Embed Size (px)

Citation preview

1

Introduction

1-2

Why study Financial Markets

and Institutions?

Markets and institutions are primary

channels to allocate capital in our society

Proper capital allocation leads to growth in:

Societal Wealth

Income

Economic opportunity

1-3

Financial Markets

Financial markets are one type of

structure through which funds flow

Financial markets can be distinguished

along two dimensions:

primary versus secondary markets

money versus capital markets

1-4

Primary versus Secondary

Markets

Primary markets

markets in which users of funds (e.g.,

corporations and governments) raise funds by

issuing financial instruments (e.g., stocks and

bonds)

Secondary markets

markets where financial instruments are traded

among investors (e.g., NYSE and Nasdaq)

2

1-5

Primary versus Secondary

Markets

1-6

Primary versus Secondary

Markets

Do secondary markets add value to

society or are they simply a legalized

form of gambling?

How does the existence of secondary markets

affect primary markets?

1-7

Money versus Capital Markets

Money markets

markets that trade debt securities with maturities of one

year or less (e.g., CDs and U.S. Treasury bills)

little or no risk of capital loss, but low return

Capital markets

markets that trade debt (bonds) and equity (stock)

instruments with maturities of more than one year

substantial risk of capital loss, but higher promised return

1-8

Foreign Exchange (FX) Markets

FX markets

trading one currency for another (e.g., dollar for yen)

Spot FX

the immediate exchange of currencies at current

exchange rates

Forward FX

the exchange of currencies in the future on a specific date

and at a pre-specified exchange rate

3

1-9

Derivative Security Markets

Derivative security a financial security whose payoff is linked to (i.e., “derived”

from) another security or commodity,

generally an agreement to exchange a standard quantity

of assets at a set price on a specific date in the future,

the main purpose of the derivatives markets is to transfer

risk between market participants.

1-10

Derivative Security Markets

Selected examples of derivative

securities

Exchange listed derivatives

Many options, futures contracts

Over the counter derivatives

Forward contracts

Forward rate agreements

Swaps

Securitized loans

1-11

Derivatives and the Crisis

1. Mortgage derivatives allowed a larger amount of mortgage

credit to be created in the mid-2000s.

2. Mortgage derivatives spread the risk of mortgages to a

broader base of investors.

3. Change in banking from ‘originate and hold’ loans to

‘originate and sell’ loans.

Decline in underwriting standards on loans

1-12

Derivatives and the Crisis

1. Subprime mortgage losses have been quite large,

reaching over $700 billion.

2. The “Great Recession” was the worst since the “Great

Depression” of the 1930s.

Trillions $ global wealth lost, peak to trough stock prices

fell over 50% in the U.S.

Lingering high unemployment in the U.S.

Sovereign debt levels in developed economies at all-

time highs

4

1-13

Financial Institutions (FIs)

Financial Institutions

institutions through which suppliers channel money to

users of funds

Financial Institutions are distinguished by:

whether they accept insured deposits,

depository versus non-depository financial institutions

whether they receive contractual payments from

customers.

1-14

Asset Size and Number of Selected

U.S. Financial Institutions 2010

INSTITUTION TOTAL ASSETS

(BILL $)

NUMBER OF

FEDERALLY INSURED

INSTITUTIONS

Commercial Banks $12,130 6,622

Savings Associations $ 1,253 1,138

Credit Unions $ 885 7,554

Insurance Companies $ 6,459

Private Pension Funds $ 5,661

Finance Companies $ 1,613

Mutual Funds $ 7,376

Money Market Mutual Funds $ 2,746

Data from September 2010, data sources include Federal Reserve Board, Flow of Funds Accounts, Levels Tables,

FDIC Stats at a Glance and the NCUA website. The mutual funds category excludes money market funds.

1-15

Users of Funds

(corporations)

Suppliers of

Funds

(households)

Financial Claims

(equity and debt

instruments)

Cash

Flow of Funds in a World without FIs

Non-Intermediated (Direct)

Flows of Funds

Direct Financing

1-16

Users of Funds FIs

(brokers)

FIs

(asset

transformers)

Suppliers of Funds

Financial Claims

(equity and debt securities)

Financial Claims

(deposits and insurance policies)

Cash Cash

Flow of Funds in a World with FIs

Intermediated Flows of Funds

Intermediated Financing

5

1-17

Depository versus Non-Depository FIs

Depository institutions:

commercial banks, savings associations, savings banks,

credit unions

Non-depository institutions

Contractual:

insurance companies, pension funds,

Non-contractual:

securities firms and investment banks, mutual funds.

1-18

FIs Benefit Suppliers of Funds

Reduce monitoring costs

Increase liquidity and lower price risk

Reduce transaction costs

Provide maturity intermediation

Provide denomination intermediation

1-19

FIs Benefit the Overall Economy

Conduit through which Federal Reserve

conducts monetary policy

Provides efficient credit allocation

Provide for intergenerational wealth

transfers

Provide payment services

1-20

Risks Faced by Financial

Institutions

Credit

Foreign exchange

Country or

sovereign

Interest rate

Market

Off-balance-sheet

Liquidity

Technology

Operational

Insolvency

6

1-21

Regulation of Financial

Institutions

FIs are heavily regulated to protect society at

large from market failures

Regulations impose a burden on FIs and before

the financial crisis, recent U.S. regulatory

changes were deregulatory in nature

Regulators attempt to maximize social welfare

while minimizing the burden imposed by

regulation

1-22

Globalization of Financial Markets

and Institutions

The pool of savings from foreign investors is

increasing and investors look to diversify globally now

more than ever before,

Information on foreign markets and investments is

becoming readily accessible and deregulation across

the globe is allowing even greater access,

International mutual funds allow diversified foreign

investment with low transactions costs,

Global capital flows are larger than ever.

1-23

FIs and the Crisis

Timeline of events

Home prices decline in late 2006 and early 2007

Delinquencies on subprime mortgages increase

Huge losses on mortgage-backed securities (MBS) announced by institutions

Bear Stearns fails and is bought out by J.P. Morgan Chase for $2 a share (deal had government backing).

1-24

FIs and the Crisis

Timeline of events

September 2008, the government seizes government-

sponsored mortgage agencies Fannie Mae and Freddie

Mac

The two had $9 billion in losses in the second half 2007

Now run by Federal Housing Finance Agency (FHFA)

September 2008, Lehman Brothers files for

bankruptcy; Dow drops 500 points

7

1-25

FIs and the Crisis

1-26

FIs and the Crisis

1-27

Government Rescue Plan

1-28

Government Rescue Plan

8

1-29

Government Rescue Plan

Determinants of

Interest Rates

1-31

Interest Rate Fundamentals

Nominal interest rates: the interest rates

actually observed in financial markets

Used to determine fair present value and prices of

securities

Two types of components

Opportunity cost

Adjustments for individual security characteristics

1-32

Real Interest Rates

Additional purchasing power

required to forego current

consumption What causes differences in nominal and real interest

rates?

If you wish to earn a 3% real return and prices are

expected to increase by 2%, what rate must you charge?

Irving Fisher first postulated that interest rates contain a

premium for expected inflation.

9

1-33

Loanable Funds Theory

Loanable funds theory explains interest rates

and interest rate movements

Views level of interest rates in financial markets

as a result of the supply and demand for

loanable funds

Domestic and foreign households, businesses,

and governments all supply and demand

loanable funds

1-34

Supply and Demand of Loanable

Funds

Interest

Rate

Quantity of Loanable Funds

Supplied and Demanded

Demand Supply

1-35

Determinants of Household

Savings

1. Interest rates and tax policy

2. Income and wealth: the greater the wealth or

income, the greater the amount saved,

3. Attitudes about saving versus borrowing,

4. Credit availability, the greater the amount of

easily obtainable consumer credit the lower the

need to save,

5. Job security and belief in soundness of

entitlements,

1-36

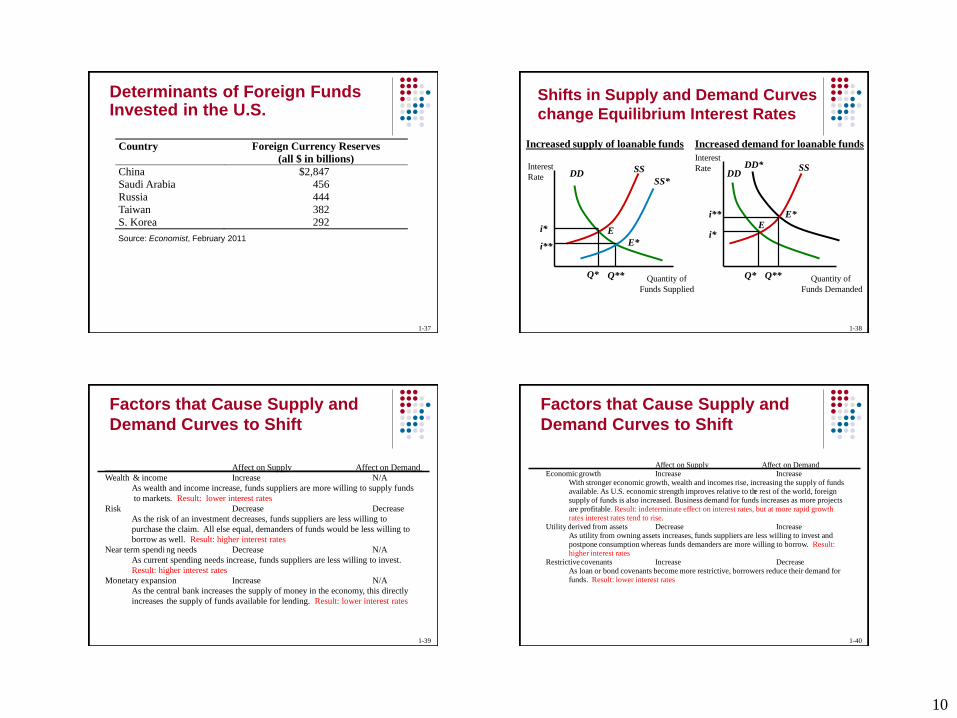

Determinants of Foreign Funds Invested in the U.S.

1. Relative interest rates and returns on global

investments

2. Expected exchange rate changes

3. Safe haven status of U.S. investments

4. Foreign central bank investments in the U.S.

10

1-37

Determinants of Foreign Funds Invested in the U.S.

Source: Economist, February 2011

Country Foreign Currency Reserves

(all $ in billions)

China $2,847

Saudi Arabia 456

Russia 444

Taiwan 382

S. Korea 292

1-38

Shifts in Supply and Demand Curves

change Equilibrium Interest Rates

Increased supply of loanable funds

Quantity of

Funds Supplied

Interest

Rate DD SS

SS*

E

E*

Q*

i*

Q**

i**

Increased demand for loanable funds

Quantity of

Funds Demanded

DD DD* SS

E E*

i*

i**

Q* Q**

Interest

Rate

1-39

Factors that Cause Supply and

Demand Curves to Shift

Affect on Supply Affect on Demand

Wealth & income Increase N/A As wealth and income increase, funds suppliers are more willing to supply funds to markets. Result: lower interest rates

Risk D ecrease Decrease As the risk of an investment decreases, funds suppliers are less willing to purchase the claim. All else equal, demanders of funds would be less willing to borrow as well. Result: higher interest rates

Near term spendi ng needs Decrease N/A As current spending needs increase, funds suppliers are less willing to invest. Result: higher interest rates

Monetary expansion I ncrease N/A

As the central bank increases the supply of money in the economy, this directly increases the supply of funds available for lending. Result: lower interest rates

1-40

Factors that Cause Supply and

Demand Curves to Shift

Affect on Supply Affect on Demand Economic growth Increase Increase

With stronger economic growth, wealth and incomes rise, increasing the supply of funds available. As U.S. economic strength improves relative to th e rest of the world, foreign supply of funds is also increased. Business demand for funds increases as more projects are profitable. Result: indeterminate effect on interest rates, but at more rapid growth rates interest rates tend to rise.

Utility derive d from assets Decrease Increase As utility from owning assets increases, funds suppliers are less willing to invest and postpone consumption whereas funds demanders are more willing to borrow. Result: higher interest rates

Restrictive covenants Increase Decreas e As loan or bond covenants become more restrictive, borrowers reduce their demand for funds. Result: lower interest rates

11

1-41

Factors that Cause Supply and

Demand Curves to Shift

Affect on Supply Affect on Demand Tax Increase Decrease Increase

Taxes on interest and capital gains reduce the returns to savers and the incentive to save. The tax deductibility of interest paid on debt increases borrowing demand. Result: Higher interest rates

Currency Appreciation Increase N/A Foreign suppliers of funds would earn a higher rate of return if the currency appreciates and a lower rate of return measured in their own currency if the dollar depreciates. Foreign central banks often buy U.S. Treasury securities as part of their attempts to prevent their currency from appreciating against the dollar. Result: Lower interest rates

Expected inflation Decrease Increase An increase in expected infl ation implies that suppliers will be repaid with dollars that will have less purchasing power than originally anticipated. Suppliers lose purchasing power and borrowers gain more than originally anticipated. This implies that supply will be reduced and d emand increased. Result: Higher interest rates

1-42

Determinants of Interest Rates

for Individual Securities

ij* = f(IP, RIR, DRPj, LRPj, SCPj, MPj)

Inflation (IP)

IP = [(CPIt+1) – (CPIt)]/(CPIt) x (100/1)

Real Interest Rate (RIR) and the Fisher

effect

RIR = i – Expected (IP)

1-43

Determinants of Interest Rates

for Individual Securities (cont’d)

Default Risk Premium (DRP)

DRPj = ijt – iTt

ijt = interest rate on security j at time t

iTt = interest rate on similar maturity U.S. Treasury

security at time t

Liquidity Risk (LRP)

Special Provisions (SCP)

Term to Maturity (MP)

1-44

Term Structure of Interest Rates:

the Yield Curve

Yield to

Maturity

Time to Maturity

(a)

(b)

(c)

(a) Upward sloping

(b) Inverted or downward

sloping

(c) Flat

12

1-45

Unbiased Expectations Theory

Long-term interest rates are geometric averages

of current and expected future short-term

interest rates

1RN = actual N-period rate today

N = term to maturity, N = 1, 2, …, 4, …

1R1 = actual current one-year rate today

E(ir1) = expected one-year rates for years, i = 1 to N

1))](1))...((1)(1[( /1

112111 N

NNrErERR

1-46

Liquidity Premium Theory

Long-term interest rates are geometric averages

of current and expected future short-term

interest rates plus liquidity risk premiums that

increase with maturity

Lt = liquidity premium for period t

L2 < L3 < …<LN

1)])(1)...()(1)(1[( /1

1212111 N

NNNLrELrERR

1-47

Market Segmentation Theory

Individual investors and FIs have specific

maturity preferences

Interest rates are determined by distinct supply

and demand conditions within many maturity

segments

Investors and borrowers deviate from their

preferred maturity segment only when

adequately compensated to do so

1-48

Implied Forward Rates

A forward rate (f) is an expected rate on a short-

term security that is to be originated at some

point in the future

The one-year forward rate for any year N in the

future is:

1])1/()1[( 1

1111

N

N

N

NNRRf

13

1-49

Time Value of Money and Interest

Rates

The time value of money is based on the

notion that a dollar received today is

worth more than a dollar received at some

future date

Simple interest: interest earned on an

investment is not reinvested

Compound interest: interest earned on an

investment is reinvested

1-50

Present Value of a Lump Sum

Discount future payments using current interest

rates to find the present value (PV)

PV = FVt[1/(1 + r)]t = FVt(PVIFr,t)

PV = present value of cash flow

FVt = future value of cash flow (lump sum) received in t

periods

r = interest rate per period

t = number of years in investment horizon

PVIFr,t = present value interest factor of a lump sum

1-51

Future Value of a Lump Sum

The future value (FV) of a lump sum

received at the beginning of an

investment horizon

FVt = PV (1 + r)t = PV(FVIFr,t)

FVIFr,t = future value interest factor of a lump sum

1-52

Relation between Interest Rates

and Present and Future Values

Present

Value

(PV)

Interest Rate

Future

Value

(FV)

Interest Rate

14

1-53

Present Value of an Annuity

The present value of a finite series of equal

cash flows received on the last day of equal

intervals throughout the investment horizon

PMT = periodic annuity payment

PVIFAr,t = present value interest factor of an annuity

i

iPMTrPMTPV

tt

j

j )1(1)]1/(1[

1

1-54

Future Value of an Annuity

The future value of a finite series of equal cash

flows received on the last day of equal intervals

throughout the investment horizon

FVIFAr,t = future value interest factor of an annuity

i

iPMTrPMTFV

tt

j

jt

1)1()1(

1

0

1-55

Effective Annual Return

Effective or equivalent annual return

(EAR) is the return earned or paid over a

12-month period taking compounding

into account

EAR = (1 + rper period)c – 1 c = the number of compounding periods per year

1-56

Financial Calculators

Setting up a financial calculator Number of digits shown after decimal point

Number of compounding periods per year

Key inputs/outputs (solve for one of five) N = number of compounding periods

I/Y = annual interest rate

PV = present value (i.e., current price)

PMT = a constant payment every period

FV = future value (i.e., future price)