Embed Size (px)

Citation preview

McGraw-Hill/Irwin1

13-1

© The McGraw-Hill Companies, Inc., 2006

Accounting for CorporationsChapter

1313

McGraw-Hill/Irwin2

13-2

© The McGraw-Hill Companies, Inc., 2006

Learning objectivesLearning objectives

Identify characteristics of corporations and their organization. Describe the components of stockholders’ equity. Explain characteristics of common and preferred stock. Explain the form and content of a complete income

statement. Explain the items reported in retained earnings. Record the issuance of corporate stock. Distribute dividends between common stock and preferred

stock. Record transactions involving cash dividends. Account for stock dividends and stock splits. Record purchases and sales of treasury stock and the

retirement of stock.

McGraw-Hill/Irwin3

13-3

© The McGraw-Hill Companies, Inc., 2006

Privately HeldPrivately HeldPrivately HeldPrivately Held

Publicly HeldPublicly HeldPublicly HeldPublicly Held

Ownership can be

Corporate Form of OrganizationCorporate Form of Organization

Existence is separate from

owners.

Existence is separate from

owners.

An entity created by law.

An entity created by law.

Has rights and privileges.

Has rights and privileges.

McGraw-Hill/Irwin4

13-4

© The McGraw-Hill Companies, Inc., 2006

Advantages

Separate Legal Entity

Limited Liability of Stockholders

Transferable Ownership Rights

Continuous Life

Stockholders Are Not Corporate Agents

Ease of Capital Accumulation

Disadvantages

Governmental Regulation

Corporate Taxation

Advantages

Separate Legal Entity

Limited Liability of Stockholders

Transferable Ownership Rights

Continuous Life

Stockholders Are Not Corporate Agents

Ease of Capital Accumulation

Disadvantages

Governmental Regulation

Corporate Taxation

Characteristics of CorporationsCharacteristics of Corporations

McGraw-Hill/Irwin5

13-5

© The McGraw-Hill Companies, Inc., 2006

StockholdersStockholders

Board of DirectorsBoard of Directors

President, Vice-President, President, Vice-President, and Other Officersand Other Officers

Employees of the CorporationEmployees of the Corporation

Organizing and Managing a CorporationOrganizing and Managing a Corporation

McGraw-Hill/Irwin6

13-6

© The McGraw-Hill Companies, Inc., 2006

C orpo ra te O rgan iza tion C hart

Secretary V ice P residentF inance

V ice P residentP roduction

V ice P residentMarketing

President

Board of D irectors

S tockholdersUltimate Ultimate control.control.

Ultimate Ultimate control.control.

Stockholders Stockholders usually meet usually meet once a year.once a year.

Stockholders Stockholders usually meet usually meet once a year.once a year.

Organizing and Managing a CorporationOrganizing and Managing a Corporation

Selected by a Selected by a vote of the vote of the

stockholders.stockholders.

Selected by a Selected by a vote of the vote of the

stockholders.stockholders.

Overall Overall responsibility responsibility for managing for managing the company.the company.

Overall Overall responsibility responsibility for managing for managing the company.the company.

McGraw-Hill/Irwin7

13-7

© The McGraw-Hill Companies, Inc., 2006

Vote at stockholders’ meetings.Sell stock. Purchase additional shares of stock.Receive dividends, if any.Share equally in any assets remaining

after creditors are paid in a liquidation.

Vote at stockholders’ meetings.Sell stock. Purchase additional shares of stock.Receive dividends, if any.Share equally in any assets remaining

after creditors are paid in a liquidation.

Rights of StockholdersRights of Stockholders

McGraw-Hill/Irwin8

13-8

© The McGraw-Hill Companies, Inc., 2006

Each unit of ownership is called a share of stock.

A stock certificate serves as proof that a stockholder has purchased shares.

Each unit of ownership is called a share of stock.

A stock certificate serves as proof that a stockholder has purchased shares.

Stock Certificates and TransferStock Certificates and Transfer

When the stock is sold, the stockholder signs a transfer endorsement on the back of the stock

certificate.

When the stock is sold, the stockholder signs a transfer endorsement on the back of the stock

certificate.

McGraw-Hill/Irwin9

13-9

© The McGraw-Hill Companies, Inc., 2006

Basics of Capital StockBasics of Capital Stock

Total amount of stock that a Total amount of stock that a corporation’s charter authorizes it to sell.corporation’s charter authorizes it to sell.

Total amount of stock that a Total amount of stock that a corporation’s charter authorizes it to sell.corporation’s charter authorizes it to sell.

McGraw-Hill/Irwin10

13-10

© The McGraw-Hill Companies, Inc., 2006

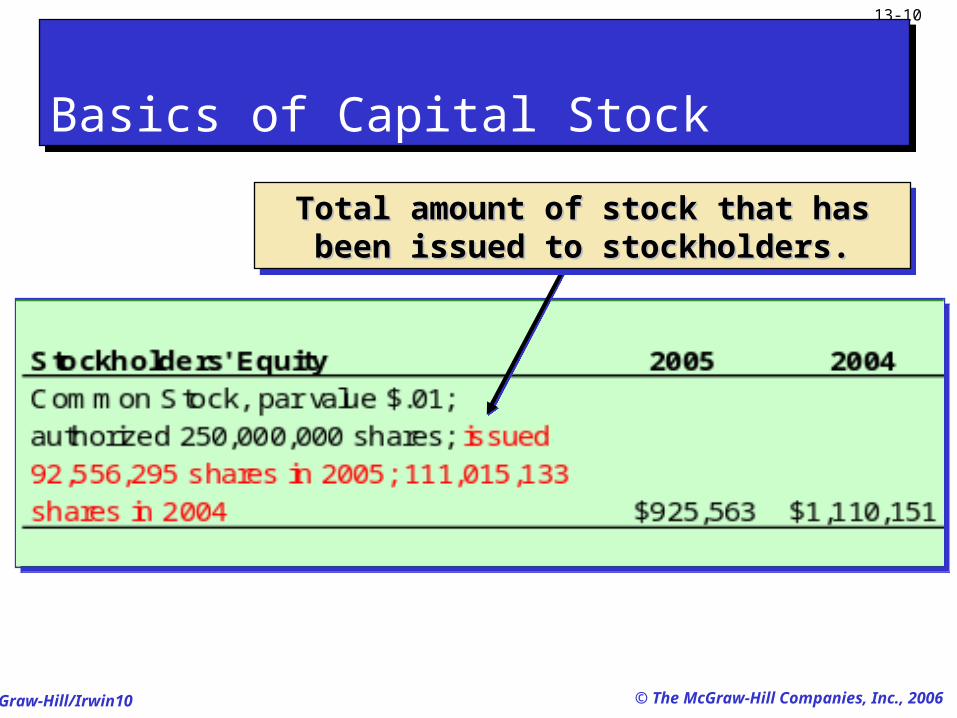

Basics of Capital StockBasics of Capital Stock

Total amount of stock that has been Total amount of stock that has been issued to stockholders.issued to stockholders.

Total amount of stock that has been Total amount of stock that has been issued to stockholders.issued to stockholders.

McGraw-Hill/Irwin11

13-11

© The McGraw-Hill Companies, Inc., 2006

Par valuePar value is an is an arbitrary amount arbitrary amount assigned to each assigned to each

share of stock when share of stock when it is authorized.it is authorized.

Par valuePar value is an is an arbitrary amount arbitrary amount assigned to each assigned to each

share of stock when share of stock when it is authorized.it is authorized.

Market priceMarket price is the is the amount that each amount that each share of stock will share of stock will

sell for in the market.sell for in the market.

Market priceMarket price is the is the amount that each amount that each share of stock will share of stock will

sell for in the market.sell for in the market.

Selling (Issuing) StockSelling (Issuing) Stock

McGraw-Hill/Irwin12

13-12

© The McGraw-Hill Companies, Inc., 2006

Par Value Stock

On September 1, Matrix, Inc. issued 100,000 shares of $2 par value stock for $25 per share.

Let’s record this transaction.

Par Value Stock

On September 1, Matrix, Inc. issued 100,000 shares of $2 par value stock for $25 per share.

Let’s record this transaction.

Record:1. The cash received.

2. The number of shares issued × the par value per share in the Common Stock account.

3. The remainder is assigned to Contributed Capital in Excess of Par.

Record:1. The cash received.

2. The number of shares issued × the par value per share in the Common Stock account.

3. The remainder is assigned to Contributed Capital in Excess of Par.

Issuing Par Value StockIssuing Par Value Stock

McGraw-Hill/Irwin13

13-13

© The McGraw-Hill Companies, Inc., 2006

Issuing Par Value StockIssuing Par Value Stock

Par Value Stock

On September 1, Matrix, Inc. issued 100,000 shares of $2 par value stock for $25 per share.

Let’s record this transaction.

Par Value Stock

On September 1, Matrix, Inc. issued 100,000 shares of $2 par value stock for $25 per share.

Let’s record this transaction.

Sept. 1 Cash 2,500,000 Common stock, $2 par value 200,000

Contributed capital in excess of par value 2,300,000

Sold and issued 100,000 shares of common stock

McGraw-Hill/Irwin14

13-14

© The McGraw-Hill Companies, Inc., 2006

Issuing Par Value StockIssuing Par Value Stock

McGraw-Hill/Irwin15

13-15

© The McGraw-Hill Companies, Inc., 2006

Record:1. The asset received at its market value.

2. The number of shares issued × the par value per share in the Common Stock account.

3. The remainder is assigned to Contributed Capital in Excess of Par.

Record:1. The asset received at its market value.

2. The number of shares issued × the par value per share in the Common Stock account.

3. The remainder is assigned to Contributed Capital in Excess of Par.

Issuing Stock for Noncash AssetsIssuing Stock for Noncash Assets

Par Value Stock

On September 1, Matrix, Inc. issued 100,000 shares of $2 par value stock for land valued at

$2,500,000. Let’s record this transaction.

Par Value Stock

On September 1, Matrix, Inc. issued 100,000 shares of $2 par value stock for land valued at

$2,500,000. Let’s record this transaction.

McGraw-Hill/Irwin16

13-16

© The McGraw-Hill Companies, Inc., 2006

Issuing Stock for Noncash AssetsIssuing Stock for Noncash Assets

Sept. 1 Land 2,500,000 Common stock, $2 par value 200,000

Contributed capital in excess of par value 2,300,000

Exchanges 100,000 common shares for land

Par Value Stock

On September 1, Matrix, Inc. issued 100,000 shares of $2 par value stock for land valued at

$2,500,000. Let’s record this transaction.

Par Value Stock

On September 1, Matrix, Inc. issued 100,000 shares of $2 par value stock for land valued at

$2,500,000. Let’s record this transaction.

McGraw-Hill/Irwin17

13-17

© The McGraw-Hill Companies, Inc., 2006

A separate class of stock, typically having priority over common shares in . . .

Dividend distributions.

Distribution of assets in case of liquidation.

A separate class of stock, typically having priority over common shares in . . .

Dividend distributions.

Distribution of assets in case of liquidation.

Usually has a stated dividend rate.

Usually has a stated dividend rate.

Normally has no voting rights.

Normally has no voting rights.

Preferred StockPreferred Stock

McGraw-Hill/Irwin18

13-18

© The McGraw-Hill Companies, Inc., 2006

Preferred StockPreferred Stock

Dillon Snowboards issues 50 shares of $100 par value preferred stock for $6,000 cash on July 1, 2005.

Dr. Cash 6,000

Cr. Preferred Stock, $100 par value 5,000

Cr. Contributed Capital in Excess

of par value, preferred stock 1,000

McGraw-Hill/Irwin19

13-19

© The McGraw-Hill Companies, Inc., 2006

Reasons for Issuing Preferred StockReasons for Issuing Preferred Stock

To raise capital without sacrificing control.

To appeal to investors who may believe the common stock is too risky or that the expected return on common stock is too low.

To raise capital without sacrificing control.

To appeal to investors who may believe the common stock is too risky or that the expected return on common stock is too low.

McGraw-Hill/Irwin20

13-20

© The McGraw-Hill Companies, Inc., 2006

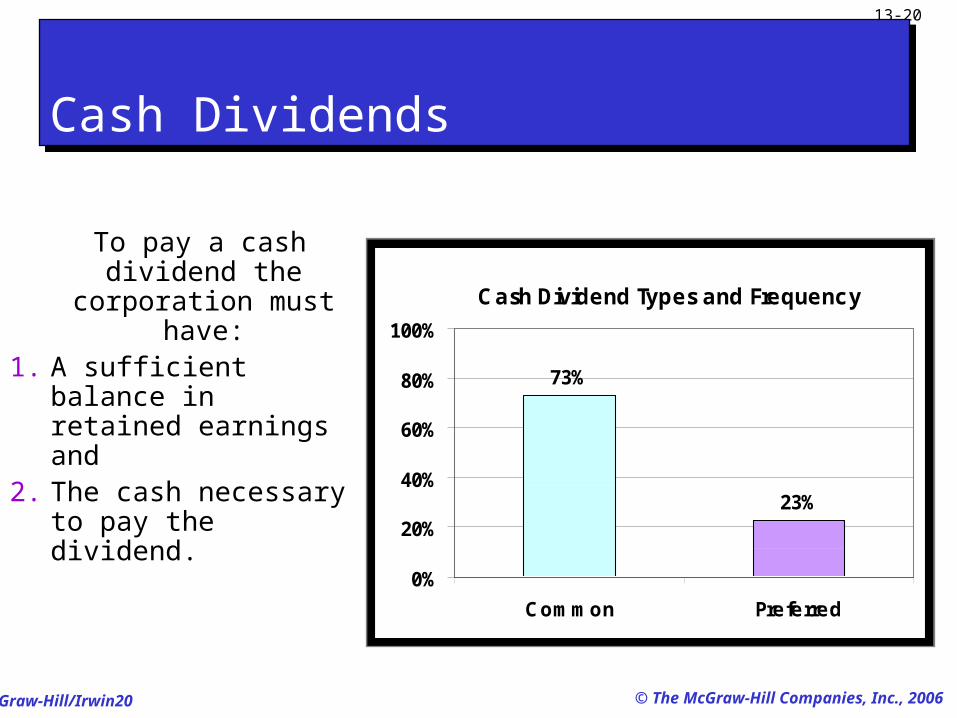

To pay a cash dividend the

corporation must have:

1. A sufficient balance in retained earnings and

2. The cash necessary to pay the dividend.

Cash Dividend Types and Frequency

73%

23%

0%

20%

40%

60%

80%

100%

Common Preferred

Cash DividendsCash Dividends

McGraw-Hill/Irwin21

13-21

© The McGraw-Hill Companies, Inc., 2006

Regular cash dividends provide a return to investors and almost always affect the

stock’s market value.

Dividends

Stockholders

June30

Cash DividendsCash Dividends

Corporation

McGraw-Hill/Irwin22

13-22

© The McGraw-Hill Companies, Inc., 2006

Three important datesThree important dates

Date of Declaration

Record liabilityfor dividend.

Dividends

Date of Record

No entryrequired.

Date of Payment

Record payment ofcash to stockholders.

Entries for Cash DividendsEntries for Cash Dividends

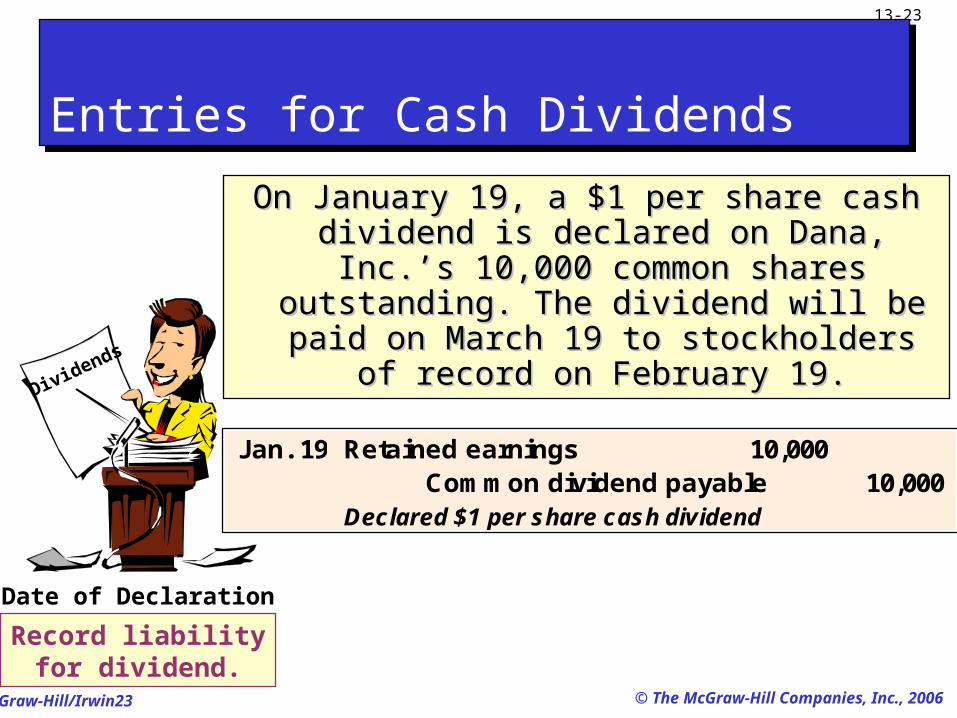

McGraw-Hill/Irwin23

13-23

© The McGraw-Hill Companies, Inc., 2006

Date of Declaration

Record liabilityfor dividend.

Dividends

On January 19, a $1 per share cash On January 19, a $1 per share cash dividend is declared on Dana, Inc.’s dividend is declared on Dana, Inc.’s 10,000 common shares outstanding. 10,000 common shares outstanding.

The dividend will be paid on March 19 to The dividend will be paid on March 19 to stockholders of record on February 19.stockholders of record on February 19.

Entries for Cash DividendsEntries for Cash Dividends

Jan. 19 Retained earnings 10,000 Common dividend payable 10,000

Declared $1 per share cash dividend

McGraw-Hill/Irwin24

13-24

© The McGraw-Hill Companies, Inc., 2006

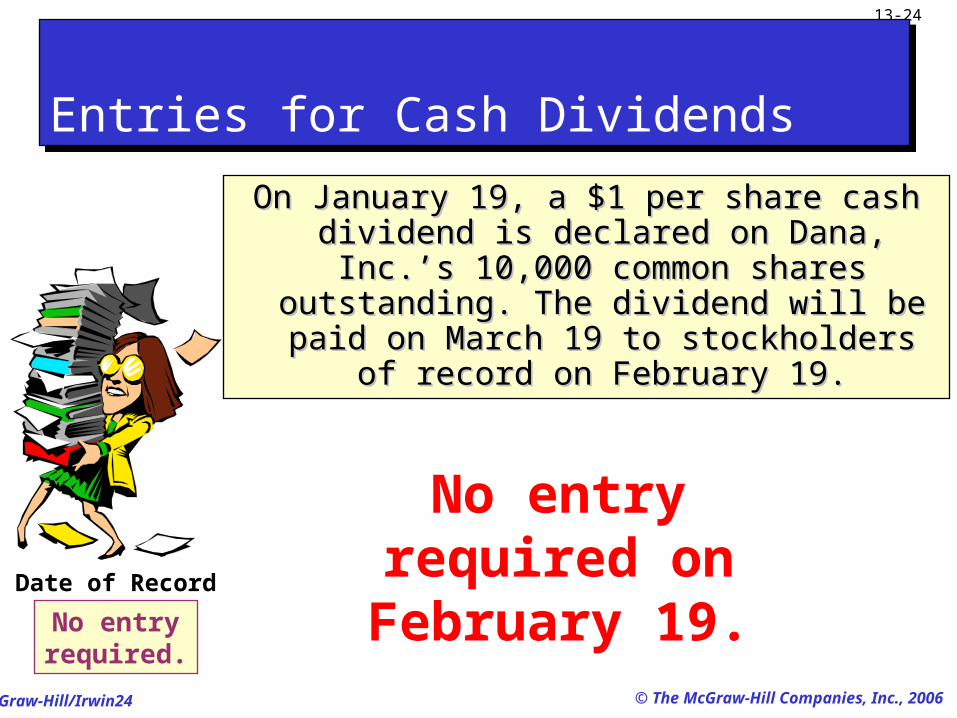

Date of Record

No entryrequired.

Entries for Cash DividendsEntries for Cash Dividends

On January 19, a $1 per share cash On January 19, a $1 per share cash dividend is declared on Dana, Inc.’s dividend is declared on Dana, Inc.’s 10,000 common shares outstanding. 10,000 common shares outstanding.

The dividend will be paid on March 19 to The dividend will be paid on March 19 to stockholders of record on February 19.stockholders of record on February 19.

No entry required on February 19.

McGraw-Hill/Irwin25

13-25

© The McGraw-Hill Companies, Inc., 2006

Date of Payment

Record payment ofcash to stockholders.

Entries for Cash DividendsEntries for Cash Dividends

On January 19, a $1 per share cash On January 19, a $1 per share cash dividend is declared on Dana, Inc.’s dividend is declared on Dana, Inc.’s 10,000 common shares outstanding. 10,000 common shares outstanding.

The dividend will be paid on March 19 to The dividend will be paid on March 19 to stockholders of record on February 19.stockholders of record on February 19.

Mar. 19 Common dividend payable 10,000 Cash 10,000

Paid $1 per share cash dividend

McGraw-Hill/Irwin26

13-26

© The McGraw-Hill Companies, Inc., 2006

Created when a company incurs cumulative losses or pays dividends greater than total profits earned

in other years.

Deficits and Cash DividendsDeficits and Cash Dividends

McGraw-Hill/Irwin27

13-27

© The McGraw-Hill Companies, Inc., 2006

The corporation distributes additional shares of its own stock to its stockholders without

receiving any payment in return.

The corporation distributes additional shares of its own stock to its stockholders without

receiving any payment in return.

Stockholders

Stock DividendsStock Dividends

Why a stock dividend?

•Can be used to keep the market price on the stock affordable.

•Can provide evidence of management’s confidence that the company is doing well.

Why a stock dividend?

•Can be used to keep the market price on the stock affordable.

•Can provide evidence of management’s confidence that the company is doing well.

100 Shares

$1 par value

HotAir, Inc.Common Stock

100 shares

$1 par

McGraw-Hill/Irwin28

13-28

© The McGraw-Hill Companies, Inc., 2006

Stock DividendsStock Dividends

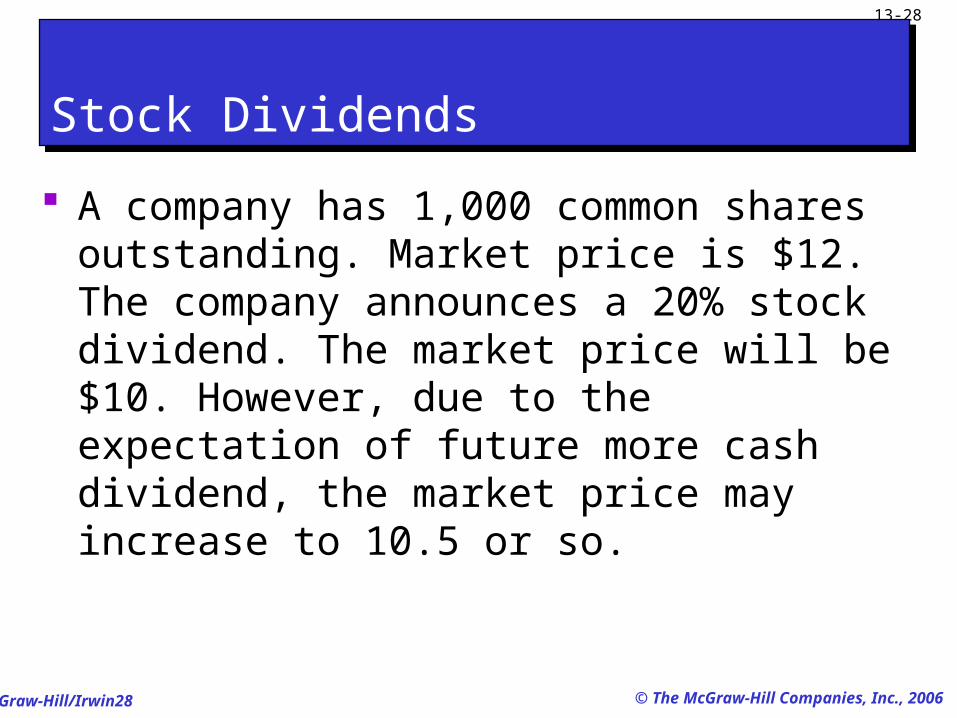

A company has 1,000 common shares outstanding. Market price is $12. The company announces a 20% stock dividend. The market price will be $10. However, due to the expectation of future more cash dividend, the market price may increase to 10.5 or so.

McGraw-Hill/Irwin29

13-29

© The McGraw-Hill Companies, Inc., 2006

Small Stock DividendDistribution is 25% of the previously

outstanding shares.Capitalize retained earnings for the market

value of the shares to be distributed.

Small Stock DividendDistribution is 25% of the previously

outstanding shares.Capitalize retained earnings for the market

value of the shares to be distributed.

Stock DividendsStock Dividends

Large Stock DividendDistribution is > 25% of the previously

outstanding shares.Capitalize retained earnings for the minimum

amount required by state law, usually par or stated value of the shares.

Large Stock DividendDistribution is > 25% of the previously

outstanding shares.Capitalize retained earnings for the minimum

amount required by state law, usually par or stated value of the shares.

McGraw-Hill/Irwin30

13-30

© The McGraw-Hill Companies, Inc., 2006

Here is the stockholders’ equity section of Quest’s balance sheet prior to the declaration of a small stock dividend.

Here is the stockholders’ equity section of Quest’s balance sheet prior to the declaration of a small stock dividend.

Recording a Small Stock DividendRecording a Small Stock Dividend

McGraw-Hill/Irwin31

13-31

© The McGraw-Hill Companies, Inc., 2006

On December 31, 2005, Quest declared a 2% stock dividend, when the stock was selling for $10 per share. The stock will be distributed to stockholders on January 20, 2006. Let’s make

the December 31 entry.

On December 31, 2005, Quest declared a 2% stock dividend, when the stock was selling for $10 per share. The stock will be distributed to stockholders on January 20, 2006. Let’s make

the December 31 entry.

Recording a Small Stock DividendRecording a Small Stock Dividend

100,000 × 2% = 2,000 × $10 = $20,000/ 100,000 × 2% = 2,000 × $10 = $20,000/ 10000*.02=2000shares10000*.02=2000shares

2,000 × $1 par = $2,000 × $1 par = $2,000/2000*$10=20000RE, 2000*$1=20002,000/2000*$10=20000RE, 2000*$1=2000

100,000 × 2% = 2,000 × $10 = $20,000/ 100,000 × 2% = 2,000 × $10 = $20,000/ 10000*.02=2000shares10000*.02=2000shares

2,000 × $1 par = $2,000 × $1 par = $2,000/2000*$10=20000RE, 2000*$1=20002,000/2000*$10=20000RE, 2000*$1=2000

Dec. 31 Retained earnings 20,000 Common stock dividend distributable 2,000 Contributed capital in excess of par value 18,000

Declared a 2,000 shares (2%) stock dividend

McGraw-Hill/Irwin32

13-32

© The McGraw-Hill Companies, Inc., 2006

Before theBefore thestockstock

dividend.dividend.

After theAfter thestockstock

dividend.dividend.

McGraw-Hill/Irwin33

13-33

© The McGraw-Hill Companies, Inc., 2006

Router, Inc. shows the following stockholders’ equity section just prior to

issuing a large stock dividend.

Router, Inc. shows the following stockholders’ equity section just prior to

issuing a large stock dividend.

Recording a Large Stock DividendRecording a Large Stock Dividend

McGraw-Hill/Irwin34

13-34

© The McGraw-Hill Companies, Inc., 2006

On December 31, 2005, Router declared a 40% stock dividend, when the stock was selling

for $8 per share. State law requires that large stock dividends be capitalized at par

value per share.

On December 31, 2005, Router declared a 40% stock dividend, when the stock was selling

for $8 per share. State law requires that large stock dividends be capitalized at par

value per share.

50,000 × 40% = 20,000 shares × $1 par value = $20,00050,000 × 40% = 20,000 shares × $1 par value = $20,00050,000 × 40% = 20,000 shares × $1 par value = $20,00050,000 × 40% = 20,000 shares × $1 par value = $20,000

Recording a Large Stock DividendRecording a Large Stock Dividend

Dec. 31 Retained earnings 20,000 Common stock dividend distributable 20,000

Declared a 20,000 shares (40%) stock dividend

McGraw-Hill/Irwin35

13-35

© The McGraw-Hill Companies, Inc., 2006

A distribution of additional shares of stock to stockholders according to their percent

ownership.

A distribution of additional shares of stock to stockholders according to their percent

ownership.

Common Stock

$10 par value

100 shares

OldShares

NewShares Common Stock

$5 par value

200 shares

Stock SplitsStock Splits

McGraw-Hill/Irwin36

13-36

© The McGraw-Hill Companies, Inc., 2006

Thomas, Inc. has the following stockholders’ Thomas, Inc. has the following stockholders’ equity section just prior to a 2-for-1 stock split.equity section just prior to a 2-for-1 stock split.Thomas, Inc. has the following stockholders’ Thomas, Inc. has the following stockholders’ equity section just prior to a 2-for-1 stock split.equity section just prior to a 2-for-1 stock split.

Stock SplitsStock Splits

McGraw-Hill/Irwin37

13-37

© The McGraw-Hill Companies, Inc., 2006

After the 2-for-1 split the stockholders’ equity section After the 2-for-1 split the stockholders’ equity section of the balance sheet looks like this . . .of the balance sheet looks like this . . .

After the 2-for-1 split the stockholders’ equity section After the 2-for-1 split the stockholders’ equity section of the balance sheet looks like this . . .of the balance sheet looks like this . . .

No accountingentry is made.No accountingentry is made.

Stock SplitsStock Splits

McGraw-Hill/Irwin38

13-38

© The McGraw-Hill Companies, Inc., 2006

Stock SplitsStock Splits

The split does not affect any equity amounts reported on balance sheet or any individual stockholder’s percent ownership. Both the contributed capital and retained earnings accounts are unchanged by a split.

McGraw-Hill/Irwin39

13-39

© The McGraw-Hill Companies, Inc., 2006

Corporations acquire shares of their own stock.

Why would acompany do

that?

Why would acompany do

that?

Use the shares to acquireUse the shares to acquirecontrol of another corporation.control of another corporation.

To avoid a hostile takeover.To avoid a hostile takeover.

Use the shares forUse the shares foremployee stock options.employee stock options.

To maintain a strong market forTo maintain a strong market forits stock or show managementits stock or show managementconfidence in the current price.confidence in the current price.

Use the shares to acquireUse the shares to acquirecontrol of another corporation.control of another corporation.

To avoid a hostile takeover.To avoid a hostile takeover.

Use the shares forUse the shares foremployee stock options.employee stock options.

To maintain a strong market forTo maintain a strong market forits stock or show managementits stock or show managementconfidence in the current price.confidence in the current price.

Treasury StockTreasury Stock

McGraw-Hill/Irwin40

13-40

© The McGraw-Hill Companies, Inc., 2006

Treasury StockTreasury Stock

McGraw-Hill/Irwin41

13-41

© The McGraw-Hill Companies, Inc., 2006

On May 8, Whitt, Inc. purchased 2,000 of its own shares of stock in the open market for

$8,000.

On May 8, Whitt, Inc. purchased 2,000 of its own shares of stock in the open market for

$8,000.

Purchasing Treasury StockPurchasing Treasury Stock

Treasury stock is shown as a reduction in totalTreasury stock is shown as a reduction in totalstockholders’ equity on the balance sheet.stockholders’ equity on the balance sheet.

Treasury stock is shown as a reduction in totalTreasury stock is shown as a reduction in totalstockholders’ equity on the balance sheet.stockholders’ equity on the balance sheet.

May 8 Treasury stock, common 8,000 Cash 8,000

Purchase 2,000 treasury shares at $4 per share

McGraw-Hill/Irwin42

13-42

© The McGraw-Hill Companies, Inc., 2006

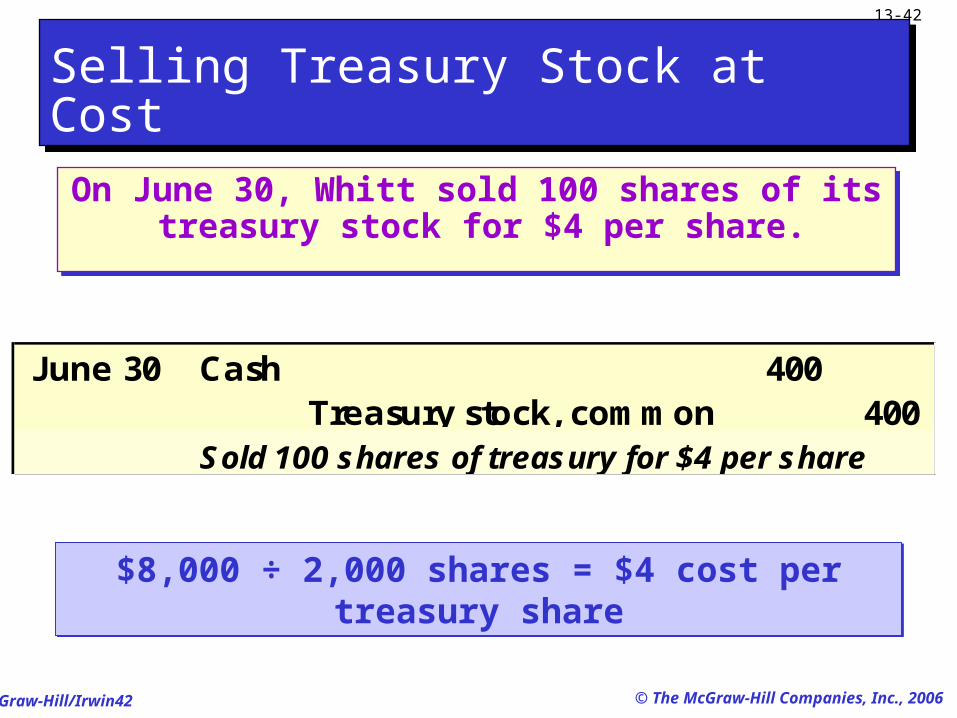

On June 30, Whitt sold 100 shares of its treasury stock for $4 per share.

On June 30, Whitt sold 100 shares of its treasury stock for $4 per share.

Selling Treasury Stock at CostSelling Treasury Stock at Cost

$8,000 ÷ 2,000 shares = $4 cost per treasury share$8,000 ÷ 2,000 shares = $4 cost per treasury share

June 30 Cash 400 Treasury stock, common 400

Sold 100 shares of treasury for $4 per share

McGraw-Hill/Irwin43

13-43

© The McGraw-Hill Companies, Inc., 2006

On July 19, Whitt, Inc. sold an additional 500 shares of its treasury stock for $8 per

share.

On July 19, Whitt, Inc. sold an additional 500 shares of its treasury stock for $8 per

share.

Selling Treasury Stock Above CostSelling Treasury Stock Above Cost

July 19 Cash 4,000 Treasury stock, 2,000 Contributed capital, treasury stock 2,000

Sold 500 treasury shares for $8 per share

McGraw-Hill/Irwin44

13-44

© The McGraw-Hill Companies, Inc., 2006

On August 27, Whitt sold an additional 400 shares of its treasury stock for $1.50 per

share.

On August 27, Whitt sold an additional 400 shares of its treasury stock for $1.50 per

share.

Selling Treasury Stock Below CostSelling Treasury Stock Below Cost

Aug. 27 Cash 600

1,000 Treasury stock, 1,600

Sold 500 treasury shares for $1.50 per share

Contributed capital, treasury stock

McGraw-Hill/Irwin45

13-45

© The McGraw-Hill Companies, Inc., 2006

Net IncomeNet IncomeNet IncomeNet Income

Reporting Income and EquityReporting Income and Equity

DiscontinuedSegments

Changes inAccounting

Principle

ExtraordinaryItems

ContinuingOperations

McGraw-Hill/Irwin46

13-46

© The McGraw-Hill Companies, Inc., 2006

Revenues, expensesRevenues, expensesand income generatedand income generated

by the company’sby the company’scontinuing operations.continuing operations.

Revenues, expensesRevenues, expensesand income generatedand income generated

by the company’sby the company’scontinuing operations.continuing operations.

Continuing OperationsContinuing Operations

Net IncomeNet IncomeNet IncomeNet IncomeContinuingOperations

McGraw-Hill/Irwin47

13-47

© The McGraw-Hill Companies, Inc., 2006

Income from operating the discontinued segment prior Income from operating the discontinued segment prior to its disposal to its disposal andand gain or loss on the sale of the net gain or loss on the sale of the net

assets of the segment.assets of the segment.

Income from operating the discontinued segment prior Income from operating the discontinued segment prior to its disposal to its disposal andand gain or loss on the sale of the net gain or loss on the sale of the net

assets of the segment.assets of the segment.

Discontinued SegmentsDiscontinued Segments

Net IncomeNet IncomeNet IncomeNet Income

DiscontinuedSegments

McGraw-Hill/Irwin48

13-48

© The McGraw-Hill Companies, Inc., 2006

A gain or loss thatA gain or loss thatis is unusualunusual in nature in nature

and and infrequentinfrequent in inoccurrence.occurrence.

A gain or loss thatA gain or loss thatis is unusualunusual in nature in nature

and and infrequentinfrequent in inoccurrence.occurrence.

Extraordinary ItemsExtraordinary Items

Net IncomeNet IncomeNet IncomeNet Income

ExtraordinaryItems

McGraw-Hill/Irwin49

13-49

© The McGraw-Hill Companies, Inc., 2006

The increase or The increase or decrease in income decrease in income when changing fromwhen changing from

one generally acceptedone generally acceptedaccounting principle to accounting principle to

another.another.

The increase or The increase or decrease in income decrease in income when changing fromwhen changing from

one generally acceptedone generally acceptedaccounting principle to accounting principle to

another.another.

Changes in Accounting PrinciplesChanges in Accounting Principles

Net IncomeNet IncomeNet IncomeNet Income

Changes inAccounting

Principle

McGraw-Hill/Irwin50

13-50

© The McGraw-Hill Companies, Inc., 2006

Income StatementIncome Statement

McGraw-Hill/Irwin51

13-51

© The McGraw-Hill Companies, Inc., 2006

Earnings per share is one of the most widely cited items of accounting information.

Earnings per share is one of the most widely cited items of accounting information.

Earnings Per ShareEarnings Per Share

Basicearningsper share

= Net income - Preferred dividends Weighted-average common shares outstanding

McGraw-Hill/Irwin52

13-52

© The McGraw-Hill Companies, Inc., 2006

Derby, Inc. reports net income of $75,000 and paid preferred dividends of $10,000 during 2005. The company started the year with

10,000 shares of common stock outstanding. Derby sold an additional 4,000 share of stock on March 31, and purchased 2,000 treasury

shares on September 30, 2005.

Derby, Inc. reports net income of $75,000 and paid preferred dividends of $10,000 during 2005. The company started the year with

10,000 shares of common stock outstanding. Derby sold an additional 4,000 share of stock on March 31, and purchased 2,000 treasury

shares on September 30, 2005.

Changes in Shares OutstandingChanges in Shares Outstanding

McGraw-Hill/Irwin53

13-53

© The McGraw-Hill Companies, Inc., 2006

EPS = EPS = $75,000 - $10,000 $75,000 - $10,000

12,50012,500 = = $5.20$5.20

Changes in Shares OutstandingChanges in Shares Outstanding

Derby, Inc. reports net income of $75,000 and paid preferred dividends of $10,000 during 2005. The company started the year with

10,000 shares of common stock outstanding. Derby sold an additional 4,000 share of stock on March 31, and purchased 2,000 treasury

shares on September 30, 2005.

Derby, Inc. reports net income of $75,000 and paid preferred dividends of $10,000 during 2005. The company started the year with

10,000 shares of common stock outstanding. Derby sold an additional 4,000 share of stock on March 31, and purchased 2,000 treasury

shares on September 30, 2005.

McGraw-Hill/Irwin54

13-54

© The McGraw-Hill Companies, Inc., 2006

The right to purchase common stock at a fixed price over a specified period of time. As the

stock’s price rises above the fixed option price, the value of the option increases.

The right to purchase common stock at a fixed price over a specified period of time. As the

stock’s price rises above the fixed option price, the value of the option increases.

Optionpurchaseprice $30 per share.

Stock OptionsStock Options

Marketprice of

stock $75 per share.

McGraw-Hill/Irwin55

13-55

© The McGraw-Hill Companies, Inc., 2006

Options are given to key employees to motivate them to:

focus on company performance,take a long-run perspective, andremain with the company.

Options are given to key employees to motivate them to:

focus on company performance,take a long-run perspective, andremain with the company.

Stock OptionsStock Options

McGraw-Hill/Irwin56

13-56

© The McGraw-Hill Companies, Inc., 2006

McGraw-Hill/Irwin57

13-57

© The McGraw-Hill Companies, Inc., 2006

Total cumulative amount of reported net income less any net losses and dividends declared

since the company started operating.

Total cumulative amount of reported net income less any net losses and dividends declared

since the company started operating.

Statement of Retained EarningsStatement of Retained Earnings

McGraw-Hill/Irwin58

13-58

© The McGraw-Hill Companies, Inc., 2006

LegalLegal ContractualContractual

Most states restrictthe amount oftreasury stock

purchases to theamount of retained

earnings.

Most states restrictthe amount oftreasury stock

purchases to theamount of retained

earnings.

Loan agreementscan include

restrictions on paying

dividends below acertain amount ofretained earnings.

Loan agreementscan include

restrictions on paying

dividends below acertain amount ofretained earnings.

Restricted Retained EarningsRestricted Retained Earnings

McGraw-Hill/Irwin59

13-59

© The McGraw-Hill Companies, Inc., 2006

A corporation’s directors can voluntarily limit dividends because of a special need for cash

such as the purchase of new facilities.

A corporation’s directors can voluntarily limit dividends because of a special need for cash

such as the purchase of new facilities.

Appropriated Retained EarningsAppropriated Retained Earnings

McGraw-Hill/Irwin60

13-60

© The McGraw-Hill Companies, Inc., 2006

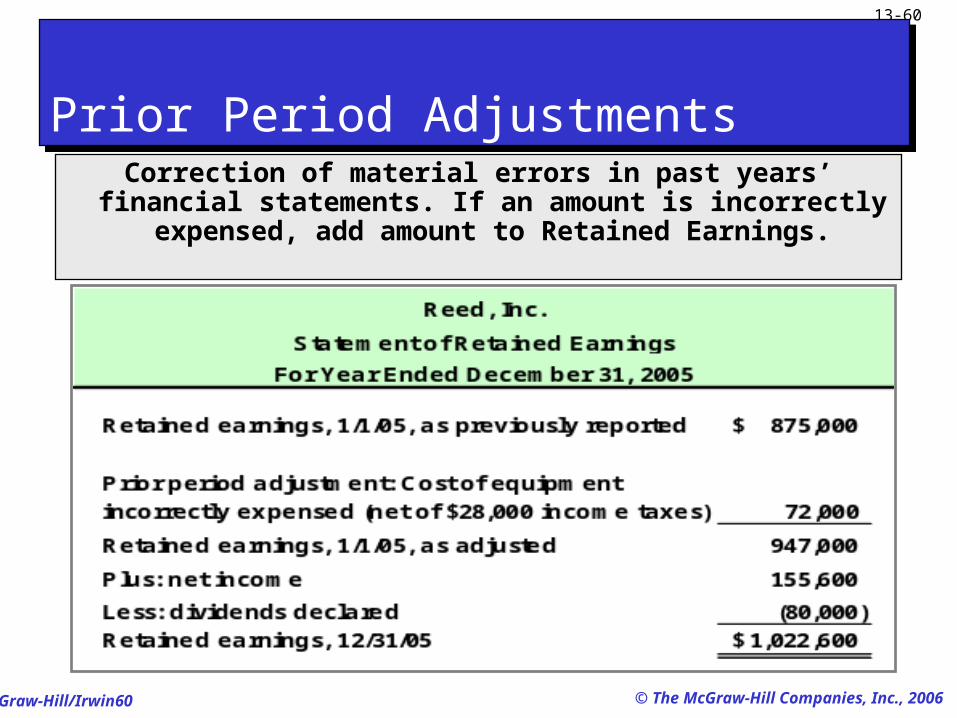

Correction of material errors in past years’ financial statements. If an amount is incorrectly

expensed, add amount to Retained Earnings.

Prior Period AdjustmentsPrior Period Adjustments

McGraw-Hill/Irwin61

13-61

© The McGraw-Hill Companies, Inc., 2006

(In millions) Retained

Shares Amount Earnings TotalBalance at January 1, 2005 821 2,500$ 9,500$ 12,000$ Stock sales 17 500 500 Stock repurchases and retirement (17) (260) (925) (1,185) Cash dividends declared (150) (150) Other, net 70 70 Net income 5,100 5,100 Balance at December 31, 2005 821 2,740$ 13,595$ 16,335$

Common stock and capital in excess of par

Matrix, Inc.

Statement of Stockholders' Equity

For the Year Ended December 31, 2005

(In millions) Retained

Shares Amount Earnings TotalBalance at January 1, 2005 821 2,500$ 9,500$ 12,000$ Stock sales 17 500 500 Stock repurchases and retirement (17) (260) (925) (1,185) Cash dividends declared (150) (150) Other, net 70 70 Net income 5,100 5,100 Balance at December 31, 2005 821 2,740$ 13,595$ 16,335$

Common stock and capital in excess of par

Matrix, Inc.

Statement of Stockholders' Equity

For the Year Ended December 31, 2005

Statement of Stockholders’ EquityStatement of Stockholders’ Equity

This is a more inclusive statement than the statement of retained earnings.

McGraw-Hill/Irwin62

13-62

© The McGraw-Hill Companies, Inc., 2006

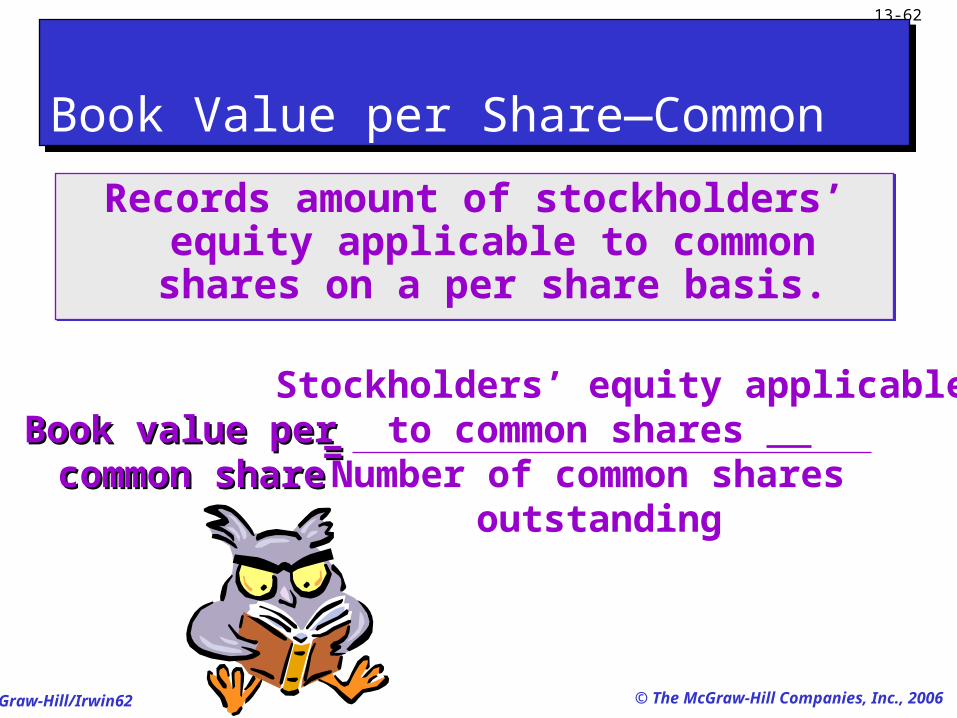

Records amount of stockholders’ equity applicable to common shares on a per

share basis.

Records amount of stockholders’ equity applicable to common shares on a per

share basis.

Book Value per Share—CommonBook Value per Share—Common

Book value per Book value per common sharecommon share

==

Stockholders’ equity applicable to common shares

Number of common shares outstanding

McGraw-Hill/Irwin63

13-63

© The McGraw-Hill Companies, Inc., 2006

Records amount of stockholders’ equity applicable to preferred shares on a per

share basis.

Records amount of stockholders’ equity applicable to preferred shares on a per

share basis.

Book Value per Share—PreferredBook Value per Share—Preferred

Book value per Book value per preferredpreferred share share

==

Stockholders’ equity applicable to preferred shares

Number of preferred shares outstanding

McGraw-Hill/Irwin64

13-64

© The McGraw-Hill Companies, Inc., 2006

Tells us the annual amount of cash dividends distributed to common stockholders relative to

the stock’s market price.

Tells us the annual amount of cash dividends distributed to common stockholders relative to

the stock’s market price.

Dividend YieldDividend Yield

DividendDividendYieldYield

== Annual cash dividends per share Annual cash dividends per share

Market value per shareMarket value per share

McGraw-Hill/Irwin65

13-65

© The McGraw-Hill Companies, Inc., 2006

This ratio reveals information about the stock market’s This ratio reveals information about the stock market’s expectations for a company’s future growth in expectations for a company’s future growth in

earnings, dividends, and opportunities.earnings, dividends, and opportunities.

This ratio reveals information about the stock market’s This ratio reveals information about the stock market’s expectations for a company’s future growth in expectations for a company’s future growth in

earnings, dividends, and opportunities.earnings, dividends, and opportunities.

If earnings go up,will the market priceof my stock follow?

Price EarningsPrice Earnings

Price-Price-EarningsEarnings ==

Market value per shareMarket value per share Earnings per shareEarnings per share

McGraw-Hill/Irwin66

13-66

© The McGraw-Hill Companies, Inc., 2006

Homework for Chapter 13Homework for Chapter 13

Ex 13-16, 13-17 Problem 13-2A, 13-4A Due on July 12, 2006 (Wednesday)

McGraw-Hill/Irwin67

13-67

© The McGraw-Hill Companies, Inc., 2006

End of Chapter 13End of Chapter 13