Embed Size (px)

Citation preview

Production and Cost Analysis I 12

Production and Cost Analysis I

Production is not the application of

tools to materials, but logic to work.

— Peter Drucker

CHAPTER 12

Copyright © 2010 by the McGraw-Hill Companies, Inc. All rights reserved.McGraw-Hill/Irwin

Production and Cost Analysis I 12

Maximizing Profit

• The goal of a firm is to maximize profits

• Profit = Total Revenue – Total Cost

12-2

Production and Cost Analysis I 12

Explicit versus Implicit Costs

• Explicit cost =money paid out (rent, wages, etc.)

• Implicit cost=opportunity cost of the factors of production used by the firm

12-3

Production and Cost Analysis I 12

Economic versus Accounting Profit

• Economists and accountants measure profit differently

• Unlike accountants, economists also consider implicit costs (the opportunity cost of what they could have done instead)

McGraw-Hill/Irwin Colander, Economics 4

Production and Cost Analysis I 12

Economic versus Accounting Profit

• Economists focus on both explicit and implicitcosts and revenue

• Economic profit = (explicit + implicit revenue) – (explicit + implicit cost)

• Accountants focus on explicit costs and revenues

• Accounting profit = explicit revenue –explicit cost

McGraw-Hill/Irwin Colander, Economics 5

Production and Cost Analysis I 12

Economic versus Accounting Profit

• When discussing costs, if a firm is making zeroeconomic profit they are always making a positive accounting profit

• This is because accounting profit does not take into consideration the opportunity cost of what they could have done instead

McGraw-Hill/Irwin Colander, Economics 6

Production and Cost Analysis I 12

Short run versus Long run

McGraw-Hill/Irwin Colander, Economics 7

• In the short run a firm is limited in regard to what production decisions it can make• Some inputs are fixed and cannot be

changed

• In the long run all inputs are variable inputs and can be changed

Production and Cost Analysis I 12

The Production Function

• The production function tells the maximum amount of output that can be derived from a given number of inputs

• Note it has three stages

McGraw-Hill/Irwin Colander, Economics 8

Production and Cost Analysis I 12

Graphing a Production Function Q

Increasing marginal productivity

Diminishingmarginal productivity

DiminishingAbsolute productivity

Number of workers

TP

A production function is the

relationship between then inputs and the

outputs

32

26

20

14

8

2

1 2 3 4 5 6 7 8 9 10

12-9

Production and Cost Analysis I 12

Law of Diminishing Marginal Productivity

• Law of diminishing marginal productivity: as more of a variable input is added to an existing fixed input, after some point the additional output from the additional input will fall

McGraw-Hill/Irwin Colander, Economics 10

Production and Cost Analysis I 12

Law of Diminishing Marginal Productivity

# of

workers

Total

Output

Marginal

Product

Average

Product

0 04

6

7

6

5

3

1

0

-2

-5

---

1 4 4

2 10 5

3 17 5.7

4 23 5.8

5 28 5.6

6 31 5.2

7 32 4.6

8 32 4.0

9 30 3.3

10 25 2.5

Increasing marginal productivity

Diminishingmarginal productivity

DiminishingAbsolute productivity

12-11

Production and Cost Analysis I 12

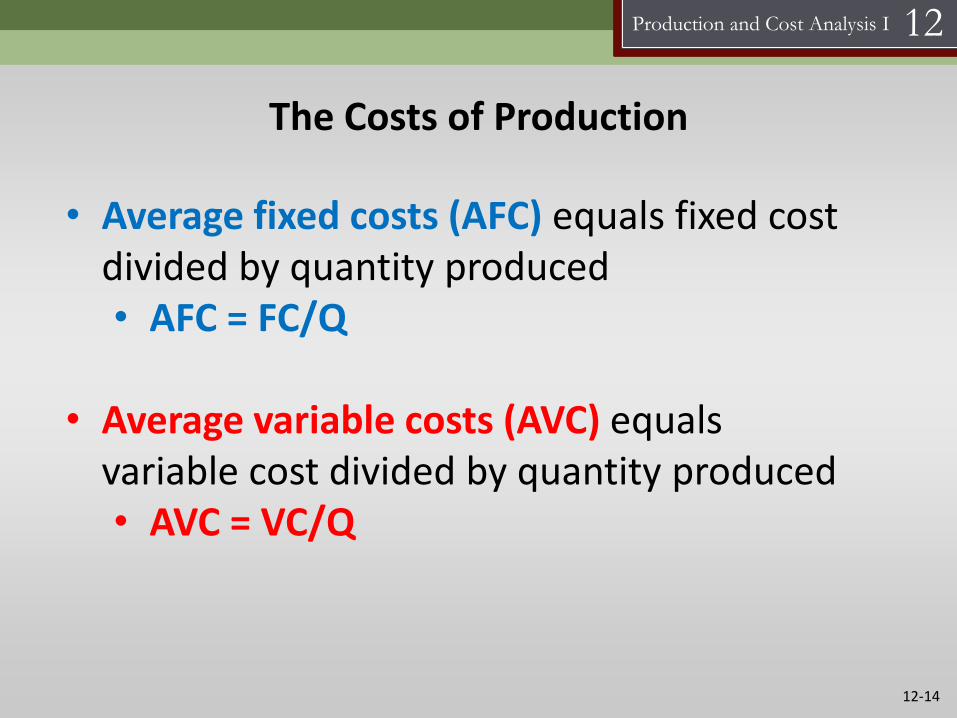

The Costs of Production

• Fixed costs (FC) are those that are spent and cannot be changed in the period of time under consideration

• In the short run, a number of inputs and their costs will be fixed

• In the long run, there are NO fixed costs since all inputs are variable

12-12

Production and Cost Analysis I 12

The Costs of Production

• Variable costs (VC) are costs that change as output changes

• Workers are an example of VC

• Total cost (TC) is the sum of the variable and fixed costs

• TC = FC + VC

McGraw-Hill/Irwin Colander, Economics 13

Production and Cost Analysis I 12

The Costs of Production

• Average fixed costs (AFC) equals fixed cost divided by quantity produced• AFC = FC/Q

• Average variable costs (AVC) equals variable cost divided by quantity produced• AVC = VC/Q

12-14

Production and Cost Analysis I 12

The Costs of Production

• Average total cost (ATC) equals total cost divided by quantity produced

• ATC = TC/Q or ATC = AFC + AVC

• Marginal cost (MC) is the increase in total cost when output increases by one unit

• MC = ΔTC/ΔQ

McGraw-Hill/Irwin Colander, Economics 15

Production and Cost Analysis I 12

Costs of Production Table

Output FC ($) VC ($) TC ($) MC ($) AFC ($) AVC ($) ATC ($)

3 50 38 8812

16.67 12.66 29.33

4 50 50 100 12.50 12.50 25.00

9 50 100 1508

5.56 11.11 16.67

10 50 108 158 5.00 10.80 15.80

16 50 150 2007

3.13 9.38 12.51

17 50 157 207 2.94 9.24 12.18

22 50 200 25010

2.27 9.09 11.36

23 50 210 260 2.17 9.13 11.30

27 50 255 30515

1.85 9.44 11.29

28 50 270 320 1.79 9.64 11.43

32 50 400 450 1.56 12.50 14.06

12-16

Production and Cost Analysis I 12

The Shapes of Cost Curves

• The variable and total cost curves have the same shape

• Increasing output increases VC and TC

• The fixed cost curve is always constant

• Increasing output doesn’t change FC

12-17

Production and Cost Analysis I 12

Graphing Total Cost Curves

FC

Total Cost

FC curve is constant

TC and VC curves

increase as Q increases

Q

500

400

300

200

100

04 8 12 16 20 24 28 32

VC

TC

12-18

Production and Cost Analysis I 12

The Shapes of Cost Curves

• The average fixed cost (AFC) curve is downward sloping

• Increasing output decreases AFC

• The marginal cost (MC), average variable cost (AVC), and average total cost curves (ATC) are U-shaped

• Increasing output initially leads to a decrease in MC, AVC, and ATC but eventually they increase

McGraw-Hill/Irwin Colander, Economics 19

Production and Cost Analysis I 12

Graphing Per Unit Output Cost Curves

AVC

MC

ATC

AFCQ

Cost

AFC curve decreases

MC, ATC, and AVC curves

are U-shaped

35

30

25

20

15

10

5

04 8 12 16 20 24 28 32

12-20

Production and Cost Analysis I 12

The Shapes of Cost Curves

• The marginal cost curve goes through the minimum points of the ATC and AVC curves (remember this)

McGraw-Hill/Irwin Colander, Economics 21

Production and Cost Analysis I 12

Draw the Graph: Marginal Cost, AVC, and ATC

AVC

MC

Q

Costs per unit

ATCThe marginal cost curve goes through the minimum point

of both the ATC and AVC curves

12-22

Production and Cost Analysis I 12

• If MC > ATC, then ATC is rising

• If MC > AVC, then AVC is rising

• If MC < ATC, then ATC is falling

• If MC < AVC, then AVC is falling

• If MC = AVC and MC = ATC, then AVC and ATC are at their minimum points

The Relationship Between Marginal Cost and Average Cost

12-23

Production and Cost Analysis I 12

Profit Maximization Using Total Revenue and Total Cost (CH 14; Not in your notes)

• Total Revenue= Price x Quantity

• Total revenue and total cost curves can be used to determine the profit-maximizing level of output

• Total cost is the cumulative sum of the marginal costs, plus the fixed costs

• Total profit is the difference between total revenue and total cost curves

14-24

Production and Cost Analysis I 12

Total Revenue and Total Cost Table(CH 14; Not in your notes)

Q Total Revenue ($) Total Cost ($) Total Profit ($)

0 0 40 -40

1 35 68 -33

2 70 88 -18

3 105 104 1

4 140 118 22

5 175 130 45

6 210 147 63

7 245 169 76

8 280 199 81

9 315 239 76

10 350 293 57

Total profit is maximized at 8 units

of output

14-25

Production and Cost Analysis I 12

Total Revenue and Total Cost Table (CH 14; Not in your notes)

Total Cost, Total Revenue

TC

$175

Q

$130

$280

85

TRThe total revenue curve is a

straight line

The total cost curve is bowed upward at most

quantities reflecting increasing marginal cost

Could see this graph in the multiple choice

3

Losses LossesProfits

Profits are maximized when the vertical distance

between TR and TC is greatest

14-26

Production and Cost Analysis I 12

Chapter Summary

• Accounting profit is explicit revenue less explicit cost

• Economists include implicit revenue and cost in determining

economic profit

• Implicit revenue includes the increases in the value of assets

owned by the firm

• Implicit costs include opportunity cost of time and capital

provided by owners of the firm

• In the long run a firm can choose among all possible

production techniques; in the short run it is constrained in

its choices because at least one input is fixed

12-27

Production and Cost Analysis I 12

Chapter Summary

• The law of diminishing marginal productivity states that as more

of a variable input is added to a fixed input, the additional

output will eventually be decreasing

• Costs are generally divided into fixed costs, variable costs, and

marginal costs

• TC = FC + VC

• MC = ΔTC/ΔQ

• AFC = FC/Q

• AVC = VC/Q

• ATC = AFC + AVC

12-28

Production and Cost Analysis I 12

Chapter Summary

• The law of diminishing marginal productivity causes marginal

and average costs to rise

• MC goes through the minimum points of the AVC and ATC

• If MC > ATC, then ATC is rising

• If MC = ATC, then ATC is constant

• If MC < ATC, then ATC is falling

12-29

Production and Cost Analysis II 13

Production and Cost Analysis II

Economic efficiency consists of making

things that are worth more than they cost.

— J. M. Clark

CHAPTER 13

Copyright © 2010 by the McGraw-Hill Companies, Inc. All rights reserved.McGraw-Hill/Irwin

Production and Cost Analysis II 13

Technical Efficiency and Economic Efficiency

• Technical efficiency in production means that as few inputs as possible are used to produce a given output

• The economically efficient method of production produces a given level of output at the lowest possible cost

13-31

Production and Cost Analysis II 13

Shape of the Long run ATC

• The law of diminishing marginal productivity does not apply in the long run since all inputs are variable

• The shape of the long-run cost curve is due to the existence of economies and diseconomies of scale

13-32

Production and Cost Analysis II 13

Economies of Scale

• Economies of scale exist when long-run average total costs decrease as output increases

• These are shown by the downward sloping portion of the long-run ATC

13-33

Production and Cost Analysis II 13

Economies of Scale

• The minimum efficient level of production is the amount of production that spreads setup costs out sufficiently for firms to undertake production profitably

• This is where average total costs are at a minimum

13-34

Production and Cost Analysis II 13

Diseconomies of Scale

• Diseconomies of scale exist when long-run average total costs increase as output increases

• These are shown by the upward sloping portion of the long-run average total cost curve

13-35

Production and Cost Analysis II 13

A Typical Long run Average Total Cost Curve

Q

Costs per unit

11

$50

$55

17

$60

14 20

Long-run average total cost (LRATC)

Economies of scale Constant returns to scale

Diseconomies of scale

Minimum efficient level

of production

13-36

Production and Cost Analysis II 13

Constant Returns to Scale

• Constant returns to scale exist when average total costs do not change as output increases

• This is shown by the flat portion of the long-run average total cost curve

• Constant returns to scale occur when production techniques can be replicated again and again to increase output

13-37

Production and Cost Analysis II 13

A Typical Long run ATC Table

QTC of Labor

($)

TC of Machines

($)TC ($) ATC ($)

11 381 254 635 58

12 390 260 650 54

13 402 268 670 52

14 420 280 700 50

15 450 300 750 50

16 480 320 800 50

17 510 340 850 50

18 549 366 915 51

19 600 400 1000 53

20 666 444 1110 56

ATC falls because of economies of

scale

ATC is constant because of

constant returns to scale

ATC rises because of

diseconomies of scale

13-38

Production and Cost Analysis II 13

Chapter Summary

• An economically efficient production process must be technically efficient, but a technically efficient process may not be economically efficient

• The long-run average total cost curve is U-shaped because economies of scale cause average total cost to decrease; diseconomies of scale eventually cause average total cost to increase

• Marginal cost and short-run average cost curves slope upward because of diminishing marginal productivity

13-39

Production and Cost Analysis II 13

Chapter Summary

• The long-run average cost curve slopes upward because of diseconomies of scale

• Costs in the real world are affected by:

• Economies of scope

• Learning by doing and technological change

• Many dimensions to output

• Unmeasured costs, such as opportunity costs

13-40