Embed Size (px)

Citation preview

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

©2013 C

lifto

nLars

onA

llen L

LP

CLAconnect.com

Doing Business in Canada May 7, 2014

Jen Leary, CliftonLarsonAllen

Jonathan Bicher, Nexia Friedman

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

Disclaimers

To ensure compliance imposed by IRS Circular 230, any U. S. federal tax advice contained in this presentation is not intended or written to be used, and cannot be used by any taxpayer, for the purpose of avoiding penalties that may be imposed by governmental tax authorities.

The information contained herein is general in nature and is not intended, and should not be construed, as legal, accounting, or tax advice or opinion provided by CliftonLarsonAllen LLP to the user. The user also is cautioned that this material may not be applicable to, or suitable for, the user’s specific circumstances or needs, and may require consideration of non-tax and other tax factors if any action is to be contemplated. The user should contact his or her CliftonLarsonAllen LLP or other tax professional prior to taking any action based upon this information. CliftonLarsonAllen LLP assumes no obligation to inform the user of any changes in tax laws or other factors that could affect the information contained herein.

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

Housekeeping

• If you are experiencing technical difficulties, please dial: 800-422-3623.

• Q&A session will be held at the end of the presentation.

– Your questions can be submitted via the Questions Function at any time during the presentation.

• The PowerPoint presentation, as well as the webinar recording, will be sent to you within the next 10 business days.

• Please complete our online survey.

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

CPE Requirements

• Answer the polling questions

• If you are participating in a group, complete the CPE sign-in sheet and return within two business days

– Contact [email protected]

• Allow four weeks for receipt of your certificate; it will be sent to you via email

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

Learning Objectives

• At the end of this session, you will be able to:

– Understand key developments in the Canadian economy, as well as practical guidance and considerations for doing business in Canada

– Understand the common forms needed to do business in Canada and their major tax structure for individuals and businesses operating in Canada

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

About CliftonLarsonAllen

• A professional services firm with three distinct business lines

– Accounting and Consulting

– Outsourcing

– Wealth Advisory

• 3,600 employees

• Offices coast to coast

• Independent member of Nexia International

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

CLA’s Global Services practice includes over 250 team

members throughout the U.S.

Our experience serving international businesses

allows us to provide support and insight.

CLA is the largest independent member of

Nexia International, a top 10 worldwide network of

independent accounting and consulting firms.

Founded in 1971

Top 10 network

worldwide

590 offices in over

100 countries

20,000 worldwide

staff

$2.1 billion in revenue

CLA’s Global Reach

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

Speaker Introductions

• Jennifer Leary, CliftonLarsonAllen A leader in our global services team, Jen has over 17 years of experience in audit, advisory, mergers and acquisitions, internal audit, corporate governance, controls and risk assessments and internal audit department quality assurance reviews. She advises companies through due diligence and reverse due diligence engagements in conjunction with mergers and acquisitions within the U.S. and cross-border.

• Jonathan Bicher, Nexia Friedman Jonathan is the Chair of the Nexia Canada Tax Committee. He specializes in corporate and personal tax planning as well as both domestic and cross-border reorganizations and transactions. He has strong expertise in mergers and acquisitions architecture and execution. Jonathan provides services to U.S. companies doing business in Canada, working with diverse clientele as the entertainment industry, comedians, family-owned businesses, and service companies.

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

9

May 2014

Presented by: Jonathan Bicher, CPA, CA

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

CANADA

Largest bilateral trading relationship in the world

300,000 people cross our shared border, daily

$1.6 billion worth of goods cross our shared border, daily

Why should you pay attention to this webinar?

10

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

11

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

12

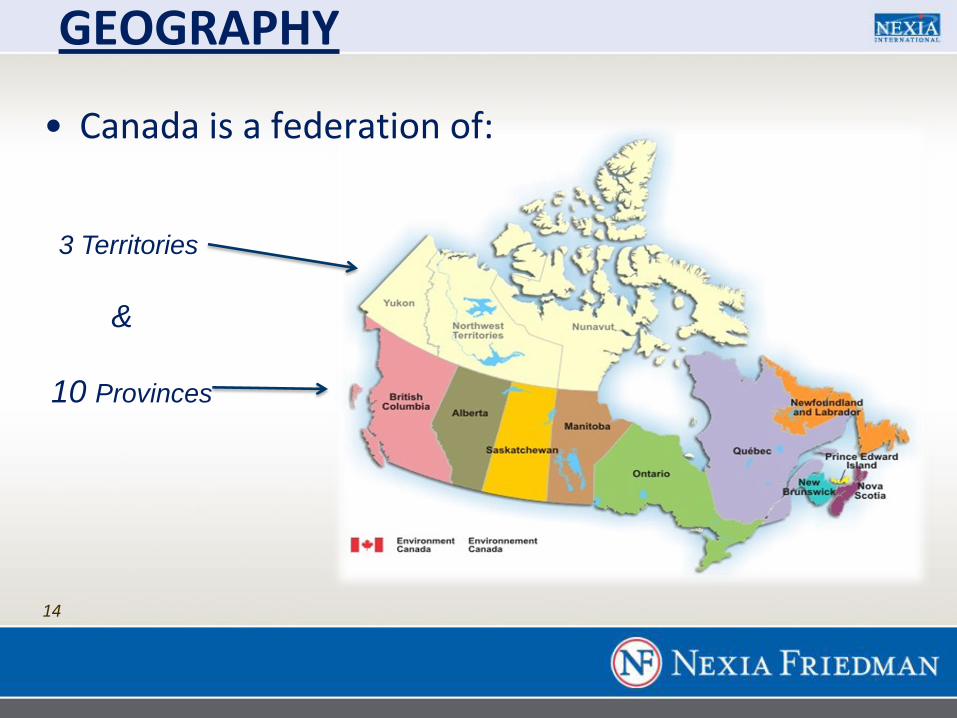

GEOGRAPHY

Second largest country in area in the world after

Russia

Over 3,850,000 square miles

Almost 9% is fresh water located in over 31,000

large lakes

125,570 miles: Longest coastline in the world

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

13

GEOGRAPHY

Canada/US border over 5,525 miles

Stretches from Maine to Washington State

Longest undefended border in the world

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

14

GEOGRAPHY

• Canada is a federation of:

10 Provinces

3 Territories

&

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

15

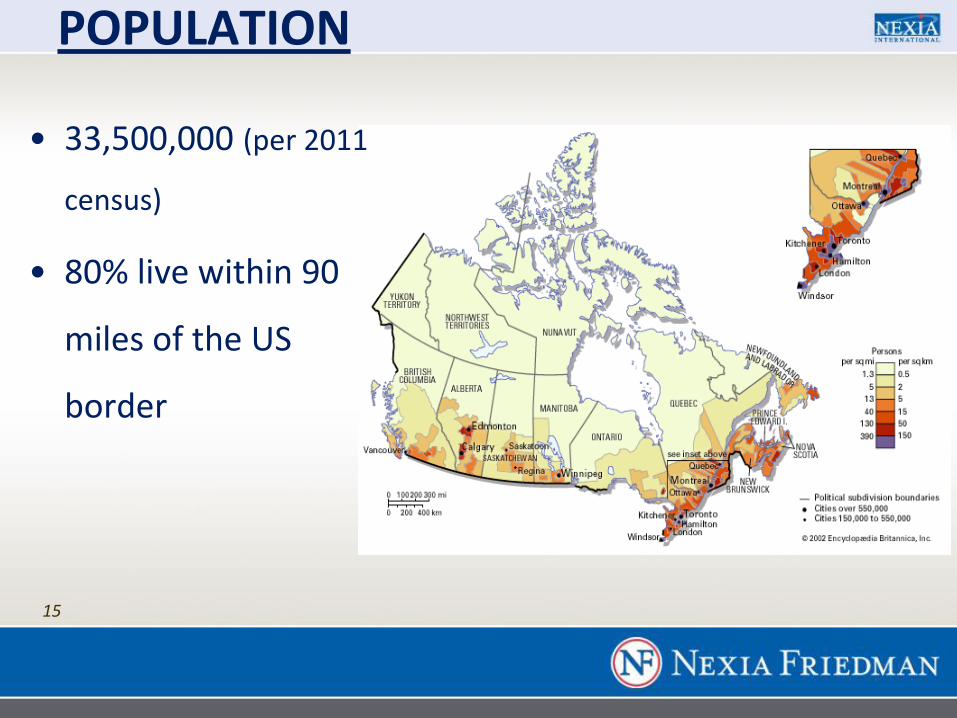

POPULATION

• 33,500,000 (per 2011

census)

• 80% live within 90

miles of the US

border

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

16

POPULATION

- Toronto

(5.6 million)

- Montreal

(3.8 million)

- Vancouver

(2.3 million)

The largest cities are:

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

17

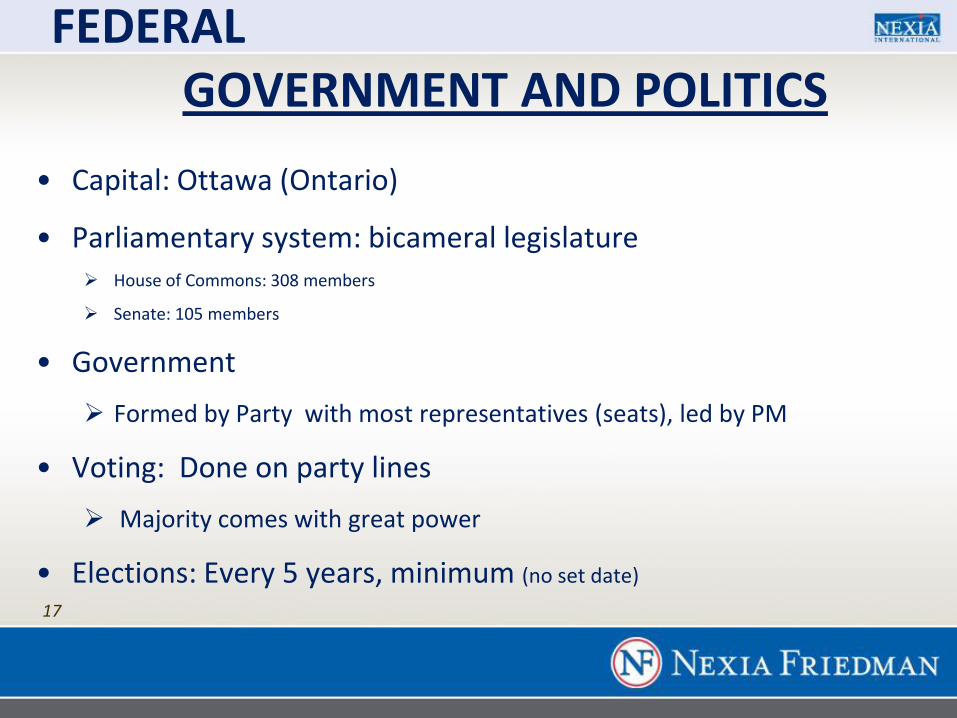

FEDERAL GOVERNMENT AND POLITICS

• Capital: Ottawa (Ontario)

• Parliamentary system: bicameral legislature House of Commons: 308 members

Senate: 105 members

• Government

Formed by Party with most representatives (seats), led by PM

• Voting: Done on party lines

Majority comes with great power

• Elections: Every 5 years, minimum (no set date)

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

18

PROVINCIAL GOVERNMENT AND POLITICS

• Mimics Federal system, except:

Unicameral legislature

• Provinces are very powerful and autonomous

• Some provincial responsibilities include:

Healthcare

Education

Welfare

• Provinces collect more revenue than the federal government

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

19

LEGAL SYSTEM

• Constitutional Act of 1982

Ended all legislative ties to the UK

• Common law prevails

• Quebec civil law predominates

• Criminal law is federal

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

20

LANGUAGE

• Canada is officially a bilingual country

English

French

• Primary language in most of Canada: English

Exception:

In Quebec, French is the primary language

• However, even in Quebec, one can conduct business in English

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

21

THINGS TO CONSIDER WHEN VISITING

1. Passport: needed to get into Canada

2. Temperature: measured in Celsius not Fahrenheit 32C = 90F

Thus pack accordingly

3. Distance: measured in KPH not MPH

100KPH = 60 MPH

Thus drive accordingly

4. Canada has its own currency

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

22

BUSINESS CLIMATE

• Ranked best place for doing business among G-7 (per 2013 study of the Economist)

• Highly developed infrastructure

• Rated first in recent study measuring a country’s ability to attract

foreign investment on the basis of economic infrastructure

• Low business costs

• Low corporate taxes

• Little red tape for business

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

23

DOING BUSINESS IN CANADA

• Banking

– 5 major chartered banks

– Other second tier banks

– Very profitable and stable

– Centralized decision making

– Highly regulated

– Minimally affected by the world banking crisis

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

24

DOING BUSINESS IN CANADA

• Banking

– Non-residents Opening a Bank Account

– Individuals

– Need proper identification

– Corporations

– Must have proper identification

– Must have valid reason

• Once proper information and documentation is provided, account can normally be opened within 48 hours

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

25

DOING BUSINESS IN CANADA

– Banking

• One can open bank accounts in Canadian

or U.S. dollars

• Funds can be wired back and forth effortlessly

• Cheques drawn on U.S. banks may take time to clear and

there may be a holding period

• Not all banks are equal; some banks are more U.S. focused

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

26

DOING BUSINESS IN CANADA

– Investment / Wealth Management

• Not all firms licensed to deal with U.S.

Residents

• Not all advisors at the same firm are licensed to deal with U.S. residents

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

27

DOING BUSINESS IN CANADA

– Investment / Wealth Management

• Investments often structured with Canadian

tax laws in mind

• Must always analyze investments to determine what the impact would be for U.S. Taxpayer; Canadian advisors are not structuring keeping U.S. in mind

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

28

DOING BUSINESS IN CANADA

– Provincially controlled

Rules vary from province to province

– Be aware of funding requirements for social programs

(such as manpower training)

– Pay equity, language

– Often the employee receives the benefit of the doubt

Labour standards:

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

29

DOING BUSINESS IN CANADA

• Canada has a national healthcare system

HOWEVER:

The management and funding is the responsibility of the

Provinces

• Funding: usually done through employer as a function of salaries

• Each province in which one has employees may require funding

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

30

BUSINESS CLIMATE GDP Growth

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

31

BUSINESS CLIMATE GDP Growth (cont’d)

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

32

BUSINESS CLIMATE WORKFORCE

• 51%: Highest % of individuals 25-64 having attained post-secondary education (2012 OECD study)

Compared to 42% in the U.S. And 38% in the U.K.

• 3 : Canadian universities in the top 100 in the world per QS World University

– McGill University

– University of Toronto

– University of British Columbia

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

33

BUSINESS CLIMATE WORKFORCE (cont’d)

• Canadian work-force

Multilingual

Well-travelled

Highly recognized for ability to work in international contexts

• Canada ranked first in G-7 in 2012 study measuring how management education meets needs of business community

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

34

BUSINESS CLIMATE TRADE WITH U.S.

• 53.7% of foreign direct investment in Canada held by U.S.

Investors (in 2011)

• By far, the U.S. is Canada’s largest trading partner

• Trade benefits from:

Streamlined trans-border transportation system

RESULT:

Making it one of the world’s most efficient border systems

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

35

INVESTMENT CLIMATE

• Generous tax incentives for R&D

• World-leader in post-secondary research

• Many Canadian production hubs closer to U.S. Markets than

American production sites

• Canada’s GDP per capita was highest among G-7 countries

offering ex-pats a very high standard of living (Per 2012 World Bank study)

• Low inflation and low interest rates

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

36

COMMON FORM FOR BUSINESS

1. Corporations

2. Partnerships

3. Unlimited Liability Corporations (ULC)

4. Branches

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

37

COMMON FORMS FOR BUSINESS Corporations

• Most popular vehicle for business

• Can be federally or provincially incorporated;

Generally use federal companies or companies

established under legislation of province of operation

• Income tax paid within corporation

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

38

COMMON FORMS FOR BUSINESS Partnerships

• Income taxed in hands of partners

• Historically offered tax deferral opportunities,

which were removed in the last few years

• Often complex reporting requirements

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

39

COMMON FORMS FOR BUSINESS ULCs

• Alberta, British Columbia and Nova Scotia offer Unlimited Liability

Corporations

• For Canadian purposes

Treated as ordinary corporations

• For US purposes

Possible to treat a disregarded entity

• Could be subject to 25% withholding tax on the payment of

dividends

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

40

COMMON FORMS FOR BUSINESS Branches

• Earnings in Canada of a branch of a foreign

corporation taxed in Canada

• In addition, such branches may be subject to an

additional branch tax

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

41

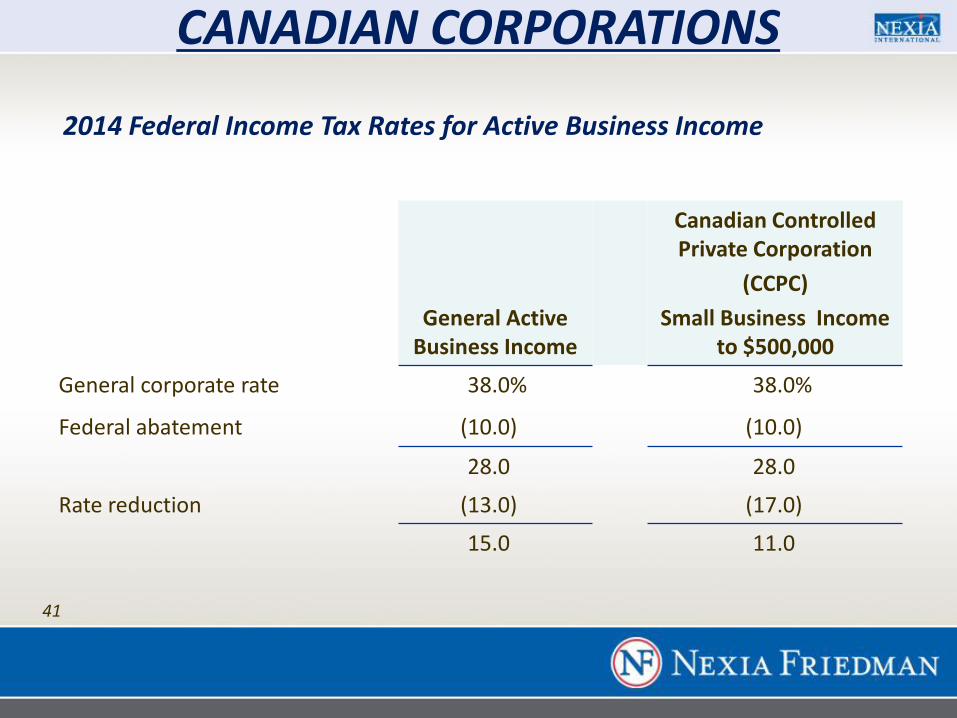

2014 Federal Income Tax Rates for Active Business Income

General Active Business Income

Canadian Controlled Private Corporation

(CCPC)

Small Business Income to $500,000

General corporate rate 38.0% 38.0%

Federal abatement (10.0) (10.0)

28.0 28.0

Rate reduction (13.0) (17.0)

15.0 11.0

CANADIAN CORPORATIONS

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

42

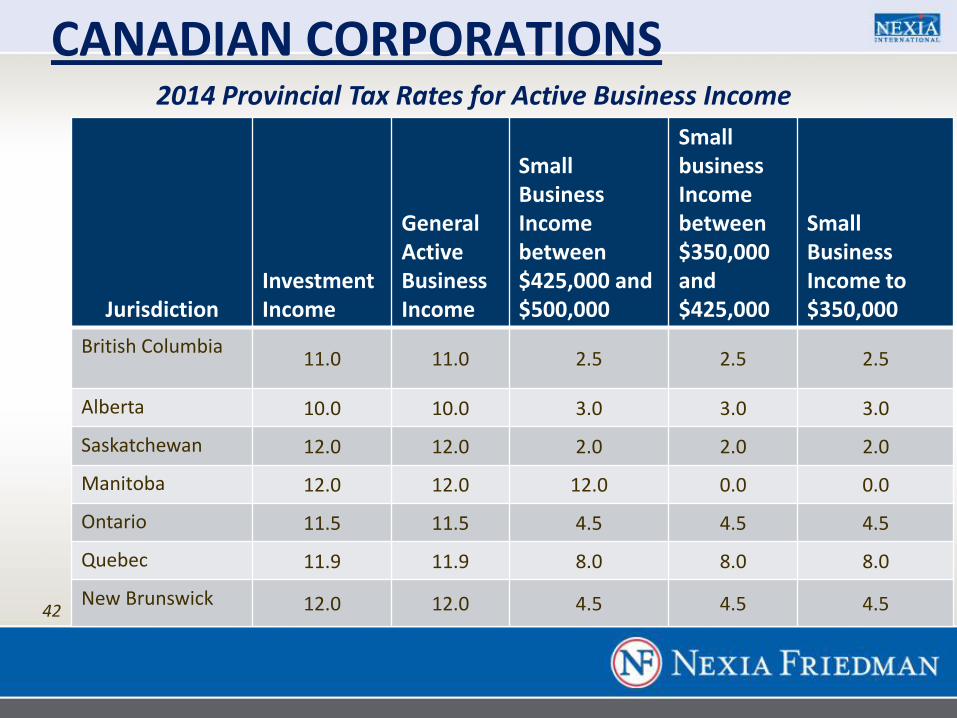

CANADIAN CORPORATIONS 2014 Provincial Tax Rates for Active Business Income

Jurisdiction Investment Income

General Active Business Income

Small Business Income between $425,000 and $500,000

Small business Income between $350,000 and $425,000

Small Business Income to $350,000

British Columbia 11.0 11.0 2.5 2.5 2.5

Alberta 10.0 10.0 3.0 3.0 3.0

Saskatchewan 12.0 12.0 2.0 2.0 2.0

Manitoba 12.0 12.0 12.0 0.0 0.0

Ontario 11.5 11.5 4.5 4.5 4.5

Quebec 11.9 11.9 8.0 8.0 8.0

New Brunswick 12.0 12.0 4.5 4.5 4.5

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

43

2014 Provincial Tax Rates for Active Business Income

CANADIAN CORPORATIONS

Jurisdiction Investment Income

General Active Income

Small Business Income between $425,000 and $500,000

Small Business Income between $350,000 and $425,000

Small Business Income to $350,000

Nova Scotia 16.0% 16.0% 16.0% 16.0% 3.0%

Prince Edward Island

16.0 16.0 1.0/4.5 1.0/4.5 1.0/4.5

Newfoundland 14.0 14.0 4.0/3.0 4.0/3.0 4.0/3.0

Northwest Territories

11.5 11.5 4.0 4.0 4.0

Yukon 15.0 15.0 4.0 4.0 4.0

Nunavut 12.0 12.0 4.0 4.0 4.0

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

44

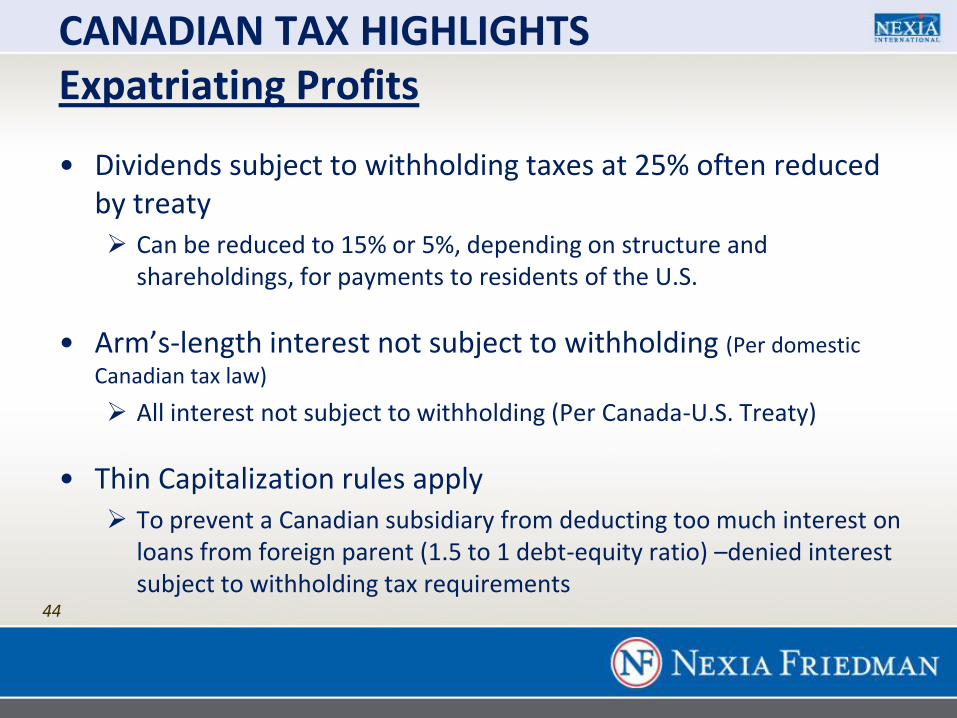

CANADIAN TAX HIGHLIGHTS Expatriating Profits

• Dividends subject to withholding taxes at 25% often reduced by treaty Can be reduced to 15% or 5%, depending on structure and

shareholdings, for payments to residents of the U.S.

• Arm’s-length interest not subject to withholding (Per domestic

Canadian tax law)

All interest not subject to withholding (Per Canada-U.S. Treaty)

• Thin Capitalization rules apply To prevent a Canadian subsidiary from deducting too much interest on

loans from foreign parent (1.5 to 1 debt-equity ratio) –denied interest subject to withholding tax requirements

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

45

ACTIVITIES CARRIED OUT IN CANADA

1. Sending employees to perform services in Canada

2. Renting a warehouse in Canada

3. Engaging an independent sales force in Canada

4. Disposition of Taxable Canadian Property

5. Importing goods into Canada

THAT MAY LEAD TO CANADIAN TAX

FILING

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

46

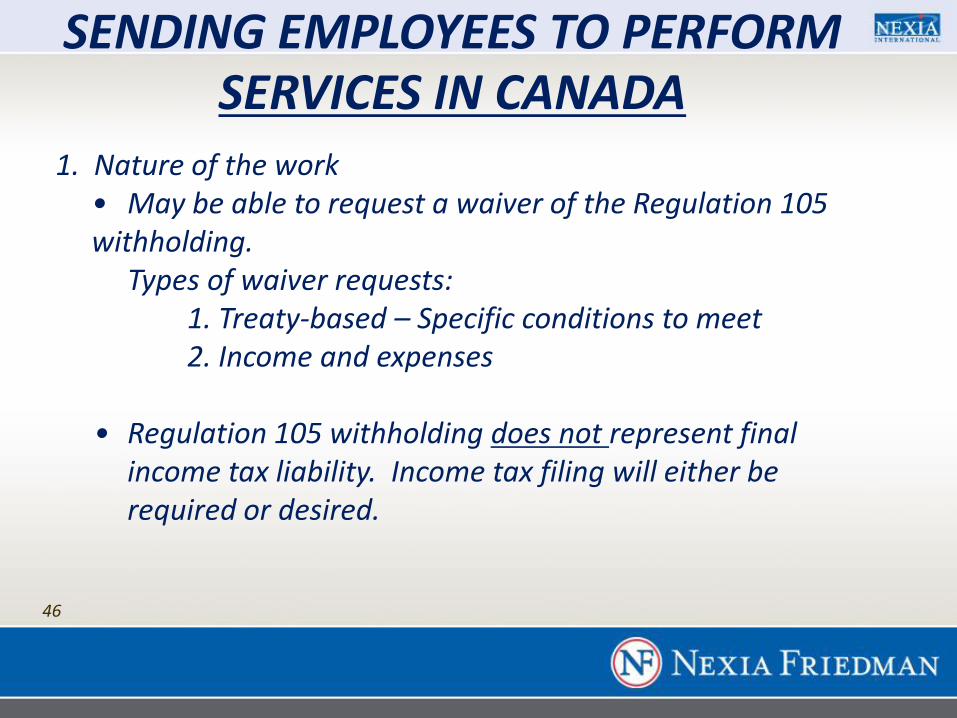

SENDING EMPLOYEES TO PERFORM SERVICES IN CANADA

1. Nature of the work • May be able to request a waiver of the Regulation 105

withholding. Types of waiver requests: 1. Treaty-based – Specific conditions to meet 2. Income and expenses

• Regulation 105 withholding does not represent final income tax liability. Income tax filing will either be required or desired.

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

47

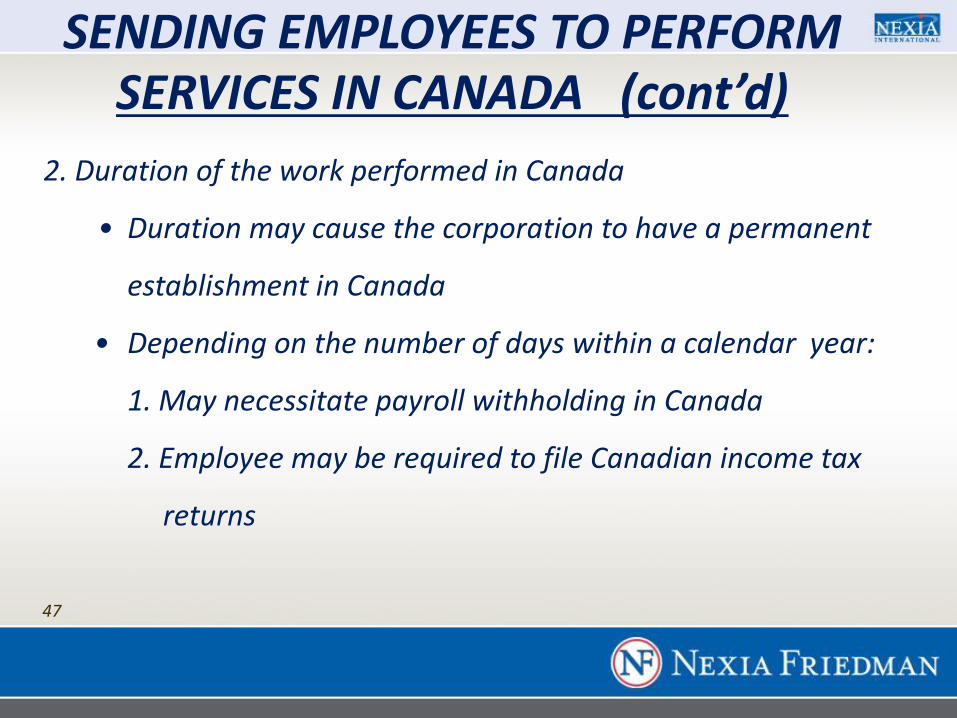

2. Duration of the work performed in Canada

• Duration may cause the corporation to have a permanent

establishment in Canada

• Depending on the number of days within a calendar year:

1. May necessitate payroll withholding in Canada

2. Employee may be required to file Canadian income tax

returns

SENDING EMPLOYEES TO PERFORM SERVICES IN CANADA (cont’d)

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

48

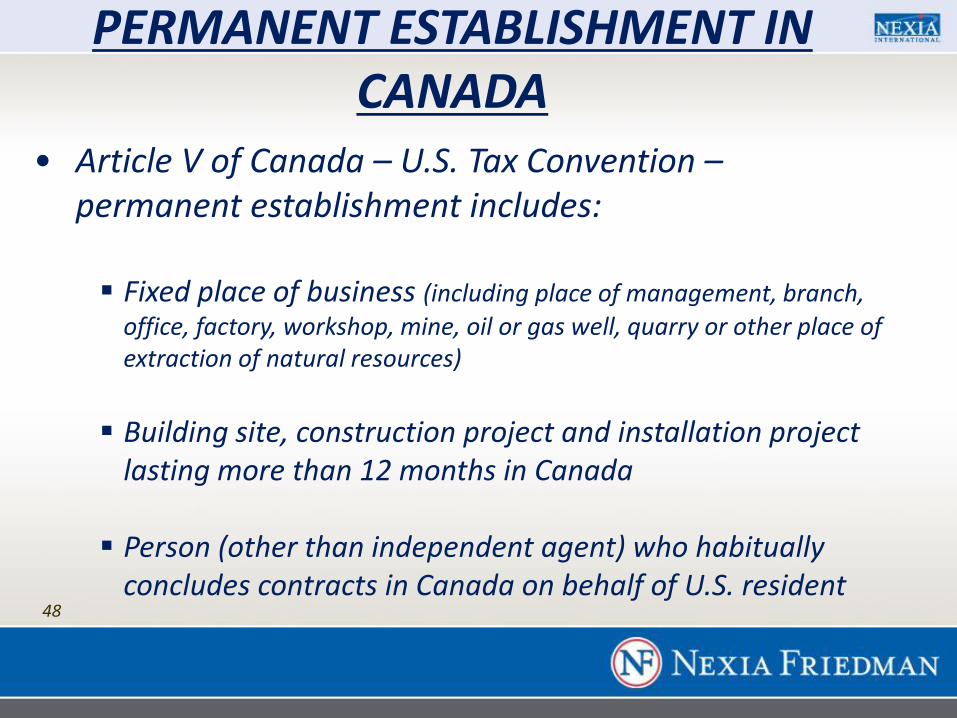

PERMANENT ESTABLISHMENT IN CANADA

• Article V of Canada – U.S. Tax Convention – permanent establishment includes:

Fixed place of business (including place of management, branch,

office, factory, workshop, mine, oil or gas well, quarry or other place of extraction of natural resources)

Building site, construction project and installation project

lasting more than 12 months in Canada Person (other than independent agent) who habitually

concludes contracts in Canada on behalf of U.S. resident

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

49

• Permanent establishment does not include:

Fixed place of business used solely for storage, display or

delivery (e.g., warehouse or showroom)

Independent agent

• May have to file treaty-based return

PERMANENT ESTABLISHMENT IN CANADA (cont’d)_

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

50

The Fifth Protocol

• Fifth Protocol expands definition of permanent

establishment to include, in 2010 and later years:

Services provided by an individual that has a presence for

183 days or more in any 12 month period and, during that

period, more than 50% of gross active business revenues

consist of income derived from services performed in that

country by that individual

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

51

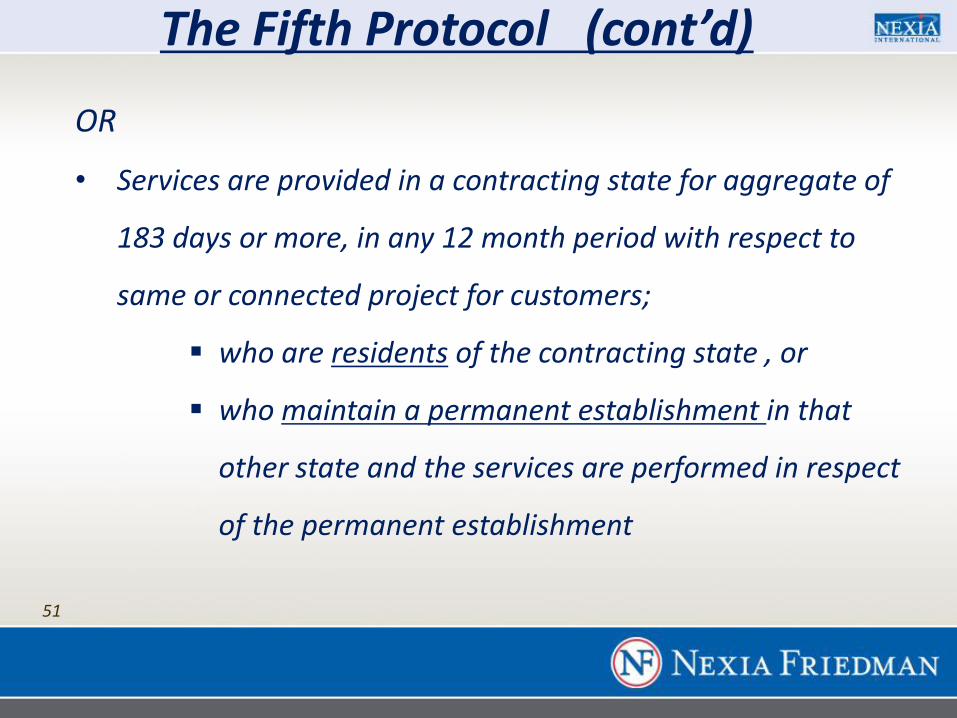

OR

• Services are provided in a contracting state for aggregate of

183 days or more, in any 12 month period with respect to

same or connected project for customers;

who are residents of the contracting state , or

who maintain a permanent establishment in that

other state and the services are performed in respect

of the permanent establishment

The Fifth Protocol (cont’d)

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

52

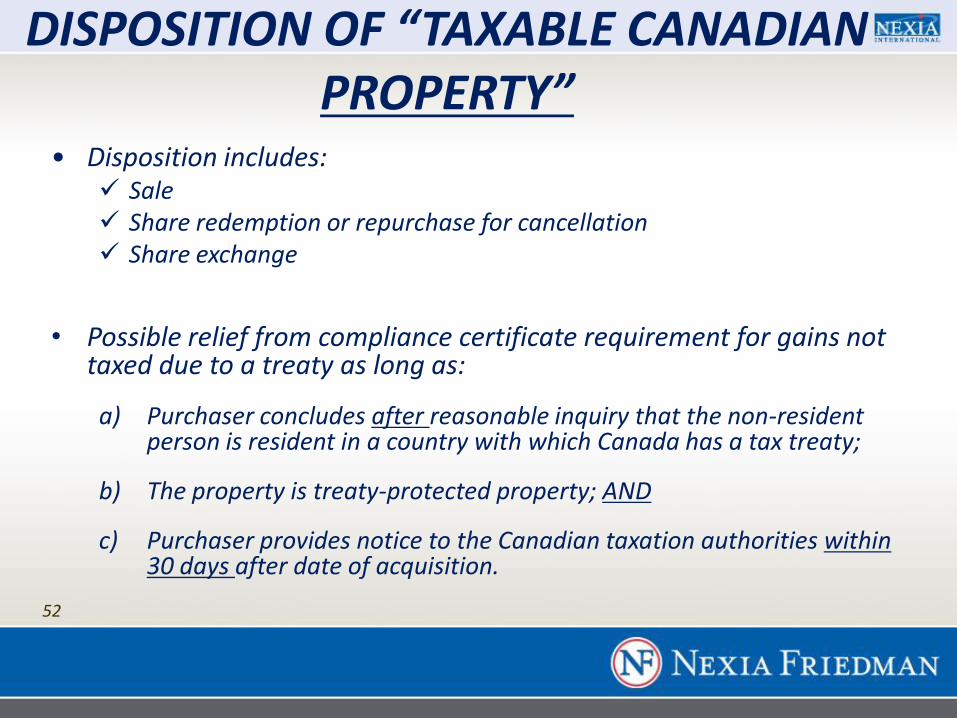

DISPOSITION OF “TAXABLE CANADIAN PROPERTY”

• Disposition includes: Sale Share redemption or repurchase for cancellation Share exchange

• Possible relief from compliance certificate requirement for gains not taxed due to a treaty as long as:

a) Purchaser concludes after reasonable inquiry that the non-resident person is resident in a country with which Canada has a tax treaty;

b) The property is treaty-protected property; AND

c) Purchaser provides notice to the Canadian taxation authorities within 30 days after date of acquisition.

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

53

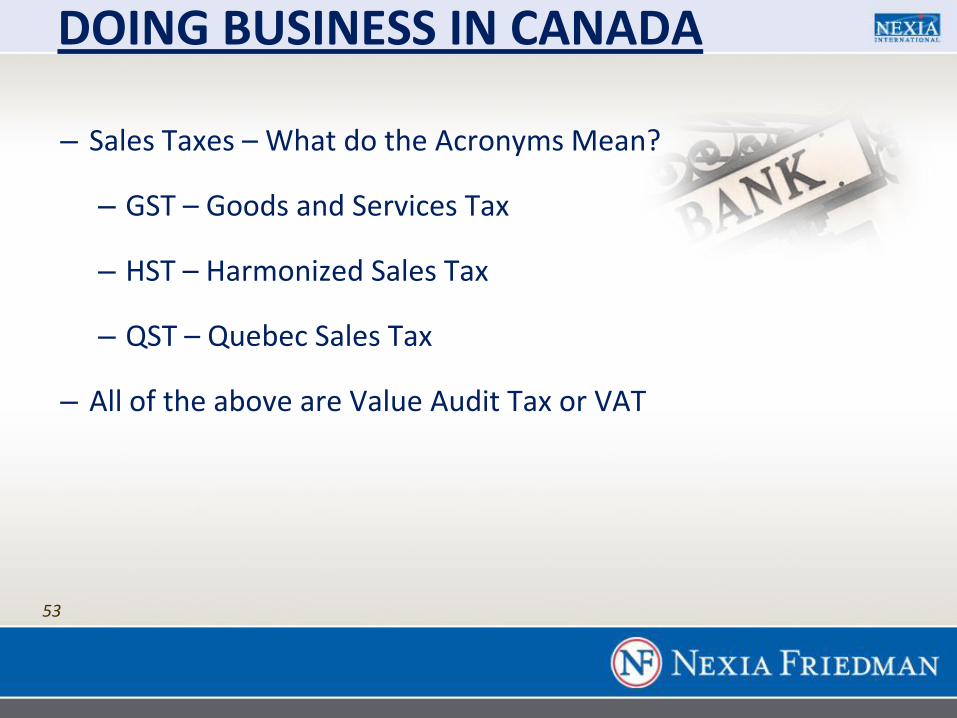

DOING BUSINESS IN CANADA

– Sales Taxes – What do the Acronyms Mean?

– GST – Goods and Services Tax

– HST – Harmonized Sales Tax

– QST – Quebec Sales Tax

– All of the above are Value Audit Tax or VAT

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

54

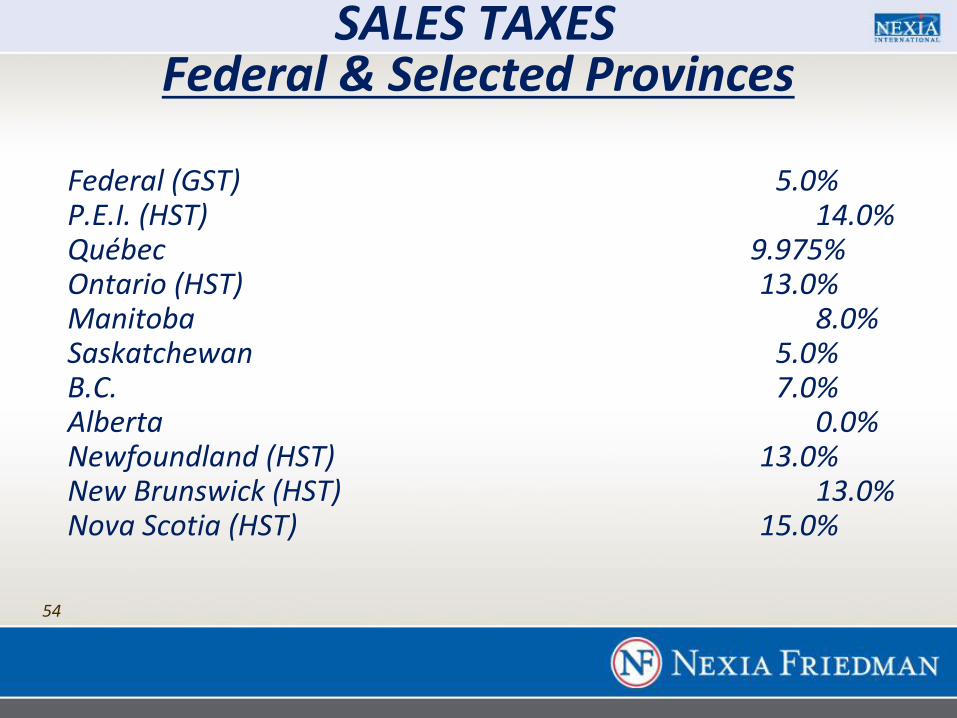

SALES TAXES Federal & Selected Provinces

Federal (GST) 5.0% P.E.I. (HST) 14.0% Québec 9.975% Ontario (HST) 13.0% Manitoba 8.0% Saskatchewan 5.0% B.C. 7.0% Alberta 0.0% Newfoundland (HST) 13.0%

New Brunswick (HST) 13.0%

Nova Scotia (HST) 15.0%

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

55

Mechanics of VAT in Canada

• GST is collected and remitted at each stage in the

production and marketing of most goods and services,

unless the supply is zero-rated or exempt

• Registrants may recover GST paid on properties and

services acquired in order to make taxable and zero-rated

supplies

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

56

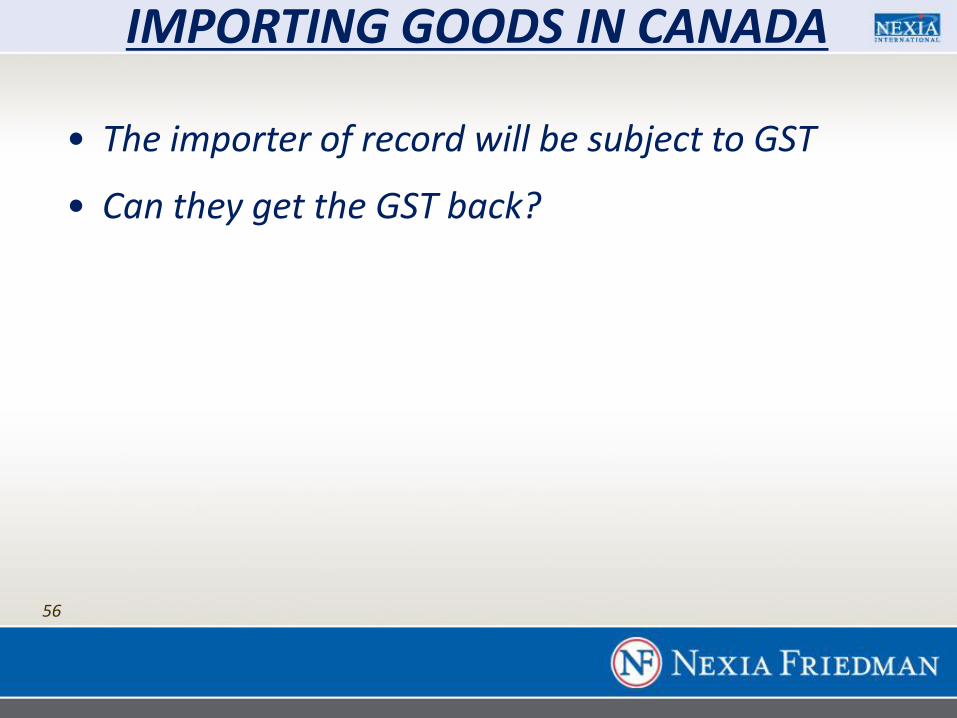

IMPORTING GOODS IN CANADA

• The importer of record will be subject to GST

• Can they get the GST back?

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

57

GST REGISTRATION

• A person, including a non-resident, must register if the person carries on business in Canada and is not a small supplier 1

• Non-residents who do not carry on business in Canada may voluntary register if they are engaged in a commercial activity in Canada, regularly solicit orders for goods to be delivered in Canada, provide services in Canada or intangibles to be used in Canada

• Non-residents who do not carry on business in Canada through a

permanent establishment may have to provide a security deposit • The particular facts of each situation must be examined to

determine whether GST registration for a non-resident is required or desired

1 Taxable sales equal to or less than $30,000 in four preceding quarters

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

58

REAL ESTATE RENTALS

• 25% withholding tax on gross rental income

• Can file section 216 election to have withholding based on net rental income before depreciation

• Will be required to file a Canadian tax return with final numbers

• Vehicle through which to own Canadian real estate depends upon the situation

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

Questions?

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

60

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

CLAconnect.com

twitter.com/ CLAconnect

facebook.com/ cliftonlarsonallen

linkedin.com/company/ cliftonlarsonallen

Thank you

Jen Leary

704-998-5283

Jonathan Bicher [email protected] 514-731-7901