Embed Size (px)

Citation preview

Michael Culver TEP CTAPS Associate Solicitor and Team Leader

Bolt Burdon Solicitors [email protected]

020 7288 474107833 239187

Care Home Planning: The Care Act 2014

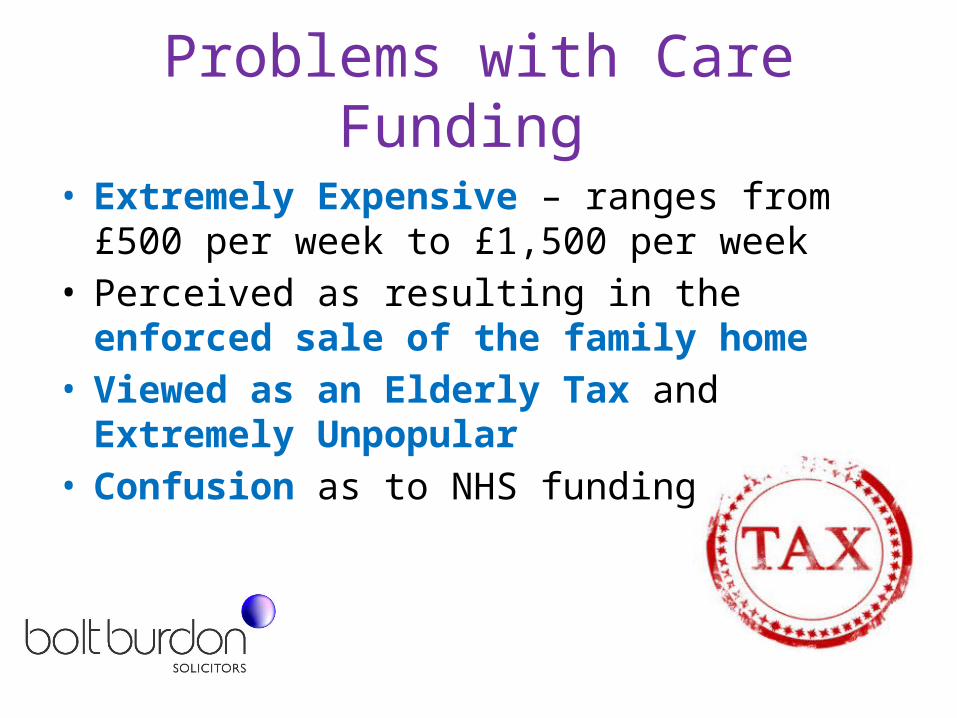

Problems with Care Funding

• Extremely Expensive – ranges from £500 per week to £1,500 per week

• Perceived as resulting in the enforced sale of the family home

• Viewed as an Elderly Tax and Extremely Unpopular

• Confusion as to NHS funding

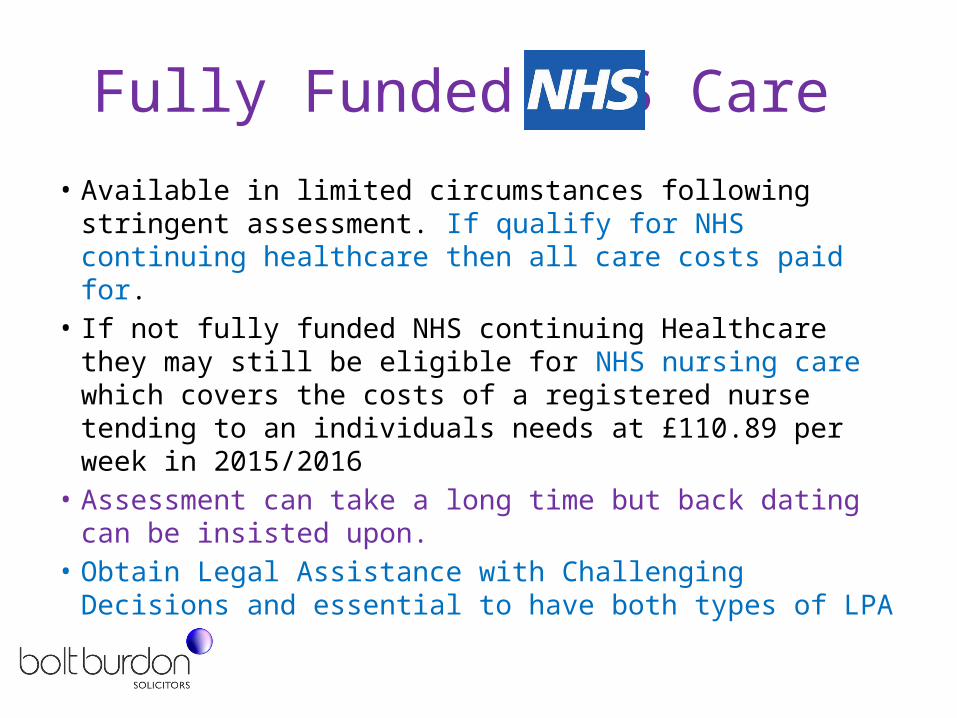

Fully Funded NHS Care

• Available in limited circumstances following stringent assessment. If qualify for NHS continuing healthcare then all care costs paid for.

• If not fully funded NHS continuing Healthcare they may still be eligible for NHS nursing care which covers the costs of a registered nurse tending to an individuals needs at £110.89 per week in 2015/2016

• Assessment can take a long time but back dating can be insisted upon.

• Obtain Legal Assistance with Challenging Decisions and essential to have both types of LPA

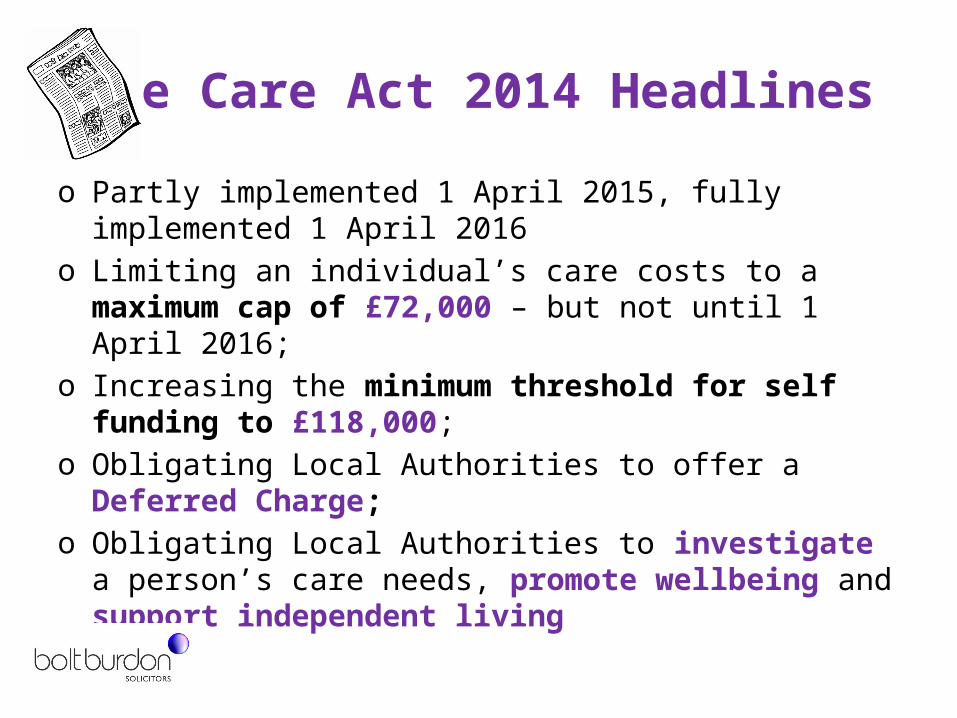

The Care Act 2014 Headlines

o Partly implemented 1 April 2015, fully implemented 1 April 2016

o Limiting an individual’s care costs to a maximum cap of £72,000 – but not until 1 April 2016;

o Increasing the minimum threshold for self funding to £118,000;

o Obligating Local Authorities to offer a Deferred Charge; o Obligating Local Authorities to investigate a person’s

care needs, promote wellbeing and support independent living

Maximum Cap of £72,000

• Not all payments go towards the cap Only core care costs

Hotel costs not included i.e. heating, electricity, food etc.

Still make some contributions even when the cap is reached

Example:

So if paying £1,500 per week for care an amount as low as £270 per week may be going towards the cap meaning the person involved would be in the care home for 22 years before the cap is reached and in that time they would have paid £1.7m towards their care

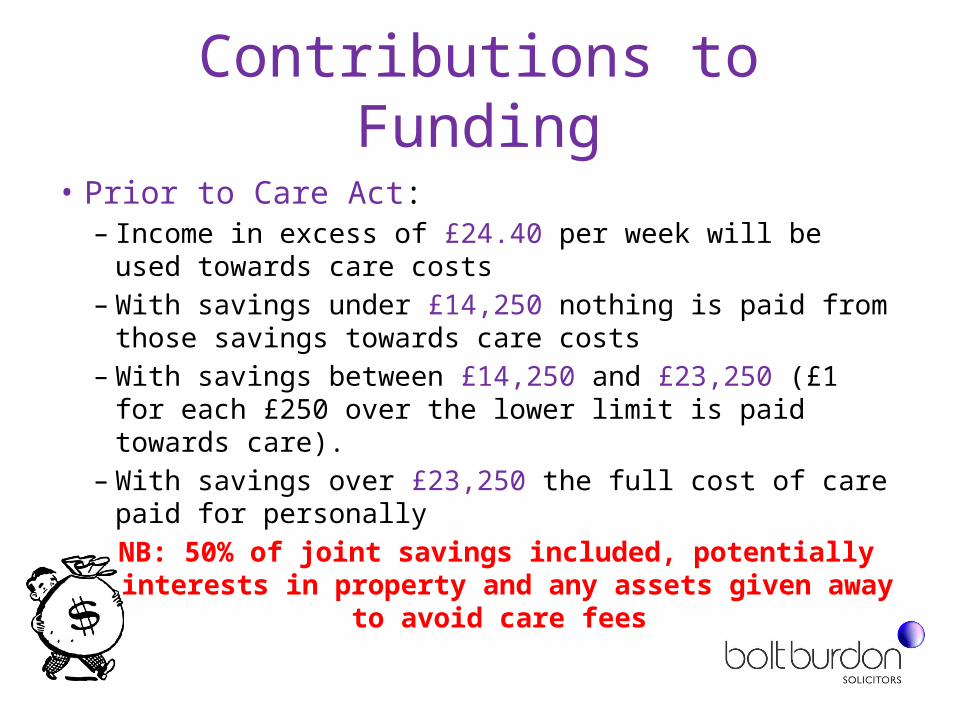

Contributions to Funding

• Prior to Care Act: – Income in excess of £24.40 per week will be used

towards care costs – With savings under £14,250 nothing is paid from those

savings towards care costs – With savings between £14,250 and £23,250 (£1 for

each £250 over the lower limit is paid towards care). – With savings over £23,250 the full cost of care paid for

personally

NB: 50% of joint savings included, potentially interests in property and any assets given away to

avoid care fees

Contributions to Funding

• Following the Care Act – Lower limit remains £14,250 (increasing to

£17,000 in 2016)– Upper limit increased to £118,000 (but only to

£27,000 if the property is disregarded!) – £1 for every £250 over lower limit continues to be

paid towards care in addition to income over £24.40 per week

If a person has £117,000 in savings then they will pay £400 per week (£20,800 per year towards their care plus their available income).

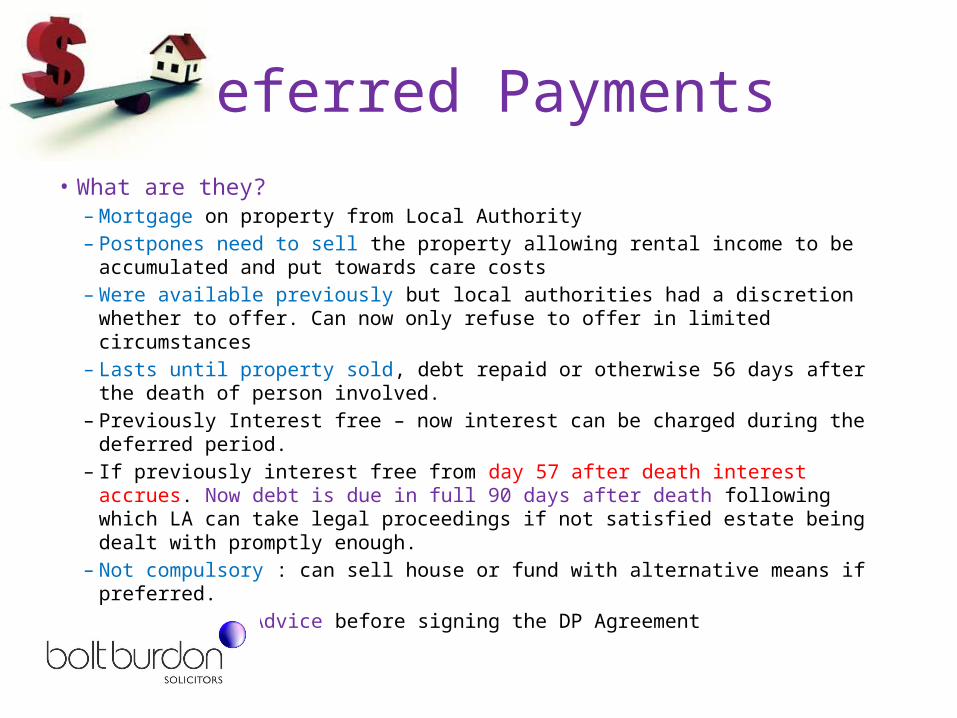

Deferred Payments

• What are they? – Mortgage on property from Local Authority – Postpones need to sell the property allowing rental income to be

accumulated and put towards care costs – Were available previously but local authorities had a discretion whether to

offer. Can now only refuse to offer in limited circumstances – Lasts until property sold, debt repaid or otherwise 56 days after the death

of person involved.– Previously Interest free – now interest can be charged during the deferred

period.– If previously interest free from day 57 after death interest accrues. Now

debt is due in full 90 days after death following which LA can take legal proceedings if not satisfied estate being dealt with promptly enough.

– Not compulsory : can sell house or fund with alternative means if preferred.– Obtain Legal Advice before signing the DP Agreement

Local Authority Obligations

• To access care needs and separately to access funding

• Over four years to March 2014 LA’s budgets for adult social care reduced by £2.68 billion

• How will they cope?

What not to do

• Take advice in the pub • What is suitable for one family may be totally unsuitable for another

• Rely on “my kids will sort this for me” • This is often said with all the best intentions but can be deeply regrettable if

measures/plans not made in advance

• Protected Property Trusts Opinions vary but downsides are: – Costs– No Guarantee will work– House belongs to trustees – duty to act in beneficiaries interests subject to any

limitations – Tax implications of Trust on creation/every ten years and when payments made

from it

What not to do

• Give House to Children/other relatives during lifetime – Does not work – anti avoidance provisions – Risks – divorce, bankruptcy, falling out with children, death of children without adequate wills in

place – No effect for tax planning and can lead to capital gains tax being paid by non owners in addition to

Inheritance tax

• Sell House to children– To repay mortgage for example – If sold at an undervalue the result is the amount of the under value

being used in care calculations– If child obtains a mortgage on own home or extends own mortgage consider placing a charge on

parents property – Funds used must pass to parents or otherwise be used to pay off their debts/mortgages. If not or

otherwise suggestion of gifting funds back to children then entire property still used in assessment

• Be fooled by the 7 year rule – This is for inheritance tax purposes not care home planning!

What not to do

• Set up a joint account with main caring child • Child has control of funds• Inherits balance on death irrespective of will • Can be viewed as asset deprivation • Transactions looked upon with suspicion• Lasting Power of Attorney achieves the same desired result and more

• Sell house and use proceeds to extend children's home for accommodation.

– If relationship becomes strained no protection unless Trust/charge put in place which then evidences parents ownership/interest

– Divorce, bankruptcy, death problems as discussed earlier – Reasons behind gift i.e. Avoiding care likely to be investigated and deemed suspicions leading

to costly challenges

What Can we do?

Essential Steps:

1. Lasting Powers of Attorney – both types essential

2. Prior to needing care - Independent Financial Advice – planning for additional income

3. At time of needing care - Legal Advice re funding options

4. Tenants in Common

5. Life Interest Trust in Wills

Any Questions?

Bolt Burdon Solicitors

Please contact us with enquiries:

Michael CulverE: [email protected] T: 020 7288 4741M: 07833 239187

![HILLESLEY HAPPENINGS · Whitbread [07833 491242] 4farmcotian@gmail.com The JFMC held their AGM on 7th February with the main areas of discussion being around the future of the field](https://img.dokumen.tips/doc/110x75/5fb4563ae2ad4126e53cecf3/hillesley-happenings-whitbread-07833-491242-4farmcotiangmailcom-the-jfmc-held.jpg)