Embed Size (px)

Citation preview

© 2015 FARIN & Associates Inc.

Liquidity BasicsMeasuring and Managing Liquidity

Urum Urumoglu

Senior [email protected]

800-236-3724 x4210

1

© 2015 FARIN & Associates Inc.

Course Agenda

• Understanding Nature of Liquidity

– Definition of Liquidity

– Traditional Regulatory Measures

– How to Classify Sources and Uses

– Causes of Liquidity Risk in FI’s

– Regulatory Actions and Expectations

• Building New Measurement Framework

– Liquidity Coverage Ratio (LCR)

– Net Stable Funding Ratio (NSFR)

– Cash Flow Liquidity Gap (Sources & Uses)

2

© 2015 FARIN & Associates Inc.

What is Liquidity & Where Does it

Come From?

3

© 2015 FARIN & Associates Inc.

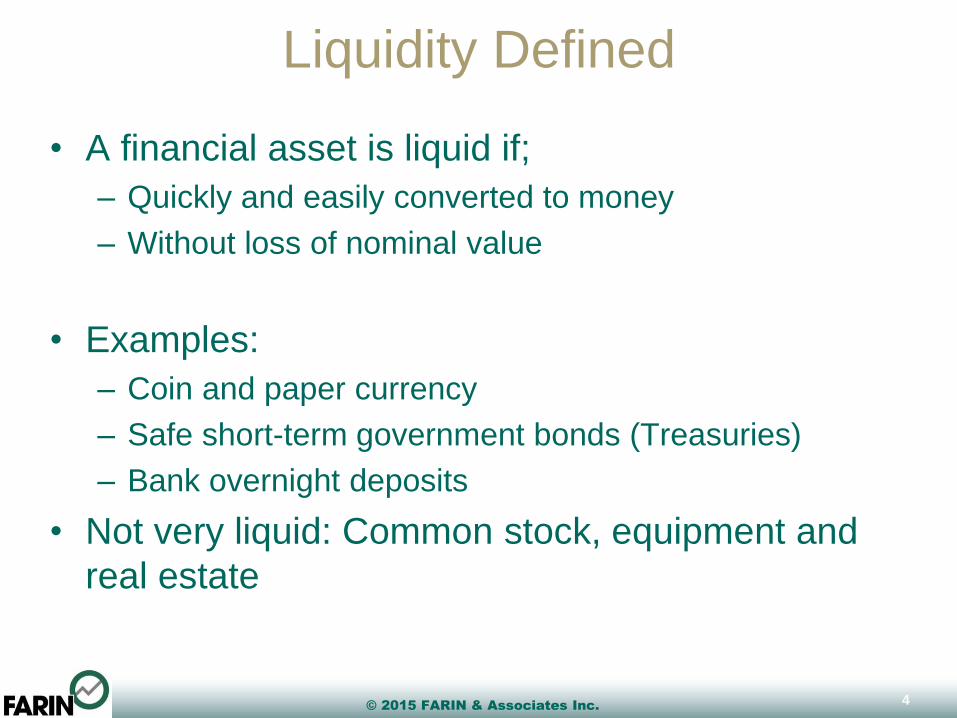

Liquidity Defined

• A financial asset is liquid if;

– Quickly and easily converted to money

– Without loss of nominal value

• Examples:

– Coin and paper currency

– Safe short-term government bonds (Treasuries)

– Bank overnight deposits

• Not very liquid: Common stock, equipment and

real estate

4

© 2015 FARIN & Associates Inc.

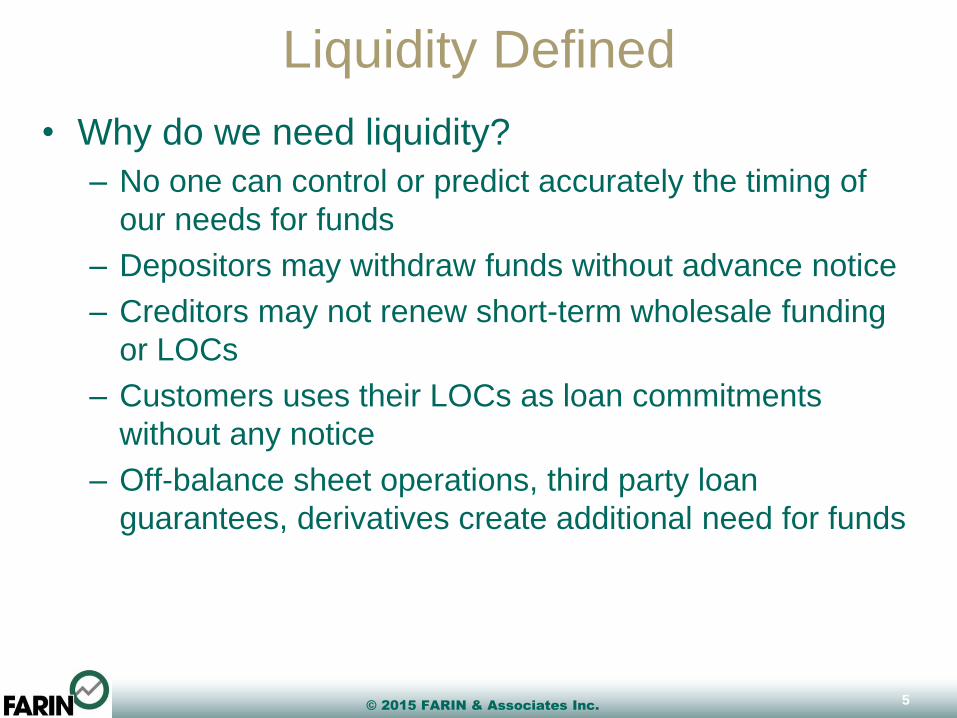

Liquidity Defined

• Why do we need liquidity?

– No one can control or predict accurately the timing of

our needs for funds

– Depositors may withdraw funds without advance notice

– Creditors may not renew short-term wholesale funding

or LOCs

– Customers uses their LOCs as loan commitments

without any notice

– Off-balance sheet operations, third party loan

guarantees, derivatives create additional need for funds

5

© 2015 FARIN & Associates Inc.

Liquidity Defined

• Liquidity is:

– The ability to meet demands for cash

at a reasonable cost.

• Liquidity Risk is:

– The risk that the institution may not

have sufficient sources of cash to

meet demands

• What would cause changes in

liquidity levels or needs

• ALM Process measures risks

taken versus returns derived.

– Risk is to be MANAGED, not

MITIGATED

6

Asset/Liability Management

Interest Rate Risk

Credit RiskRegulatory

Risk

Liquidity Risk

© 2015 FARIN & Associates Inc.

• FDIC/OCC/Federal Reserve Liquidity Definition:

– The capacity to readily meet cash and collateral

obligations at a reasonable cost.

– Maintaining Adequate levels depends on the institution’s

ability to meet expected and unexpected cash flow and

collateral needs without adversely affecting daily

operations or financial performance

– Sources

• Assets readily convertible to cash

• Net operating cash flows

• Ability to acquire funding through

– Deposits

– Borrowings

– Capital Injections

7

Liquidity Defined

© 2015 FARIN & Associates Inc.

• Mismatch Risk

– Insufficient cash to meet obligations in normal course

• Market Liquidity Risk

– Market constraints will affect the conversion of assets

into cash

• Contingent Liquidity Risk

– Risk from unexpected events

8

Types of Liquidity Risk

© 2015 FARIN & Associates Inc.

• Sources of Liquidity Risk :

– Funding Mismatches

• Not enough funding to meet withdrawal needs

– Market constraints on ability to convert assets into cash

or inability to access sources of funds (market illiquidity)

– Contingent Liability Events

• Line of Credit Usage

• Loan commitments

– Changes in Economic Conditions

– Exposure to credit, market, operational, legal, and

reputation risks

9

Liquidity Risk

© 2015 FARIN & Associates Inc.

Financial Institutions Risk Management

Financial & Business Risk Management

Financial Risks

Liquidity Risk

Maturity Mismatch

Asset/Liability Imbalance

Cash Flow

Credit Risk

Default

Downgrade

Counterparty

Interest Rate Risk

Commodity Prices

Equity Prices

Interest Rate Changes

Business Risks

Management Risks

Strategic Risk

Operational Risks

People Risks

Legal Risks

System Risks

External Risks

10

© 2015 FARIN & Associates Inc.

Financial Institutions Risk Management

• Prior Diagram Indicates “Silos” of Risk

– Liquidity Is Managed and Measured separate from Credit, Interest

Rate, etc.

• Reality is that the risks are interrelated

– Liquidity Risk may cause market and credit risk

– Credit and interest rate risk can cause liquidity risk

• In addition to cross risk measures within an area,

institutions must consider cross area risks

– How do staff relationships impact financial performance?

• Reputation risk?

• Legal risks?

– How are Business Risks related to Financial and Operational

Risks?

11

© 2015 FARIN & Associates Inc.

Factors Effecting Liquidity Risk

Internal Factors

• High levels of off balance

sheet exposure

• Heavy reliance on corporate,

brokered or wholesale funding

• Maturity mismatches

• Rapid asset growth in excess

of deposits

• Short term deposit

concentrations

• Lack of unencumbered,

marketable securities

External Factors

• Highly sensitive depositors

• Fragile financial markets

• Low economic performance

• Lack of trust in banking sector

12

© 2015 FARIN & Associates Inc.

Liquidity Risk Management

• Maintaining balance between

available sources vs. needs while

meeting capital planning goals for:

– Earnings

– Growth

– Capital

• Expected & potential scenarios

• Effective liquidity management

helps produce maximum levels of

earnings

– by investing excess funds

– While maintaining sufficient flows

and sources of funds

13

© 2015 FARIN & Associates Inc.

• Examination Consideration:

– Access to funding sources

– Overall Cost of Funds

– Undue reliance on wholesale or market based funding

(brokered CDs)

– Contingency Plan

• So, we now have the premise and scope of the

examination process, what do we need to do?

14

Liquidity Examination

© 2015 FARIN & Associates Inc.

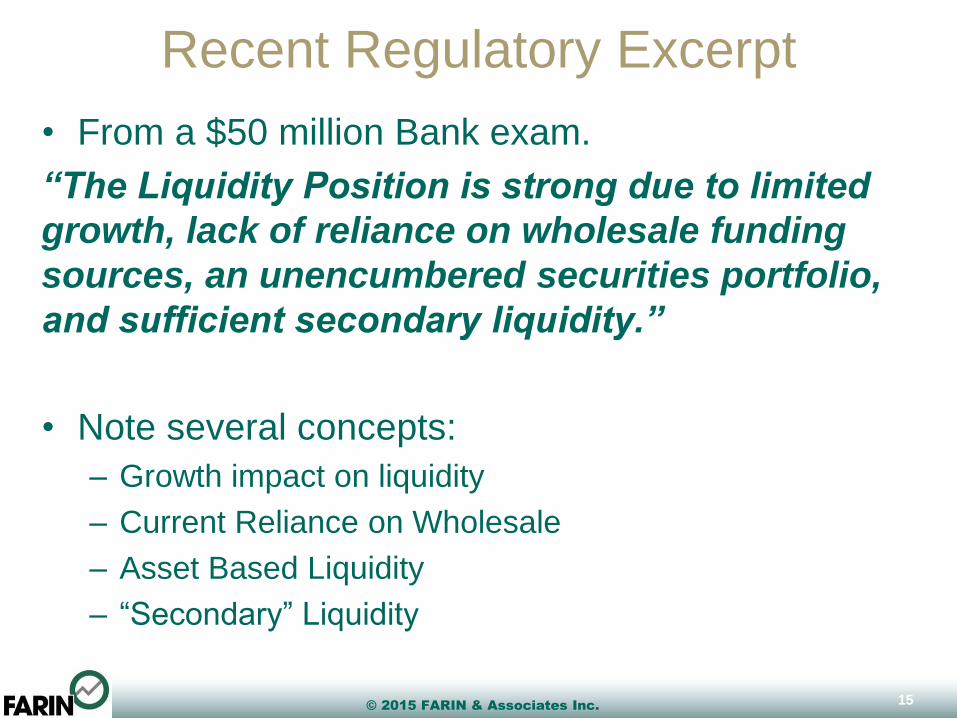

Recent Regulatory Excerpt

• From a $50 million Bank exam.

“The Liquidity Position is strong due to limited

growth, lack of reliance on wholesale funding

sources, an unencumbered securities portfolio,

and sufficient secondary liquidity.”

• Note several concepts:

– Growth impact on liquidity

– Current Reliance on Wholesale

– Asset Based Liquidity

– “Secondary” Liquidity

15

© 2015 FARIN & Associates Inc.

Recent Regulatory Excerpt

• From a $100 million Bank exam.

“On-balance sheet liquidity has declined due to

recent deposit withdrawals. Cash equivalents

declined from 17.29% of total assets to 13.36%

which is comparable to peer levels. The bank

does not have a securities portfolio to serve as a

secondary source of liquidity which has resulted

in a ratio of loans to deposits of 103% compared

to the peer median of 70.17%”

• This bank received a downgrade to a 2 rating

16

© 2015 FARIN & Associates Inc.

Recent Regulatory Initiatives

• 2010 - “Interagency Policy Statement –

Funding and Liquidity Risk Management”

– Issued 4/5/10 – FRB, OCC, FDIC, OTS, NCUA

Liquidity Requirements

• More asset based liquidity (cash & securities)

– No guidance on how much is enough!

– Why: It is the only form of liquidity you can absolutely count

on being there during a liquidity stress event

• Less reliance on wholesale funding for core growth

– What is your core funding plan?

– Where will you raise the funding needed to:

• Increase investments?

• Reduce non-core funding?

17

© 2015 FARIN & Associates Inc.

Impact of 2010 Liquidity Guidance

Liquidity Requirements

• Cash Flow Based Liquidity Measurement

– How do we to integrate with IRR measurements

• Stress Tests

– Like Rate Shocks in IRR?

– What kinds of stress tests do we have to run?

• Adverse and Severely Adverse scenarios

– How frequently do we run them?

18

© 2015 FARIN & Associates Inc.

Historical Measures of Liquidity

• Measurements Based on Balance Sheet Levels

– Static Measurements

– Historically Based

• Examples:

– Short Term Assets / Short Term Liabilities

• Measures coverage of possible loss of funding with assets

– Volatile Funds Ratio

– Borrowings / Total Assets

• Measures the level of non-market funding sources used to build the

balances sheet

• Total Loans / Total Assets

– Basic Surplus Ratio

• All Sources minus Uses within 30 days / Total Assets

• Target Ratio = 3-5% minimum

19

© 2015 FARIN & Associates Inc.

UBPR/FPR RatiosBank UBPR Ratios

• Net Non-Core funding ratio

• Loans/Assets

• Projection of Net Cash Flows

Credit Union FPR Ratios

• Net Long-term assets/Total Assets

• Total Loans / Total Shares

• Cash & ST Investments / Total Assets

• Total Shares, Deposits & Borrowings / Earning Assets

• Regular Shares & Share Drafts / Total Shares &

Borrowings

• Borrowings / Total Shares & Net Worth

20

© 2015 FARIN & Associates Inc.

Regulatory Ratio Definitions

• Net Non-Core Funding Ratio: Measures the extent

to which the bank if funding longer term assets (>

1 Yr.) with volatile funds.

– non-core liabilities, less short-term investments divided

by long-term assets

– Non-core funding is funding that can be very sensitive to

changes in interest rates such as brokered deposits,

CDs greater than $100,000, and borrowed money

• Loan/Assets: Measures the extent to which the

bank is likely to have liquidity

– Higher Loan/Asset ratios reduces liquidity levels

– Lower Loan/Asset ratios impacts earnings & capital

21

© 2015 FARIN & Associates Inc.

Regulatory Ratio Definitions

• Long term assets / Total Assets: Measures the

level of long term assets that are less liquid

– sum of real estate loans which will not refinance, reprice

or mature within 5 years, member business loans,

investments with remaining maturities of more than 3

years, NCUSIF deposit, land and building, and other

fixed assets divided by total assets.

• Loan/Share – Measures extent to which the CU is

relying on capital or borrowings to make loans

which are less liquid

• Cash & ST Investments /Total Assets: Measures

available short-term liquidity levels

22

© 2015 FARIN & Associates Inc.

Regulatory Ratio Definitions

• Total Shares, Deposits & Borrowings / Earning

Assets: This really measures the efficiency of use

of funding to generate earnings

– If it’s not in a loan or an investment, where is it? Are

buildings and fixed assets liquid?

• Regular Shares & Share Drafts / Total Shares &

Borrowings: Measures the level of “core” type

funding that is considered less volatile

– Really more of an ALM ratio than liquidity

– Higher levels are less volatile, requiring lower liquid

assets

23

© 2015 FARIN & Associates Inc.

Regulatory Ratio Definitions

• Borrowings / Total Shares & Net Worth: Measures

the reliance on non-member funding.

– Higher reliance posed liquidity concerns as the sources

may be unreliable

24

© 2015 FARIN & Associates Inc.

Trigger Ratios

• Definition – Ratios or events being monitored to

assess trends in performance

– UBPR or FPR Ratios

• Used as early warning indicators

• Allows for historical liquidity or call report ratios in

policy without them becoming primary measures.

• They are NOT policy limits

25

© 2015 FARIN & Associates Inc.

Liquidity Definitions vs. Ratios

• Definition: The capacity to readily meet cash and

collateral obligations at a reasonable cost.

• What is missing from all these UBPR/FPR Ratios

and Examination Review?

26

© 2015 FARIN & Associates Inc.

Triggers vs. Limits

• Triggers (Monitoring Ratios) Can be set to

watch for different possible changes to future

liquidity.

– Maturity Mismatch is an indicator of potential risk.

• Measurement of “maturity mismatch” can be an

early warning indicator of possible risks

– A/L Imbalance

• Measure of asset/liability mix vs. goals gives an

easy measure of possible problems

– Cash Flow projections tells more complete story

on potential needs

• Common for monthly ratios to be set on

individual risk components with quarterly

overall limit tests

27

© 2015 FARIN & Associates Inc.

Basic Liquidity Trap

• General Rule:

– The more liquid as asset or liability, the lower the rate

earned or paid

• Regulatory Pressure

– Increased levels of liquid assets

– Lower levels of volatile liabilities

• Large deposits, Brokered CDs

• Impact

– More liquid assets = lower yield on assets

• Downward Pressure on Earnings

– Less Volatile Liabilities = More Core Funding

• How do we raise more core funding?

28

© 2015 FARIN & Associates Inc.

Liquidity Regulations

Asset Side Liquidity Focus

• Excessive holding of asset classes

• Regulations to hold minimum

amount of liquid assets– Cash & deposits in central banks

– Short-term high quality government

bonds

• Losses of asset values, in turn,

depletes bank’s capital

• Market dislocations

Liability Side Liquidity Focus

• Dependency on volatile source of

funds– Uninsured deposits, brokered deposits

– Short-term wholesale borrowings

• Regulations require stable funding– Retail deposits protected by deposit

insurance

– Medium & long-term borrowings

– Capital

• Inability to raise new deposits

29

© 2015 FARIN & Associates Inc.

Minimizing Cost of Liquidity

• Goal of Liquidity Management:

– Ensure sufficient available funds at the lowest possible

cost.

• Requirements of Liquidity Risk Management

Program

– Set objectives around funding costs, funding

concentrations, and other financial ratios

– Establish Cash Flow Forecasting Model to measure

sources & uses in business plan

– Run Scenarios on various funding source cost/benefit

30

© 2015 FARIN & Associates Inc.

Liquidity Sources & Uses

• Asset Sources

– Cash and Cash Equivalents

– Securities or Loans available

for sale

– Maturing Loans & Securities

– Loan & Security repayments

• Liability Sources

– New Deposit Growth

– Borrowing Sources

• Asset Uses

– Loan Originations

– Investment Purchases

– Fixed Asset Purchases

– Draws on Lines of Credit

• Liability Uses

– Deposit Outflows

– Maturing Borrowings

31

Note: Majority of Sources and Uses are based on Cash Flows associated

with assets & liabilities

© 2015 FARIN & Associates Inc.

Major Cash Flow Assumptions

• Option Risk:

– The risk that the expected cash flows change due to

contract options

• Call Options

• Put Options

• Prepayment Options

• Bump Rate CD/Early Withdrawal Options

– Changes in Cash Flows Impact

• Liquidity Levels

• Income Levels

• Potentially Credit Risk Levels

– Lower repayment of loans an indicator of credit problems?

32

© 2015 FARIN & Associates Inc.

Major Cash Flow Assumptions

• Prepayment Speeds on Loans & Securities

– Determining Prepayment Levels

• Schedule Contractual Repayments

• Observe Actual Repayments

• Subtract Actual from Scheduled to arrive at prepayment $

• Convert to annual % prepayment by dividing by average

balance

• Compare to National Prepayment speeds to develop factor

– Example:

• National Bloomberg Prepayment Speeds = 12% CPR

• Calculated Speeds = 8% CPR

• Factor for ALM Model = Bloomberg speeds * 67%

– Use Bloomberg speeds for all changing rates

33

© 2015 FARIN & Associates Inc.

Liquidity Definitions

• Asset Based or Core Liquidity: Cash and other

financial assets that can be easily converted to

cash for operational needs

– Withdrawals

– Originations

• Total (Cash Flow Based) Liquidity : Does your

projection maintain sufficient sources to meet

financial obligations: withdrawals, loan demands

and other commitments.

– To what extent is liquidity changing level and/or form

– Should include measures of debt or borrowing

capacity.

34

© 2015 FARIN & Associates Inc.

Sound Liquidity Practices

• A Comprehensive method for cash flow

forecasting

• Reasonable and appropriate assumptions

• Integrated management information & reporting

system

• Customized reports

• Stress testing

• Ongoing monitoring

• Contingency funding plans

35

© 2015 FARIN & Associates Inc.

MEASURING ASSET BASED

LIQUIDITY

A Practical Approach to Liquidity

36

© 2015 FARIN & Associates Inc.

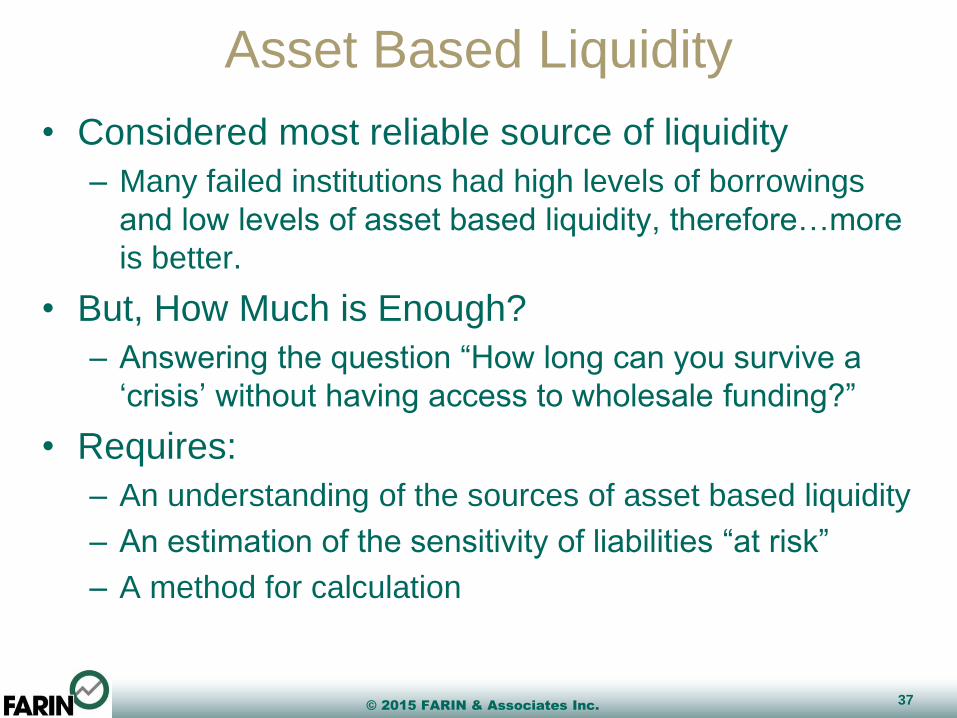

Asset Based Liquidity

• Considered most reliable source of liquidity

– Many failed institutions had high levels of borrowings

and low levels of asset based liquidity, therefore…more

is better.

• But, How Much is Enough?

– Answering the question “How long can you survive a

‘crisis’ without having access to wholesale funding?”

• Requires:

– An understanding of the sources of asset based liquidity

– An estimation of the sensitivity of liabilities “at risk”

– A method for calculation

37

© 2015 FARIN & Associates Inc.

Calculating Asset Based Liquidity

• Sources of Asset Based Liquidity

– Cash & Cash Equivalents (FF, MMA, etc.)

– Unpledged Securities (at market value or deeper discounts)

– Scheduled Investment cash flows and maturities

– Scheduled Loan cash flows and maturities

• Uses that you have to cover

– Firm Loan commitments

– Maturing Borrowings/Non-Core funding

– Maturing CDs

– Some amount of Non-maturity balances considered “at risk”

– Potential draw down on lines of credit

38

© 2015 FARIN & Associates Inc.

Basic Surplus

• Long time measure of 30 day need

39

© 2015 FARIN & Associates Inc.

Basic Surplus

• Add to the basic measure in step 2 – FHLB

availability

40

© 2015 FARIN & Associates Inc.

Basic Surplus

• Add in other non-core funding sources in Step 3

41

© 2015 FARIN & Associates Inc.

Basic Surplus

Advantages

• Easy measure of real

sources

• Quantifies level of sources

by type

• Provides a measure

consistent with policy

control limits

Disadvantages

• Usually used on historical

balance sheet

• Ignores primary source of

most community FI

liquidity

– Loan Repayments!

• Ignores Off Balance Sheet

Risks

– Lines of Credit

– Firm Commitments to

Originate

42

Compare Basic Surplus to New Liquidity Coverage Ratio

© 2015 FARIN & Associates Inc.

Asset Based Liquidity: LCR Ratio

• Basel Liquidity Coverage Ratio (LCR)

– Test – Can you survive a 30 day stress event with assets only?

– Numerator

• Cash & Due From

• Highly Liquid Unencumbered Marketable Securities

– Denominator

• Projected Deposit Runoff

• Loss of all Non-Core Funding renewing in time horizon

• Projected Increased Line Draw Downs

• Less Cash Inflows from loans (& securities?) - Limited amounts

included

– Note that this is the first Liquidity rate to consider loan

cash flows as a source!

43

© 2015 FARIN & Associates Inc.

Deposit Definitions – Stable/Less Stable

• Basel Says…Stable is

– Fully insured

– Meaningful business

relationship

– Applies to retail, small

business, large business

– Penalties adequate on CDs

– just count 30 day

maturities

– Penalties inadequate –

count all the balances

• Less Stable

– Deposits not meeting the

above definition

• Bank Regulators (Likely)

– Fully Insured – Call Reports

– Internal systems?

– Not sure how bank

regulators will deal with

penalty issue

44

© 2015 FARIN & Associates Inc.

Liquidity Coverage RatioNumerator (Basel Approach)

45

Available liquid assets in 30 days

We would add stressed cash flows coming off

loans and non-highly liquid securities.

© 2015 FARIN & Associates Inc.

Liquidity Coverage RatioFunding Outflows – Denominator

46

Sum of Outflows = Potential 30 day liquidity needs

© 2015 FARIN & Associates Inc.

Liquidity Coverage RatioNet Loan Outflows

47

© 2015 FARIN & Associates Inc.

Liquidity Coverage Ratio

48

Available

Needs

FARIN Suggested LCR Changes:

• Move Loan Cash Flows to the Numerator to track all Sources together

• Establish consistency on deposit outflow assumptions with core deposit study

info used in IRR Calculations

• Remove limit on amount of total loan flows counted (Move to numerator

eliminates negative denominator)

• Remove prepayment limitation assumptions on loan flows

• Consider calculating how much runoff would be necessary to “fail” assuming

sources are solid.

© 2015 FARIN & Associates Inc.

LCR Concept - Numerator

• Level 1 assets (0%

haircut)

– Generally Basel 1 0% risk

weight assets

– Broad stable markets

– Full government

guarantees

– Can be repo’d

– Everyone accepts as

collateral

• Level 2 Assets (15%

haircut)

– Generally Basel 1 20% risk

weight assets, but there

are exceptions

– Broad stable markets

markets

– Lack full government

guarantees

– Can be repo’d

– Everyone accepts as

collateral

• Non-Qualifying

– Everything else

49

Note that we work with market value rather than book value of assets.

© 2015 FARIN & Associates Inc.

Net Stable Funding Ratio

• Ratio Introduced in

Original Basel III Proposal

• Designed to look at 1 Year

Potential Funding Needs

– Numerator – stable funding

– Denominator – assets

needing stable funding

– Guideline - >=100%

• Not planned to phase-in

until 2019

• Why we choose not

incorporate into Liquidity

Calculations

– Static ratio

– Lots of clarification needed

– Late phase-in

– Unsure how US regulators

will interpret

• Adopting internal sources

and uses provides more

meaningful measurement

50

Regulatory Attempt at Sources & Uses – But Static!

© 2015 FARIN & Associates Inc.

Net Stable Funding Ratio

• Compares

Available

Liquidity Sources

• To Known

maturities & loan

renewal/payoffs

• Plus OBS

exposures

51

© 2015 FARIN & Associates Inc.

Net Stable Funding Ratio

Example shows institution short $34 million

• Options for Correcting?

– Lower reliance on assets with higher funding needs

• Fixed assets require $1 for every $1

• How fast can this be changed?

– Lower off balance sheet exposures

• Firm commitments

• Reduce outstanding lines of credit

– Change mix in deposit funding or terms or both

• High concentration of brokered deposits < 1 Yr which are not

given full credit

– Rely on Wholesale Funding

52

© 2015 FARIN & Associates Inc.

Net Stable Funding Ratio

Advantages

• Can be easily captured

from call report data

– Requires minimal new

changes

• Eliminates Assumption

Risk from Analysis

Disadvantages

• Removes all unused

wholesale sourcing from

calculation

• Not Effective in Examining

the Cost/Benefit of various

alternative strategies

– Rewards long-term

borrowing position without

regard to cost

53

© 2015 FARIN & Associates Inc.

OCC Liquid Assets – OCC Handbook

54

© 2015 FARIN & Associates Inc.

US Treasuries

55

Liquidity/Yield Relationship

Basel Criteria other than risk weight

Our judgment based on above criteria

We added as they are likely to be

additional US Regulatory factors

Nothing controversial about this security – clearly a Level 1, only potential issue

is adjustment for long-term Treasuries because of interest rate risk

© 2015 FARIN & Associates Inc.

Federal Reserve EBA

56

No controversy here, clearly a Level 1

© 2015 FARIN & Associates Inc.

Fed Funds Sold

57

We placed in level 2 if unsecured …

© 2015 FARIN & Associates Inc.

GSE Bullets

58

Under Basel definitions, this is a Level 2. Given 80% of US bank federal government

securities are GSAs, how will bank regulators treat? Other issue is interest rate risk

in long-term bullets.

© 2015 FARIN & Associates Inc.

Money Market Instruments

59

Under Basel definitions, this is a Level 2. Given 80% of US bank federal government

securities are GSAs, how will bank regulators treat?

© 2015 FARIN & Associates Inc.

Callable Agencies

60

Under Basel definitions, this is a Level 2. Given 80% of US bank federal government

securities are GSAs, how will bank regulators treat? Other issue is interest rate risk in

long-term bullets and option risk associated with call options.

© 2015 FARIN & Associates Inc.

Agency Asset-Backed

61

Under Basel definitions, this is a Level 2. Given 80% of US bank federal government

securities are GSAs, how will bank regulators treat? Other issue is interest rate risk

and option risk associated with prepayment options.

© 2015 FARIN & Associates Inc.

Agency Mortgage Obligations

62

Under Basel definitions, this is a Level 2. Given 80% of US bank federal government

securities are GSAs, how will bank regulators treat? Other issue is interest rate risk

and option risk associated with prepayment options and the structure of the classes.

© 2015 FARIN & Associates Inc.

Corporate Bonds

63

If credit grade is AA- or higher, qualifies as level 2 under Basel in spite of 100% risk

weight. Additional issue is interest rate risk on ling-term, and option risk if they

are callable.

© 2015 FARIN & Associates Inc.

Commercial Paper

64

Appears to meet Basel Level 2 tests in spite of 100% risk weight.

© 2015 FARIN & Associates Inc.

Bank Issued CDs

65

Will be controversial

• On one hand they are fully secured.

• On the other hand they generally are not accepted as collateral or in repo transactions

• We’re betting they won’t make the Level 2 cut – we could be wrong

© 2015 FARIN & Associates Inc.

Municipal Bonds

66

Not really dealt with by Basel. We applied same criteria as with corporate

bonds. Troubled market right now. Additional issues are potential interest

rate risk and option risk.

© 2015 FARIN & Associates Inc.

Revenue Bonds

67

Not really dealt with by Basel. We applied same criteria as with corporate

bonds. Troubled market right now. Additional issues are potential interest

rate risk and option risk. Could have more credit risk than general obligation bonds.

© 2015 FARIN & Associates Inc.

Asset-Backed Securities

68

Nobody’s favorite security now. Very unlikely to make the level 2 cut.

© 2015 FARIN & Associates Inc.

MEASURING CASH FLOW

BASED LIQUIDITY

A Practical Approach to Liquidity

69

© 2015 FARIN & Associates Inc.

Liquidity Gap Report

• Pro forma cash flow analysis:

– Projected sources and uses of funds over various scenarios

• Like rate movements or what-if plans

– Show exposures to variables and report to board and establish

contingencies

• What sources change and why (optionality, credit risk, performance

risk)

• What uses change and why (loan demand, potential deposit outflow,

etc.)

– Assumptions should be reasonable and appropriate.

– Institutions with reliance on securitization and sale for cash should

consider impact of conditions that may effect availability of funds.

70

© 2015 FARIN & Associates Inc.

Liquidity Gap Report

• Liquidity Gap Report

– Summary of Cash Flow sources and uses impact on

liquidity

• Use a forecast (Plan) for growth assumptions

• Use starting cash flows to project inflows and outflows

– Allows for Assessment of Contingency Funding Plan

Stress Tests to Determine Liquidity needs

• Impact of missing deposit growth by 10%

• What if loan repayments accelerate or slow?

• What happens to total ratio if access to key funding sources is

gone?

– Brokered CDs

– FHLB

71

© 2015 FARIN & Associates Inc.

Asset Sources/Uses

72

First two of forecast show

• Assets are a net drain of funds in years 1 & 2: $25.7 million

• Investments are providing sources of funds to fund loan growth

•$3.8 million over 2 years

• Loans using $29 million in funding by end of Yr. 2

© 2015 FARIN & Associates Inc.

Liability Sources/Uses

73

• Non-maturity funding providing $2.7 million over 2 years

• CDs expected to provide $6.9 million.

• Equity growth from earnings also contributing (not shown)

• Remainder is “borrowed” by model. Sources MUST = USES

© 2015 FARIN & Associates Inc.

Sources/Uses Summary

74

Sec 1

Sec 2

Sec 3

Section 1 – Net Cash flow sources/uses – Removing balancing accounts.

Section 2 – Adds in asset and liability adjustments

Section 3 – Recalculates Gap with adjustments and buffers

© 2015 FARIN & Associates Inc.

Sources/Uses Summary

75

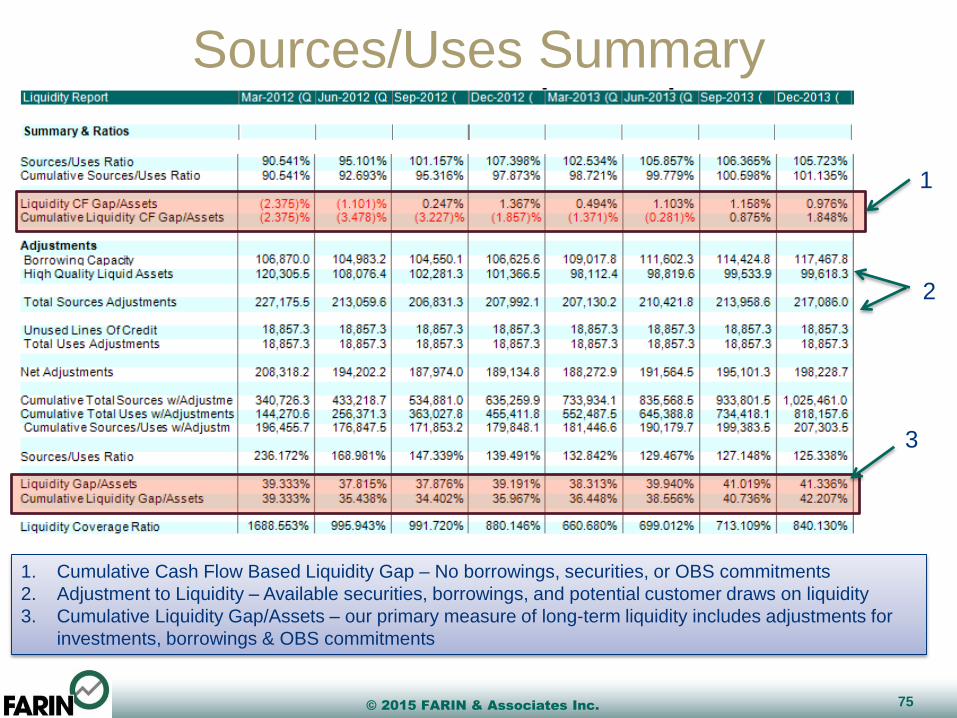

1

2

3

1. Cumulative Cash Flow Based Liquidity Gap – No borrowings, securities, or OBS commitments

2. Adjustment to Liquidity – Available securities, borrowings, and potential customer draws on liquidity

3. Cumulative Liquidity Gap/Assets – our primary measure of long-term liquidity includes adjustments for

investments, borrowings & OBS commitments

© 2015 FARIN & Associates Inc.

Sources/Uses Summary

76

•Test passed because of wholesale and investments

available for liquidity, NOT CASH FLOW.

•Determining Adequacy of limits by applying realistic

stress tests and deciding how low you can go.

© 2015 FARIN & Associates Inc.

Using Liquidity Gap

• Advantages

– Dynamic measure derived

from business plan

– Considers sources and uses

of funds

– Gap between sources and

uses is liquidity buffer

– Buffer includes cash flow

mismatch, asset based

buffer (LCR), and liability

based buffer (unused

borrowing capacity)

– Liquidity gap/assets can be

used as control ratio

– Can be stress tested

• Recommendation

– Primary long-term measure

of liquidity in policy

statement

– Limits set on pre- and post-

stress ratios

77

© 2015 FARIN & Associates Inc.

Putting this to Work

• Review your existing Liquidity Management

Process

– Are you measuring triggers or real ratios?

– What Asset-Based Measures are you using?

– Do you run a cash flow based measure?

• Develop Your Revised Reports to Integrate with

ALCO Reporting

– Do you measure forward-looking ratios or only

historical?

• Develop Trends in Performance and compare to

projections….

78

© 2015 FARIN & Associates Inc.

How We Can Help

79

www.farin.com