Embed Size (px)

Citation preview

University of Arkansas, FayettevilleScholarWorks@UARK

Research Reports and Research Bulletins Arkansas Agricultural Experiment Station

1-1-1998

Marketing Practices of Arkansas Beef CattleProducersMichael P. PoppUniversity of Arkansas, Fayetteville

Lucas D. ParschUniversity of Arkansas, Fayetteville

Follow this and additional works at: https://scholarworks.uark.edu/aaesrb

Part of the Agribusiness Commons, Agricultural Economics Commons, and the Animal StudiesCommons

This Bulletin is brought to you for free and open access by the Arkansas Agricultural Experiment Station at ScholarWorks@UARK. It has beenaccepted for inclusion in Research Reports and Research Bulletins by an authorized administrator of ScholarWorks@UARK. For more information,please contact [email protected], [email protected].

Recommended CitationPopp, Michael P. and Parsch, Lucas D., "Marketing Practices of Arkansas Beef Cattle Producers" (1998). Research Reports and ResearchBulletins. 39.https://scholarworks.uark.edu/aaesrb/39

ARKANSAS AGRICULTURAL EXPERIMENT STATIONDivision of Agriculture University of Arkansas

January 1998 Research Bulletin 957

Marketing Practicesof Arkansas

Beef Cattle Producers

Michael P. Poppand Lucas D. Parsch

ARKANSAS EXPERIMENT STATION RESEARCH BULLETIN 957

2

Marketing Practicesof Arkansas Beef Cattle Producers

Michael P. Popp Lucas D. ParschAsst. Professor Assoc. Professor

Dept. of Agricultural Economics Dept. of Agricultural Economicsand Agribusiness and Agribusiness

University of Arkansas1 University of Arkansas

1Now at the University of Manitoba, Department of Agricultural Economics and Farm Management,Faculty of Agricultural and Food Sciences, Winnipeg, Manitoba, Canada.

Arkansas Agricultural Experiment StationFayetteville, Arkansas 72701

MARKETING PRACTICES OF ARKANSAS BEEF CATTLE PRODUCERS

3

ABSTRACT

This report contains information from a 1996 survey on marketing prac-tices of Arkansas beef cattle producers. While several studies have been com-pleted on the profitability of retained ownership of beef cattle, few data areavailable on what marketing techniques and decision criteria cow-calf andstocker operations use to market their cattle. This report shows that there aresome differences in opinions on marketing issues such as pooled cattle salesand retained ownership across cow-calf and stocker operations. Further, theseoperations use different sources of information to make marketing decisions.The results of this study can be particularly helpful in providing the needed datafor studying the potential economic impact of feeding weaned calves to heavierweights in Arkansas as a value-added marketing alternative to selling calves atweaning.

Key words: retained ownership, pooled cattle sales, direct marketing, opinionsurvey.

Editing and cover design: Nancy G. Wyatt

Agricultural Experiment Station, University of Arkansas Division of Agriculture, Fayetteville. MiloJ. Shult, Vice President for Agriculture and Director: Charles J. Scifres, Associate Vice Presidentfor Agriculture. SB1.2M198.

The Arkansas Agricultural Experiment Station follows a nondiscriminatory policy in programs andemployment.ISSN:0097-3491 CODEN:AKABA7

ARKANSAS EXPERIMENT STATION RESEARCH BULLETIN 957

4

CONTENTS

INTRODUCTION .................................................................................................... 5

SAMPLING PROCEDURE AND SURVEY DESIGN ........................................... 6

OPERATOR OPINIONS ON FEEDING WEANED CALVESTO HEAVIER WEIGHTS................................................................................. 7Opinions on Problems of On-farm Feeding of Weaned Calves ......................... 8Opinions on Problems of Having Weaned Calves Custom Fed ...................... 10Opinions on Benefits of On-farm and Custom Feeding of Weaned Calves .... 13Ranking of Opinions on Problems and Benefits of Feeding Weaned Calves .. 13

TOOLS USED FOR FORECASTING ................................................................... 15

DECISION CRITERIA FOR SELL VS. HOLD AND FEED DECISION ............ 17

USE OF MARKETING METHODS ..................................................................... 19Marketing Methods Used ................................................................................ 19Volume of Trade Reported for Each Marketing Method ................................. 21

FREQUENCY OF CONSULTING PRICES INFORMATION ............................. 25

OPERATOR OPINIONS ON POOLING CATTLE FOR SALE ........................... 28Opinions on Benefits of Pooling Cattle for Sale ............................................. 28Opinions on Concerns About Pooling Cattle for Sale ..................................... 30Ranking of Opinions on Benefits of and Concerns about Pooling Cattle Sales32

SUMMARY AND CONCLUDING COMMENTS ............................................... 33

LITERATURE CITED ........................................................................................... 35

APPENDIX A: SURVEY INSTRUMENT ............................................................ 36

MARKETING PRACTICES OF ARKANSAS BEEF CATTLE PRODUCERS

5

MARKETING PRACTICESOF ARKANSAS BEEF CATTLE PRODUCERS

Michael P. Popp and Lucas D. Parsch

INTRODUCTION

survey was conducted in 1996 in order to obtain information regardinglivestock production and marketing practices of Arkansas cattle pro-ducers. This report highlights current marketing practices. Three types

of operations were surveyed: 1) cow/calf operations that sell calves at weaning;2) cow/calf operations that feed weaned calves to a heavier weight; and 3)stocker or backgrounding operations that prepare weaned calves for feedlotplacement. These enterprises operate at different processing stages of the beefcattle marketing channel and exhibit different degrees of specialization in pro-duction. Operations that have a single business focus, either cow/calf orstockering, are more specialized than cow/calf operations that also feed weanedcalves. Because of more diversified production methods, the latter operationtype may have more marketing options with additional freedom over the timingof sales. For example, weaned calves can be sold immediately or fed to heavierweights. The questionnaire was designed to address what similarities or differ-ences exist across these different operations.

In particular, information regarding producers� attitudes about benefits andproblems associated with retained ownership, pooling of cattle sales and value-added feeding alternatives was collected. The survey also assessed what infor-mation producers use to make marketing decisions and which marketing meth-ods they used.

There are a number of studies that compare returns to selling calves atweaning versus returns obtained from continuing to feed weaned calves to

A

1This paper is part of a set of reports funded by the University of Arkansas Agricultural ExperimentStation, Research Initiation Program. The authors are thankful for the help of Michel Pardue, DianaDanforth and other support staff for helping with the data entry and questionnaire design.

ARKANSAS EXPERIMENT STATION RESEARCH BULLETIN 957

6

heavier weights either on farm or on a custom basis (Watt et al., 1987; Johnsonet al., 1989; Gage, 1993 and 1994; Feuz and Wagner, 1996). Results usuallysupport the feeding of calves to heavier weights as a profitable alternative toselling calves at weaning. These studies often make various assumptions aboutthe timing of sales and what marketing techniques were used. To providefurther insight on these latter issues, this study was conducted to show theextent of retained ownership programs such as stockering or custom feeding inArkansas in 1996 and the marketing techniques and decision criteria that wereused.

This information is valuable because 1) it updates statistics on livestockmarketing practices in Arkansas; 2) it can be used to show how producers�attitudes on marketing issues differ at various stages in the beef cattle marketingchannel; 3) it shows that producers at different levels in the marketing channelseek alternative types of information and; 4) it provides the background forfurther study.

SAMPLING PROCEDURE AND SURVEY DESIGN

A mail survey (Salant and Dillman, 1994) was chosen in order to allowrespondents to consult records and to respond to a lengthy and difficult set ofquestions. The questionnaire (see Appendix A) was mailed to mid- and large-sized beef cattle operations in Arkansas because these operations would belarge enough and sufficiently specialized to answer questions of interest. Inaddition, these operations handle a majority of the cattle in Arkansas (see Table1). Table 1 describes the size distribution of beef cattle operations in Arkansas

Table 1. Number of beef cattle operations by size group, 1996.Numberof Farms

1,4412,6006,7763,8872,1201,060

17226

2018,102

% of All BeefCattle Farms

8.014.437.421.511.75.91.00.1

0.1100.0

Est. No. ofCattle2

7,20537,700

233,772289,582316,940370,470128,91432,487

n/a3

1,417,070

% of Est. TotalNo. of Cattle

0.52.7

16.520.422.426.19.12.3

n/a3

100.0

Size Group1

1 - 910 - 1920 - 4950 - 99

100 - 199200 - 499500 - 999

1000 - 14991500 - 9999Total Farms

Notes: Percentages may not add due to rounding. (Source: James Ewing of Arkansas Agricultural StatisticsService who coordinated the mail survey and sampling procedure. Arkansas Agricultural Statistics Service,1996)

1 Cattle includes cows, heifers that have calved and animals over 500 lb.2 The estimated number of cattle per size group is the product of the number of farms and the mid-point oraverage number of cattle per farm per size group. For example, the estimated number of cattle in the ‘1-9’head size group is 1,441 farms * [(1+9)/2] average head of cattle / farm with 1 - 9 head = 7,205 head ofcattle.

3 Not included as the average or mid-point because this category might be misleading.

MARKETING PRACTICES OF ARKANSAS BEEF CATTLE PRODUCERS

7

for 1996. The subsample of mid- to large-sized beef producers with more than50 and less than 1,000 cattle contained 7,239 producers or approximately 40%of the total number of beef cattle operations in Arkansas. Further, this subsampleof producers represents nearly 80% of beef cattle in Arkansas. The first mailingwas sent out 6 May 1996 with 2,500 addresses across the entire state ofArkansas picked at random by Arkansas Agricultural Statistics Service. On 20May, two weeks after the initial mailing, a follow-up survey was sent out. In all,1,094 surveys were returned with 1,057 usable observations, which amounts toa 42.3% mail return rate.

The survey was organized to ask specific questions of producers by theirtype of operation. The three types of operations were classified into the follow-ing categories:

1) Cow/calf - operations that sell calves at weaning except for replacementheifers. The sample contained 851 (80.5%) observations in this category;

2) Feeder - operations that are involved in either purchasing weanedcalves and feeding to heavier weights or custom feeding them to getweaned calves ready for feedlot placement. These operations maygraze animals (stockering) and/or feed them in a drylot environment(backgrounding). The sample contained 34 (3.2%) observations in thiscategory;

3) Mixed - operations that have a cow/calf and a feeding component intheir business. The sample involved 172 (16.3%) observations in thiscategory.

The results of the survey are presented to summarize responses and todifferentiate among the above three types of operations. One section deals withresults to questions specific to �Cow/calf� operations that sell weaned calves and�Mixed� cow/calf operations that also feed their calves. In this section, the focusof the questions was on attitudes concerning retained ownership and feeding toheavier feeder cattle weights. The remainder of the report analyzes responsesfrom all three types of operations. The emphasis was on tools used for forecast-ing prices, on opinions regarding pooled cattle sales, how sell vs. hold and feeddecisions are made, what marketing methods are employed, how frequentlyprices are compared on cattle characteristics and which sources of informationwere most important.

OPERATOR OPINIONS ON FEEDING WEANED CALVESTO HEAVIER WEIGHTS

Regardless of their experience with feeding weaned calves, opinions re-garding problems and benefits of on-farm feeding and custom feeding of weanedcalves were ascertained from �Cow/calf� and �Mixed� operations (see AppendixA, Question 8). �Feeder� operations were not asked to answer these questionsbecause a large majority of the problems and benefits did not apply to them.

ARKANSAS EXPERIMENT STATION RESEARCH BULLETIN 957

8

The questions were formatted so that a respondent could register one of fivelevels of agreement with each statement (strongly agree, agree, neutral, dis-agree or strongly disagree).

The first set of questions was designed to determine whether 1) price risk;2) lack of facilities; 3) cost of financing; or 4) lack of profitability were perceivedto be problems affecting the on-farm feeding of calves.

A subsequent set of questions was posed to establish whether 5) availabilityof custom feeders (location); 6) lack of trust; 7) difficulty in establishing trust; or8) knowledge of custom feeding as an option were perceived to be problemsrelated to the custom feeding of calves. Because the large majority (90%) of therespondents had never been involved with custom feeding (Popp and Parsch,1997), responses to these questions should be interpreted primarily as opinionsgrounded in minimal experience.

A final set of questions attempted to evaluate how the use of animalperformance data was perceived to be beneficial for both on-farm and customfeeding of weaned calves. Responses to these questions are summarized inTables 2 through 4. Each table presents the percentage breakdown of answersfor �Cow/calf� and �Mixed� operations on each statement.

Opinions on Problems of On-farm Feeding of Weaned CalvesTable 2 shows the breakdown of responses to problems �Cow/calf� and

�Mixed� operations may experience with on-farm feeding of weaned calves. Forexample, answers to the statement �The problem with feeding calves on myfarm is that, prices of feeder cattle change too much (too risky)� are reported inthe first row of the table. Numbers of respondents are included in the second-to-last column. Finally, the null hypothesis, that there is no difference in thedistribution of answers across operation type, is tested with the χ2-statistic andassociated probability1. High χ2- values and probabilities below 0.05, shown inthe last column, indicate that the distribution of answers is different acrossoperation type with 95% confidence. For the above example, the χ2- value andprobability mean that �Cow/calf� and �Mixed� operations had different percep-tions on whether feeder cattle price risk is problematic for feeding weanedcalves. This is illustrated in Fig. 1 graphically. The distribution of answers for�Cow/calf� operations is more heavily skewed in favor of the statement thatfeeder cattle price risk is a problem with on-farm feeding of weaned calves. Inother words, �Cow/calf� operations that do not feed weaned calves viewed thegrazing or feeding of weaned calves as more risky than �Mixed� operations.

Nearly 60% of the �Cow/calf� operations indicated that facilities to feedweaned calves were a problem on their farm while only 20% didn�t think that

1All statistical tests were run using Windows version 6.12 of SAS. To test for statistically significantdifferences in the distribution of answers across operation type, χ2 tests were used (Huntsberger andBillingsley, 1987).

MARKETING PRACTICES OF ARKANSAS BEEF CATTLE PRODUCERS

9

Tab

le 2

. Res

pons

es o

f ‘C

ow/c

alf’

and

‘Mix

ed’ o

pera

tions

to q

uest

ions

reg

ardi

ng p

robl

ems

with

on

farm

feed

ing

of w

eane

d ca

lves

.T

he p

robl

em w

ith f

eedi

ngO

pera

tion

Str

ongl

yS

tron

gly

No.

of

χ2 -st

atis

ticca

lves

on

my

farm

is t

hat,

Typ

eA

gree

Agr

eeN

eutr

alD

isag

ree

Dis

agre

eR

espo

nden

ts(P

roba

bilit

y)--

----

----

----

----

----

----

---%

----

----

----

----

----

----

----

--P

rices

of

feed

er c

attle

Cow

/cal

f24

.336

.031

.18.

10.

574

290

.196

chan

ge t

oo m

uch

(too

ris

ky)

Mix

ed6.

623

.537

.428

.34.

216

6(0

.001

)A

ll21

.033

.732

.311

.81.

290

81

I do

n’t

have

the

fac

ilitie

sC

ow/c

alf

19.4

39.0

20.8

16.5

4.4

754

150.

942

to fe

ed w

eane

d ca

lves

Mix

ed3.

113

.615

.450

.617

.316

2(0

.001

)A

ll16

.534

.519

.922

.56.

791

61

Bor

row

ing

mon

ey t

o fin

ance

Cow

/cal

f38

.835

.320

.74.

81.

072

976

.925

the

feed

ing

is t

oo c

ostly

Mix

ed13

.832

.729

.620

.13.

815

9(0

.001

)A

ll34

.334

.821

.97.

61.

588

81

Fee

ding

is n

ot p

rofit

able

Cow

/cal

f24

.430

.031

.212

.32.

175

712

9.46

8M

ixed

5.5

16.4

25.5

41.8

10.9

165

(0.0

01)

All

21.0

27.6

30.2

17.6

3.7

9221

1R

espo

nse

rate

s va

ried

from

86.

8% to

90.

1% w

hich

tran

slat

e to

135

to 1

01 m

issi

ng o

bser

vatio

ns, r

espe

ctiv

ely.

ARKANSAS EXPERIMENT STATION RESEARCH BULLETIN 957

10

facilities were a problem. While the question doesn�t really apply to �Mixed�operations, as they feed weaned calves with their facilities, one-sixth of theseoperations still had problems with facilities.

Both types of operations expressed concerns with the cost of financing thefeeding of weaned calves. Results showed that �Mixed� operations that hadexperience with feeding weaned calves perceived financing as less of a problemthan operations that did not feed calves. It may be that �Mixed� operations havebetter ties to financial institutions given their experience and thus receive lowerinterest rates, which would lead to a lessened perception of financing as aproblem.

Finally, the lack of profitability was perceived as a problem by more thanhalf of the �Cow/calf� operations but only by approximately one-fifth of the�Mixed� operations. This problem was also rephrased as a benefit in a latersection (see Table 4). Results were consistent across both statements. Theseresults indicate that there may be a need to educate �Cow/calf� operationsregarding the profitability of feeding weaned calves to heavier weights.

Opinions on Problems of Having Weaned Calves Custom FedTable 3 summarizes the responses of �Cow/calf� and �Mixed� operations on

problems associated with having their weaned calves custom fed. The first rowin the table summarizes the location problem. Since there were very few opera-tions that custom fed weaned calves for cow/calf operations, it may be thattransportation cost or location of custom feeders was perceived as a problem1.

Cow/calf Mixed

Prices of feeder cattle change too much (too risky)Strongly Agree Agree Neutral D isagree Strongly Disagree

0

10

20

30

40

Fig. 1. Opinion regarding feeder cattle price risk, cow/calf vs. mixed operations.

1Popp and Parsch (1997) showed that only 1.6% of the cattle fed by �Feeder� and �Mixed� enterprisesis done on a custom basis for �Cow/calf� operations.

MARKETING PRACTICES OF ARKANSAS BEEF CATTLE PRODUCERS

11

Tab

le 3

. Res

pons

es o

f ‘C

ow/c

alf’

and

‘Mix

ed’ o

pera

tions

to q

uest

ions

reg

ardi

ng p

robl

ems

with

hav

ing

wea

ned

calv

es c

usto

m fe

d.T

he p

robl

em w

ith h

avin

g ca

lves

Ope

ratio

nS

tron

gly

Str

ongl

yN

o. o

fχ2 -

stat

istic

fed

with

a c

usto

m f

eede

r is

tha

t,T

ype

Agr

eeA

gree

Neu

tral

Dis

agre

eD

isag

ree

Res

pond

ents

(Pro

babi

lity)

----

----

----

----

----

----

----

-%--

----

----

----

----

----

----

----

No

cust

om f

eede

rs a

re n

earb

yC

ow/c

alf

31.9

42.2

21.7

3.2

1.1

728

29.8

86M

ixed

21.9

51.9

13.8

11.3

1.3

160

(0.0

01)

All

30.1

43.9

20.3

4.6

1.1

8881

I do

n’t

trus

t cu

stom

fee

ders

Cow

/cal

f10

.517

.661

.88.

51.

769

819

.583

Mix

ed5.

820

.551

.918

.03.

915

6(0

.001

)A

ll9.

618

.260

.010

.22.

185

41

It is

too

har

d to

est

ablis

h tr

ust

Cow

/cal

f10

.518

.461

.67.

91.

769

725

.468

with

cus

tom

fee

ders

Mix

ed5.

725

.547

.818

.52.

615

7(0

.001

)A

ll9.

619

.759

.09.

81.

985

41

I ha

ve n

ot c

onsi

dere

d th

is o

ptio

nC

ow/c

alf

23.5

34.2

31.3

9.9

1.0

766

49.0

09M

ixed

15.3

22.9

33.1

21.0

7.6

157

(0.0

01)

All

22.1

32.3

31.6

11.8

2.2

9231

1R

espo

nse

rate

s va

ried

from

83.

5% to

90.

2% w

hich

tran

slat

e to

169

to 1

00 m

issi

ng o

bser

vatio

ns, r

espe

ctiv

ely.

ARKANSAS EXPERIMENT STATION RESEARCH BULLETIN 957

12

Tab

le 4

. Res

pons

es o

f ‘C

ow/c

alf’

and

‘Mix

ed’ o

pera

tions

to q

uest

ions

reg

ardi

ng b

enef

itsof

on-

farm

and

cus

tom

feed

ing

of w

eane

d ca

lves

.T

he b

enef

it of

fee

ding

cal

ves

Ope

ratio

nS

tron

gly

Str

ongl

yN

o. o

fχ2 -

stat

istic

(ow

n or

cus

tom

) is

tha

t,T

ype

Agr

eeA

gree

Neu

tral

Dis

agre

eD

isag

ree

Res

pond

ents

(Pro

babi

lity)

----

----

----

----

----

----

----

-%--

----

----

----

----

----

----

----

I kn

ow h

ow w

ell a

nim

als

perf

orm

Cow

/cal

f13

.341

.939

.54.

60.

772

137

.651

Mix

ed17

.263

.817

.21.

80.

016

3(0

.001

)A

ll14

.045

.935

.44.

10.

688

41

I ca

n ad

just

my

bree

ding

pro

gram

Cow

/cal

f12

.343

.139

.44.

40.

772

019

.840

bette

r, b

ecau

se I

kno

w h

ow w

ell

Mix

ed15

.557

.826

.10.

60.

016

1(0

.001

)an

imal

s pe

rfor

mA

ll12

.945

.737

.03.

80.

688

11

On

aver

age

it is

mor

e pr

ofita

ble

Cow

/cal

f8.

919

.851

.415

.94.

073

198

.879

than

sel

ling

wea

ned

calv

esM

ixed

20.9

47.9

29.5

1.2

0.6

163

(0.0

01)

All

11.1

24.9

47.4

13.2

3.4

8941

1R

espo

nse

rate

s va

ried

from

86.

1% to

87.

4% w

hich

tran

slat

e to

142

to 1

29 m

issi

ng o

bser

vatio

ns, r

espe

ctiv

ely.

MARKETING PRACTICES OF ARKANSAS BEEF CATTLE PRODUCERS

13

�Cow/calf� operations expressed stronger concern about custom feeding thanoperations that feed calves. This seems rational because operations that feedcalves themselves would be less dependent on transportation costs to customfeeders than operations that do not have this option.

There were two statements on the level and establishment of trust withcustom feeders. The first was stronger in the sense that the respondents wereasked directly whether they trusted custom feeders. The second question askedabout the difficulty of establishing trust with a custom feeder. The results werenearly identical for the two statements. In general, both types of operationsagreed that trust or the difficulty in establishing trust was of concern. �Cow/calf�operations were more neutral on this question than �Mixed� operations.

The final statement attempted to ascertain the level of knowledge about theavailability of custom feeding. Nearly 60% of �Cow/calf� operations had notconsidered having their calves custom fed. This compares to only 38.2% of�Mixed� operations. On the basis of these results, it appears that custom feedersare not actively pursuing �Cow/calf� operations as customers in this area ofbusiness. It may be that larger quantities of cattle are required for customfeeders to pursue a client. This topic is also discussed below.

Opinions on Benefits of On-farm and Custom Feeding of WeanedCalves

Table 4 summarizes the benefits of on-farm feeding and custom feeding ofweaned calves. There were two statements that related to the benefits of knowl-edge and use of animal performance data. The first statement asked whetherknowledge of animal performance data was a benefit. The second statementwent further and asked whether this knowledge of animal performance helpedwith breeding decisions and was therefore regarded as a benefit of feedingweaned calves. Responses to both statements were similar and indicated that�Mixed� operations viewed access to animal performance data as a more impor-tant benefit than did �Cow/calf� operations.

Ranking of Opinions on Problems and Benefits of Feeding WeanedCalves

The previous sections on problems and benefits of feeding weaned calvescan be summarized by ranking the importance of the different issues. Rankingswere assigned on the basis of the combined percentage of respondents thateither �strongly agreed� or �agreed� with a statement. The statement with thehighest percentage was given the highest ranking, indicating that most respon-dents in the grouping agreed with the statement identifying the problem orbenefit.

Table 5 shows the percentages of respondents and rankings by operationtype as well as overall percentages and rankings. The rankings were very similaracross operation types. The cost of financing was perceived as the number-one

ARKANSAS EXPERIMENT STATION RESEARCH BULLETIN 957

14

on-farm problem not only by the operations that fed cattle (�Mixed�) but also byoperations that did not (�Cow/calf�).

An example of typical interest costs demonstrates how important financingcharges can be. For example, assuming a 40% equity position in the cattle,total interest charges could range from $5.16 to $18.07/head using annualinterest rates of 4% to 14%, respectively (see Table 6, row ( F )). These aresignificant changes in cost given the expected average returns to feeding calvesshown in Row ( G ) of Table 6.

Price risk was identified as the number-two issue (Table 5), indicating thatimproved price risk management is a strong priority for producers. The avail-ability of feeding facilities ranked third in importance by �Cow/calf� operations.The lack of profitability was of least concern to �Cow/calf� producers, mostlikely due to the fact that they were not feeding calves. The combination of highinterest cost and a perception of high price risk appears to be the reason for areluctance to invest in feeding facilities by �Cow/calf� operations.

Problems with custom feeding (Table 5) were mostly associated with a lackof availability of custom feeders and knowledge of this option. Another interest-ing result was that the difficulty in establishing trust with custom feeders wasranked as more of a problem than trusting custom feeders outright. Again, thismay be related to the lack of availability of this feeding option in Arkansas.

Finally, the major advantage or benefit to feeding calves was knowinganimal performance. The primary reason for �Cow/calf� operations to rank thisbenefit highly may have been that they can adjust their breeding program

Table 5. Rankings of problems and benefits of feeding weaned calvesby ‘Cow/calf’ vs. ‘Mixed’ vs. ‘Cow/calf & Mixed’.

Cow/calf Mixed Cow/calf & Mixed% of % of % of

Statement responses1 Rank responses1 Rank responses1 Rank

Problems with on-farm feeding:Price risk 60.3 2 30.1 2 54.7 2Availability of feeding facilities 58.4 3 16.7 4 51.0 3Financing charges 74.1 1 46.5 1 69.1 1Lack of profitability 54.4 4 21.9 3 48.6 4

Problems with custom feeding:Location 74.1 1 73.8 1 74.0 1Trust 28.1 4 26.3 4 27.8 4Establish trust 28.9 3 31.2 3 29.3 3Knowledge of custom feeding 57.7 2 38.2 2 54.4 2

Benefits of own or custom feeding:Know animal performance data 55.2 2 81.0 1 59.9 1Adjust breeding because of data 55.4 1 73.3 2 58.6 2Profitability 28.7 3 68.8 3 36.0 3

1The combined percentage of respondents that strongly agreed or agreed with the statement outlined in theleft most column.

MARKETING PRACTICES OF ARKANSAS BEEF CATTLE PRODUCERS

15

better. For �Mixed� operations, which also purchase weaned calves for feeding,knowing animal performance data affected not only their breeding decisionsbut also their purchasing decisions. That may be the reason why they did notrank the answers to this question in the same manner as the �Cow/calf� respon-dents. Profitability was again ranked lowest.

Overall these rankings suggest that feeding weaned calves or having weanedcalves custom fed is not very common in Arkansas. The primary reason for thisappears to be an aversion to price risk and/or a lack of low-cost financing. Theprimary motivation for feeding weaned calves was not profitability but insteadaccess to information regarding animal performance.

TOOLS USED FOR FORECASTING

Respondents in all three categories of operations (�Cow/calf�, �Mixed� and�Feeder�) were asked about the source of information or tools they used forforecasting or predicting sale prices at the end of a feeding period (Appendix A,Question 16). The responses to this query are summarized in Table 7 and showrankings according to the highest percentage of respondents who reported thatthey had used a specified tool or information source. A χ2 - statistic wascalculated to see if the distribution of reported usage of the different informa-tion sources was different across the three operation types. Associated probabil-ity values below 0.05 again indicate that the distribution of information usagewas statistically significantly different across operation type.

Auction barn prices were ranked number one by �Cow/calf� and �Mixed�operations and number two by �Feeder� operations. In all cases, over three-quarters of the respondents used auction barn data to forecast prices. In addi-tion, reported use of auction prices was not significantly different across type ofoperation. However, reported use of other tools and sources of information inTable 7 differed by operation type at the 0.05 significance level.

Table 6. Typical interest cost on feeder cattle and feed using different interest rates.( A ) Value of #450 steer calf @ $65.00/cwt: $292.50( B ) Cost of gain -- 300 lb @ $40.00/cwt: $120.00( C ) Amount financed -- 60% of (A) + 50% of (B): $243.00( D ) Number of days financed -- 300 lb @ 1.5 ADG 200( E ) Sale Value of #750 steer calf @ $60.00/cwt: $450.00

Annual Interest Rate: 4% 6% 8% 10% 12% 14%

Interest cost in $/head:Interest on 60% of calf 3.85 5.77 7.69 9.62 11.54 13.46Interest on 50% of feed 1.32 1.97 2.63 3.29 3.95 4.60

Total Interest cost ( F ) 5.16 7.74 10.32 12.90 15.48 18.07Returns per head ( G ) 32.34 29.76 27.18 24.60 22.02 19.43

Notes: Returns per head ( G ) are calculated as ( E ) - ( A ) - ( B ) - ( F ). This information is provided simplyas an example of returns for 1996. Cost of gain includes vet & drug charges, feed, death loss and marketingcosts and excludes returns to land, labor and capital. (Pardue et al., 1997).

ARKANSAS EXPERIMENT STATION RESEARCH BULLETIN 957

16

Tab

le 7

. Pro

port

ion

of o

pera

tors

rep

ortin

g on

the

type

s of

info

rmat

ion

used

to fo

reca

st o

r pr

edic

t sal

e pr

ices

at th

e en

d of

a fe

edin

g pe

riod

by o

pera

tion

type

.T

ype

of I

nfor

mat

ion

Cow

/cal

fM

ixed

Fee

der

All

or T

ool U

sed

%1

Ran

k2%

Ran

k%

Ran

k%

R

ank

χ2 -s

tatis

ticP

roba

bilit

yA

uctio

n ba

rn p

rices

81.6

185

.21

75.0

282

.01

2.33

40.

311

Live

stoc

k re

port

s67

.62

79.3

278

.11

69.9

210

.099

0.00

6M

arke

t tr

ends

37.4

358

.03

68.8

341

.93

34.1

160.

001

Fee

der

cattl

e fu

ture

s30

.84

56.8

475

.02

36.6

461

.646

0.00

1C

ontr

acte

d P

rice

6.4

514

.25

34.4

48.

65

38.8

320.

001

Oth

er6.

06

9.5

615

.65

6.9

66.

569

0.03

7N

otes

: Res

pons

e ra

tes

varie

d fr

om 9

2.5%

to 9

8.3%

acr

oss

oper

atio

n ty

pe.

Non

-res

pons

e to

this

que

stio

n w

as d

efin

ed a

s no

che

ck m

arks

to th

e en

tire

ques

tion.

1%

is th

e pe

rcen

tage

of r

espo

nden

ts w

ho in

dica

ted

that

they

use

this

info

rmat

ion

or to

ol fo

r m

akin

g pr

ice

fore

cast

s.2R

ank

is a

ssig

ned

on th

e ba

sis

of th

e hi

ghes

t per

cent

age

of u

se o

f the

info

rmat

ion

or to

ol.

MARKETING PRACTICES OF ARKANSAS BEEF CATTLE PRODUCERS

17

�Feeder� operations used livestock reports as their number-one source forinformation followed closely by auction barn prices, feeder cattle futures pricesand market trends. Contractual arrangements and other information sourceswere used the least by all respondents. Information from market trends, feedercattle futures markets and contractual arrangements were used the least by�Cow/calf� operations by a considerable margin. This suggests that �Cow/calf�operations largely used livestock reports and auction barn prices as sources ofinformation.

Written comments were solicited in the �Other� category, shown as the lastitem in the list of sources consulted. Respondents included other producers andprofessionals in the livestock industry in this category.

DECISION CRITERIA FOR SELL VS. HOLD AND FEED DECISION

Respondents were asked how frequently they used different decision crite-ria when deciding whether to sell or to continue feeding (Appendix A, Question17). The following four choices were available:

1) Marginal Analysis - comparison of calculated feed costs with sale pricesof animals. This choice entails the calculation of expected profits bylooking at the difference in added revenue versus added feed cost;

2) High/Low Price - sell when prices are high and hold when prices arelow;

3) Age/Weight - sell regardless of price when the cattle are a certain ageor weight;

4) Pasture Condition - feeding restricted to pasture availability;Table 8 summarizes the breakdown of responses on the frequency of use of

the above decision criteria by the different types of operations.The first section of Table 8 shows the frequency of use of the marginal cost

vs. marginal revenue decision rule. �Feeder� operations tended to use this methodthe most, and �Cow/calf� operations reported that they used this method theleast. The reason for this difference might simply be that �Cow/calf� operationstended to hold and feed cattle intended for sale for shorter periods of time than�Mixed� and �Feeder� operations. For this reason, marginal analysis may not beas important to them. �Feeder� operations may also be more flexible withrespect to the timing of purchase and sale decisions as they don�t face breeding,culling and weaning decisions.

The frequency of using the decision rule of selling when prices are high andfeeding or holding cattle when prices are low is shown in the second section ofTable 8. All types of operations appeared to use this decision rule in a similarmanner as the distribution of answers was not statistically significantly differentacross operation types. 90% of all operations reported using this method atleast sometimes.

ARKANSAS EXPERIMENT STATION RESEARCH BULLETIN 957

18

The decision rule according to which operators would sell their calves at acertain age and weight showed a significantly different distribution of answersacross operation types. �Feeder� and �Mixed� operations were the least likely touse the age-weight criterion often. �Mixed� operations showed the most aver-sion to this method of deciding on when to sell vs. keep feeding. It may be that�Mixed� operations are feeding weaned calves in order to gain flexibility in theirmarketing approach�a rigid decision rule, such as selling at a certain weight orage would be the direct opposite.

Finally, the sale decision based on pasture condition was not differentacross operation type. Approximately one-fifth of the operations used it rarely,suggesting that these operations make greater use of the other decision rules,that pasture availability is calculated conservatively at the beginning of thefeeding period or that supplemental feed is used to prevent feed shortage.

Table 9 summarizes the above discussion on the decision criteria used bythe different operation types. �Feeder� operations were most likely to calculateprofits on lots of cattle they processed at the margin as they had the highestaverage response of 2.43 in the first row. �Mixed� operations were least likely tofeed calves according to age and weight but concentrated instead on moreflexible criteria. �Cow/calf� operations differed the least across decision rulesthey used, as shown in the narrow range of average ratings. This may be due to

Table 8. Frequency of use of four alternative decision criteriato sell vs. hold and feed calves by operation type.

Decision Operation No. of χ2-statisticCriteria Type Always Sometimes Rarely respondents (Probability)

-----------------%-----------------Marginal Cow/calf 27.1 40.7 32.3 669 18.522Analysis Feeder 50.0 42.9 7.1 28 (0.001)

Mixed 37.2 41.9 21.0 148All 29.6 41.0 29.5 8451

High/Low Cow/calf 24.9 65.0 10.1 722 2.288Price Feeder 17.9 71.4 10.7 28 (0.683)

Mixed 28.0 64.7 7.3 150All 25.2 65.1 9.7 9001

Age/ Cow/calf 26.3 54.8 18.9 741 24.918Weight Feeder 29.0 41.9 29.0 31 (0.001)

Mixed 15.9 48.4 35.7 157All 24.7 53.3 22.1 9291

Pasture Cow/calf 22.6 61.9 15.5 704 1.369Condition Feeder 19.2 61.5 19.2 26 (0.850)

Mixed 20.8 60.4 18.8 154All 22.2 61.7 16.2 8841

1 Response rates varied from 79.9% to 87.9% which translate to 212 to 128 missing observations, respectively.

MARKETING PRACTICES OF ARKANSAS BEEF CATTLE PRODUCERS

19

breeding, culling and weaning constraints that these operations face more sothan operations that also feed calves or operations that are solely in the busi-ness of feeding calves.

USE OF MARKETING METHODS

Respondents were asked to identify the marketing methods they used tobuy or sell cattle in 1995 by choosing one or more items from a list of eightmarketing alternatives (Appendix A, Question 18). In addition to indicatingwhether or not they had used each method, respondents also noted howfrequently they had used it and the number of cattle they had sold/purchasedvia each marketing alternative. The list of marketing alternatives appears below.

1) Cash - I sold/bought at a sale barn or auction market;2) Direct - stocker - I sold directly to a stocker or backgrounder;3) Direct - feedlot - I sold directly to a feedlot;4) Video - I sold/bought through video auction;5) Futures - I used cattle futures and options;6) Contract - I sold/bought cattle on contract;7) Pooled - I sold cattle together with another producer(s);8) Other - I sold/bought using other methods.

Marketing Methods UsedTable 10 presents rankings of the eight marketing alternatives by operation

type based on the proportion of respondents who used the technique in 1995.The reported χ2-statistic and associated probability indicate whether use of amarketing alternative was significantly different across operation type. A highχ2-value and a probability below 0.05 indicate that answers were differentacross operation type with 95% confidence.

Cash sales were the most common marketing method. Over 90% of all ofthe respondents used sale barns or auction markets to sell or buy cattle in 1995.Because this information records only the proportion of operators who usedeach method, this does not mean that over 90% of cattle traded moved throughauction markets.

Table 9. Decision criteria used for sell vs. hold and feed decision by operation type.Type of Information Cow/calf Mixed Feeder All Operationsor Tool Used Avg.1 Rank2 Avg. Rank Avg. Rank Avg. Rank

Marginal Analysis 1.95 3 2.16 2 2.43 1 2.00 4High/Low Price 2.15 1 2.21 1 2.07 2 2.16 1Age/Weight 2.07 2 1.80 4 2.00 3 2.03 3Pasture Condition 2.07 2 2.02 3 2.00 3 2.06 21 Avg. is the average response of respondents. 1 = Rarely, 2 = Sometimes, 3 = Always.2 Rank is assigned on the basis of the highest average response for the decision criteria category.

ARKANSAS EXPERIMENT STATION RESEARCH BULLETIN 957

20

Tab

le 1

0. P

ropo

rtio

n of

ope

rato

rs r

epor

ting

use

of e

ight

alte

rnai

tve

mar

ketin

g m

etho

ds b

y op

erat

ion

type

.T

ype

of M

arke

ting

Cow

/cal

fM

ixed

Fee

der

All

Met

hod

Use

d%

1R

ank2

%R

ank

% R

ank

%

Ran

k χ

2 -sta

tistic

Pro

babi

lity

Cas

h93

.81

93.9

187

.91

93.7

11.

914

0.38

4D

irect

- s

tock

er8.

02

8.5

315

.24

8.3

22.

114

0.34

7D

irect

- f

eedl

ot0.

66

7.3

427

.32

2.6

410

6.95

10.

001

Vid

eo0.

66

3.0

712

.15

1.4

734

.520

0.00

1F

utur

es1.

25

4.2

59.

16

2.0

515

.237

0.00

1C

ontr

act

0.6

64.

25

15.2

41.

76

48.1

710.

001

Poo

led

2.5

43.

66

0.0

72.

64

1.64

70.

439

Oth

er3

4.7

39.

72

18.2

36.

03

15.2

500.

001

Ave

rage

14.0

-16

.8-

23.1

-14

.8-

--

Not

es: R

espo

nse

rate

s va

ried

from

95.

2% to

97.

1% a

cros

s op

erat

ion

type

. N

on-r

espo

nse

to th

is q

uest

ion

was

def

ined

as

no c

heck

mar

ks to

the

entir

e qu

estio

n.1%

is t

he p

erce

ntag

e of

res

pond

ents

tha

t re

port

ed u

sing

thi

s m

arke

ting

met

hod.

N

ote

that

a p

rodu

cer

can

sell

or b

uy u

sing

mor

e th

an o

ne m

arke

ting

met

hod.

T

hepe

rcen

tage

s pr

esen

ted

for

each

ope

ratio

n ty

pe a

cros

s al

l mar

ketin

g m

etho

ds th

eref

ore

do n

ot a

dd to

100

%.

2R

ank

is a

ssig

ned

on th

e ba

sis

of th

e hi

ghes

t per

cent

age

of u

se o

f the

mar

ketin

g m

etho

d.3O

ther

incl

udes

ret

aine

d ow

ners

hip

until

sla

ught

er,

dire

ct s

ale

of p

ureb

red

cattl

e, s

ale

of r

epla

cem

ent

heife

rs v

ia p

rivat

e tr

eaty

, or

der

buye

r pu

rcha

ses

with

unk

now

nde

stin

atio

n, c

alf s

ales

to r

odeo

s an

d m

isce

llane

ous

othe

r m

arke

ting

met

hods

.

MARKETING PRACTICES OF ARKANSAS BEEF CATTLE PRODUCERS

21

The second-most-common marketing method was direct sales to stockeroperations, feedlots or other producers. As expected, a very common marketingmethod for �Feeder� operations was direct sales to feedlots.

Selling cattle together with other producers, i.e., pooling, was most com-mon among �Cow/calf� operations and was not used at all by �Feeder� opera-tions. Volume considerations that make pooling attractive are likely not a con-cern for �Feeder� operations. Video sales were used least frequently by �Cow/calf� and �Mixed� operations but were more common among �Feeder� opera-tions. Futures and options hedging and other contractual arrangements werenot very common for any operation type.

In the final row of Table 10, average use of all the different marketingmethods was the highest for �Feeder� operations and the lowest for �Cow/calf�operations. This suggests that operations that feed weaned calves may paymore attention to an array of potential marketing methods.

Volume of Trade Reported for Each Marketing MethodTable 11 summarizes statistics on the volume of cattle traded for each of

the different marketing alternatives. The second column reports the total vol-ume per category, and the third column provides the percentage breakdownamong all marketing alternatives. The fifth column indicates the number ofnon-zero responses in each category�i.e. the number of respondents that actu-ally traded cattle in each category. Columns six through nine report severalstatistics on the number of cattle traded per respondent. Unfortunately, it wasnot possible to calculate statistics on �cattle traded per transaction� due to a lowresponse rate to the relevant question (last column of Question 18 in AppendixA).

The bottom row in Table 11 shows the total volume of trade across allmarketing methods. This total was calculated as a separate statistic for eachrespondent and summarizes cattle trade for all the respondents across all cat-egories. Futures and options trade was not included in this total. In addition,adjustments noted in the footnote to the table were made to avoid doublecounting.

Cash sales were the dominant marketing category with slightly over 80% ofthe total volume of cattle traded. As a separate group, direct sales to stockers,feedlots and other producers, as well as contractual sales that may be part ofthe above direct sales, were of secondary importance. Finally, video sales andpooled sales arrangements were least common. Futures and options were notcommonly used.

A factor that may explain some of the differences in the volume of trade forthe different categories is the reported average, minimum and maximum vol-ume of trade per respondent numbers. Review of the last four columns in Table11 suggests that certain types of marketing methods were associated with highernumbers of cattle traded. The implication may be that some of these marketing

ARKANSAS EXPERIMENT STATION RESEARCH BULLETIN 957

22

Tab

le 1

1. V

olum

e of

cat

tle tr

aded

in 1

995

usin

g ei

ght a

ltern

ativ

e m

arke

ting

met

hods

.T

ype

of M

arke

ting

Tot

al N

o. o

fP

erce

ntag

e of

No.

of

Cat

tle T

rade

d pe

r R

espo

nden

tM

etho

d U

sed

Cat

tle T

rade

dT

otal

Tra

deR

ank1

resp

onde

nts2

Avg

.S

td.

Dev

.M

in.

Max

.

Cas

h69

,007

81.3

180

985

136.

51

2,50

0D

irect

--

stoc

ker

4,86

25.

73

6575

74.5

337

5D

irect

--

feed

lot

5,34

06.

32

1731

460

9.0

152,

500

Vid

eo1,

069

1.3

78

134

238.

12

700

Fut

ures

31,

636

1.9

63

545

826.

866

1,50

0C

ontr

act

4,07

54.

84

1234

069

3.9

152,

500

Poo

led

825

1.0

817

4951

.53

200

Oth

er4

3,07

13.

65

4077

99.9

150

0T

otal

584

,904

100.

0-

843

101

221.

81

5,00

01R

ank

is a

ssig

ned

on th

e ba

sis

of th

e hi

ghes

t vol

ume

of c

attle

trad

e re

port

ed.

2T

he n

umbe

r of

res

pond

ents

that

rep

orte

d gr

eate

r th

an z

ero

trad

e in

a c

ateg

ory.

3T

he n

umbe

rs o

n th

is e

ntry

sho

uld

be r

egar

ded

as c

attle

hed

ged

usin

g fu

ture

s an

d op

tions

rat

her

than

trad

ed.

In a

dditi

on th

is, c

ateg

ory

is n

ot in

clud

ed in

the

tota

l fig

ures

in th

e bo

ttom

row

.4O

f the

40

resp

onse

s in

this

cat

egor

y, 1

2 re

spon

dent

s in

dica

ted

that

they

ret

aine

d ow

ners

hip

on th

e ca

ttle

until

sla

ught

er, 1

0 so

ld p

ureb

red

cattl

e, s

even

sol

d re

plac

emen

the

ifers

via

priv

ate

trea

ty,

thre

e ha

d an

ord

er b

uyer

buy

cat

tle w

ith u

nkno

wn

dest

inat

ion,

and

one

sol

d ca

lves

for

rod

eos.

T

he r

emai

nder

did

not

indi

cate

a m

arke

ting

met

hod.

5T

he t

otal

fig

ure

does

not

incl

ude

repo

rted

num

bers

in t

he f

utur

es a

nd o

ptio

ns c

ateg

ory

as t

hese

are

hed

ging

tra

nsac

tions

tha

t do

not

invo

lve

phys

ical

del

iver

y in

mos

tca

ses.

In

addi

tion,

som

e of

the

cate

gorie

s ar

e no

t mut

ually

exc

lusi

ve.

Res

pons

es o

f res

pond

ents

that

sho

wed

the

sam

e tr

ade

volu

me

in c

ontr

actu

al s

ales

as

in e

ither

of

the

dire

ct s

ales

cat

egor

ies

or v

ideo

sal

es w

ere

trea

ted

as o

ne r

espo

nse

whe

n to

talin

g ca

ttle

trad

e pe

r re

spon

dent

. T

his

was

don

e to

avo

id d

oubl

e co

untin

g.

MARKETING PRACTICES OF ARKANSAS BEEF CATTLE PRODUCERS

23

methods are not available to smaller producers. The reported minimum num-bers suggest that some smaller producers were using some or all of the market-ing methods with the exception of futures and options trading and direct salesto feedlots. Futures and options hedging transactions, as well as direct market-ing to feedlots through contractual arrangements or otherwise, showed thelargest average trade volume figures per respondent.

Differences in the 1995 average trade volume per respondent across opera-tion types are shown in Table 12. To test whether average trade volume perrespondent was different across operation type, t-statistics were calculated1. A t-statistic (>2.0) with an associated probability less than 0.05 indicates that theaverage trade volume per respondent was different across operation type with95% confidence. Since these tests can be applied to only two operation types ata time, the table is broken into comparisons of differences between �Cow/calf�vs. �Mixed�, �Feeder� vs. �Mixed� and �Cow/calf� vs. �Feeder� operations in thebottom half of the table. Statistically significant differences are highlighted withasterisks in the table. Corresponding average trade volumes and sample sizesfor each operation are reported in the top portion of the table.

While there were a number of statistically significant results, the number ofobservations for the marketing alternatives other than �Cash� and �Other� weretoo small for testing differences. In the �Cash� marketing category, �Cow/calf�operations had the lowest number of cattle traded per respondent followed by�Mixed� operations. Finally, the �Feeder� operations reported the largest averagevolume per respondent in the �Cash� category.

Direct marketings to stockers had nearly the same volume for �Cow/calf�and �Mixed� operations and showed an average trade volume per respondentclose to that required for a semi-truck trailer load of cattle. �Feeder� operationsagain had the largest average volume per respondent in this category.

The results in the �Other� category show that �Feeder� operations tended tohave the largest average volume of trade per respondent in this category. Saleof purebred cattle and replacement heifers noted in the footnote to Table 11may explain why average trade volume for �Cow/calf� operations was higherthan that for �Mixed� operations, although the difference in average trade wasonly marginally significant. Retained ownership of cattle and purchases of orderbuyers likely explain the difference between �Feeder� vs. �Mixed� and �Feeder�vs. �Cow/calf� results.

Overall, the statistics in Table 12 support the conclusions of Tables 10 and11 in the sense that �Feeder� operations tend to be more involved in marketingalternatives to cash markets. An interesting result was the lack of pooling ar-

1These tests were performed using the UNIVARIATE procedure in SAS. Based on the results of an F-test on equal or unequal variances across the samples, differences in means across samples were testedwith the appropriate t-statistic (Huntsberger and Billingsley, 1987).

ARKANSAS EXPERIMENT STATION RESEARCH BULLETIN 957

24

Tab

le 1

2. D

iffer

ence

s in

ave

rage

trad

e vo

lum

e pe

r re

spon

dent

by

oper

atio

n ty

pe.

Dire

ct-

Dire

ct-

Des

crip

tion

Ope

ratio

n T

ype

Cas

hS

tock

erF

eedl

otV

ideo

Fut

ures

Con

trac

tP

oole

dO

ther

Ave

rage

Num

ber

of C

attle

Cow

/cal

f69

6347

11n/

a1

7736

71T

rade

d pe

r R

espo

nden

tF

eede

r32

220

059

725

9n/

a94

2n/

a26

2M

ixed

117

8225

513

0n/

a21

789

42

Num

ber

of R

espo

nden

tsC

ow/c

alf

644

485

3n/

a5

1325

that

Tra

ded

Cat

tleF

eede

r27

46

31

3n/

a3

Mix

ed13

813

62

24

412

Dire

ct-

Dire

ct-

Des

crip

tion

Ope

ratio

n T

ype

Cas

hS

tock

erF

eedl

otV

ideo

Fut

ures

Con

trac

tP

oole

dO

ther

Cow

/cal

f vs

.T

-sta

tistic

-2.7

06**

*2-1

.199

-1.3

76-1

.700

n/a

-1.4

47-1

.228

1.35

3M

ixed

Pro

babi

lity

0.00

80.

240

0.22

70.

337

n/a

0.19

10.

301

0.18

6

Fee

der

vs.

T-s

tatis

tic2.

269*

*2.

502*

0.83

20.

444

n/a

0.92

1n/

a3.

492*

Mix

edP

roba

bilit

y0.

031

0.07

80.

435

0.68

7n/

a0.

452

n/a

0.07

1

Cow

/cal

f vs

.T

-sta

tistic

-2.8

61**

*-3

.660

***

-1.4

37-1

.121

n/a

-1.1

06n/

a-3

.106

***

Fee

der

Pro

babi

lity

0.00

80.

001

0.21

00.

379

n/a

0.38

4n/

a0.

005

1T

here

wer

e no

t eno

ugh

resp

onse

s to

rep

ort a

vera

ges

or to

per

form

a t-

test

.2**

*, *

*, a

nd *

indi

cate

0.0

1, 0

.05,

and

0.1

0 si

gnifi

canc

e le

vels

, res

pect

ivel

y.

MARKETING PRACTICES OF ARKANSAS BEEF CATTLE PRODUCERS

25

rangements among stocker operations. Apparently their average trade volumeper respondent was large enough to eliminate consideration of pooling as analternative marketing method.

FREQUENCY OF CONSULTING PRICES INFORMATION

Respondents were asked to indicate whether or not they consulted priceson specified cattle characteristics to help in making marketing decisions. Thosewho consulted prices were also asked to note how frequently they did so(Appendix A, Question 19). The three specified cattle attributes�weight, type,and breed�are defined as follows:

1) Weight - comparing prices across different weight categories, such asprices for #4-500 calves, #6-700 calves, finished cattle, carcass prices,cut out prices, retail prices;

2) Type - comparing prices across different types of cattle, such as steers,heifers, bulls, replacements and cull cows;

3) Breed - Comparing prices across different cattle breeds, such Hereford,Angus, etc.

In addition, producers were also queried about what sources of informationthey used and if they used a source of information, how often they consultedeach of the following categories of information:

1) Own Sales - examining own sales records;2) Auction Sales - analyzing sales prices at different auctions and markets;3) Other - looking at information in trade magazines, other market news

reports, TV, radio and other sources.The results were differentiated by operations that fed weaned calves (�Mixed

& Feeder�) and those that did not (�Cow/calf�), i.e., responses from �Mixed� and�Feeder� operations were grouped into one category and responses of �Cow/calf� operations made up the other category. This was done on the basis of theresults obtained earlier regarding the benefits of knowing animal performanceand adjusting breeding programs on the basis of that information (Table 4).�Cow/calf� operations were more interested in the breeding information than the�Mixed� operations. A similar breakdown on information sources and cattleattributes is expected here.

The importance of different cattle attributes was ranked by assigning anumber to the frequency choices of each individual, i.e., No = 0, Yes = 1,Yearly = 2, At Saletime = 3, Monthly = 4, Weekly = 5, Daily = 6. Using thismethod, a high value implies frequent comparison of prices. Averaging re-sponses across observations can then lead to an �ordinal� measure of impor-tance for each of the cattle attributes, where a high value represents frequentuse of information and a low value represents infrequent use of information.

ARKANSAS EXPERIMENT STATION RESEARCH BULLETIN 957

26

However, the average values in themselves convey no meaning�i.e. an averageof 3.5 does not indicate a frequency between �Monthly� and �At Saletime�.

In order to test the null hypothesis that there is no difference in the distribu-tion of answers between �Cow/calf� and �Mixed & Feeder� operations, χ2-statis-tics were calculated and reported together with probabilities. High χ2-valuesand probabilities below 0.05 indicate that statistically significant differencesexist across operation type with 95% confidence.

Table 13 shows that all operations have the same ranking for the differentcattle price attributes and that �Mixed & Feeder� operations tended to examinethe price information more frequently than �Cow/calf� operations. The mostimportant attribute used for price comparison was the type of cattle. Comparingprices across weight categories was a close second. There was also a largerdifference between the �Type� and �Weight� category rankings for the �Cow/calf�operations than for the �Mixed & Feeder� operations. This supports the earliercontention that �Cow/calf� operations are less concerned with looking at pricedifferentials associated with feeding cattle to heavier weights than operationsthat feed calves.

The results concerning the frequency of price comparisons across breedswere opposite to expectations. �Cow/calf� operations paid the least attention toprice differences across breeds but had considered animal performance data toadjust breeding programs to be a more significant benefit to feeding calves than�Mixed� operations (Table 4). Either prices do not appropriately reflect thequality attributes of different breeds or �Cow/calf� operations are more inter-ested in non-price attributes in breeds. The authors hypothesize the latter to bea more accurate description of Arkansas cow/calf operators.

For the �Auction Sales� and �Other� information sources, the frequency ofuse was higher for the �Mixed & Feeder� operations than the frequency ratingsfor the �Cow/calf� operations. The opposite was true for the �Own Sales� cat-egory. One of the differences between the sources of information may be thevalidity and ease of access associated with external versus internal information.�Own Sales� records are an internal source of information that is easily accessedand known to be valid. As an alternative, external sources of information suchas prices at various auction markets, information in trade magazines and othermarket news reports may not be as easy to obtain or reliable for �Cow/calf�operators and are, therefore, consulted less often.

Finally, �Mixed & Feeder� operations used the �Other� category the mostoften with an average rating between weekly and monthly. Some producerscommented on the use of other information. Quoted most frequently as �Other�sources of information were electronic news media such as satellite uplinkservices provided by the �Date Transmission Network, DTN� and �FarmBureau�information pages on computer terminals located throughout the state.

MARKETING PRACTICES OF ARKANSAS BEEF CATTLE PRODUCERS

27

Tab

le 1

3. R

anki

ng o

f pric

e at

trib

utes

and

info

rmat

ion

sour

ces

by o

pera

tion

type

.F

requ

ency

(%

of

resp

onde

nts

in e

ach

cate

gory

)A

ttrib

ute

orO

pera

tion

No

Yes

Yea

rlyA

t S

alet

ime

Mon

thly

Wee

kly

Dai

lyN

o. o

fχ2 -

stat

istic

Sou

rce

Typ

e(

0 )

( 1

)(

2 )

( 3

)(

4 )

( 5

)(

6 )

Avg

.1R

ank2

resp

onde

nts

(Pro

babi

lity)

Typ

eC

ow/c

alf

11.6

6.4

3.6

21.3

15.5

36.1

5.7

3.5

167

332

.232

Mix

ed &

Fee

der

9.5

2.8

1.7

10.1

11.7

53.6

10.6

4.2

117

9(0

.001

)A

ll11

.25.

63.

218

.914

.739

.86.

73.

71

8523

Wei

ght

Cow

/cal

f21

.65.

02.

019

.513

.833

.25.

03.

22

662

45.0

34M

ixed

& F

eede

r11

.71.

70.

011

.110

.654

.410

.64.

12

180

(0.0

01)

All

19.5

4.3

1.5

17.7

13.1

37.8

6.2

3.4

284

23

Bre

edC

ow/c

alf

40.0

5.3

8.7

11.8

13.2

17.9

3.0

2.2

364

218

.753

Mix

ed &

Fee

der

34.8

3.1

7.3

9.2

9.8

32.9

3.1

2.7

316

4(0

.005

)A

ll39

.04.

88.

411

.312

.521

.03.

02.

33

8063

Auc

tion

Sal

esC

ow/c

alf

10.0

8.8

1.7

25.7

14.0

35.2

4.7

3.5

175

241

.713

Mix

ed &

Fee

der

6.4

3.2

0.0

14.4

11.2

56.4

8.5

4.2

218

8(0

.001

)A

ll9.

37.

71.

423

.413

.439

.55.

43.

61

9403

Oth

erC

ow/c

alf

22.4

5.7

1.8

10.1

23.0

26.2

10.9

3.3

267

355

.721

Mix

ed &

Fee

der

7.5

1.2

0.0

5.8

22.0

38.2

25.4

4.5

117

3(0

.001

)A

ll19

.44.

71.

49.

222

.828

.613

.83.

52

8463

Ow

n S

ales

Cow

/cal

f29

.23.

87.

825

.313

.615

.84.

52.

63

664

18.9

59M

ixed

& F

eede

r33

.31.

114

.118

.67.

318

.66.

82.

53

177

(0.0

04)

All

30.1

3.2

9.2

23.9

12.3

16.4

5.0

2.5

384

13

1A

vg.

is t

he w

eigh

ted

aver

age

resp

onse

of

resp

onde

nts.

It

is c

alcu

late

d as

the

sum

of

the

prod

uct

of t

he p

erce

ntag

es a

nd t

heir

wei

ghts

, i.e

. N

o =

0,

Yes

= 1

, et

c.,

for

each

cat

egor

y. A

hig

h av

erag

e re

spon

se im

plie

s fr

eque

nt c

ompa

rison

of p

rices

for

cattl

e at

trib

utes

or

freq

uent

use

of a

cer

tain

sou

rce

of in

form

atio

n, w

hile

a lo

w a

vera

gere

spon

se im

plie

s th

e op

posi

te o

r in

freq

uent

com

paris

on o

r us

e.2R

ank

is a

ssig

ned

on th

e ba

sis

of th

e hi

ghes

t ave

rage

res

pons

e fo

r th

e ca

tego

ry.

3R

espo

nse

rate

s va

ried

from

76.

3% to

88.

9%, w

hich

tran

slat

e to

251

to 1

17 m

issi

ng o

bser

vatio

ns, r

espe

ctiv

ely.

ARKANSAS EXPERIMENT STATION RESEARCH BULLETIN 957

28

OPERATOR OPINIONS ON POOLING CATTLE FOR SALE

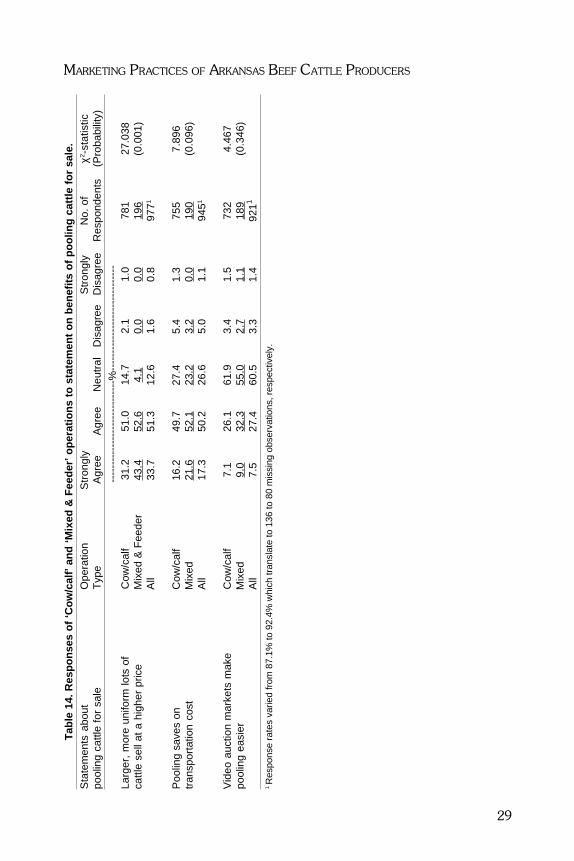

Respondents were asked to provide their opinions on pooling cattle for sale(Appendix A, Question 20). For purposes of comparison, two groups of respon-dents were defined��Cow/calf� operations and �Mixed� and �Feeder� operationsthat fed weaned calves. Pooling cattle for sale was defined as �combining yourcattle to be sold with cattle of other producers rather than just selling your cattleas an individual producer�.

Regardless of their experience with pooling cattle, respondents were askedto indicate their opinion regarding two groups of statements about poolingcattle. The first group of statements targeted the following positive aspects: 1)the availability of price premiums; 2) transportation cost savings; and 3) theease of pooling with video auctions. The second group of statements empha-sized the following potentially negative aspects: 4) average pricing; 5) lack ofknowledge of pooling as an option; and 6) the lack of flexibility in the timing ofa sale. The questions were formatted so that a respondent could either stronglyagree, agree, be neutral, disagree or strongly disagree with the statement.

For all operations, 2.6% and 1.4% of respondents had reported someexperience with pooled sales and video auctions, respectively (Table 10). For1995, the combined volume of trade for both categories was 1,894 head tradedor 2.2% of the total volume of trade (Table 11). The results to this query onpooling cattle, therefore, need to be interpreted as opinions grounded in mini-mal experience.

The responses were tested for statistically significant differences across op-eration type using a χ2-test on the distribution of answers provided. High χ2-values and probabilities below 0.05 indicate that �Cow/calf� operators havedifferent opinions on the various statements than �Mixed & Feeder� operationswith 95% confidence.

Opinions on Benefits of Pooling Cattle for SaleTable 14 summarizes the level of agreement of producers to the statements

provided in the first column of the table. Columns three through seven showthe breakdown of responses by operation type. The remaining columns list thenumber of responses for each operation type and the χ2-values and probabili-ties.

Responses to the statement, �Larger, more uniform lots of cattle sell at ahigher price� are recorded in the first row (Table 14). Both types of operationsfelt strongly that price premiums are available for larger, more uniform lots ofcattle. Over 95% of the �Mixed & Feeder� operations strongly agreed or agreedwith this statement. While answers to this statement reflect opinions, the strengthof the responses in favor of price premiums suggests that they are, in fact,available.

Responses to the statement, �Pooling saves on transportation cost� appearto indicate that both types of operations agreed that there would be transporta-

MARKETING PRACTICES OF ARKANSAS BEEF CATTLE PRODUCERS

29

Tab

le 1

4. R

espo

nses

of ‘

Cow

/cal

f’ an

d ‘M

ixed

& F

eede

r’ op

erat

ions

to s

tate

men

t on

bene

fits

of p

oolin

g ca

ttle

for

sale

.S

tate

men

ts a

bout

Ope

ratio

nS

tron

gly

Str

ongl

yN

o. o

fχ2 -

stat

istic

pool

ing

cattl

e fo

r sa

leT

ype

Agr

eeA

gree

Neu

tral

Dis

agre

eD

isag

ree

Res

pond

ents

(Pro

babi

lity)

----

----

----

----

----

----

----

-%--

----

----

----

----

----

----

----

Larg

er,

mor

e un