Embed Size (px)

Citation preview

This material is prepared on the purpose of information reference only. The information based upon our most up-to-date and reliable sources. Please note that Bangkok Bank PCL and its officers do not solicit any action based upon this information. Investors should consider this report as only a single factor in making their investment decision.

--- 1 ---

Treasury Division

TMU 01 :(66) 2021 1111 TMU 02 :(66) 2021 1222 TMU 03 :(66) 2021 1333

Market Outlook

9 - 15 November 2015

Hig

hli

gh

t

Last Week: Last week, the market is move in a narrow range while waiting for U.S. labor data

on Friday. However, the USD have a supporting from Positive Fed president’s comment, Jenet

Yellen.

This Week: The dollar move up against the basket as stronger than expected U.S. labor data

which released on Friday (6/11). This week, the main focus is on ECB chief comment about

market outlook which investor expected that ECB may use more easing to stimulate the

economic on Wednesday (11/11). Despite, the U.S. ministry of commerce will release retail

sales data on Friday (13/11).

USD

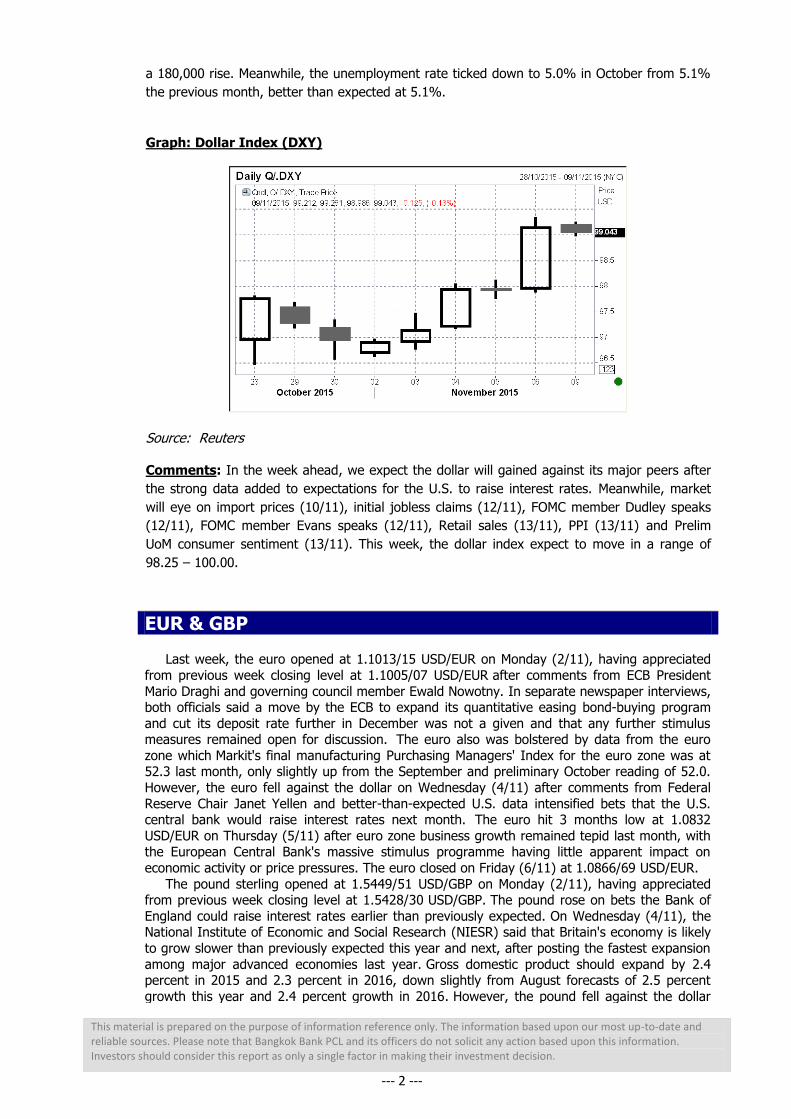

The USD opened on Monday (2/11) at 96.7, dropped from Friday (30/10) closing level at

97.00 as data showed worse-than-expected U.S. economic data. Personal spending increased

by 0.1% in October, below than expected at 0.2%. Moreover, Revised UoM consumer

sentiment fell to 90.0 in October, worse than expected at 92.6. At the beginning of the week,

the dollar moved in narrow range against its major peers as the investor awaited for any

development in news or events especially upcoming U.S. job data to indicate the market’s

movement. Meanwhile, the report showed mixed U.S. economic data. Manufacturing PMI

dropped to 50.1 in October from 50.2 in September. This is the slowest level of expansion in

more than two years. Moreover, construction spending rose 0.6% in September from 0.7% in

the previous month. However, at the end of the week, the dollar appreciated against its major

peers after Federal Reserve officials indicated that a U.S. interest rate hike next month was

possible. Fed Chair Janet Yellen said that the U.S. economy was performing well, and that

December would represent a live possibility for raising interest rates if upcoming economic data

supported it. Separately, New York Fed President William Dudley said he would completely

agree with Yellen that December was a live possibility for a rate loft-off. Moreover, the report

showed the release of strong U.S. employment and trade balance data boosted optimism over

the strength of the U.S. economy. ADP non-farm private employment rose by 182,000 last

month from 190,000 in September, above expectations for an increase of 180,000. In addition,

trade deficit declined to USD 40.8 billion in September from USD 48.0 billion in August, better

than expected at USD 42.7 billion. On Friday (6/11), the dollar index hit a six-month-high

against its major peers and closed at 99.25 after the U.S. Labor Department said the economy

added 271,000 jobs last month from 137,000 in the previous month, exceeding expectations for

This material is prepared on the purpose of information reference only. The information based upon our most up-to-date and reliable sources. Please note that Bangkok Bank PCL and its officers do not solicit any action based upon this information. Investors should consider this report as only a single factor in making their investment decision.

--- 2 ---

a 180,000 rise. Meanwhile, the unemployment rate ticked down to 5.0% in October from 5.1%

the previous month, better than expected at 5.1%.

Graph: Dollar Index (DXY)

Source: Reuters Comments: In the week ahead, we expect the dollar will gained against its major peers after

the strong data added to expectations for the U.S. to raise interest rates. Meanwhile, market

will eye on import prices (10/11), initial jobless claims (12/11), FOMC member Dudley speaks

(12/11), FOMC member Evans speaks (12/11), Retail sales (13/11), PPI (13/11) and Prelim

UoM consumer sentiment (13/11). This week, the dollar index expect to move in a range of

98.25 – 100.00.

EUR & GBP

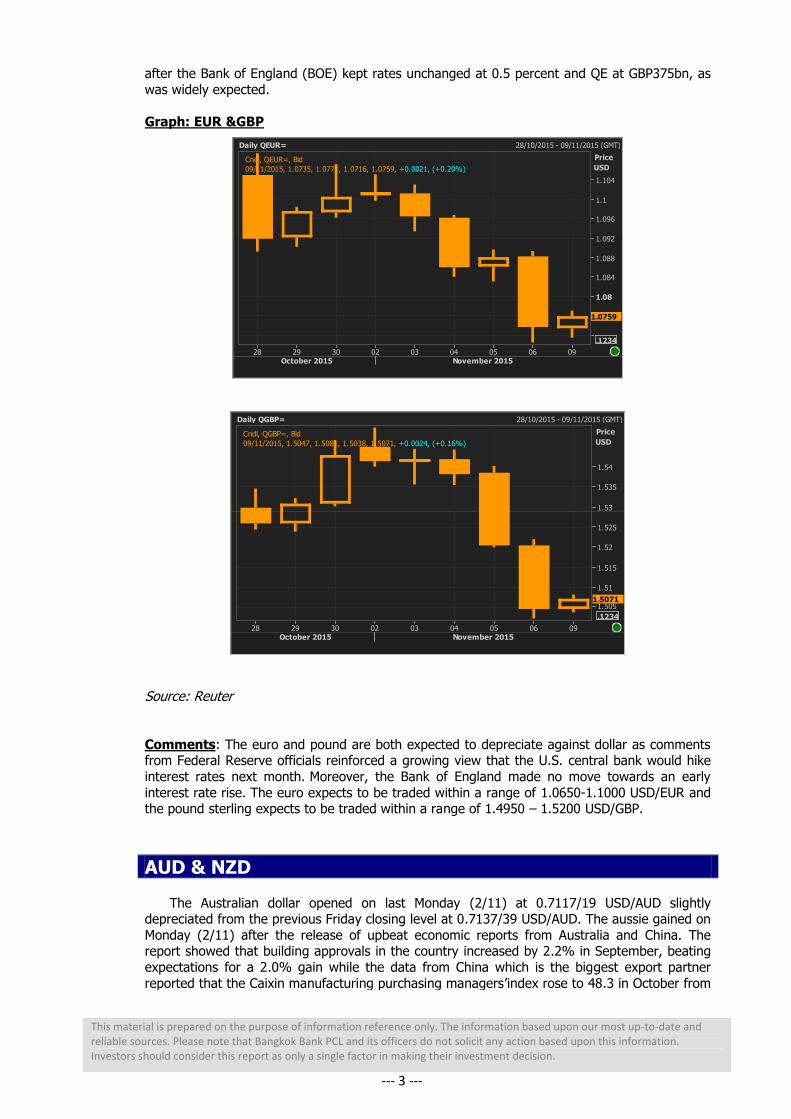

Last week, the euro opened at 1.1013/15 USD/EUR on Monday (2/11), having appreciated

from previous week closing level at 1.1005/07 USD/EUR after comments from ECB President

Mario Draghi and governing council member Ewald Nowotny. In separate newspaper interviews, both officials said a move by the ECB to expand its quantitative easing bond-buying program

and cut its deposit rate further in December was not a given and that any further stimulus measures remained open for discussion. The euro also was bolstered by data from the euro

zone which Markit's final manufacturing Purchasing Managers' Index for the euro zone was at 52.3 last month, only slightly up from the September and preliminary October reading of 52.0.

However, the euro fell against the dollar on Wednesday (4/11) after comments from Federal

Reserve Chair Janet Yellen and better-than-expected U.S. data intensified bets that the U.S. central bank would raise interest rates next month. The euro hit 3 months low at 1.0832

USD/EUR on Thursday (5/11) after euro zone business growth remained tepid last month, with the European Central Bank's massive stimulus programme having little apparent impact on

economic activity or price pressures. The euro closed on Friday (6/11) at 1.0866/69 USD/EUR.

The pound sterling opened at 1.5449/51 USD/GBP on Monday (2/11), having appreciated from previous week closing level at 1.5428/30 USD/GBP. The pound rose on bets the Bank of

England could raise interest rates earlier than previously expected. On Wednesday (4/11), the National Institute of Economic and Social Research (NIESR) said that Britain's economy is likely

to grow slower than previously expected this year and next, after posting the fastest expansion

among major advanced economies last year. Gross domestic product should expand by 2.4 percent in 2015 and 2.3 percent in 2016, down slightly from August forecasts of 2.5 percent

growth this year and 2.4 percent growth in 2016. However, the pound fell against the dollar

This material is prepared on the purpose of information reference only. The information based upon our most up-to-date and reliable sources. Please note that Bangkok Bank PCL and its officers do not solicit any action based upon this information. Investors should consider this report as only a single factor in making their investment decision.

--- 3 ---

after the Bank of England (BOE) kept rates unchanged at 0.5 percent and QE at GBP375bn, as

was widely expected.

Graph: EUR &GBP

Source: Reuter

Comments: The euro and pound are both expected to depreciate against dollar as comments from Federal Reserve officials reinforced a growing view that the U.S. central bank would hike

interest rates next month. Moreover, the Bank of England made no move towards an early

interest rate rise. The euro expects to be traded within a range of 1.0650-1.1000 USD/EUR and the pound sterling expects to be traded within a range of 1.4950 – 1.5200 USD/GBP.

AUD & NZD

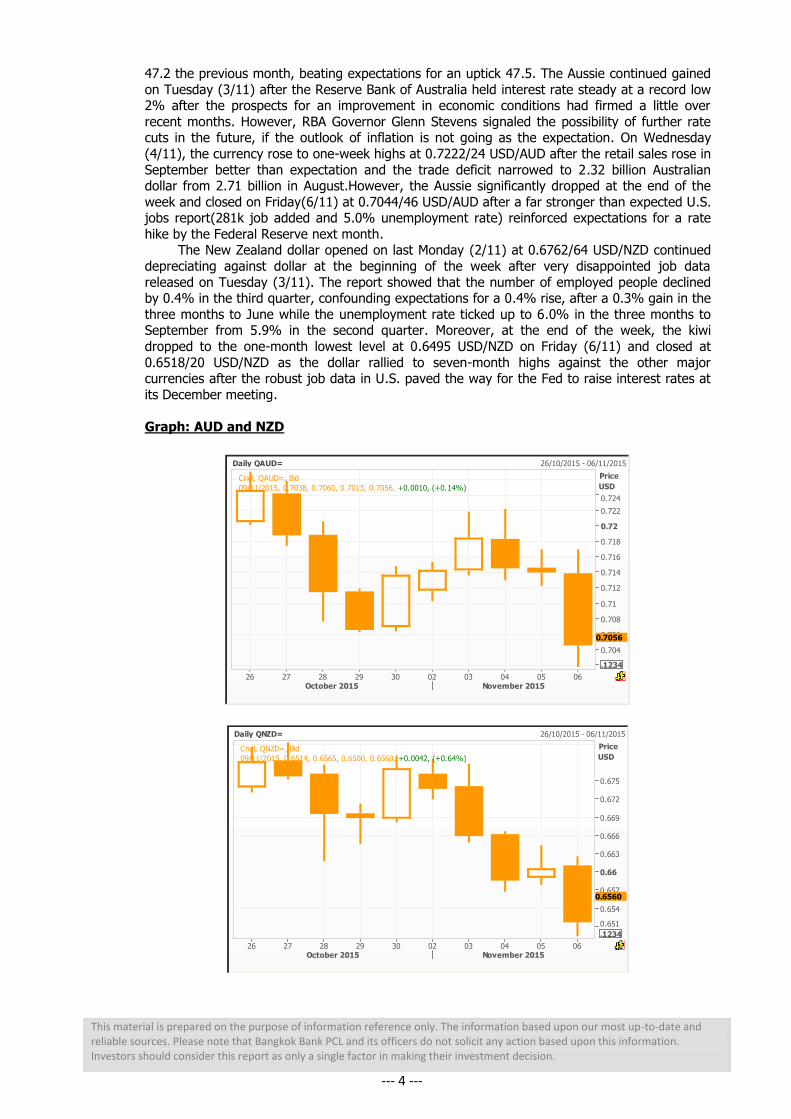

The Australian dollar opened on last Monday (2/11) at 0.7117/19 USD/AUD slightly depreciated from the previous Friday closing level at 0.7137/39 USD/AUD. The aussie gained on

Monday (2/11) after the release of upbeat economic reports from Australia and China. The report showed that building approvals in the country increased by 2.2% in September, beating

expectations for a 2.0% gain while the data from China which is the biggest export partner

reported that the Caixin manufacturing purchasing managers’index rose to 48.3 in October from

Daily QEUR= 28/10/2015 - 09/11/2015 (GMT)

Cndl, QEUR=, Bid

09/11/2015, 1.0735, 1.0771, 1.0716, 1.0759, +0.0021, (+0.20%)

Price

USD

.1234

1.076

1.08

1.084

1.088

1.092

1.096

1.1

1.104

1.0759

28 29 30 02 03 04 05 06 09October 2015 November 2015

Daily QGBP= 28/10/2015 - 09/11/2015 (GMT)

Cndl, QGBP=, Bid

09/11/2015, 1.5047, 1.5081, 1.5038, 1.5071, +0.0024, (+0.16%)

Price

USD

.1234

1.505

1.51

1.515

1.52

1.525

1.53

1.535

1.54

1.5071

28 29 30 02 03 04 05 06 09October 2015 November 2015

This material is prepared on the purpose of information reference only. The information based upon our most up-to-date and reliable sources. Please note that Bangkok Bank PCL and its officers do not solicit any action based upon this information. Investors should consider this report as only a single factor in making their investment decision.

--- 4 ---

47.2 the previous month, beating expectations for an uptick 47.5. The Aussie continued gained

on Tuesday (3/11) after the Reserve Bank of Australia held interest rate steady at a record low 2% after the prospects for an improvement in economic conditions had firmed a little over

recent months. However, RBA Governor Glenn Stevens signaled the possibility of further rate cuts in the future, if the outlook of inflation is not going as the expectation. On Wednesday

(4/11), the currency rose to one-week highs at 0.7222/24 USD/AUD after the retail sales rose in

September better than expectation and the trade deficit narrowed to 2.32 billion Australian dollar from 2.71 billion in August.However, the Aussie significantly dropped at the end of the

week and closed on Friday(6/11) at 0.7044/46 USD/AUD after a far stronger than expected U.S. jobs report(281k job added and 5.0% unemployment rate) reinforced expectations for a rate

hike by the Federal Reserve next month. The New Zealand dollar opened on last Monday (2/11) at 0.6762/64 USD/NZD continued

depreciating against dollar at the beginning of the week after very disappointed job data

released on Tuesday (3/11). The report showed that the number of employed people declined by 0.4% in the third quarter, confounding expectations for a 0.4% rise, after a 0.3% gain in the

three months to June while the unemployment rate ticked up to 6.0% in the three months to September from 5.9% in the second quarter. Moreover, at the end of the week, the kiwi

dropped to the one-month lowest level at 0.6495 USD/NZD on Friday (6/11) and closed at

0.6518/20 USD/NZD as the dollar rallied to seven-month highs against the other major currencies after the robust job data in U.S. paved the way for the Fed to raise interest rates at

its December meeting.

Graph: AUD and NZD

Daily QAUD= 26/10/2015 - 06/11/2015

Cndl, QAUD=, Bid

09/11/2015, 0.7038, 0.7060, 0.7013, 0.7056, +0.0010, (+0.14%)

Price

USD

.1234

0.704

0.706

0.708

0.71

0.712

0.714

0.716

0.718

0.72

0.722

0.724

0.7056

26 27 28 29 30 02 03 04 05 06October 2015 November 2015

Daily QNZD= 26/10/2015 - 06/11/2015

Cndl, QNZD=, Bid

09/11/2015, 0.6514, 0.6565, 0.6500, 0.6560, +0.0042, (+0.64%)

Price

USD

.1234

0.651

0.654

0.657

0.66

0.663

0.666

0.669

0.672

0.675

0.6560

26 27 28 29 30 02 03 04 05 06October 2015 November 2015

This material is prepared on the purpose of information reference only. The information based upon our most up-to-date and reliable sources. Please note that Bangkok Bank PCL and its officers do not solicit any action based upon this information. Investors should consider this report as only a single factor in making their investment decision.

--- 5 ---

Source: Reuters

Comments: This week, we expected the Aussie and the kiwi are both going to continue

depreciat ing as the market st i l l weigh on the possib i l i ty of the U.S. rate hike in December.However,the data in New Zealand such as house sales and Manufacturing PMI will be

focused.We expected the Australia dollar and the New Zealand dollar will be traded in the range

of 0.6900-0.7150 USD/AUD and 0.6400-0.6650 USD/NZD respectively.

JPY

This material is prepared on the purpose of information reference only. The information based upon our most up-to-date and reliable sources. Please note that Bangkok Bank PCL and its officers do not solicit any action based upon this information. Investors should consider this report as only a single factor in making their investment decision.

--- 6 ---

The yen opened on last Monday (2/11) at 120.47/49 JPY/USD, strengthened from previous week closing level on Friday (30/10) at 120.62/64 JPY/USD after the Bank of Japan (BoJ)

decided to leave the bank's policy target unchanged as expected on Friday (30/10). In addition, the yen gained as investors concerns over slowing growth in China, the world’s second-largest

economy, sapping risk appetite. Data on Monday (2/11) showed that China’s Caixin

manufacturing purchasing managers index edged up to 48.3 in October from 47.2 in September, but it was the eighth straight month that the index remained below 50, which is the

cut-off point between expansion and contraction. On Tuesday (3/11), the yen was little changed against the U.S. dollar as a market holiday in Japan. However, the yen weakened

against the U.S. dollar along the week after the release of strong U.S. employment and trade

balance data boosted optimism over the strength of the economy. Moreover, Fed Chair Janet Yellen said on Wednesday (4/11) that a December rate hike is a "live possibility," depending on

the data, supported the U.S. dollar gained against the major currencies. Moreover, on Friday (6/11), Bank of Japan Governor Haruhiko Kuroda warned that a deeper-than-expected

slowdown in China and other emerging economies was the biggest risk facing Japan's economic

outlook. Kuroda added that the BOJ will not hesitate to ease its monetary policy if necessary to support the economy, although he said Japan can hit the central bank's 2% inflation target

without additional stimulus for now. Also, the yen sharply depreciated against the U.S. dollar after the release of stronger than expected U.S. employment data on Friday (6/11), added to

expectations for a December rate hike by the Federal Reserve. Last week, the yen moved in a range of 120.24 – 123.26 JPY/USD before closed on Friday (6/11) at 123.13/15 JPY/USD.

Graph: JPY

Source: Reuters

Comments: This week, investors will focus on Japan’s current account and China inflation data, with reports on both the consumer and producer price index on Tuesday (10/11). Also,

Japan’s core machinery orders will be released on Thursday (12/11). We expect that this week the yen will move in a range between 122.50.-124.50 JPY/USD.

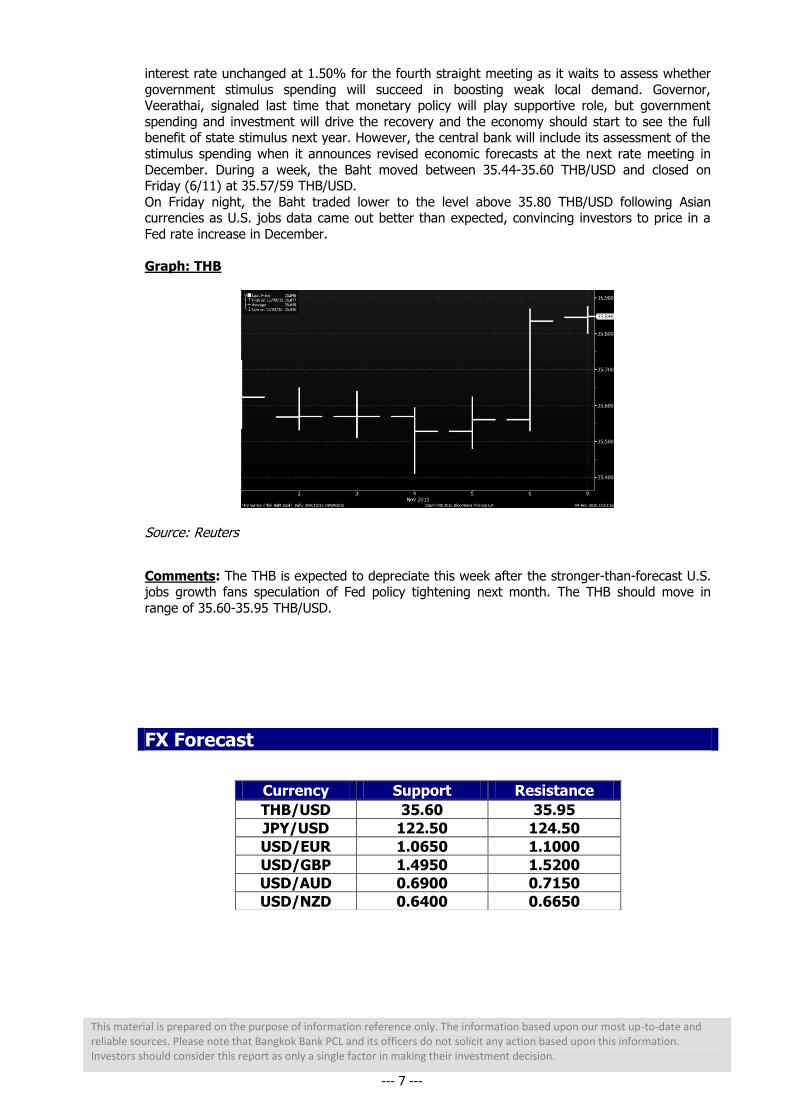

THB

The Baht opened on Monday (2/11) at 35.54/56 THB/USD, relatively the same level as

Friday’s close. The Baht traded in a narrow range during last week as investors waited for the U.S. payroll report which was due last Friday (6/11) for a sign of interest rate hike from Fed. On

Wednesday (4/11), the Baht strengthened by 0.4% to 35.47 a dollar as the equities climbed

0.8%, rising along with other Asian share markets, and after the Thailand’s central bank kept its

Daily QJPY= 29/10/2015 - 12/11/2015 (GMT)

Cndl, QJPY=, Bid

09/11/2015, 123.14, 123.36, 123.14, 123.31, +1.57, (+1.29%)

Price

/USD

Auto

120

120.4

120.8

121.2

121.6

122

122.4

122.8

123.2123.31

29 30 02 03 04 05 06 09 10 11 12October 2015 November 2015

This material is prepared on the purpose of information reference only. The information based upon our most up-to-date and reliable sources. Please note that Bangkok Bank PCL and its officers do not solicit any action based upon this information. Investors should consider this report as only a single factor in making their investment decision.

--- 7 ---

interest rate unchanged at 1.50% for the fourth straight meeting as it waits to assess whether

government stimulus spending will succeed in boosting weak local demand. Governor, Veerathai, signaled last time that monetary policy will play supportive role, but government

spending and investment will drive the recovery and the economy should start to see the full benefit of state stimulus next year. However, the central bank will include its assessment of the

stimulus spending when it announces revised economic forecasts at the next rate meeting in

December. During a week, the Baht moved between 35.44-35.60 THB/USD and closed on Friday (6/11) at 35.57/59 THB/USD.

On Friday night, the Baht traded lower to the level above 35.80 THB/USD following Asian currencies as U.S. jobs data came out better than expected, convincing investors to price in a

Fed rate increase in December.

Graph: THB

Source: Reuters

Comments: The THB is expected to depreciate this week after the stronger-than-forecast U.S. jobs growth fans speculation of Fed policy tightening next month. The THB should move in

range of 35.60-35.95 THB/USD.

FX Forecast

Currency Support Resistance

THB/USD 35.60 35.95

JPY/USD 122.50 124.50

USD/EUR 1.0650 1.1000

USD/GBP 1.4950 1.5200

USD/AUD 0.6900 0.7150

USD/NZD 0.6400 0.6650

This material is prepared on the purpose of information reference only. The information based upon our most up-to-date and reliable sources. Please note that Bangkok Bank PCL and its officers do not solicit any action based upon this information. Investors should consider this report as only a single factor in making their investment decision.

--- 8 ---

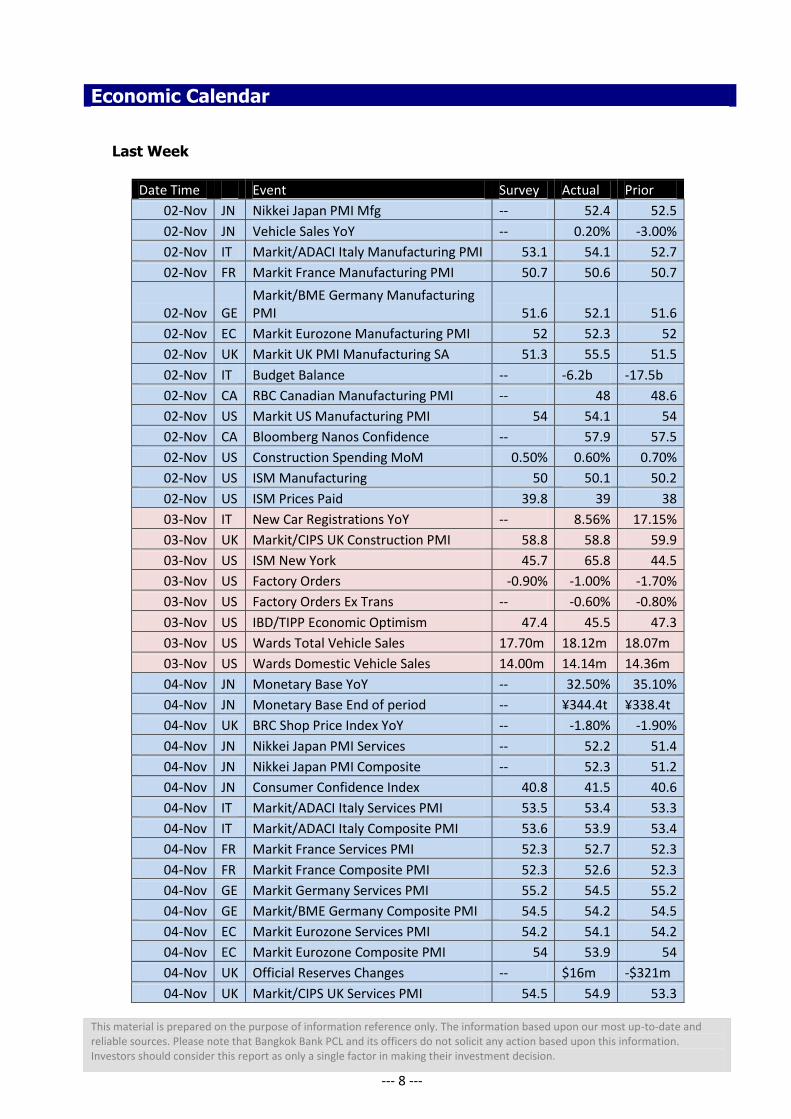

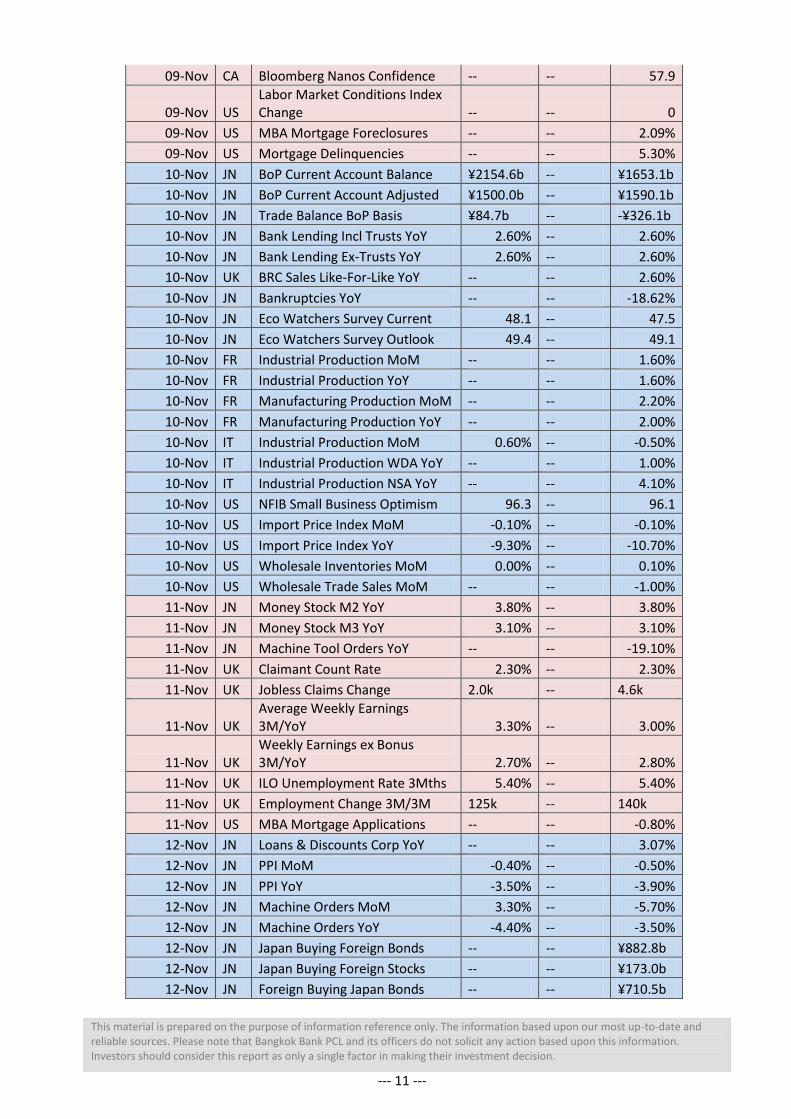

Economic Calendar

Last Week

Date Time Event Survey Actual Prior

02-Nov JN Nikkei Japan PMI Mfg -- 52.4 52.5

02-Nov JN Vehicle Sales YoY -- 0.20% -3.00%

02-Nov IT Markit/ADACI Italy Manufacturing PMI 53.1 54.1 52.7

02-Nov FR Markit France Manufacturing PMI 50.7 50.6 50.7

02-Nov GE Markit/BME Germany Manufacturing PMI 51.6 52.1 51.6

02-Nov EC Markit Eurozone Manufacturing PMI 52 52.3 52

02-Nov UK Markit UK PMI Manufacturing SA 51.3 55.5 51.5

02-Nov IT Budget Balance -- -6.2b -17.5b

02-Nov CA RBC Canadian Manufacturing PMI -- 48 48.6

02-Nov US Markit US Manufacturing PMI 54 54.1 54

02-Nov CA Bloomberg Nanos Confidence -- 57.9 57.5

02-Nov US Construction Spending MoM 0.50% 0.60% 0.70%

02-Nov US ISM Manufacturing 50 50.1 50.2

02-Nov US ISM Prices Paid 39.8 39 38

03-Nov IT New Car Registrations YoY -- 8.56% 17.15%

03-Nov UK Markit/CIPS UK Construction PMI 58.8 58.8 59.9

03-Nov US ISM New York 45.7 65.8 44.5

03-Nov US Factory Orders -0.90% -1.00% -1.70%

03-Nov US Factory Orders Ex Trans -- -0.60% -0.80%

03-Nov US IBD/TIPP Economic Optimism 47.4 45.5 47.3

03-Nov US Wards Total Vehicle Sales 17.70m 18.12m 18.07m

03-Nov US Wards Domestic Vehicle Sales 14.00m 14.14m 14.36m

04-Nov JN Monetary Base YoY -- 32.50% 35.10%

04-Nov JN Monetary Base End of period -- ¥344.4t ¥338.4t

04-Nov UK BRC Shop Price Index YoY -- -1.80% -1.90%

04-Nov JN Nikkei Japan PMI Services -- 52.2 51.4

04-Nov JN Nikkei Japan PMI Composite -- 52.3 51.2

04-Nov JN Consumer Confidence Index 40.8 41.5 40.6

04-Nov IT Markit/ADACI Italy Services PMI 53.5 53.4 53.3

04-Nov IT Markit/ADACI Italy Composite PMI 53.6 53.9 53.4

04-Nov FR Markit France Services PMI 52.3 52.7 52.3

04-Nov FR Markit France Composite PMI 52.3 52.6 52.3

04-Nov GE Markit Germany Services PMI 55.2 54.5 55.2

04-Nov GE Markit/BME Germany Composite PMI 54.5 54.2 54.5

04-Nov EC Markit Eurozone Services PMI 54.2 54.1 54.2

04-Nov EC Markit Eurozone Composite PMI 54 53.9 54

04-Nov UK Official Reserves Changes -- $16m -$321m

04-Nov UK Markit/CIPS UK Services PMI 54.5 54.9 53.3

This material is prepared on the purpose of information reference only. The information based upon our most up-to-date and reliable sources. Please note that Bangkok Bank PCL and its officers do not solicit any action based upon this information. Investors should consider this report as only a single factor in making their investment decision.

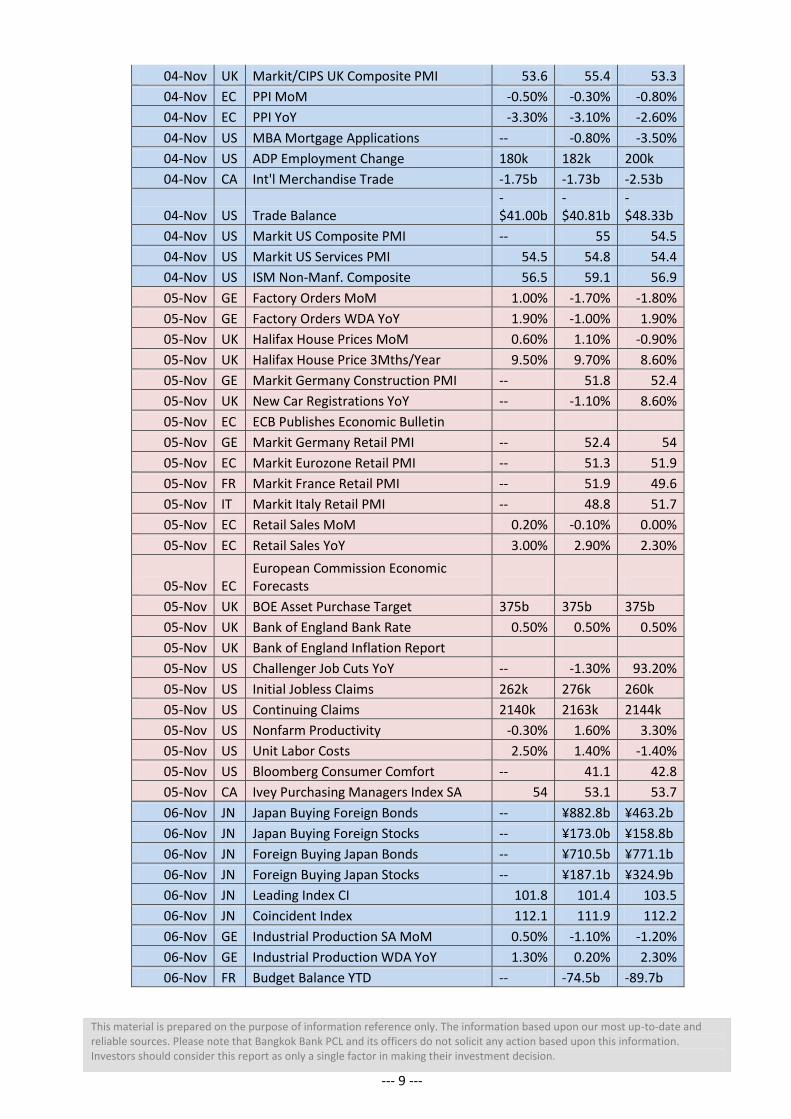

--- 9 ---

04-Nov UK Markit/CIPS UK Composite PMI 53.6 55.4 53.3

04-Nov EC PPI MoM -0.50% -0.30% -0.80%

04-Nov EC PPI YoY -3.30% -3.10% -2.60%

04-Nov US MBA Mortgage Applications -- -0.80% -3.50%

04-Nov US ADP Employment Change 180k 182k 200k

04-Nov CA Int'l Merchandise Trade -1.75b -1.73b -2.53b

04-Nov US Trade Balance -$41.00b

-$40.81b

-$48.33b

04-Nov US Markit US Composite PMI -- 55 54.5

04-Nov US Markit US Services PMI 54.5 54.8 54.4

04-Nov US ISM Non-Manf. Composite 56.5 59.1 56.9

05-Nov GE Factory Orders MoM 1.00% -1.70% -1.80%

05-Nov GE Factory Orders WDA YoY 1.90% -1.00% 1.90%

05-Nov UK Halifax House Prices MoM 0.60% 1.10% -0.90%

05-Nov UK Halifax House Price 3Mths/Year 9.50% 9.70% 8.60%

05-Nov GE Markit Germany Construction PMI -- 51.8 52.4

05-Nov UK New Car Registrations YoY -- -1.10% 8.60%

05-Nov EC ECB Publishes Economic Bulletin

05-Nov GE Markit Germany Retail PMI -- 52.4 54

05-Nov EC Markit Eurozone Retail PMI -- 51.3 51.9

05-Nov FR Markit France Retail PMI -- 51.9 49.6

05-Nov IT Markit Italy Retail PMI -- 48.8 51.7

05-Nov EC Retail Sales MoM 0.20% -0.10% 0.00%

05-Nov EC Retail Sales YoY 3.00% 2.90% 2.30%

05-Nov EC European Commission Economic Forecasts

05-Nov UK BOE Asset Purchase Target 375b 375b 375b

05-Nov UK Bank of England Bank Rate 0.50% 0.50% 0.50%

05-Nov UK Bank of England Inflation Report

05-Nov US Challenger Job Cuts YoY -- -1.30% 93.20%

05-Nov US Initial Jobless Claims 262k 276k 260k

05-Nov US Continuing Claims 2140k 2163k 2144k

05-Nov US Nonfarm Productivity -0.30% 1.60% 3.30%

05-Nov US Unit Labor Costs 2.50% 1.40% -1.40%

05-Nov US Bloomberg Consumer Comfort -- 41.1 42.8

05-Nov CA Ivey Purchasing Managers Index SA 54 53.1 53.7

06-Nov JN Japan Buying Foreign Bonds -- ¥882.8b ¥463.2b

06-Nov JN Japan Buying Foreign Stocks -- ¥173.0b ¥158.8b

06-Nov JN Foreign Buying Japan Bonds -- ¥710.5b ¥771.1b

06-Nov JN Foreign Buying Japan Stocks -- ¥187.1b ¥324.9b

06-Nov JN Leading Index CI 101.8 101.4 103.5

06-Nov JN Coincident Index 112.1 111.9 112.2

06-Nov GE Industrial Production SA MoM 0.50% -1.10% -1.20%

06-Nov GE Industrial Production WDA YoY 1.30% 0.20% 2.30%

06-Nov FR Budget Balance YTD -- -74.5b -89.7b

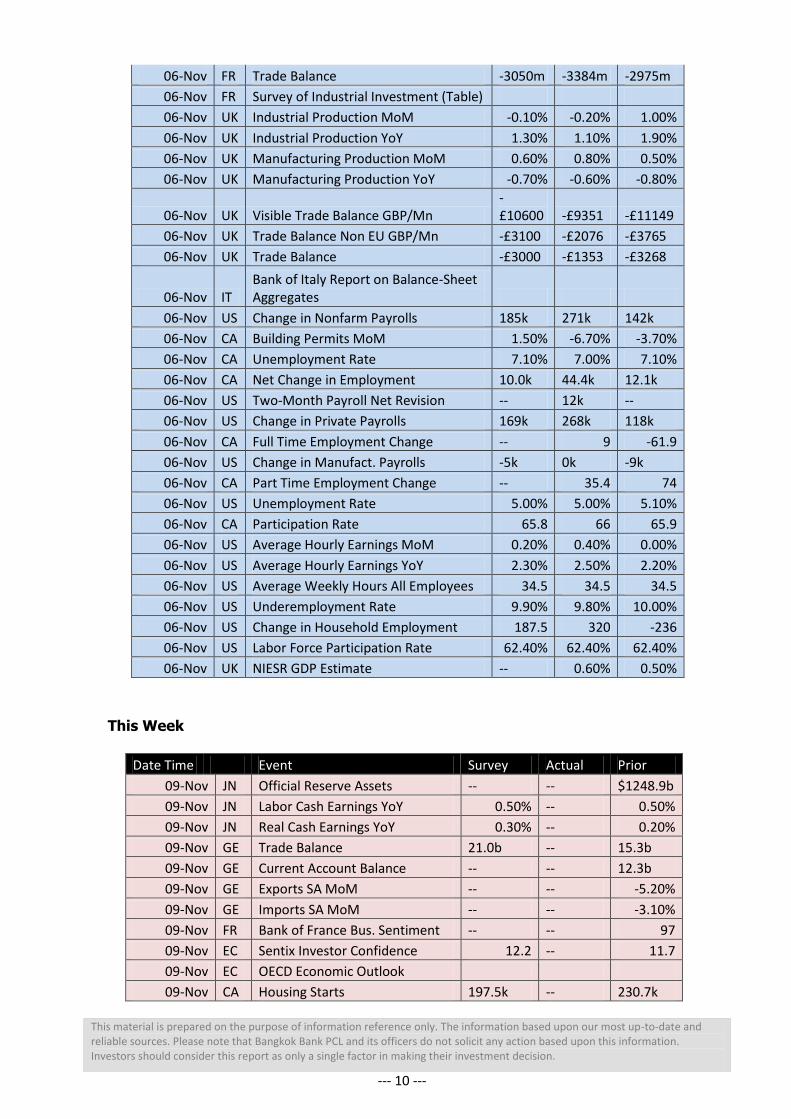

This material is prepared on the purpose of information reference only. The information based upon our most up-to-date and reliable sources. Please note that Bangkok Bank PCL and its officers do not solicit any action based upon this information. Investors should consider this report as only a single factor in making their investment decision.

--- 10 ---

06-Nov FR Trade Balance -3050m -3384m -2975m

06-Nov FR Survey of Industrial Investment (Table)

06-Nov UK Industrial Production MoM -0.10% -0.20% 1.00%

06-Nov UK Industrial Production YoY 1.30% 1.10% 1.90%

06-Nov UK Manufacturing Production MoM 0.60% 0.80% 0.50%

06-Nov UK Manufacturing Production YoY -0.70% -0.60% -0.80%

06-Nov UK Visible Trade Balance GBP/Mn -£10600 -£9351 -£11149

06-Nov UK Trade Balance Non EU GBP/Mn -£3100 -£2076 -£3765

06-Nov UK Trade Balance -£3000 -£1353 -£3268

06-Nov IT Bank of Italy Report on Balance-Sheet Aggregates

06-Nov US Change in Nonfarm Payrolls 185k 271k 142k

06-Nov CA Building Permits MoM 1.50% -6.70% -3.70%

06-Nov CA Unemployment Rate 7.10% 7.00% 7.10%

06-Nov CA Net Change in Employment 10.0k 44.4k 12.1k

06-Nov US Two-Month Payroll Net Revision -- 12k --

06-Nov US Change in Private Payrolls 169k 268k 118k

06-Nov CA Full Time Employment Change -- 9 -61.9

06-Nov US Change in Manufact. Payrolls -5k 0k -9k

06-Nov CA Part Time Employment Change -- 35.4 74

06-Nov US Unemployment Rate 5.00% 5.00% 5.10%

06-Nov CA Participation Rate 65.8 66 65.9

06-Nov US Average Hourly Earnings MoM 0.20% 0.40% 0.00%

06-Nov US Average Hourly Earnings YoY 2.30% 2.50% 2.20%

06-Nov US Average Weekly Hours All Employees 34.5 34.5 34.5

06-Nov US Underemployment Rate 9.90% 9.80% 10.00%

06-Nov US Change in Household Employment 187.5 320 -236

06-Nov US Labor Force Participation Rate 62.40% 62.40% 62.40%

06-Nov UK NIESR GDP Estimate -- 0.60% 0.50%

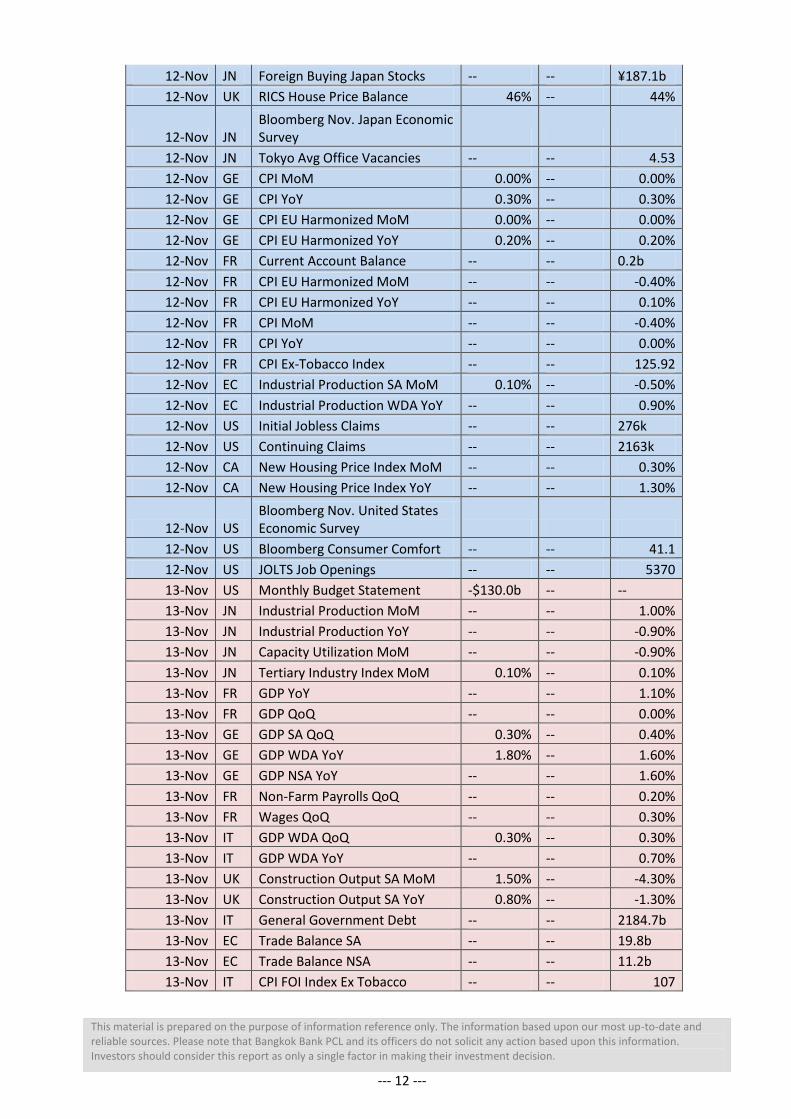

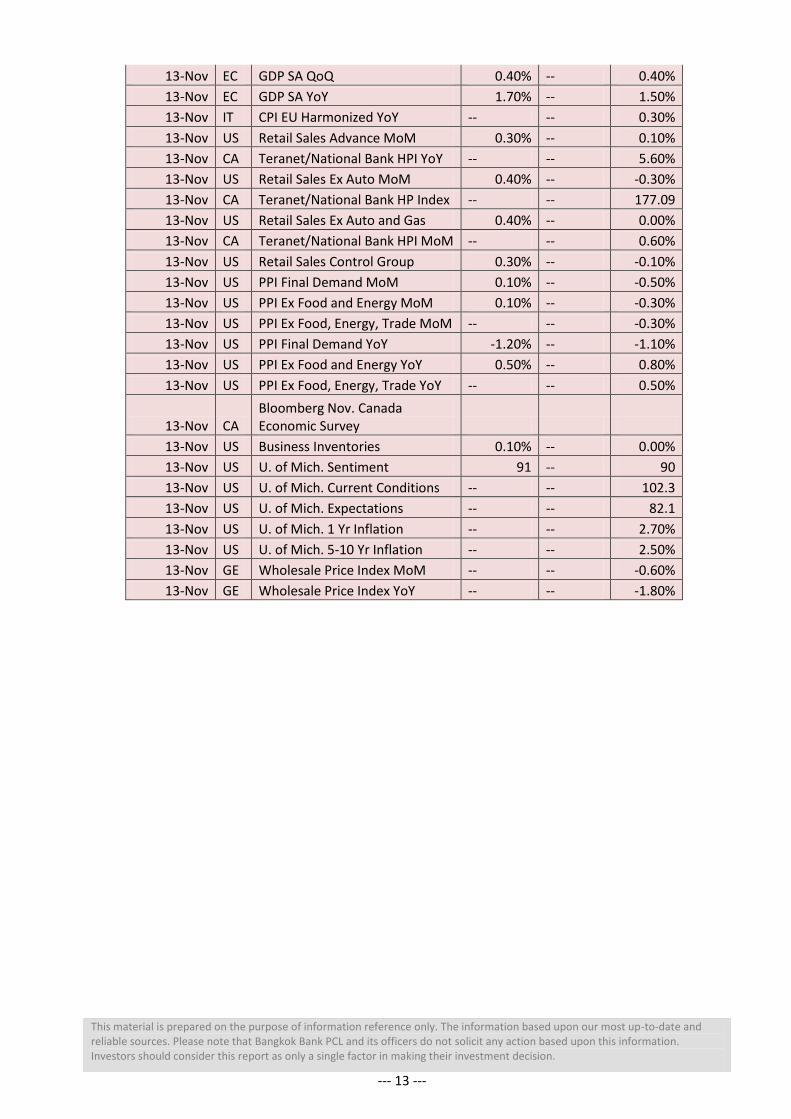

This Week

Date Time Event Survey Actual Prior

09-Nov JN Official Reserve Assets -- -- $1248.9b

09-Nov JN Labor Cash Earnings YoY 0.50% -- 0.50%

09-Nov JN Real Cash Earnings YoY 0.30% -- 0.20%

09-Nov GE Trade Balance 21.0b -- 15.3b

09-Nov GE Current Account Balance -- -- 12.3b

09-Nov GE Exports SA MoM -- -- -5.20%

09-Nov GE Imports SA MoM -- -- -3.10%

09-Nov FR Bank of France Bus. Sentiment -- -- 97

09-Nov EC Sentix Investor Confidence 12.2 -- 11.7

09-Nov EC OECD Economic Outlook

09-Nov CA Housing Starts 197.5k -- 230.7k

This material is prepared on the purpose of information reference only. The information based upon our most up-to-date and reliable sources. Please note that Bangkok Bank PCL and its officers do not solicit any action based upon this information. Investors should consider this report as only a single factor in making their investment decision.

--- 11 ---

09-Nov CA Bloomberg Nanos Confidence -- -- 57.9

09-Nov US Labor Market Conditions Index Change -- -- 0

09-Nov US MBA Mortgage Foreclosures -- -- 2.09%

09-Nov US Mortgage Delinquencies -- -- 5.30%

10-Nov JN BoP Current Account Balance ¥2154.6b -- ¥1653.1b

10-Nov JN BoP Current Account Adjusted ¥1500.0b -- ¥1590.1b

10-Nov JN Trade Balance BoP Basis ¥84.7b -- -¥326.1b

10-Nov JN Bank Lending Incl Trusts YoY 2.60% -- 2.60%

10-Nov JN Bank Lending Ex-Trusts YoY 2.60% -- 2.60%

10-Nov UK BRC Sales Like-For-Like YoY -- -- 2.60%

10-Nov JN Bankruptcies YoY -- -- -18.62%

10-Nov JN Eco Watchers Survey Current 48.1 -- 47.5

10-Nov JN Eco Watchers Survey Outlook 49.4 -- 49.1

10-Nov FR Industrial Production MoM -- -- 1.60%

10-Nov FR Industrial Production YoY -- -- 1.60%

10-Nov FR Manufacturing Production MoM -- -- 2.20%

10-Nov FR Manufacturing Production YoY -- -- 2.00%

10-Nov IT Industrial Production MoM 0.60% -- -0.50%

10-Nov IT Industrial Production WDA YoY -- -- 1.00%

10-Nov IT Industrial Production NSA YoY -- -- 4.10%

10-Nov US NFIB Small Business Optimism 96.3 -- 96.1

10-Nov US Import Price Index MoM -0.10% -- -0.10%

10-Nov US Import Price Index YoY -9.30% -- -10.70%

10-Nov US Wholesale Inventories MoM 0.00% -- 0.10%

10-Nov US Wholesale Trade Sales MoM -- -- -1.00%

11-Nov JN Money Stock M2 YoY 3.80% -- 3.80%

11-Nov JN Money Stock M3 YoY 3.10% -- 3.10%

11-Nov JN Machine Tool Orders YoY -- -- -19.10%

11-Nov UK Claimant Count Rate 2.30% -- 2.30%

11-Nov UK Jobless Claims Change 2.0k -- 4.6k

11-Nov UK Average Weekly Earnings 3M/YoY 3.30% -- 3.00%

11-Nov UK Weekly Earnings ex Bonus 3M/YoY 2.70% -- 2.80%

11-Nov UK ILO Unemployment Rate 3Mths 5.40% -- 5.40%

11-Nov UK Employment Change 3M/3M 125k -- 140k

11-Nov US MBA Mortgage Applications -- -- -0.80%

12-Nov JN Loans & Discounts Corp YoY -- -- 3.07%

12-Nov JN PPI MoM -0.40% -- -0.50%

12-Nov JN PPI YoY -3.50% -- -3.90%

12-Nov JN Machine Orders MoM 3.30% -- -5.70%

12-Nov JN Machine Orders YoY -4.40% -- -3.50%

12-Nov JN Japan Buying Foreign Bonds -- -- ¥882.8b

12-Nov JN Japan Buying Foreign Stocks -- -- ¥173.0b

12-Nov JN Foreign Buying Japan Bonds -- -- ¥710.5b

This material is prepared on the purpose of information reference only. The information based upon our most up-to-date and reliable sources. Please note that Bangkok Bank PCL and its officers do not solicit any action based upon this information. Investors should consider this report as only a single factor in making their investment decision.

--- 12 ---

12-Nov JN Foreign Buying Japan Stocks -- -- ¥187.1b

12-Nov UK RICS House Price Balance 46% -- 44%

12-Nov JN Bloomberg Nov. Japan Economic Survey

12-Nov JN Tokyo Avg Office Vacancies -- -- 4.53

12-Nov GE CPI MoM 0.00% -- 0.00%

12-Nov GE CPI YoY 0.30% -- 0.30%

12-Nov GE CPI EU Harmonized MoM 0.00% -- 0.00%

12-Nov GE CPI EU Harmonized YoY 0.20% -- 0.20%

12-Nov FR Current Account Balance -- -- 0.2b

12-Nov FR CPI EU Harmonized MoM -- -- -0.40%

12-Nov FR CPI EU Harmonized YoY -- -- 0.10%

12-Nov FR CPI MoM -- -- -0.40%

12-Nov FR CPI YoY -- -- 0.00%

12-Nov FR CPI Ex-Tobacco Index -- -- 125.92

12-Nov EC Industrial Production SA MoM 0.10% -- -0.50%

12-Nov EC Industrial Production WDA YoY -- -- 0.90%

12-Nov US Initial Jobless Claims -- -- 276k

12-Nov US Continuing Claims -- -- 2163k

12-Nov CA New Housing Price Index MoM -- -- 0.30%

12-Nov CA New Housing Price Index YoY -- -- 1.30%

12-Nov US Bloomberg Nov. United States Economic Survey

12-Nov US Bloomberg Consumer Comfort -- -- 41.1

12-Nov US JOLTS Job Openings -- -- 5370

13-Nov US Monthly Budget Statement -$130.0b -- --

13-Nov JN Industrial Production MoM -- -- 1.00%

13-Nov JN Industrial Production YoY -- -- -0.90%

13-Nov JN Capacity Utilization MoM -- -- -0.90%

13-Nov JN Tertiary Industry Index MoM 0.10% -- 0.10%

13-Nov FR GDP YoY -- -- 1.10%

13-Nov FR GDP QoQ -- -- 0.00%

13-Nov GE GDP SA QoQ 0.30% -- 0.40%

13-Nov GE GDP WDA YoY 1.80% -- 1.60%

13-Nov GE GDP NSA YoY -- -- 1.60%

13-Nov FR Non-Farm Payrolls QoQ -- -- 0.20%

13-Nov FR Wages QoQ -- -- 0.30%

13-Nov IT GDP WDA QoQ 0.30% -- 0.30%

13-Nov IT GDP WDA YoY -- -- 0.70%

13-Nov UK Construction Output SA MoM 1.50% -- -4.30%

13-Nov UK Construction Output SA YoY 0.80% -- -1.30%

13-Nov IT General Government Debt -- -- 2184.7b

13-Nov EC Trade Balance SA -- -- 19.8b

13-Nov EC Trade Balance NSA -- -- 11.2b

13-Nov IT CPI FOI Index Ex Tobacco -- -- 107

This material is prepared on the purpose of information reference only. The information based upon our most up-to-date and reliable sources. Please note that Bangkok Bank PCL and its officers do not solicit any action based upon this information. Investors should consider this report as only a single factor in making their investment decision.

--- 13 ---

13-Nov EC GDP SA QoQ 0.40% -- 0.40%

13-Nov EC GDP SA YoY 1.70% -- 1.50%

13-Nov IT CPI EU Harmonized YoY -- -- 0.30%

13-Nov US Retail Sales Advance MoM 0.30% -- 0.10%

13-Nov CA Teranet/National Bank HPI YoY -- -- 5.60%

13-Nov US Retail Sales Ex Auto MoM 0.40% -- -0.30%

13-Nov CA Teranet/National Bank HP Index -- -- 177.09

13-Nov US Retail Sales Ex Auto and Gas 0.40% -- 0.00%

13-Nov CA Teranet/National Bank HPI MoM -- -- 0.60%

13-Nov US Retail Sales Control Group 0.30% -- -0.10%

13-Nov US PPI Final Demand MoM 0.10% -- -0.50%

13-Nov US PPI Ex Food and Energy MoM 0.10% -- -0.30%

13-Nov US PPI Ex Food, Energy, Trade MoM -- -- -0.30%

13-Nov US PPI Final Demand YoY -1.20% -- -1.10%

13-Nov US PPI Ex Food and Energy YoY 0.50% -- 0.80%

13-Nov US PPI Ex Food, Energy, Trade YoY -- -- 0.50%

13-Nov CA Bloomberg Nov. Canada Economic Survey

13-Nov US Business Inventories 0.10% -- 0.00%

13-Nov US U. of Mich. Sentiment 91 -- 90

13-Nov US U. of Mich. Current Conditions -- -- 102.3

13-Nov US U. of Mich. Expectations -- -- 82.1

13-Nov US U. of Mich. 1 Yr Inflation -- -- 2.70%

13-Nov US U. of Mich. 5-10 Yr Inflation -- -- 2.50%

13-Nov GE Wholesale Price Index MoM -- -- -0.60%

13-Nov GE Wholesale Price Index YoY -- -- -1.80%