Embed Size (px)

Citation preview

Market Intelligence &

Consulting Institute http://www.marketresearch.com/Market Intelligence-

v3289/

Publisher Sample

Phone: 800.298.5699 (US) or +1.240.747.3093 or +1.240.747.3093 (Int'l)

Hours: Monday - Thursday: 5:30am - 6:30pm EST

Fridays: 5:30am - 5:30pm EST

Symposium Industry Intelligence Programs

Document Code: SVSYM14110501

Publication Date: November 2014

© Copyright 2014 Market Intelligence & Consulting Institute, a division of Institute for Information Industry. All rights reserved.

Development of Chinese and Taiwanese

Semiconductor Industry’s Major Sectors,

2014 and Beyond

Sample

Symposium

© 2014 Market Intelligence & Consulting Institute Industry Intelligence Programs Page 1

Abstract

Although Taiwan’s semiconductor industry still remains ahead of China in terms of shipment value and

technology development, China has been catching up fast, with an aim to beef up the industry with

a series of governmental preferential and incentive policies to attract foreign investors

With massive funding and aggressive talent poaching strategies, China has brought a negative

impact on Taiwan’s fabless IC design industry where IC designers are most needed

Presently, China and Taiwan have competed fiercely in the mobile communications domain and

thus Taiwanese companies have been looking for international cooperation chances while

increasing integration and R&D capabilities for high-end products to maintain edge

Other than looking into the Chinese domestic market domains with high potential (mobile

communications and telematics), Taiwan’s fabless IC design houses also have been trying to tap

the demand in emerging markets and domains (such as medicine, IoT and sensor) so as to

reduce dependence on China

As with IC manufacturing, China has been cooperating with international brands in advanced

manufacturing processes in the hope of revving up its fabless IC design industry; by streamlining its IC

manufacturing technologies and capacities, China aims to provide one-stop service solutions after

filling the back-end packaging and testing service gap

Taiwan’s IC manufacturing and packaging & testing vendors still outperform Chinese counterparts

but China is expanding fast; for this reason, Taiwanese packaging and testing vendors have been

accelerating its pace to advance into high-end packaging and testing services so as to obtain

orders from Chinese wafer foundries one step ahead of their Chinese counterparts

Available Only for Paid User

Symposium

© 2014 Market Intelligence & Consulting Institute Industry Intelligence Programs Page 2

Contents

Key Developments of the Semiconductor Industry

in China and Taiwan

Major Battlegrounds Between the Chinese and

Taiwanese Semiconductor Industries

China’s Incentive Policies for the Semiconductor

Industry and Their Consequences

Symposium

© 2014 Market Intelligence & Consulting Institute Industry Intelligence Programs Page 3

The Chinese Semiconductor Industry

Addresses More on Fabless IC Design

19% 24% 25% 27% 29% 32%

32%31% 31% 22% 23%

24%

50% 45% 44%50% 48% 44%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2008 2009 2010 2011 2012 2013

IC Packaging and Testing IC Manufacturing

IC Design

27% 31% 27% 28% 27% 26%

49%46% 51% 49% 50% 54%

24% 22% 22% 23% 23% 20%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2008 2009 2010 2011 2012 2013

IC Packaging and Testing IC Manufacturing IC Design

Chinese Semiconductor Market Share by Industry Sector, 2008-2013

Taiwanese Semiconductor Share by Industry Sector, 2008-2013

Source: CSIA (China Semiconductor Industry Association), MIC, October 2014

The differences between the Chinese and Taiwanese semiconductor industry remain significant; with its dominance in IC manufacturing, Taiwan has relied heavily on the semiconductor industry as its major source of revenue; on contrary, China relies more on the joint ventures between international brands and Chinese local brands and packaging and testing services are major source of revenues for Chinese semiconductor industry

Fuelled by the government’s preferential policy, Chinese fabless IC design houses ‘ share has been increasing and reached over 30% in 2013

Available Only for Paid User

Available Only for Paid User

Available Only for Paid User

Symposium

© 2014 Market Intelligence & Consulting Institute Industry Intelligence Programs Page 4

Chinese Fabless IC Design Industry Grows Rapidly

Chinese vs. Taiwanese IC Design House Shipment Value and Their Global Share, 2007 - 2014

Source: CSIA, compiled by MIC, September 2014

Leveraging China’s subsidization for fabless IC design, some IC design houses have been able to see a rise in market share at the cost of profits as they can use government’s subsidies to make up losses, while increasing the adoption share of China-made component at the terminal end

The new no.18 document sets up a dedicated funds for semiconductor R&D that after MIIT acknowledges that the IC development is related to emerging industries, R&D funds will be given unconditionally; companies like Rockchip, Nufront, and Allwinner have obtained funds from the government to obtain the latest IP licenses, thereby narrowing down the technology gap with international brands

2007 2008 2009 2010 2011 2012 20132014(e)

Taiwan's Fabless IC 12.2 11.3 11.6 14.0 13.5 14.1 15.7 17.5

China's Fabless IC 3.0 3.4 4.0 5.7 8.1 9.8 12.5 15.0

Taiwan's Global Share 22.7% 20.4% 21.2% 20.3% 18.2% 18.2% 18.7% 18.8%

China's Global Share 5.5% 6.1% 7.2% 8.2% 10.9% 12.6% 14.9% 16.1%

0%

5%

10%

15%

20%

25%

0

4

8

12

16

20

2013 Chinese IC Design House Ranking

Company Annual

Revenue (US$ Mln)

Major Deliverables

Hisilicon 1,355 Communications ASIC, mobile phone baseband ICs, digital video decoders

Spreadtrum 1,050 Mobile phone baseband ICs

Datang Semi. 396 Mobile phone ICs, smart cards, automotive electronic ICs

RDA Micro. 380 Communications ICs, wireless ICs

Nari Smartchip 350 Security ICs, smart meters, optical fiber network

GalaxyCore 300 CMOS image sensor

Rockchip 300 Application processor

Silan 293 Digital audio processor IC, MCU, PMU

SDIC 291 PMU, smart card

Allwinner 260 Application processor

USD (Billion)

Available Only for Paid User Available Only for

Paid User

Available only for Paid User

Symposium

© 2014 Market Intelligence & Consulting Institute Industry Intelligence Programs Page 5

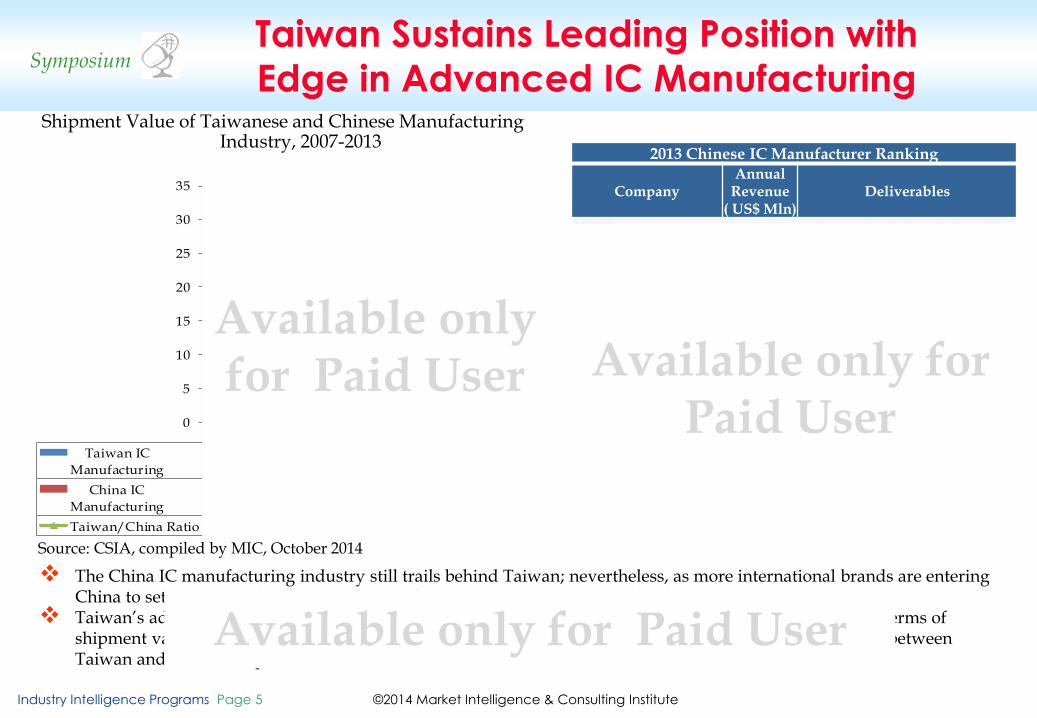

Taiwan Sustains Leading Position with

Edge in Advanced IC Manufacturing Shipment Value of Taiwanese and Chinese Manufacturing

Industry, 2007-2013

2007 2008 2009 2010 2011 2012 2013

Taiwan IC

Manufacturing22.4 20.6 17.4 25.9 24.3 26.3 32.6

China IC

Manufacturing6.6 6.5 5.6 7.4 7.1 8.3 9.9

Taiwan/China Ratio 3.4 3.2 3.1 3.5 3.4 3.2 3.3

2.8

2.9

3.0

3.1

3.2

3.3

3.4

3.5

3.6

0

5

10

15

20

25

30

35

Source: CSIA, compiled by MIC, October 2014

The China IC manufacturing industry still trails behind Taiwan; nevertheless, as more international brands are entering China to set up plants, the Chinese IC manufacturing industry is expected to keep on growing

Taiwan’s advanced manufacturing capabilities still allow the industry to advance China by three-folds in terms of shipment value; supported by the increasing scale of China’s industrial subsidies, the shipment value gap between Taiwan and China is expected to be shortened

2013 Chinese IC Manufacturer Ranking

Company Annual

Revenue ( US$ Mln)

Deliverables

SMIC 2,070 Chinese-funded wafer foundry

Hynix (China) 1,600 Foreign-funded Memory

Intel (Daliang) 690 Foreign-funded IDM

CR Microelectronics 650 Chinese-funded IDM/Wafer

foundry/separate parts

TSMC (China) 585 Taiwanese-funded wafer

foundry

Huahong NEC 580 Chinese- and Japanese-funded

IDM/wafer foundry

Xi’an XIGU Micro. 260 Chinese-funded IDM

HJTC (Suzhou) 230 Taiwanese-funded wafer

foundry

Sino-Microelectronics

210 Chinese-funded IDM

ASMC 170 Chinese-funded wafer foundry

USD (Billion) Ratio

Available only for Paid User Available only for

Paid User

Available only for Paid User

Symposium

© 2014 Market Intelligence & Consulting Institute Industry Intelligence Programs Page 6

SMIC Still Trailing Behind TSMC and UMC

40/45nm13%

55/65nm26%

90nm4%

0.13um12%

0.15/0.18um40%

0.25/0.35um5%

14Q2 SMIC Revenue Share (by process

technology)

Source: respective companies, compiled by MIC, October 2014

Process Development Roadmap of Major Chinese and Taiwanese Wafer Foundries, 2013-2015

28nm37%

40/45nm19%

65nm15%

90nm7%

0.11/0.13um3%

0.15 /0.18um

14%

0.25um and above

5%

14Q2 TSMC Revenue Share (by process technology)

40nm and

below22%

65nm

31%90nm

6%

0.11/0.13um

13%

0.15/0.18um

13%

0.25um and

above15%

14Q2 UMC Revenue Share (by process technology)

13Q1 13Q2 13Q3 13Q4 14Q1 14Q2 14Q3 14Q4 15Q1 15Q2 15Q3 15Q4 TSMC 28nm 20nm 16nm UMC 40nm 28nm 14nm SMIC 40nm 28nm

SMIC capitalizes existing process technologies for differentiation, receiving selected orders from outstanding IC design houses such as bankcard ICs, CMOS image sensors and e-Flash; fully controlling the local IC design houses’ orders while concentrating on 0.11um and below process technologies

Other than existing product lines, SMIC also steps towards high-end process technology to jointly invest into 12” fab in Beijing with Zhongguancun Development Group and Beijing Industrial Developing Investment Mgmt. Co. and a 12” wafer bumping fab with JCET

Digital Logic RF e-NVM FSI CIS PMIC Others

40nm ◎ ◎

65nm/ 55 nm ◎ ◎ ◎

90nm ◎ ◎ ◎

Less than 0.11um ◎ ◎ ◎ ◎ ◎ ◎

In the short turn, SMIC still focus on product differentiation strategy; presently, 90nm technology remains mainstream while expanding its Shenzhen and Shanghai fabs

Available Only for Paid User

Symposium

© 2014 Market Intelligence & Consulting Institute Industry Intelligence Programs Page 7

Foreign-funded IDMs Play a Key Role in Upholding the

Chinese Packaging and Testing Industry

The Chinese IC testing and packaging industry is mainly constituted by foreign-funded and Chinese-foreign joint ventures; their major businesses are to perform packaging and testing services for the mother company; international IDMs such as Intel have been helping the Chinese packaging and testing industry bolster its shipment value after the IC manufacturing and IC packaging and testing facilities that it has capitalized on since 2010 begun to operate; with the help of Intel, the Chinese IC packaging and testing industry’s had outperformed Taiwan in 2011 in terms of shipment value

Fuelled by increasing demand for packaging and testing service from foreign-funded IDMs, as well as the rapid rise of Chinese local IC design houses following the policy incentives from the Chinese government, the Chinese IC packaging and testing industry has seen growth; in 2014, Chinese packaging and testing industry’s shipment value is expected to top US$18 billion, up 13% year-on-year

USD (Billion)

Source: CSIA, compiled by MIC, October 2014

Comparison of Chinese and Taiwanese IC Packaging and Testing Industry’s Shipment Value, 2007 - 2014

2013 Chinese Packaging and Testing Vendor Ranking

Company Annual Revenue

(US$ Mln) Major Players

JCET(Xinchao Group) 1,246 China investment and contract services

Micron (Xi’an) 1,182 Foreign IDM

Freescale (China) 1,078 Foreign-funded IDM

RFMD (Beijing) 904 Foreign-funded IDM

Intel Semiconductor (Chengdu)

830 Foreign-funded IDM

Nantong Huada Microelectronics

733 Chinese-foreign JV

Tian Shui Hua Tian 571 China-funded & contract making services

Hitech (Wuxi) 526 Chinese-foreign JV

Panasonic (Shanghai) 447 Foreign-funded IDM

Infineon (Wuxi) 436 Foreign-funded IDM

2007 2008 2009 2010 2011 2012 2013 2014

Taiwan IC Manufacturing 10.1 9.8 8.2 11.1 11.5 11.7 12.4 13.4

China IC Manufacturing 8.3 8.9 7.3 9.3 12.7 13.8 16.0 18

Taiwan's Global Share 48.8% 48.9% 48.1% 47.1% 47.8% 47.9% 49.1% 49.3%

China' Global Share 40.1% 44.3% 42.5% 39.6% 52.9% 56.3% 63.6% 66.3%

0%

10%

20%

30%

40%

50%

60%

70%

0

2

4

6

8

10

12

14

16

18

20

Available only for Paid

User

Available only for Paid User

Available only for Paid User

Symposium

© 2014 Market Intelligence & Consulting Institute Industry Intelligence Programs Page 8

Contents

Key Developments of the Semiconductor Industry

in China and Taiwan

Major Battlegrounds Between the Chinese and

Taiwanese Semiconductor Industries

China’s Incentive Policies for the Semiconductor

Industry and Their Consequences

Symposium

© 2014 Market Intelligence & Consulting Institute Industry Intelligence Programs Page 9

Chinese and Taiwanese IC Design Houses

Compete Fiercely in Mobile Phone Domain

Source: MIC, October 2014

Observing China’s top 10 IC design houses in 2013, Hisilicon and Spreadtrum continued to dominate the Chinese market; fuelled by the increasing shipments for Huawei, Hisilicon’s revenue already exceeded Taiwan’s 3rd largest IC design house as Hisilicon’s revenue in 2010 topped around US$650 million, which was equivalent to the revenue of Taiwan’s sixth largest IC design house in 2010 and Taiwan’s fourth largest design house in 2012

Taiwanese and Chinese IC design houses compete bitterly in mobile phone baseband ICs; have low degree of overlap in other domains

Taiwan/China Top 10 Fabless IC Design Houses

Rank

Taiwan China

Company Revenue

(US$ Mln) Main Deliverables Company

Revenue (US$ Mln)

Main Deliverables

1 MediaTek 4,568 Mobile Phone Baseband IC Hisilicon 1,355 Communications ASIC, mobile phone baseband IC, digital video decoder

2 Novatek 1,392 LCD Driver Spreadtrum 1,050 Mobile Phone Baseband IC

3 Morningstar 1,130 LCD TV SoC Datang Semi 396 Mobile Phone IC, Smart card, Auto electric IC

4 Phison 1,080 NAND Flash Controller IC RDA 380 Communications IC, wireless IC

5 Realtek 947 Data Communications IC Beijing KT

Micro 350 Safety IC, smart meter, optical networks

6 Himax 767 LCD Driver GalaxyCore 300 CMOS image sensor

7 Raydium 366 LCD Driver Rockchip 300 Application processor

8 Richtek 360 PMU Silan 293 Digital audio processor, MCU, PMU

9 ILItek 323 LCD Driver SDIC 291 PMU, Smart Card

10 Orise 314 LCD Driver Allwinner 260 Application processor

Available Only for Paid User

Available Only for Paid User

Symposium

© 2014 Market Intelligence & Consulting Institute Industry Intelligence Programs Page 10

Qualcomm and MediaTek Still Dominate in Chinese

Smartphone Application Processor Market

Chinese Smartphone Application Processor Market Share by Chip Supplier, 1H 2014

Qualcomm42%

MediaTek36%

Apple8%

Spreadtrum5%

Marvell3%

Hisilicon3%

Chinese Application Processor Shipment Share by Number of Cores per CPU, 1H 201

Chinese smartphone market volume reached 193 million in the first half of 2014, nearly 80% of which were provided by Qualcomm and MediaTek

Chinese application processor suppliers Spreadtrum and Hisilicon only accounted for 8%

Based on number of cores per CPU shipped, five major AP suppliers for Chinese smartphones are mainly quod-core ones; only Spreadtrum still provides dual-core processors because of lowing speed of product development in 2013

Hisilicon only provides 4-and higher-cores CPU for Huawei, while other Chinese brands embrace IC solutions from Qualcomm and MediaTek

33.3%

31.7%

12.7%

40.7%

63.5%

61.6%

26.0%

72.1%

97.4%

25.2%

0% 20% 40% 60% 80% 100%

Qualcomm

MediaTek

Spreadtrum

Marvell

Hisilicon

Single Dual Quad Octa

Available Only for Paid User

Available Only for Paid User

Available Only for Paid User

Symposium

© 2014 Market Intelligence & Consulting Institute Industry Intelligence Programs Page 11

Low-cost Quad-core CPU to Hit 4G Battlefield

0%

50%

100%

Qualcomm

17.9%

11.6%8.6%7.3%

54.6%

Others MSM 8225(Q)MSM 8674(Q) MSM 8974(Q)MSM 8926(Q)

0%

20%

40%

60%

80%

100%

MTK

32.5%

28.1%

24.5%

14.9%

MT6582(Q) MT 6589(Q)

MT6592(O) Others

0%

20%

40%

60%

80%

100%

Spreadtrum

40.7%

25.2%

15.5%

18.6%

SC 8825(D) SC 8810(S)

SC 8830(Q) Others

0%

20%

40%

60%

80%

100%

Marvell

32.4%

26.8%

25.4%

15.4%

Others

PXA1920(Q)

PXA986(D)

PXA1088(Q)

0%

20%

40%

60%

80%

100%

Hisilicon

76.0%

20.7%3.3%

Others

K3V2(Q)

Kirin910(Q)

Source: MIC, October 2014

Available Only for Paid User

Available Only for Paid User

Symposium

© 2014 Market Intelligence & Consulting Institute Industry Intelligence Programs Page 12

Qualcomm Spots Opportunities from the

Rising Local Brands

Chinese Smartphone Market Share by Branded Vendor, 1H 2014

Vendor, 1H 2014 SAMSUNG, 13.3%

XIAOMI, 13.2%

LENOVO, 12.2%

COOLPAD, 10.8%

HUAWEI, 10.4%

APPLE, 7.7%

ZTE, 5.3%

OPPO, 2.6%

GIONEE, 2.5%

BBK, 2.2%

Others, 19.8%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Qualcomm MediaTek Spreadtrum

Marvell Hisilicon

Chinese Branded Smartphones’ AP adoption, 1H 2014

Source: MIC, September 2014

The Chinese smartphone market is no longer dominated by international brands as Chinese brands Xiaomi, Lenovo, and Coolpad have fetched the places into top-five brands

Aside from Samsung, ZTE and OPPO, other top-10 branded vendors use MediaTek’s IC solutions; MediaTek had absolute edge in the first quarter of 2014; Qualcomm’s market share is rising following Xiaomi’s switchover to Qualcomm’s solutions and Chinese operators’ growing ambition in 4G

Available Only for Paid User

Available Only for Paid User

Symposium

© 2014 Market Intelligence & Consulting Institute Industry Intelligence Programs Page 13

Reference Design is Where IC Competition Lies

Key component suppliers in QRD

Snapdragon S200 S400 S600 S800

Driver IC: Novatek, Orise, Himax, ILItek, Renesas

Display

LCD Module: Truly, Tianma, BOE, TCL, BYD

Main Board

Touch IC: Synaptics, FocalTech, Goodix Cypress, Atmel

Touch Module: O-Film, Truly, Toptouch, Goword

CMOS Image Sensor: OmniVision, Sony, Samsung, GalaxyCore, SuperPix, Aptina

CCM: Sony, O-Film, Truly, Qtech

Sensor:Bosch, Freescale, ST, Avago, Invense, AKM, Intersil, LiteOn, Sitronix

International and Chinese suppliers

Key component suppliers in Intel Tablet Reference Design

Source: MIC, October 2014

Intel Atom

Driver IC: Novatek, Himax, ILItek

Display

LCD Module: BOE, Infovision, AUO, CPT, Innolux

Main Board

Touch IC: Goodix, Silead, FocalTech

CMOS Image Sensor: OmniVision, GalaxyCore, Superpix

Sensor:Bosch, InvenSense

International and Chinese suppliers

Aside from panel driver ICs, key component suppliers in international vendors’ reference design are comprised of international and Chinese local IC design houses and Taiwanese IC design houses’ share is relatively small except in Touch IC and sensor areas

Available Only for Paid User

Available only for Paid User

Symposium

© 2014 Market Intelligence & Consulting Institute Industry Intelligence Programs Page 14

Contents

Key Developments of the Semiconductor Industry

in China and Taiwan

Major Battlegrounds Between the Chinese and

Taiwanese Semiconductor Industries

China’s Incentive Policies for the Semiconductor

Industry and Their Consequences

Symposium

© 2014 Market Intelligence & Consulting Institute Industry Intelligence Programs Page 15

China Semiconductor Policy Now Centers on

Integrated Planning

Incentives in taxation, financial investment, R&D, talent poaching, intelligence property rights

New No. 18 Document

Core electronic devices, high-end general

ICs, basic software product items (approx.

60 billion RMB budget in total)

Manufacturing Equipment and Assembly

Techniques for Ultra Large Scale

Integrated Circuit(approx. 1,20 billion

RMB budget in total)

National Science & Technology Major Project (2006-2020)

Energy-saving environmental protection industry

Next ICT Industry Promote mobile communications,

IoT devices, smart devices Tri-network convergence, IoT,

cloud computing Semiconductor

Biology Industry High-end equipment manufacturing

industry New energy industry New material industry New energy automotive industry

7 Strategic Emerging Industries of 12th Five-year Plan

Source: State Council, October 2014

In the past years, China’s MIIT, Ministry of Science and Technology and Ministry of Finance have been in charge of fostering the semiconductor industry with different subsidy plans under national science & technology major projects and 12th Five-year Plan; however, target completion rate is low due to subsidy inconsistency across departments

Available Only for Paid User

Available Only for Paid User

Available Only for Paid User

Available Only for Paid User

Symposium

© 2014 Market Intelligence & Consulting Institute Industry Intelligence Programs Page 16

Strong Market Demand in China Allures Taiwanese IC

Packaging and Testing Service Providers to Deploy

IC design houses have different deployment plans due to different attributes

Major IC Packaging and Testing Vendors

Using X86 as core processor, VIA has been expanding its product lines to cover ARM and communications domain and yield prominent results in communications

MediaTek (Hefei)

MediaTek Core Software Design (Chengdu)

MediaTek Shanghai

MediaTek Software (Wuhan)

MediaTek Software(Shenzhen)

Goodix (Shenzhen)

MediaTek’s China deployment focuses mainly on areas involving communications with subsequent investments focusing mainly on Reference Design integration

Vendor Plants in Taiwan Plants in China

ASE

Kaohsiung (K5/K7/K11), Zhongli, Taichung (including 8”-12” Bumping and high-end packaging service)

Weihai(Shandong)-packaging and testing services for separate parts Kunshan (Shanghai)-Analog IC packaging & testing components (Suzhou)

SPIL Changhua, Zhongshan, Hsinchu (inlcuding 8” and 12” Bumping and high-end packaging service)

Suzhou(3rd fab)-mainly provides traditional wire-based packaging service

PowerTech Hsinchu Suzhou

Source: respective companies, compiled by MIC, October 2014

Market demand and industrial clusters are main reasons why they set up plants in Suzhou

Available Only for Paid User

Symposium

© 2014 Market Intelligence & Consulting Institute Industry Intelligence Programs Page 17

China Takes Aim at Global Share with Dedicated Policy

Notice of the State Council on Issuing Several Policies on Further Encouraging the development of Software and Integrated Circuit Industries (no. 4 document)

State Council Issues National Outline of Integrated Circuit Industry in June 2014 – 120 Billion RMB

State Council sets up an industry working group to integrate MIIT, Ministry of Science and Technology, Ministry of Finance

Focal Areas How It Operates

Establishing National IC Working Group

Preparing National Development Fund

Effects on the Industry • It is anticipated that Kai Ma will act as the group leader

while minister of MIIT, Miao Wei, will act as vice group leader

• Kai Ma is the 4th-ranked VP takes over duties of the Premier, in charge of industry pipe industry, transportation, finance, human resources and social security work

• Group members are to include MIIT, National Development and Reform Commission, Ministry of Science and Technology and Ministry of Finance

• MIIT is in preparation to the group-in-charge; the national development funds are to be jointly funded by Ministry of Finance, state-run banks, private-controlled companies and Chinese-funded enterprises and has been approved by State Council

• National funds will be released by investing into dedicated companies with growth potential

• Aside from the central government, local governments will set up their own development funds (Beijing has set up 30 billion RMB development fund for the semiconductor industry)

• The completion of policy integration will facilitate the implementation of no. 18 and no. 4 documents

• National development funds will benefit more on IC design than on manufacturing and packaging & testing

• Chinese semiconductor and packaging and testing industries will expand faster

Source: CSIA, compiled by MIC, October 2014

Available Only for Paid User

Symposium

© 2014 Market Intelligence & Consulting Institute Industry Intelligence Programs Page 18

Vimicro

Superpix

China’s Deployment for IC Design and Manufacturing

Through National Development Fund, the central government attempts to control the IC industry by

becoming shareholders

Encouraging and forcing foreign semiconductors to cooperate with Chinese counterparts

UNIS China Electronics Co

Datang Telecom

RDA LeadCore Datang Microelectronics

Datang Semi.

NXP

SMIC

16%

19%

Datang NXP Semi.

Developing mix-mode automotive ICs (Datang 51% /NXP 49%)

Qualcomm

Shareholding

Co-develop 28 nm

Under China’s anti-trust investigation, Qualcomm may face a huge fine and may have to change

its royalty-charging method

Local gov’ts also set up own funds to support hidden champions

Intel

Solomon

SDIC

Hua Hong

Great Wall

Panda

TPV

Beijing Shanghai Shenzhen

Wuhan

Chengdu

Xi’an

Hefei

GalaxyCore SDIC

Source: respective companies, compiled by MIC, October 2014

Diga Device

VeriSilicon Fudan Montage

Tongfang

HuaHong On-Bright Country Mate Technology

Capital/ Technology Investment

Spreadtrum

Available Only for Paid User

Symposium

© 2014 Market Intelligence & Consulting Institute Industry Intelligence Programs Page 19

China is Building One-stop Service Model with

Help from International Brands

Tablet Smartphone NB

Rockchip 9.3%

Intel 6.4% 0.1% 88%

Spreadtrum 5%

RDA

Chinese mobile comm. IC market share and partnerships

UNIS (state-run enterprise) bought Spreadtrum for US$1.7 billion and RDA for US$900 million

Strategic agreement allows Intel to obtain tablet channels from Rockchip and Rockchip can access Intel’s Atom 3G&4G SoC production lines covering smartphone, tablet, notebook PC

It is reported that Intel will purchase 20% stake in Spreadtrum for US$1.5 billion; through the acquisition, Spreadtrum is able to strengthen chip integration and enhance chip efficiency

China determines to build up a comprehensive mobile IC supply chain (GalaxyCore, Goodix, Silead, etc) by cooperating with major chipmakers

Economies of Scale, High-end Packaging and Testing

28nm

OmniVision

Hua Capital +PuDong

SMIC

UNIS

US$1.67 billion

WLCSP Co.

13.4% shareholding

JECT STATS Qualcomm 12” bumping

Available Only for Paid User

Symposium

© 2014 Market Intelligence & Consulting Institute Industry Intelligence Programs Page 20

Taiwan’s IC Design Houses Cooperating with

Chinese Local Governments

Beginning in 2013, Taiwanese IC design houses have begun to strengthen cooperation with Chinese local governments, while seeking cooperation with Chinese companies in mobile phone, automotive, smart wearables and smart cards which have economies of scale but are lack of related ICs

To reduce the impact from the rise of Chinese semiconductor industry, Taiwanese IC design houses have taken aggressive stance towards high-end product development, stepping into emerging domains while diversifying products, technologies, and customers in order to widen the technological gap with Chinese counterparts

Strategy for selling mature products in China

Strategy for emerging domains in China

Recent collaboration with Chinese local

governments

MediaTek MediaTek continues to cooperate with Chinese white-box, branded and operators in smartphone sector

Automotive IC, e-wallet Hefei (500 RMB)

Realtek Realtek strives to cut into Chinese white-box tablet and TV brands with Wi-Fi, TV and audio offerings

Smart home appliances, smart meter, automotive IC

VIA

VIA continues to develop its Chinese brand; VIA Telecom enters into CDMA technology license with MediaTek to jointly develop Chinese smartphone market

Smart grid, OTT BOX Semiconductor Mfg. International (Shanghai) to form JV with state-run firms in Shanghai

Comparison of Development Strategies of Major Fabless IC Design Houses

64bit, Octa Core, LTE multi-mode adopted by LG and Sony

Set up R&D center in Singapore, to focus on smart city, smart medicine, and IoT

Ethernet and communications-related technology are its cores and most of international brands are already its clients

Set up a subsidiary in Singapore, focusing on IoT apps

Cooperation with European brands with automotive ICs to obtain leading position

Source: respective companies, compiled by MIC, October 2014 Available Only for Paid User

Symposium

© 2014 Market Intelligence & Consulting Institute Industry Intelligence Programs Page 21

5j03rup

TSMC (16nm) focuses on communications ICs while joint developing 3D ICs with DRAM brand Micron

SMIC(28nm) Mainly consumption ICs Looking for Korean brands to jointly develop NAND Flash

Taiwanese Firms Seeks Frontrunner Advantage in the

Chinese Packaging and Testing Industry

Xi’an plant: US$7 billion for 3D NAND flash manufacturing (10nm); completes packaging and testing facility before 2014 ends

Logic IC DRAM

Projects to invest US$30 billion into Xi’an plant and whether to add logistic manufacturing for 3D IC remains to be seen

ASE Kaohsiung Expanding high-end and bumping packaging services in Taiwan

SPIL Expanding and high-end and wafer packaging services in Taiwan

PTL Increasing logic ICs and NAND Flash

ASE Kaohsiung Through Universal Scientific Industrial (Shanghai) to increase SiP packaging lines at its Shanghai plant

SPIL Expanding FC CSP capacity at Suzhou plant

PTL Increasing investment to NT$70 million

Eon Silicon (NOR Flash) is seeking to enter China with NAND Flash

JCET Developing high-end packaging and joining hands with SMIC for 12” wafer bumping

Source: respective companies, compiled by MIC, October 2014

Leading wafer foundries in China and Taiwan have their own deployment for 3D ICs; China has succeeded in attracting Samsung to set up plant for 3D Memory and also has teamed up with Taiwanese companies in NAND Flash

Available Only for Paid User

Symposium

© 2014 Market Intelligence & Consulting Institute Industry Intelligence Programs Page 22

Copyright and Intellectual Property Policy

Any use or reproduction for commercial purposes without

prior written permission is forbidden

All trademarks, product names, and company names and

logos appearing herein are the property of their respective

owners

The content herein represents our analysis of information

generally available to the public or communicated to us by

knowledgeable individuals or companies, but is not

guaranteed as to its accuracy or completeness

Symposium

© 2014 Market Intelligence & Consulting Institute Industry Intelligence Programs Page 23

© Copyright 2014 Market Intelligence & Consulting Institute, a division of Institute for Information Industry. All rights reserved. Reproduction of this publication without prior written permission is forbidden. The content herein represents our analysis of information generally available to the public or communicated to us by knowledgeable individuals or companies, but is not guaranteed as to its accuracy or completeness.

Subscription Hotline +886.2.27356070 Fax +886.2.27321351 E-mail Address [email protected] Web Address http://mic.iii.org.tw