investors would have made in the 1780s, when the Dutchpublic itself was unwilling to buy bonds – perhaps the Netherlands could have overcome thepolitical crisis and interest rates might have remained lower.

Again the earlier mentioned aspect of centralised control in the English case should bestressed. The kind of concentration that occurred in the Netherlands, towards a growingdependency upon the Amsterdam capital market, turned out a disadvantage when politicaldevelopments separated the goals between Patriots (strong in Amsterdam) and Orangists(strong in The Hague). Both towns had commanded always the largest potential investors –with the political rift the Dutch capital market got even more split up.

Perhaps we should try to find some advantages for the Dutch too. Surely, without thefinancial revolution, the Netherlands could not have maintained its independent status for solong. The system of obligations had rendered the management of the Dutch public debt quiteflexible. Perhaps the comparison with England has pictured the Dutch system too obsolete inthis paper; in comparison with most other European states the Republic’s credit was stillstrong. The investing public in the Netherlands was remarkably diversified, due to thedecentralised setting of the state bankers. The participation in the public credit by so many inthe Netherlands furthered the relative peacefulness of the Dutch state and secured thedomestic income from tax revenues (up to the Patriot movement, of course).80